Embed Size (px)

Citation preview

Measuring Credit Risk of CBs andDeriving Term Structure of Default

Probabilities一橋大学研究集会【金融工学からERM】へ

Takeaki KariyaGraduate School of Business

Advanced Mathematical SciencesMeiji University

(Jointly with Y.Yamamura, K.Inui, Z.Wang)[email protected]

1Credit Spread

Problem of Measuring Credit Risk

• Credit risk = Probability that a firm breaks a financialcontract

• Basic information on credit risk: Backward looking vsForward lookingForward looking

• Price spread vs Yield spread

• Effectiveness of Agency’s Rating

• Term Structure of Default Probabilities (TSDP)

2Credit Spread

( ){ ( ) ( ) : 0 }k k kM kp s P s s s

( )kp s

s

Basic information on credit riskForward-Looking vs Backward-Looking

Backward-Looking:model using past time series data overa period, generated under different environments

-interest rates:statistical or econometric model

-credit data: past defaults and non-defaults, intensitymodel, classification, transition, logit-probit model

Forward-Looking :model using current (cross-sectional)market data, which includes investors’ future views,projection and perspectives on economic and financialmovements of firms, given past time series information

―current interest rates, bond prices, swap rates

-current CBs (corporate bonds)、CDS, stocks

3NUS RMI Workshop 2012.11

GB Prices and Attributes

• GBs are priced by two types of investors ; holdingmotive and trading motive

• Prices are affected by such attributes as maturity andcoupon preferences ?

• Institutional investors are mostly of holding motivefor income in ALM where duration (coupon andfor income in ALM where duration (coupon andmaturity) and CF pattern are important

• The presence of the attribute effects in prices will denythe no-arbitrage theory in math finance that dependson a logic of trading motive.

4Credit Spread

H0:Hypothesis of No Attribute Effect

• The sum of individually discounted future coupons

and principal is not equal to the bond price!

• A-effects are directly included in prices.

• To test H0, we need a model for bond prices:

Rejection of H0 ⇒ Rejection of the no-arbitrage theory in math finance

To test H we need a model for bond prices:

Traditionally yields are derived from bond prices and H0

is tested in a regression model for yields .

It is difficult to derive yields independent of attributes.

• Nelson-Siegel ModelCredit Spread 5

Price Model vs Interest Rate Model

Yield Approach• Price is a convex function of YTM (Yield to Maturity)

• YTM is a function of price, coupon and maturity, and is aconvex function of price.

• A mean yield curve is derived from individual yields of

( )

1

( )(1 ) g m

M gsYT M

g g g m gm

P C s r

• A mean yield curve is derived from individual yields ofindividual bond prices, and spreads are analyzed by

• MTi is maturity dummy where MTi =1 if the yield belongs to[i,i+1) in years.

6Credit Spread

+ ݅ ݅

9

=݅1

逼迫期には満期7年(7年以上8年未

満)の国債スプレッドが小さくなっている.回復期は6から8年のゾーンが相対的に低く

-0.035

-0.030

-0.025

-0.020

-0.015

-0.010

-0.005

0.000

0.005

0.010

0.015

MT1

MT2

MT3

MT4

MT5

MT6

MT7

MT8

MT9

Uptern Eco.

Downtern Eco.

Financial Crisis

Post Fin. Crisis

Averaged Coefficients ofmaturity effect

Credit Spread 7

(15.00)

(10.00)

(5.00)

0.00

5.00

10.00

15.00

t values of coupon

Hypothesis of No Attribute Effectand GB-Equivalent CB price

H:No Attribute Effect

1) What is GBECB ?

