Embed Size (px)

Citation preview

《如何準備第一份環境、社會及管治報告》研討會

《環境、社會及管治報告》的常見錯誤及第三方認證

MR. WK WONG

黃偉國先生

如何進行ESG報告的第三方認證

在ESG報告中的常見錯誤

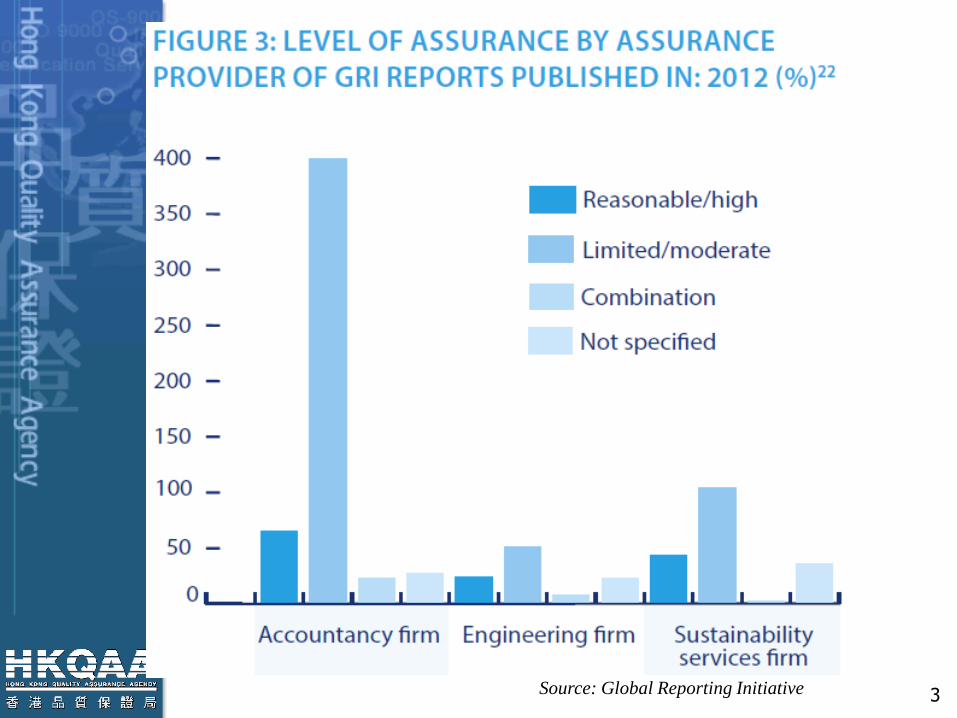

3 Source: Global Reporting Initiative

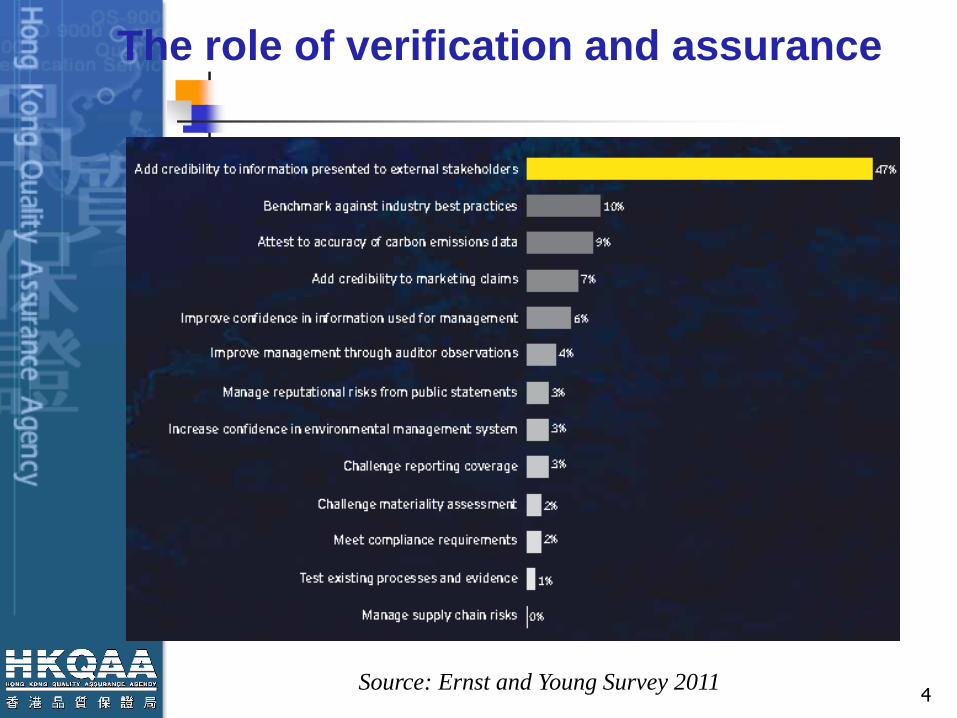

The role of verification and assurance

4 Source: Ernst and Young Survey 2011

REPORT VERIFICATION

PROCESS

5

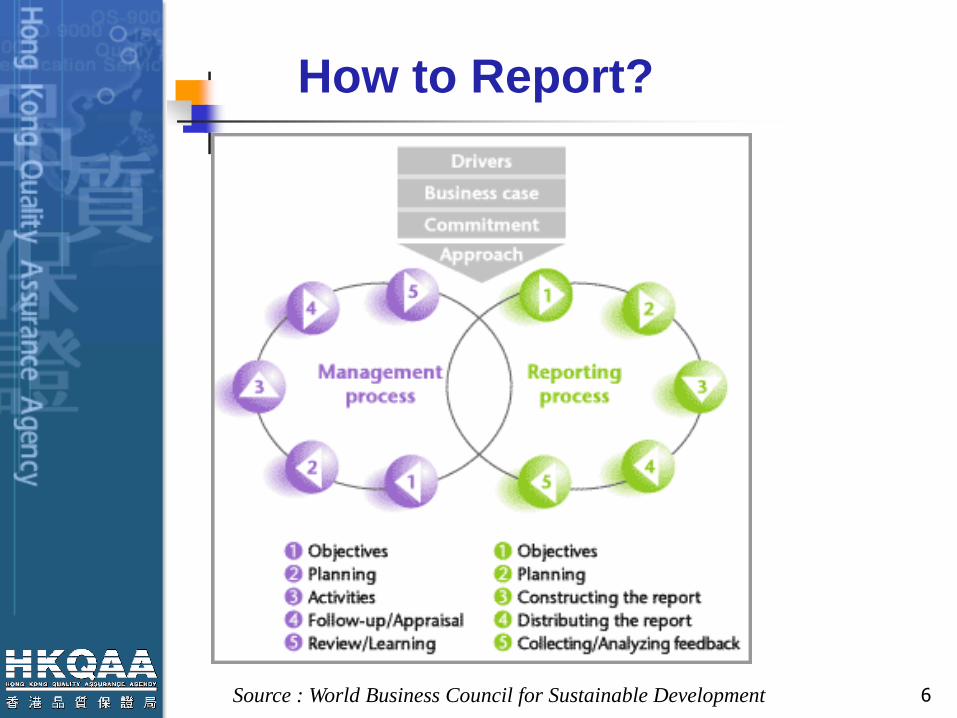

How to Report?

6 Source : World Business Council for Sustainable Development

Objectives of Verification

To provide assurance of the sustainability performance data / information stated in the report against adherence to the reporting principles:

◦ Report Content Stakeholder Inclusiveness, Sustainability Context,

Materiality, Completeness

◦ Report Quality Balance, Comparability, Accuracy, Timeliness, Clarity,

Reliability

To map the report against the application level / “in accordance” of GRI’s GX Sustainability Reporting Guidelines

