Embed Size (px)

Citation preview

PRESENTED BYSAMIR SHEKHAR

SUBPRIME CRISIS 2008Housing Bubble: USA

MEANING OF SUBPRIME :

• The word means subordinate to primary• It is the loan given to people with a bad credit rating

who are not eligible for Prime loan ( normal loans )• Characterized by higher interest rates, poor quality

collateral, and less favorable terms in order to compensate for higher credit risk

• Sub-prime lending may be utilized for sub-prime mortgages, sub-prime car loans, sub-prime credit cards etc.

MEANING-

Why are Subprime loans issued ?

• For banks to earn more money by tapping the defaulting customers

• For young people who do not have enough money for down payment

• For people having financial problems

• For people who are discriminated

REASONS -

• The US subprime mortgage crisis was a set of events and conditions that led to a financial crisis and subsequent recession that began in 2008

• Characterized by a rise in the inability to pay housing mortgages resulting in the decline of securities backed by mortgages

• These mortgage-backed securities (MBS) initially offered attractive rates of return

• However, the lower credit quality ultimately caused massive defaults

• The money was sucked out of several banks, financial institutions and the economy as a whole in September 2008

• Several European and developing countries had invested heavily in American banks

• The subsequent loss of funds resulted in the Global Recession of 2008

Subprime Crisis in Brief

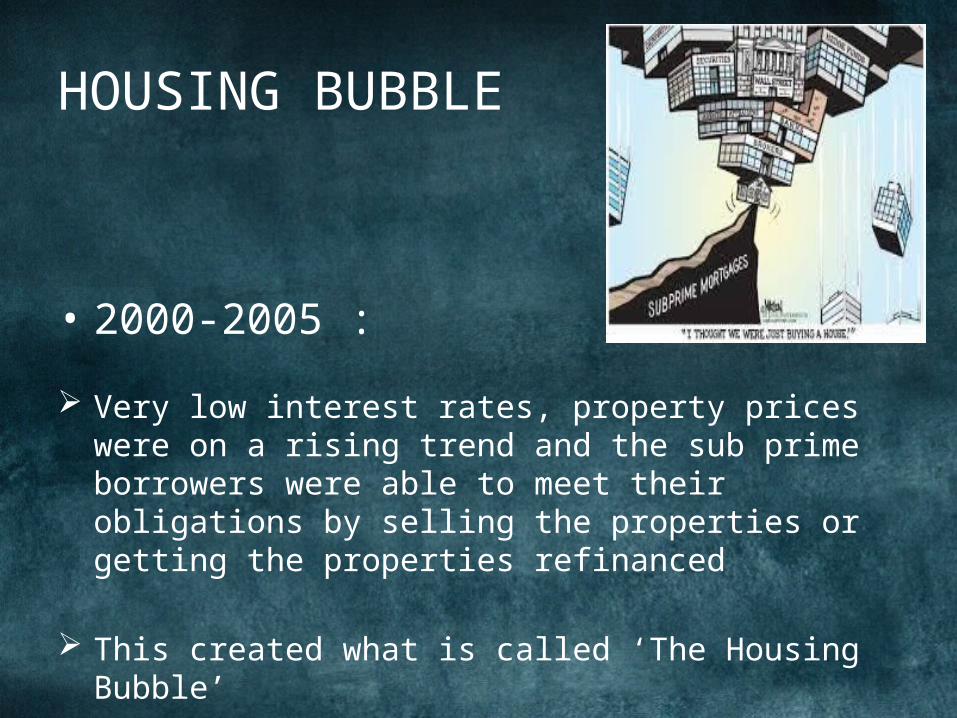

• 2000-2005 :

Very low interest rates, property prices were on a rising trend and the sub prime borrowers were able to meet their obligations by selling the properties or getting the properties refinanced

This created what is called ‘The Housing Bubble’

