Embed Size (px)

Citation preview

1

INVESTING IN THE FUTUREof Healthcare

Jefferies 2015 Global Healthcare Conference

June 1, 2015

2

SAFE HARBOR

This presentation includes “forward-looking statements” within the meaning of securities laws of applicable jurisdictions.

Forward-looking statements can generally be identified by the use of forward-looking words such as “may”, “will”, “would”,

“could”, “expect”, “intend”, “plan”, “aim”, “estimate”, “target”, “anticipate”, “believe”, “continue”, “objectives”, “outlook”,

“guidance” or other similar words, and include statements regarding MPT’s plans, strategies, objectives, targets, future

expansion and development activities and expected financial performance. Forward-looking statements involve known and

unknown risks, uncertainties and other factors that may cause the actual results of the Company or future events to differ

materially from those expressed in or underlying such forward-looking statements, including without limitation: the

satisfaction of all conditions to, and the timely closing (if at all) of the MEDIAN acquisition and sale-leaseback transactions;

the Company’s financing of the transactions described herein; the capacity of MEDIAN and the Company’s other tenants to

meet the terms of their agreements; expected rent coverage; Normalized FFO per share; expected payout ratio, the

amount of acquisitions of healthcare real estate, if any; capital markets conditions, the repayment of debt arrangements;

statements concerning the additional income to the Company as a result of ownership interests in certain hospital

operations and the timing of such income; the payment of future dividends, if any; completion of additional debt

arrangement, and additional investments; national and international economic, business, real estate and other market

conditions; the competitive environment in which the Company operates; the execution of the Company's business plan;

financing risks; the Company's ability to maintain its status as a REIT for federal income tax purposes; acquisition and

development risks; potential environmental and other liabilities; and other factors affecting the real estate industry generally

or healthcare real estate in particular; and the value of our real estate assets, which may limit our ability to dispose of

assets at attractive prices or obtain or maintain equity or debt financing secured by our properties or on an unsecured

basis, and the factors referenced under the section captioned “Item 1.A Risk Factors” in our annual report on Form 10-K for

the year ended December 31, 2014. Actual results, performance or achievements may vary materially from any projections

and forward looking statements and the assumptions on which those statements are based. Readers are cautioned not to

place undue reliance on forward-looking statements, and MPT disclaims any responsibility to update such information.

3

INTRODUCTION TO MEDICAL PROPERTIES TRUST

Unparalleled expertise in hospital real estate, finance and operations

4

FOCUSING EXCLUSIVELY ON THE MOST CRITICALcomponents of healthcare delivery

MPT FOCUSES ON

the heart of healthcare:

• General Acute Care hospitals

• Long Term Acute Care hospitals

• Inpatient Rehabilitation hospitals

SKILLED

NURSING

facilities

INPATIENT

REHAB

hospitals

MEDICAL

office

ASSISTEDliving

HOMEHEALTH

care

GENERAL

ACUTE CARE

hospitals

LTAC

hospitals

INDEPENDENTliving

5

PORTFOLIO OVERVIEW

Note: Portfolio statistics as of March 31, 2015 and assume fully funded commitments and consummation of the MEDIAN transaction.

(1) Includes 3 medical office buildings and 6 wellness centers.

