Embed Size (px)

Citation preview

BUDAPEST STOCK EXCHANGEAnalysis of stock index of an emerging economy

Santosh J K

Introduction

• Stock Index: BUX, Budapest Stock Exchange, Hungary

• Applications utilised: Microsoft Excel 2011, Eviews 7.0

• Significant models: ARIMA(3,1,3), GARCH(2,3) & GARCH(3,2)

• In-sample data: April 01’ 1997 to March 31’ 2009

• Out-sample data: April 01’ 2009 to November 12’ 2013

Time series plot of BUX

0"

5,000"

10,000"

15,000"

20,000"

25,000"

30,000"

35,000"

01/04/1997"

01/04/1998"

01/04/1999"

01/04/2000"

01/04/2001"

01/04/2002"

01/04/2003"

01/04/2004"

01/04/2005"

01/04/2006"

01/04/2007"

01/04/2008"

01/04/2009"

01/04/2010"

01/04/2011"

01/04/2012"

01/04/2013"

BUX$

Data description

0

100

200

300

400

500

600

700

4000 8000 12000 16000 20000 24000 28000

Series: BUXSample 4/01/1997 11/12/2013Observations 4034

Mean 14658.74Median 14695.23Maximum 30118.12Minimum 3775.020Std. Dev. 6833.213Skewness 0.184081Kurtosis 1.560072

Jarque-Bera 371.2852Probability 0.000000

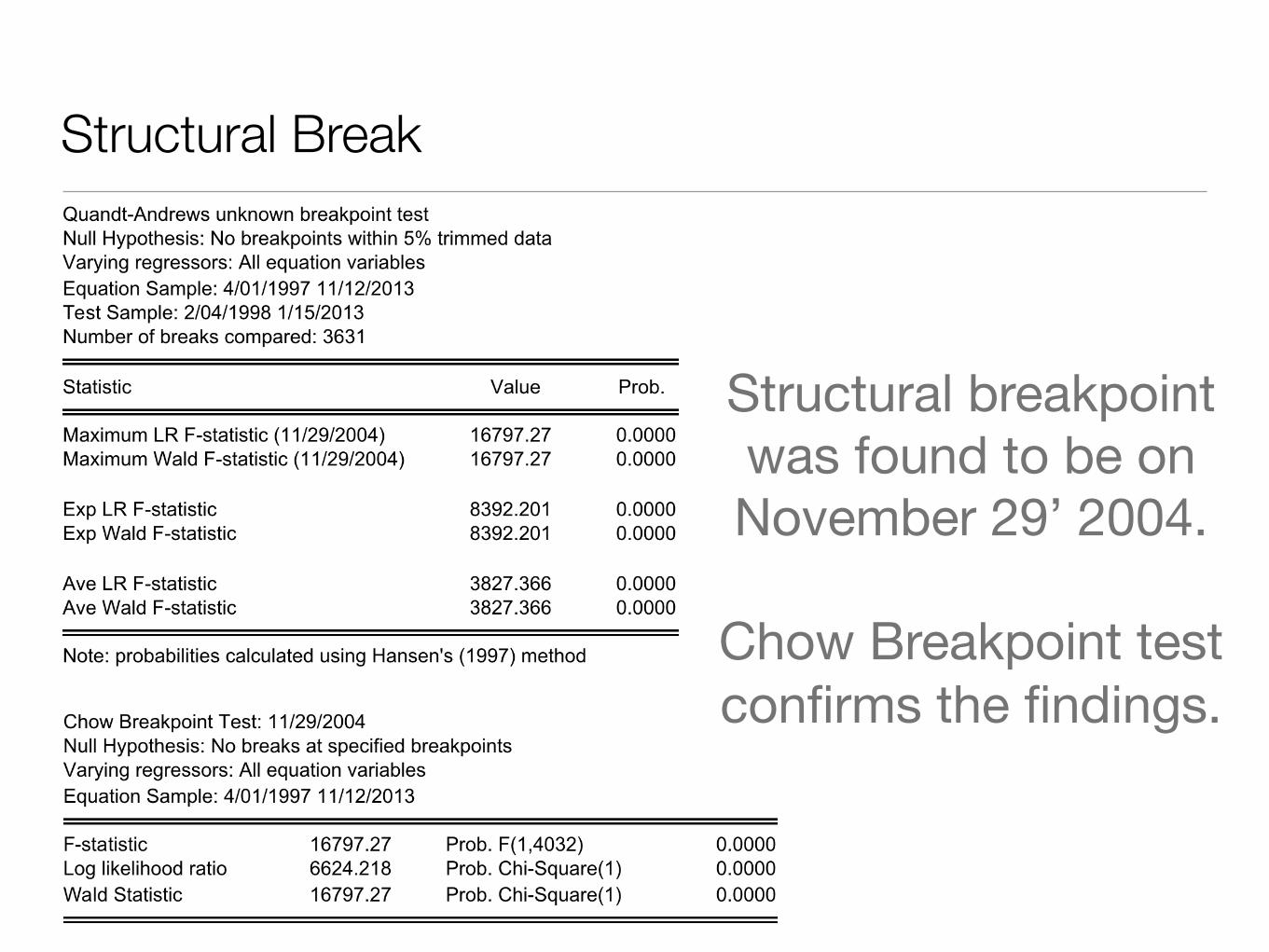

Structural Break

Structural breakpoint was found to be on November 29’ 2004.

