Embed Size (px)

Citation preview

AGRICULTURAL BANK OF CHINA LIMITED

中 國 農 業 銀 行 股 份 有 限 公 司

(a joint stock company incorporated in the People’s Republic of China with limited liability)

(Stock Code: 1288)

2017 CAPITAL ADEQUACY RATIO REPORT

Contents

1 Overview......................................................................................................................................1

1.1 Profile................................................................................................................................1

1.2 Capital Adequacy Ratio.................................................................................................... 1

1.3 Disclosure Statement........................................................................................................ 3

2 Risk Management Framework.....................................................................................................5

2.1 Firm-wide Risk Management........................................................................................... 5

2.2 Risk Appetite.................................................................................................................... 6

2.3 Structure and Organization of Risk Management.............................................................6

2.4 Risk Management Policies and Systems.......................................................................... 8

2.5 Risk Management Tools and IT Systems......................................................................... 9

3 Information on Composition of Capital.....................................................................................12

3.1 Scope for Calculating Capital Adequacy Ratio.............................................................. 12

3.2 Regulatory Capital Shortfall of Investees.......................................................................14

3.3 Restrictions on Intra-group Capital Transfers.................................................................14

3.4 Contrast between Regulatory Consolidation and Financial Statement...........................14

3.5 Composition of Capital...................................................................................................16

3.6 Main Features of Eligible Capital Instruments............................................................... 22

3.7 Threshold Deductions Limit and Limit of Excess Loan Loss Provisions...................... 32

3.8 Changes in Paid-in Capital............................................................................................. 34

3.9 Significant Capital Investments...................................................................................... 34

4 Credit Risk................................................................................................................................. 35

4.1 Credit Risk Management................................................................................................ 35

4.2 Credit Risk Exposure...................................................................................................... 36

4.3 Internal Ratings-Based Approach...................................................................................38

4.4 Credit Risk Exposure Uncovered under Internal Ratings-Based....................................41

4.5 Credit Risk Mitigation.................................................................................................... 43

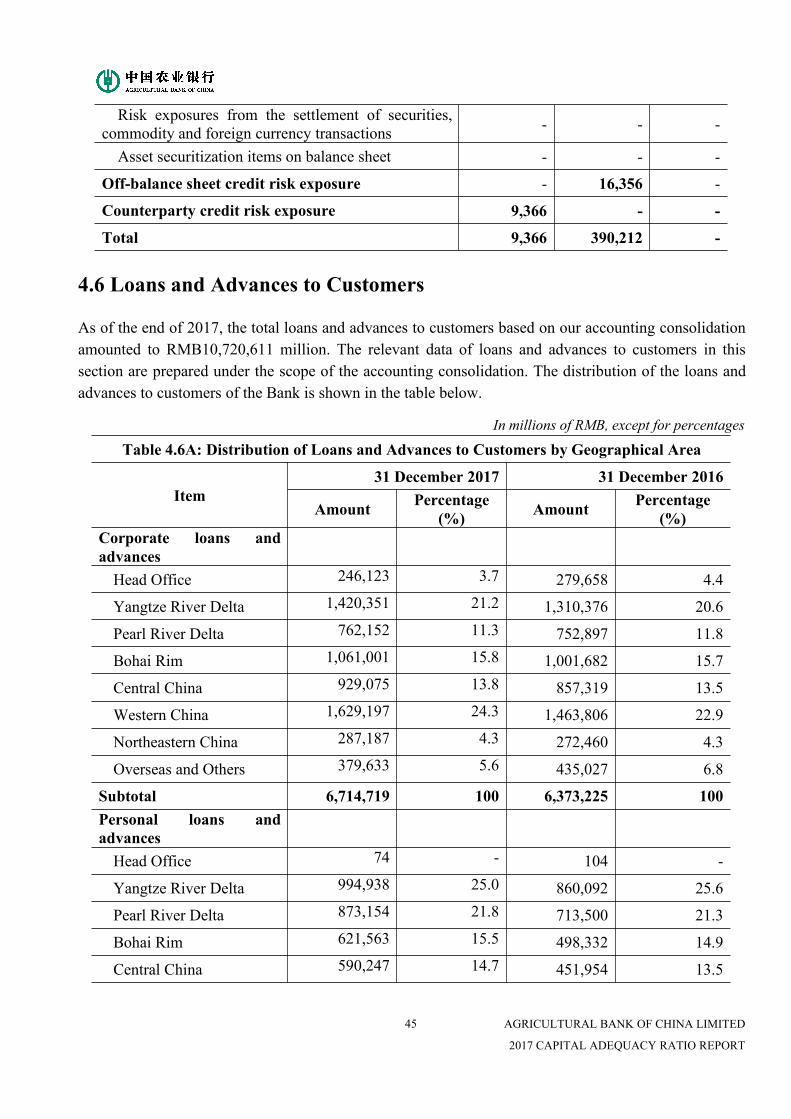

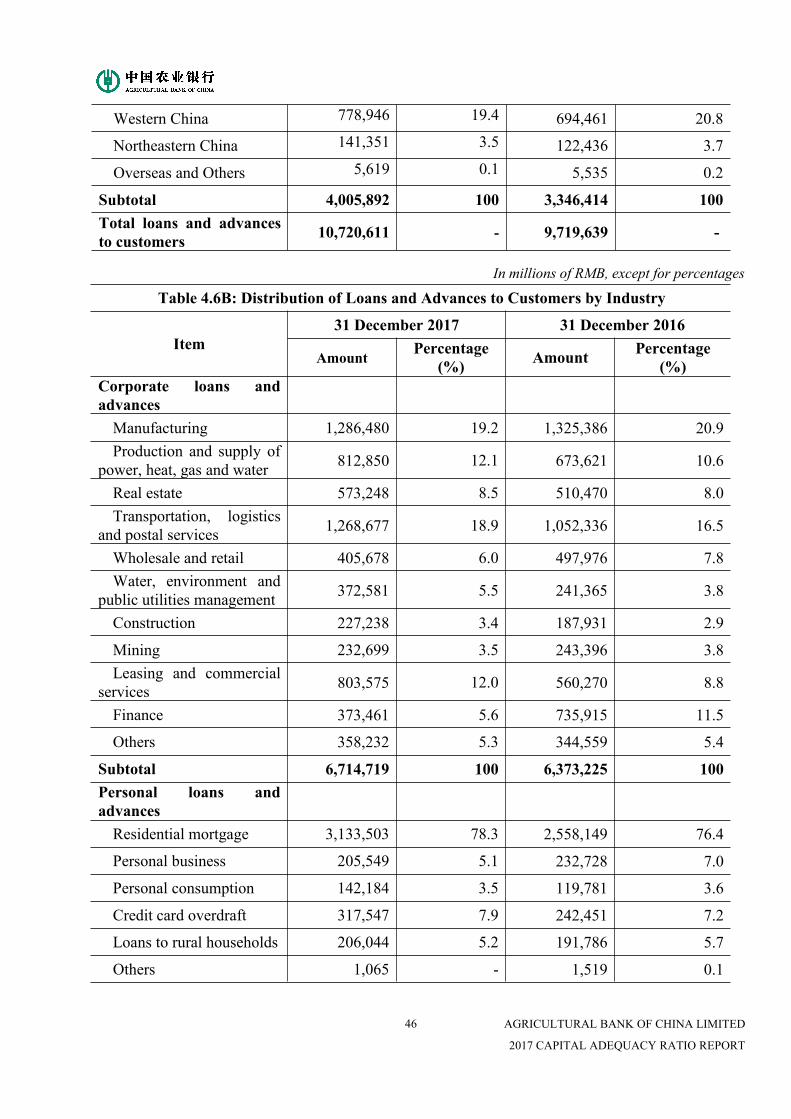

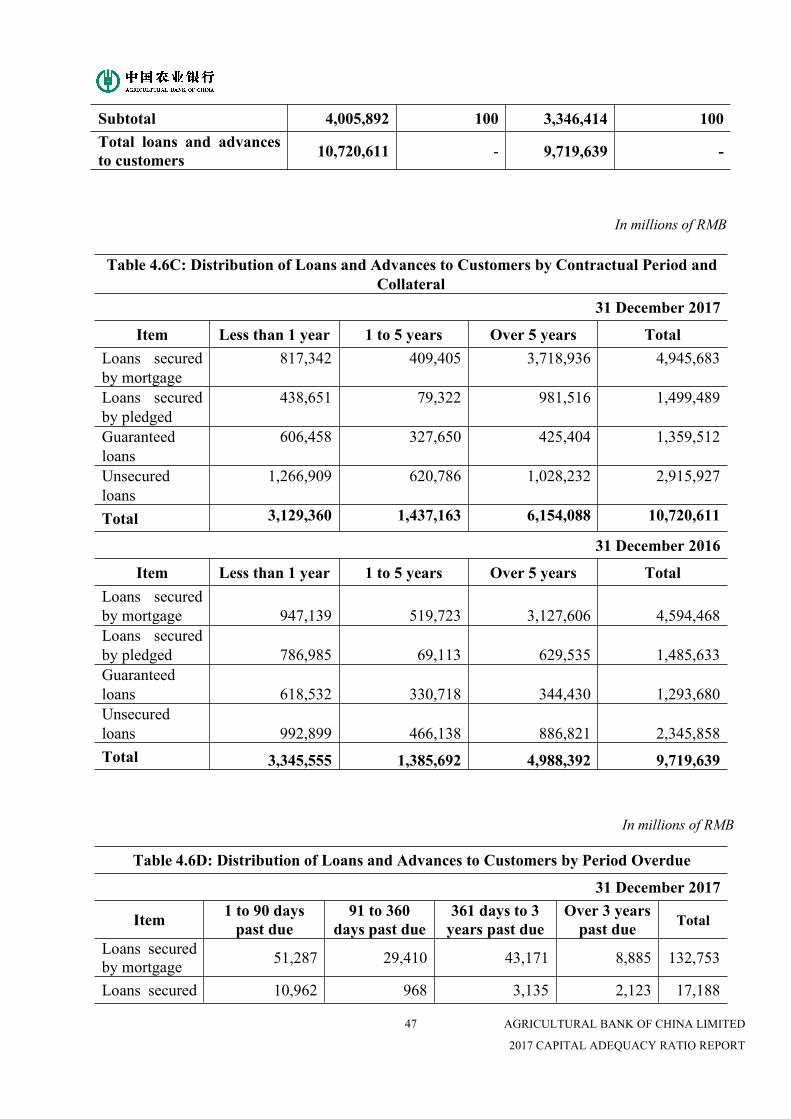

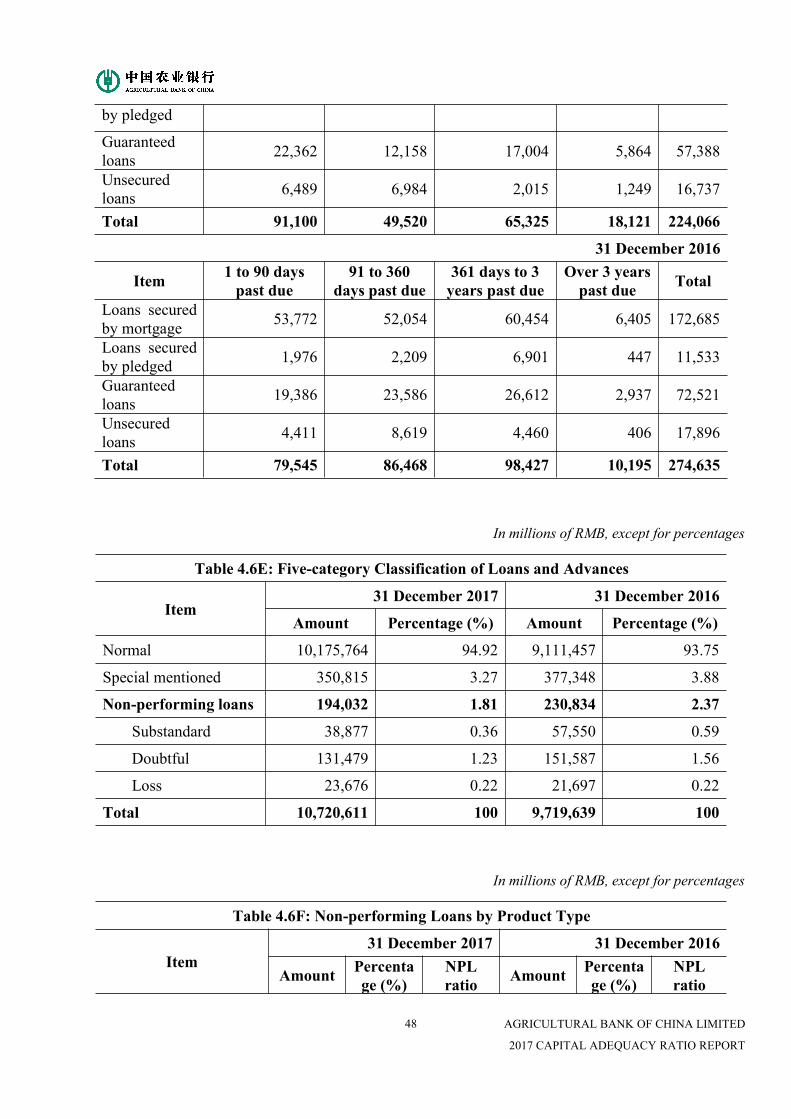

4.6 Loans and Advances to Customers.................................................................................45

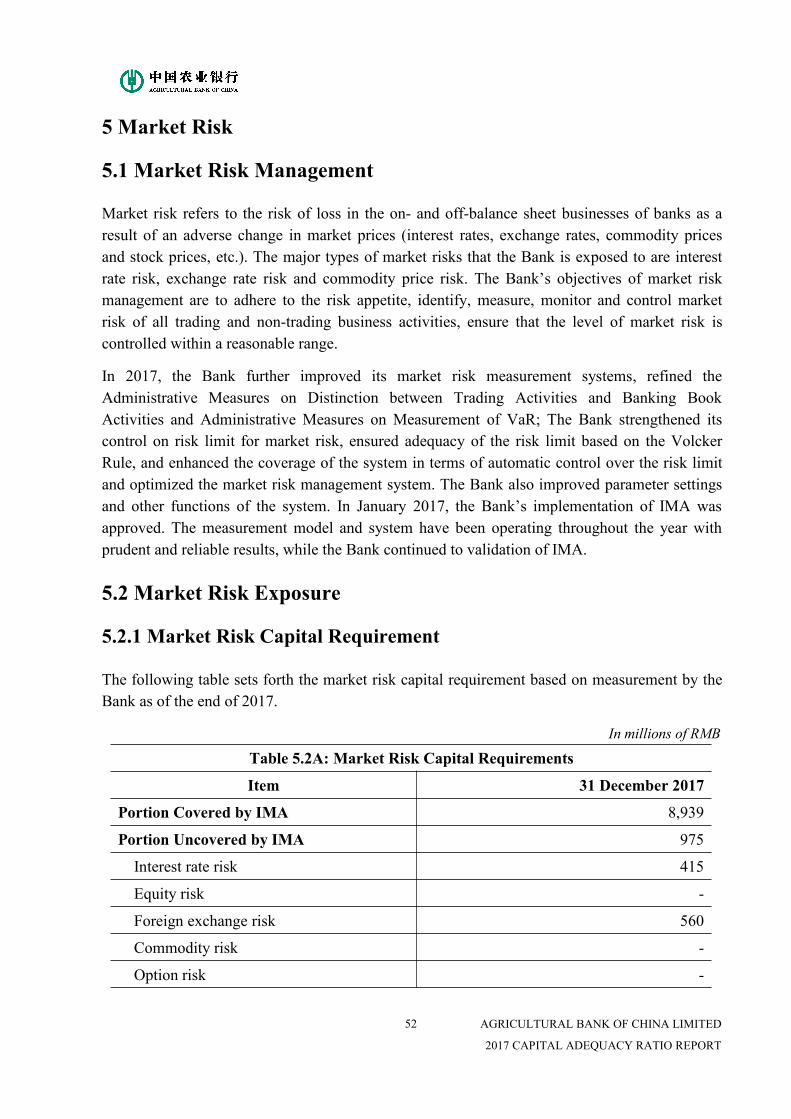

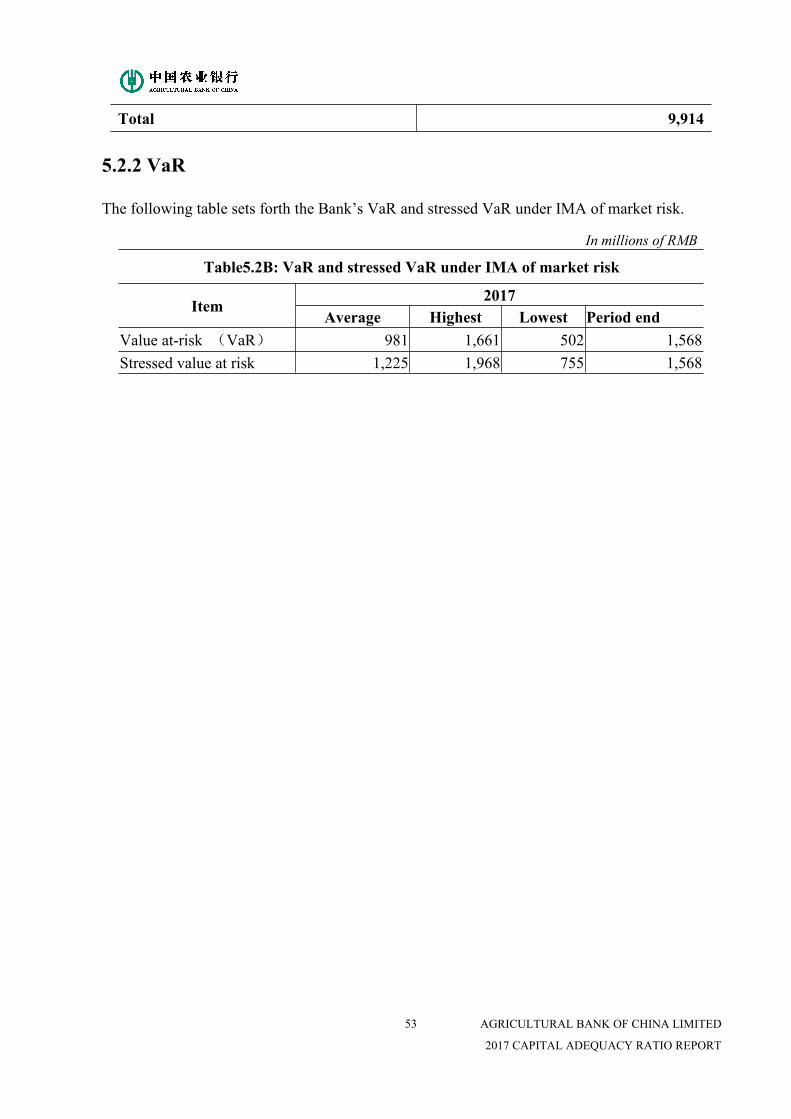

5 Market Risk................................................................................................................................52

5.1 Market Risk Management...............................................................................................52

5.2 Market Risk Exposure.................................................................................................... 52

6 Operational Risk........................................................................................................................ 54

6.1 Operational Risk Management....................................................................................... 54

6.2 Operational Risk Exposure............................................................................................. 54

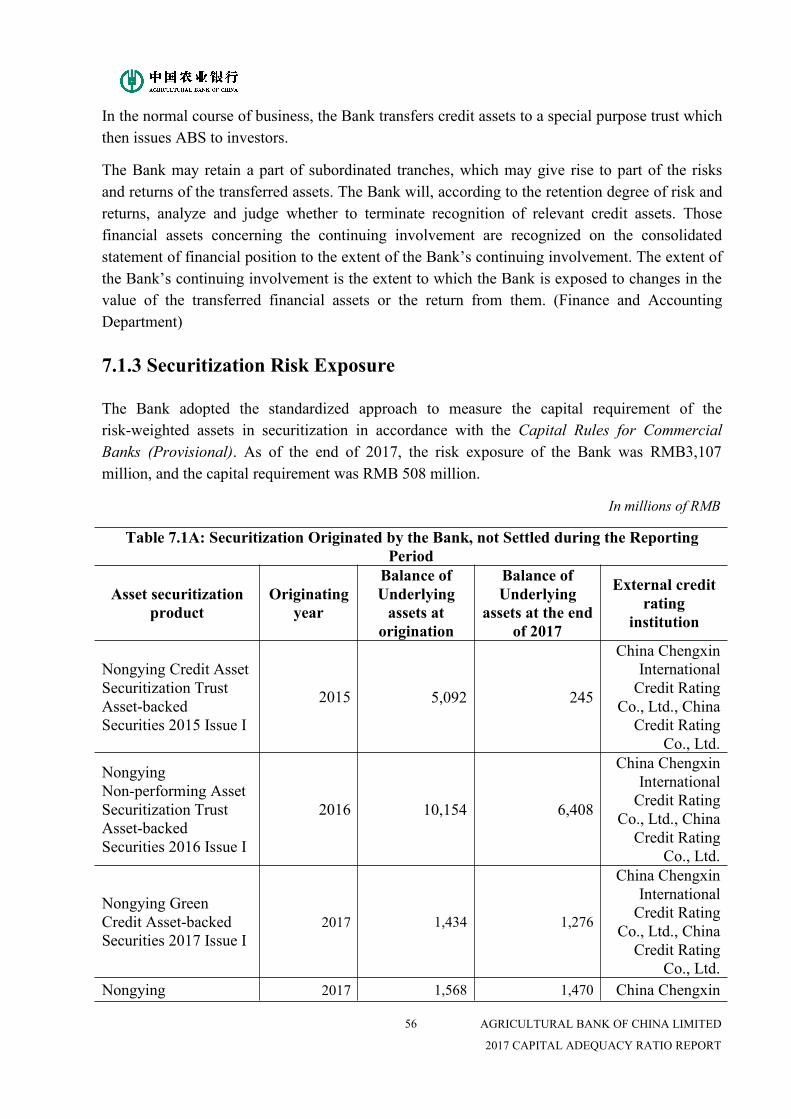

7 Other Risks................................................................................................................................ 55

7.1 Securitization Risk..........................................................................................................55

7.2 Counterparty Credit Risk................................................................................................ 59

7.3 Equity Risk of Banking Book.........................................................................................59