HOUSING BUBBLE

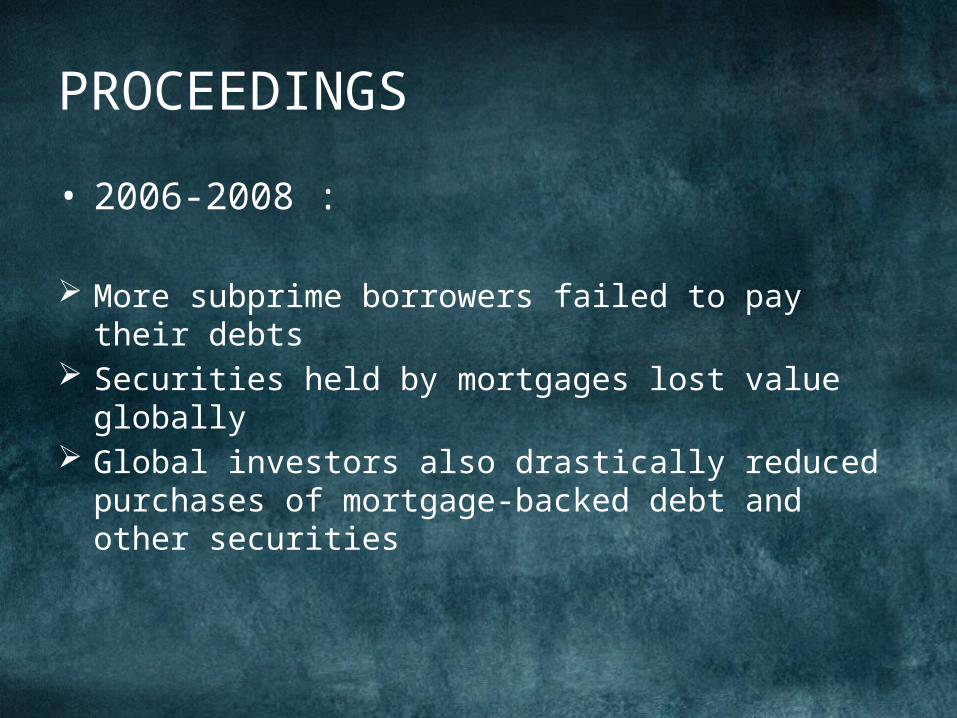

• 2006-2008 :

More subprime borrowers failed to pay their debts Securities held by mortgages lost value globally Global investors also drastically reduced purchases of

mortgage-backed debt and other securities

PROCEEDINGS

WHEN DID IT ALL START?

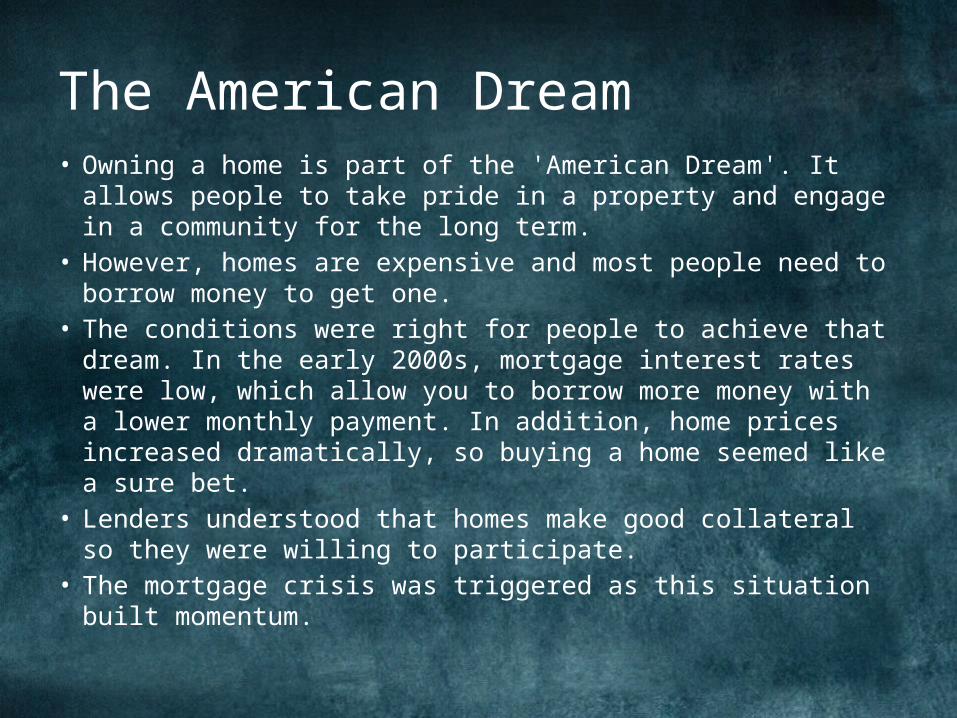

• Owning a home is part of the 'American Dream'. It allows people to take pride in a property and engage in a community for the long term.