2)Investors’ behaviors in GB market2)Investors’ behaviors in GB market

3)Maturity effect and coupon effect

8Credit Spread

( )

1

( ) ( ) ( 1, , )M g

g g gj g gjj

P C s D s g G

0( ) ex p ( )

s

g g uD s f d u

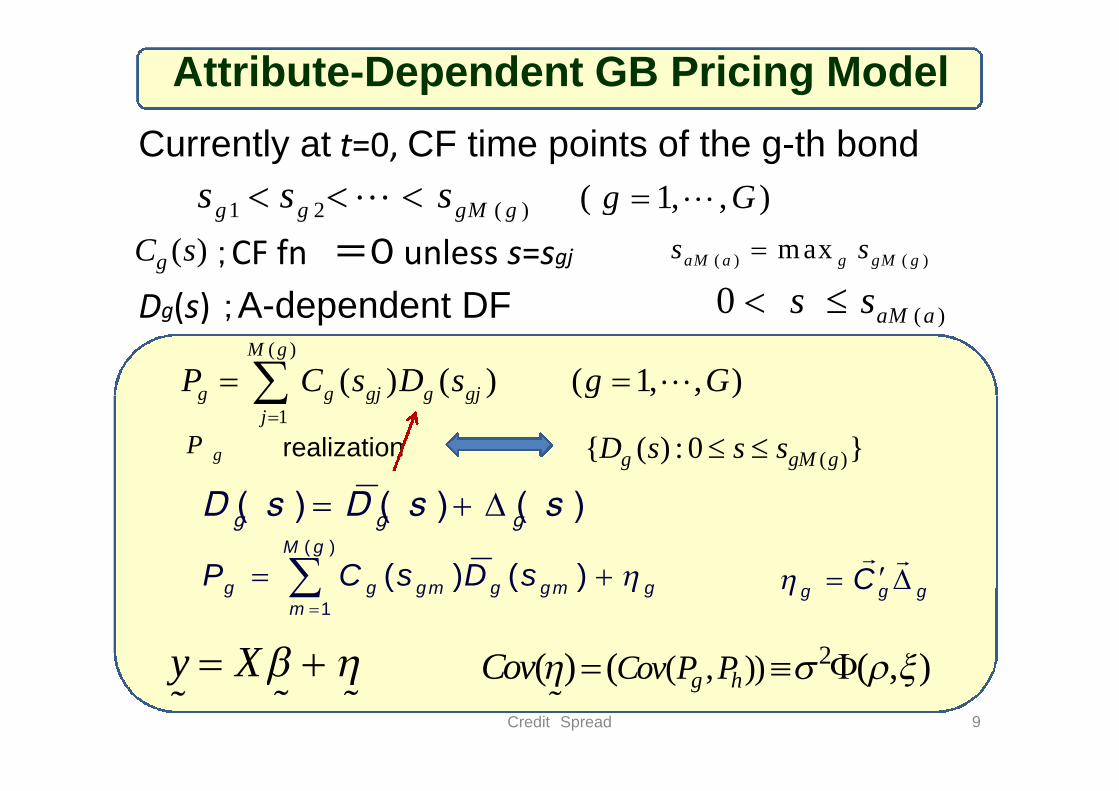

Attribute-Dependent GB Pricing Model

Currently at t=0, CF time points of the g-th bond

;CF fn =0 unless s=sgj

Dg(s) ;A-dependent DF

1 2 ( )g g gM gs s s ( 1, , )g G

( )gC s

( )0 aM as s ( ) ( )maxaM a g gM gs s

( )

( ) ( ) ( 1, , )M g

g g gj g gjP C s D s g G

Credit Spread 9

1

( ) ( ) ( 1, , )g g gj g gjj

P C s D s g G

( ){ ( ) : 0 }g gM gD s s s gP realization

( ) ( ) ( )g g g

D s D s s

( )

1

( ) ( )M g

g g gm g gm gm

P C s D s

g g gC

y X

2( , ))( ) ( ( , )g hCov P PCov

M0 : (1,0,0); basic model with no attributesM1 : (1,1,0): M0 + maturity effect,M2 : (1,0,1); M0 + coupon effectM3 :(1,1,1); M0 +maturity effect+coupon effect