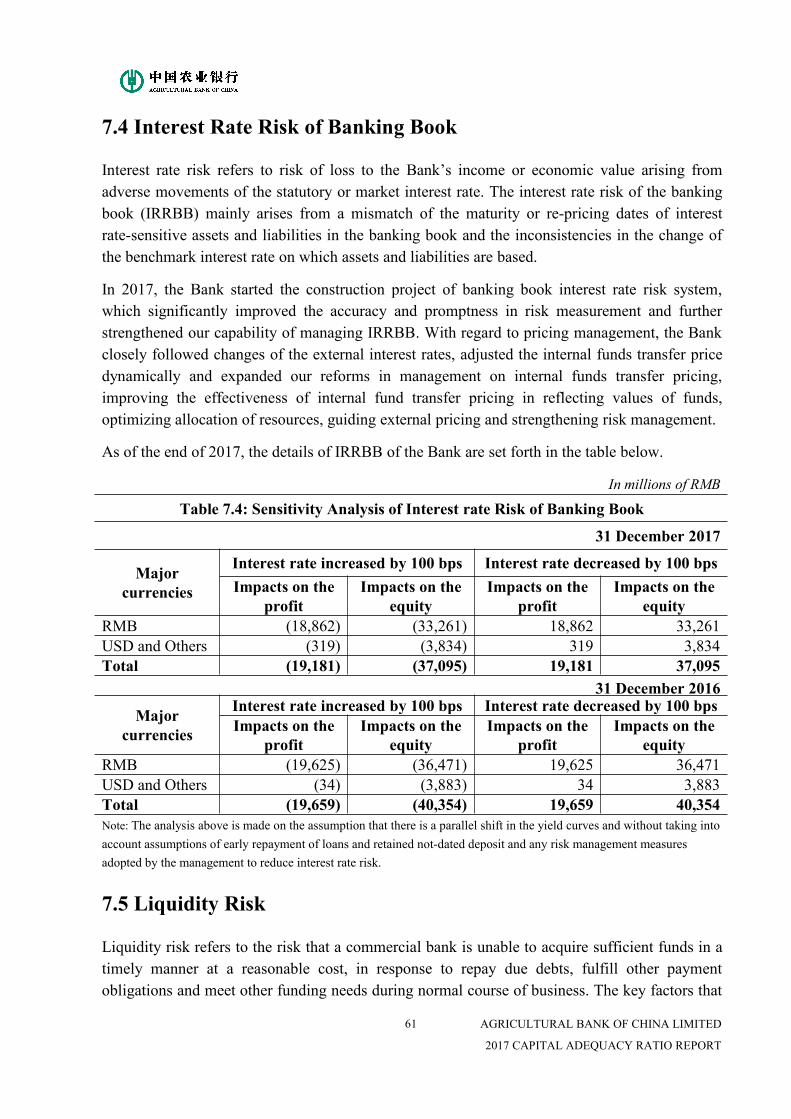

7.4 Interest Rate Risk of Banking Book............................................................................... 61

7.5 Liquidity Risk................................................................................................................. 61

8 Internal Capital Adequacy Assessment..................................................................................... 64

8.1 Internal Capital Adequacy Assessment Methods and Process....................................... 64

8.2 Capital Planning and Capital Adequacy Ratio Management Plan..................................64

9 Remuneration.............................................................................................................................65

9.1Nomination and Remuneration Committee of the Board of Directors............................65

9.2Remuneration Policy........................................................................................................65

10 Outlook.................................................................................................................................... 67

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

1

1 Overview

1.1 Profile

The predecessor of the Bank was Agricultural Cooperative Bank established in 1951. Since the late1970s, the Bank has evolved from a state-owned specialized bank to a wholly state-owned commercialbank and subsequently a state-controlled commercial bank. The Bank was restructured into a joint stocklimited liability company in January 2009. In July 2010, the Bank was listed on the Shanghai StockExchange and the Hong Kong Stock Exchange.

As one of the major integrated financial service providers in China, the Bank is committed to buildingan international first-class commercial banking group with featured operations, efficient and convenientservices, diversified functions, as well as demonstrated value-creation capability. Capitalizing on itscomprehensive business portfolio, extensive distribution network and advanced IT platform, the Bankprovides a diverse portfolio of corporate and retail banking products and services for a broad range ofcustomers, and conducts treasury operations and asset management. Our business scope also includes,among other things, investment banking, fund management, financial leasing and life insurance. At theend of 2017, the Bank had total assets of RMB 21,053,382 million, loans and advances to customers ofRMB 10,720,611 million and deposits from customers of RMB 16,194,279 million. Our capitaladequacy ratio was 13.74%. The Bank achieved a net profit of RMB 193,133 million in 2017.

The Bank had a total of 23,661 domestic branch outlets at the end of 2017, including the Head Office,the Business Department of the Head Office, three specialized business units managed by the HeadOffice, three Training Institutes, 37 tier-1 branches (including 5 branches directly managed by the HeadOffice), 378 tier-2 branches (including business departments of branches in provinces), 3,485 tier-1sub-branches (including business departments in municipalities, business departments of branchesdirectly managed by the Head Office and business departments of tier-2 branches), 19,701 branchoutlets, and 52 other establishments. Our overseas branch outlets consisted of 13 overseas branches and4 overseas representative offices. The Bank had 15 major subsidiaries, including 10 domesticsubsidiaries and 5 overseas subsidiaries.

The Financial Stability Board has included the Bank into the list of Global Systemically ImportantBanks for four consecutive years since 2014. In 2017, the Bank ranked No. 38 in Fortune’s Global 500,and ranked No. 6 in The Banker’s “Top 1000 World Banks” list in terms of tier 1 capital. The Bank’sissuer credit ratings assigned by Standard & Poor’s were A/A-1, and the long-/short-term issuer defaultratings assigned by Fitch Ratings were A/F1.

1.2 Capital Adequacy Ratio

In 2014, the China Banking Regulatory Commission (hereinafter referred to as the “CBRC”) approvedthe Bank’s use of foundation Internal Ratings-Based (IRB) approach for non-retail exposures, IRBapproach for retail exposures and standardized approach for operational risk on bank and group levels.

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

2

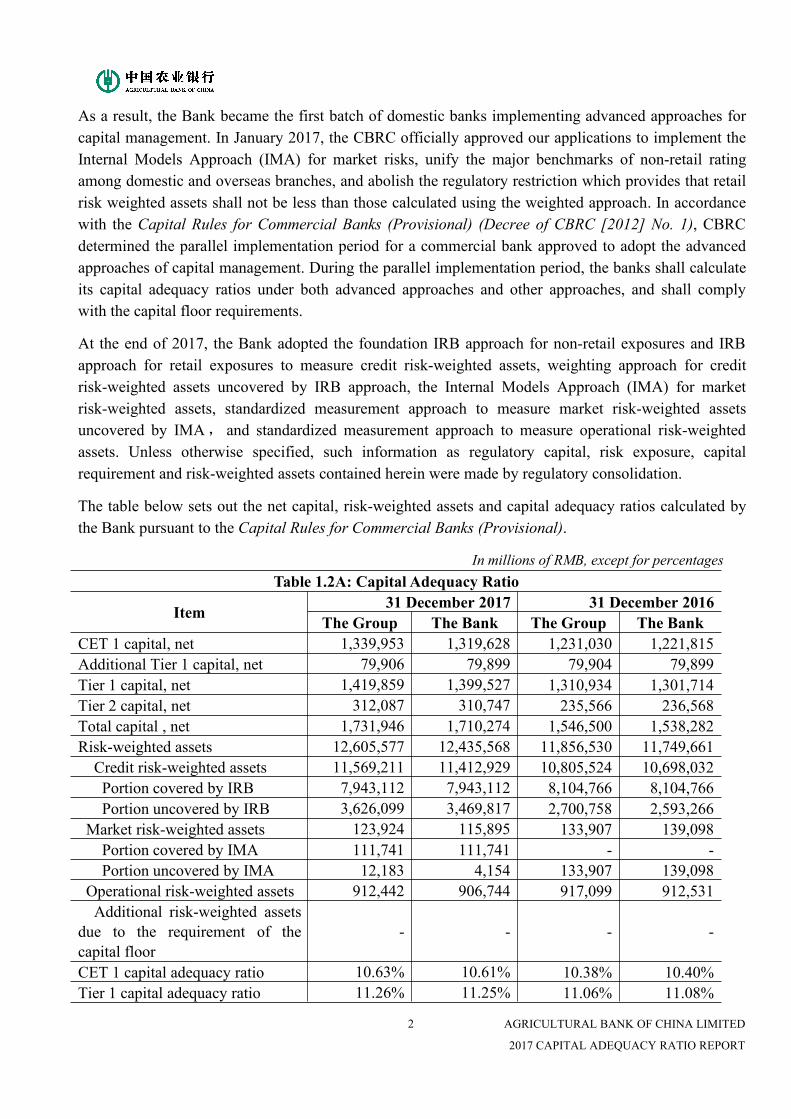

As a result, the Bank became the first batch of domestic banks implementing advanced approaches forcapital management. In January 2017, the CBRC officially approved our applications to implement theInternal Models Approach (IMA) for market risks, unify the major benchmarks of non-retail ratingamong domestic and overseas branches, and abolish the regulatory restriction which provides that retailrisk weighted assets shall not be less than those calculated using the weighted approach. In accordancewith the Capital Rules for Commercial Banks (Provisional) (Decree of CBRC [2012] No. 1), CBRCdetermined the parallel implementation period for a commercial bank approved to adopt the advancedapproaches of capital management. During the parallel implementation period, the banks shall calculateits capital adequacy ratios under both advanced approaches and other approaches, and shall complywith the capital floor requirements.

At the end of 2017, the Bank adopted the foundation IRB approach for non-retail exposures and IRBapproach for retail exposures to measure credit risk-weighted assets, weighting approach for creditrisk-weighted assets uncovered by IRB approach, the Internal Models Approach (IMA) for marketrisk-weighted assets, standardized measurement approach to measure market risk-weighted assetsuncovered by IMA, and standardized measurement approach to measure operational risk-weightedassets. Unless otherwise specified, such information as regulatory capital, risk exposure, capitalrequirement and risk-weighted assets contained herein were made by regulatory consolidation.

The table below sets out the net capital, risk-weighted assets and capital adequacy ratios calculated bythe Bank pursuant to the Capital Rules for Commercial Banks (Provisional).

In millions of RMB, except for percentagesTable 1.2A: Capital Adequacy Ratio

Item 31 December 2017 31 December 2016The Group The Bank The Group The Bank

CET 1 capital, net 1,339,953 1,319,628 1,231,030 1,221,815Additional Tier 1 capital, net 79,906 79,899 79,904 79,899Tier 1 capital, net 1,419,859 1,399,527 1,310,934 1,301,714Tier 2 capital, net 312,087 310,747 235,566 236,568Total capital , net 1,731,946 1,710,274 1,546,500 1,538,282Risk-weighted assets 12,605,577 12,435,568 11,856,530 11,749,661Credit risk-weighted assets 11,569,211 11,412,929 10,805,524 10,698,032Portion covered by IRB 7,943,112 7,943,112 8,104,766 8,104,766Portion uncovered by IRB 3,626,099 3,469,817 2,700,758 2,593,266

Market risk-weighted assets 123,924 115,895 133,907 139,098Portion covered by IMA 111,741 111,741 - -Portion uncovered by IMA 12,183 4,154 133,907 139,098

Operational risk-weighted assets 912,442 906,744 917,099 912,531Additional risk-weighted assets

due to the requirement of thecapital floor

- - - -

CET 1 capital adequacy ratio 10.63% 10.61% 10.38% 10.40%Tier 1 capital adequacy ratio 11.26% 11.25% 11.06% 11.08%

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

3

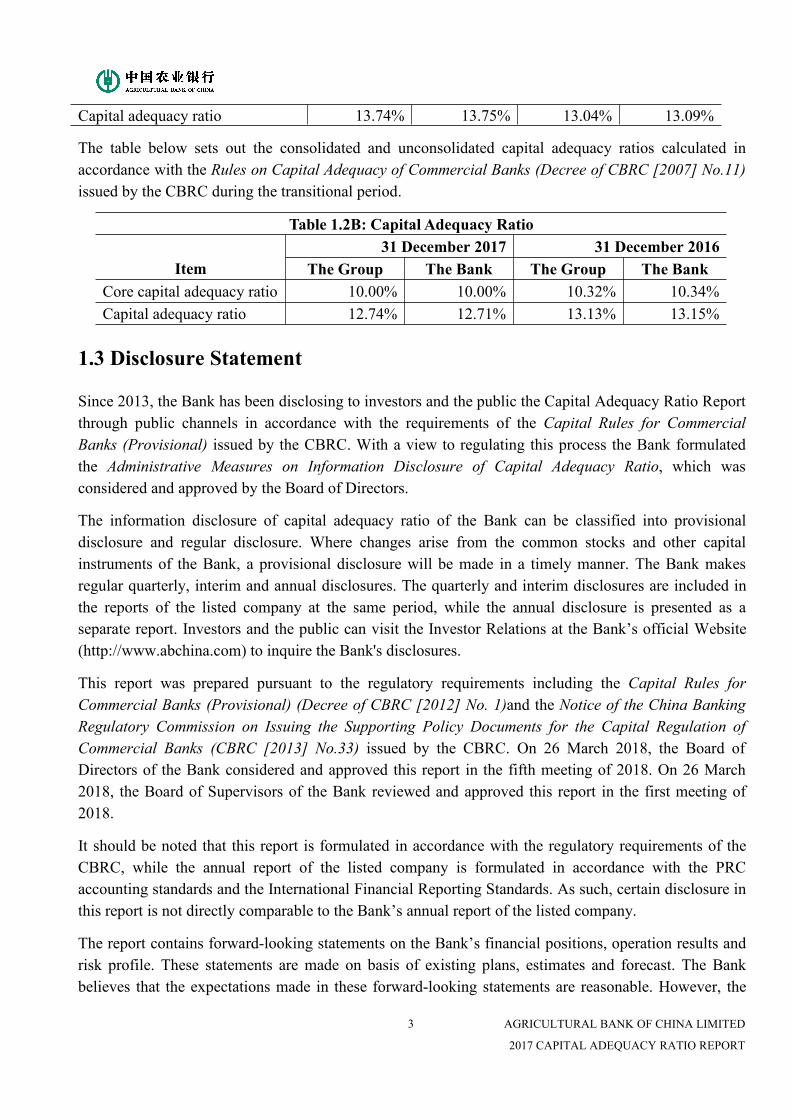

Capital adequacy ratio 13.74% 13.75% 13.04% 13.09%

The table below sets out the consolidated and unconsolidated capital adequacy ratios calculated inaccordance with the Rules on Capital Adequacy of Commercial Banks (Decree of CBRC [2007] No.11)issued by the CBRC during the transitional period.

Table 1.2B: Capital Adequacy Ratio

Item31 December 2017 31 December 2016

The Group The Bank The Group The BankCore capital adequacy ratio 10.00% 10.00% 10.32% 10.34%Capital adequacy ratio 12.74% 12.71% 13.13% 13.15%

1.3 Disclosure Statement

Since 2013, the Bank has been disclosing to investors and the public the Capital Adequacy Ratio Reportthrough public channels in accordance with the requirements of the Capital Rules for CommercialBanks (Provisional) issued by the CBRC. With a view to regulating this process the Bank formulatedthe Administrative Measures on Information Disclosure of Capital Adequacy Ratio, which wasconsidered and approved by the Board of Directors.

The information disclosure of capital adequacy ratio of the Bank can be classified into provisionaldisclosure and regular disclosure. Where changes arise from the common stocks and other capitalinstruments of the Bank, a provisional disclosure will be made in a timely manner. The Bank makesregular quarterly, interim and annual disclosures. The quarterly and interim disclosures are included inthe reports of the listed company at the same period, while the annual disclosure is presented as aseparate report. Investors and the public can visit the Investor Relations at the Bank’s official Website(http://www.abchina.com) to inquire the Bank's disclosures.

This report was prepared pursuant to the regulatory requirements including the Capital Rules forCommercial Banks (Provisional) (Decree of CBRC [2012] No. 1)and the Notice of the China BankingRegulatory Commission on Issuing the Supporting Policy Documents for the Capital Regulation ofCommercial Banks (CBRC [2013] No.33) issued by the CBRC. On 26 March 2018, the Board ofDirectors of the Bank considered and approved this report in the fifth meeting of 2018. On 26 March2018, the Board of Supervisors of the Bank reviewed and approved this report in the first meeting of2018.

It should be noted that this report is formulated in accordance with the regulatory requirements of theCBRC, while the annual report of the listed company is formulated in accordance with the PRCaccounting standards and the International Financial Reporting Standards. As such, certain disclosure inthis report is not directly comparable to the Bank’s annual report of the listed company.

The report contains forward-looking statements on the Bank’s financial positions, operation results andrisk profile. These statements are made on basis of existing plans, estimates and forecast. The Bankbelieves that the expectations made in these forward-looking statements are reasonable. However, the

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

4

Bank considers that the actual operation condition is related to the future external events, internalfinance, progress of business development, risk occurrence conditions or other performance, therefore,investors shall not heavily rely on these statements.

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

5

2 Risk Management Framework

2.1 Firm-wide Risk Management

Firm-wide risk management refers to the timely identification, measurement, monitoring, reporting andcontrol of risks in all aspects of business operations, processes and staff through the integration ofelements of risk management including risk appetite, policies, organizations, tools and models, ITsystems and risk culture, so as to ensure effective risk management in decision making, implementationand supervision.

In 2017, in response to the complicated and ever-changing domestic and international circumstance ofrisk management and control, the Bank kept pushing forward the establishment of firm-wide riskmanagement system. Under the general requirement of emphasizing the importance of preventing andcontrolling risks and fighting against the risks, the bank stuck to the risk bottom line by keeping theprincipal line of preventing new risks and reducing existing risks. The Bank optimized theresponsibility and duty of risk management departments, perfected the risk management accountabilityand performance assessment mechanism fulfilled the daily management of risks in a solid manner,strengthened the efforts to mitigate risk in key areas, maintained improvement in asset quality. TheBank continuously enhanced the market risk management in bond investment, asset management andfinancial services with banks and other financial institutions, and deepened case prevention and controland operational risk management. The Bank further enhanced the risk assessment system at bothhorizontal and vertical levels, with standards for risk assessment and evaluation improved. Thus theeffectiveness of risk management of the Bank was further improved.

In January 2017, the CBRC officially approved our applications to implement the Internal ModelsApproach (IMA) for market risks, unify the major benchmarks of non-retail rating among domestic andoverseas branches, and abolish the regulatory restriction which provides that retail risk weighted assetsshall not be less than those calculated using the weighted approach, so the implementation andapplication of the advanced approach of capital management were furtherly reinforced. In 2017, wecontinued to advance the unification and management of the non-retail Internal Rating Systems (IRS)among domestic and overseas branches, and optimized the non-retail customer rating system. Wecarried out early warning and identification of fraud risks in respect of retail loans based on big data.We reinforced the application of IMA for market risk to improve data quality and increase monitoringcoverage of exposure limit system. We deepened the internal application of advanced approaches foroperational risk to improve the measurement of case and anti-money laundering risks.

In 2017, the Risk Management Committee under the Board of Directors of the Bank held 5 meetingswhich discussed and considered various motions and reports, including the risk appetite statement,administrative measures on consolidated risk management, comprehensive risk management report,liquidity risk management report, analysis of implementation of advanced approaches of IRS Operationand capital management and consumer interests protection report. In 2017, the Risk ManagementCommittee under the Bank’s senior management held 6 meetings which discussed and considered

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

6

various motions and reports, including self-assessment report on the Bank’s comprehensive riskmanagement system, administrative measures on limit management of industry-specific exposures,administrative measures on risk management on subsidiaries, administrative measures on riskmanagement of overseas branches and subsidiary banks, the working rules of the Risk ManagementCommittee under the senior management and the IT risk assessment report at the Bank’s level.

2.2 Risk Appetite

Risk appetite is a term that refers to the types and levels of risks acceptable to the Bank as determinedby the Board of Directors of the Bank, which depends on the expectations and constraints of the Bank’smajor stakeholders, external operating environment and the conditions of the Bank, in order to achievestrategic targets and effective risk management. In 2017, the Risk Appetite Statement of the Bank wasrevised by the Bank and was considered and approved for implementation. Based on comprehensiveconsideration at the Group level, the revised Risk Appetite Statement covers all non-bank financialsubsidiaries and overseas branches and subsidiaries. In addition, new types of risk such as IT risk andmoney laundering risk are included, quantitative risk measurement are refined, and the transmissionmechanism for risk appetite is improved, which help provide further guidelines for risk managementand operation management. Meanwhile, we further improved the management system of risk appetiteby monitoring the implementation of risk appetite measurement on a monthly basis. We conduct annualreview of the risk appetite measurement to improve the quantitative and qualitative risk measurementand statement.

The Bank adhered to the comprehensive policy relating to risk appetite which is: The Bank is devotedto developing itself into a first-class global commercial banking group, maintaining its prudent riskappetite, operating in compliance with laws and regulations and trying to keep balance between capital,risks and revenue while taking into consideration of the security, profitability and liquidity. The Bankopposed over-aggressive or over-conservative attitude in undertaking risks, received the moderatereturns through undertaking proper risks, and maintained an adequate reserve and capital adequacy. TheBank will promote comprehensive development of its ability of risk management to meet the needs ofbusiness development and innovation, which helps the Bank to achieve value through risk managementand ultimately provide sound support for the Bank to achieve its strategic goals.