To make recommendations for future improvement

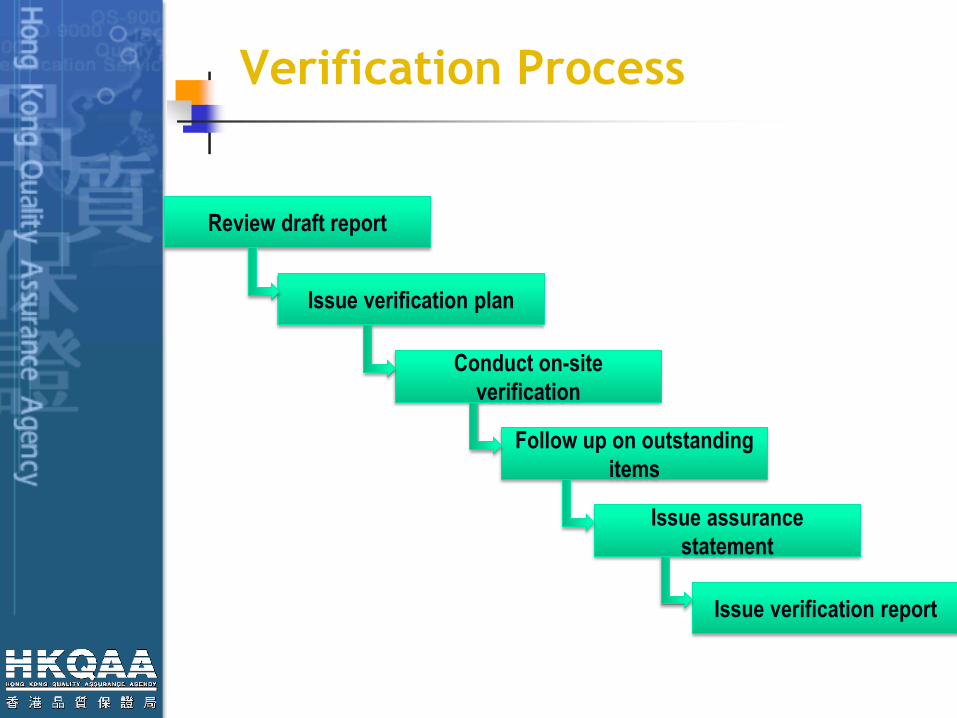

Verification Process

Review draft report

Issue verification plan

Conduct on-site

verification

Follow up on outstanding

items

Issue assurance

statement

Issue verification report

9

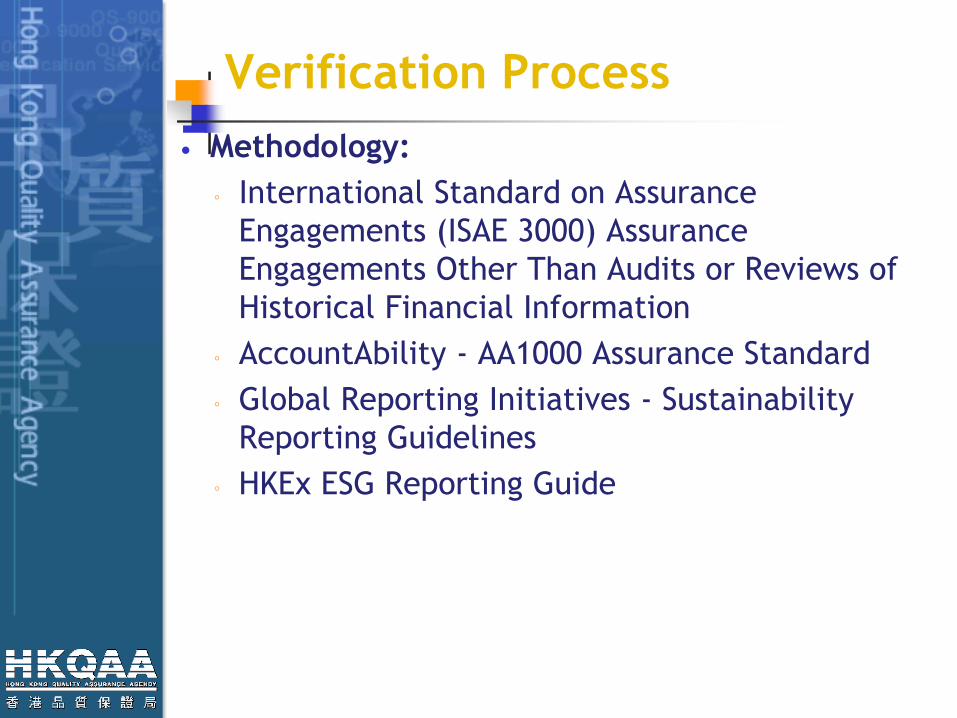

Verification Process

Methodology:

◦ International Standard on Assurance

Engagements (ISAE 3000) Assurance

Engagements Other Than Audits or Reviews of

Historical Financial Information

◦ AccountAbility - AA1000 Assurance Standard

◦ Global Reporting Initiatives - Sustainability

Reporting Guidelines

◦ HKEx ESG Reporting Guide

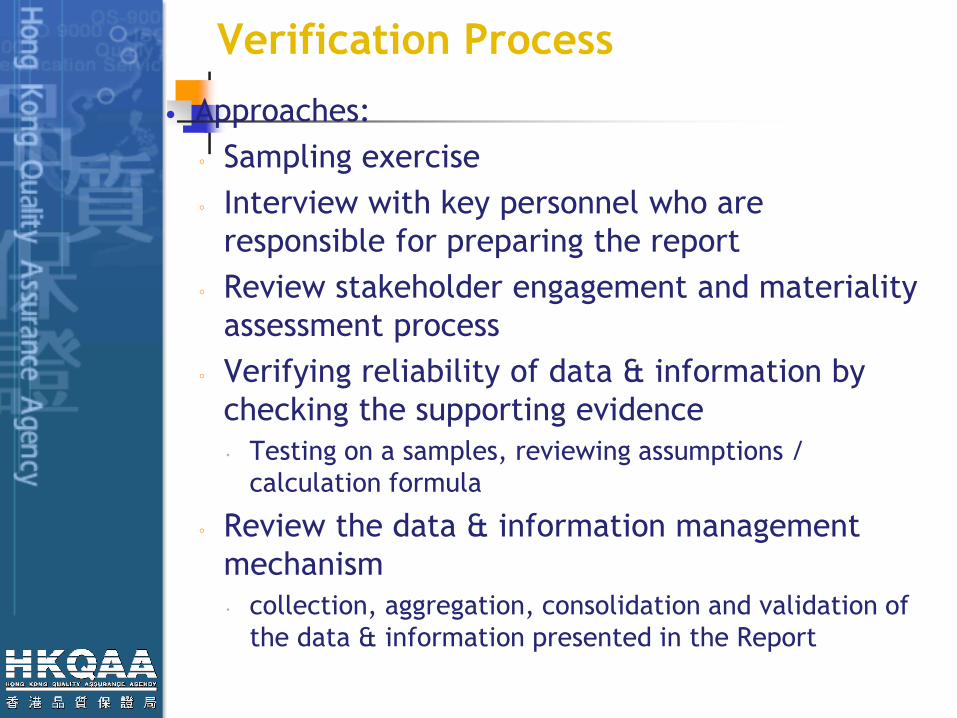

Verification Process

Approaches:

◦ Sampling exercise

◦ Interview with key personnel who are

responsible for preparing the report

◦ Review stakeholder engagement and materiality

assessment process

◦ Verifying reliability of data & information by

checking the supporting evidence

Testing on a samples, reviewing assumptions /

calculation formula

◦ Review the data & information management

mechanism

collection, aggregation, consolidation and validation of

the data & information presented in the Report

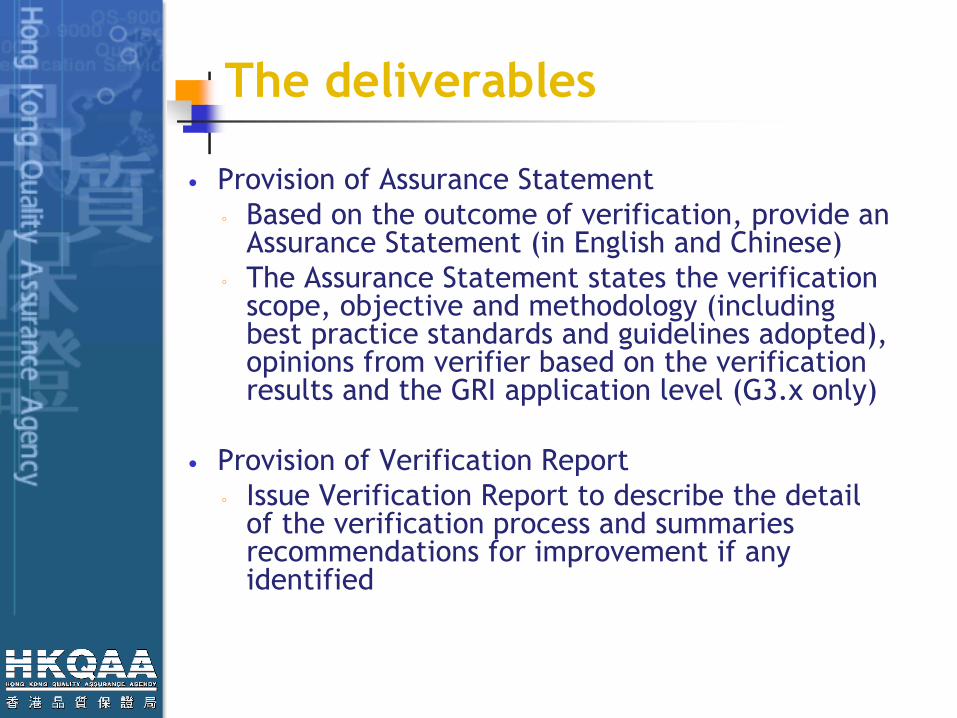

The deliverables

Provision of Assurance Statement

◦ Based on the outcome of verification, provide an Assurance Statement (in English and Chinese)

◦ The Assurance Statement states the verification scope, objective and methodology (including best practice standards and guidelines adopted), opinions from verifier based on the verification results and the GRI application level (G3.x only)

Provision of Verification Report

◦ Issue Verification Report to describe the detail of the verification process and summaries recommendations for improvement if any identified

