Embed Size (px)

Citation preview

1

Corporate Presentation

August, 2013

History and Business Model

3

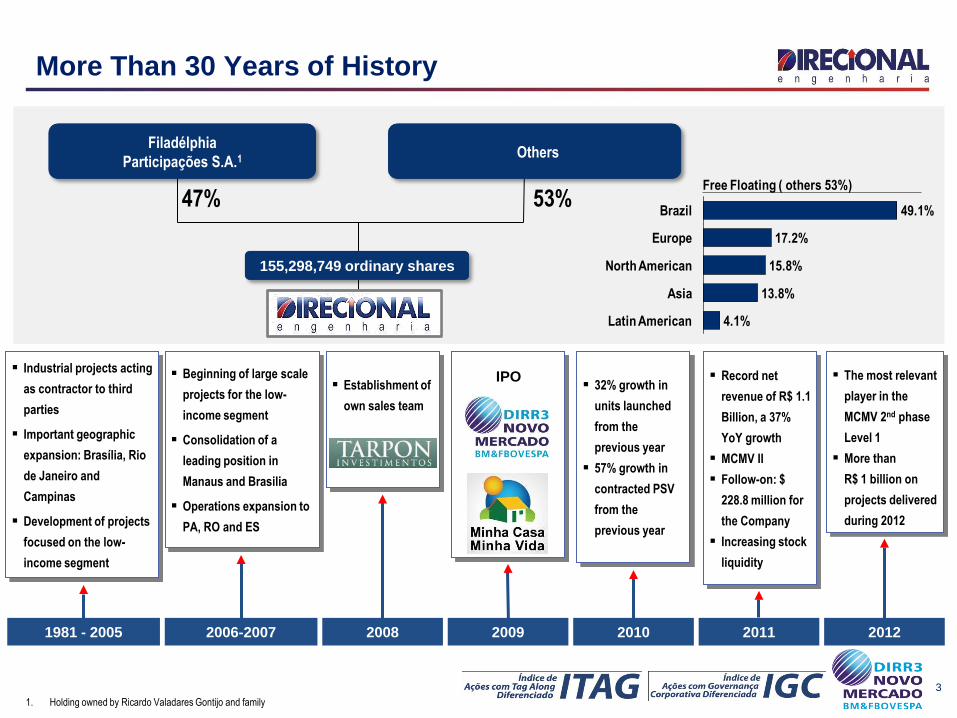

More Than 30 Years of History

47%

Filadélphia

Participações S.A.1 Others

53%

155,298,749 ordinary shares

1. Holding owned by Ricardo Valadares Gontijo and family

Industrial projects acting

as contractor to third

parties

Important geographic

expansion: Brasília, Rio

de Janeiro and

Campinas

Development of projects

focused on the low-

income segment

Beginning of large scale

projects for the low-

income segment

Consolidation of a

leading position in

Manaus and Brasilia

Operations expansion to

PA, RO and ES

IPO 32% growth in

units launched

from the

previous year

57% growth in

contracted PSV

from the

previous year

Establishment of

own sales team

1981 - 2005 2006-2007 2008 2009 2010 2011

Record net

revenue of R$ 1.1

Billion, a 37%

YoY growth

MCMV II

Follow-on: $

228.8 million for

the Company

Increasing stock

liquidity

The most relevant

player in the

MCMV 2nd phase

Level 1

More than

R$ 1 billion on

projects delivered

during 2012

2012

Latin American

Asia 13.8%

North American

4.1%

Europe

15.8%

Brazil

17.2%

49.1%

Free Floating ( others 53%)

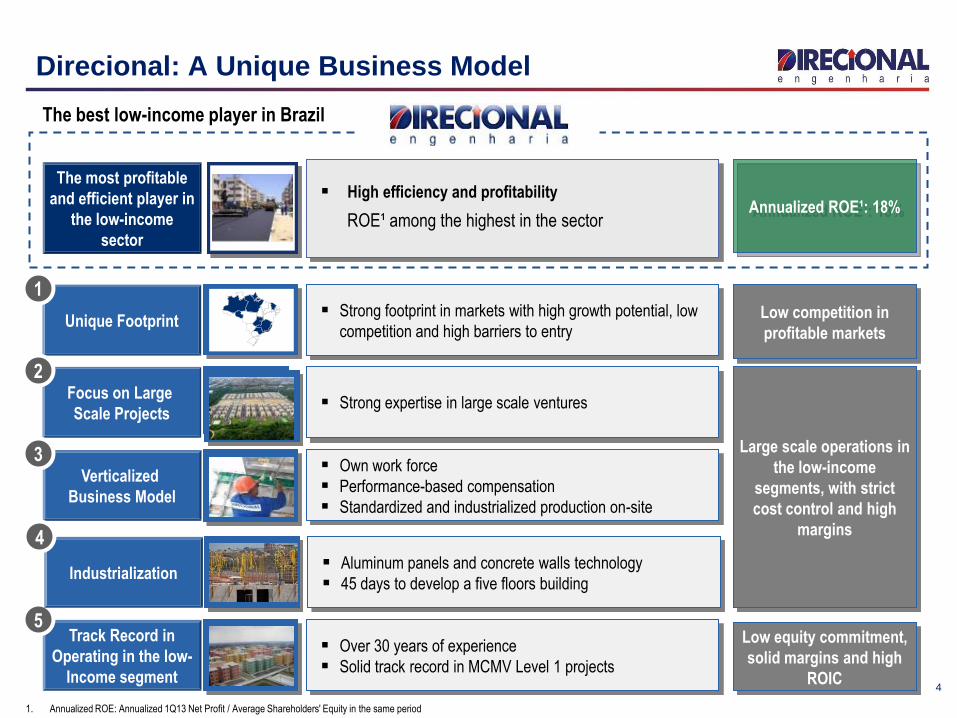

Unique Footprint Strong footprint in markets with high growth potential, low

competition and high barriers to entry Low competition in

profitable markets

Track Record in

Operating in the low-

Income segment

Over 30 years of experience

Solid track record in MCMV Level 1 projects

Low equity commitment,

solid margins and high

ROIC

Focus on Large

Scale Projects

Verticalized

Business Model

Strong expertise in large scale ventures

Own work force

Performance-based compensation

Standardized and industrialized production on-site

Large scale operations in

the low-income

segments, with strict

cost control and high

margins

4

Direcional: A Unique Business Model

The most profitable

and efficient player in

the low-income

sector

‘’’’