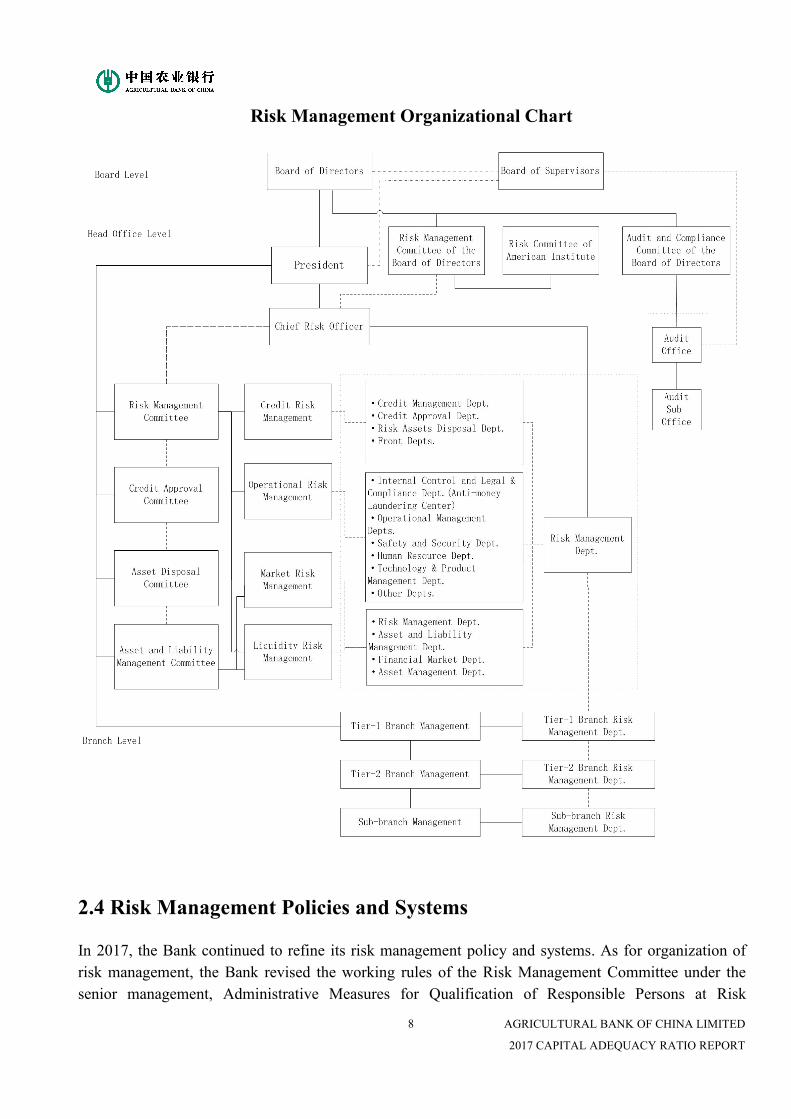

2.3 Structure and Organization of Risk Management

The Board of Directors of the Bank assumes the ultimate responsibility for risk management. The RiskManagement Committee, the Audit and Compliance Committee and the Risk Management Committeeof Institutions in the United States Regions under the Board of Directors perform the risk managementfunctions, review the key risk management issues and supervise and evaluate the establishment of riskmanagement system and the risk level of the Bank.

The Board of Supervisors is the supervisory body of the Bank. It is primarily responsible forsupervising the Board of Directors and Senior Management in their performance and due diligence, and

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

7

supervising financial activities, operating decision-making, risk management and internal control withinthe Bank.

Senior Management is the organizer and executor of risk management of the Bank. Under the seniormanagement oversight, the Bank has various risk management committees with different functions,including Risk Management Committee, Credit Approval Committee, Asset and Liability ManagementCommittee and Asset Disposal Committee. Risk Management Committee is primarily responsible forconsidering material risk management issues, studying and drafting risk management policies, systemsand tools, and analyzing and evaluating the overall risk profile of the Bank.

Based on the principles of "centralized management and control, matrix distribution, overall coverage,all-staff participation", the Bank has established "Three Lines of Defense" for risk managementconsisting of business operation departments (risk-taking departments), risk management departments,and the Internal Audit Department. In 2017, the Bank continued to improve its risk management systemand enhancing the expertise of our risk management team by strengthening comprehensive riskmanagement and the management units that take charge of credit, market, operating and other key risks.The Bank kept on developing a professional group of risk management, and strived to achievecontinuous improvement in the performance and competence of the bank-wide risk management staffthrough job rotation, special training programme, qualification verification and expertise tests.

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

8

Risk Management Organizational Chart

2.4 Risk Management Policies and Systems

In 2017, the Bank continued to refine its risk management policy and systems. As for organization ofrisk management, the Bank revised the working rules of the Risk Management Committee under thesenior management, Administrative Measures for Qualification of Responsible Persons at Risk

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

9

Management Department of Tier-1 branch of the Bank and Implementing Rules for the Supervisionover due diligence at all risk management functions of the Bank. As for credit risk management, theBank formulated the Opinions Relating to Further Strengthening the Development of Credit Teams,the Opinions Relating to Further Strengthening the Regulation on Loans and Strengthening OverallCredit Risk Management, the Administrative Measures on Filing of Credits to CorporateCustomer ,Administrative Measures on limit management of industry-specific exposures of the Bankand Administrative Measures on risks relating to credit assets of overseas branches of the Bank. As forconsolidated risk management, the Bank formulated the Administrative Measures on Risk Managementof Subsidiaries, Administrative Measures on Risk Management of overseas branches and subsidiarybanks. Meanwhile, the Bank formulated the policies in relation to the annual rating, classification,financing/borrowing transactions and market risk, which provide effective guidelines for daily riskmanagement of the Bank.

2.5 Risk Management Tools and IT Systems

Implementation of the advanced approaches for capital management

The Bank further reinforced the implementation of the advanced approaches of capital management. InJanuary 2017, the CBRC formally approved the Bank’s application to expand the implementation of theadvanced approaches of capital management through implementation of the Internal Model Approach(IMA) for market risks, setting unified benchmarks for non-retail portfolios in domestic and overseasbranches, and removing the restriction that retail risk-weighted asset shall be no less than the levelrequired under the weighting approach, facilitating the implementation and application of advancedapproaches for capital management.

In respect of credit risk, the Bank launched the online application of the foreign and domestic non-retailInternal Ratings-Based (IRB) system in 2007 and 2009 respectively, and the retail IRB system wasbrought online in 2011. Since then, the quality of data gradually improved, while the model, riskparameters and risk identification ability have remained satisfactory, and widening use of risk rating hasbeen evident. During the Reporting Period, the Bank strictly improved the parameters of the model toenhance the application of the rating model. The Bank further strengthened sensitivity management incredit rating and the ability to timely detect potential default risk by conducting investigation on risk ofdefault and enhancing the dynamic adjustment mechanism for credit ratings. The Bank strengthened themanagement on rating of customers of overseas institutions to enhance coverage of the internal rating.The Bank strengthened the leading role of rating in risk management. The Bank expanded andintensified the application of the rating mechanism for retail portfolios by refining the scoring cardrelating to applications for residential mortgage loans and loans to commodity houses, which furtherenhanced the ability to identify risks. The Bank continued to strengthen the management on retail ratingmechanism to enhance accuracy and prudence of the rating mechanism.

In respect of market risk, the CBRC formally approved the Bank’s implementation of the InternalModel Approach (IMA) for market risks. The Bank launched the application of Internal ModelsApproach (IMA) in 2013 and established the advanced measurement and management system for

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

10

market risk with regard to organizational structure, policies and procedures, measurement methods andIT systems. In addition, the Bank applied the measurement results of the IMA to risk limit managementand policy-making process in order to provide strong support to the risk analysis and investmentdecision-making in financial market business. In 2017, the Bank conducted overall assessment on IMAfor market risks to further refine its measurement mechanism. The measurement mechanism has beenoperating throughout the year with prudent and reliable results.

In respect of operational risk, the Bank kept on promoting the implementation of the advancedmeasurement approaches for operational risk, collected the internal loss data since 2008 and establishedan advanced measurement approach system based on the loss distribution approach, which has beenapplied in measuring operational risk economic capital since January 2014. During the internaloperation procedure of the advanced approaches, the Bank continued to optimize the measurementmodels and measurement engines and explored measurement approaches that are suitable to ourconditions; the Bank improved the reporting standards for the internal loss data and enhanced thereview in order to ensure the data quality about internal loss; the Bank optimized the operational riskmanagement scoring card, and raised the weighting of quantitative indicators, which helped tostrengthened the sensitivity to and early detection of operational risk.

Internal Capital Adequacy Assessment Process (ICAAP). In 2017, the Bank kept pushing forward theimplementation of ICAAP and actively carried out the 2017 ICAAP. The assessment report has beenreviewed and approved by the Board of Directors. The Bank organized and carried out the 2017 specialaudit on ICAAP.

Information disclosure on capital adequacy ratio. In 2017, according to the requirements of the CapitalRules for Commercial Banks (Provisional), the Bank completed the 2016 Capital Adequacy RatioReport, which was published together with the Annual Report. The quarterly and semi-annualinformation of capital adequacy ratio were included in Quarterly Report and Interim Report of theBank.

Tools and measures for risk management

The Bank actively promoted the implementation of the advanced approaches for capital management,and established an operation and transmission mechanism of risk management to balance capital, riskand return. We strengthened monitoring, analysis and warning of risks related to key areas industriesand customers by using various risk management tools, such as economic capital, risk limits, creditrating, risk classification, impairment provision, stress test and risk appraisal. As such, the capability ofrisk identification, measurement, monitoring, control and reporting has been extensively enhanced.

The Bank continually refined the management of economic capital. In 2017, based on the principle of“adhering to objective measurement while accurately reflecting the risks”, the Bank optimized themeasurement plan for economic capital, which served as the guidelines for the Bank to strengthen therisk management. The Bank adjusted the parameters of the model in light of the historical performancein asset risks and the risk parameters applied to the rating model to reflect the objective changes in risks,The Bank continued to adjust the mechanism with the economic capital to strengthen the efforts in

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

11

disposal and mitigation of risks in relation to guarantee circle with high risks and transactions withdubious motives and further reduced credit to controlled industries and strengthened risk managementon key areas.

The Bank continued to strengthen industry-specific exposure limit management. In 2017, the Bankactively adjusted and refine its asset structure through limit management on 13 industries among thecoal and steel industries with serious overcapacity and high risks, with a focus on the government’ssupply-side structural reform and the initiative to “cut overcapacity, reduce inventory, deleverage,lower costs and bolster areas of weakness”. At the end of the year, credits granted to all controlledindustries were kept within limit. The limit control effectively contained the risk exposure to steel andcoal industries with overcapacity, optimizing the credit structure of controlled industries.

The Bank’s risk management information system links up with its core business systems and data poolsfor credit risk, market risk and operational risk has been established. The risk management tools, datapool and information system we built and used provided a solid base for enhancing the delicacy andscientific quality of risk management and facilitated decision making for business operation andmanagement.

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

12

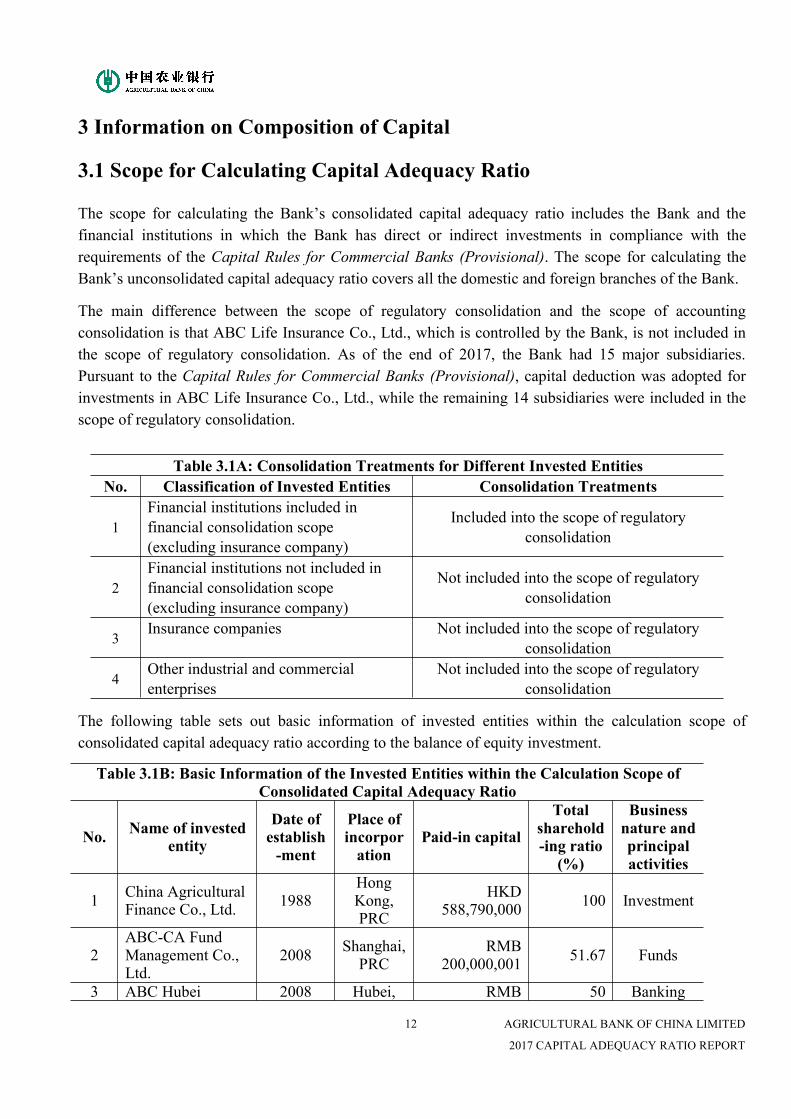

3 Information on Composition of Capital

3.1 Scope for Calculating Capital Adequacy Ratio

The scope for calculating the Bank’s consolidated capital adequacy ratio includes the Bank and thefinancial institutions in which the Bank has direct or indirect investments in compliance with therequirements of the Capital Rules for Commercial Banks (Provisional). The scope for calculating theBank’s unconsolidated capital adequacy ratio covers all the domestic and foreign branches of the Bank.

The main difference between the scope of regulatory consolidation and the scope of accountingconsolidation is that ABC Life Insurance Co., Ltd., which is controlled by the Bank, is not included inthe scope of regulatory consolidation. As of the end of 2017, the Bank had 15 major subsidiaries.Pursuant to the Capital Rules for Commercial Banks (Provisional), capital deduction was adopted forinvestments in ABC Life Insurance Co., Ltd., while the remaining 14 subsidiaries were included in thescope of regulatory consolidation.

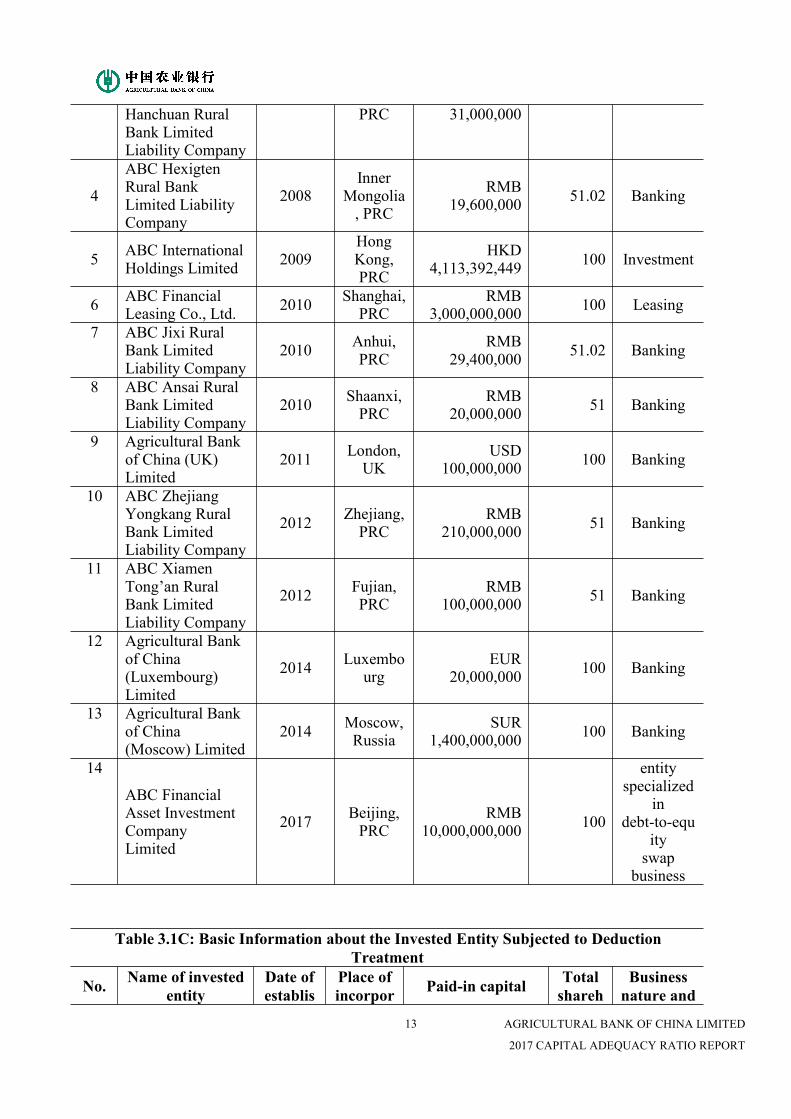

The following table sets out basic information of invested entities within the calculation scope ofconsolidated capital adequacy ratio according to the balance of equity investment.

Table 3.1B: Basic Information of the Invested Entities within the Calculation Scope ofConsolidated Capital Adequacy Ratio

No. Name of investedentity

Date ofestablish-ment

Place ofincorporation

Paid-in capital

Totalsharehold-ing ratio

(%)

Businessnature andprincipalactivities

1 China AgriculturalFinance Co., Ltd. 1988

HongKong,PRC

HKD588,790,000 100 Investment

2ABC-CA FundManagement Co.,Ltd.

2008 Shanghai,PRC

RMB200,000,001 51.67 Funds

3 ABC Hubei 2008 Hubei, RMB 50 Banking

Table 3.1A: Consolidation Treatments for Different Invested EntitiesNo. Classification of Invested Entities Consolidation Treatments

1Financial institutions included infinancial consolidation scope(excluding insurance company)

Included into the scope of regulatoryconsolidation

2Financial institutions not included infinancial consolidation scope(excluding insurance company)

Not included into the scope of regulatoryconsolidation

3Insurance companies Not included into the scope of regulatory

consolidation

4Other industrial and commercialenterprises

Not included into the scope of regulatoryconsolidation

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

13

Hanchuan RuralBank LimitedLiability Company

PRC 31,000,000

4

ABC HexigtenRural BankLimited LiabilityCompany

2008Inner

Mongolia, PRC

RMB19,600,000 51.02 Banking

5 ABC InternationalHoldings Limited 2009

HongKong,PRC

HKD4,113,392,449 100 Investment

6 ABC FinancialLeasing Co., Ltd. 2010 Shanghai,

PRCRMB

3,000,000,000 100 Leasing

7 ABC Jixi RuralBank LimitedLiability Company

2010 Anhui,PRC

RMB29,400,000 51.02 Banking

8 ABC Ansai RuralBank LimitedLiability Company

2010 Shaanxi,PRC

RMB20,000,000 51 Banking

9 Agricultural Bankof China (UK)Limited

2011 London,UK

USD100,000,000 100 Banking

10 ABC ZhejiangYongkang RuralBank LimitedLiability Company

2012 Zhejiang,PRC

RMB210,000,000 51 Banking

11 ABC XiamenTong’an RuralBank LimitedLiability Company

2012 Fujian,PRC

RMB100,000,000 51 Banking

12 Agricultural Bankof China(Luxembourg)Limited

2014 Luxembourg

EUR20,000,000 100 Banking

13 Agricultural Bankof China(Moscow) Limited

2014 Moscow,Russia

SUR1,400,000,000 100 Banking

14

ABC FinancialAsset InvestmentCompanyLimited

2017 Beijing,PRC

RMB10,000,000,000 100

entityspecialized

indebt-to-equ

ityswap

business

Table 3.1C: Basic Information about the Invested Entity Subjected to DeductionTreatment

No. Name of investedentity

Date ofestablis

Place ofincorpor Paid-in capital Total

sharehBusinessnature and

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

14

hment ation oldingratio(%)

principalactivities

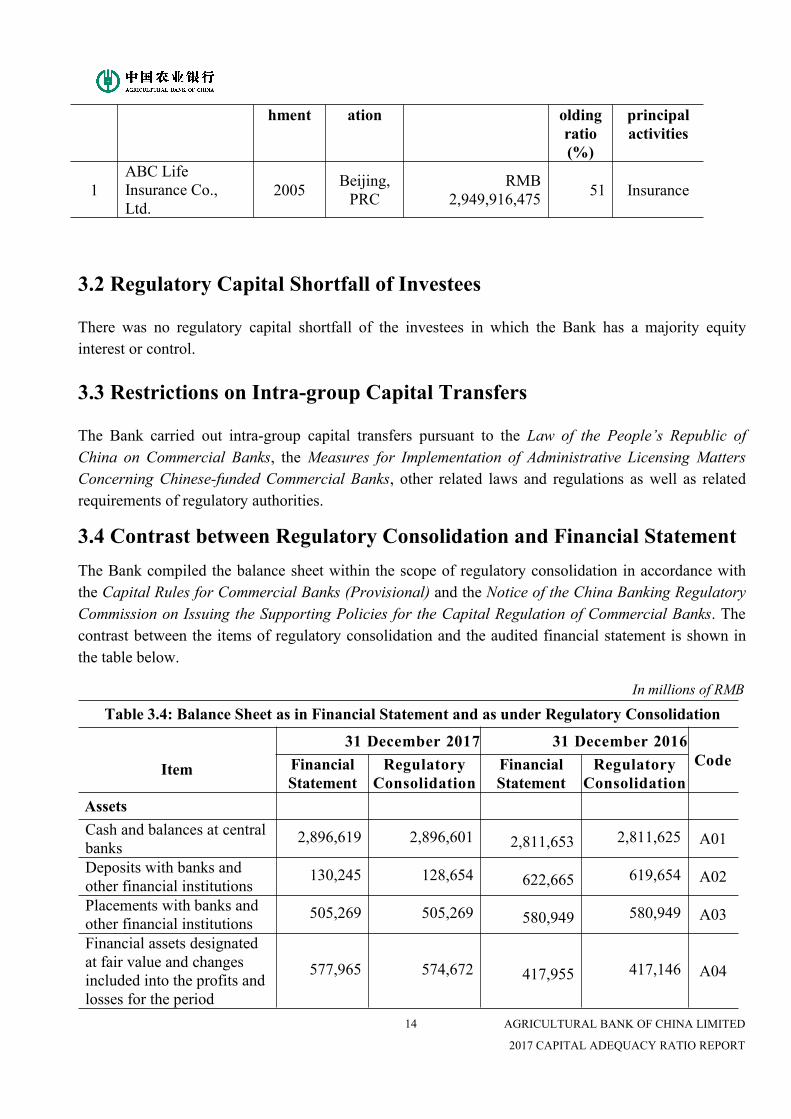

1ABC LifeInsurance Co.,Ltd.

