Embed Size (px)

Citation preview

1

Chapter 9 Partnership Goodwill (合夥商譽) 9.2 Goodwill (商譽) Goodwill is the excess of the value of an entire business (企業的整體價值) over the fair value (market value) (公允價值) of its

separate net assets (可分離淨資產). Goodwill is not a separable asset (可分離資產) as it cannot be sold separately (分割出售).

Reasons for the existence of goodwill (商譽的存在的原因) Good reputation (良好的聲譽)

Experienced, efficient and reliable employees (經驗豐富、效率高和可靠的員工)

Good relationships with suppliers and customers (與供應商和顧客有良好關係)

These advantages (優勢) are intangible assets (non-current) (無形非流動) of a business that may contribute to the existence of

goodwill (可導致商譽的形成).

Purchased goodwill (購買商譽) Purchased goodwill is the excess of the purchase price of the acquired business over the fair value of its separable net assets. It will be shown in the books of the buyer as goodwill (顯示在買家的帳簿內) together with other assets and liabilities acquired (連同其

他收購的資產和負債).

Inherent goodwill (內在商譽) Inherent goodwill is the goodwill generated internally (內部產生的商譽), which is not purchased upon the acquisition of another

entity. It should not be shown in the accounting books of a business, unless it is a partnership (除非是合夥,內在商譽不應展示在

企業的帳目上).

9.3 Valuation of goodwill (商譽計價) There is no uniform method of valuing goodwill. Some common methods (一些常用的方法) are illustrated as follow:

1 Average sales method (平均銷貨法) Goodwill is valued as a multiple of the average annual sales over a number of past years (商譽價值按過去若干年的平均銷貨額,

乘以某個倍數計算). This method is particularly applicable to trading business (此方法特別適用於從事貨品買賣的企業).

Example 1

If the goodwill is to be valued at four year’s purchase of the average annual sales of the business over last three years, we have Year Yearly sales $ 2008 120,000 2009 140,000 2010 160,000

420,000

2 Average fee income method (平均服務費收益法) Goodwill is valued as a multiple of the average annual fee income over a number of past years (商譽價值按過去數年的平均服務

費收益,乘以某個倍數計算). This method is particularly applicable to professional service business (此方法特別適用於從事專業

服務行業的企業).

Example 2

If the goodwill is to be valued at four year ’s purchase of the average annual fee income of the business over last four years, we have Year Yearly fee income $ 2007 100,000 2008 140,000 2009 180,000 2010 220,000

640,000

Name : _________________ Serial No: _____

Average annual sales = $420,000 ÷ 3 = $140,000

Goodwill = Average annual sales x No. of years’ purchase

= $140,000x4 = $560,000

Average annual fee income = $640,000 ÷ 4 = $160,000

Goodwill = Average annual fee income x No. of years’ purchase

= $160,000x3 = $480,000

2

3 Average net profit method (平均純利法) Goodwill is valued as a multiple of the average annual net profit over a number of past years (商譽價值按過去數年的平均純利,

乘以某個倍數計算). This method is particularly applicable to any type of business (此方法適用於任何類型的企業).

Example 3

If the goodwill is to be valued at two year’s purchase of the average annual net profit of the business over last four years, we have

Average annual net profit = $270,000 ÷ 4 = $67,500

Goodwill = Average annual net profit x No. of years’ purchase

= $67,500x2 = $135,000

= $135,000

Class work 1

Goodwill was to be valued at two years’ purchase of the last five years’ average net profits. The net profits for the last five years were as follows:

4 Average super profit method (平均超越利潤法) The net profit used in the above method is not true profit. This is because the net profit has not taken into the account the following factors: (a) Value of time and effort contributed by the owner(s). (salaries to partnership) (東主付出的時間、心血的價值)

(b) Value of alternative use of capital contributed by the owner(s). (opportunity cost) (東主投入的資本的應得回報)

Super profit (超越利潤) is the amount left after deducting the above two items from net profit (從純利扣除上述兩項). Goodwill

is then valued as multiple of the average annual super profit over a number of past years (商譽價值便按過去數年的平均超越利

潤,乘以某個倍數計算).

Example 4

If the goodwill is to be valued at two year ’s purchase of the average annual super profit of the business over last four years, we have Year Yearly net profit Salaries to partners Net assets $ $ $ 2007 60,000 8,000 180,000 2008 62,000 8,000 200,000 2009 69,000 9,000 210,000 2010 79,000 9,000 230,000 Suppose the industry average return on net assets was 10%. The super profits for the four years are calculated as follows: Year Yearly net profit $ 2007 [$60,000 – $8,000 – ($180,000x10%)] = 34,000 2008 [$62,000 – $8,000 – ($200,000x10%)] = 34,000 2009 [$69,000 – $9,000 – ($210,000x10%)] = 39,000 2010 [$79,000 – $9,000 – ($230,000x10%)] = 47,000

154,000

Average annual super profit = $154,000 ÷ 4 = $38,500

Goodwill = Average annual super profit x No. of years’ purchase

= $38,500x2 = $77,000

Opportunity cost

Year Yearly net profit $ 2007 60,000 2008 62,000 2009 69,000 2010 79,000

270,000

$ Year ended 31 December 2006 35,000

2007 45,000 2008 44,000 2009 40,000 2010 46,000

Goodwill

= ($35,000 + $45,000 + $44,000 + $40,000 + $46,000) × 2/5

= 84,000

3

9.4 Changes in the profit and loss sharing ratio (損益分配比率的改變) The profit and loss sharing ratio is usually a basis on which profits and losses as well as the net assets (tangible and intangible) of a partnership are to be shared among the partners (把企業的損益及有形、無形的淨資產攤分給合夥人). Therefore, whenever

there is a change in the profit and loss sharing ratio (每當損益分配比率有變動時), the share of goodwill by each partner will be

affected (合夥人的商譽分配將受影響).

Example 5

Henry and Jason had been partners for a number of years, sharing profits and losses equally. The partners agreed to change the profit and loss sharing ratio as follows: Henry 2 : Jason 1 with effect from the financial year starting on 1 January 2011. Suppose the partnership’s goodwill was valued for the first time at $150,000.

(a) A goodwill account is opened (開設商譽帳戶) The adjusting entries are (所需的調整分錄如下):

Dr Goodwill account (with the value of goodwill) Cr Partners’ capital accounts (with the goodwill shared in the old profit and loss sharing ratio)

Goodwill 2011 $ Jan 1 Capital: Henry 75,000

Jason 75,000

Capital Henry Jason 2011 $ $

Jan 1 Goodwill 75,000 75,000 As the value of goodwill was ascertained before the change in the profit and loss sharing ratio (由於商譽價值是在損益分配比率

改變前確定), it should be shared among the partners in the old instead of the new ratio (因此應按舊比率而非新比率攤分給各

合夥人). Since a goodwill account is opened, the goodwill balance would be shown separately as an intangible non-current asset

below tangible non-current assets in the balance sheet (商譽帳戶的餘額會獨立顯示在資產負債表上,列作無形非流動資產,

放在有形非流動資產的下面).

Henry and Jason

Balance Sheet $ $

Non-current assets Premises 600,000 Plant and equipment 100,000 700,000 Goodwill 150,000

(b) A goodwill account is not opened (不開設商譽帳戶) Since a goodwill account is not opened, there isn’t any goodwill balance in the balance sheet and the effects of the change in the profit and loss sharing ratio on the share of goodwill would be affected in partners’ capital accounts only (損益分配比率的改變對

商譽分攤的影響只會反映在合夥人的資本帳戶內). The calculations of goodwill adjustment are:

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment Henry (1/2)$75,000 (2/3)$100,000 $25,000 Dr Capital: Henry $25,000 Jason (1/2)$75,000 (1/3)$50,000 ($25,000) Cr Capital: Jason $25,000

$150,000 $150,000

Capital

Henry Jason Henry Jason 2011 $ $ 2011 $ $ Jan 1 Goodwill adjustment 25,000 --- Jan 1 Goodwill adjustment --- 25,000

If the partnership is later sold, all its assets (including goodwill) will be realized in cash (如果合夥日後以繼續經營方式出售,企業

的所有資產(包括商譽)將會變現為現金). The goodwill realized will then be shared among the partners according to the new

profit and loss sharing ratio (而變現的商譽會按新的損益分配比率攤分). Therefore, for a partner who loses goodwill when it is

shared in the new ratio, he must be compensated by having his capital account credited with the amount of the loss (因此,如有合

夥人按新比率攤分商譽而蒙受損失時,其他合夥人要立刻向他作補償,在其資本帳戶貸記損失的金額). Conversely, for a

partner who gains goodwill when it is shared in the new ratio (如有合夥人按新比率攤分商譽而獲益時), he must be charged by

having his capital account debited with the amount of the gain (其資本帳戶借記獲益的金額).