High efficiency and profitability

ROE¹ among the highest in the sector

1

2

3

5

Annualized ROE¹: 18%

1. Annualized ROE: Annualized 1Q13 Net Profit / Average Shareholders' Equity in the same period

The best low-income player in Brazil

Industrialization Aluminum panels and concrete walls technology

45 days to develop a five floors building

4

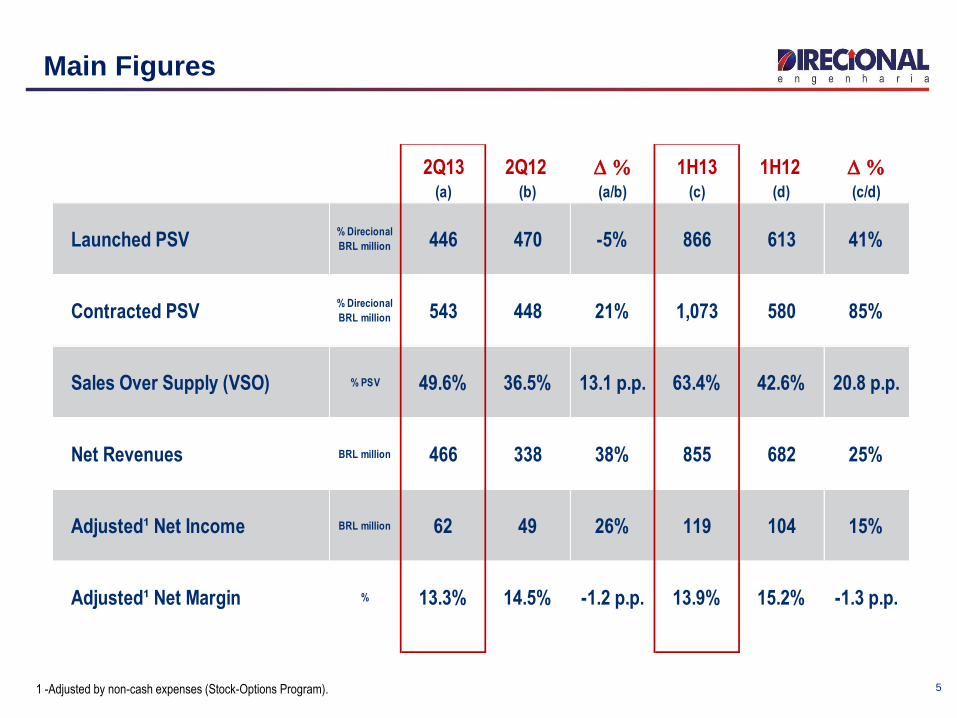

Main Figures

5 1 -Adjusted by non-cash expenses (Stock-Options Program).

2Q13 2Q12 D % 1H13 1H12 D %(a) (b) (a/b) (c) (d) (c/d)

Launched PSV% Direcional

BRL million 446 470 -5% 866 613 41%

Contracted PSV% Direcional

BRL million 543 448 21% 1,073 580 85%

Sales Over Supply (VSO) % PSV 49.6% 36.5% 13.1 p.p. 63.4% 42.6% 20.8 p.p.

Net Revenues BRL million 466 338 38% 855 682 25%

Adjusted¹ Net Income BRL million 62 49 26% 119 104 15%

Adjusted¹ Net Margin % 13.3% 14.5% -1.2 p.p. 13.9% 15.2% -1.3 p.p.

6

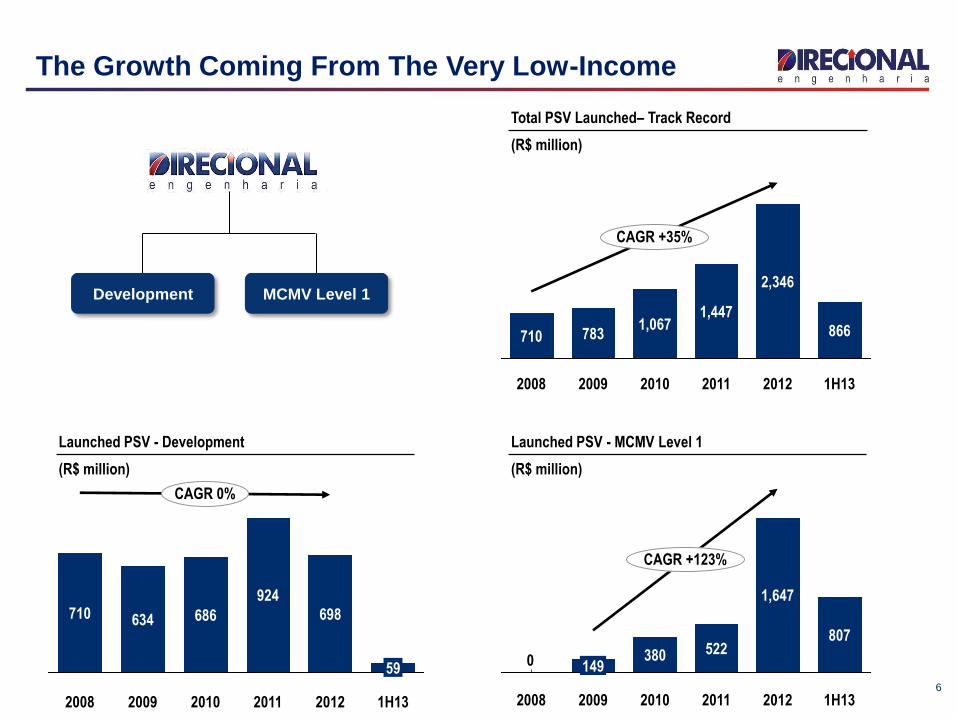

The Growth Coming From The Very Low-Income

Total PSV Launched– Track Record

(R$ million)

CAGR +35%

1H13

866

2012

2,346

2011

1,447

2010

1,067

2009

783

2008

710

Development MCMV Level 1

Launched PSV - MCMV Level 1

(R$ million)

686

2009

634

2008

710

CAGR 0%

1H13

59

2012

698

2011

924

2010

Launched PSV - Development

(R$ million)

0 380

CAGR +123%

1H13

807

2012

1,647

2011

522

2010 2009

149

2008

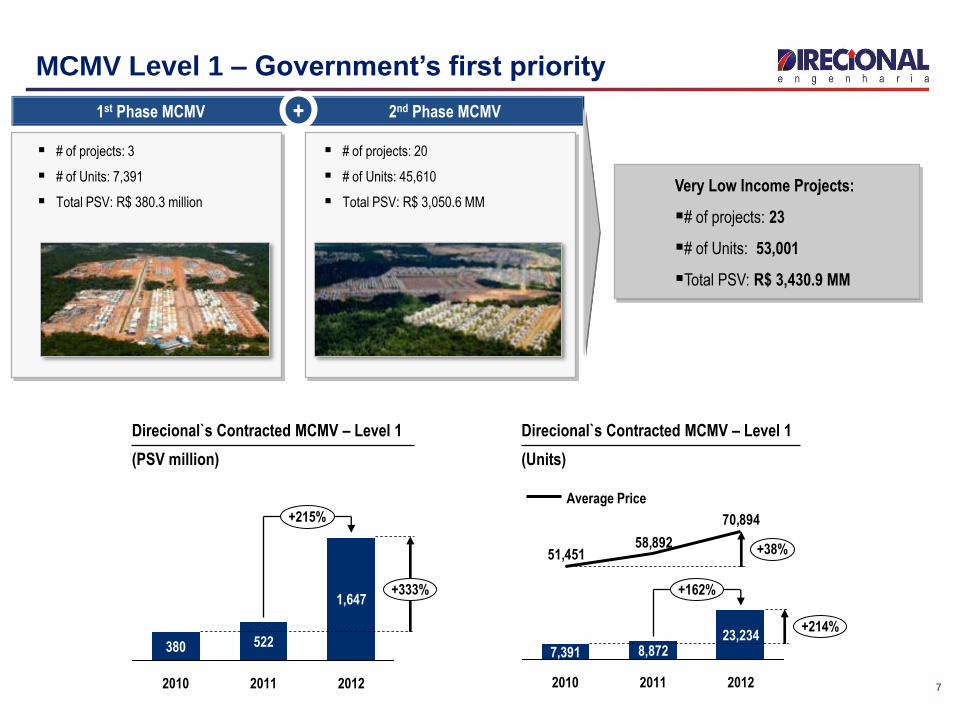

Very Low Income Projects:

# of projects: 23

# of Units: 53,001

Total PSV: R$ 3,430.9 MM

7

MCMV Level 1 – Government’s first priority

1st Phase MCMV 2nd Phase MCMV

# of projects: 3

# of Units: 7,391

Total PSV: R$ 380.3 million

# of projects: 20

# of Units: 45,610

Total PSV: R$ 3,050.6 MM

+

Direcional`s Contracted MCMV – Level 1

(PSV million)

Direcional`s Contracted MCMV – Level 1

(Units)