2005 Beijing,PRC

RMB2,949,916,475 51 Insurance

3.2 Regulatory Capital Shortfall of Investees

There was no regulatory capital shortfall of the investees in which the Bank has a majority equityinterest or control.

3.3 Restrictions on Intra-group Capital Transfers

The Bank carried out intra-group capital transfers pursuant to the Law of the People’s Republic ofChina on Commercial Banks, the Measures for Implementation of Administrative Licensing MattersConcerning Chinese-funded Commercial Banks, other related laws and regulations as well as relatedrequirements of regulatory authorities.

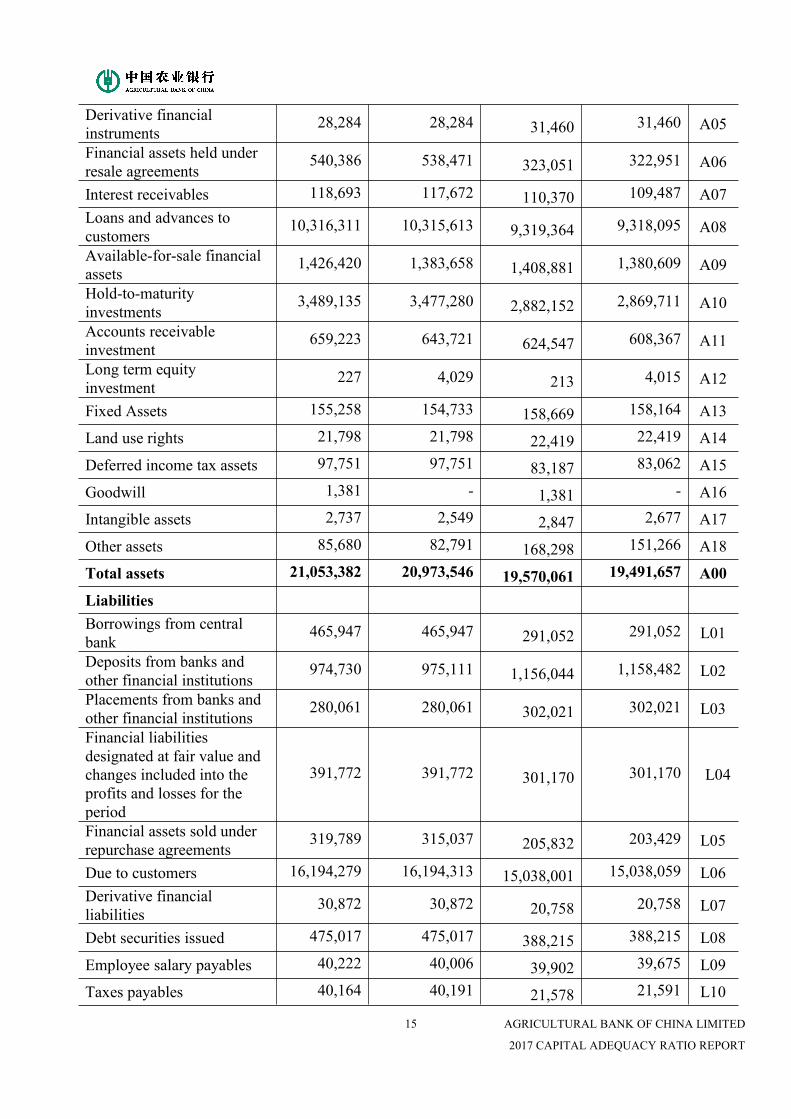

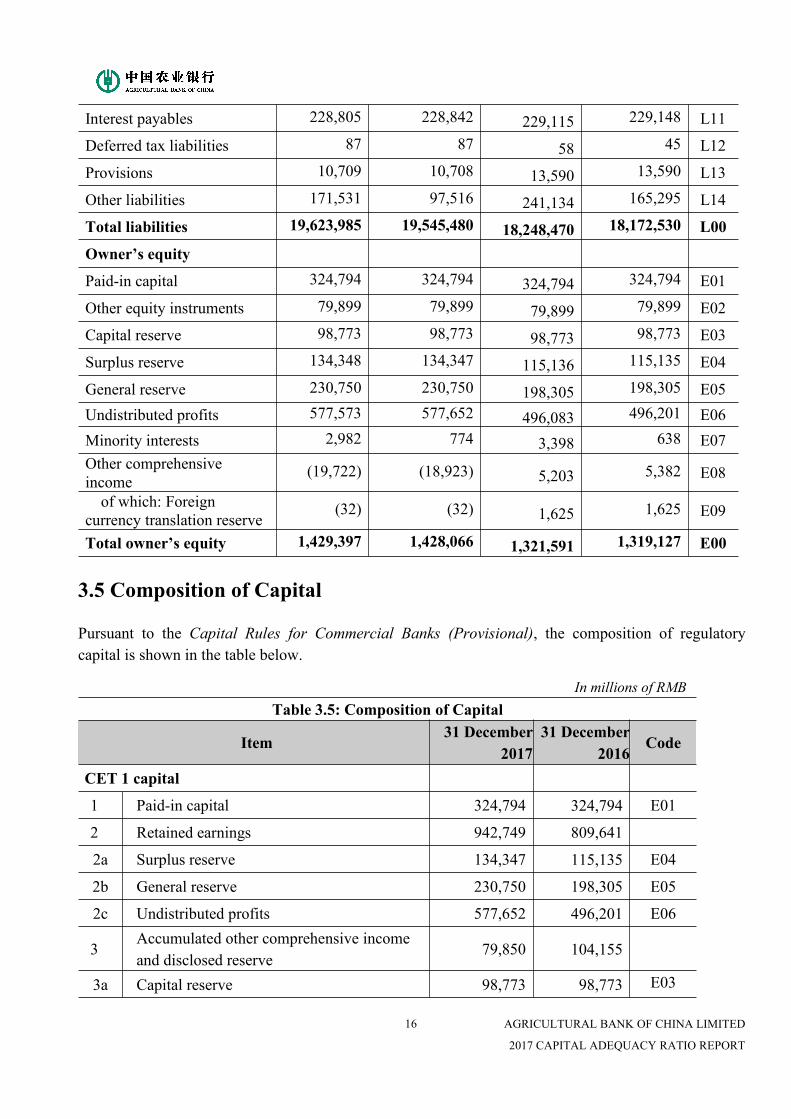

3.4 Contrast between Regulatory Consolidation and Financial StatementThe Bank compiled the balance sheet within the scope of regulatory consolidation in accordance withthe Capital Rules for Commercial Banks (Provisional) and the Notice of the China Banking RegulatoryCommission on Issuing the Supporting Policies for the Capital Regulation of Commercial Banks. Thecontrast between the items of regulatory consolidation and the audited financial statement is shown inthe table below.

In millions of RMB

Table 3.4: Balance Sheet as in Financial Statement and as under Regulatory Consolidation

Item

31 December 2017 31 December 2016CodeFinancial

StatementRegulatory

ConsolidationFinancialStatement

RegulatoryConsolidation

AssetsCash and balances at centralbanks

2,896,619 2,896,601 2,811,653 2,811,625 A01

Deposits with banks andother financial institutions

130,245 128,654 622,665 619,654 A02

Placements with banks andother financial institutions

505,269 505,269 580,949 580,949 A03

Financial assets designatedat fair value and changesincluded into the profits andlosses for the period

577,965 574,672 417,955 417,146 A04

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

15

Derivative financialinstruments

28,284 28,284 31,460 31,460 A05

Financial assets held underresale agreements

540,386 538,471 323,051 322,951 A06

Interest receivables 118,693 117,672 110,370 109,487 A07Loans and advances tocustomers

10,316,311 10,315,613 9,319,364 9,318,095 A08

Available-for-sale financialassets

1,426,420 1,383,658 1,408,881 1,380,609 A09

Hold-to-maturityinvestments

3,489,135 3,477,280 2,882,152 2,869,711 A10

Accounts receivableinvestment

659,223 643,721 624,547 608,367 A11

Long term equityinvestment

227 4,029 213 4,015 A12

Fixed Assets 155,258 154,733 158,669 158,164 A13

Land use rights 21,798 21,798 22,419 22,419 A14

Deferred income tax assets 97,751 97,751 83,187 83,062 A15

Goodwill 1,381 - 1,381 - A16

Intangible assets 2,737 2,549 2,847 2,677 A17

Other assets 85,680 82,791 168,298 151,266 A18

Total assets 21,053,382 20,973,546 19,570,061 19,491,657 A00

LiabilitiesBorrowings from centralbank

465,947 465,947 291,052 291,052 L01

Deposits from banks andother financial institutions

974,730 975,111 1,156,044 1,158,482 L02

Placements from banks andother financial institutions

280,061 280,061 302,021 302,021 L03

Financial liabilitiesdesignated at fair value andchanges included into theprofits and losses for theperiod

391,772 391,772 301,170 301,170 L04

Financial assets sold underrepurchase agreements

319,789 315,037 205,832 203,429 L05

Due to customers 16,194,279 16,194,313 15,038,001 15,038,059 L06Derivative financialliabilities

30,872 30,872 20,758 20,758 L07

Debt securities issued 475,017 475,017 388,215 388,215 L08

Employee salary payables 40,222 40,006 39,902 39,675 L09

Taxes payables 40,164 40,191 21,578 21,591 L10

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

16

Interest payables 228,805 228,842 229,115 229,148 L11

Deferred tax liabilities 87 87 58 45 L12

Provisions 10,709 10,708 13,590 13,590 L13

Other liabilities 171,531 97,516 241,134 165,295 L14

Total liabilities 19,623,985 19,545,480 18,248,470 18,172,530 L00

Owner’s equity

Paid-in capital 324,794 324,794 324,794 324,794 E01

Other equity instruments 79,899 79,899 79,899 79,899 E02

Capital reserve 98,773 98,773 98,773 98,773 E03

Surplus reserve 134,348 134,347 115,136 115,135 E04

General reserve 230,750 230,750 198,305 198,305 E05Undistributed profits 577,573 577,652 496,083 496,201 E06Minority interests 2,982 774 3,398 638 E07Other comprehensiveincome

(19,722) (18,923) 5,203 5,382 E08

of which: Foreigncurrency translation reserve

(32) (32) 1,625 1,625 E09

Total owner’s equity 1,429,397 1,428,066 1,321,591 1,319,127 E00

3.5 Composition of Capital

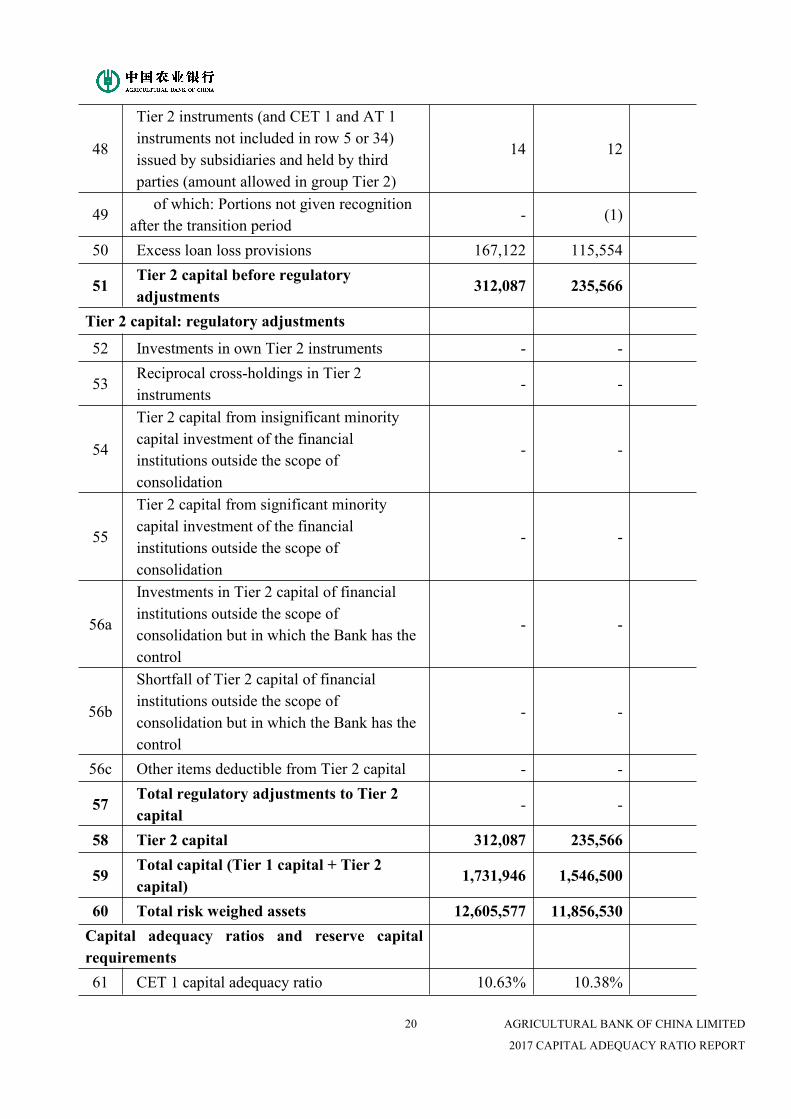

Pursuant to the Capital Rules for Commercial Banks (Provisional), the composition of regulatorycapital is shown in the table below.

In millions of RMBTable 3.5: Composition of Capital

Item31 December

201731 December

2016Code

CET 1 capital

1 Paid-in capital 324,794 324,794 E01

2 Retained earnings 942,749 809,641

2a Surplus reserve 134,347 115,135 E04

2b General reserve 230,750 198,305 E05

2c Undistributed profits 577,652 496,201 E06

3Accumulated other comprehensive incomeand disclosed reserve

79,850 104,155

3a Capital reserve 98,773 98,773 E03

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

17

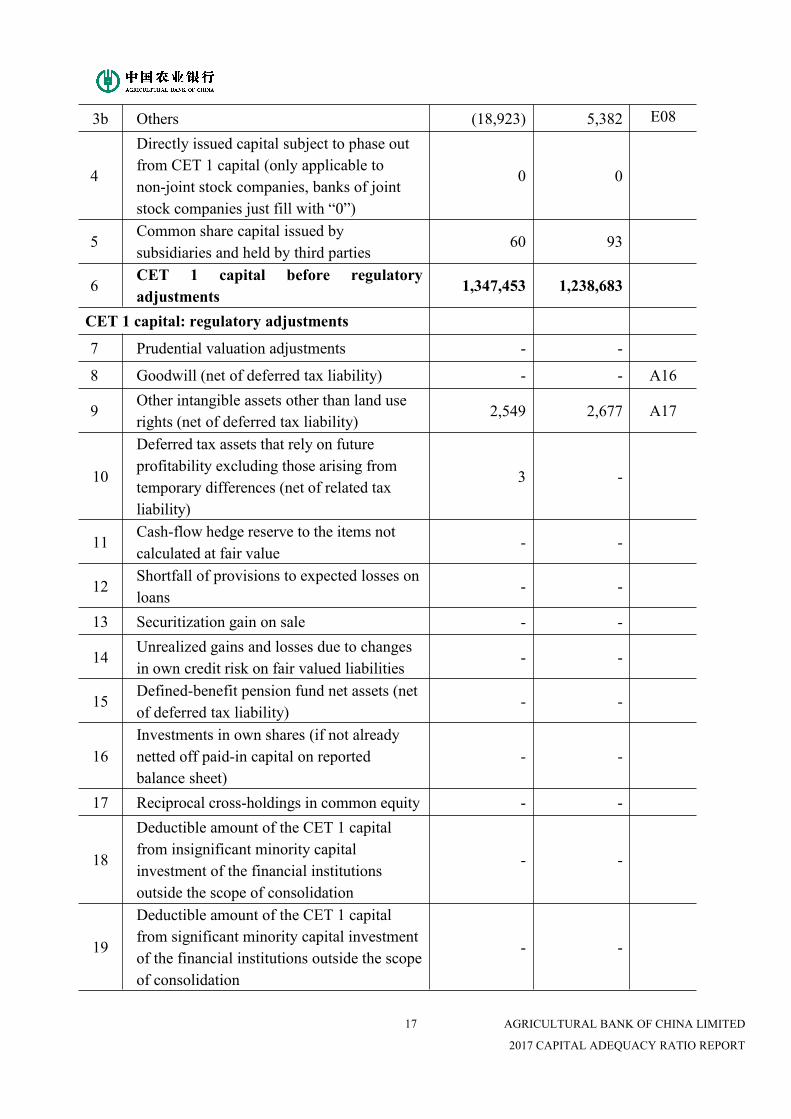

3b Others (18,923) 5,382 E08

4

Directly issued capital subject to phase outfrom CET 1 capital (only applicable tonon-joint stock companies, banks of jointstock companies just fill with “0”)

0 0

5Common share capital issued bysubsidiaries and held by third parties

60 93

6CET 1 capital before regulatoryadjustments

1,347,453 1,238,683

CET 1 capital: regulatory adjustments

7 Prudential valuation adjustments - -

8 Goodwill (net of deferred tax liability) - - A16

9Other intangible assets other than land userights (net of deferred tax liability)

2,549 2,677 A17

10

Deferred tax assets that rely on futureprofitability excluding those arising fromtemporary differences (net of related taxliability)

3 -

11Cash-flow hedge reserve to the items notcalculated at fair value

- -

12Shortfall of provisions to expected losses onloans

- -

13 Securitization gain on sale - -

14Unrealized gains and losses due to changesin own credit risk on fair valued liabilities

- -

15Defined-benefit pension fund net assets (netof deferred tax liability)

- -

16Investments in own shares (if not alreadynetted off paid-in capital on reportedbalance sheet)

- -

17 Reciprocal cross-holdings in common equity - -

18

Deductible amount of the CET 1 capitalfrom insignificant minority capitalinvestment of the financial institutionsoutside the scope of consolidation

- -

19

Deductible amount of the CET 1 capitalfrom significant minority capital investmentof the financial institutions outside the scopeof consolidation

- -

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

18

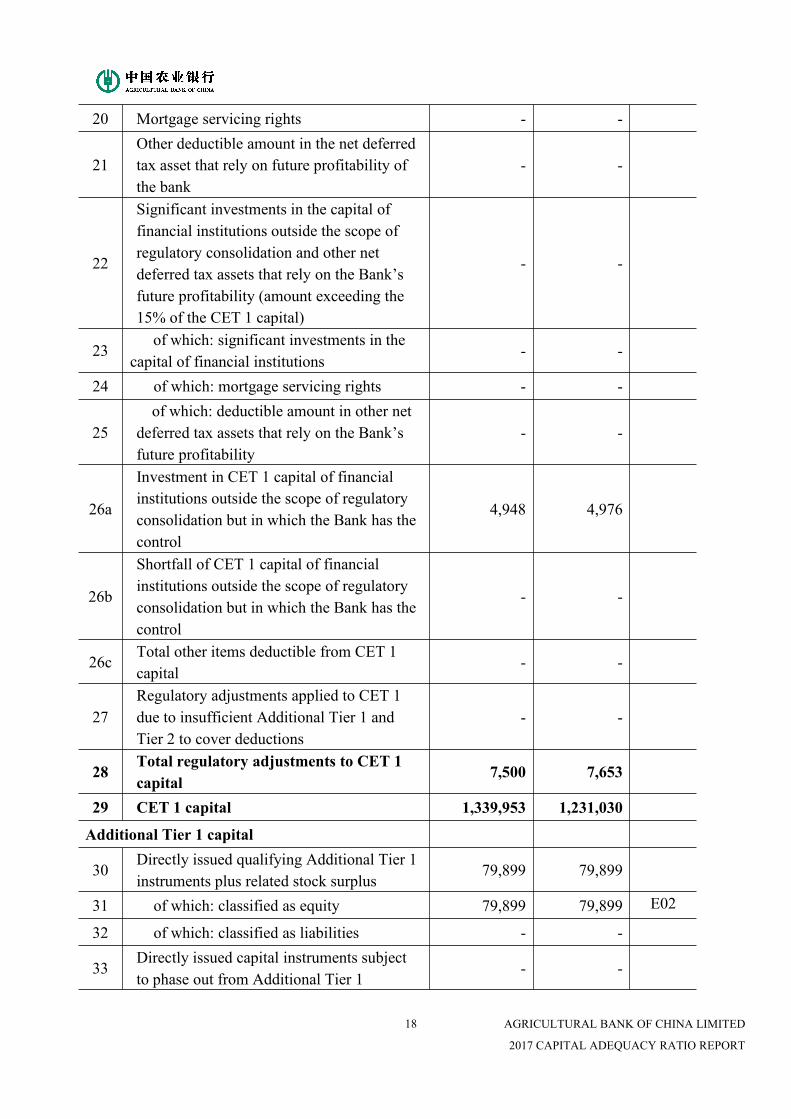

20 Mortgage servicing rights - -

21Other deductible amount in the net deferredtax asset that rely on future profitability ofthe bank

- -

22

Significant investments in the capital offinancial institutions outside the scope ofregulatory consolidation and other netdeferred tax assets that rely on the Bank’sfuture profitability (amount exceeding the15% of the CET 1 capital)

- -

23of which: significant investments in the

capital of financial institutions- -

24 of which: mortgage servicing rights - -

25of which: deductible amount in other net

deferred tax assets that rely on the Bank’sfuture profitability

- -

26a

Investment in CET 1 capital of financialinstitutions outside the scope of regulatoryconsolidation but in which the Bank has thecontrol

4,948 4,976

26b

Shortfall of CET 1 capital of financialinstitutions outside the scope of regulatoryconsolidation but in which the Bank has thecontrol

- -

26cTotal other items deductible from CET 1capital

- -

27Regulatory adjustments applied to CET 1due to insufficient Additional Tier 1 andTier 2 to cover deductions

- -

28Total regulatory adjustments to CET 1capital

7,500 7,653

29 CET 1 capital 1,339,953 1,231,030

Additional Tier 1 capital

30Directly issued qualifying Additional Tier 1instruments plus related stock surplus