Column form

4

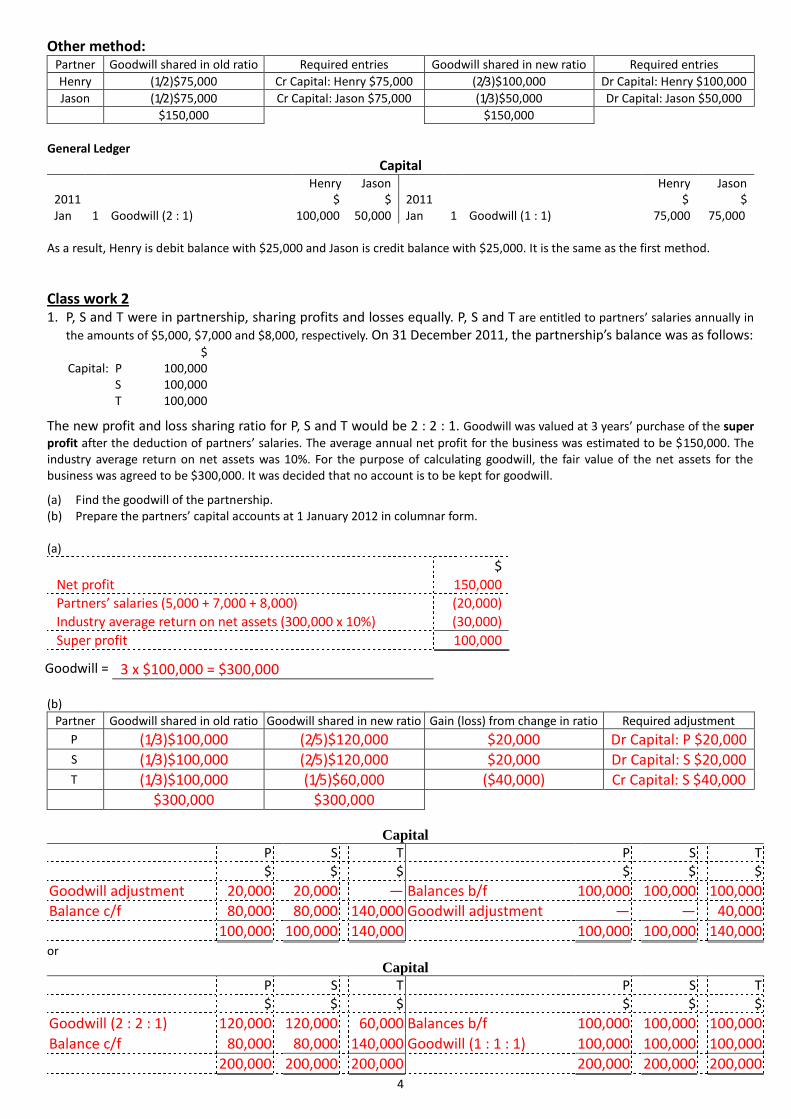

Other method: Partner Goodwill shared in old ratio Required entries Goodwill shared in new ratio Required entries

Henry (1/2)$75,000 Cr Capital: Henry $75,000 (2/3)$100,000 Dr Capital: Henry $100,000

Jason (1/2)$75,000 Cr Capital: Jason $75,000 (1/3)$50,000 Dr Capital: Jason $50,000

$150,000 $150,000

General Ledger

Capital Henry Jason Henry Jason 2011 $ $ 2011 $ $ Jan 1 Goodwill (2 : 1) 100,000 50,000 Jan 1 Goodwill (1 : 1) 75,000 75,000

As a result, Henry is debit balance with $25,000 and Jason is credit balance with $25,000. It is the same as the first method.

Class work 2

1. P, S and T were in partnership, sharing profits and losses equally. P, S and T are entitled to partners’ salaries annually in

the amounts of $5,000, $7,000 and $8,000, respectively. On 31 December 2011, the partnership’s balance was as follows: $ Capital: P 100,000 S 100,000 T 100,000

The new profit and loss sharing ratio for P, S and T would be 2 : 2 : 1. Goodwill was valued at 3 years’ purchase of the super

profit after the deduction of partners’ salaries. The average annual net profit for the business was estimated to be $150,000. The industry average return on net assets was 10%. For the purpose of calculating goodwill, the fair value of the net assets for the business was agreed to be $300,000. It was decided that no account is to be kept for goodwill. (a) Find the goodwill of the partnership. (b) Prepare the partners’ capital accounts at 1 January 2012 in columnar form. (a)

$

Net profit 150,000

Partners’ salaries (5,000 + 7,000 + 8,000) (20,000)

Industry average return on net assets (300,000 x 10%) (30,000)

Super profit 100,000 Goodwill = 3 x $100,000 = $300,000 (b)

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment

P (1/3)$100,000 (2/5)$120,000 $20,000 Dr Capital: P $20,000 S (1/3)$100,000 (2/5)$120,000 $20,000 Dr Capital: S $20,000 T (1/3)$100,000 (1/5)$60,000 ($40,000) Cr Capital: S $40,000

$300,000 $300,000

Capital

P S T P S T

$ $ $ $ $ $

Goodwill adjustment 20,000 20,000 — Balances b/f 100,000 100,000 100,000

Balance c/f 80,000 80,000 140,000 Goodwill adjustment — — 40,000

100,000 100,000 140,000 100,000 100,000 140,000 or

Capital

P S T P S T

$ $ $ $ $ $

Goodwill (2 : 2 : 1) 120,000 120,000 60,000 Balances b/f 100,000 100,000 100,000

Balance c/f 80,000 80,000 140,000 Goodwill (1 : 1 : 1) 100,000 100,000 100,000

200,000 200,000 200,000 200,000 200,000 200,000

5

2. The following partners decided to change their profit and loss sharing ratio on 1 July 2010 as follows: Old ratio New ratio Young 2 3 Chan 3 4 Long 4 3 But 1 2

They agreed that goodwill was valued at $18,000 as at 30 June 2010. The last balance sheet before the change was as follows:

Young, Chan, Long and But Balance Sheet as at 30 June 2010

$ $ Net assets (not including goodwill) 18,800 Capital: Young 7,000 Chan 3,200 Long 5,000 But 3,600

18,800 18,800

Show the capital accounts and the balance sheet as at 1 July 2010 if: (a) a goodwill account was to be opened. (b) a goodwill account was not to be opened. (a)

Capital Young Chan Long But Young Chan Long But

$ $ $ $ $ $ $ $

Balances c/d 10,600 8,600 12,200 5,400 Balances b/f 7,000 3,200 5,000 3,600 Goodwill 3,600 5,400 7,200 1,800 10,600 8,600 12,200 5,400 10,600 8,600 12,200 5,400

Young, Chan, Long and But

Balance Sheet as at 30 June 2010 $ $

Net assets (not including goodwill) 18,800 Capital: Young 10,600

Goodwill 18,000 Chan 8,600

Long 12,200

But 5,400

36,800 36,800

(b)

Goodwill Adjustment

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment

Young (2/10)$3,600 (3/12)$4,500 $900 Dr Capital: Young $900

Chan (3/10)$5,400 (4/12)$6,000 $600 Dr Capital: Chan $600

Long (4/10)$7,200 (3/12)$4,500 ($2,700) Cr Capital: Long $2,700

But (1/10)$1,800 (2/12)$3,000 $1,200 Dr Capital: But $1,200

$18,000 $18,000

Capital Young Chan Long But Young Chan Long But

$ $ $ $ $ $ $ $

Goodwill adjustment 900 600 --- 1,200 Balances b/f 7,000 3,200 5,000 3,600

Balances c/d 6,100 2,600 7,700 2,400 Goodwill adjustment --- --- 2,700 ---

7,000 3,200 7,700 3,600 7,000 3,200 7,700 3,600

Young, Chan, Long and But Balance Sheet as at 30 June 2010

$ $

Net assets 18,800 Capital: Young 6,100

Chan 2,600

Long 7,700

But 2,400

18,800 18,800

6

3. Amy, Bob and Cary were in partnership, sharing profits and losses in the ratio of 3 : 2: 1. The partnership’s balance sheet as at 31 December 2010 was as follows:

Amy, Bob and Cary Balance Sheet as at 31 December 2010

$ $ $ $

Non-current assets Capital account

Office equipment, at net book value 438,000 Amy 338,000

Motor vehicles, at net book value 200,000 Bob 200,000

638,000 Cary 200,000 738,000

Current assets

Inventory 53,551 Current account

Accounts receivable 170,000 Amy 80,000

Bank 131,800 355,351 Bob 30,000

Cary (10,000) 100,000

Current liabilities

Accounts payable 155,351

993,351 993,351

For personal reasons, Amy decided to spend less time in the partnership. The partners agreed to share the profits and losses

equally with effect from 1 January 2011.