13

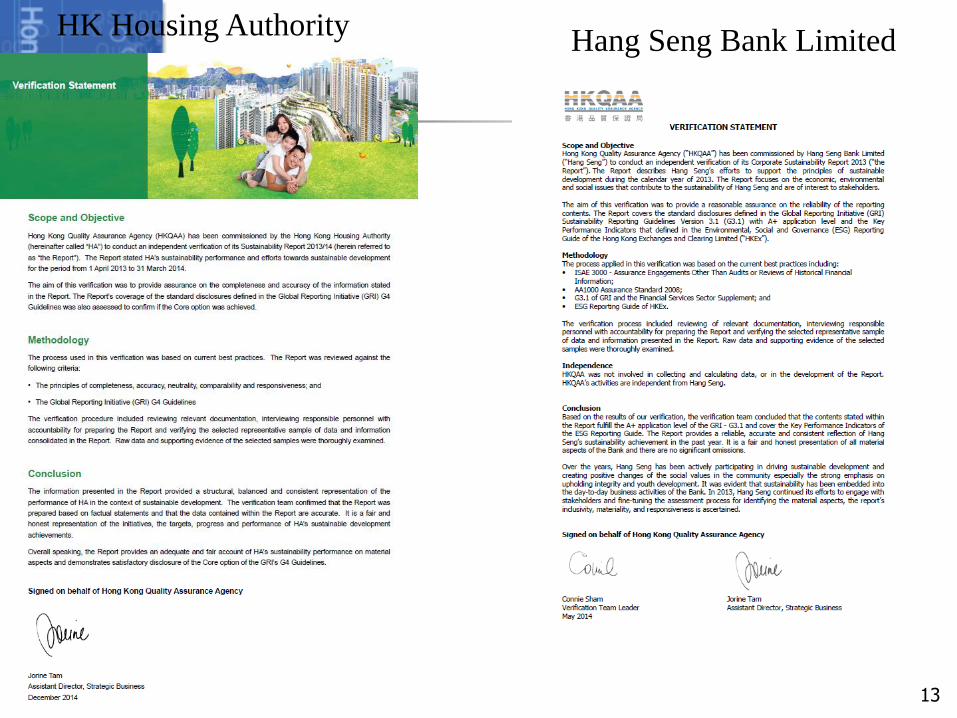

HK Housing Authority Hang Seng Bank Limited

14

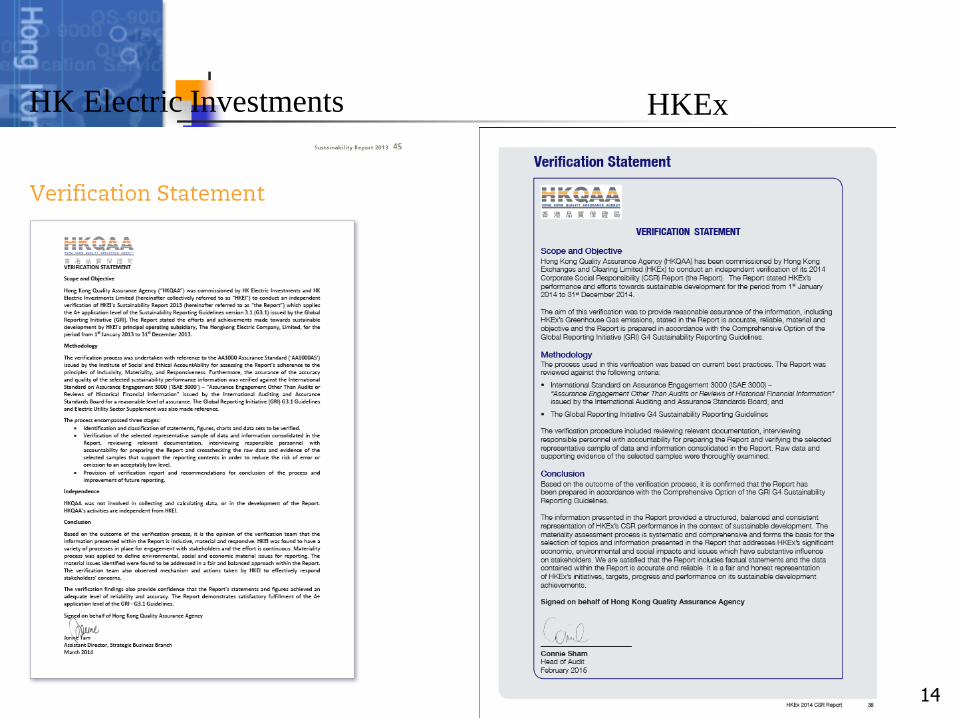

HK Electric Investments HKEx

15