+215%

+333%

2012 2011

1,647

522

2010

380

70,894

58,89251,451

2010

7,391

+214%

+162%

+38%

2012

23,234

2011

8,872

Average Price

8

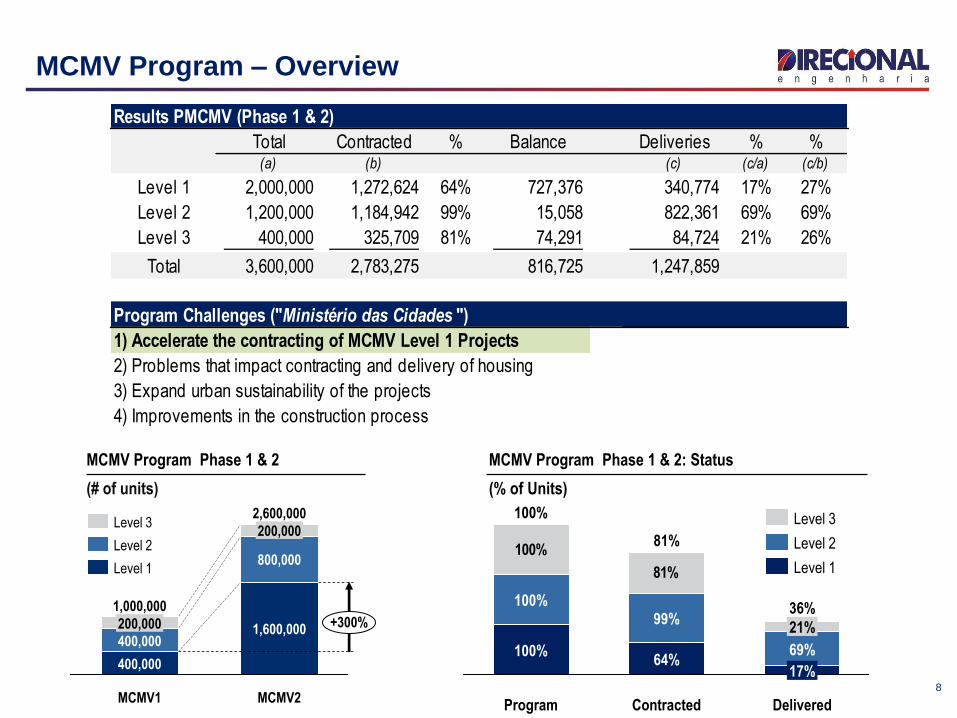

100%

81%

Delivered

36%

17%

69%

21%

Contracted

81%

64%

99%

Program

100%

100%

100%

Level 1

Level 2

Level 3

MCMV Program – Overview

2,600,000

+300%

MCMV2

1,600,000

800,000

200,000

MCMV1

1,000,000

400,000

400,000

200,000

Level 1

Level 2

Level 3

MCMV Program Phase 1 & 2

(# of units)

MCMV Program Phase 1 & 2: Status

(% of Units)

Results PMCMV (Phase 1 & 2)

Total Contracted % Balance Deliveries % %(a) (b) (c) (c/a) (c/b)

Level 1 2,000,000 1,272,624 64% 727,376 340,774 17% 27%

Level 2 1,200,000 1,184,942 99% 15,058 822,361 69% 69%

Level 3 400,000 325,709 81% 74,291 84,724 21% 26%

Total 3,600,000 2,783,275 816,725 1,247,859

Program Challenges ("Ministério das Cidades ")

1) Accelerate the contracting of MCMV Level 1 Projects

2) Problems that impact contracting and delivery of housing

3) Expand urban sustainability of the projects

4) Improvements in the construction process

9

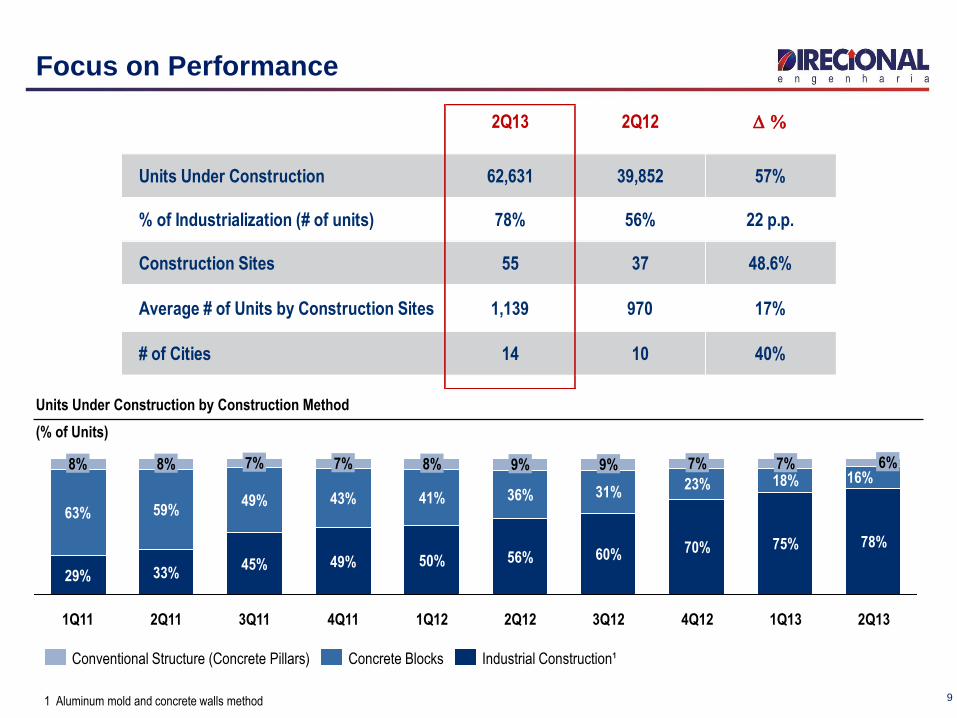

Focus on Performance

36%

9%

1Q12

50%

41%

60%

31%

9%

2Q12

56%

8%

4Q11

49%

43%

7%

3Q11

45%

49%

7%

2Q11

33%

59%

8%

1Q11

29%

63%

8%

1Q13

75%

18% 7%

4Q12

70%

23%

7%

3Q12 2Q13

6% 16%

78%

Units Under Construction by Construction Method

(% of Units)

1 Aluminum mold and concrete walls method

Industrial Construction¹ Concrete Blocks Conventional Structure (Concrete Pillars)

2Q13 2Q12 D %

Units Under Construction 62,631 39,852 57%

% of Industrialization (# of units) 78% 56% 22 p.p.

Construction Sites 55 37 48.6%

Average # of Units by Construction Sites 1,139 970 17%

# of Cities 14 10 40%

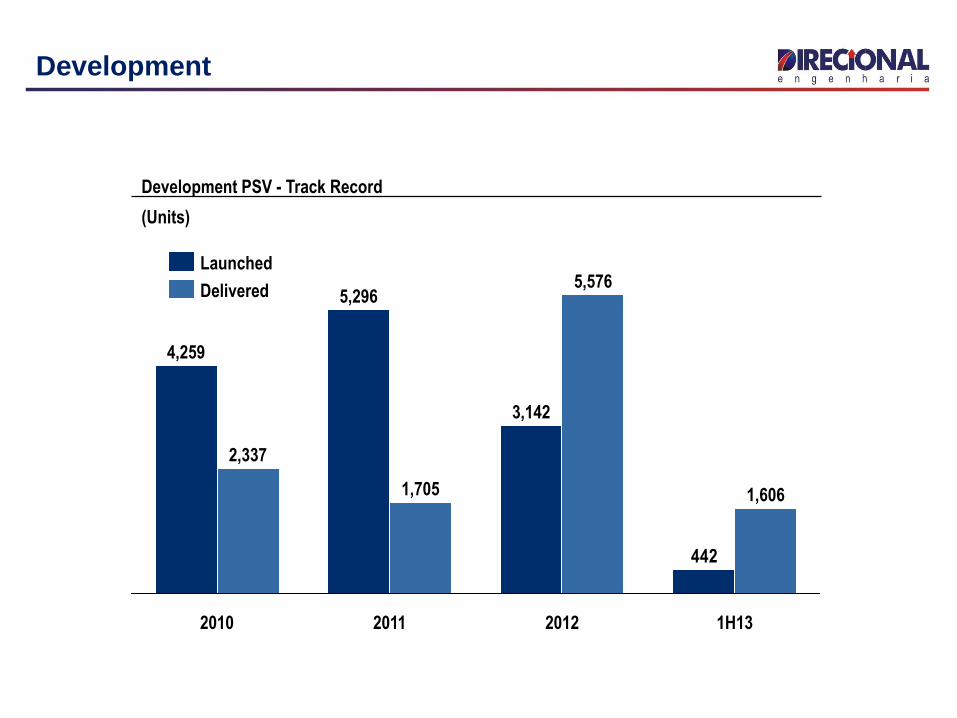

Development

Development PSV - Track Record

(Units)