Goodwill was to be valued at three years’ purchase of the average net profit of the partnership over the last four years. Net profits over the last four years were as follows: Year $ 2007 250,000 2008 135,000 2009 68,000 2010 147,000 (a) Show the capital accounts (in columnar form) and the balance sheet as at 1 January 2011 if (i) a goodwill account was to be opened. (ii) a goodwill account was not to be opened. (b) Prepare the journal entries for the goodwill adjustment in (a). (No narrations are required.) (a) (i)

Capital

Amy Bob Cary Amy Bob Cary

2011 $ $ $ 2011 $ $ $

Jan 1 Balances c/d 563,000 350,000 275,000 Jan 1 Balances b/f 338,000 200,000 200,000

" 1 Goodwill 225,000 150,000 75,000

563,000 350,000 275,000 563,000 350,000 275,000

Amy, Bob and Cary Balance Sheet as at 1 January 2011

$ $ $ $

Non-current assets Capital account

Office equipment, at net book value 438,000 Amy 563,000

Motor vehicles, at net book value 200,000 638,000 Bob 350,000

Goodwill 450,000 Cary 275,000 1,188,000

1,088,000

Current assets Current account

Inventory 53,551 Amy 80,000

Accounts receivable 170,000 Bob 30,000

Bank 131,800 355,351 Cary (10,000) 100,000

Current liabilities

Accounts payable 155,351

1,443,351 1,443,351

7

(a) (ii)

Goodwill Adjustment

Partner Goodwill shared in old ratio Required entries Goodwill shared in new ratio Required entries

Amy (3/6)$ 225,000 Cr Capital: Amy $225,000 (1/3)$ 150,000 Dr Capital: Amy $150,000

Bob (2/6)$ 150,000 Cr Capital: Bob $150,000 (1/3)$ 150,000 Dr Capital: Bob $150,000

Cary (1/6)$ 75,000 Cr Capital: Cary $75,000 (1/3)$ 150,000 Dr Capital: Cary $150,000

$450,000 $450,000

Capital

Amy Bob Cary Amy Bob Cary

2011 $ $ $ 2011 $ $ $

Jan 1 Goodwill (1 : 1 : 1) 150,000 150,000 150,000 Jan 1 Balances b/f 338,000 200,000 200,000

" 1 Balances c/d 413,000 200,000 125,000 " 1 Goodwill (3 : 2 : 1) 225,000 150,000 75,000

563,000 350,000 275,000 563,000 350,000 275,000

Amy, Bob and Cary Balance Sheet as at 1 January 2011

$ $ $ $

Non-current assets Capital account

Office equipment, at net book value 438,000 Amy 413,000

Motor vehicles, at net book value 200,000 Bob 200,000

638,000 Cary 125,000 738,000

Current assets

Inventory 53,551 Current account

Accounts receivable 170,000 Amy 80,000

Bank 131,800 355,351 Bob 30,000

Cary (10,000) 100,000

Current liabilities

Accounts payable 155,351

933,351 933,351 (b)

Journal

Details Dr Cr

$ $

a (i) Goodwill 450,000

Capital: Amy 225,000

Capital: Bob 150,000

Capital: Cary 75,000

a (ii) Capital: Cary 75,000

Capital: Amy 75,000

4. Test 1

8

5. Jenny and Sandy were in partnership, sharing profit and losses equally. A balance sheet as at 31 December 2010 was prepared as follows:

Jenny and Sandy

Balance sheet as at 31 December 2010 $ $ $ Non-current assets Premises 600,000 Plant and equipment 100,000 700,000 Current assets Inventory 15,000 Accounts receivable 35,000 Cash at bank 20,000 70,000 Less Current liabilities

Accounts payable (40,000) Net current assets 30,000 730,000 Financed by: Capital account: Jenny 365,000 Sandy 365,000 730,000

Sandy decided to reduce the amount of time she would work for the partnership from five days a week to 2.5 days a week. The partners agreed that starting from 1 January 2011, the profits and losses would be shared between Jenny and Sandy in the ratio of 2 : 1. Goodwill was to be valued at two years’ purchase of the last five years’ average net profits. The net profits for the last five years were as follows:

$ Year ended 31 December 2006 35,000

2007 45,000 2008 44,000 2009 40,000 2010 46,000

(a) Show the capital accounts (in columnar form) and the balance sheet as at 1 January 2011 if: (i) a goodwill account was to be opened. (ii) a goodwill account was not to be opened. (b) Suggest one alternative method of valuing goodwill. (a) (i)

Capital Jenny Sandy Jenny Sandy 2011 $ $ 2011 $ $ Jan 1 Balances c/d 407,000 407,000 Jan 1 Balances b/f 365,000 365,000

“ 1 Goodwill 42,000 42,000 407,000 407,000 407,000 407,000

Jenny and Sandy Balance sheet as at 1 January 2011

$ $ $ Non-current assets Premises 600,000 Plant and equipment 100,000 700,000

Goodwill ($35,000 + $45,000 + $44,000 + $40,000 + $46,000) × 2/5 84,000 784,000 Current assets Inventory 15,000 Accounts receivable 35,000 Cash at bank 20,000 70,000 Less Current liabilities

Accounts payable (40,000) Net current assets 30,000 814,000

Financed by: Capital account: Jenny 407,000 Sandy 407,000 814,000

9

(a) (ii) Capital

Jenny Sandy Jenny Sandy 2011 $ $ 2011 $ $ Jan 1 Goodwill adjustment 14,000 --- Jan 1 Balances b/f 365,000 365,000

“ 1 Balances c/d 351,000 379,000 “ 1 Goodwill adjustment --- 14,000 365,000 379,000 365,000 379,000

Jenny and Sandy Balance sheet as at 1 January 2011

$ $ $ Non-current assets Premises 600,000

Plant and equipment 100,000 700,000

Current assets

Inventory 15,000

Accounts receivable 35,000 Cash at bank 20,000 70,000 Less Current liabilities

Accounts payable (40,000) Net current assets 30,000 730,000

Financed by: Capital account: Jenny 351,000

Sandy 379,000 730,000

(b) Average sales method : Goodwill is valued as a multiple of the average annual sales over a number of past

years. This method is particularly applicable to trading business.

6. Test 2

10

9.5 Admission of partners (合夥人加入) Whenever a new partner is admitted, the goodwill of the old partnership has to be valued and adjusting entries are required in the partners’ capital accounts.

Example 6

Dennis and Eddy were partners, sharing profits and losses equally. On 1, January 2011, the partners agreed to admit John as a new partner and the new profit and loss sharing ratio would be: Dennis 1 : Eddy 2 : John 2. John brought in $40,000 cash as capital. On the date of John’s admission, the goodwill of the partnership between Dennis and Eddy was valued for the first time at $60,000 and the partners’ capital balances were adjusted as follows.