A-dependent Mean Discount FunctionPolynomial Approximation

1 2 3( , , )w w w

( ) 1 ( )D s w z w z w z s

,

zg1=1, zg2 : maturity, zg3 : coupon

Credit Spread 10

11 1 1 12 2 2 13 3 3

1 1 1 2 2 2 3 3 3

( ) 1 ( )

( )

g g g g

pp g p g p g

D s w z w z w z s

w z w z w z s

0( ) [ ( ) ] [ e x p ( ) ]

g js

g g j g g j g sD s E D s E f d s

1log ( )sR D s

s Term structure of interest rates

Covariance Structure

2

2

( )

e x p ( ) ( )g h

g h

s s g h

2( , ) ( , ) ghg h g h ghCov P P Cov

( ) ( )

1 1

( ) ( )M g M m

g g jg h h h mj m

C s C s

Kariya&Kurata(2004)Generalized Least Squares Wiley

Credit Spread 11

2( ) ( )e x p ( ) ( )

g h

g M g h M hs s g h

A-dependent cov structure: Duration effect is naturallyintroduced

y X

1( , ) [ ] '[ ( , )] [ ]y X y X

2 2( ) ( , ) ( )gh ghCov

GLSEatimation

GLSV

I II III IV

Performances of 4 models

月次分析2005.09から2010.08

Polynomial order:p=6

Credit Spread 12

RSD

F ratios of noattribute effects

JGB

F ratio =[{QSR(0) – QSR(1)}/#]/[QSR(1)/df],

[{QSR(0) – QSR(1)}/#] > 2[QSR(1)/df].

0

2

4

6

8

1005/09

05/11

06/01

06/03

06/05

06/07

06/09

06/11

07/01

07/03

07/05

07/07

07/09

07/11

08/01

08/03

08/05

08/07

08/09

08/11

09/01

09/03

09/05

09/07

09/09

09/11

10/01

10/03

10/05

10/07

(a)F ratios of M0 vs M1

6

8

10

(b)F ratios of M0 vs M2

Maturity effect

Credit Spread 13

0

2

4

05/09

05/11

06/01

06/03

06/05

06/07

06/09

06/11

07/01

07/03

07/05

07/07

07/09

07/11

08/01

08/03

08/05

08/07

08/09

08/11

09/01

09/03

09/05

09/07

09/09

09/11

10/01

10/03

10/05

10/07

0

2

4

6

8

10

05/09

05/11

06/01

06/03

06/05

06/07

06/09

06/11

07/01

07/03

07/05

07/07

07/09

07/11

08/01

08/03

08/05

08/07

08/09

08/11

09/01

09/03

09/05

09/07

09/09

09/11

10/01

10/03

10/05

10/07

(c)F ratios of M1 vs M3

Coupon effect

M1 vs M3

F-ratios of no attributeeffects based on

USGB

F ratio =[{QSR(0) – QSR(1)}/#]/[QSR(1)/df],

[{QSR(0) – QSR(1)}/#] > 2[QSR(1)/df].

Hypothesis of no maturity effectPI:Upturn

14

Hypothesis of no coupon effect

M1 vs M3

CB Credit Risk Price SpreadTSDP:Term Structure of DP

2010.8 Cross-Sectional Analysis

1)Definition of CRPS

2)Rating Information will improve on credit2)Rating Information will improve on credit

analysis to make credit homogeneous group?

3) Industry categorization will help?