442

2,337

4,259

1H13

1,606

2012

5,576

3,142

2011

1,705

5,296

2010

Delivered

Launched

Operating Highlights

11

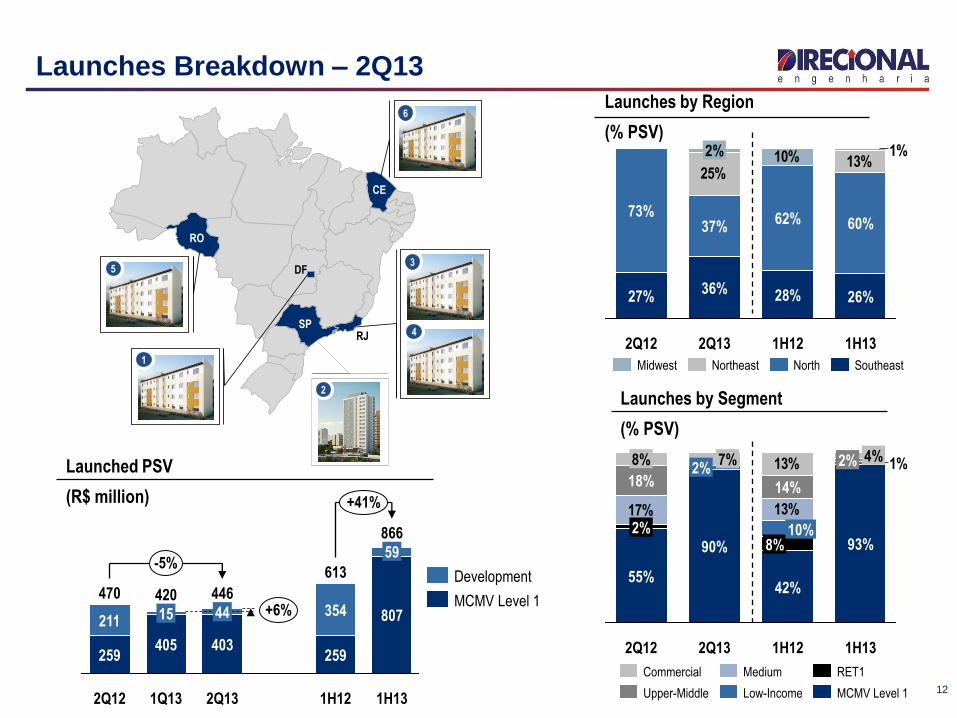

Launches Breakdown – 2Q13

12

Launches by Segment

(% PSV)

Launches by Region

(% PSV)

10% 13%25%

1%

1H13

26%

60%

1H12

28%

62%

2Q13

36%

37%

2%

2Q12

27%

73%

Southeast North Northeast Midwest

1%

13%17%

13%

1H13

93%

2% 4%

1H12

42%

8% 10%

14%

2Q13

90%

2% 7%

2Q12

55%

2%

18%

8%

MCMV Level 1

RET1

Low-Income

Medium

Upper-Middle

Commercial

Launched PSV

(R$ million)

+41%

-5%

2Q12

470

259

211

1H12

613

259

354

2Q13

446

403

44

1Q13

420

405

15 +6%

1H13

866

807

59

MCMV Level 1

Development

RO

RJSP

4

DF

CE

35

6

1

2

13

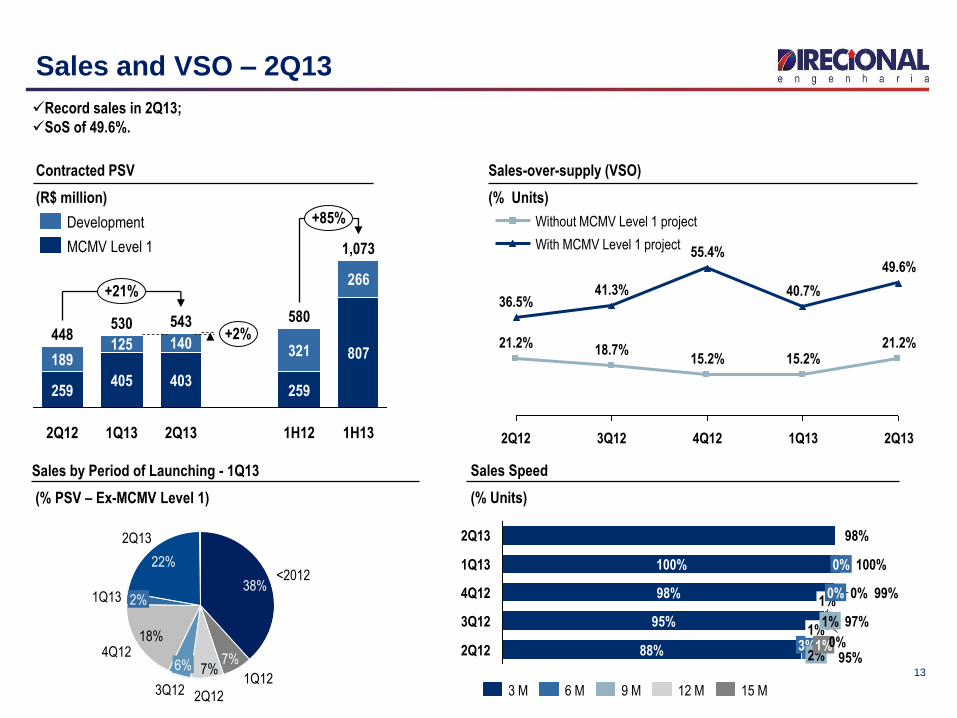

Sales and VSO – 2Q13

2Q13

49.6%

21.2%

1Q13

40.7%

15.2%

4Q12

55.4%

15.2%

3Q12

41.3%

18.7%

2Q12

36.5%

21.2%

With MCMV Level 1 project

Without MCMV Level 1 project

2Q12 95%

88% 3% 2%

1% 1%

3Q12 97% 95%

1%

1%

0%

4Q12 99% 98% 0% 0%

1Q13 100% 100% 0%

2Q13 98%

3 M 6 M 9 M 12 M 15 M

Sales by Period of Launching - 1Q13

(% PSV – Ex-MCMV Level 1)

7%

2Q13

22%

1Q13 2%

4Q12 18%

3Q12

6%

2Q12

1Q12

7%

<2012 38%

Contracted PSV

(R$ million)

Sales-over-supply (VSO)

(% Units)

Sales Speed

(% Units)

Record sales in 2Q13;

SoS of 49.6%.