1

6

INVESTMENT THESIS

Stable and predictable income from essential community assets

7

ALWAYS A NEED

FOR HOSPITALS

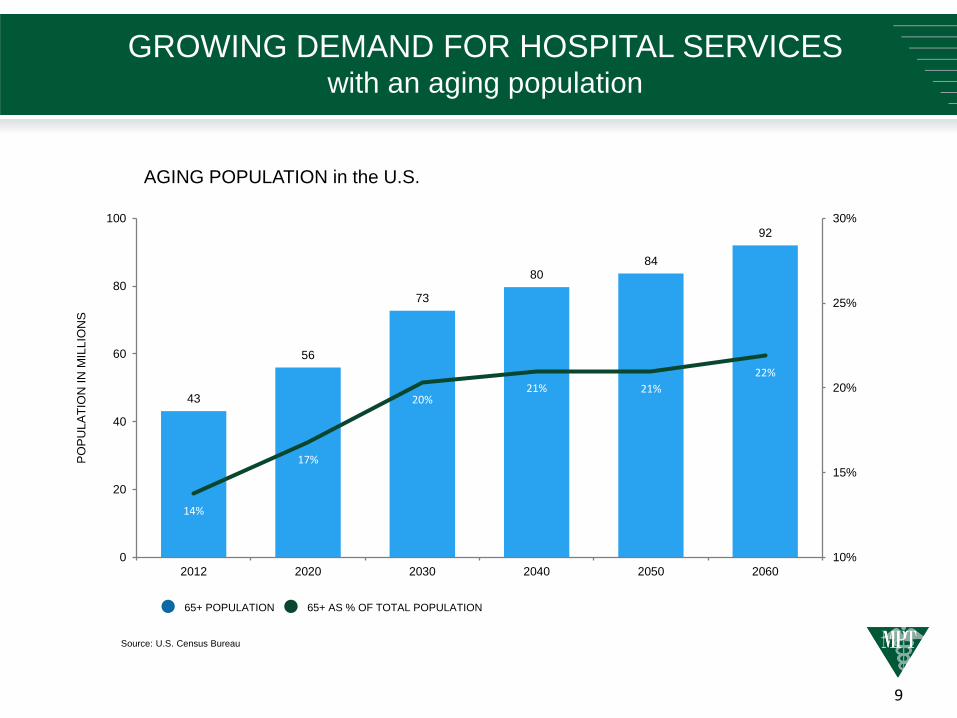

• An aging population will result in increased demand for hospital services

• Healthcare will continue to evolve, but hospitals will remain foundational

to the effective delivery and coordination of care

CRITICAL PART OF

COMMUNITY

INFRASTRUCTRE

HOSPITAL

ECONOMICS

• Specialized physical plant is essential to the diagnosis and treatment

of acute illness

• Hospitals are big employers in local communities ~ 4.8 million full-time

equivalent hospital workers in the U.S.

• Physical relocation is often impractical

• Physician and patients are resistant to new locations

• Highest yielding healthcare real estate

• Well run hospitals generate strong margins

• Lease payments represent minor portion of net revenue

• Hospitals economics are improving

• CMS projects hospital expenditures will increase at 6% CAGR over

next 10 years

HOSPITALS ARE NEEDED IN THEIR COMMUNITIES and current dynamics are highly favorable

8

HIGHER RENTAL YIELDS and lease coverages from hospitals

• Hospitals provide the highest rental yields in healthcare real estate

• Superior lease coverage compared to other healthcare property types

2014 RETURNS

from Healthcare Real Estate1

LEASE COVERAGE

by Property Type2

11%

10%

9%

0%

2%

4%

6%

8%

10%

12%

LTACH Acute Care IRF

4.3

2.01.9

1.4

1.2

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

AcuteCare

IRF LTACH SkilledNursing

SeniorHousing

(1) Actual MPT Real Estate returns through December 31, 2014.

(2) MPT TTM lease coverage as of February 28, 2015 for mature portfolio (properties in portfolio at least one year). Lease coverage ratios are

derived solely from the financial information provided to us by our tenants. We do not independently audit or otherwise verify this information.

Senior Housing average and Skilled Nursing average are calculated as the average of lease coverage for the HCN, HCP and VTR in respective

property types. Lease coverage defined as EBITDAR divided by rent payment under the lease.

9

43

56

73

8084

92

14%

17%

20%21% 21%

22%

10%

15%

20%

25%

30%

0

20

40

60

80

100

2012 2020 2030 2040 2050 2060

PO

PU

LA

TIO

N I

N M

ILL

ION

S

AGING POPULATION in the U.S.

