Embed Size (px)

DESCRIPTION

Citation preview

ASX ANNOUNCEMENT DATE 11 May 2007

REF NO. 070509

SUBJECT Presentation to USA Investors

Attached is a copy of the presentation Richard Selwood, Managing Director Natural Fuel Ltd, gave at the recent Jefferies Clean Tech Conference held in New York.

The presentation focused on

Natural Fuel’s business model and global strategy and it’s development of Singapore, Darwin and Houston operations

Revenues to be generated by each of the plants in a full year of operation

Management strategy being undertaken to deal with such issues as feedstock, technology and operations

For further details regarding Natural Fuel Ltd, please contact:

Richard Selwood Managing Director Natural Fuel Limited P: 08 9286 6788 E: [email protected]

Anna Candler Managing Director 6 Hats Investor Relations P:02 9908 8815 E: [email protected]

Australia’s largest biodiesel producerBuilding an integrated global biodiesel operation

RICHARD SELWOOD | MANAGING DIRECTOREARL McCONCHIE | CEO - AMERICAS JEFFRIES CLEAN TECH | 2 MAY 2007

PAGE 2

Introduction

Natural Fuel Australia’s largest biodiesel producer

Multiple revenue streams – biodiesel, glycerine, carbon credits

Focus on international growth

Business model replicates oil industry distribution

Pro-active risk management processes

International and local partners – construction, feedstock,

Strong cashflows from 2008

PAGE 3

Natural Fuel business model

Integration with Fuel Industry

Production capacity

Multiple Revenue Streams

Feedstock

Industrial-scale production located at oil refining and fuel industry hubsUse existing fuel terminal facilities and services

Staged development of plants to meet industry growthTargeting bottom of international cost curve – strong cost managementSupply chain flexibility – operations in feedstock logistics hubsIndustry leading alliances with international companies

Biodiesel Distribution strategy builds strong revenue baseGlycerine Pharmaceutical grade 10% of revenuesCo-products All have commercial valueCarbon Not yet added into revenue calculations

Direct relationships with plantation owners/companies Existing supply agreements with ConAgra Trade Group Exploring owning own cropsActive participation in sustainable feedstock industry initiatives

PAGE 4

First three facilities

US$14.7mUS$123.1mUS$6.9mNPAT **

US$30.8mUS$130.3mUS$15.5mEBITDA **

AU$188.9mUS$530.7mUS$108.3mAnnual Revenue **

20092008S2 2007 / S1 2008Pivotal Year*

Q4 2008Q4 2007Jan 2007Start-up Date

US$65mUS$110mUS$42mCapital Cost

200,000 mta600,000 mta122,500 mta Plant Capacity - Phase 1

HoustonSingaporeDarwin

* Pivotal year = first year of full production **Based on (long term) assumptions: Palm Olein: US$500 MT FOB; Soybean oil US$580 MT FOB; 0.78 AU$:US$

PAGE 5

Case for Darwin

PAGE 6

Case for Darwin

History

Investment Criteria

Capacity

Markets

50:50 Joint Venture Babcock & Brown Environmental Investments (BEI)

Capability to add additional plantsEasy access to local and regional feedstocksHigher margins for diesel fuel in Northern AustraliaAbility to integrate distribution into local diesel fuel infrastructure

Biodiesel 122,500 mtaGlycerine 12,250 mtaSite capacity for additional 200,000 mta

Domestic Northern Australia – higher margins – transport and farmSydney & NSW regions – largest market for diesel

PAGE 7

Feedstock

Partnerships

Next Steps

Primarily RBD Palm Olein supplemented with Soybean Oil100,000 mta (~80%) contracted through ConAgraDirect plantation supply under negotiation

Lurgi Transesterification & pharmaceutical glycerine technology

Vopak Regional fuel/diesel distribution terminal; In-line blending

Finalise equipment installation to meet feedstock variabilityQuality Assurance & Environmental Assurance certificationOptimisation of plant’s operationsAchieve typical operating capacity (> 20% above nameplate)

Case for Darwin

PAGE 8

Case for Singapore

PAGE 9

Case for Singapore

History

Investment Criteria

Capacity

Markets

Construction began February 2007

Hub for US and European fuel marketsPlant expansion capability & fully serviced Good access to regional feedstock suppliesHigh financial returns; Pioneer Status = tax honeymoon 10+ years