• However, homes are expensive and most people need to borrow money to get one.

• The conditions were right for people to achieve that dream. In the early 2000s, mortgage interest rates were low, which allow you to borrow more money with a lower monthly payment. In addition, home prices increased dramatically, so buying a home seemed like a sure bet.

• Lenders understood that homes make good collateral so they were willing to participate.

• The mortgage crisis was triggered as this situation built momentum.

The American Dream

DOT COM COLLAPSE – 2000

SEPTEMBER 11 TERRORIST ATTACK

• Low interest rates

• Increase in loan incentives

• Easy credit conditions

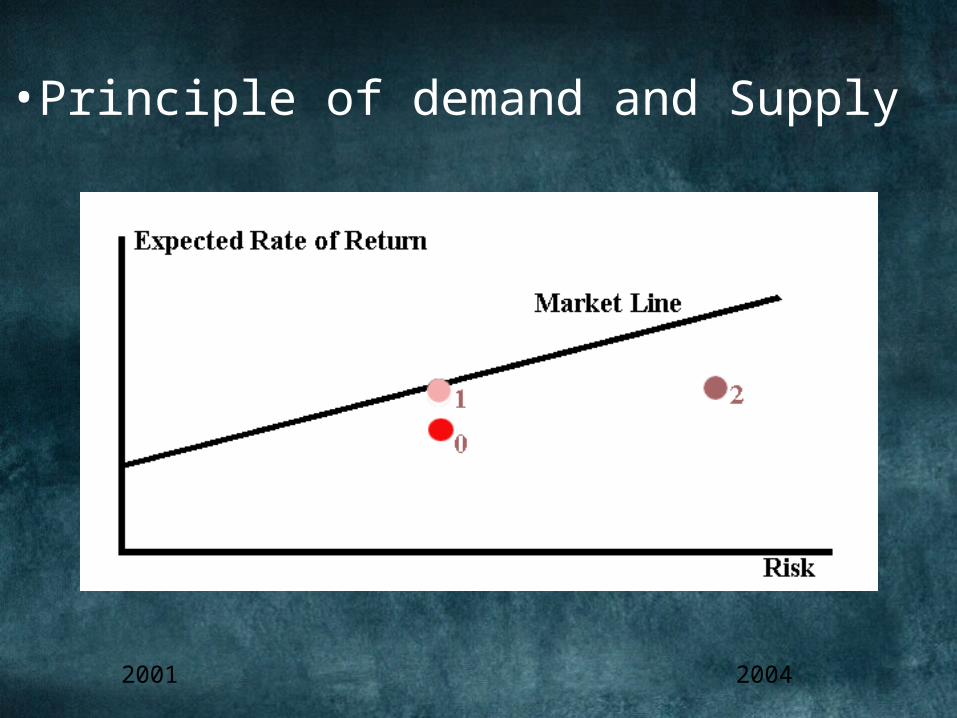

•Principle of demand and Supply

2001 2004

When house prices ceased rising in mid 2006 and then started falling, subprime mortgage defaults began accelerating.

Effects • Sub prime borrowers• Financial institutions• Banks

2006

• On December 1, 2008, the National Bureau of Economic Research announced that the economy had entered into a recession in December of 2007. Real GDP increased by only 0.4 percent for the year 2008, and it decreased at annual rates of 5.4 percent in the 4th quarter of 2008 and 6.4 percent in the 1st quarter of 2009. The unemployment rate increased from 4.9 percent in December of 2007 to 9.5 percent in June of 2009.

• The total real estate equity in The United States was valued at $13 trillion during the 2006 peak, had fallen to $8.8 trillion by mid 2008.

2008

FALL DOWN

The Main Players

The people who contributed to the deadly chain of events that sent the entire world economy into recession.