(a) A goodwill account is opened (開設商譽帳戶) General Ledger

Goodwill 2011 $ Jan 1 Capital: Dennis 30,000

Eddy 30,000

Capital Dennis Eddy John 2011 $ $ $ Jan 1 Cash --- --- 40,000

“ 1 Goodwill 30,000 30,000 ---

(b) A goodwill account is not opened (不開設商譽帳戶) The effects of the admission of a new partner on the share of goodwill are as follows:

Partner Goodwill shared

in old ratio Goodwill shared in

new ratio Gain (loss) from change in ratio

Required adjustment

Dennis (1/2)$30,000 (1/5)$12,000 ($18,000) Cr Capital: Dennis $18,000

Eddy (1/2)$30,000 (2/5)$24,000 ($6,000) Cr Capital: Eddy $6,000

John ---- (2/5)$24,000 $24,000 Dr Capital: John $24,000

$60,000 $60,000

General Ledger

Capital Dennis Eddy John Dennis Eddy John 2011 $ $ $ 2011 $ $ $ Jan 1 Goodwill adjustment --- --- 24,000 Jan 1 Cash --- --- 40,000

“ 1 Goodwill adjustment 18,000 6,000 ---

New partner pays for his gain in share of goodwill (新合夥人為商譽分攤的獲益付款) Sometimes, the new partner may be asked to pay for his gain in share of goodwill. Suppose John brought in $40,000 cash as capital and an additional sum of cash for his share of goodwill (i.e., $24,000) General Ledger

Capital Dennis Eddy John Dennis Eddy John 2011 $ $ $ 2011 $ $ $ Jan 1 Goodwill adjustment --- --- 24,000 Jan 1 Cash ($40,000 + $24,000) --- --- 64,000

“ 1 Goodwill adjustment 18,000 6,000 ---

New partner pays the old partners privately for their loss in share of goodwill Sometimes, the new partner may choose to pay the old partners privately for their loss in share of goodwill (有時,新合夥人會選

擇私下付款給舊合夥人,補償他們商譽分攤的損失). For example, John paid $18,000 and $6,000 directly to Dennis and Eddy,

respectively. No entries are required for these payments in the partnership books. Moreover, no adjustments are required for goodwill in the partners’ capital accounts (在此情況下,合夥的帳目不用記錄這些付款,合夥也不用在合夥人的資本帳戶內作

任何調整).

11

Other Method: The effects of the admission of a new partner on the share of goodwill are as follows:

Partner Goodwill shared in old ratio Required entries Goodwill shared in new ratio Required entries

Dennis (1/2)$30,000 Cr Capital: Dennis $30,000 (1/5)$12,000 Dr Capital: Dennis $12,000

Eddy (1/2)$30,000 Cr Capital: Eddy $30,000 (2/5)$24,000 Dr Capital: Eddy $24,000

John — — (2/5)$24,000 Dr Capital: Eddy $24,000

$60,000 $60,000

General Ledger

Capital Dennis Eddy John Dennis Eddy John 2011 $ $ $ 2011 $ $ $ Jan 1 Goodwill (1 : 2 : 2) 12,000 24,000 24,000 Jan 1 Cash --- --- 40,000

“ 1 Goodwill (1 : 1) 30,000 30,000 --- As a result, Dennis is credit balance with $18,000, Eddy is credit balance with $6,000 and John is credit balance with $16,000. It is the same as the first method.

New partner pays for his gain in share of goodwill (新合夥人為商譽分攤的獲益付款) Sometimes, the new partner may be asked to pay for his gain in share of goodwill. Suppose John brought in $40,000 cash as capital and an additional sum of cash for his share of goodwill (i.e., $24,000) General Ledger

Capital Dennis Eddy John Dennis Eddy John 2011 $ $ $ 2011 $ $ $ Jan 1 Goodwill (1 : 2 : 2) 12,000 24,000 24,000 Jan 1 Cash ($40,000 + $24,000) --- --- 64,000

“ 1 Goodwill (1 : 1) 30,000 30,000 ---

As a result, Dennis is credit balance with $18,000, Eddy is credit balance with $6,000 and John is credit balance with $40,000. It is the same as the first method.

Class work 3

1. S and T were in partnership, sharing profits and losses equally. On 31 December 2011, the partnership’s balance was as follows: $

Capital: S 100,000

T 100,000 On 1 January 2012, P was admitted to the partnership with an initial capital contribution of $200,000 and profits and losses are to be shared equally. Goodwill was valued at $300,000. It was decided that no account is to be kept for goodwill. Prepare the partners’ capital accounts at 1 January 2012 in columnar form. Answer:

Partner Goodwill shared in old ratio Required entries Goodwill shared in new ratio Required entries

S (1/2)$150,000 Cr Capital: S $150,000 (1/3)$100,000 Dr Capital: S $100,000

T (1/2)$150,000 Cr Capital: T $150,000 (1/3)$100,000 Dr Capital: T $100,000

P — — (1/3)$100,000 Dr Capital: P $100,000

$300,000 $300,000

Capital

S T P S T P

$ $ $ $ $ $

Goodwill (1 : 1 : 1) 100,000 100,000 100,000 Balances b/f 100,000 100,000 —

Balance c/f 150,000 150,000 100,000 Goodwill (1 : 1) 150,000 150,000 —

Bank — — 200,000

250,000 250,000 200,000 250,000 250,000 200,000

12

2. Anderson, Benson, Derek have been in partnership, sharing profits and losses in the ratio of 3 : 2 : 5, respectively. Their capital accounts showed the following balances as at 31 December 2010:

Anderson 25,000 Cr Benson 18,000 Cr Derek 32,000 Cr On 1 Jul 2011, Eason was admitted to the partnership with an initial capital contribution of $25,000. Goodwill was valued at $20,000. The new profit and loss sharing ratio would be Anderson 4 : Benson 3 : Derek 2 : Eason 1. Show the required entries in the partners’ capital accounts in columnar form.

Goodwill Adjustment

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment

Anderson (3/10)$6,000 (4/10)$8,000 $2,000 Dr Capital: Anderson $2,000

Benson (2/10)$4,000 (3/10)$6,000 $2,000 Dr Capital: Benson $2,000

Derek (5/10)$10,000 (2/10)$4,000 ($6,000) Cr Capital: Derek $6,000

Eason ---- (1/10)$2,000 $2,000 Dr Capital: Eason $2,000

$20,000 $20,000

Capital

Anderson Benson Derek Eason Anderson Benson Derek Eason

2011 $ $ $ $ 2011 $ $ $ $

Jul 1 Goodwill adj. 2,000 2,000 — 2,000 Jul 1 Balances b/d 25,000 18,000 32,000 —

" 30 Balances c/d 23,000 16,000 38,000 23,000 " 1 Bank — — — 25,000

" 1 Goodwill adj. — — 6,000 —

25,000 18,000 38,000 25,000 25,000 18,000 38,000 25,000

3. John and Jason were in partnership and their capital accounts showed credit balances: John $20,000 and Jason $10,000. They

shared profits and losses in the ratio of 3 : 2. It was decided to admit a new partner, Joe. The goodwill of the old partnership was valued at $15,000, but this had not been recorded in the books. Joe brought in $20,000 cash as capital and also made an additional payment to the partnership for his share of goodwill. The new profit and loss sharing ratio would be John 5 : Jason 3 : Joe 2. Show the required entries in the journal and partners’ capital accounts to record Joe’s admission.

Goodwill Adjustment

Partner Goodwill shared in old ratio Required entries Goodwill shared in new ratio Required entries

John (3/5)$9,000 Cr Capital: John $9,000 (5/10)$7,500 Dr Capital: John $7,500

Jason (2/5)$6,000 Cr Capital: Jason $6,000 (3/10)$4,500 Dr Capital: Jason $4,500

Joe — — (2/10)$3,000 Dr Capital: Joe $3,000

$15,000 $15,000

Capital John Jason Joe John Jason Joe

$ $ $ $ $ $

Goodwill (5 : 3 : 2) 7,500 4,500 3,000 Balances b/f 20,000 10,000 — Balances c/d 21,500 11,500 20,000 Cash ($20,000 + $3,000) — — 23,000