Source: U.S. Census Bureau

65+ POPULATION 65+ AS % OF TOTAL POPULATION

GROWING DEMAND FOR HOSPITAL SERVICESwith an aging population

10

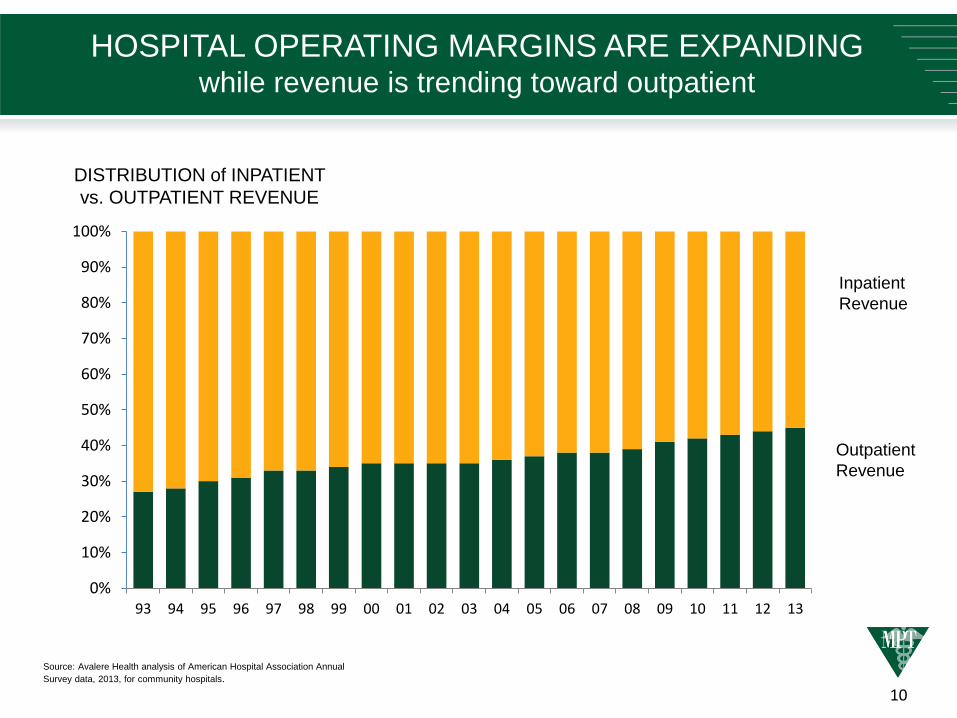

HOSPITAL OPERATING MARGINS ARE EXPANDING while revenue is trending toward outpatient

Source: Avalere Health analysis of American Hospital Association Annual

Survey data, 2013, for community hospitals.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

DISTRIBUTION of INPATIENT

vs. OUTPATIENT REVENUE

Inpatient

Revenue

Outpatient

Revenue

11

DISCIPLINED PORTFOLIO MANAGEMENTand a comprehensive investment process

Solid shareholder returns from a well-diversified and growing portfolio

12

HISTORY OF ATTRACTIVE shareholder returns

16.5%

20.8%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

RMS

89%

83%

79%

50%

60%

70%

80%

90%

2012 2013 2014

4.5% 4.5%

5.7%

6.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

CURRENT DIVIDEND Yield MPT PAYOUT Ratio AVERAGE ANNUAL

Total Return (2012 - Q1 2015)

(1) Peer yields from Bloomberg as of May 28,2015. MPT yield based on Q1 annualized dividend and share price as of May 28, 2015.

(2) Based on annualized share price performance between 12/30/11 and 3/31/15 inclusive of dividend reinvestment, sourced from FactSet.

(3) RMS is the MSCI US REIT Total Return Index.

Source: Bloomberg, FactSet

3

1

2

13

5%

19%

17%

11%11%

7%

5%

3%2%

2%

2%

16%

Note: Mix based on investment amounts. Property type diversification by investment based on both U.S. and European investments. All measures are pro forma for uncompleted

acquisitions and development commitments, including the acquisition of MEDIAN.

27 Operators

STRONG PORTFOLIO DIVERSIFICATIONgenerates reliable cash flow

Property Type Breakdown Operator Breakdown

54%

1%5%

IASIS

ADEPTUS/FC

RHM

PRIME

ERNEST

MEDIAN

ALECTO

IJKG/HUMC

LHP

KINDRED

18 OTHER OPERATORS

NON RE ASSETS

9%

31%

OTHER

NON RE ASSETS

GENERAL ACUTE CARE

LONG-TERM ACUTE

INPATIENT REHABILITATION

176 Properties

International Geographic Mix

UNITED STATES

GERMANY

UNITED KINGDOM

77%

22%

1%

3 Countries

14

MPT’S OPERATOR REVENUE comes from reliable payors

(1) Based on MPT US portfolio.

(2) Based on breakdown of total German rehab market.

(3) Includes private insurance, employers insurance for civil servants, accident insurance, self pay and others.

(4) Based on payor breakdown for MPT’s facility in the UK.