79,899 79,899

31 of which: classified as equity 79,899 79,899 E02

32 of which: classified as liabilities - -

33Directly issued capital instruments subjectto phase out from Additional Tier 1

- -

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

19

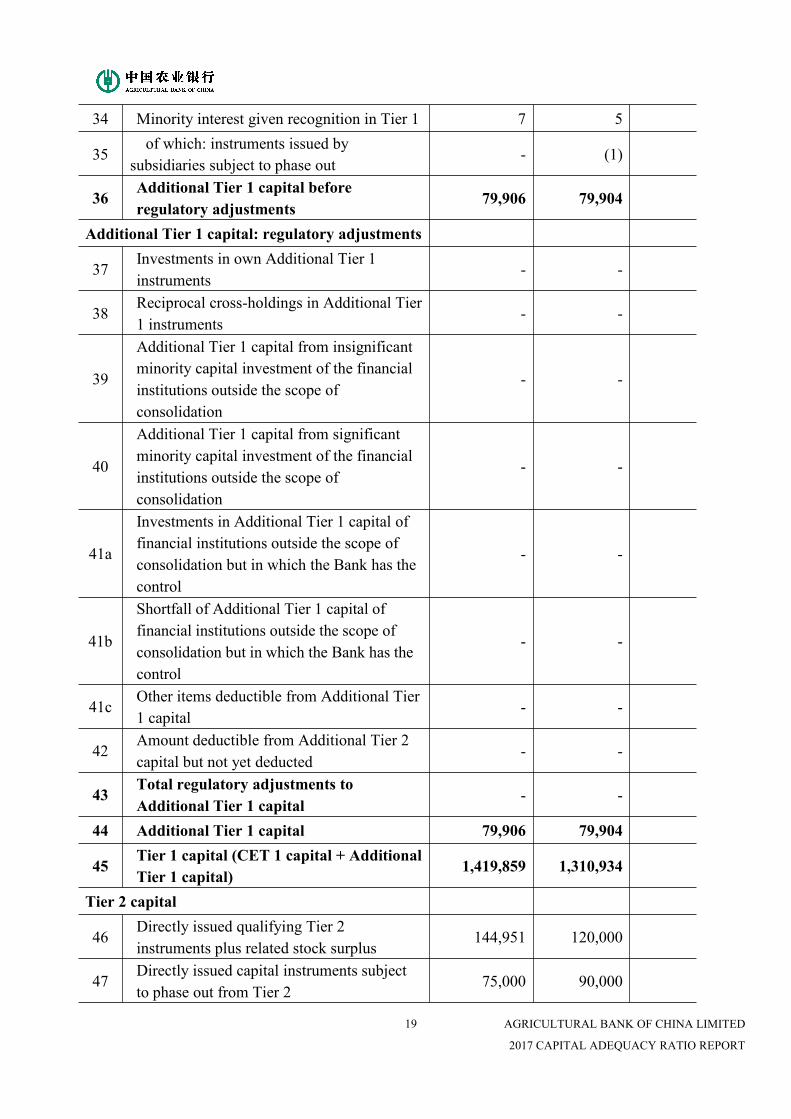

34 Minority interest given recognition in Tier 1 7 5

35of which: instruments issued by

subsidiaries subject to phase out- (1)

36Additional Tier 1 capital beforeregulatory adjustments

79,906 79,904

Additional Tier 1 capital: regulatory adjustments

37Investments in own Additional Tier 1instruments

- -

38Reciprocal cross-holdings in Additional Tier1 instruments

- -

39

Additional Tier 1 capital from insignificantminority capital investment of the financialinstitutions outside the scope ofconsolidation

- -

40

Additional Tier 1 capital from significantminority capital investment of the financialinstitutions outside the scope ofconsolidation

- -

41a

Investments in Additional Tier 1 capital offinancial institutions outside the scope ofconsolidation but in which the Bank has thecontrol

- -

41b

Shortfall of Additional Tier 1 capital offinancial institutions outside the scope ofconsolidation but in which the Bank has thecontrol

- -

41cOther items deductible from Additional Tier1 capital

- -

42Amount deductible from Additional Tier 2capital but not yet deducted

- -

43Total regulatory adjustments toAdditional Tier 1 capital

- -

44 Additional Tier 1 capital 79,906 79,904

45Tier 1 capital (CET 1 capital + AdditionalTier 1 capital)

1,419,859 1,310,934

Tier 2 capital

46Directly issued qualifying Tier 2instruments plus related stock surplus

144,951 120,000

47Directly issued capital instruments subjectto phase out from Tier 2

75,000 90,000

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

20

48

Tier 2 instruments (and CET 1 and AT 1instruments not included in row 5 or 34)issued by subsidiaries and held by thirdparties (amount allowed in group Tier 2)

14 12

49of which: Portions not given recognition

after the transition period- (1)

50 Excess loan loss provisions 167,122 115,554

51Tier 2 capital before regulatoryadjustments

312,087 235,566

Tier 2 capital: regulatory adjustments

52 Investments in own Tier 2 instruments - -

53Reciprocal cross-holdings in Tier 2instruments

- -

54

Tier 2 capital from insignificant minoritycapital investment of the financialinstitutions outside the scope ofconsolidation

- -

55

Tier 2 capital from significant minoritycapital investment of the financialinstitutions outside the scope ofconsolidation

- -

56a

Investments in Tier 2 capital of financialinstitutions outside the scope ofconsolidation but in which the Bank has thecontrol

- -

56b

Shortfall of Tier 2 capital of financialinstitutions outside the scope ofconsolidation but in which the Bank has thecontrol

- -

56c Other items deductible from Tier 2 capital - -

57Total regulatory adjustments to Tier 2capital

- -

58 Tier 2 capital 312,087 235,566

59Total capital (Tier 1 capital + Tier 2capital)

1,731,946 1,546,500

60 Total risk weighed assets 12,605,577 11,856,530Capital adequacy ratios and reserve capitalrequirements61 CET 1 capital adequacy ratio 10.63% 10.38%

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

21

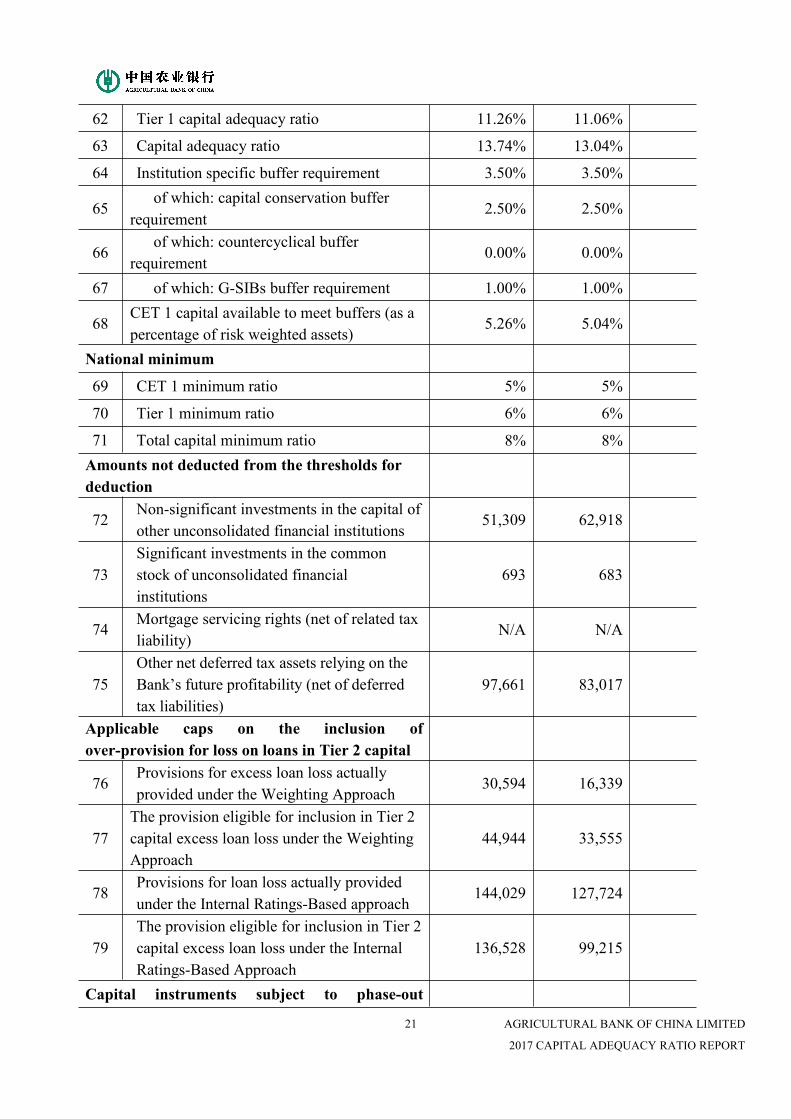

62 Tier 1 capital adequacy ratio 11.26% 11.06%

63 Capital adequacy ratio 13.74% 13.04%

64 Institution specific buffer requirement 3.50% 3.50%

65of which: capital conservation buffer

requirement2.50% 2.50%

66of which: countercyclical buffer

requirement0.00% 0.00%

67 of which: G-SIBs buffer requirement 1.00% 1.00%

68CET 1 capital available to meet buffers (as apercentage of risk weighted assets)

5.26% 5.04%

National minimum

69 CET 1 minimum ratio 5% 5%

70 Tier 1 minimum ratio 6% 6%

71 Total capital minimum ratio 8% 8%Amounts not deducted from the thresholds fordeduction

72Non-significant investments in the capital ofother unconsolidated financial institutions

51,309 62,918

73Significant investments in the commonstock of unconsolidated financialinstitutions

693 683

74Mortgage servicing rights (net of related taxliability)

N/A N/A

75Other net deferred tax assets relying on theBank’s future profitability (net of deferredtax liabilities)

97,661 83,017

Applicable caps on the inclusion ofover-provision for loss on loans in Tier 2 capital

76Provisions for excess loan loss actuallyprovided under the Weighting Approach

30,594 16,339

77The provision eligible for inclusion in Tier 2capital excess loan loss under the WeightingApproach

44,944 33,555

78Provisions for loan loss actually providedunder the Internal Ratings-Based approach

144,029 127,724

79The provision eligible for inclusion in Tier 2capital excess loan loss under the InternalRatings-Based Approach

136,528 99,215

Capital instruments subject to phase-out

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

22

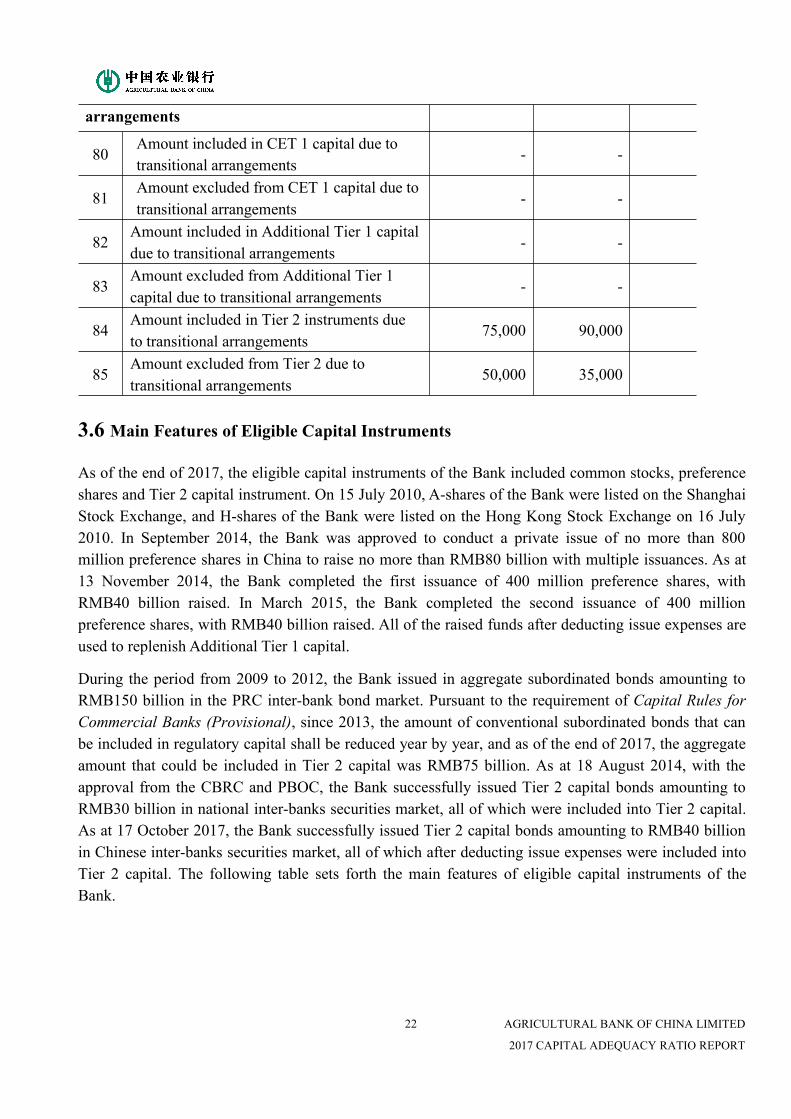

arrangements

80Amount included in CET 1 capital due totransitional arrangements

- -

81Amount excluded from CET 1 capital due totransitional arrangements

- -

82Amount included in Additional Tier 1 capitaldue to transitional arrangements

- -

83Amount excluded from Additional Tier 1capital due to transitional arrangements

- -

84Amount included in Tier 2 instruments dueto transitional arrangements

75,000 90,000

85Amount excluded from Tier 2 due totransitional arrangements

50,000 35,000

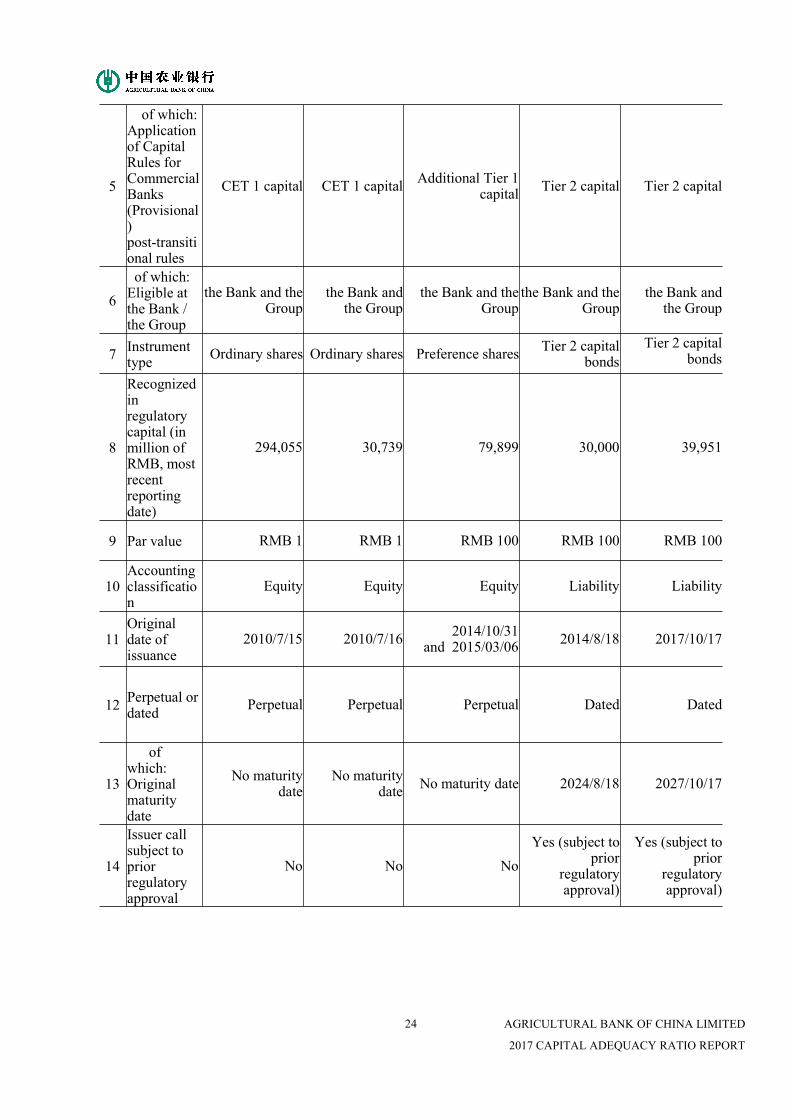

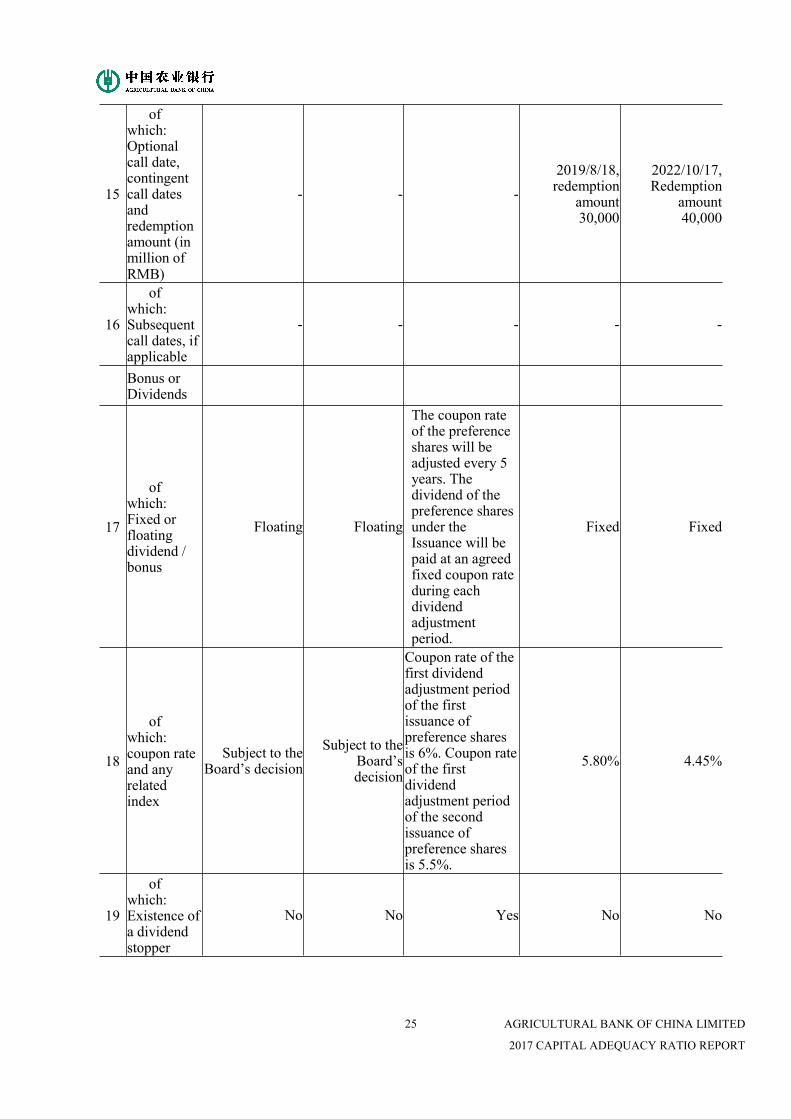

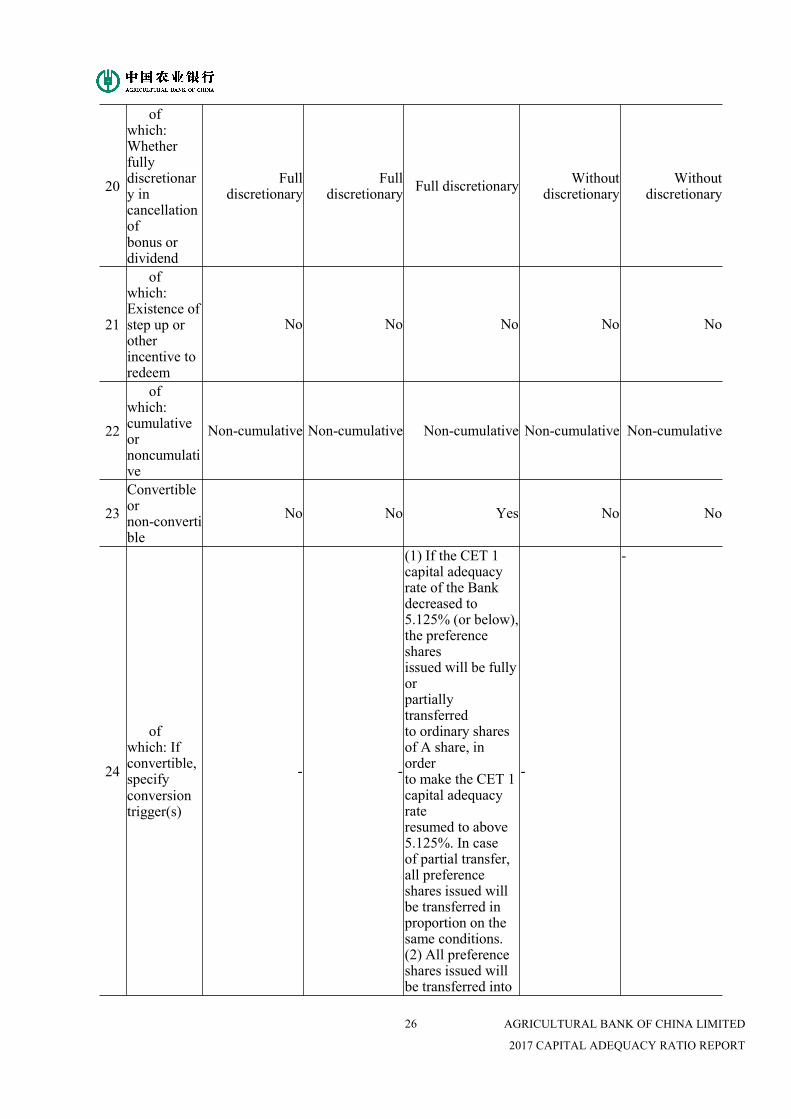

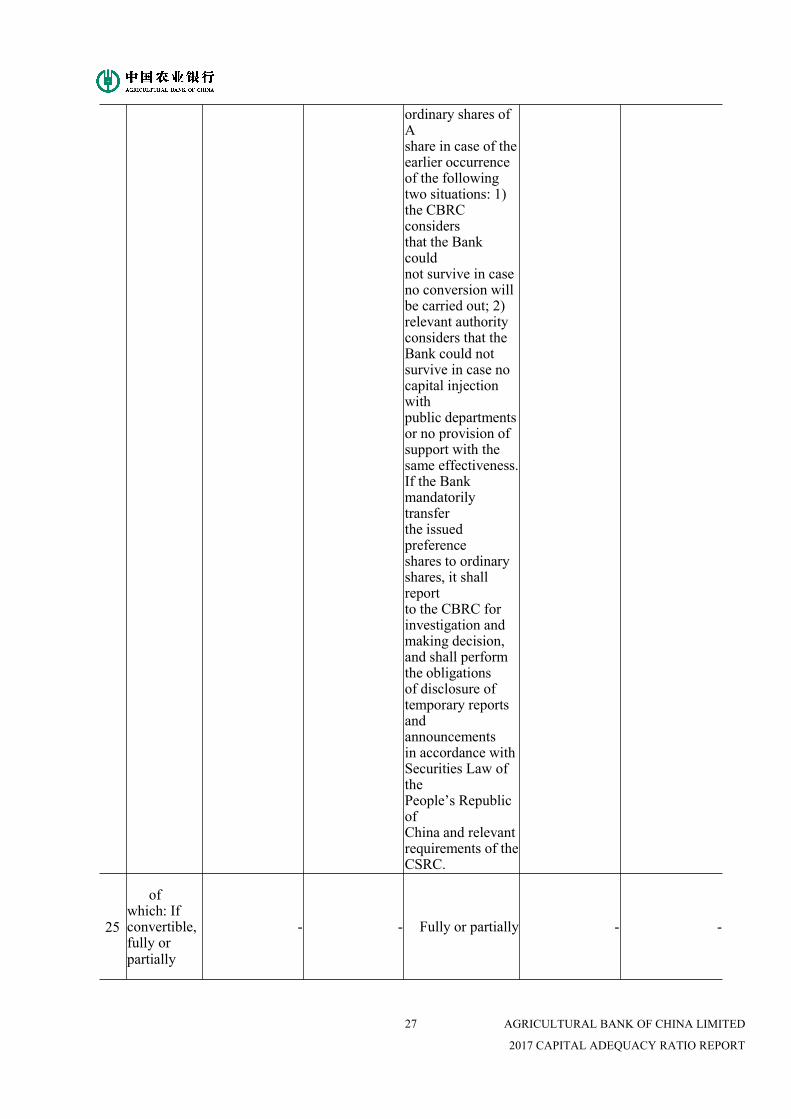

3.6 Main Features of Eligible Capital Instruments

As of the end of 2017, the eligible capital instruments of the Bank included common stocks, preferenceshares and Tier 2 capital instrument. On 15 July 2010, A-shares of the Bank were listed on the ShanghaiStock Exchange, and H-shares of the Bank were listed on the Hong Kong Stock Exchange on 16 July2010. In September 2014, the Bank was approved to conduct a private issue of no more than 800million preference shares in China to raise no more than RMB80 billion with multiple issuances. As at13 November 2014, the Bank completed the first issuance of 400 million preference shares, withRMB40 billion raised. In March 2015, the Bank completed the second issuance of 400 millionpreference shares, with RMB40 billion raised. All of the raised funds after deducting issue expenses areused to replenish Additional Tier 1 capital.