543

403

140

1Q13

530

405

125

2Q12

448

259

807

266

1H12

580

259

+85%

+21%

+2%

1H13

1,073

321

2Q13

189

MCMV Level 1

Development

14

Land Bank

58,5% are large scale projects (over 1,000 units)

76,6% are eligible for the MCMV Program

77,4% were acquired by physical or financial Swap

Average acquisition price of 9,5% over PSV

R$ 6.6 Billion

60,702 units

Land Bank by Segment

(% PSV)

Land Bank Track Record in 1Q13

(R$ million in PSV)

293159 6,549 -101

2Q13 Launches

33

Review of

Assumptions

Acquired

Land Bank

1Q13

6,448

Land Bank by Region

(% PSV)

Type of Payment

(1Q13 – % PSV)

58.9% Cash 41.1% Swap

RET

6%

Low-Income

39%

Upper-Middle 12%

Medium 39%

Commercial 4%

ES2%

AM15%

MG42%

RO2%

SP8%

PA9%

DF21%

GO1%

15

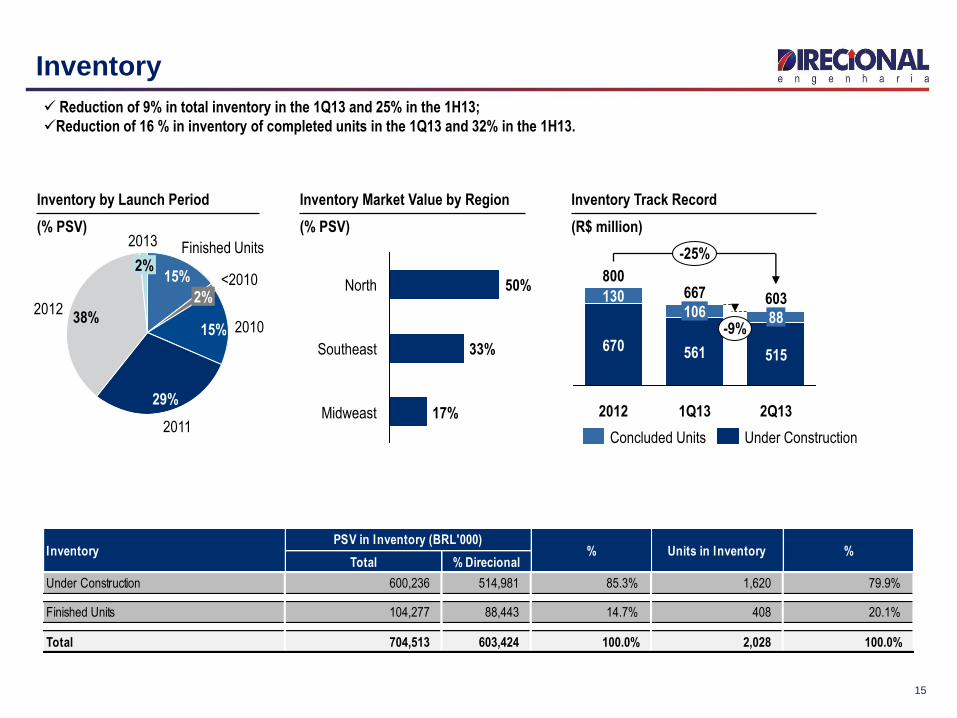

Inventory

Reduction of 9% in total inventory in the 1Q13 and 25% in the 1H13;

Reduction of 16 % in inventory of completed units in the 1Q13 and 32% in the 1H13.

2013

2%

2012 38%

2011

29%

2010 15%

<2010 2%

Finished Units

15%

Midweast 17%

Southeast 33%

North 50% 603

-9%

-25%

2Q13

515

88

1Q13

667

561

106

2012

800

670

130

Under Construction Concluded Units

Inventory Market Value by Region

(% PSV)

Inventory by Launch Period

(% PSV)

Inventory Track Record

(R$ million)

Total % Direcional

Under Construction 600,236 514,981 85.3% 1,620 79.9%

Finished Units 104,277 88,443 14.7% 408 20.1%

Total 704,513 603,424 100.0% 2,028 100.0%

InventoryPSV in Inventory (BRL'000)

% Units in Inventory %

Financial Highlights

16

17

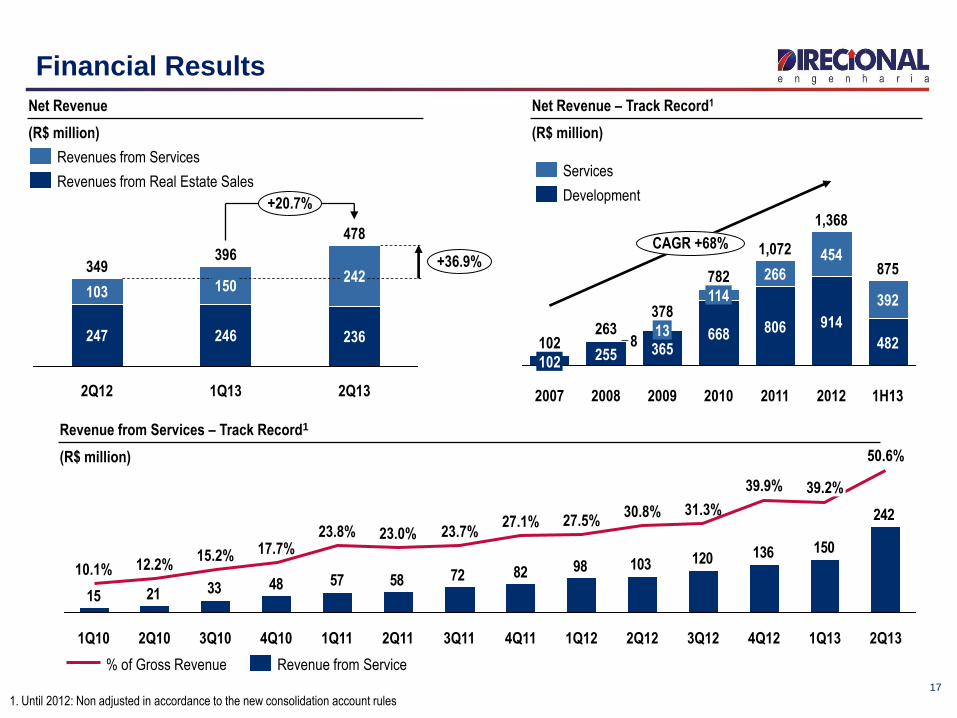

Financial Results

478

+36.9%

+20.7%

2Q13

236

242

1Q13

396

246

150

2Q12

349

247

103

Net Revenue

(R$ million)

8

CAGR +68%

1H13

875

482

392

2012

1,368

914

454

2011

1,072

806

266

2010

782

668

114

2009

378

365 13

2008

263

255

2007

102

102

Net Revenue – Track Record1

(R$ million)

Development

Services

Revenue from Services – Track Record1

(R$ million)