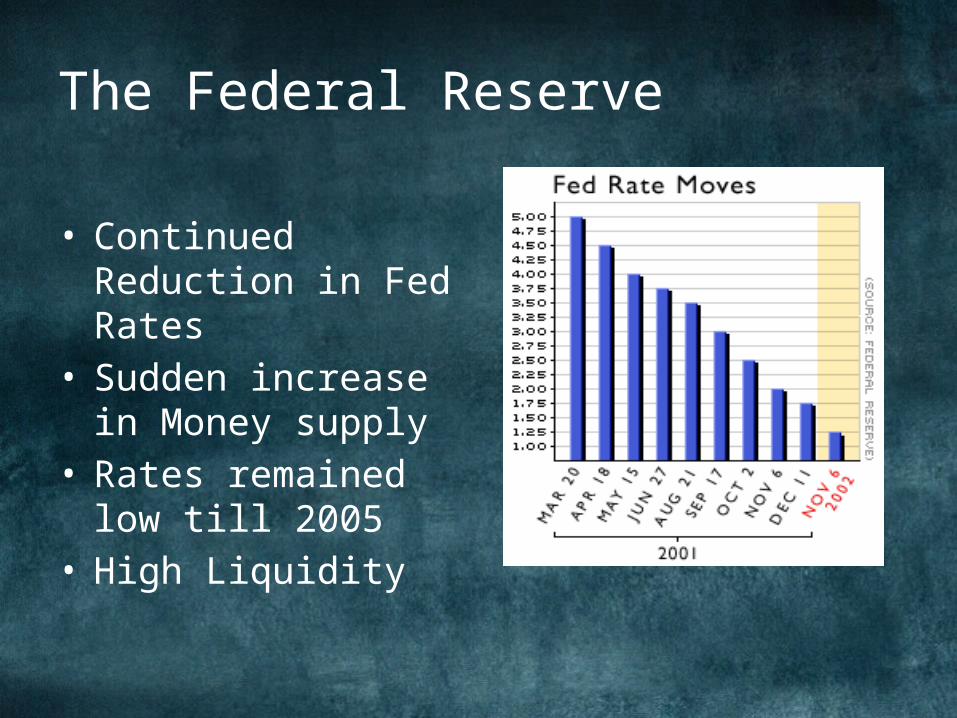

• Continued Reduction in Fed Rates

• Sudden increase in Money supply

• Rates remained low till 2005

• High Liquidity

The Federal Reserve

• Lowered to lending rates to increase loan off take

• As the prime market was nearing saturation, began lending to subprime borrowers

• Aggressively sold MBS, CDO• Additional funds raised by securitization was re-

deployed in the same manner

Commercial Banks

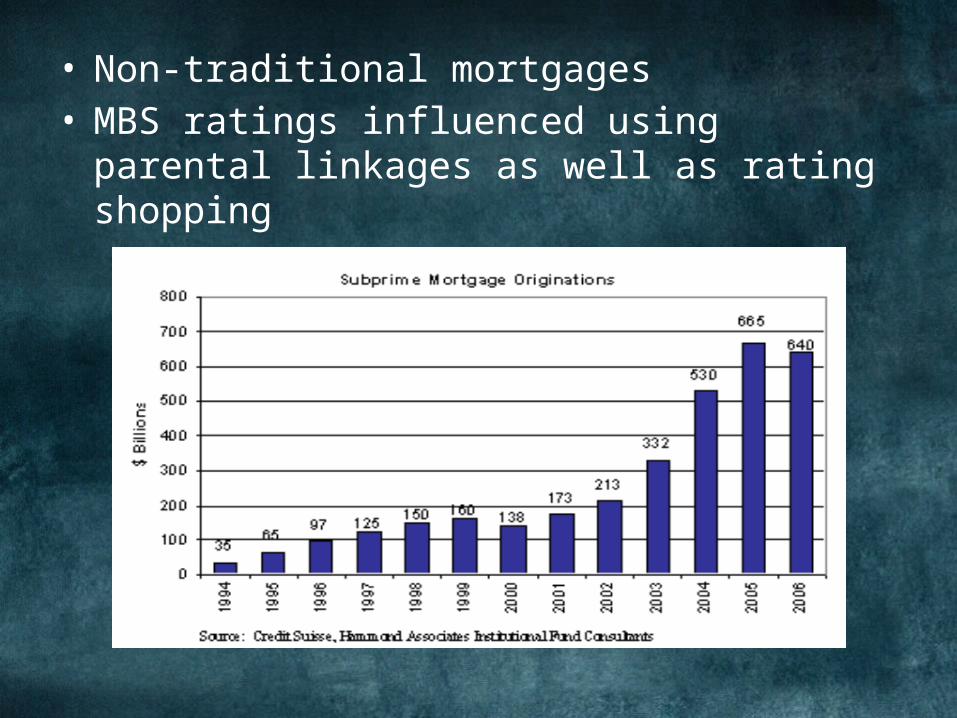

• Non-traditional mortgages• MBS ratings influenced using parental linkages

as well as rating shopping

• Increased use of Secondary mortgage market• Lenders sold their mortgages in the secondary

market• Pooled mortgages into securities like CDOs and

MBS

Investment Banks

Investors:• Investors were the ones willing to purchase

these CDOs at ridiculously low premiums over Treasury bonds.

