Embed Size (px)

Citation preview

DO YOU REALLY NEED A LOCAL POLICY?GRM 005

Speakers:

• Roxsann Wilson, Vice President, Risk Management, Cardinal Health, Inc.

• Rick Jensen, Managing Director, Willis Towers Watson

Learning Objectives

At the end of this session, you will:

• Answer the seven questions that determine your need for a local policy

• Weigh the relative need for a local policy in various countries

• Identify the parties—inside and outside your company—who can help you decide the local policy question

Background

• CMPs: Coverage and Cost optimization

• Past practice• 60s/70s

• “FLEXA plus DIC”

• Increased regulatory and fiscal scrutiny

• Increased risks to insureds/insurers/brokers• Retrospective tax liabilities, fines and penalties

• Local authorities may declare sanctions against local operations

• Carriers could lose their license

• Strict penalties, including fines, suspensions and imprisonment of offending insurers

• Penalties could apply to insured, the insurer and/or broker

Landscape

• Over 90% of countries have restrictions on the use of non-admitted insurance

• Almost no country entirely open (think compulsory covers)

• Example: USA

• Many countries – very few exceptions

How Strict?

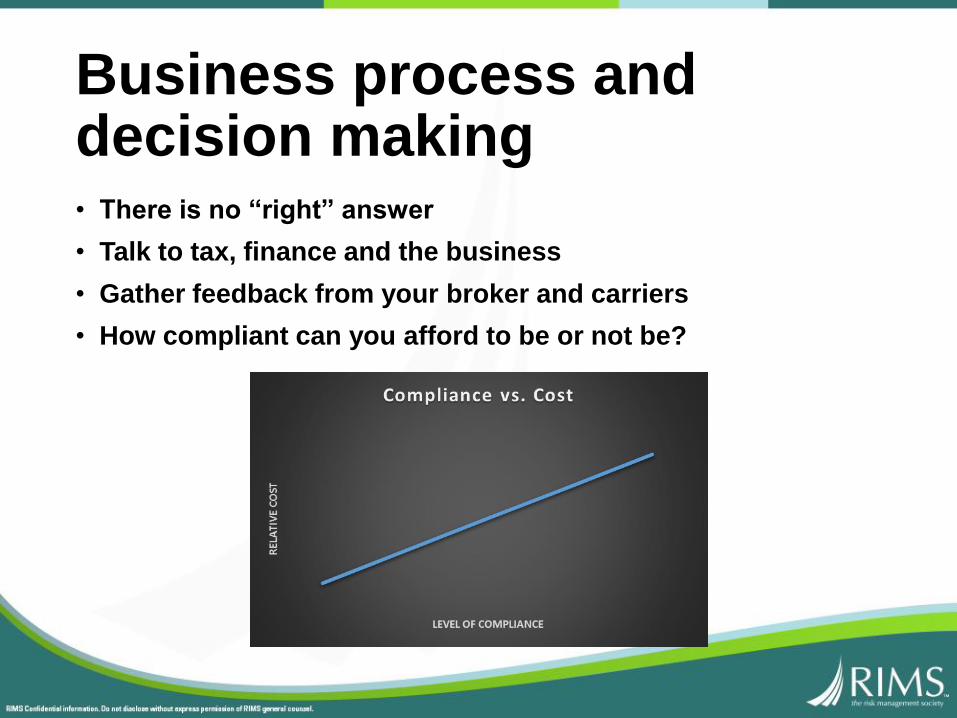

Business process and decision making• There is no “right” answer

• Talk to tax, finance and the business

• Gather feedback from your broker and carriers

• How compliant can you afford to be or not be?

Business process and decision making• Ask yourself, if you have a loss, where would you want it to

be paid?

• What are the implications from a tax perspective?• If the local entity is receiving the benefit of the global coverage, they

should be allocated premium.

• Some carriers will file the local taxes without requiring a local policy to be issued.