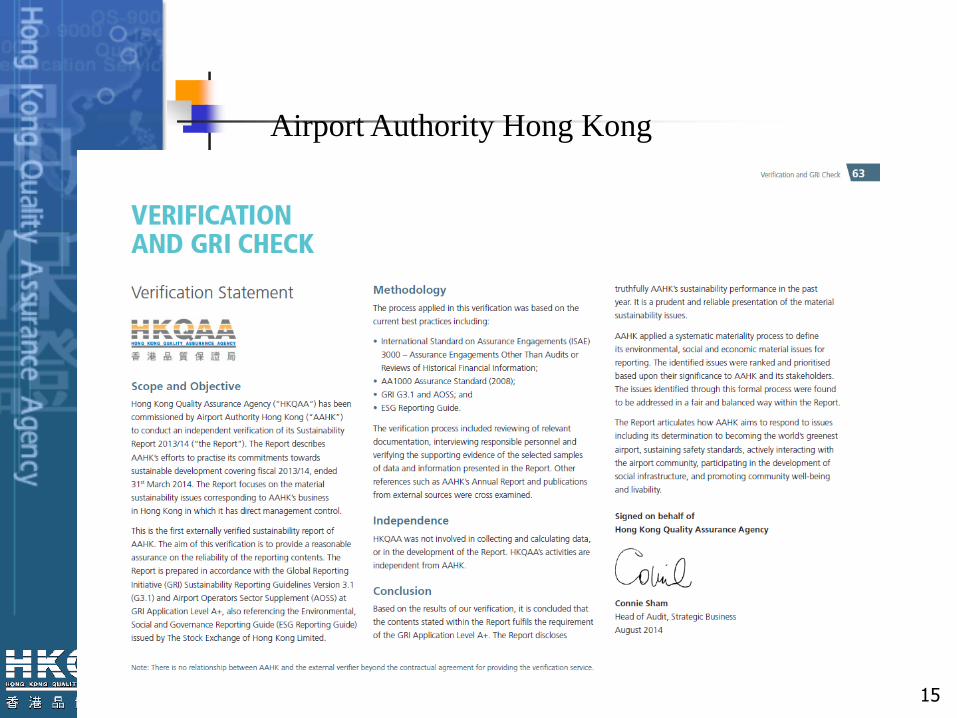

Airport Authority Hong Kong

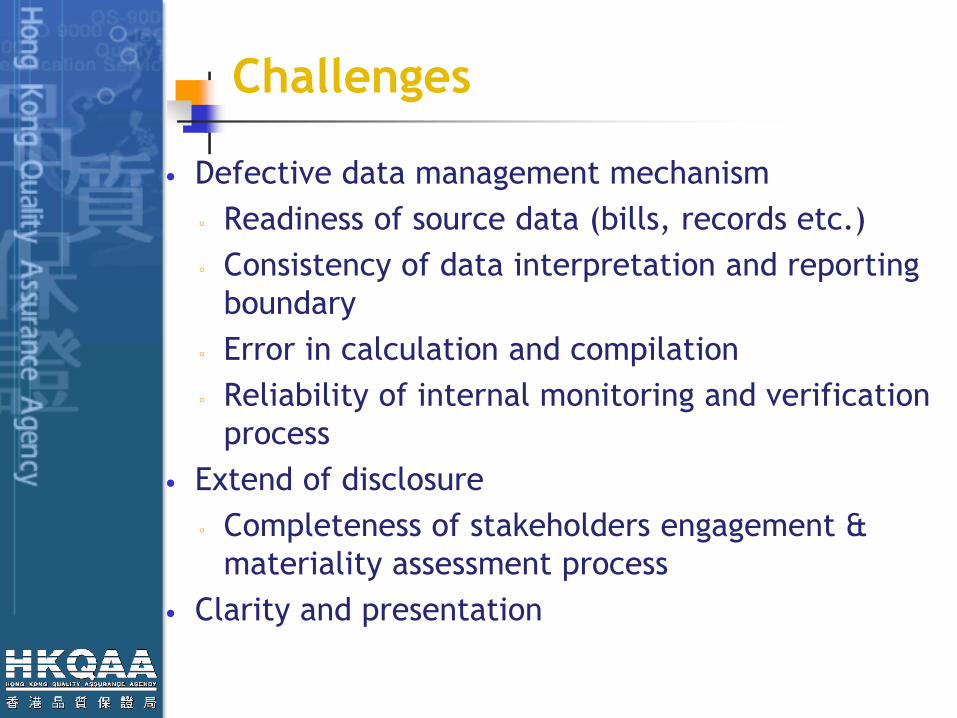

Challenges

Defective data management mechanism

◦ Readiness of source data (bills, records etc.)