During the period from 2009 to 2012, the Bank issued in aggregate subordinated bonds amounting toRMB150 billion in the PRC inter-bank bond market. Pursuant to the requirement of Capital Rules forCommercial Banks (Provisional), since 2013, the amount of conventional subordinated bonds that canbe included in regulatory capital shall be reduced year by year, and as of the end of 2017, the aggregateamount that could be included in Tier 2 capital was RMB75 billion. As at 18 August 2014, with theapproval from the CBRC and PBOC, the Bank successfully issued Tier 2 capital bonds amounting toRMB30 billion in national inter-banks securities market, all of which were included into Tier 2 capital.As at 17 October 2017, the Bank successfully issued Tier 2 capital bonds amounting to RMB40 billionin Chinese inter-banks securities market, all of which after deducting issue expenses were included intoTier 2 capital. The following table sets forth the main features of eligible capital instruments of theBank.

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

23

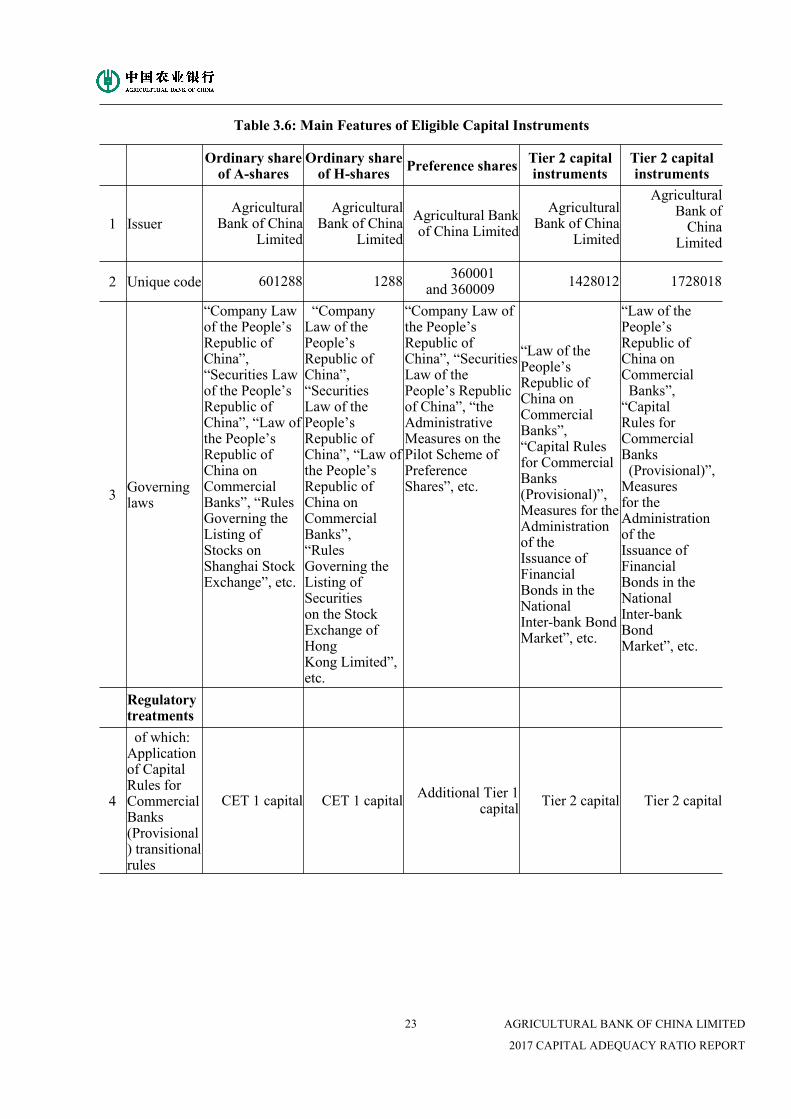

Table 3.6: Main Features of Eligible Capital Instruments

Ordinary shareof A-shares

Ordinary shareof H-shares Preference shares Tier 2 capital

instrumentsTier 2 capitalinstruments

1 IssuerAgricultural

Bank of ChinaLimited

AgriculturalBank of China

LimitedAgricultural Bankof China Limited

AgriculturalBank of China

Limited

AgriculturalBank ofChina

Limited

2 Unique code 601288 1288 360001and 360009 1428012 1728018

3 Governinglaws

“Company Lawof the People’sRepublic ofChina”,“Securities Lawof the People’sRepublic ofChina”, “Law ofthe People’sRepublic ofChina onCommercialBanks”, “RulesGoverning theListing ofStocks onShanghai StockExchange”, etc.

“CompanyLaw of thePeople’sRepublic ofChina”,“SecuritiesLaw of thePeople’sRepublic ofChina”, “Law ofthe People’sRepublic ofChina onCommercialBanks”,“RulesGoverning theListing ofSecuritieson the StockExchange ofHongKong Limited”,etc.

“Company Law ofthe People’sRepublic ofChina”, “SecuritiesLaw of thePeople’s Republicof China”, “theAdministrativeMeasures on thePilot Scheme ofPreferenceShares”, etc.

“Law of thePeople’sRepublic ofChina onCommercialBanks”,“Capital Rulesfor CommercialBanks(Provisional)”,Measures for theAdministrationof theIssuance ofFinancialBonds in theNationalInter-bank BondMarket”, etc.

“Law of thePeople’sRepublic ofChina onCommercialBanks”,“CapitalRules forCommercialBanks(Provisional)”,Measuresfor theAdministrationof theIssuance ofFinancialBonds in theNationalInter-bankBondMarket”, etc.

Regulatorytreatments

4

of which:Applicationof CapitalRules forCommercialBanks(Provisional) transitionalrules

CET 1 capital CET 1 capital Additional Tier 1capital Tier 2 capital Tier 2 capital

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

24

5

of which:Applicationof CapitalRules forCommercialBanks(Provisional)post-transitional rules

CET 1 capital CET 1 capital Additional Tier 1capital Tier 2 capital Tier 2 capital

6of which:Eligible atthe Bank /the Group

the Bank and theGroup

the Bank andthe Group

the Bank and theGroup

the Bank and theGroup

the Bank andthe Group

7 Instrumenttype Ordinary shares Ordinary shares Preference shares Tier 2 capital

bondsTier 2 capital

bonds

8

Recognizedinregulatorycapital (inmillion ofRMB, mostrecentreportingdate)

294,055 30,739 79,899 30,000 39,951

9 Par value RMB 1 RMB 1 RMB 100 RMB 100 RMB 100

10Accountingclassification

Equity Equity Equity Liability Liability

11Originaldate ofissuance

2010/7/15 2010/7/16 2014/10/31and 2015/03/06 2014/8/18 2017/10/17

12 Perpetual ordated Perpetual Perpetual Perpetual Dated Dated

13

ofwhich:Originalmaturitydate

No maturitydate

No maturitydate No maturity date 2024/8/18 2027/10/17

14

Issuer callsubject topriorregulatoryapproval

No No NoYes (subject to

priorregulatoryapproval)

Yes (subject toprior

regulatoryapproval)

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

25

15

ofwhich:Optionalcall date,contingentcall datesandredemptionamount (inmillion ofRMB)

- - -2019/8/18,redemption

amount30,000

2022/10/17,Redemption

amount40,000

16

ofwhich:Subsequentcall dates, ifapplicable

- - - - -

Bonus orDividends

17

ofwhich:Fixed orfloatingdividend /bonus

Floating Floating

The coupon rateof the preferenceshares will beadjusted every 5years. Thedividend of thepreference sharesunder theIssuance will bepaid at an agreedfixed coupon rateduring eachdividendadjustmentperiod.

Fixed Fixed

18

ofwhich:coupon rateand anyrelatedindex

Subject to theBoard’s decision

Subject to theBoard’sdecision

Coupon rate of thefirst dividendadjustment periodof the firstissuance ofpreference sharesis 6%. Coupon rateof the firstdividendadjustment periodof the secondissuance ofpreference sharesis 5.5%.

5.80% 4.45%

19

ofwhich:Existence ofa dividendstopper

No No Yes No No

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

26

20

ofwhich:Whetherfullydiscretionary incancellationofbonus ordividend

Fulldiscretionary

Fulldiscretionary Full discretionary Without

discretionaryWithout

discretionary

21

ofwhich:Existence ofstep up orotherincentive toredeem

No No No No No

22

ofwhich:cumulativeornoncumulative

Non-cumulative Non-cumulative Non-cumulative Non-cumulative Non-cumulative

23Convertibleornon-convertible

No No Yes No No

24

ofwhich: Ifconvertible,specifyconversiontrigger(s)

- -

(1) If the CET 1capital adequacyrate of the Bankdecreased to5.125% (or below),the preferencesharesissued will be fullyorpartiallytransferredto ordinary sharesof A share, inorderto make the CET 1capital adequacyrateresumed to above5.125%. In caseof partial transfer,all preferenceshares issued willbe transferred inproportion on thesame conditions.(2) All preferenceshares issued willbe transferred into

-

-

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

27

ordinary shares ofAshare in case of theearlier occurrenceof the followingtwo situations: 1)the CBRCconsidersthat the Bankcouldnot survive in caseno conversion willbe carried out; 2)relevant authorityconsiders that theBank could notsurvive in case nocapital injectionwithpublic departmentsor no provision ofsupport with thesame effectiveness.If the Bankmandatorilytransferthe issuedpreferenceshares to ordinaryshares, it shallreportto the CBRC forinvestigation andmaking decision,and shall performthe obligationsof disclosure oftemporary reportsandannouncementsin accordance withSecurities Law ofthePeople’s RepublicofChina and relevantrequirements of theCSRC.

25

ofwhich: Ifconvertible,fully orpartially

- - Fully or partially - -

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

28

26

ofwhich: Ifconvertible,determinemethods forconversionprice

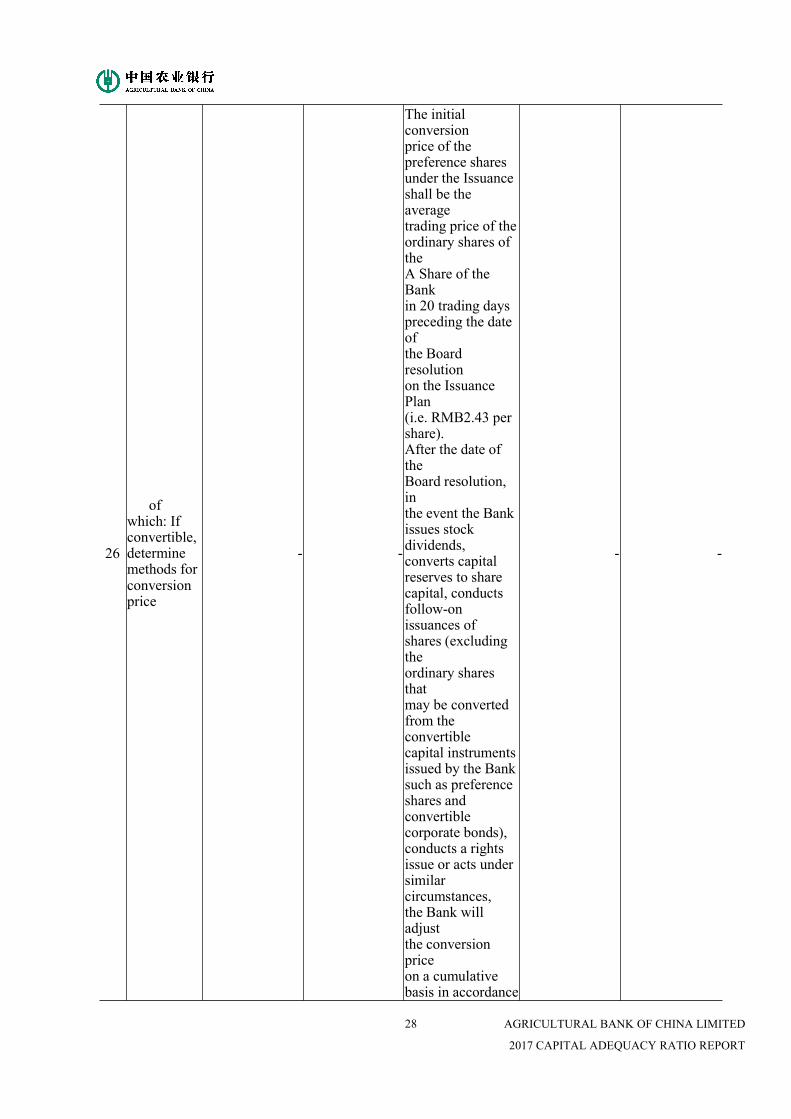

- -

The initialconversionprice of thepreference sharesunder the Issuanceshall be theaveragetrading price of theordinary shares oftheA Share of theBankin 20 trading dayspreceding the dateofthe Boardresolutionon the IssuancePlan(i.e. RMB2.43 pershare).After the date oftheBoard resolution,inthe event the Bankissues stockdividends,converts capitalreserves to sharecapital, conductsfollow-onissuances ofshares (excludingtheordinary sharesthatmay be convertedfrom theconvertiblecapital instrumentsissued by the Banksuch as preferenceshares andconvertiblecorporate bonds),conducts a rightsissue or acts undersimilarcircumstances,the Bank willadjustthe conversionpriceon a cumulativebasis in accordance

- -

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

29

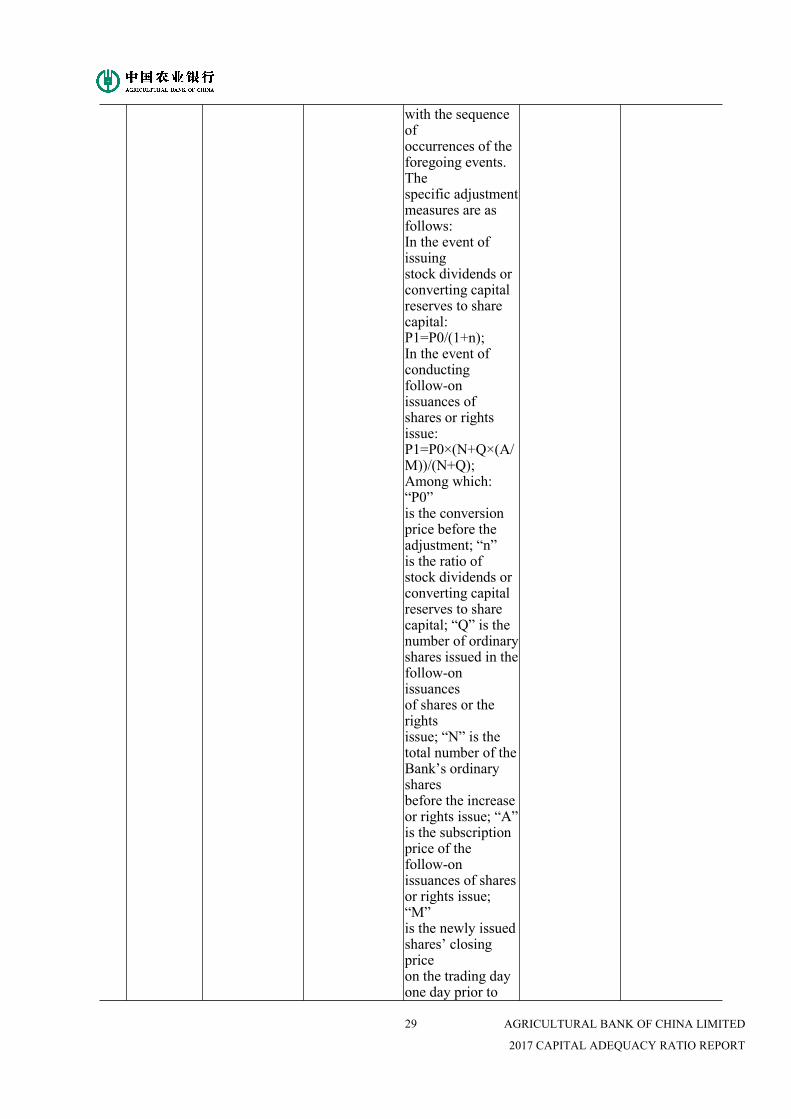

with the sequenceofoccurrences of theforegoing events.Thespecific adjustmentmeasures are asfollows:In the event ofissuingstock dividends orconverting capitalreserves to sharecapital:P1=P0/(1+n);In the event ofconductingfollow-onissuances ofshares or rightsissue:P1=P0×(N+Q×(A/M))/(N+Q);Among which:“P0”is the conversionprice before theadjustment; “n”is the ratio ofstock dividends orconverting capitalreserves to sharecapital; “Q” is thenumber of ordinaryshares issued in thefollow-onissuancesof shares or therightsissue; “N” is thetotal number of theBank’s ordinarysharesbefore the increaseor rights issue; “A”is the subscriptionprice of thefollow-onissuances of sharesor rights issue;“M”is the newly issuedshares’ closingpriceon the trading dayone day prior to

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

30

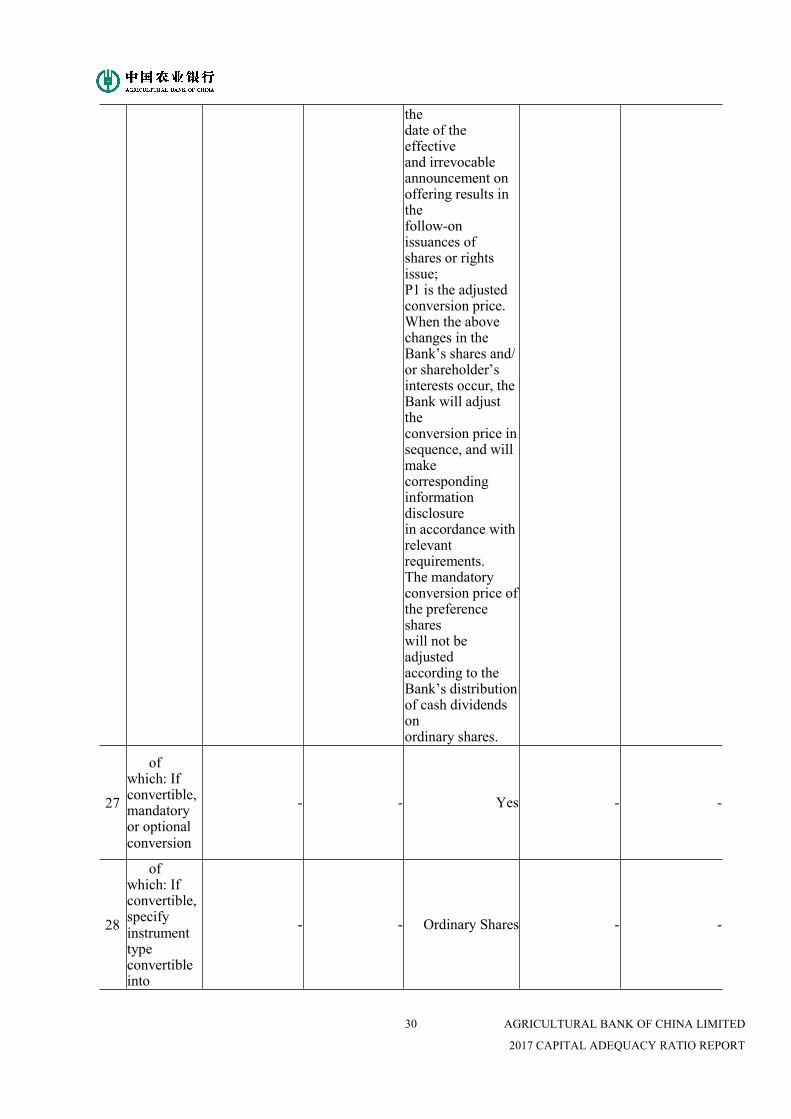

thedate of theeffectiveand irrevocableannouncement onoffering results inthefollow-onissuances ofshares or rightsissue;P1 is the adjustedconversion price.When the abovechanges in theBank’s shares and/or shareholder’sinterests occur, theBank will adjusttheconversion price insequence, and willmakecorrespondinginformationdisclosurein accordance withrelevantrequirements.The mandatoryconversion price ofthe preferenceshareswill not beadjustedaccording to theBank’s distributionof cash dividendsonordinary shares.