15Credit Spread

Direct trigger of Defaults is lack of financial liquidityPL-Black firms listed in TSE got defaulted(Real Estate)

CB-Credit Risk Price Spread

• CRPS of individual CB

=CB price-GB-equivalent CB price

= CB price-GBECB with same maturity and coupon( )

( ) ( ) ( ) ( )

1

ˆ ˆ, ( ) ( )M k

i i i ik k k k k k j k k j

j

y V P P C s D s

M0 Spread vs M3 Spread

• Standardized CRPS(uncertainty standardization)

1j

16Credit Spread

( 0,3)i

(3) (3)( )/k k kM ky s

486

676

537

649

400

500

600

700

800

M0

M3

Distribution of CRPS:1 yen split

96

30 22

44

82 85

153

227

373

257

176

0

50

100

150

200

250

300

350

400

-4未満 -4 -3.6 -3.2 -2.8 -2.4 -2 -1.6 -1.2 -0.8 -0.4

0.4 yen split0.4 yen split

Credit Spread 17

213 4 5 14 19 26

72

190

29214 3 6 14 18 30

73

190

00

100

200

300

-10未満 -10 -9 -8 -7 -6 -5 -4 -3 -2 -1 0以上

M3

M0defect

Credit-homogeneous grouping

• Industry, Rating;is it empirically effective?

• Cluster Analysis

• Standardized CRPS defines x-rule.

• Ranking categorization: Logit-Probit analysis

( ) ( ( ,1), ( ,2), , ( , ); (1), (2), , ( ))I k F x k x k x k N z z z L

• Effective ?

is time-dependent. And many factors affect default andnon-default results.

Credit Spread 18

( ) ( ( ,1), ( ,2), , ( , ); (1), (2), , ( ))t t t t t t t tI k F x k x k x k N z z z L

( ) 1,2, ,tI k H

( , ) {( ( ,1), ( ,2), , ( , ); (1), (2), , ( )) : ( ) }t t t t t t t tA k j x k x k x k N z z z L I k j

R&I Rating Groups

Rating does not providehomogeneous information on

( 3 )( )( , )kM k ks y

Credit Spread 19

homogeneous information ondefault risk

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 1

-7

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 2

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 3

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 4

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 5

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 6

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 7

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 8

1 F00ds 2 Cnstrn 3 Mtrls 4 Auto

5 Metals 6 Mchn 7 Utensil 8 ICT

Credit Spread 20

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

Industry 9

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

0 5 10 15

1

2

3

4

Industry 13

-70

-60

-50

-40

-30

-20

-10

0

0 5 10 15

1

2

3

4

Industry 14

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

0 5 10 15

1

2

3

4

Industry 15

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

4

IIndustry 11

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

0 5 10 15

IIndustry 10

-6

-6

-5

-4

-3

-2

-1

0

0 5 10 15

1

2

3

Industry 12

×4

11 Trading9 Epwr/G

14 NonB

12 Retails

13 Bank

10 Trns/D

15 R Rstate

Industry-wiseCRPS-Plot

-3

-2.5

-2

-1.5

-1

-0.5

0

0 2 4 6 8 10

2006.9

-3

-2.5

-2

-1.5

-1

-0.5

0

0 2 4 6 8 10

2007.8

-1.5

-1

-0.5

0

-1.5

-1

-0.5

0

(1) (2)

(3) (4)

Changes of CRPS in E-Power Industry;Business Cycles

Credit Spread 21

-3

-2.5

-2

-1.5

0 2 4 6 8 10

2008.8

-3

-2.5

-2

-1.5

0 2 4 6 8 10

2009.8

-3

-2.5

-2

-1.5

-1

-0.5

0

0 2 4 6 8 10

20010.8

(5)

Electric Power

CRPS-Plots for International Distribution and Metal Industries

Credit Spread 22

International Distributers (Trading,or “Sougoshosha”)

Metal

-4

-3

-2

-1

0

0 2 4 6 8 10Itochu En

Itochu A

Marubeni A-

Mitsui&Co AA-

Mitsubishi AA-

Sumitomo AA-

Sojitsu BBB

N.Pulp A-

Toyoda A+International Distribution

Credit Spread 23

-4

-4

-3

-2

-1

0

0 2 4 6 8 10

DOWA A-JFE AA-Fujikura AFurukawa B3+Mitui M A-Mitsbsh M B3+Smtm MSmtm MinSmtm E AA-Nppn Stl AA-Kobe Stl ADaido Stl A-Nisshin StlHitachi M A