◦ Consistency of data interpretation and reporting

boundary

◦ Error in calculation and compilation

◦ Reliability of internal monitoring and verification

process

Extend of disclosure

◦ Completeness of stakeholders engagement &

materiality assessment process

Clarity and presentation

For Detail: www.hkqaa.org or srr.hkqaa.org

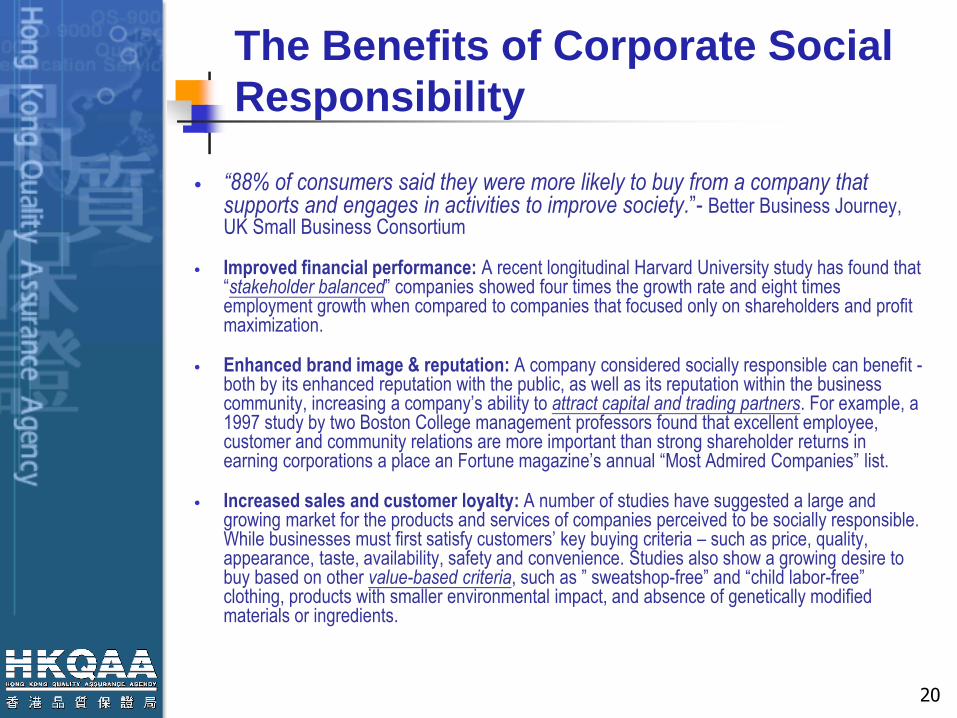

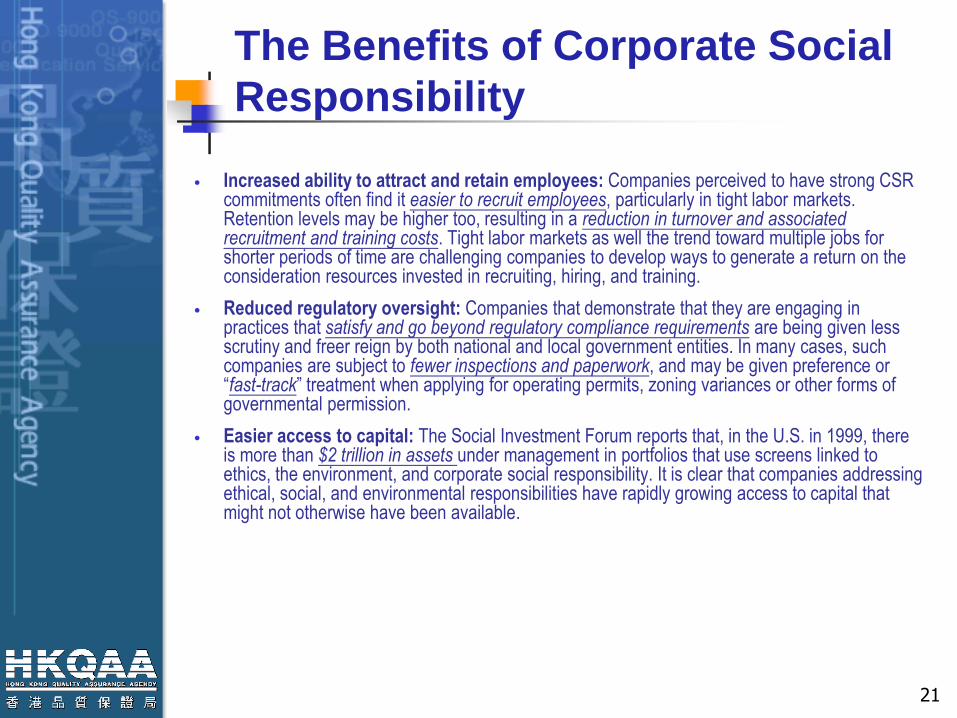

The Benefits of Corporate Social

Responsibility

20

“88% of consumers said they were more likely to buy from a company that supports and engages in activities to improve society.”- Better Business Journey, UK Small Business Consortium

Improved financial performance: A recent longitudinal Harvard University study has found that “stakeholder balanced” companies showed four times the growth rate and eight times employment growth when compared to companies that focused only on shareholders and profit maximization.

Enhanced brand image & reputation: A company considered socially responsible can benefit -both by its enhanced reputation with the public, as well as its reputation within the business community, increasing a company’s ability to attract capital and trading partners. For example, a 1997 study by two Boston College management professors found that excellent employee, customer and community relations are more important than strong shareholder returns in earning corporations a place an Fortune magazine’s annual “Most Admired Companies” list.

Increased sales and customer loyalty: A number of studies have suggested a large and growing market for the products and services of companies perceived to be socially responsible. While businesses must first satisfy customers’ key buying criteria – such as price, quality, appearance, taste, availability, safety and convenience. Studies also show a growing desire to buy based on other value-based criteria, such as ” sweatshop-free” and “child labor-free” clothing, products with smaller environmental impact, and absence of genetically modified materials or ingredients.

The Benefits of Corporate Social

Responsibility

21

Increased ability to attract and retain employees: Companies perceived to have strong CSR commitments often find it easier to recruit employees, particularly in tight labor markets. Retention levels may be higher too, resulting in a reduction in turnover and associated recruitment and training costs. Tight labor markets as well the trend toward multiple jobs for shorter periods of time are challenging companies to develop ways to generate a return on the consideration resources invested in recruiting, hiring, and training.

Reduced regulatory oversight: Companies that demonstrate that they are engaging in practices that satisfy and go beyond regulatory compliance requirements are being given less scrutiny and freer reign by both national and local government entities. In many cases, such companies are subject to fewer inspections and paperwork, and may be given preference or “fast-track” treatment when applying for operating permits, zoning variances or other forms of governmental permission.

Easier access to capital: The Social Investment Forum reports that, in the U.S. in 1999, there is more than $2 trillion in assets under management in portfolios that use screens linked to ethics, the environment, and corporate social responsibility. It is clear that companies addressing ethical, social, and environmental responsibilities have rapidly growing access to capital that might not otherwise have been available.

Why report sustainability?