• These enticingly low rates are what ultimately led to such huge demand for subprime loans.

INVESTORS-

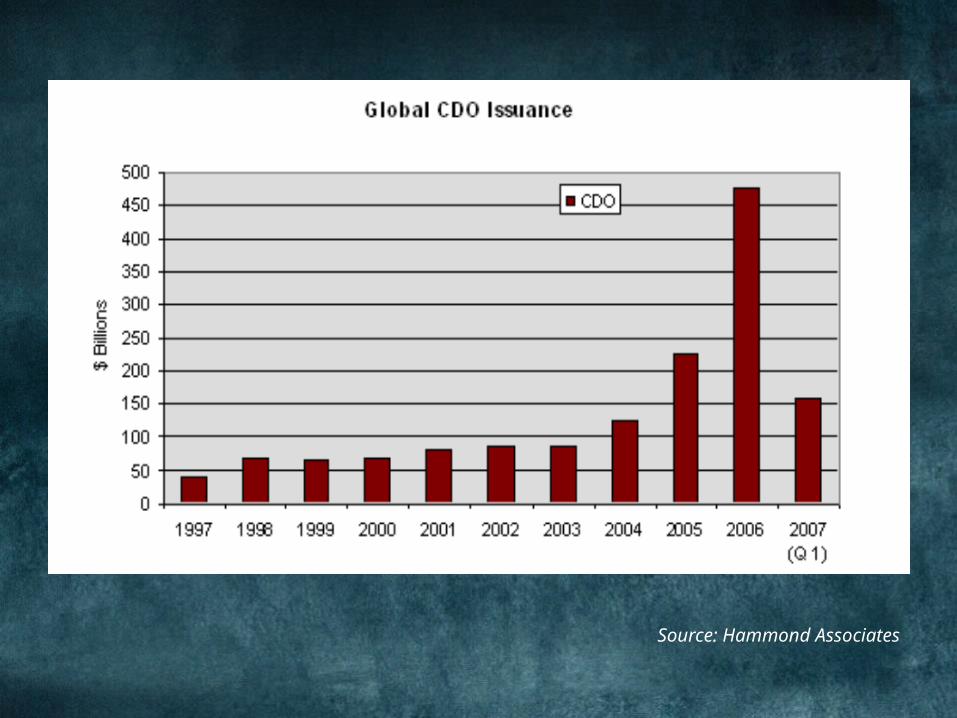

Source: Hammond Associates

• Fuelled volatility through credit arbitrage• Credit Default Swaps• Influenced banks to bring out more MBS &