Metal

(1) (2) (3)

3 stage cluster analysis:14groups ( 3 ) ( 3 )( )/k k k M ky s

Credit Spread 24

1 2 3 4 5 6 7 8 9 10 11 12 13 14 合計債権数 988 351 80 38 37 10 7 1 7 10 9 2 4 1 1545最大値 -0.033 -0.303 -0.620 -0.826 -1.051 -1.367 -1.589 -2.165 -2.471 -3.048 -4.619 -12.224 -15.588 -17.578最小値 -0.302 -0.614 -0.810 -1.027 -1.301 -1.480 -1.898 -2.165 -2.820 -3.809 -5.854 -13.854 -16.019 -17.578

NoMaxMin

total

1st 1 2 3(CG11) 4(CG12) 5(CG13) 6(CG14) Total #

# of CBs 1504 25 9 2 4 1 1545

Max -0.33 -15.89 -46.19 -122.24 -155.88 -175.78

Min -14.80 -38.09 -58.54 -138.54 -160.19 -175.78

2nd 1 2 3(CG7) 4(CG8) 5(CG9) 6(CG(10) Total

# of CBs 1339 165 7 1 7 10 1529

Max -0.33 -6.20 -15.89 -21.65 -24.71 -30.48

Min -6.14 -14.80 -18.98 -21.65 -28.20 -38.09

3rd 1(CG1) 2(CG2) 3(CG3) 4(CG4) 5(CG5) 6(CG6) Total

# of CBs 988 351 80 38 37 10 1504

Max -0.33 -3.03 -6.20 -8.26 -10.51 -13.67

Min -3.02 -6.14 -8.10 -10.27 -13.01 -14.80

Credit Spread 25

Min -3.02 -6.14 -8.10 -10.27 -13.01 -14.80

Final Cluster Groups

CG1 CG2 CG3 CG4 CG5 CG6 CG7

# of CBs 988 351 80 38 37 10 7

Max -0.33 -3.03 -6.20 -8.26 -10.51 -13.67 -15.89

Min -3.02 -6.14 -8.10 -10.27 -13.01 -14.80 -18.98

CG8 CG9 CG10 CG11 CG12 CG13 CG14 total

1 7 10 9 2 4 1 1545

-21.65 -24.71 -30.48 -46.19 -122.24 -155.88 -175.78

-21.65 -28.20 -38.09 -58.54 -138.54 -160.19 -175.78

Credit-homogeneous Groups via 3 Stage Cluster Analysis

( 3 )( )( , )kM k ks y

アイフル

All cluster groups・CRPS-Plot

Credit Spread 26

,

CRPS-Plot for CGs

FIR 1 FIR 2 FIR 3 FIR 4 FIR 5

FG 0.5Yen # FG 1Yen # FG M1Yen # FG 1.5Yen # FG 2Yen #

1 [-0.5,0) 10 1 [-1,0) 42 1 [-1,0) 42 1 [-1.5,0) 213 1 [-2,0) 618

2 [-1.0,-0.5) 32 2 [-2,-1) 576 2 [-2,-1) 576 2 [-3.0,-1.5) 773 2 [-4,-2) 526

3 [-1.5,-1.0) 171 3 [-3,-2) 368 3 [-3,-2) 368 3 [-4.5,-3.0) 214 3 [-6,-4) 186

4 [-2.0,-1.5) 405 4 [-4,-3) 158 4 [-4,-3) 158 4 [-6.0,-4.5) 130 4 [-8,-6) 86

5 [-2.5,-2.0) 223 5 [-5,-4) 111 5 [-5,-4) 111 5 [-7.5,-6.0) 64 5 [-10,-8) 35

6 [-3.0,-2.5) 145 6 [-6,-5) 75 6 [-6,-5) 75 6 [-9.0,-7.5) 41 6 (-∞,-10) 94

7 [-3.5,-3.0) 81 7 [-7,-6) 46 7 [-8,-6) 86 7 [-10.5,-9.0) 22