242

150136120103988272585748332115

2Q13

50.6%

1Q13

39.2%

4Q12

39.9%

3Q12

31.3%

2Q12

30.8%

1Q12

27.5%

4Q11

27.1%

3Q11

23.7%

2Q11

23.0%

1Q11

23.8%

4Q10

17.7%

3Q10

15.2%

2Q10

12.2%

1Q10

10.1%

Revenue from Service % of Gross Revenue

Revenues from Real Estate Sales

Revenues from Services

1. Until 2012: Non adjusted in accordance to the new consolidation account rules

18

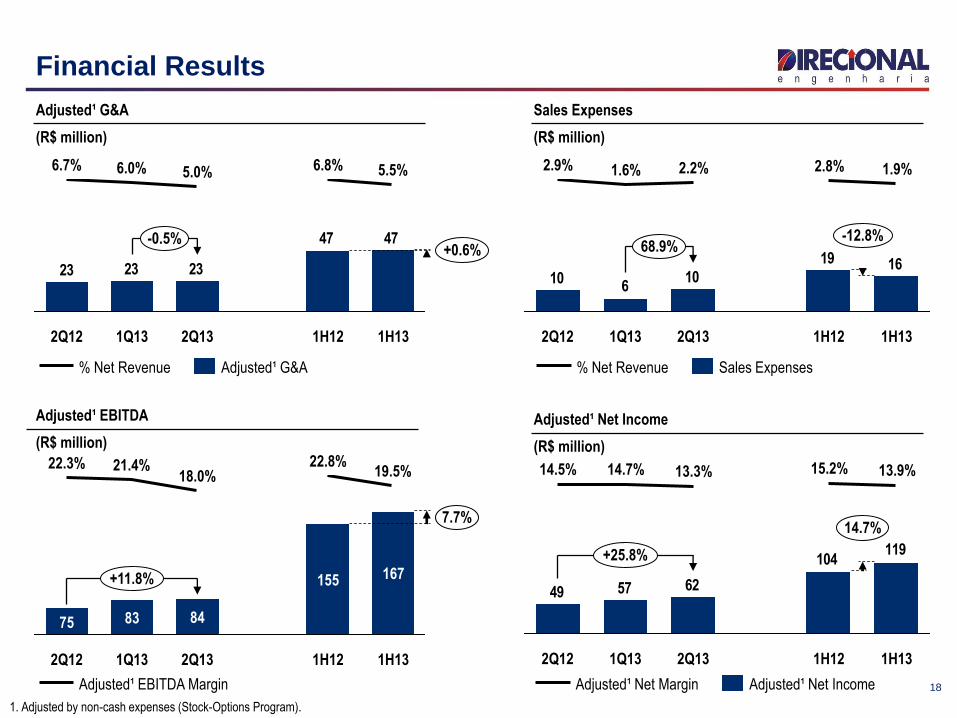

Financial Results

1. Adjusted by non-cash expenses (Stock-Options Program).

Adjusted¹ G&A

(R$ million)

Sales Expenses

(R$ million)

4747

232323

-0.5% +0.6%

1H13

5.5%

1H12

6.8%

2Q13

5.0%

1Q13

6.0%

2Q12

6.7%

1619

106

10

68.9% -12.8%

1H13

1.9%

1H12

2.8%

2Q13

2.2%

1Q13

1.6%

2Q12

2.9%

Sales Expenses % Net Revenue Adjusted¹ G&A % Net Revenue

+11.8%

7.7%

1H13

167

19.5%

1H12

155

22.8%

2Q13

84

18.0%

1Q13

83

21.4%

2Q12

75

22.3%

Adjusted¹ EBITDA Margin

Adjusted¹ EBITDA

(R$ million)

119104

625749

14.7%

1H13

13.9%

1H12

15.2%

2Q13

13.3%

1Q13

14.7%

2Q12

14.5%

+25.8%

Adjusted¹ Net Income

(R$ million)

Adjusted¹ Net Income Adjusted¹ Net Margin

19

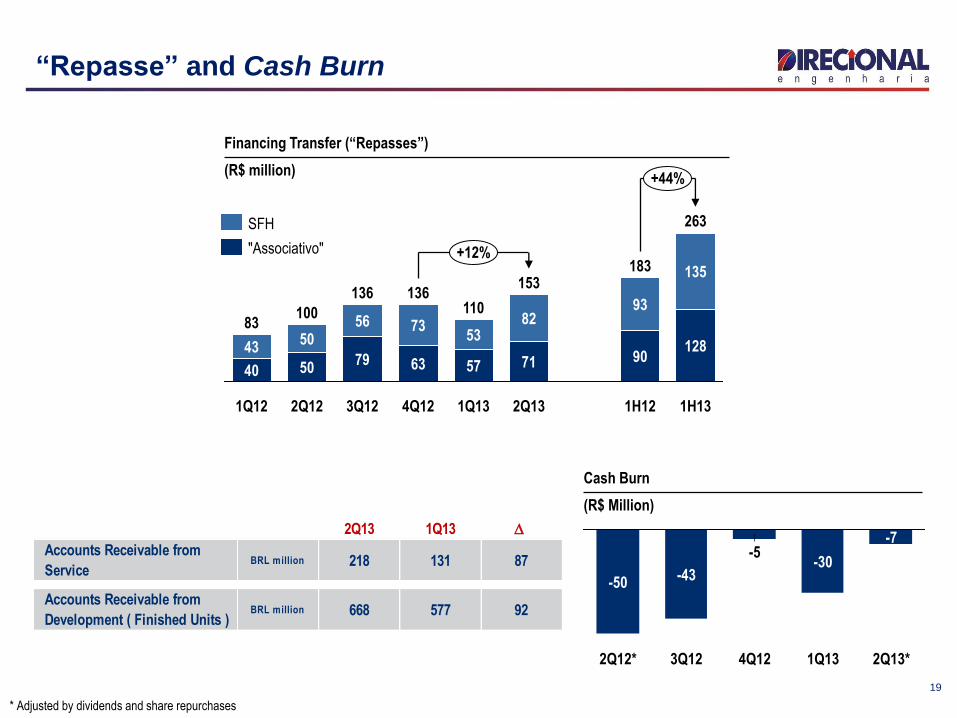

“Repasse” and Cash Burn

Financing Transfer (“Repasses”)

(R$ million)

57

53

4Q12

136

63

73

3Q12

136

79

56

2Q12

100

50

93

1Q12

83

40

43

2Q13

153

71

82

1Q13

110

+12%

+44%

1H13

263

128

135

1H12

183

90 50

"Associativo"

SFH

-7

2Q13* 1Q13

-30

4Q12

-5

3Q12

-43

2Q12*

-50

Cash Burn

(R$ Million)

* Adjusted by dividends and share repurchases

2Q13 1Q13 D

Accounts Receivable from

ServiceBRL million 218 131 87

Accounts Receivable from

Development ( Finished Units )BRL million 668 577 92

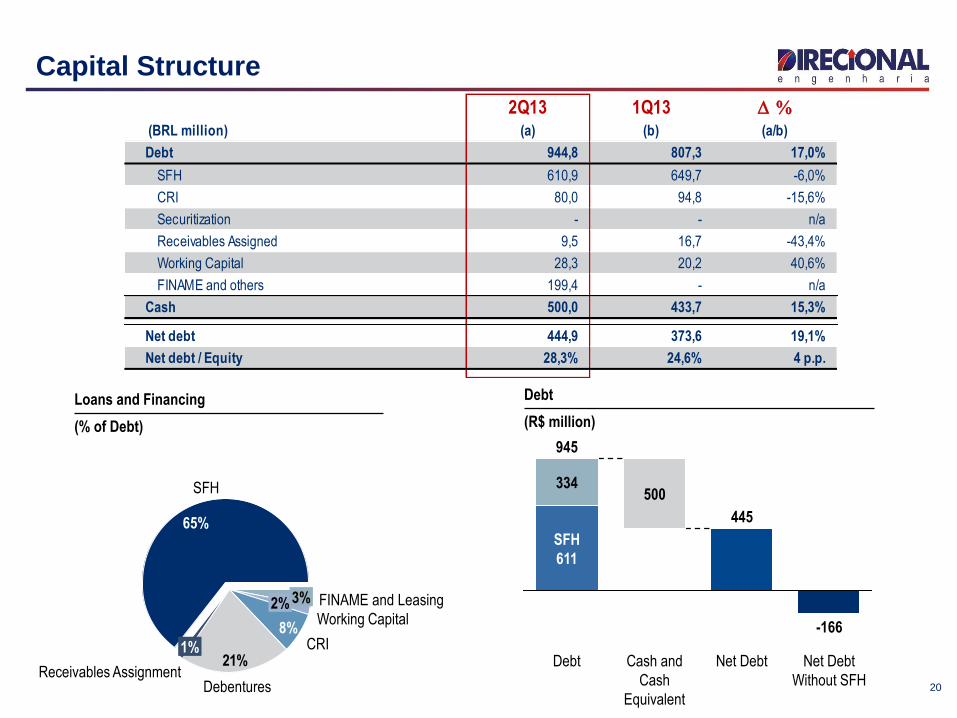

2Q13 1Q13 D %

(BRL million) (a) (b) (a/b)

Debt 944,8 807,3 17,0%

SFH 610,9 649,7 -6,0%

CRI 80,0 94,8 -15,6%

Securitization - - n/a

Receivables Assigned 9,5 16,7 -43,4%

Working Capital 28,3 20,2 40,6%

FINAME and others 199,4 - n/a

Cash 500,0 433,7 15,3%

Net debt 444,9 373,6 19,1%

Net debt / Equity 28,3% 24,6% 4 p.p.