CDOs as it was a good avenue to invest in

Hedge Funds

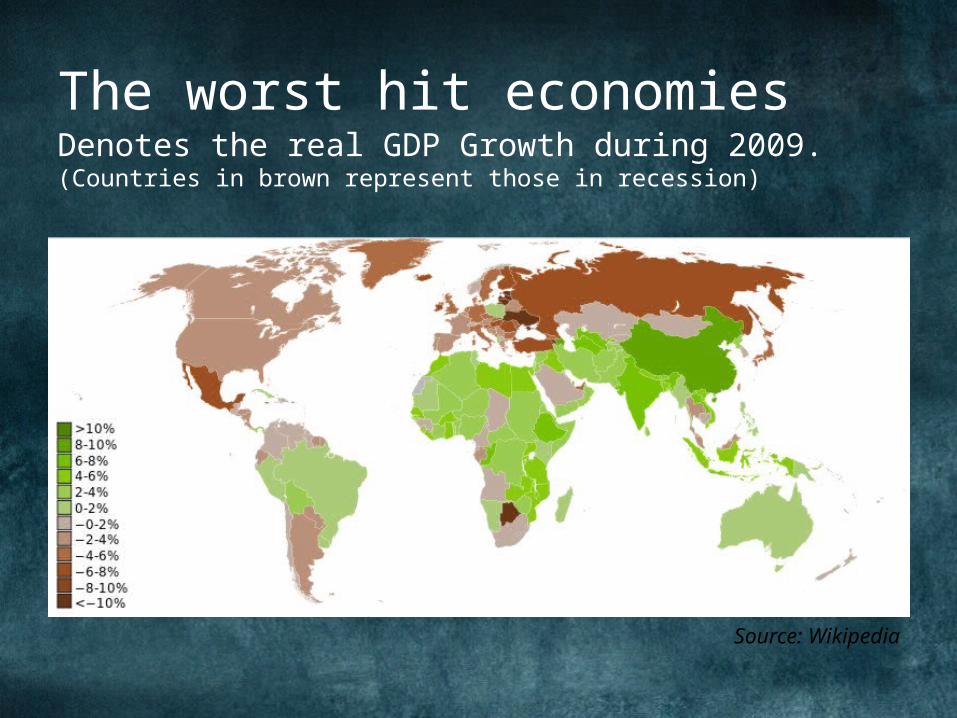

The worst hit economies

Source: Wikipedia

Denotes the real GDP Growth during 2009.(Countries in brown represent those in recession)

SUBPRIME CRISIS AND

INDIA

Impacts of the US Financial Crisis on India

The US meltdown which shook the world had little impact on India, because of India’s strong fundamental and less exposure of Indian

financial sector with the global financial market. Perhaps this has saved Indian economy from

being swayed over instantly. Unlike in US where capitalism rules, in India, market is

closely regulated by the government.

India’s GDP growth rate

Year Growth Rate

2005-06 9.5

2006-07 9.6

2007-08 9.3

2008-09 6.8

2009-10 8.0

2010-11 8.6

Source: http://planningcommission.nic.in/data/datatable/1705/final_1.pdf

Year Growth (US$ Bn)

2006-07 22.6

2007-08 29.0

2008-09 13.7

2009-10 -3.62010-11 29.5

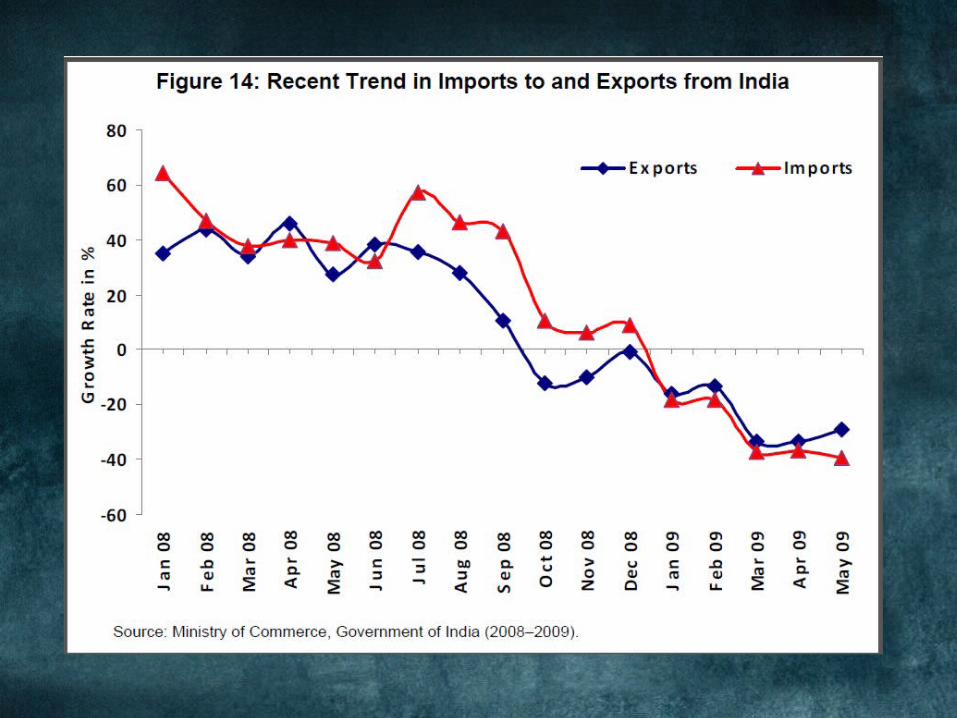

India’s export growth rate

15 per cent of total export in 2006-07 was directed toward USA. Official statistics released on the first day of the New Year, showed that

exports had dropped to $1.5 billion in November 2008, (Sivaraman, 2008) from $12.7 billion a year ago.

Manufacturing sectors like leather, textile, gems and jewellery got hit hard.