Urge for sustainable development

Expansion of expectations on transparency and accountability

22

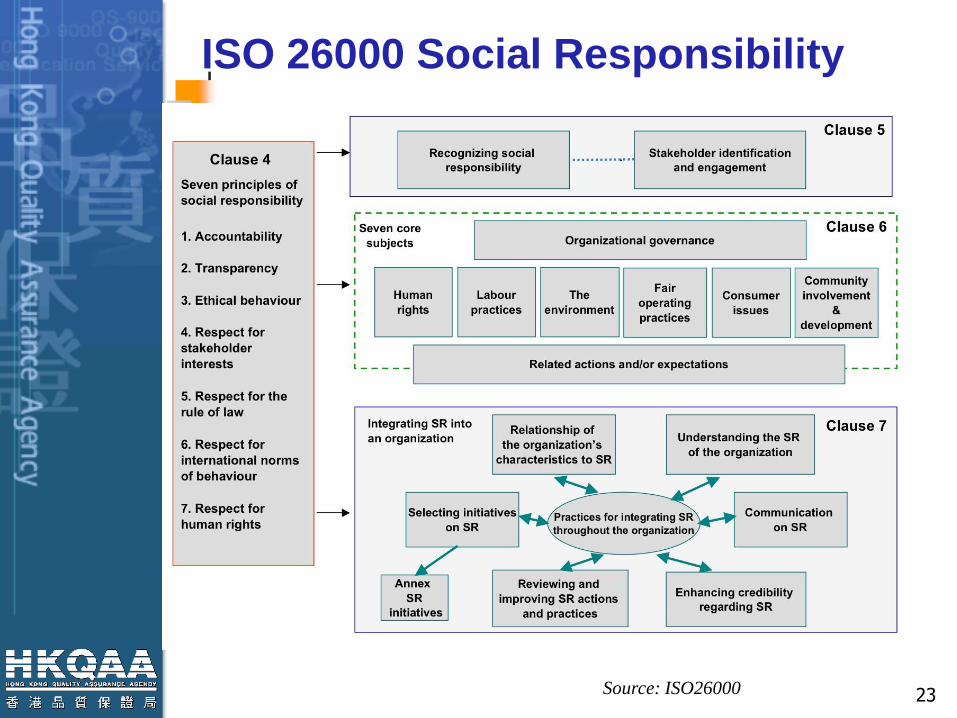

ISO 26000 Social Responsibility

23 Source: ISO26000

The Global Reporting Initiative (GRI) G4

Guidelines

General Standard Disclosures

• Strategy and Analysis

• Organizational Profile

• Identified Material Aspects and Boundaries

• Stakeholder Engagement

• Report Profile

• Governance

• Ethics and Integrity

Specific Standard Disclosures Overview

• Disclosures on Management Approach

• Economic

• Environmental

• Social

• Labor Practices and Decent Work

• Human Rights

• Society

• Product Responsibility

Source: Global Reporting Initiative

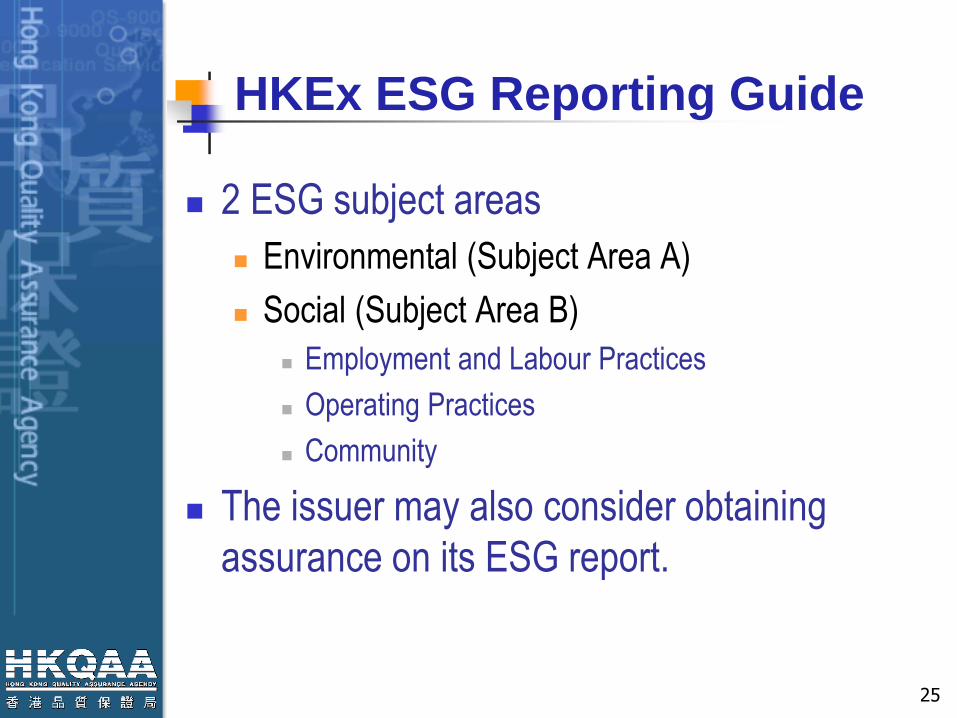

HKEx ESG Reporting Guide

2 ESG subject areas

Environmental (Subject Area A)

Social (Subject Area B)

Employment and Labour Practices

Operating Practices

Community

The issuer may also consider obtaining

assurance on its ESG report.

25

![[FR] trendwatching.com’s VIRGIN CONSUMERS](https://img.pdfslide.tips/doc/110x75/558a1ef0d8b42af6448b459a/fr-trendwatchingcoms-virgin-consumers.jpg)

![[PT] trendwatching.com’s VIRGIN CONSUMERS](https://img.pdfslide.tips/doc/110x75/54bf9a4a4a7959f47f8b464c/pt-trendwatchingcoms-virgin-consumers.jpg)

![[TR] trendwatching.com’s VIRGIN CONSUMERS](https://img.pdfslide.tips/doc/110x75/54917a47b47959962d8b52d1/tr-trendwatchingcoms-virgin-consumers.jpg)

![[KR] trendwatching.com’s VIRGIN CONSUMERS](https://img.pdfslide.tips/doc/110x75/5582efabd8b42a32168b4994/kr-trendwatchingcoms-virgin-consumers.jpg)

![[ES] trendwatching.com’s VIRGIN CONSUMERS](https://img.pdfslide.tips/doc/110x75/54bf99fb4a7959f47f8b463f/es-trendwatchingcoms-virgin-consumers.jpg)