Goodwill (3 : 2) 9,000 6,000 — 29,000 16,000 23,000 29,000 16,000 23,000

The Journal

Details Dr Cr

$ $

Cash 23,000

Capital: John 1,500

Capital: Jason 1,500

Capital: Joe 20,000

13

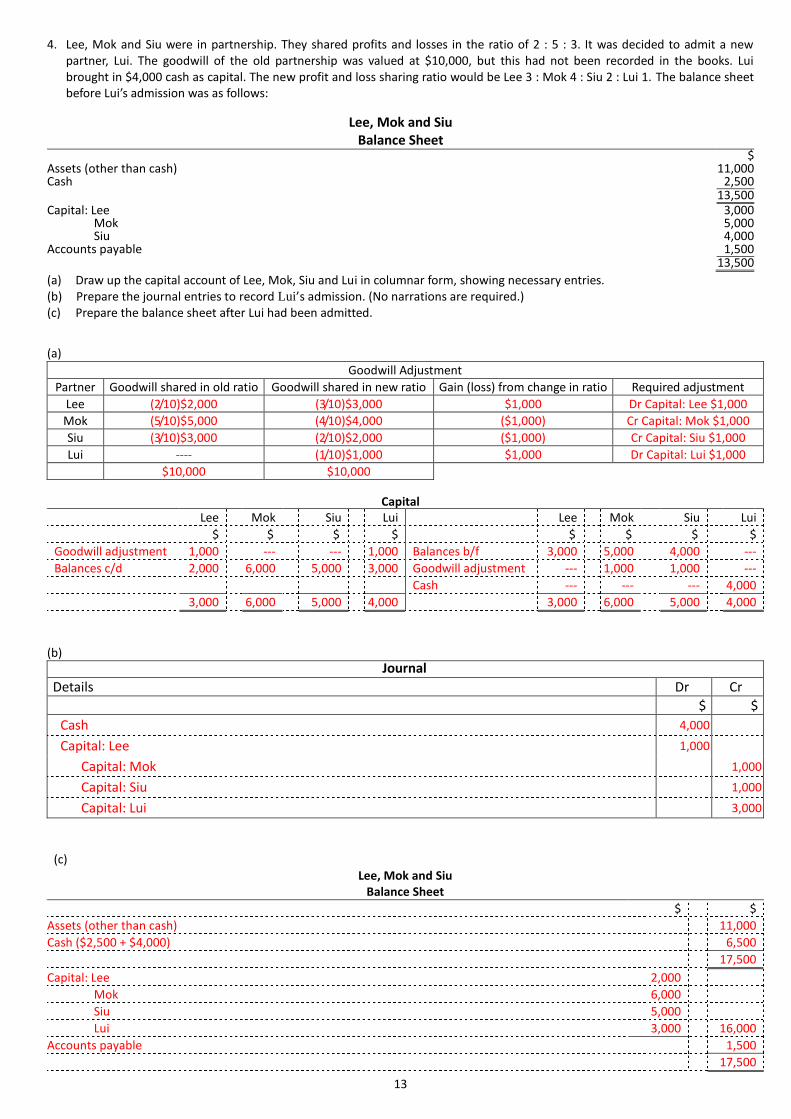

4. Lee, Mok and Siu were in partnership. They shared profits and losses in the ratio of 2 : 5 : 3. It was decided to admit a new partner, Lui. The goodwill of the old partnership was valued at $10,000, but this had not been recorded in the books. Lui brought in $4,000 cash as capital. The new profit and loss sharing ratio would be Lee 3 : Mok 4 : Siu 2 : Lui 1. The balance sheet before Lui’s admission was as follows:

Lee, Mok and Siu

Balance Sheet $

Assets (other than cash) 11,000 Cash 2,500 13,500 Capital: Lee 3,000 Mok 5,000 Siu 4,000 Accounts payable 1,500

13,500

(a) Draw up the capital account of Lee, Mok, Siu and Lui in columnar form, showing necessary entries. (b) Prepare the journal entries to record Lui’s admission. (No narrations are required.) (c) Prepare the balance sheet after Lui had been admitted. (a)

Goodwill Adjustment

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment

Lee (2/10)$2,000 (3/10)$3,000 $1,000 Dr Capital: Lee $1,000

Mok (5/10)$5,000 (4/10)$4,000 ($1,000) Cr Capital: Mok $1,000

Siu (3/10)$3,000 (2/10)$2,000 ($1,000) Cr Capital: Siu $1,000

Lui ---- (1/10)$1,000 $1,000 Dr Capital: Lui $1,000

$10,000 $10,000

Capital

Lee Mok Siu Lui Lee Mok Siu Lui

$ $ $ $ $ $ $ $

Goodwill adjustment 1,000 --- --- 1,000 Balances b/f 3,000 5,000 4,000 ---

Balances c/d 2,000 6,000 5,000 3,000 Goodwill adjustment --- 1,000 1,000 ---

Cash --- --- --- 4,000

3,000 6,000 5,000 4,000 3,000 6,000 5,000 4,000

(b)

Journal

Details Dr Cr

$ $

Cash 4,000

Capital: Lee 1,000

Capital: Mok 1,000

Capital: Siu 1,000

Capital: Lui 3,000

(c)

Lee, Mok and Siu Balance Sheet

$ $

Assets (other than cash) 11,000

Cash ($2,500 + $4,000) 6,500

17,500

Capital: Lee 2,000

Mok 6,000

Siu 5,000

Lui 3,000 16,000

Accounts payable 1,500

17,500

14

5. Chan and Tai had been in partnership for many years, sharing profits and losses in the ratio of 3 : 2. As at 31 December 2010, their capital accounts showed credit balances: Chan $60,000 and Tai $40,000. As their workloads were increasing, they intended to admit one more partner, Lam, on 1 January 2011. No goodwill account had ever been opened. The goodwill of the old partnership was valued at $12,000. Lam contributed $20,000 cash as capital. The new profit and loss sharing ratio would be: Chan 3 : Tai 2 : Lam 1. No goodwill account was to be opened. Show the required entries in the partners’ capital accounts in columnar form.

Capital

Chan Tai Lam Chan Tai Lam

$ $ $ $ $ $

Goodwill (3 : 2 : 1) 6,000 4,000 2,000 Balances b/f 60,000 40,000 ---

Balances c/d 61,200 40,800 18,000 Cash --- --- 20,000

Goodwill (3 : 2) 7,200 4,800 ---

67,200 44,800 20,000 67,200 44,800 20,000

6. Test 3

7. Koo and Lee were in partnership, operating as an accounting firm in Central. They agreed to share profits and losses in the

ratio of 3 : 2. It was also agreed that both partners’ opening capital balances would be credited with interest at a rate of 5% per annum.

The balance sheet as at 31 December 2010 was as follows:

Koo and Lee Balance Sheet as at 31 December 2010

$ $ Non-current assets and current assets (excluding cash at bank) 465,000 Bank 125,000 Accounts payable (110,000) 15,000

480,000

Capital: Koo 300,000 Lee 180,000

480,000

A new partner, Mi was admitted on 1 January 2011. The profit and loss sharing ratio was then revised to Koo 3 : Lee 4 : Mi 2. Mi contributed $300,000 as capital and also made an additional payment to the partnership for his share of goodwill. Fixed capital accounts were maintained by the new partnership. Goodwill was to be valued at three years’ purchase of the average annual fee income of the business over the last four years. The annual fee income over the last four years was as follows: Year $ 2007 165,800 2008 73,660 2009 288,540 2010 147,000

It was agreed that interest would continue to be paid on capital balances in the new partnership but no goodwill account was to be

opened.

The following information was available as at 31 December 2011:

(i) Net profit before appropriations for the year ended 31 December 2011 was $93,297.

(ii) Financial position as at 31 December 2011:

$ $ Non-current assets and current assets (excluding cash at bank) 558,297 Bank 487,500 Accounts payable (60,000) 427,500

985,797

Required: (a) Prepare the journal entries to record Mi’s admission. (No narrations are required.) (b) Prepare the income statement and draw up the capital accounts of Koo, Lee and Mi in columnar form Prepare the income

statement and (c) Prepare the balance sheet of the new partnership as at 31 December 2011.