20

Capital Structure

Net Debt

Without SFH

-166

Net Debt

445

Cash and

Cash

Equivalent

500

Debt

945

SFH

611

334

Debt

(R$ million)

21%Receivables Assignment

1%

Debentures

CRI 8%

Working Capital 2% FINAME and Leasing 3%

SFH

65%

Loans and Financing

(% of Debt)

21

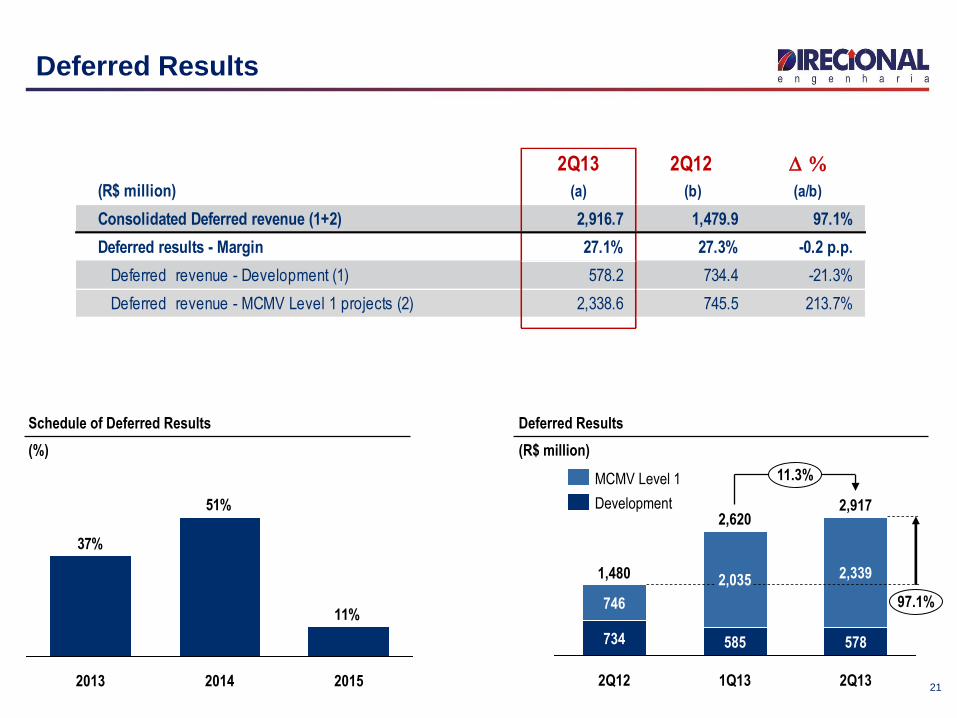

Deferred Results

Schedule of Deferred Results

(%)

11%

51%

37%

2013 2015 2014

Deferred Results

(R$ million)

2,917

97.1%

11.3%

2Q13

578

2,339

1Q13

2,620

585

2,035

2Q12

1,480

734

746

Development

MCMV Level 1

2Q13 2Q12 D %

(R$ million) (a) (b) (a/b)

Consolidated Deferred revenue (1+2) 2,916.7 1,479.9 97.1%

Deferred results - Margin 27.1% 27.3% -0.2 p.p.

Deferred revenue - Development (1) 578.2 734.4 -21.3%

Deferred revenue - MCMV Level 1 projects (2) 2,338.6 745.5 213.7%

22

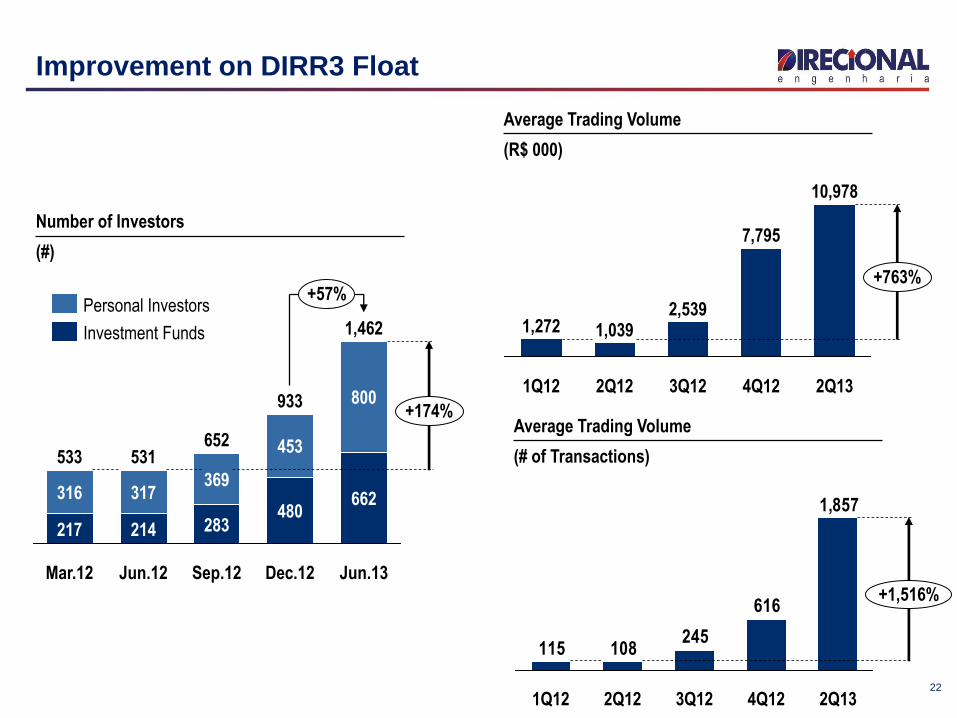

Improvement on DIRR3 Float

Number of Investors

(#)

+57%

1,462

+174%

Jun.13

662

800

Dec.12

933

480

453

Sep.12

652

283

369

Jun.12

531

214

317

Mar.12

533

217

316

Investment Funds

Personal Investors

10,978

+763%

2Q13 4Q12

7,795

3Q12

2,539

2Q12

1,039

1Q12

1,272

Average Trading Volume

(# of Transactions)

Average Trading Volume

(R$ 000)