Impact on Indian Stock Market

BSE ‘SENSEX’ PERFORMANCE IN 2008

Month Open High Low Close

January 20325.27 21,206.77 15,332.42 17468.71

February 17820.67 18,895.34 16,457.74 17578.72

March 17227.56 17,227.56 14,677.24 15644.44

April 15771.72 17,480.74 15,297.96 17287.31

May 17560.15 17,735.70 16,196.02 16415.57

June 16591.46 16,632.72 13,405.54 13461.60

July 13480.02 15,130.09 12,514.02 14355.75

August 14064.26 15,579.78 14,002.43 14564.53

September 14412.99 15,107.01 12,153.55 12860.43

October 13006.72 13,203.86 7,697.39 9788.06

November 10209.37 10,945.41 8,316.39 9092.72

December 9162.94 10,188.54 8,467.43 9647.31

Source: http://www.bseindia.com/indices/indexarchivedata.aspx

Impact on India’s tradeImpact on India’s handloom

sector, jewellery export and tourism

Exchange rate depreciationInformation technology-BPO

sectorForeign institutional investors

and FDI

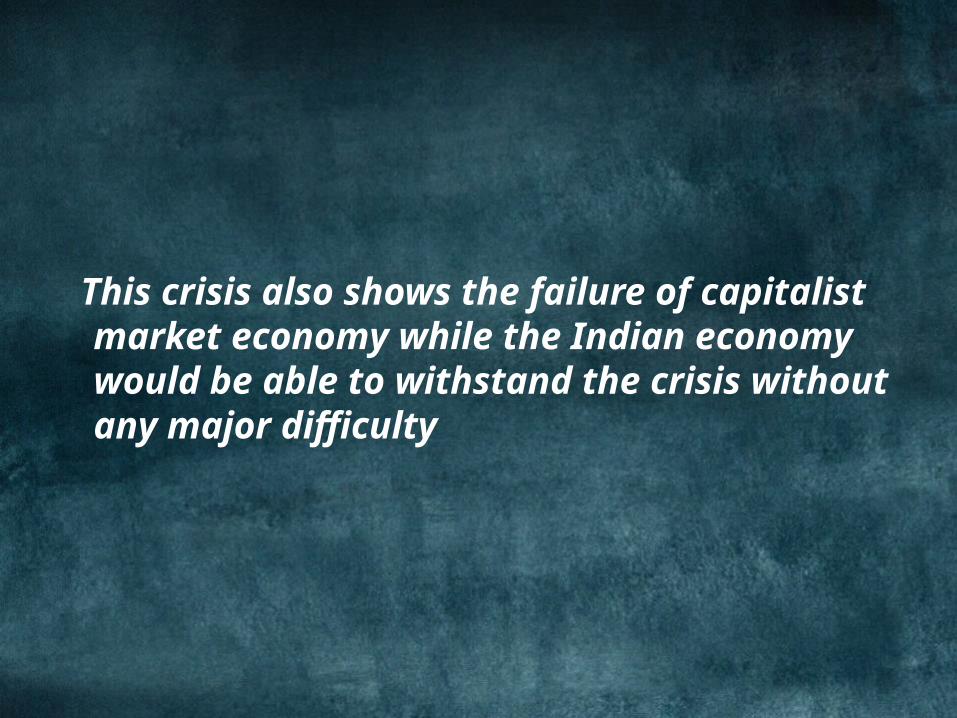

This crisis also shows the failure of capitalist market economy while the Indian economy would be able to withstand the crisis without any major difficulty

Why sub prime is not a crisis in

India ??