8 [-4.0,-3.5) 77 8 [-8,-7) 40 8 [-11,-8) 48 8 (-∞,-10.5) 88

FIR(Fixed Interval Rating) based on S-CRPS measure ζ:2010.8

Credit Spread 27

8 [-4.0,-3.5) 77 8 [-8,-7) 40 8 [-11,-8) 48 8 (-∞,-10.5) 88

9 [-4.5,-4.0) 56 9 [-9,-8) 19 9 [-15,-11) 40

10 [-5.0,-4.5) 55 10 [-10,-9) 16 10 (-∞,-15) 41

11 [-5.5,-5.0) 36 11 (-∞,-10) 94

12 [-6.0,-5.5) 39

13 [-7.0,-6.0) 46

14 [-8.0,-7.0) 40

15 [-9.0,-8.0) 19

16 [-10.0,-9.0) 16

17 (-∞,-10) 94

OurFIRGr

(3) (3)( )/k k kM ky s

Market Grouping via FIR 3 (Total 1545 CBs)

R&IF1

(0,-1]

F2

(-1,-2]

F3

(-2,-3]

F4

(-3,-4]

F5

(-4,-5]

F6

(-5,-6]

F7

(-6,-8]

F8

(-8,-11]

F9

(-11,-15]

F10

(-15,∞)Total # CBs

AAA 0.0 22.2 77.8 0.0 0.0 0.0 0.0 0.0 0.0 0.0 100 9

AA+ 6.6 84.9 8.5 0.0 0.0 0.0 0.0 0.0 0.0 0.0 100 497

AA 0.8 52.1 45.4 1.7 0.0 0.0 0.0 0.0 0.0 0.0 100 119

AA- 3.5 27.9 66.3 1.7 0.0 0.0 0.6 0.0 0.0 0.0 100 172

A+ 0.6 12.8 52.0 14.0 7.8 6.1 3.4 3.4 0.0 0.0 100 179

FIR vs R&I Rating Cross Table: Distribution

Credit Spread 28

A 0.0 0.7 13.8 46.7 9.9 3.9 7.9 8.6 8.6 0.0 100 152

A- 0.0 0.6 8.6 25.3 27.2 11.1 9.9 6.2 2.5 8.6 100 162

BBB+ 0.0 0.0 1.1 5.3 20.0 14.7 27.4 9.5 9.5 12.6 100 95

BBB 0.0 0.0 0.0 0.0 9.6 28.8 34.6 9.6 11.5 5.8 100 52

BBB- 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 100 100 1

CCC+ 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 100 100 7

None 1.0 17.0 22.0 11.0 14.0 11.0 7.0 5.0 8.0 4.0 100 100

# of CBs 42 576 368 158 111 75 86 48 40 41 100 1545

-6

-4

-2

0

0 2 4 6 8 10 12

G1

G2

G3

G4

G5

F1

F2

F3

F4

F5

F6

Credit-homogeneous Groups via FIR grouping:2010.8

Credit Spread 29

-14

-12

-10

-8

G5

G6

G7

G8

G9

F7

F8

F9

( )

1

( ) ( )

M k

k k k j k k jj

V C s D s

CB Pricing Model

( ) ( ) ( )kk kD s D s s

CB Pricing Model Expected CFs

1

( ) ( )[1 ( )]

100 [ ( ) ( )]

k mj k mj k mj

k k mj k mj

C s C s p s

p s p s

StochasticDiscount Fn

Credit Spread 30

1

( : ( )) ( ) ( : ( ), )J

k k

j

p s i k w j p s i k j

1)(,0)(1

J

jkk jwjw

21 2( ; , ) ij ij ij q

qp s i j s s s

Kariya(2012)