27

ofwhich: Ifconvertible,mandatoryor optionalconversion

- - Yes - -

28

ofwhich: Ifconvertible,specifyinstrumenttypeconvertibleinto

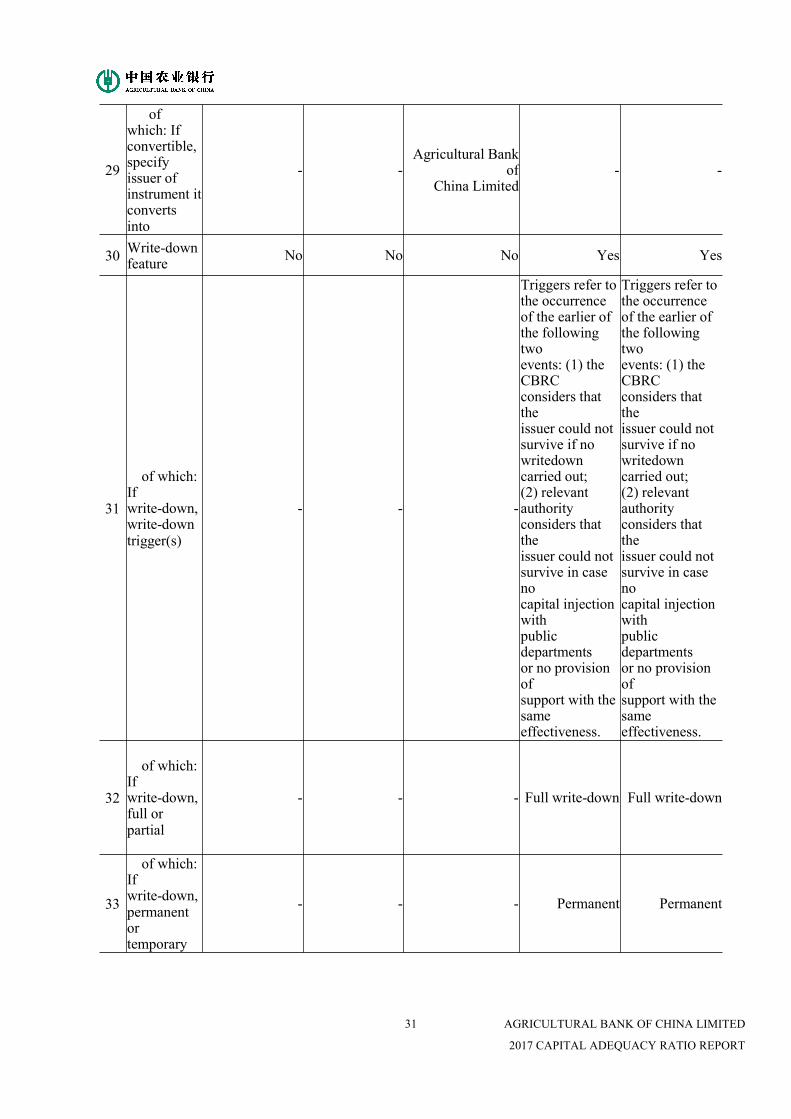

- - Ordinary Shares - -

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

31

29

ofwhich: Ifconvertible,specifyissuer ofinstrument itconvertsinto

- -Agricultural Bank

ofChina Limited

- -

30 Write-downfeature No No No Yes Yes

31

of which:Ifwrite-down,write-downtrigger(s)

- - -

Triggers refer tothe occurrenceof the earlier ofthe followingtwoevents: (1) theCBRCconsiders thattheissuer could notsurvive if nowritedowncarried out;(2) relevantauthorityconsiders thattheissuer could notsurvive in casenocapital injectionwithpublicdepartmentsor no provisionofsupport with thesameeffectiveness.

Triggers refer tothe occurrenceof the earlier ofthe followingtwoevents: (1) theCBRCconsiders thattheissuer could notsurvive if nowritedowncarried out;(2) relevantauthorityconsiders thattheissuer could notsurvive in casenocapital injectionwithpublicdepartmentsor no provisionofsupport with thesameeffectiveness.

32

of which:Ifwrite-down,full orpartial

- - - Full write-down Full write-down

33

of which:Ifwrite-down,permanentortemporary

- - - Permanent Permanent

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

32

34

ofwhich: Iftemporarywrite-down,descriptionof write-upmechanism

- - - - -

35

Position insubordinationhierarchy inliquidation(instrumenttypeimmediatelysenior toinstrument)

Subordinate tothedepositors,creditors,junior debt andAdditional Tier1capitalinstruments

Subordinate tothedepositors,creditors,junior debt andAdditional Tier1capitalinstruments

Subordinate to thedepositors,creditors,junior debt, priorto CET 1 capitalinstruments

Subordinate tothedepositors,creditors,junior debt,priorto CET 1 capitalinstruments

Subordinate tothedepositors,creditors,junior debt, priorto CET 1 capitalinstruments

36Non-eligibletransitionedfeatures

No No No No No

37

of which:If yes,specifynon-eligiblefeatures

- - - - -

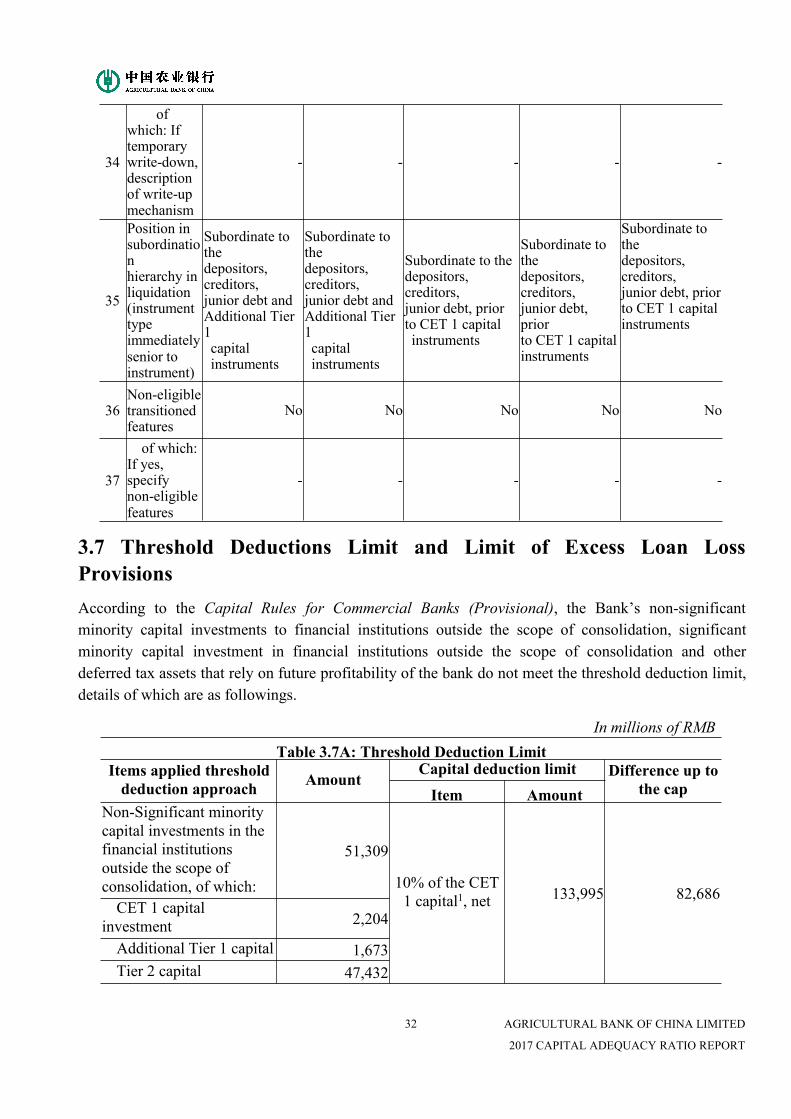

3.7 Threshold Deductions Limit and Limit of Excess Loan LossProvisionsAccording to the Capital Rules for Commercial Banks (Provisional), the Bank’s non-significantminority capital investments to financial institutions outside the scope of consolidation, significantminority capital investment in financial institutions outside the scope of consolidation and otherdeferred tax assets that rely on future profitability of the bank do not meet the threshold deduction limit,details of which are as followings.

In millions of RMBTable 3.7A: Threshold Deduction Limit

Items applied thresholddeduction approach Amount

Capital deduction limit Difference up tothe capItem Amount

Non-Significant minoritycapital investments in thefinancial institutionsoutside the scope ofconsolidation, of which:

51,309

10% of the CET1 capital1, net 133,995 82,686

CET 1 capitalinvestment 2,204

Additional Tier 1 capital 1,673Tier 2 capital 47,432

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

33

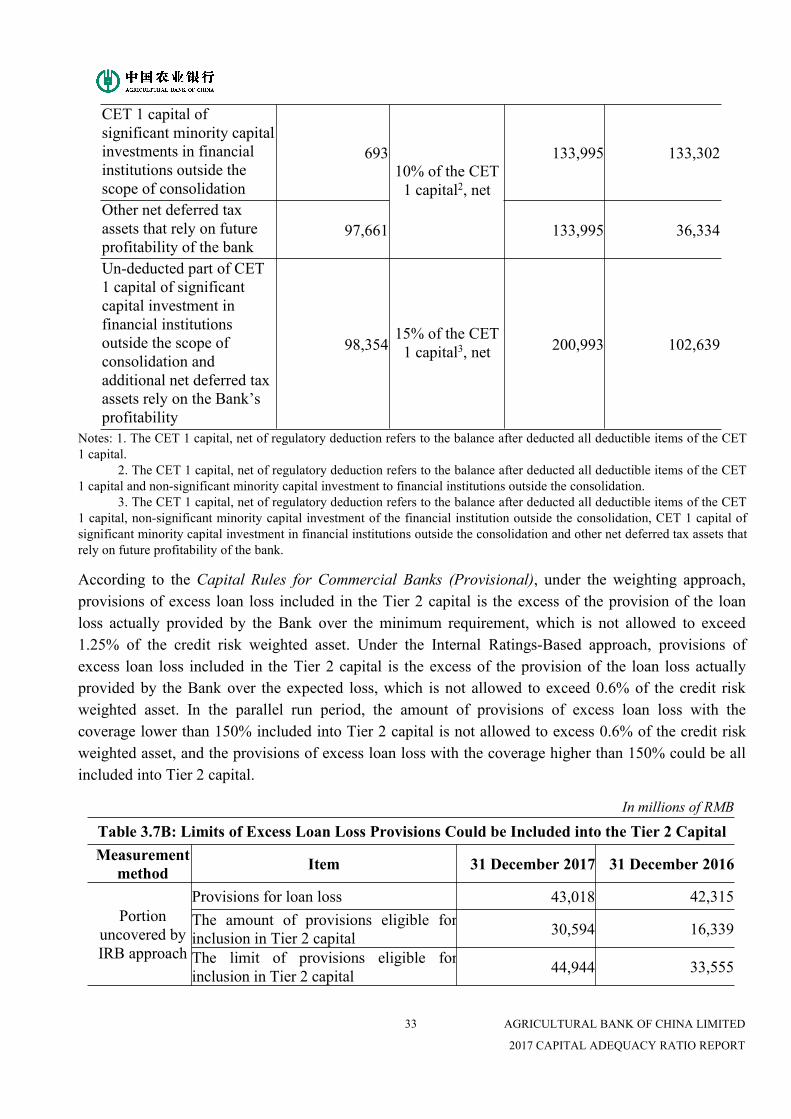

CET 1 capital ofsignificant minority capitalinvestments in financialinstitutions outside thescope of consolidation

69310% of the CET1 capital2, net

133,995 133,302

Other net deferred taxassets that rely on futureprofitability of the bank

97,661 133,995 36,334

Un-deducted part of CET1 capital of significantcapital investment infinancial institutionsoutside the scope ofconsolidation andadditional net deferred taxassets rely on the Bank’sprofitability

98,35415% of the CET1 capital3, net 200,993 102,639

Notes: 1. The CET 1 capital, net of regulatory deduction refers to the balance after deducted all deductible items of the CET1 capital.

2. The CET 1 capital, net of regulatory deduction refers to the balance after deducted all deductible items of the CET1 capital and non-significant minority capital investment to financial institutions outside the consolidation.

3. The CET 1 capital, net of regulatory deduction refers to the balance after deducted all deductible items of the CET1 capital, non-significant minority capital investment of the financial institution outside the consolidation, CET 1 capital ofsignificant minority capital investment in financial institutions outside the consolidation and other net deferred tax assets thatrely on future profitability of the bank.

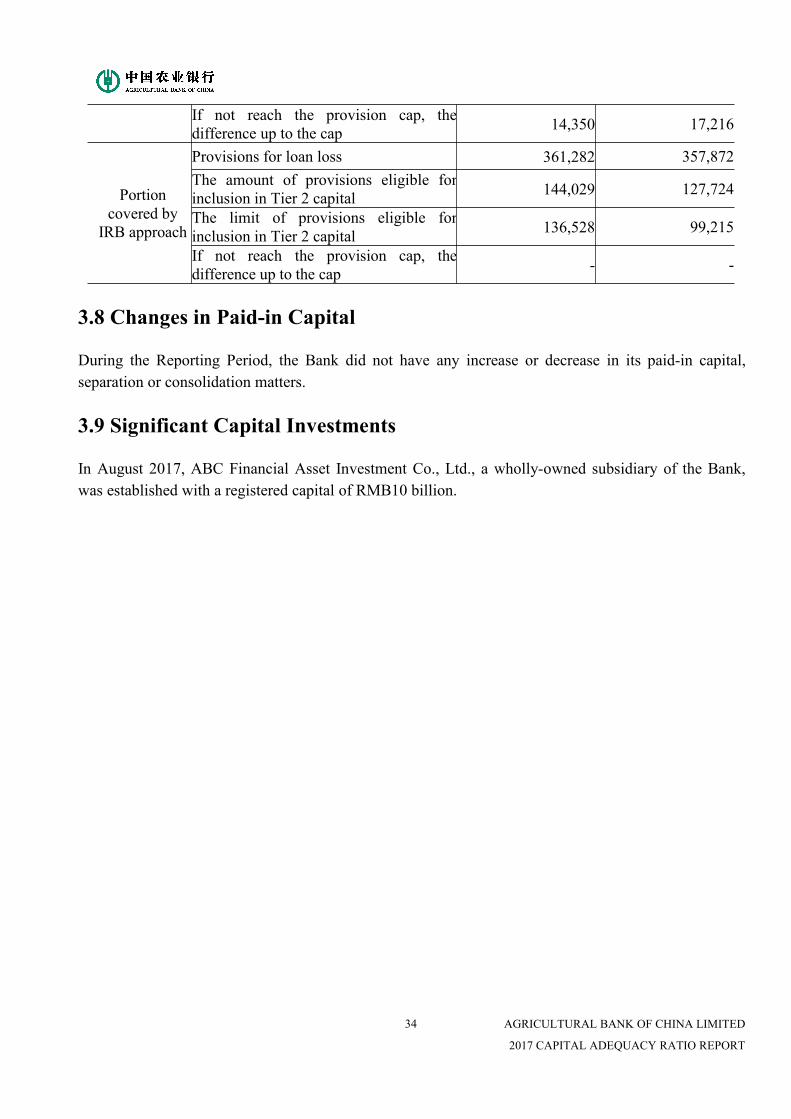

According to the Capital Rules for Commercial Banks (Provisional), under the weighting approach,provisions of excess loan loss included in the Tier 2 capital is the excess of the provision of the loanloss actually provided by the Bank over the minimum requirement, which is not allowed to exceed1.25% of the credit risk weighted asset. Under the Internal Ratings-Based approach, provisions ofexcess loan loss included in the Tier 2 capital is the excess of the provision of the loan loss actuallyprovided by the Bank over the expected loss, which is not allowed to exceed 0.6% of the credit riskweighted asset. In the parallel run period, the amount of provisions of excess loan loss with thecoverage lower than 150% included into Tier 2 capital is not allowed to excess 0.6% of the credit riskweighted asset, and the provisions of excess loan loss with the coverage higher than 150% could be allincluded into Tier 2 capital.

In millions of RMB

Table 3.7B: Limits of Excess Loan Loss Provisions Could be Included into the Tier 2 CapitalMeasurement

method Item 31 December 2017 31 December 2016

Portionuncovered byIRB approach

Provisions for loan loss 43,018 42,315The amount of provisions eligible forinclusion in Tier 2 capital 30,594 16,339

The limit of provisions eligible forinclusion in Tier 2 capital 44,944 33,555

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

34

If not reach the provision cap, thedifference up to the cap 14,350 17,216

Portioncovered by

IRB approach

Provisions for loan loss 361,282 357,872The amount of provisions eligible forinclusion in Tier 2 capital 144,029 127,724

The limit of provisions eligible forinclusion in Tier 2 capital 136,528 99,215

If not reach the provision cap, thedifference up to the cap - -

3.8 Changes in Paid-in Capital

During the Reporting Period, the Bank did not have any increase or decrease in its paid-in capital,separation or consolidation matters.

3.9 Significant Capital Investments

In August 2017, ABC Financial Asset Investment Co., Ltd., a wholly-owned subsidiary of the Bank,was established with a registered capital of RMB10 billion.

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

35

4 Credit Risk

4.1 Credit Risk Management

Credit risk is the risk of economic loss arising from a counterparty’s failure to fulfill its obligationsunder an agreed covenant. The Bank is exposed to credit risk primarily from our loan portfolio,investment portfolio, guarantee business and various other on- and off-balance sheet credit riskexposures. The Bank’s objectives of credit risk management are to adhere to its risk appetite, andassume appropriate level of credit risk and earn returns commensurate with respective risks assumedbased on its credit risk management capability and capital level, as well as to lower and control the lossfor risk as a result of the default of obligators or counterparties, or the downgrading of credit rating orthe weakening of contractual capability.

The Bank gradually established and consummated a clear, scientific and applicable and comprehensivecredit risk management policy system which included basic policies, systems and measures, based onneeds of business development and comprehensive risk management of the Bank. The basic policies ofcredit risk management mainly covered the industry-specific credit, professional reviewing andapproval, risk categorization, transaction control, code of conduct, capital insurance, etc., which servedas the fundamental standard for credit risk management of the Bank as well as the fundamental basis forsetting out management measures. Under the basic policies, sound systems and measures of credit riskmanagement including credit reviewing and approval, limit management, internal rating, creditauthority, draw-down management, collateral management, post-lending management, disposal orwrite-offs, etc. were established to make sure each risk management activity complying withregulations. In addition, the Bank continuously clarified and perfected the specific managementmeasures and operation procedures of each business, product, customer operation for each departmentand business line, ensuring that the credit risk management system be comprehensively implemented.

The Bank authorized presidents of branches to conduct business and delegation according to the riskmanagement capability of the branches, and all businesses undertaking credit risk should be conductedin accordance with procedures and permissions. The Bank designed and implemented the basic processof credit underwriting, i.e. customer’s application and acceptance → business investigation (evaluation)→ business examination, reviewed by credit approval committee and approval by authorized person →(filing) → business implementation → post-business management → (management of non-performingassets) → recovery of loans, based on credit scale, complexity, and risk characteristics on the basicprinciples of “separating the loan initiation from approval, adopting checks and balance, achievingsymmetry between powers and responsibilities, and maintaining clarity and efficiency”. The Bankimplemented customer layering management. Customer management bank was determined by therequirement of customer maintenance and risk management. The business department of the customermanagement bank led daily management of customers. Credit management department and riskmanagement department at all levels supervised and controlled customer risks, oversaw thepost-lending management of business departments, until the loan recovered upon the expiry of business.

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

36

Where there was non-performing assets (including loan), disposal department of non-performing loanwould take over the non-performing assets under required procedures and permissions by variousdisposal means.

The Bank assesses the recoverability of loans due and classifies the loans by taking account of principlefactors, including the borrower’s repayment capacity, repayment record, willingness to repay the loan,profitability of the loan project, and the reliability of the secondary repayment source in accordancewith the Guidelines of Loan Credit Risk Classification issued by the CBRC. The Bank classifies itsloans into five categories, namely normal, special mention, substandard, doubtful and loss, in whichloans classified as substandard, doubtful and loss are regarded as non-performing loans. Overdue loansrefer to loans that customers fail to repay the principal or interest in accordance with the maturity datesstipulated in the contracts. The recognition and provision for impairment losses on loans are assessedindividually and collectively. Provision made individually represents the aggregate allowance forimpairment losses from corporate loans classified as substandard, doubtful and loss. Provision madecollectively represents the aggregate allowance for impairment losses provided for corporate loansclassified as normal and special mention, as well as retail loans (including card overdraft).

In 2017, the Bank actively supported the development of real economy and adhered to the supply-sidestructural reform and key national development strategies by making more efforts in providing creditsto key areas, projected related to people’s livelihood and under-attended areas. The Bank suppressedcredits to industries with overcapacity and high risks and proceeded to optimize and adjust creditstructure and improved the quality of credit assets by refining certain policies regarding classification ofloan risks, carrying out investigations on customer default, reviewing the ratings of clients, adjustingthe measurement of economic capital based on actual situation and strengthening limit management ofindustry-specific exposures. The Bank conducted special rectification programs to address risks ofcredit assets by focusing on key areas such as risky customers taking out large loans, hidden groupcustomers, and credit business authenticity. The Bank continued to strengthen the management ofglobal credit extension and consolidated credit granting, enhance risk management of local governmentdebt and emerging businesses, and therefore resulting in an enhancement in the overall control of creditrisks. The Bank continuously promoted credit underwriting review, lending approval, establishment ofthe risk supervision center. Besides, the centralization and professionalism of management have beenenhanced, thus laying a solid foundation for credit management.