Goodwill Adjustment

Partner Goodwill shared in old ratio Required entries Goodwill shared in new ratio Required entries

Chan (3/5)$7,200 Cr Capital: Chan $7,200 (3/6)$6,000 Dr Capital: Chan $6,000

Tai (2/5)$4,800 Cr Capital: Tai $4,800 (2/6)$4,000 Dr Capital: Tai $4,000

Lam — — (1/6)$2,000 Dr Capital: Lam $2,000

$12,000 $12,000

Goodwill = (165,800 + 73,660 + 288,540 + 147,000)x3/4 = $506,250

Goodwill Adjustment

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment

Koo (3/5)$303,750 (3/9)$168,750 ($135,000) Cr Capital: Koo $135,000

Lee (2/5)$202,500 (4/9)$225,000 $22,500 Dr Capital: Lee $22,500

Mi — (2/9)$112,500 $112,500 Dr Capital: Mi $112,500

$506,250 $506,250

15

(a)

The Journal

Date Details Dr Cr

2011 $ $

Jan 1 Bank ($300,000 + $112,500) 412,500

Capital: Lee (W1) 22,500

Capital: Koo (W1) 135,000

Capital: Mi 300,000 (b)

Koo, Lee and Mi Income Statement for the year ended 31 December 2011 (extract)

$ $

Net profit for the year 93,297

Less Interest on capital: Koo ($435,000 5%) 21,750

Lee ($157,500 5%) 7,875

Mi ($300,000 5%) 15,000 (44,625)

48,672

Balance of profit shared: Koo (3/9) 16,224

Lee (4/9) 21,632

Mi (2/9) 10,816 48,672

Capital

Koo Lee Mi Koo Lee Mi 2011 $ $ $ 2011 $ $ $

Jan 1 Goodwill adj. — 22,500 112,500 Jan 1 Balances b/f 300,000 180,000 —

" 1 Balances c/d 435,000 157,500 300,000 " 1 Bank ($300,000 + $112,500) — — 412,500

" 1 Goodwill adj. 135,000 — —

435,000 180,000 412,500 435,000 180,000 412,500

Current

Koo Lee Mi Koo Lee Mi

2011 $ $ $ 2011 $ $ $

Dec 31 Balances c/f 37,974 29,507 25,816 Dec 31 Profit and loss appropriation –

Interest on capital 21,750 7,875 15,000

Share of profit 16,224 21,632 10,816

37,974 29,507 25,816 37,974 29,507 25,816

(c)

Koo, Lee and Mi Balance Sheet as at 31 December 2011

$ $ Non-current assets and current assets (except cash at bank) 558,297

Bank 487,500

Accounts payable (60,000) 427,500

985,797

Capital: Koo 435,000

Lee 157,500

Mi 300,000 892,500

Current: Koo 37,974

Lee 29,507

Mi 25,816 93,297

985,797

16

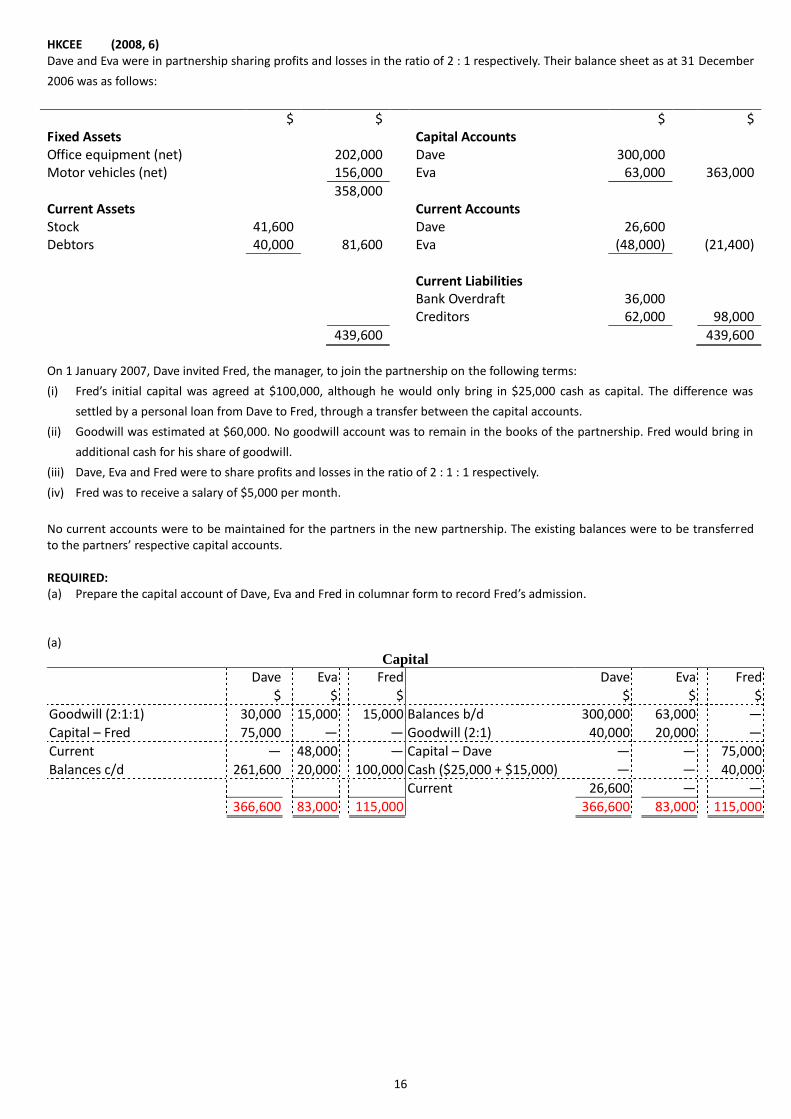

HKCEE (2008, 6) Dave and Eva were in partnership sharing profits and losses in the ratio of 2 : 1 respectively. Their balance sheet as at 31 December

2006 was as follows:

$ $ $ $ Fixed Assets Capital Accounts Office equipment (net) 202,000 Dave 300,000 Motor vehicles (net) 156,000 Eva 63,000 363,000

358,000 Current Assets Current Accounts Stock 41,600 Dave 26,600 Debtors 40,000 81,600 Eva (48,000) (21,400)

Current Liabilities Bank Overdraft 36,000 Creditors 62,000 98,000

439,600 439,600

On 1 January 2007, Dave invited Fred, the manager, to join the partnership on the following terms:

(i) Fred’s initial capital was agreed at $100,000, although he would only bring in $25,000 cash as capital. The difference was

settled by a personal loan from Dave to Fred, through a transfer between the capital accounts.

(ii) Goodwill was estimated at $60,000. No goodwill account was to remain in the books of the partnership. Fred would bring in

additional cash for his share of goodwill.

(iii) Dave, Eva and Fred were to share profits and losses in the ratio of 2 : 1 : 1 respectively.

(iv) Fred was to receive a salary of $5,000 per month.

No current accounts were to be maintained for the partners in the new partnership. The existing balances were to be transferred to the partners’ respective capital accounts. REQUIRED: (a) Prepare the capital account of Dave, Eva and Fred in columnar form to record Fred’s admission. (a)

Capital

Dave Eva Fred Dave Eva Fred

$ $ $ $ $ $

Goodwill (2:1:1) 30,000 15,000 15,000 Balances b/d 300,000 63,000 —

Capital – Fred 75,000 — — Goodwill (2:1) 40,000 20,000 —

Current — 48,000 — Capital – Dave — — 75,000

Balances c/d 261,600 20,000 100,000 Cash ($25,000 + $15,000) — — 40,000

Current 26,600 — —

366,600 83,000 115,000 366,600 83,000 115,000

17

9.6 Withdrawal or death of partners Whenever an old partner withdraws (death, ill health, retirement or other reasons) from a partnership, the goodwill of the partnership has to be valued and adjusting entries are required in the partners’ capital accounts.