PAYOR MIX- United States1

38%

37%

13%

11%1%

MEDICARE MEDICAID OTHER

MANAGED CARE SELF PAY

PAYOR MIX-

Germany Rehab2

31%39%

30%

PENSION FUNDS

STATUTORY HEALTH

INSURANCE

OTHER

PAYOR MIX- UK4

35%

65%

NATIONAL HEALTH SERVICE

PRIVATE3

15

CONTINUED DIVERSIFICATIONhas reduced property concentration

CONCENTRATION BY Largest Property

16%

9%

6%7%

4%3%

2.9% 2.6%

0%

5%

10%

15%

20%

20

04

20

06

20

08

20

10

20

12

20

13

20

14

20

15

PF

Low near-term lease maturity levels provide MPT

with stable, predictable cash flows, with no single property

accounting for > 2.6% of MPT’s portfolio

(1) 2015 PF property concentration is pro-forma for uncompleted acquisitions, including the acquisition of MEDIAN.

Note: The MEDIAN Transactions and asset development commitments are fully funded.

1

16

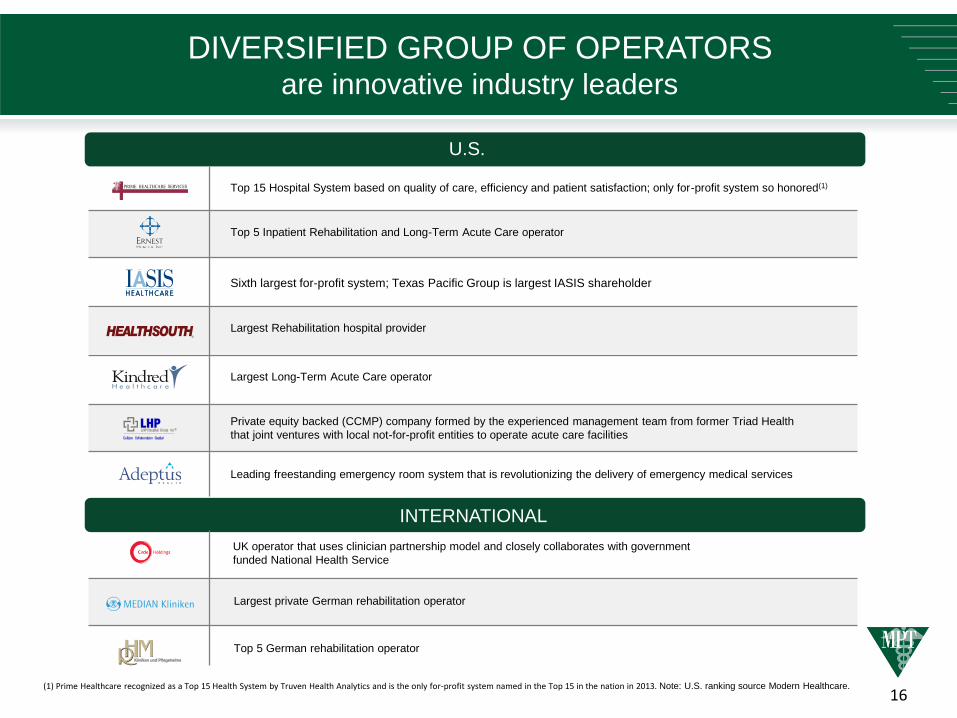

DIVERSIFIED GROUP OF OPERATORSare innovative industry leaders

U.S.

INTERNATIONAL

(1) Prime Healthcare recognized as a Top 15 Health System by Truven Health Analytics and is the only for-profit system named in the Top 15 in the nation in 2013. Note: U.S. ranking source Modern Healthcare.

Top 15 Hospital System based on quality of care, efficiency and patient satisfaction; only for-profit system so honored(1)

Top 5 Inpatient Rehabilitation and Long-Term Acute Care operator

Sixth largest for-profit system; Texas Pacific Group is largest IASIS shareholder

Largest Rehabilitation hospital provider

Largest Long-Term Acute Care operator

Private equity backed (CCMP) company formed by the experienced management team from former Triad Health

that joint ventures with local not-for-profit entities to operate acute care facilities

Leading freestanding emergency room system that is revolutionizing the delivery of emergency medical services