• Premium tax is payable even if premiums are not internally charged.

• Premium taxes can be substantial depending on the country — 1-24%

• Will the local entity be able to deduct premiums? Are they profitable?

Business process and decision making• Is “Good Local Standard” good enough?

• Challenges in getting indemnification payments from DIC/DIL to the country.

• Do you need the local policy to match the master terms and conditions?

• What are the implications for Cash flow?

=

Enable the business

• Meet your contractual requirements:

• Leases

• Customers

• Governmental agencies

• To whom do you need to provide evidence of coverage?

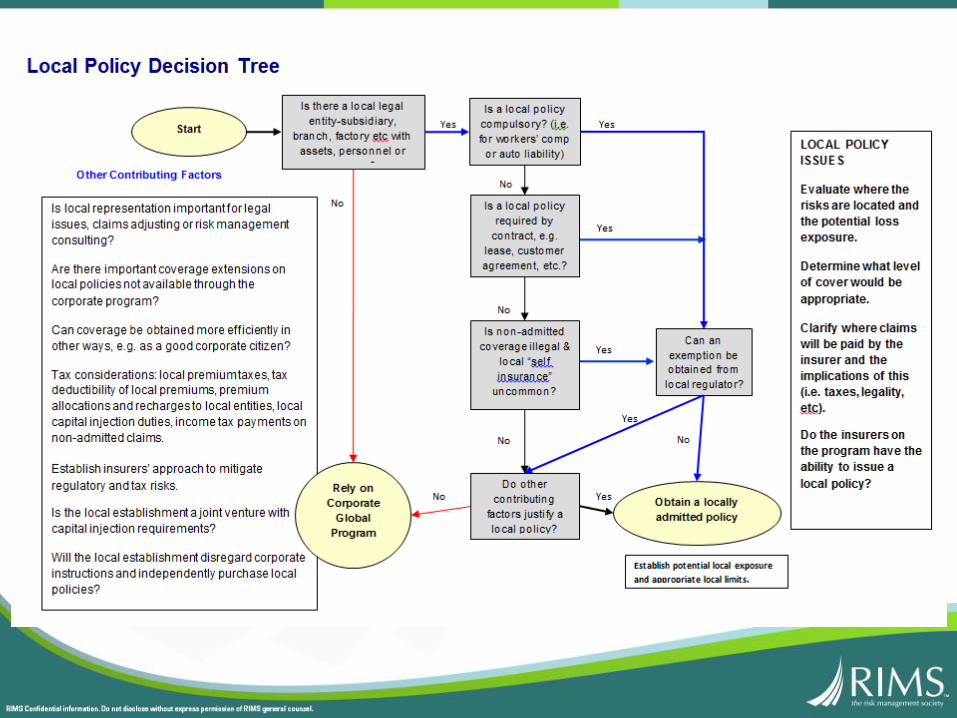

Decision Tree

• Do you have a local entity?

• Is the coverage compulsory?

• Are there any specific laws? Environmental, PL for Pharma, etc.

• Is non-admitted permitted?

• What are the size and scope of your operations?

• Are there contractual obligations?