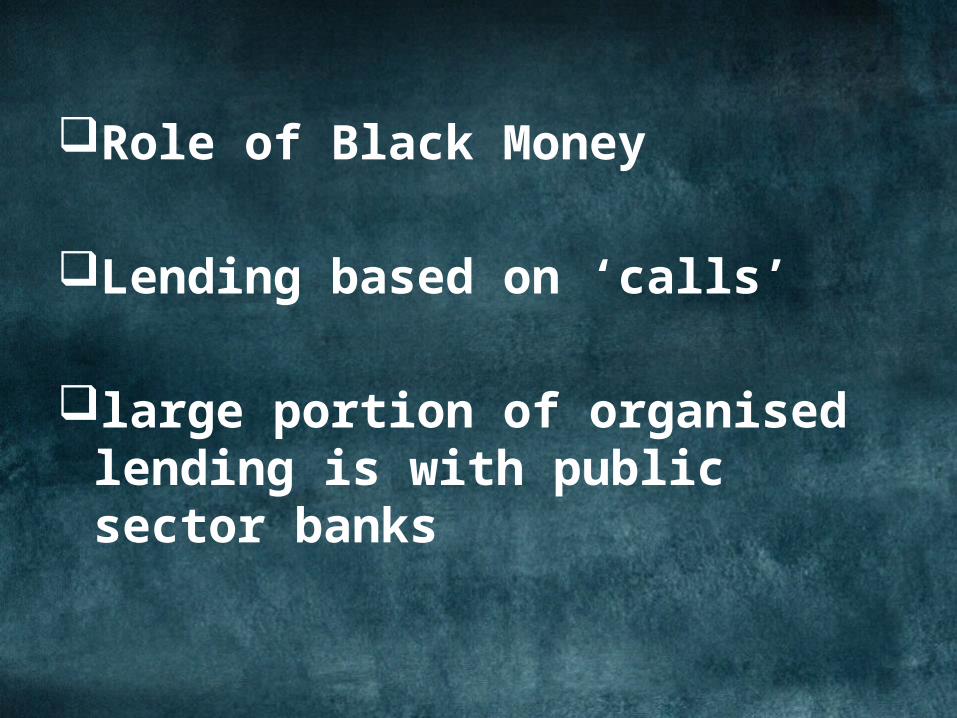

Role of Black Money

Lending based on ‘calls’

large portion of organised lending is with public sector banks

• He started sensing that real estate, in particular, had entered bubble territory before the crisis.

• One of the first moves he made was to ban the use of bank loans for the purchase of raw land.

• Only when the developer was about to commence building could the bank get involved — and then only to make construction loans.

ONE MAN ARMY of Dr. Y.V. Reddy!

• Reddy pushed interest rates up to more than 20 percent, which of course dampened the housing frenzy.

• He made banks put aside extra capital for every loan they made.

• In effect, Mr. Reddy was creating liquidity even before there was a global liquidity crisis.

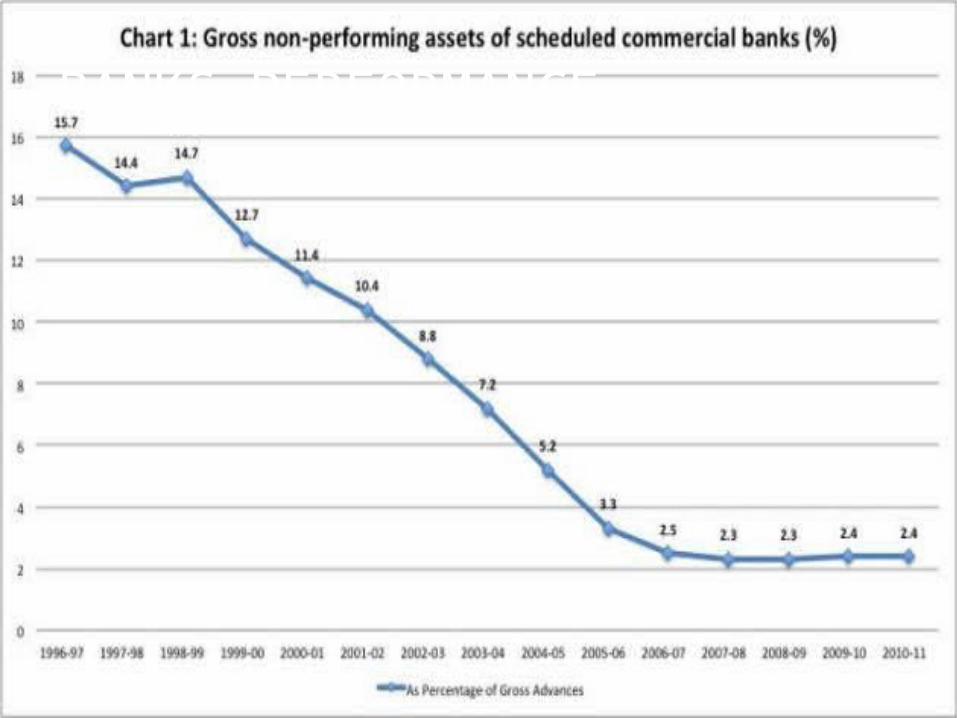

BANKS PERFORMANCE

THANK YOU