Chow Breakpoint test confirms the findings.

Stationarity

Data was found to be stationary for the log returns of the index, as per the ADF - first

difference test.

Time series plot of the log returns of BUX

-.20

-.15

-.10

-.05

.00

.05

.10

.15

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

LN(BUX)

ARIMA model

A series of iterations revealed,

ARIMA(3,1,3) to be the best fit

model.

GARCH model

Two models turned out to be highly

significant - GARCH(2,3) & GARCH(3,2).

Of the two, GARCH(2,3)

is relatively better.

GARCH model

The other highly significant GARCH

model.

Log returns of BUX and S&P 500

-.20

-.15

-.10

-.05

.00

.05

.10

.15

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

LN(BUX) LN(S&P)

Structural model - Lag order selection

Lag 6 is significant

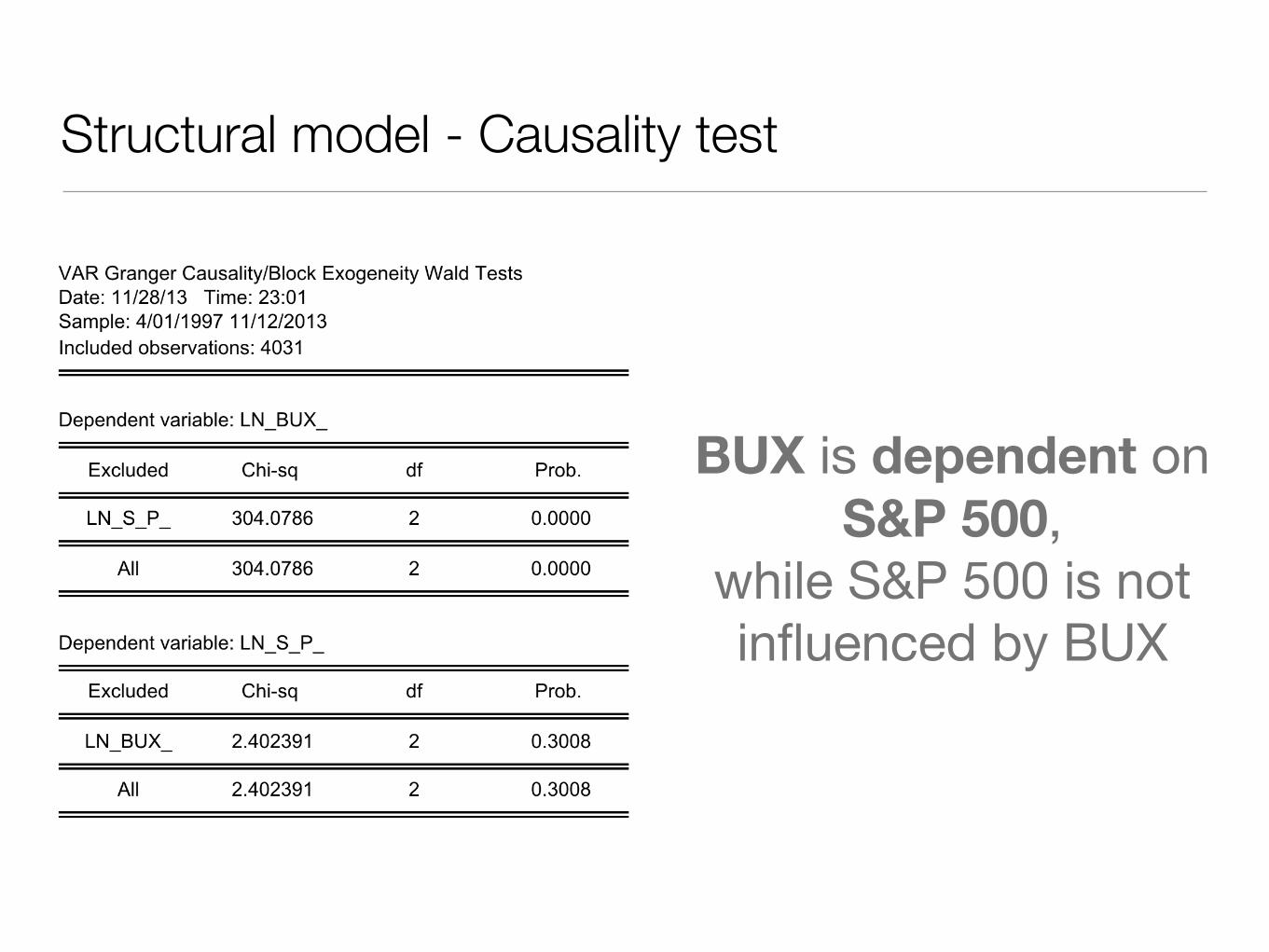

Structural model - Causality test

BUX is dependent on S&P 500,

while S&P 500 is not influenced by BUX

Forecast

-.20

-.15

-.10

-.05

.00

.05

.10

.15

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

LN(BUX) LN(BUX) (Baseline)

THANK YOU

Santosh J K