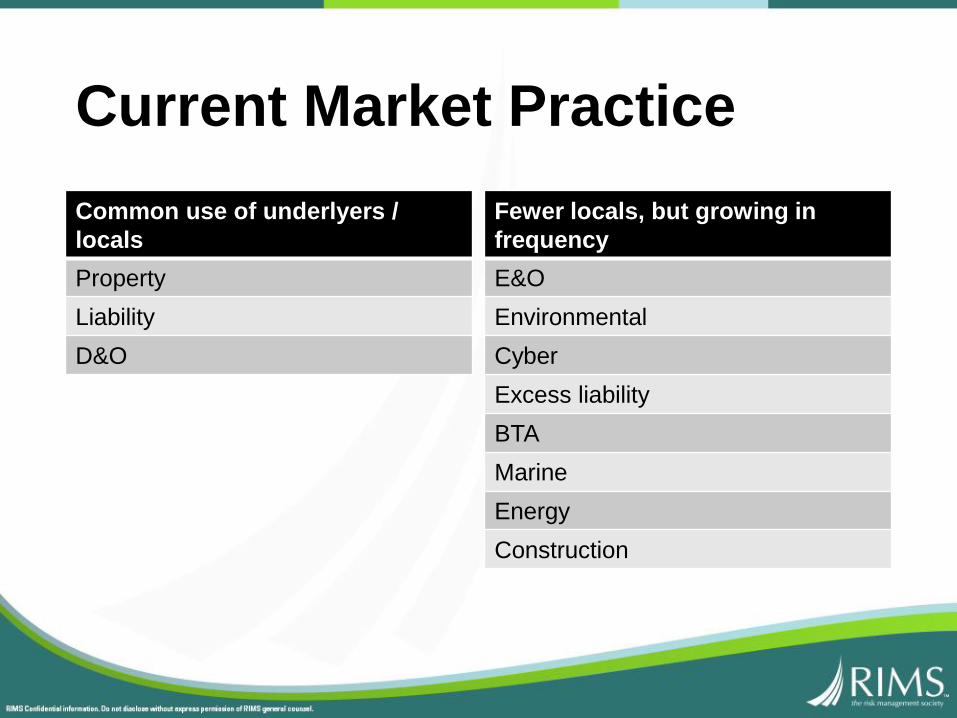

Current Market Practice

Common use of underlyers /

locals

Property

Liability

D&O

Fewer locals, but growing in

frequency

E&O

Environmental

Cyber

Excess liability

BTA

Marine

Energy

Construction

Directors & Officers

• Are you able to indemnify?

• Do you have local directors — or equivalents?

• What is the size & scope of local operations?

• What is the local regulatory environment?

• Brazil, China, India, Russia

Casualty

• Why would you NOT have a local policy?

• Lower limits than e.g. property

• Cost tends to be low

• Defense

• Foreign legal system

• Lack of local in-house counsel?

• Language of policy

• Considerations:

• All losses depend on local law

• Litigiousness of territory

• Local limits desired/needed

Property

• Questions to ask:

• Who owns the inventory?

• Where do you want the loss paid?

• Where do you report BI vs. where the loss occurs?

• Considerations:

• “Good Local Standard” coverage is often very limited

• Focus on local contract certainty

• Difficulty getting indemnification from DIC/DIL coverage

Deductibles and cost optimization

• Is your policy issued out of Lloyds of London?

• Won’t need to issue local policies in countries where they are licensed.

• Can you use an FOS to reduce the administrative costs?

• Do you allow differentiation of deductible levels?

• FX impact – some markets are seeing increases of 20-60%

• Tariff-rated countries

• Increased demand for “full limit” local programs

• Allocations – different carriers have different approaches

Challenges

Countries/Regions Factors

• Cross-border regulatory cooperation

• Fiscal vs. insurance

• IAIS positions; industry efforts

Challenges once you decide to move forward• Ability to pay & sign for the policy locally

• Administration of the program

• Carrier limitations

• Allocations

• Cash before coverage – China, India, Japan, Puerto Rico, S. Korea, parts of Africa

So?Do you really need a local policy?

• Default answer? Yes, but. . .

• Real answers vary by situation — ask the questions• Is the coverage compulsory?

• Does the country “require” locally admitted cover for the subject policy?

• Do you need to evidence local insurance?

• Your operations — are they material in size and scope?

• Who are your customers?

• Do you want or need to allocate the premium to the local operation?

• Do you need for claims to be paid directly into the country?

Questions?

![[E조] 미디어프로젝트(really)](https://img.pdfslide.tips/doc/110x75/557a9544d8b42aac568b46a6/e-really.jpg)