Embed Size (px)

Citation preview

Electricity Forward Curves with Thin Granularity

Mercati Energetici e Metodi Quantitativi: un ponte tra universitá e

aziende

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni

Accenture SPA, Milan - Italy

Padova, October 13, 2016

Curve

HPFC de�nition

The hourly price forward curve (HPFC) quoted in a given market at a day

t is a mathematical function ft (T , h) associating to each day T in the

future a price for the commitment to deliver one megawatt-hour for a

speci�c hour h of that speci�c day, i.e. the term structure of electricity

forward prices as quoted with hourly granularity across the maturity

dimension.

Academic and industrial relevance:

1 Marking energy portfolios to market quotes (Teixeira Lopes (2007)),2 Calibrating arbitrage models (Islyaev-Date (2015)),3 Analyzing risk premia (Frestad-Benth-Koekebakker (2010)),4 Conceiving and testing prop trading rules (Furio-Lucia (2009)),5 Consumption optimization in energy-intensive processes (Lima (2015)),6 Real option based physical asset valuation (Nasakkalaa-Fleten (2005)).

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Literature

Fleten-Lemming (2003) benchmark parametric curve �tting to a

proprietary equilibrium model.

Koekkebakker-OsAdland (2004) and Benth-Koekebakker-Ollmar (2007)

combine seasonalities with splines and minimize curve convexity.

Borak and Weron (2008) propose a parsimonious, smooth, and seasonal

forward curve.

Hildmann-Ka�e-Anderson (2012) model hourly prices.

Paraschiv-Fleten-Schurle (2015) extend Benth et al. (2007) method to

account for hourly granularity and weather-linked factors.

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Issue

We put forward a Rational Constructive De�nition of electricity forward

curve with thin granularity.

Constructive = Algorithmic.

Rational = Complying with 5 desirable properties:

1 Raw price series undergo a �ltering procedure to �nely detect and single

out data outliers;2 Curve shape embeds a comprehensive bundle of periodical patterns

unveiled by past quotes;3 Curve level is jointly consistent to standing baseload and peakload futures

quotations;4 Curve path satis�es regularity properties: smoothness, monotonicity

preservation, cross-sectional stability, time localness (Hagan-West (2006));5 Forward estimate quality is assessed through dedicated empirical tests.

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Example of futures market data

Figure: Futures market data from EEX, November 7, 2013. Settlement prices

are given in Eur/MWh.

Jan14 Apr14 Jul14 Oct14 Feb15 May15 Aug15 Dec1525

30

35

40

45

50

55

60

BaseloadPeakload

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Idea

1 Reduction to forward kernel:

obsF =

1

τ e − τ b

∫ τe

τbft(u)du → ft(·) → all prices.

2 Construction of forward kernel:

APT : Arbitrage-free spot model dS (t) → ft(u) := E∗t [S(u)];

Our method is dynamic model independent:

ft(u) := Λt(u) + εt(u) + ϕt (u) ,

Λ → Periodical patterns (Historical information),

εt → Calibration to baseload forwards (Risk-neutral information),

ϕt → Calibration of peakload forwards (Risk-neutral information).

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Construction

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Data

Market: EPEX Spot SE and EEX Power Derivatives;

Data:

〈Spot → 24×2,525 obs. [Jan. 1, 2009 - Nov. 27, 2015];

Forward → baseload and peakload, on Nov. 27, 2015.

Filtering:

Aug09 Dec10 May12 Sep13 Feb15-60

-40

-20

0

20

40

60

80

100Filtered pricesFilter for preprocessingIdentified Outliers

Aug09 Dec10 May12 Sep13 Feb150

10

20

30

40

50

60

70

80

90Daily priceFiltered daily trend

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Analysis of predictable components

A seasonality function for the German market

Λ(u) = a cos

(2π

365u + b

)︸ ︷︷ ︸

Long term (LT)

+7∑

j=1

cj1(u ∈ dayj )

︸ ︷︷ ︸Weekly (W)

+24∑h=1

4∑l=1

dh,l1(u ∈ hourh ∩ u ∈ Cl )︸ ︷︷ ︸Daily (D)

,

where:

u ∈ R, and a, cj , dh,l ∈ R ∀h, j, k, l and b ∈ [0, 2π].

dayj for j = 1, . . . , 7 := the set of points in the jth day of the week (i.e. j = 1 refer to

Sunday . . . , j = 7 refer to Saturday).

hourh, h = 1, . . . , 24, := the set of points in the hth hour of a day.

C1 := working days in the cold season (from October to March).

C2 := non-working days in the cold season (from October to March).

C3 := working days in the warm season (from April to September).

C4 := non-working days in the warm season (from April to September).∑24h=1 dh,l = 0, l = 1, . . . , 4.

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Long term and weekly predictable components

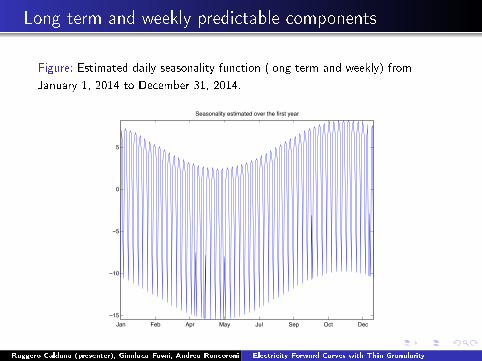

Figure: Estimated daily seasonality function (long term and weekly) from

January 1, 2014 to December 31, 2014.