TSDPs of Cluster Groups:Recovery Rate =0

Code Industry# of CBsin Gr 1

# of CBsin Gr 2

1 Food 24 18

3 Construction 16 9

4 Material /chemistry 41 46

6 Auto 30 23

7 Metal 49 30

8 Machinery 19 13

9 Electric Utensil 44 27 0.8

0.9

CG8

CG9

Credit Spread 31

9 Electric Utensil 44 27

10 ICT 53 7

11 Electric Power/Gas 459 2

12 Transportation/Log 124 81

13 Trading 56 42

14 Retail 6 1

15 Banks 1 18

16 Financial 14 22

17 Real Estate 52 12-0.1

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0 1 2 3 4 5 6 7 8 9 10

CG9

CG10

CG11

CG12

CG13

CG14

0.04

0.06

0.08

0.1

0.12

0.14

CG1

CG2

CG3

CG4

CG5

CG6

CG7

TSDPs for Cluster groups: γ=0

TSDPs for Cluster Groups:2010.8, γ=0

Credit Spread 32

-0.02

0

0.02

0.04

0 1 2 3 4 5 6 7 8 9 10

CG1 CG2 CG3 CG4 CG5 CG69yrs 2.0 3.5 5.9 10.1 10.2 13.110yrs 2.1 4.1 6.7 10.2

Default Probabilities for CGs

CG1×Indusry:TSDPs

0.02

0.025

0.03

0.035

0.04

食品

建設・資材

素材・化学

自動車・輸送機

鋼鉄・非鉄

機械

0.02

0.025

0.03

0.035

0.04

電気・精密

情報通信、サービス

運輸・物流

商社

金融(除く銀行)

不動産

Credit Spread 33

0

0.005

0.01

0.015

0 2 4 6 8 100

0.005

0.01

0.015

0 2 4 6 8 10

TSDPs in the Electric Power Industry:2010.8

Credit Spread 34

TSDPs

Changes of TSDPs ofTEPCO

Credit Spread 35

2009.2TSDPs

of TEPCO

2007.8 2008..8 2009.8

0.02

0.025

0.03

0.035

0.04Mitsubishi Corp.

Mitsui & Co.

Sumitomo Corp.

Itochu Corp.

Marubeni Corp.

Sojitz Corp.