1,857

616

245108115

+1,516%

2Q13 4Q12 3Q12 2Q12 1Q12

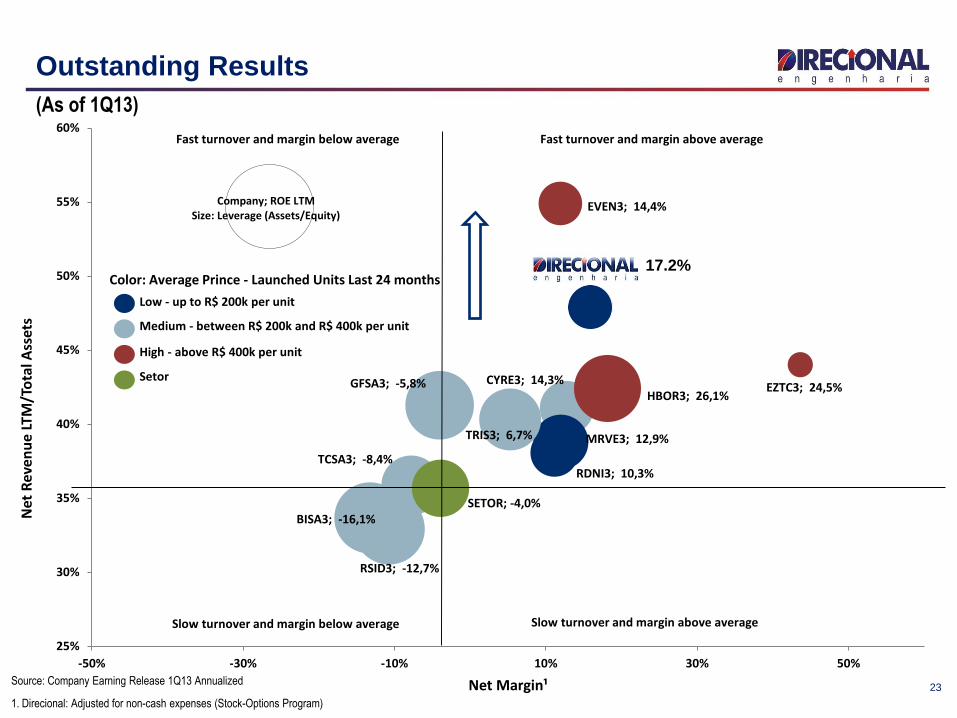

BISA3; -16,1%

CYRE3; 14,3%

EVEN3; 14,4%

EZTC3; 24,5%GFSA3; -5,8%HBOR3; 26,1%

MRVE3; 12,9%

DIRR3 17,2%

RDNI3; 10,3%

RSID3; -12,7%

TCSA3; -8,4%

SETOR; -4,0%

TRIS3; 6,7%

25%

30%

35%

40%

45%

50%

55%

60%

-50% -30% -10% 10% 30% 50%

Net

Re

ven

ue

LTM

/To

tal A

sset

s

Net Margin¹

Slow turnover and margin above averageSlow turnover and margin below average

Fast turnover and margin below average Fast turnover and margin above average

Company; ROE LTMSize: Leverage (Assets/Equity)

Color: Average Prince - Launched Units Last 24 months

Low - up to R$ 200k per unit

Medium - between R$ 200k and R$ 400k per unit

High - above R$ 400k per unit

Setor

1. Direcional: Adjusted for non-cash expenses (Stock-Options Program)

23

Outstanding Results

17.2%

Source: Company Earning Release 1Q13 Annualized

(As of 1Q13)

Appendix

24

25

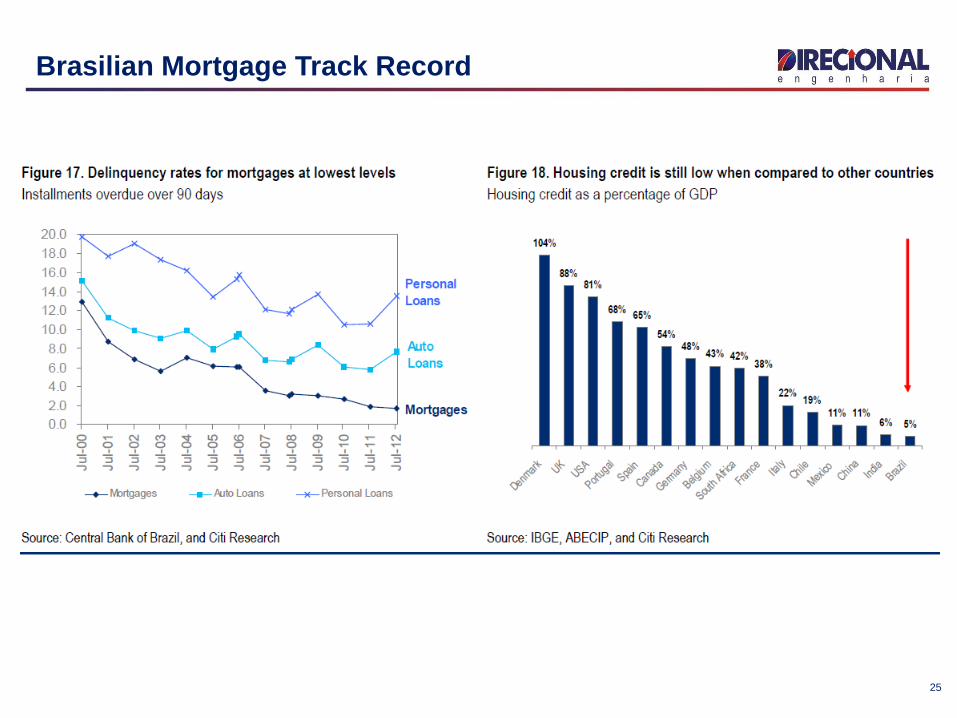

Brasilian Mortgage Track Record

26

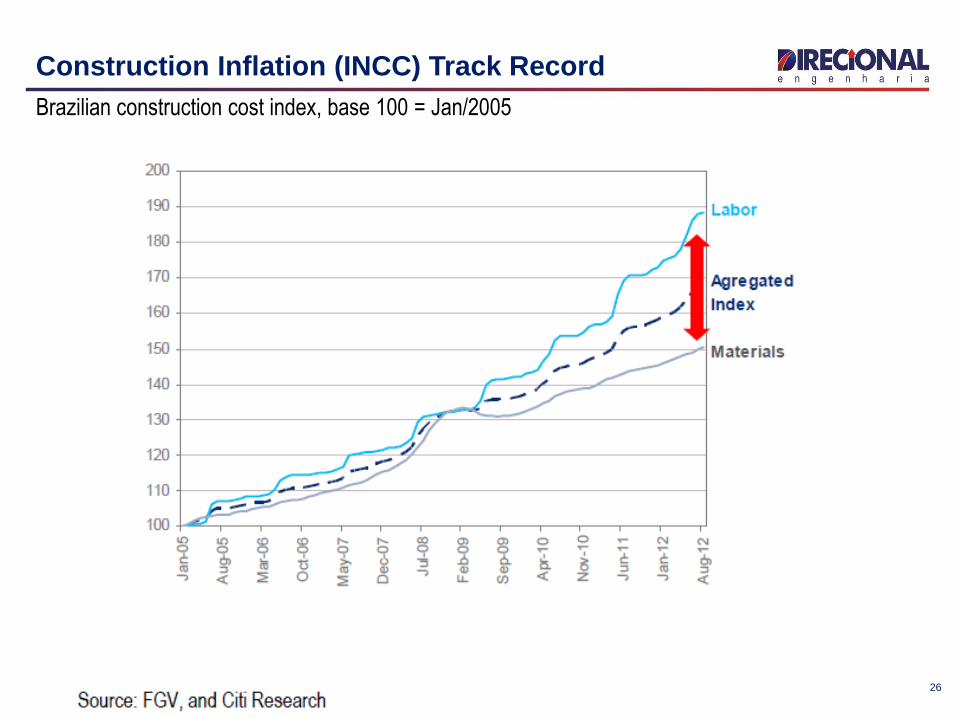

Construction Inflation (INCC) Track Record

Brazilian construction cost index, base 100 = Jan/2005

27

Contacts

Carlos Wollenweber CFO | IR Officer

Paulo Sousa IR Analyst

Luiz Felipe Almeida IR Analyst

www.direcional.com.b/ir

(55 31) 3214-6200

(55 31) 3214-6450