UK operator that uses clinician partnership model and closely collaborates with government

funded National Health Service

Largest private German rehabilitation operator

Top 5 German rehabilitation operator

17

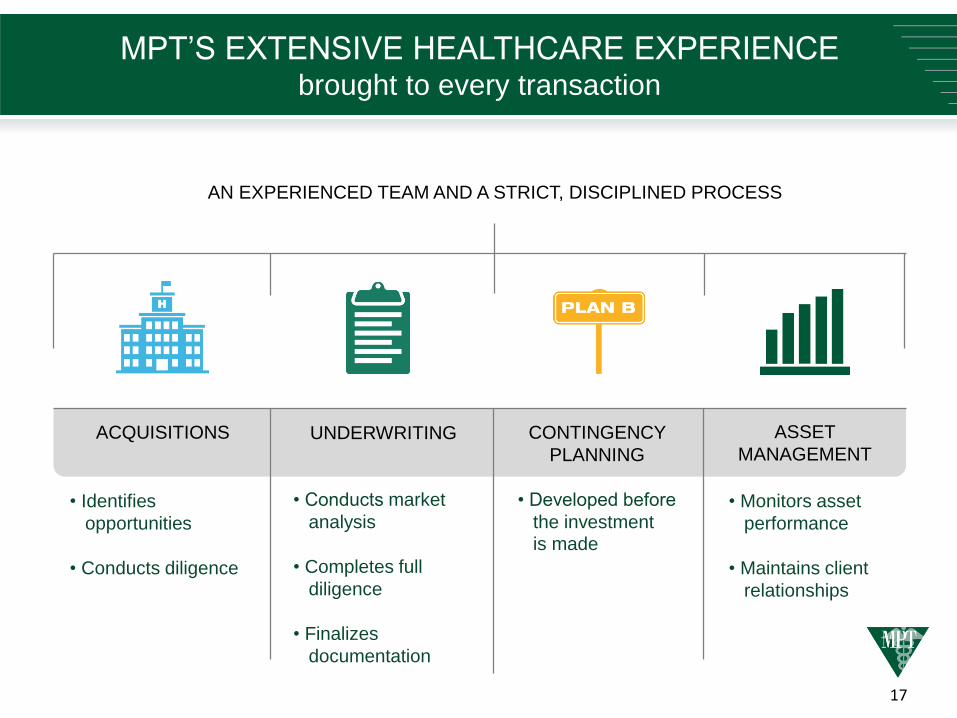

MPT’S EXTENSIVE HEALTHCARE EXPERIENCEbrought to every transaction

AN EXPERIENCED TEAM AND A STRICT, DISCIPLINED PROCESS

ACQUISITIONS UNDERWRITING CONTINGENCY

PLANNING

ASSET

MANAGEMENT

• Monitors asset

performance

• Maintains client

relationships

• Identifies

opportunities

• Conducts diligence

• Developed before

the investment is made

• Conducts market

analysis

• Completes full

diligence

• Finalizes

documentation

18

AN EXEMPLARY INVESTMENT track record

MPT’S UNDERWRITING EXPERIENCE

and Lease Provisions Protect

Against Losses

• Deep industry knowledge

(MPT knows hospitals)

• Investing in critical community

infrastructure (“Hospitals needed

by the community don’t fail”)

• Underwriting conservatively

(We always have a “Plan B”)

• Lease Defaults Provide

Opportunity to Reset Rates

TOTAL REAL ESTATE INVESTMENTS

<1% Credit Losses over 10 Years

41▀

1

(1) Does not include MEDIAN transactions.

19

STRONG EXTERNAL GROWTH from robust acquisition activity

$0.66 $0.71

$0.90 $0.96

$1.06

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

2010 2011 2012 2013 2014

$213

$331

$801

$700

$1,378

$416

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2010 2011 2012 2013 2014 YTD2015

MPT’s disciplined acquisition strategy has driven Normalized

FFO per share growth of 12.6% per annum since 2010.

Acquisitions continue to be immediately accretive to FFO.

INVESTMENTS/COMMITMENTS ($mm) NORMALIZED FFO Per Share

20

98% OF LEASES AND MORTGAGE LOANS HAVE FIXED OR CPI LINKED RENT ESCALATORS

0% to 5% increase in CPI, MPT Rents increase:

Total Leases and Mortgage Loans Pro Forma Escalated Rate

Investment Value1

Percent of Investments Escalation Provisions

$2,581,000,000 60% Full CPI (92% have a floor of 1% to 2.65%)

$1,187,000,000 27% CPI-based, most with collars ranging from 1% floor to 5% ceiling

$480,000,000 11% Fixed increases, averaging 2.4%

$67,000,000 2% Flat

$4,315,000,000

$4.3 BILLION 1.4% - 4.0%

Note: Rents would increase based on 2015 rent; Investment value includes construction in progress and assumes fully funded development projects.