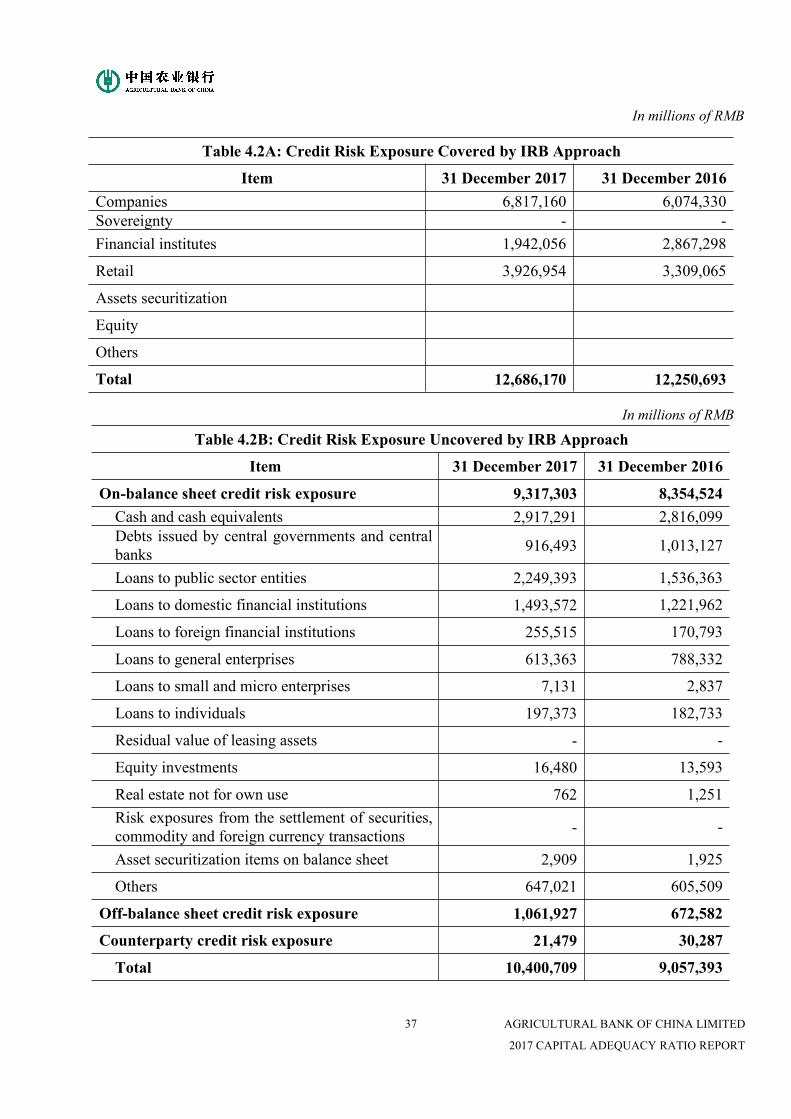

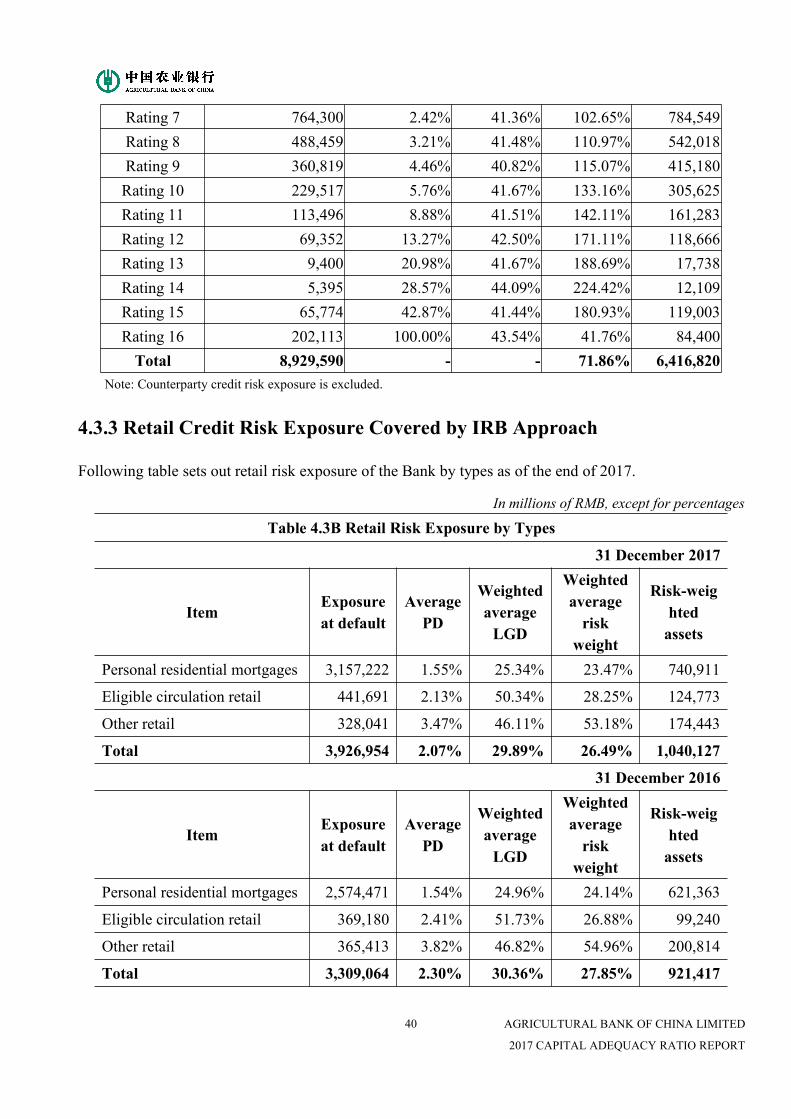

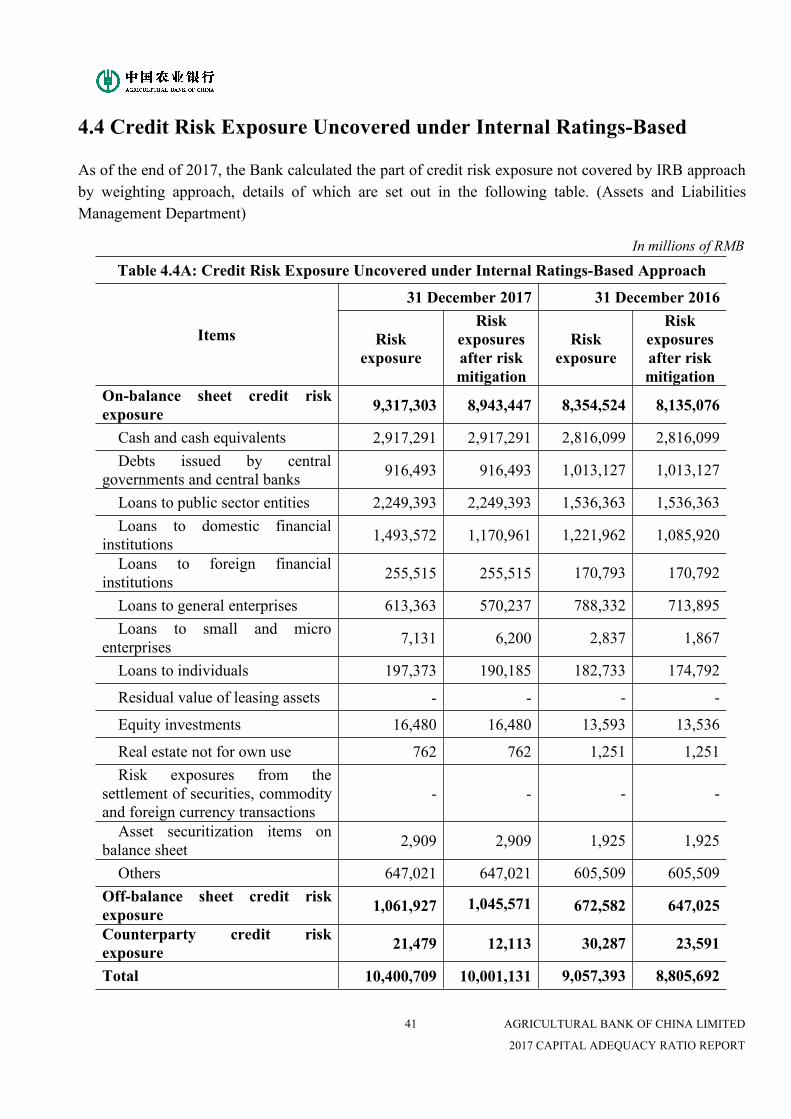

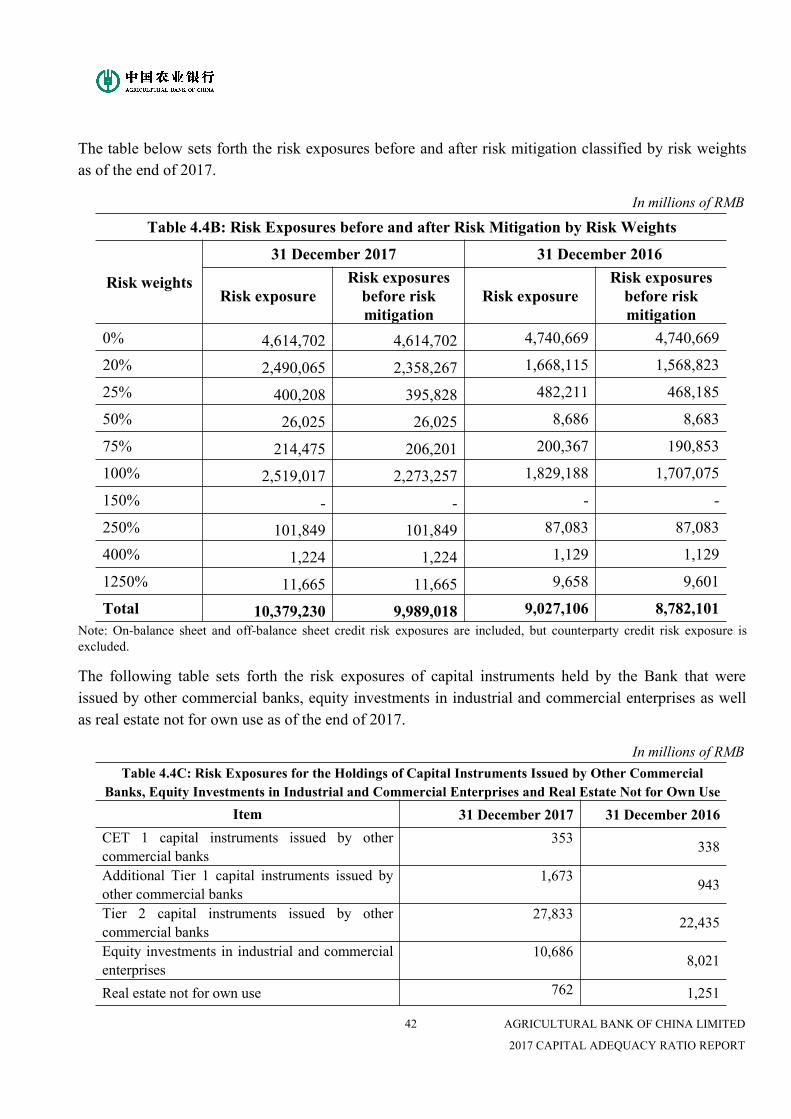

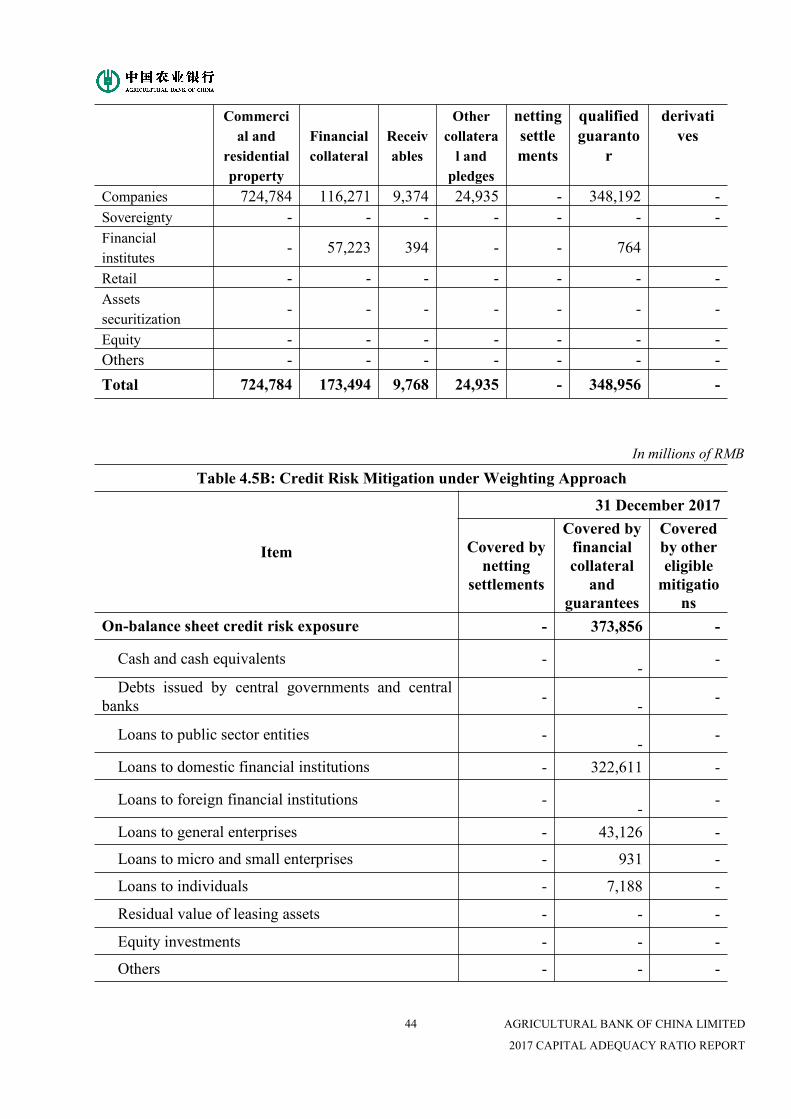

4.2 Credit Risk Exposure

During the Reporting Period, the Bank calculates the non-retail credit risk-weighted assets byfoundation Internal Ratings-Based approach (IRB). As for risk exposure of company and financialinstitution, the Bank adopted the Internal Ratings-Based approach (IRB) for retail credit risk-weightedassets and the weighting approach for the part of credit risk-weighted assets not covered by IRBapproach with approval from the regulatory authorities. (Assets and Liabilities ManagementDepartment)

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

37

In millions of RMB

Table 4.2A: Credit Risk Exposure Covered by IRB Approach

Item 31 December 2017 31 December 2016Companies 6,817,160 6,074,330Sovereignty - -Financial institutes 1,942,056 2,867,298

Retail 3,926,954 3,309,065

Assets securitization

Equity

Others

Total 12,686,170 12,250,693

In millions of RMB

Table 4.2B: Credit Risk Exposure Uncovered by IRB Approach

Item 31 December 2017 31 December 2016

On-balance sheet credit risk exposure 9,317,303 8,354,524Cash and cash equivalents 2,917,291 2,816,099Debts issued by central governments and centralbanks 916,493 1,013,127

Loans to public sector entities 2,249,393 1,536,363

Loans to domestic financial institutions 1,493,572 1,221,962

Loans to foreign financial institutions 255,515 170,793

Loans to general enterprises 613,363 788,332

Loans to small and micro enterprises 7,131 2,837

Loans to individuals 197,373 182,733

Residual value of leasing assets - -

Equity investments 16,480 13,593

Real estate not for own use 762 1,251Risk exposures from the settlement of securities,commodity and foreign currency transactions - -

Asset securitization items on balance sheet 2,909 1,925

Others 647,021 605,509

Off-balance sheet credit risk exposure 1,061,927 672,582

Counterparty credit risk exposure 21,479 30,287

Total 10,400,709 9,057,393

AGRICULTURAL BANK OF CHINA LIMITED

2017 CAPITAL ADEQUACY RATIO REPORT

38

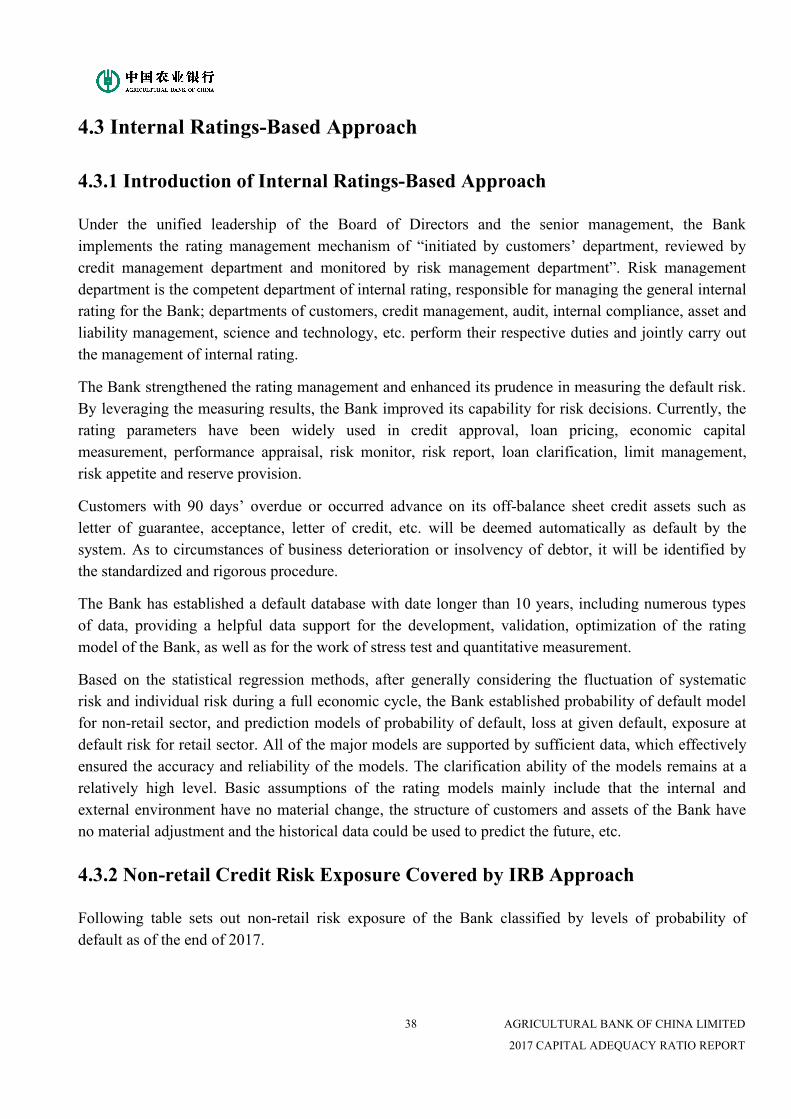

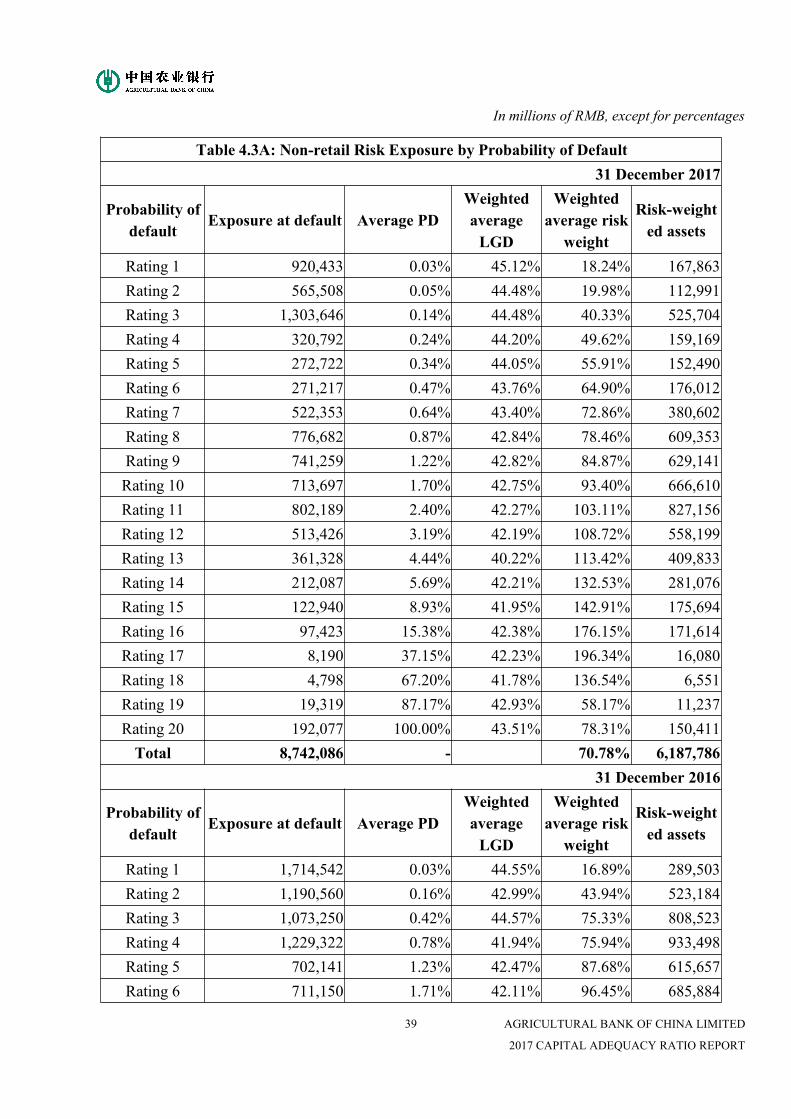

4.3 Internal Ratings-Based Approach

4.3.1 Introduction of Internal Ratings-Based Approach

Under the unified leadership of the Board of Directors and the senior management, the Bankimplements the rating management mechanism of “initiated by customers’ department, reviewed bycredit management department and monitored by risk management department”. Risk managementdepartment is the competent department of internal rating, responsible for managing the general internalrating for the Bank; departments of customers, credit management, audit, internal compliance, asset andliability management, science and technology, etc. perform their respective duties and jointly carry outthe management of internal rating.

The Bank strengthened the rating management and enhanced its prudence in measuring the default risk.By leveraging the measuring results, the Bank improved its capability for risk decisions. Currently, therating parameters have been widely used in credit approval, loan pricing, economic capitalmeasurement, performance appraisal, risk monitor, risk report, loan clarification, limit management,risk appetite and reserve provision.