Biodiesel Initially 600,000 mta; to be commissioned late 2007Glycerine Initially 60,000 mtaPhase 2 900,000 mtaPhase 3 900,000 mta

Primary USA West Coast;Secondary Northern Asia; China

Mining companies – Northern Australia

PAGE 10

Feedstock

Partnerships

Next Steps

Primarily RBD Palm Olein supplemented with Soybean Oil300,000 mta (~50%) already contracted - ConAgraDirect plantation supply under negotiation

Lurgi Transesterification & pharmaceutical glycerine technology

Vopak Regional fuel/diesel distribution terminal; In-line blending

Apply technology lessons learnt to construction and plant managementStaggered commissioning of the 3 x 200,000 plants during Q4 2007Quality Assurance and Environmental Assurance certification

Case for Singapore

PAGE 11

Case for Houston

Stolthaven Terminal

Natural Fuel site

Houston Shipping Channel

PAGE 12

Case for Houston

History

Investment Criteria

Capacity

Markets

Houston first site considered for NFLBoard approval to proceed April 2007

Integration into fuel industry infrastructurePlant expansion capability & fully serviced Good access to regional feedstock suppliesTexas government investment grant US$3m per yearCrude feedstock processing capability

Biodiesel Initially 200,000 mta – to be commissioned late 2008Glycerine 20,000 mtaPhase 2 300,000mtaPhase 3 300,000mta

Domestic Gulf Coast; Mid-West; East Coast fuel industry zonesExport Flexibility as required

PAGE 13

Feedstock Supply

Partners

Next Steps

Crude soybean oilReviewing market ConAgra to supply 200,000 mta

Connemann-ADM & Cimbria SketTransesterification & pharmaceutical glycerine

Stolthaven Terminal servicesStolt-Nielsen Logistic services

Finalise project financeFinalise appointment of contractor Apply lessons from Darwin & Singapore to engineering and construction

Case for Houston

PAGE 14

Risk Management

Biodiesel / Glycerine

Feedstock

Operations

Financial

Volume low contracts; market growthPrice medium market pricing; use of hedgingDistribution low relationships with oil majors;

independent distribution availableSupply low managed by contractsPrice medium blend of market pricing and direct

plantation supplies; use of hedgingTechnology low proven technologiesOperating low sector expertise; aligned resourcesEnvironment low operational policies & risk

mitigation policies/proceduresBusiness low demand exceeds supply

tax and government incentivesModel low oil industry distribution model

PAGE 15

Renewable fuel : way of the future

International multi-plant strategy

Scaleable business model : replicates oil industry model

Multiple revenue streams

Biodiesel plants have strong cash flow and deliver robust

financial returns

Natural Fuel

Australia’s largest biodiesel producerBuilding an integrated global biodiesel operation

PAGE 17

Appendices

PAGE 18

Glossary of Terms

AU$

US$

MT

mta

gallons

Australian dollars

US dollars

Metric tonnes1,132 litres300 gallons

Metric tonnes per annum

3.78 litres

PAGE 19

Biodiesel Industry Drivers

Legislation

Environment

Energy Security

Agriculture

USA – Biofuels Blenders’ Incentives legislative permanency anticipatedAustralia – Stable Clean Fuels Grant basis until 2016Europe – Increasing EU mandates and Member state mandatesAsia – Increasing standardisation of biofuel fuel blends, and prospective

mandates

Commercially viableEssential to reduce greenhouse gasesClean burning and cost effective

Reduce reliance on imported crude oilExtend crude oil reservesUS biodiesel industry reduces by 20% demand for crude oil by 2017

Provides new market for sale of grainsDependable revenue via forward purchase contractsRural development via job creation

PAGE 20

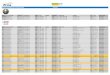

Summary Company Data

1.5 m$0.50

50.4 m$0.33Options(Exp 30/06/08)

62.8%Top 20 shareholders

3 million shares / monthAverage turnover

$0.755Low

$1.480High

12 month trading history

AU$ 270.2 mAU$ 130.0 mMarket capitalisation

337.8 m162.5 mNumber of shares

Fully dilutedUndilutedAs at 30 April 2008

26 April 2012Convert

$1.32Conversion price

8,000Number

Converting Bonds(Lead Broker: Jeffries International)