(1) Value based on undepreciated book value as of March 31, 2015 and is inclusive of MEDIAN real estate transaction and completed development projects.

1

STABLE & PREDICTABLE INTERNAL GROWTH

21

0%

1%

0%

1%

2%

0%

4%

11%

4%

1%

4%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

WELL-COVERED LEASES WITH long-term maturities

Provide long-term, inflation-protected cash

returns from critical community assets

Average annual lease maturities

through 2021 < 1.2% per annum

LEASE MATURITY Schedule

95% of 2022

Maturities under

Master Lease

Master Lease

elections are all

or none

OPERATOR OPTIONS AT MATURITY

MOST OFTEN: Elect to extend

Typically 5 years at contractual escalations

OCCASIONALLY: Elect to repurchase

Typically at the greater of fair value

or MPT’s investment

RARELY: Elect to vacate

Typically obligated to transition

business to a new operator

(1) Lease maturity schedule is pro-forma for MEDIAN transaction as of March 31, 2015.

1

22

• $723MM of revolver capacity available

for investments as of March 31, 2015

• 100% of non-credit facility debt is fixed

rate or swapped to fixed rate

• Well-staggered debt maturities

• Company’s Senior Notes recently

upgraded by S&P to investment grade2

• Long term net leverage target of 40-

45%

• Net Debt / Adjusted EBITDA target of

5.5x

• Targeting investment grade ratings

(1) As of March 31, 2015. Senior unsecured notes due 2020 are €200 million. Debt due in 2022 excludes debt premium.

(2) On December 1, 2014 S&P upgraded MPT’s corporate credit rating to BB+ from BB, with a stable outlook, post announcement of the acquisition of MEDIAN. Rating of Senior

Notes was also raised to BBB- from BB.

$125$215

$450

$350$300$302

$723

$125

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

$1,100

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Senior unsecured notes Secured loans Credit Facility Available Term Loans

PRUDENT CAPITAL STRUCTURE

DEBT MATURITIES ($ in million)1

23

SUSTAINABLE GROWTH IN THE U.S.and internationally

Increased capital needs and a growing acceptance of sale leaseback model

24

Continue to penetrate and lead

the U.S. hospital market

Deepen investments in

hospital operations

Expand into new markets

at home and abroad

Add new, high-acuity sectors that

complement our portfolio

78+ Million “Baby Boomers”

8,000/day will turn 65 through 2029

More than 60% have at least one chronic disease

Maintain as limited part of total investments

Small investments relative to the associated triple net lease component

Licensed ER Hospitals

Free-standing high traffic physician staffed Emergency facilities

All are passive

Western Europe

MPT’S GROWTH STRATEGIES

25

GOVERNMENT INITIATIVE / EVENT

INTERNATIONAL DIVERSIFICATON REDUCES RISKof disruptions in U.S. hospital M&A activity

Health Maintenance Organization (HMO) Act of 1973

Diagnosis-related Groups (DRGs) implemented by HCFA (now CMS)

Health Security Act “HillaryCare”

Balanced Budget Amendment

U.S. Presidential Elections

Patient Protection and Affordable Care Act (PPACA)

1973

1983

1993

1997

2008

2010

26

United States Western Europe(1)

GovernmentVery stable

Democratic process to elect political leaders

Very stable

Democratic process to elect political leaders

Demographics

Laws Affordable Care Act – movement towards universal care Universal healthcare and reimbursement mandated by law

Opportunities

for Growth

Continued opportunities for growth primarily through acquisition and

development of private and for-profit hospitals

Increasing opportunities for growth as private for-profit hospital operators

recognize the benefits of sale/leaseback financing model to fund facility

improvements, technology upgrades, staff additions and new construction

Germany UK

Payors

Medicare – Federal government sponsored

Medicaid – State and Federal government sponsored

Commercial insurance - Private

Statutory Health Insurance (SHI)

Pension Funds (DRV) – National

and Regional funds that pay for

rehabilitation services

Private Health Insurance – limited

to higher earners

National Health Service (NHS) –

Single payor government system

Private Health Insurance

Coverage

Coverage depends on individual’s ability to pay and/or plan

benefits

Insurance primarily offered through employers and government

German law mandates universal

access and coverage; SHI and DRV

covers 90% of German population

In the UK, defined healthcare

benefits are free to all residents of

the UK through the NHS

Physicians

Combination of private practice and employment model

Rate determined by government and negotiated health plans

German physicians are employed

doctors

While most physicians are employed

by NHS, they are free to admit

patients to private healthcare

facilities.