Example 7

Harry, Irene and Joe were partners, sharing profits and losses equally. On 1 January 2011, the first day of the new financial year, Joe would leave and the remaining partners would continue to share profits and losses equally. On the date of Joe’s withdrawal, the capital balances of the partners were: Harry $50,000, Irene $50,000, Joe $40,000; and the goodwill of the partnership was valued for the first time at $45,000. The partners’ capital balances were adjusted as follows:

(a) A goodwill account is opened General Ledger

Goodwill 2011 $ Jan 1 Capital: Harry 15,000

Irene 15,000 Joe 15,000

Capital Harry Irene Joe Harry Irene Joe 2011 $ $ $ 2011 $ $ $ Jan 1 Cash — — 55,000 Jan 1 Balance b/f 50,000 50,000 40,000

“ 31 Balance c/f 65,000 65,000 — “ 1 Goodwill 15,000 15,000 15,000

65,000 65,000 55,000 65,000 65,000 55,000

(b) A goodwill account is not opened The effects of the withdrawal of an old partner on the share of goodwill are as follows:

Partner Goodwill shared

in old ratio Goodwill shared in

new ratio Gain (loss) from change in ratio

Required adjustment

Harry (1/3)$15,000 (1/2)$22,500 $7,500 Dr Capital: Harry $7,500

Irene (1/3)$15,000 (1/2)$22,500 $7,500 Dr Capital: Irene $7,500

Joe (1/3)$15,000 ---- ($15,000) Cr Capital: Joe $15,000

$45,000 $45,000

General Ledger

Capital Harry Irene Joe Harry Irene Joe 2011 $ $ $ 2011 $ $ $ Jan 1 Goodwill adjustment 7,500 7,500 --- Jan 1 Balance b/f 50,000 50,000 40,000

“ 1 Goodwill adjustment --- --- 15,000 After adjustments, Joe’s capital balance amounted to $55,000. This balance is the same whether a goodwill account is opened or not. Joe should be paid $55,000 on his withdrawal. The required double entry for this is: Dr Joe’s capital account $55,000 Cr Cash/Bank accounts $55,000

Capital Harry Irene Joe Harry Irene Joe

2011 $ $ $ 2011 $ $ $ Jan 1 Goodwill adj. 7,500 7,500 --- Jan 1 Balance b/f 50,000 50,000 40,000

“ 1 Cash/Bank --- --- 55,000 “ 1 Goodwill adj. --- --- 15,000 “ 31 Balance b/f 42,500 42,500 ---

50,000 50,000 55,000 50,000 50,000 55,000

Again, if existing partners gain goodwill when it is shared in the new ratio, they must be charged by having their capital account debited with the amount of the gain.

18

Sometimes the withdrawing partner may not take away all his capital (and current account) balance(s) in cash. He may leave part of it with the new partnership as a loan.

Example 8

Suppose Joe take away half of his capital balance in cash on withdrawal and left the other half with the new partnership as a loan. The capital accounts would appear as follows: General Ledger

Capital Harry Irene Joe Harry Irene Joe

2011 $ $ $ 2011 $ $ $ Jan 1 Goodwill adj. 7,500 7,500 --- Jan 1 Balance b/f 50,000 50,000 40,000

“ 1 Cash/Bank --- --- 27,500 “ 1 Goodwill adj. --- --- 15,000 “ 1 Loan from Joe --- --- 27,500 “ 31 Balance b/f 42,500 42,500 ---

50,000 50,000 55,000 50,000 50,000 55,000

The loan from Joe would be shown as a liability in the balance sheet of the new partnership subsequently, and interest might be charged on it.

Class work 4

1. Chiu, Ho and Kan had been in partnership for many years, sharing profits and losses in the ratio of 4 : 3 : 1. As at 31 March 2010, their capital accounts and current accounts showed the following balances: Capital accounts Current accounts Chiu $80,000 Cr $5,620 Cr Ho $60,000 Cr $2,350 Dr Kan $20,000 Cr $6,180 Cr

As there were increasing conflicts among the partners, they decided to let Ho withdraw from the partnership and get back his capital balance on 1 April 2010. The new profit and loss sharing ratio would be: Chiu 4 : Kan 1. No goodwill account had ever been opened. Their accountant advised them to value goodwill upon the withdrawal of Ho and make certain adjustments in the books.

(a) If the partnership’s goodwill was valued at $16,000 on the withdrawal of Ho, show the necessary entries in the capital accounts if:

(i) a goodwill account was to be opened. (ii) a goodwill account was not to be opened. (b) Explain why a partner’s current account may show a debit balance instead of a credit balance. (a) (i)

Capital Chiu Ho Kan Chiu Ho Kan

$ $ $ $ $ $

Current: Ho ---- 2,350 ---- Balances b/f 80,000 60,000 20,000

Bank ---- 63,650 ---- Goodwill 8,000 6,000 2,000

Balances c/d 88,000 ---- 22,000

88,000 66,000 22,000 88,000 66,000 22,000

(ii)

Capital Chiu Ho Kan Chiu Ho Kan

$ $ $ $ $ $

Goodwill adjustment 4,800 --- 1,200 Balances b/f 80,000 60,000 20,000

Current: Ho --- 2,350 --- Goodwill adjustment --- 6,000 ---

Bank --- 63,650 ---

Balances c/d 75,200 --- 18,000

80,000 66,000 20,000 80,000 66,000 20,000

(b) When a partner’s current account shows a debit balance, this means that he is indebted to the partnership.

This situation may arise when a partnership has incurred a substantial loss one year or a partner has taken out

more than his balance of undrawn profits from the partnership.

Goodwill Adjustment

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment

Chiu (4/8)$8,000 (4/5)$12,800 $4,800 Dr Capital: Chiu $4,800

Ho (3/8)$6,000 — ($6,000) Cr Capital: Ho $6,000

Kan (1/8)$2,000 (1/5)$3,200 $1,200 Dr Capital: Kan $1,200

$16,000 $16,000

19

2. Fong, Ma and Kwan had been in partnership for many years, sharing profits and losses in the ratio of 5 : 3 : 2. As at 30 June 2009, their capital accounts showed the following credit balances: Fong $50,000, Ma $30,000, Kwan $20,000.

Fong decided to retire on 1 July 2009. But he agreed to leave half of his capital balance with the firm as a loan. The new profit and loss sharing ratio would be: Ma 4 : Kwan 3.

No goodwill account had ever been opened. If goodwill was valued at $14,000 upon the withdrawal of Fong, show the necessary entries in the capital accounts in columnar form if: (a) a goodwill account was to be opened. (b) a goodwill account was not to be opened.

(a)

Capital Fong Ma Kwan Fong Ma Kwan

$ $ $ $ $ $

Bank 28,500 ---- ---- Balances b/f 50,000 30,000 20,000

Loan 28,500 ---- ---- Goodwill 7,000 4,200 2,800

Balances c/d ---- 34,200 22,800

57,000 34,200 22,800 57,000 34,200 22,800

(b)

Capital Fong Ma Kwan Fong Ma Kwan

$ $ $ $ $ $

Goodwill adjustment --- 3,800 3,200 Balances b/f 50,000 30,000 20,000

Bank 28,500 --- --- Goodwill adjustment 7,000 --- ---

Loan 28,500 --- ---

Balances c/d ---- 26,200 16,800

57,000 30,000 20,000 57,000 30,000 20,000 3. Anderson, Benson, Cindy and Derek have been in partnership, sharing profits and losses in the ratio of 3 : 2 : 4 : 1, respectively.

Their capital accounts and current accounts showed the following balances as at 31 December 2010: Capital account: Anderson $250,000 Cr Benson $180,000 Cr Cindy $270,000 Cr Derek $320,000 Cr

Current account: Anderson $32,330 Cr Benson $42,100 Cr Cindy $12,560 Dr Derek $57,080 Cr

Additional information: (i) Each partner was entitled to a monthly salary of $10,000. (ii) Drawings of partners up to 30 June 2011 were as follows: Anderson $2,500 Benson $1,340 Cindy $5,200 Derek $6,000 (iii) Owing to her poor health, Cindy decided to withdraw from the partnership with effect from 1 July 2011. By agreement,

goodwill was valued as the average of the past three years’ profits minus the interest on capital as at 31 December 2010 that would have been earned by investing outside. No goodwill account was opened in the partnership’s books. The new profit and loss sharing ratio would be: Anderson 3 : Benson 2 : Derek 1.