Jan Feb Apr May Jul Sep Oct Dec−15

−10

−5

0

5

Seasonality estimated over the first year

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Daily shape

Figure: Hourly seasonality pro�le: variables dh,l are plotted for h = 1, . . . , 24.

Working days - cold season Non-working days - cold season

2 4 6 8 10 12 14 16 18 20 22 24−20

−15

−10

−5

0

5

10

15

20

Hourly profile cluster C1

2 4 6 8 10 12 14 16 18 20 22 24−20

−15

−10

−5

0

5

10

15

20

Hourly profile cluster C2

Working days - warm season Non-working days - warm season

2 4 6 8 10 12 14 16 18 20 22 24−20

−15

−10

−5

0

5

10

15

20

Hourly profile cluster C3

2 4 6 8 10 12 14 16 18 20 22 24−20

−15

−10

−5

0

5

10

15

20

Hourly profile cluster C4

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Market consistency adjusment

Baseload consistency adjusment

We de�ne ε through the monotone convex spline put forward in (Hagan

West, 2006) that guarantees

1 Consistency to baseload futures.

2 Positivity of ε.

3 Continuity of ε.

4 Monotonicity of ε.

Peakload consistency adjustment

Peakload consistency adjustment ϕ is obtained through a constant

pathwise shift on peak and o�-peak hours for workdays only. The

adjustment is constrained to not a�ect baseload consistency.

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Curve

Dec15 Jan16 Mar16 Apr16 Jun16 Aug16 Sep16 Nov160

10

20

30

40

50

60Hourly PriceBaseloadPeakload

Dec15 Jan16

5

10

15

20

25

30

35

40

45

50

55 Hourly PriceBaseloadPeakload

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

8. Curve Decomposition

Dec15 Jan16 Mar16 Apr16 Jun16 Aug16 Sep16 Nov16-20

-10

0

10

20

30

40LambdaEpsilonPhi

Dec15 Jan16

-15

-10

-5

0

5

10

15

20

25

30

35 LambdaEpsilonPhi

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Localness

Cross-sectional localness = Any change occurring on whatever segmented

baseload quote (e.g., spot price down by 20 EUR/MWh from Feb. 28,

2013 quote of 53.96) exclusively a�ects curve estimate on the

corresponding delivery interval as well as on the two adjacent ones.

Maximum smoothness (Bent et al. (2007)) Our model

Mar13 Jun13 Sep13 Jan14 Apr14 Jul14 Oct1410

15

20

25

30

35

40

45

50

55

6028 February 201328 February 2013 Stressed

Mar13 Jun13 Sep13 Jan14 Apr14 Jul14 Oct1415

20

25

30

35

40

45

50

5528 February 201328 February 2013 Stressed

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Stability

Time stability = Small perturbations in input data (e.g.,

26-27-28/2/2013) entail a slight curve variation.

Maximum smoothness Interpolation Our model

Mar13 Jun13 Sep13 Jan14 Apr14 Jul14 Oct140

10

20

30

40

50

60

7026 February 201327 February 201328 February 2013

Mar13 Jun13 Sep13 Jan14 Apr14 Jul14 Oct1425

30

35

40

45

50

55

60

6526 February 201327 February 201328 February 2013

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Fit Quality I

Futures prices risk premia

Futures prices incorporate risk premia and thus the realized spot price

cannot be used as benchmark to assess the HPFC �t quality.

We need to build �ctitious futures quotes that can be compared to

realized day-ahead price.

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Fit Quality II

Figure: Backtesting the �t quality for t0 = September 1, 2012. First, we

calibrate the seasonality function on realized prices preceding t0, and we use

prices following t0 to compute �ctitious futures quotations.

10/24/11 02/01/12 05/11/12 08/19/12 11/27/12 03/07/13 06/15/13

−200

−150

−100

−50

0

50

100

150

200

Realized hourly price

Seasonality estimation before t0 Fictitious futures construction after t0

t0 = 1−Sep−2012

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Fit Quality III

Testing the quality of forward estimates w.r.t. Benth et al. (2007)'s MSI.

Data: 16 evaluation dates = �rst day in Jan., Apr., Jul. 2010 → 2013.

Prices preceding an evaluation → periodical patterns estimate.

Prices following each evaluationavg→ �ctitious baseloads/peakloads.

Performance index: MAD = 1

24]S∑

T∈S∑

h=1,...,24

∣∣∣f (T , h)− S(T , h)∣∣∣

Output: 2 models×16 dates×3 patterns = 96 MAD �gures.

Main result: our model outperforms benchmark MSI on 34 out of 48

scenarios, which correspond to 70.83% of the sample.

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Conclusion

Constructive de�nition of forward curve with hourly granularity up.

Curve is jointly consistent to risk-neutral & historical market information.

Curve paths are smooth, monotonic, cross-sectionally stable, time local.

Backtesting analysis w.r.t. benchmark model of Benth et al. (2007).

What's next?

Analyzing the interplay between HPFC cross-sectional granularity and the

underlying market price of risk.

Adjustments to cope with the great variety of commodity price dynamics

featuring periodical patterns (e.g., natural gas, agriculturals)

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity

Thanks for your attention!

Ruggero Caldana (presenter), Gianluca Fusai, Andrea Roncoroni Electricity Forward Curves with Thin Granularity