Hospital

Ownership

(1) Countries constituting Western Europe from UCLA Center for European and Eurasian Studies - web.international.ucla.edu/euro/countries/westeurope.

(2) 2012 population estimates from The World Bank - data.worldbank.org/indicator/SP.POP.TOTL.

21%

58%

21%

Public Not-for-profit

Private Not-for-profit

Private For-profit

314M Total(2)

Under 65

65+

413M Total(2)

87% 13% 19%81%

50%

33%

17%

92%

0%

8%

ATTRACTIVE HEALTHCARE MARKETS

throughout Western Europe

27

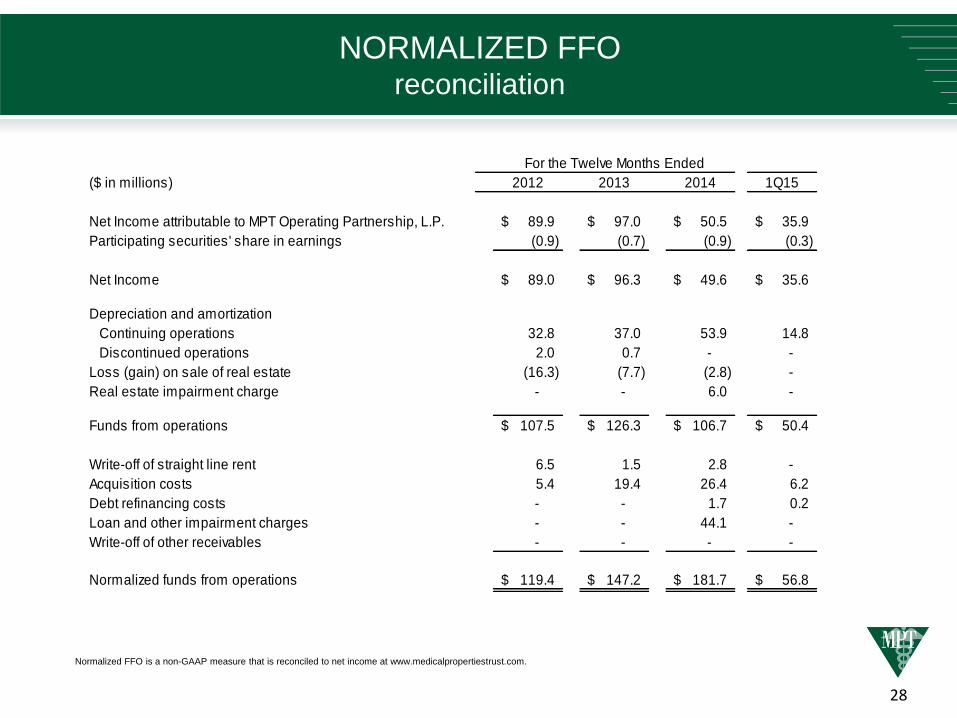

APPENDIX

Normalized FFO Reconciliation

28

Normalized FFO is a non-GAAP measure that is reconciled to net income at www.medicalpropertiestrust.com.

($ in millions) 2012 2013 2014 1Q15

Net Income attributable to MPT Operating Partnership, L.P. 89.9$ 97.0$ 50.5$ 35.9$

Participating securities' share in earnings (0.9) (0.7) (0.9) (0.3)

Net Income 89.0$ 96.3$ 49.6$ 35.6$

Depreciation and amortization

Continuing operations 32.8 37.0 53.9 14.8

Discontinued operations 2.0 0.7 - -

Loss (gain) on sale of real estate (16.3) (7.7) (2.8) -

Real estate impairment charge - - 6.0 -

Funds from operations 107.5$ 126.3$ 106.7$ 50.4$

Write-off of straight line rent 6.5 1.5 2.8 -

Acquisition costs 5.4 19.4 26.4 6.2

Debt refinancing costs - - 1.7 0.2

Loan and other impairment charges - - 44.1 -

Write-off of other receivables - - - -

Normalized funds from operations 119.4$ 147.2$ 181.7$ 56.8$

For the Twelve Months Ended

NORMALIZED FFOreconciliation

29