(iv) Profits of the business over the past three years were as follows: Year $ 2008 480,500 2009 500,100 2010 621,800 (v) Profits for the first six months of 2011 before deducting partners’ salaries were $389,000. (vi) Interest on capital that could be earned by investing outside was assumed to be 20% per annum. (vii) The balance in Cindy’s current account would be transferred to her capital account. (viii) The balance in Cindy’s capital account would be settled by issuing her a cheque immediately. (ix) On 1 September 2011, Eason was admitted to the partnership with an initial capital contribution of $250,000. Goodwill was

valued at $255,000. A goodwill account was maintained in the partnership’s books. Required: Prepare the partners’ current accounts and capital accounts as at 1 September 2011. (to the nearest dollar)

20

Answer: Current

Anderson Benson Cindy Derek Anderson Benson Cindy Derek

2011 $ $ $ $ 2011 $ $ $ $

Jan 1 Balance b/f — — 12,560 — Jan 1 Balances b/f 32,330 42,100 — 57,080

Jun 30 Drawings 2,500 1,340 5,200 6,000 Jun 30 Salaries 60,000 60,000 60,000 60,000

" 30 Capital: Cindy — — 101,840 — " 30 Share of profit 44,700 29,800 59,600 14,900

" 30 Balances c/f 134,530 130,560 — 125,980

137,030 131,900 119,600 131,980 137,030 131,900 119,600 131,980

Capital

Anderson Benson Cindy Derek Anderson Benson Cindy Derek

2011 $ $ $ $ 2011 $ $ $ $

Jun 30 Goodwill adj. 66,027 44,017 — 22,009 Jan 1 Balances b/f 250,000 180,000 270,000 320,000

" 30 Bank — — 503,893 — Jun 30 Goodwill adj. — — 132,053 —

" 30 Balances c/d 183,973 135,983 — 297,991 " 30 Current: Cindy — — 101,840 —

250,000 180,000 503,893 320,000 250,000 180,000 503,893 320,000

Capital

Anderson Benson Eason Derek Anderson Benson Eason Derek

2011 $ $ $ $ 2011 $ $ $ $

Sept 1 Balances c/d 311,473 220,983 250,000 340,491 Jul 1 Balances b/d 183,973 135,983 — 297,991

Sept 1 Bank — — 250,000 —

" 1 Goodwill 127,500 85,000 — 42,500

311,473 220,983 250,000 340,491 311,473 220,983 250,000 340,491

4. Test 4

(W1) $ $

Profit before deducting partners’ salaries from January to June 2011 389,000

Less Partners’ salaries:

Anderson ($10,000 6) 60,000

Benson ($10,000 6) 60,000

Cindy ($10,000 6) 60,000

Derek ($10,000 6) 60,000 (240,000)

Profit after deducting partners’ salaries from January to June 2011 149,000

Balance of profit shared:

Anderson ($149,000 3/10) 44,700

Benson ($149,000 2/10) 29,800

Cindy ($149,000 4/10) 59,600

Derek ($149,000 1/10) 14,900 149,000

(W2) Calculation of goodwill:

Year $ 2008 480,500 2009 500,100 2010 621,800

Total net profit over the past three years 1,602,400

Average net profit over the past three years ($1,602,400 ÷ 3) (A) $534,133

Capital as at 31 December 2010:

$

Anderson 250,000

Benson 180,000

Cindy 270,000

Derek 320,000

1,020,000

Interest on capital that could have been earned by investing outside ($1,020,000 20%) (B) $204,000

= (A) – (B) $330,133

(W2) Calculation of goodwill: Year $ 2008 480,500 2009 500,100 2010 621,800

Total net profit over the past three years 1,602,400

Average net profit over the past three years ($1,602,400 ÷ 3) (A) $534,133

Capital as at 31 December 2010:

$

Anderson 250,000

Benson 180,000

Cindy 270,000

Derek 320,000

1,020,000

Interest on capital that could have been earned by investing outside ($1,020,000 20%) (B) $204,000

= (A) – (B) $330,133

Goodwill Adjustment

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment Anderson (3/10)$99,040 (3/6)$165,067 $66,027 Dr Capital: Anderson $66,027 Benson (2/10)$66,027 (2/6)$110,044 $44,017 Dr Capital: Benson $44,017 Cindy (4/10)$132,053 — ($132,053) Cr Capital: Cindy $132,053 Derek (1/10)$33,013 (1/6)$55,022 $22,009 Dr Capital: Derek $22,009

$330,133 $330,133

21

13X

Chung and Wun were partners, sharing profits and losses in the ratio of 2 : 1. They agreed that interest was to be

allowed on capital balances at 8% per annum. No interest would be allowed on credit balances in the current accounts,

but interest of 10% per annum would be charged on any debit balances in the current accounts.

The capital and current account balances as at 31 December 2009 were as follows: Capital Current

Chung $60,000 $37,600

Wun $40,000 $7,800 Dr

They agreed to admit their finance manager, Tang, as a partner on 1 January 2010 on the following terms:

(i) Goodwill of the old partnership was valued at $36,000. No goodwill account was to be opened.

(ii) The new profit and loss sharing ratio was: Chung 4, Wun 3 and Tang 3.

(iii) Tang was to be paid an annual salary of $36,000 on the last day of each financial year.

(iv) Tang brought in cash of $20,000 on 1 January 2010.

Additional information:

1 The net profit before appropriations for the year ended 31 December 2010 was calculated as $180,000. However, it

was found that insurance on Tang’s private car of $2,000 had been charged as a business expense. In addition, a sales

invoice of $3,600 and a purchases invoice of $9,800, had been completely omitted from the books. 2 The drawings made in the year 2010 were as follows:

Chung Wun Tang

1 April $60,000 — —

1 July $10,000 — $48,000

1 October $10,000 — — You are required to:

(a) Prepare an income statement (extract) for the partnership for the year ended 31 December 2010.

(b) Draw up the partners’ current accounts for the year ended 31 December 2010.

(c) Explain why interest is allowed on capital balances but is charged on any debit balances in current accounts.

(a)

Chung, Wun and Tang Income Statement for the year ended 31 December 2010 (extract)

$ $ $

Net profit 175,800

Add Interest on current accounts:

Chung 1,710

Wun ($7,800 $1,200) x 10% 660

Tang [(10,800 x 10% x 6/12) + ($10,800 + $48,000) x 10% x 6/12] 3,480 5,850

181,650

Less Salary: Tang 36,000

Interest on capital:

Chung ($60,000 × 8%) 4,800

Won ($40,000 × 8%) 3,200

Tang ($20,000 × 8%) 1,600 9,600 (45,600)

136,050

Balance of profit shared:

Chung (4/10) 54,420

Wun (3/10) 40,815

Tang (3/10) 40,815 136,050

Interest on current account – Chung $ Apr – Jun ($60,000 − $37,600 − $9,600) × 10% × 3/12 = 320 Jul – Sept ($12,800 + $10,000) × 10% × 3/12 = 570 Oct – Dec ($22,800 + $10,000) × 10% × 3/12 = 820

1,710

Interest on current account – Wun ($7,800 − $1,200) × 10% = $660 Interest on current account – Tang

$ Jan – Jun $10,800 × 10% × 6/12 = 540 Jul – Dec ($10,800 + $48,000) × 10% × 6/12 = 2,940

3,480

Goodwill Adjustment

Partner Goodwill shared in old ratio Goodwill shared in new ratio Gain (loss) from change in ratio Required adjustment

Chung (2/3)$24,000 (4/10)$14,400 ($9,600) Cr Current: Chung $9,600

Wun (1/3)$12,000 (3/10)$10,800 ($1,200) Cr Current: Wun $1,200

Tang — (3/10)$10,800 $10,800 Dr Current: Tang $10,800

$36,000 $36,000

22

(b)

Current: Chung

2010 $ 2010 $

Apr 1 Drawings 60,000 Jan 1 Balance b/f 37,600

Jul 1 Drawings 10,000 “ 1 Goodwill adjustment (W2) 9,600

Oct 1 Drawings 10,000 Dec 31 Interest on capital 4,800

Dec 31 Interest on current a/c 1,710 “ 31 Profit and loss appropriation –

“ 31 Balance c/d 24,710 Share of profit 54,420

106,420 106,420

Current: Wun

2010 $ 2010 $

Jan 1 Balance b/f 7,800 Jan 1 Goodwill adjustment (W2) 1,200

Dec 31 Interest on current a/c 660 Dec 31 Interest on capital 3,200

“ 31 Balance c/d 36,755 “ 31 Profit and loss appropriation –

Share of profit 40,815

45,215 45,215

Current: Tang

2010 $ 2010 $

Jan 1 Goodwill adjustment (W2) 10,800 Dec 31 Interest on capital 1,600

Jul 1 Drawings 48,000 “ 31 Salary 36,000

Dec 31 Interest on current a/c 3,480 “ 31 Profit and loss appropriation –

“ 31 Balance c/d 16,135 Share of profit 40,815

78,415 78,415

(c) Interest may be allowed on partner’s capital as a minimum return on their capital contributions. A debit

balance in the current account represents excessive drawings made by the partner. Charging interest on a

debit balance is similar to charging interest on drawings and is done for a similar reason. Both are used to

discourage drawings.

23