MBS SuS MiT ITo MBN SJT

2yrs 0.30 0.34 0.37 0.63 0.75 1.32

3yrs 0.62 0.66 0.70 1.00 1.38 2.39

4yrs 0.87 0.92 1.01 1.37 1.95

5yrs 1.05 1.12 1.26 1.75 2.51

6yrs 1.23 1.31 1.45 2.19

TSDPs of individual firms in the Trading Industry:2010.8

Credit Spread 36

0

0.005

0.01

0.015

0 1 2 3 4 5 6 7 8 9 10

6yrs 1.23 1.31 1.45 2.19

7yrs 1.47 1.59 1.66 2.69

8yrs 1.84 2.00 2.07 3.23

9yrs 2.30 2.55 3.00 3.68

10yrs

2.73 3.14 3.78

Changes of TSDPs ofMitsubishi Corp

Credit Spread 37

TSDP of Spain relative to Germany

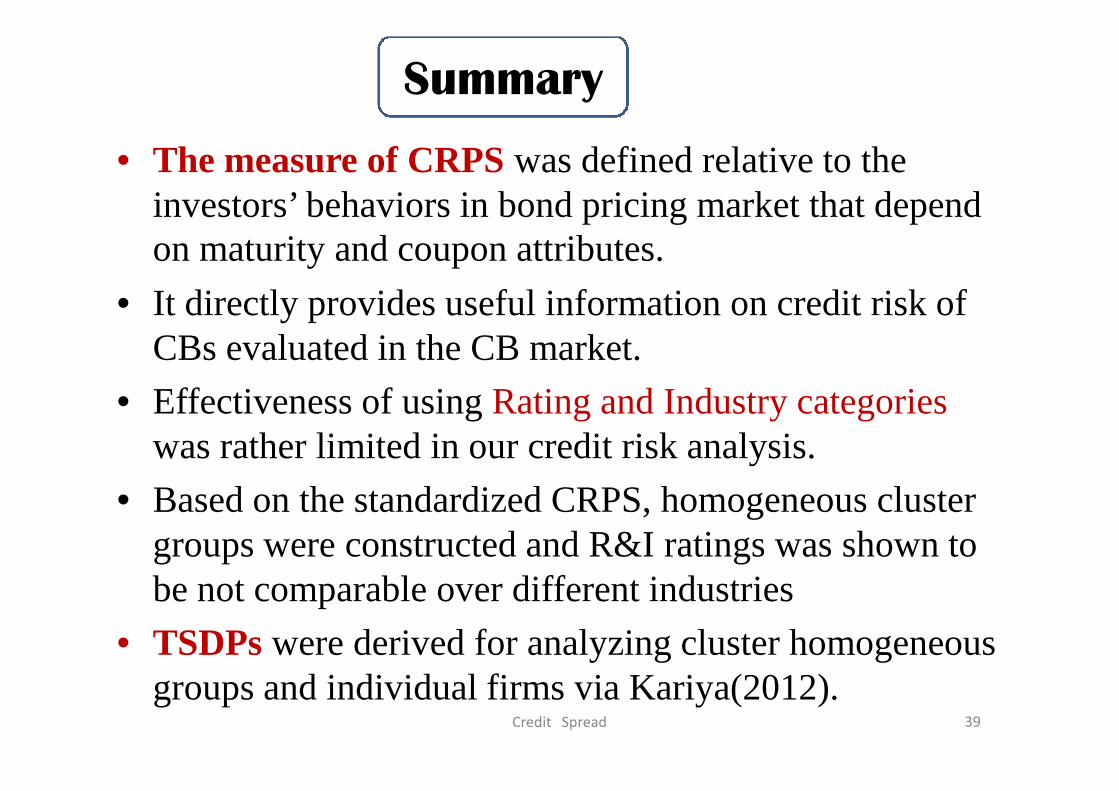

• The measure of CRPS was defined relative to theinvestors’ behaviors in bond pricing market that dependon maturity and coupon attributes.

• It directly provides useful information on credit risk ofCBs evaluated in the CB market.

• Effectiveness of using Rating and Industry categories

Summary

• Effectiveness of using Rating and Industry categorieswas rather limited in our credit risk analysis.

• Based on the standardized CRPS, homogeneous clustergroups were constructed and R&I ratings was shown tobe not comparable over different industries

• TSDPs were derived for analyzing cluster homogeneousgroups and individual firms via Kariya(2012).

Credit Spread 39

ReferencesKariya,T.(2012) A CB (corporate bond) pricing model for deriving

default probabilities and recovery rates. To appear

Kariya, T. and Kurata, H. (2004) Generalized Least Squares, JohnWiley, New York.

Kariya,T., Wang,J., Wang,Z., Doi,E., and Yamamura,Y.(2012)Empirically Effective Bond Pricing Model and Analysis on TermStructures of Implied Interest Rates in Financial Crisis Asia-PacificFinancial Markets 19:259–292Financial Markets 19:259–292

Kariya,T., Yamamura,Y., Inui,K., and wang, Z. (2012) Measuring creditrisk price spreads of CBs and deriving term structures of defaultprobabilities

Duan, J.C., J. Sun and T. Wang(2011) Multiperiod Corporate DefaultPrediction-A forward Intensity Approach, RMI working paperNo.10/07, National University of Singapore

Duffie, D. (2011). Measuring Corporate Default Risk. ClarendonLectures in Finance, Oxford University PressCredit Spread 40