Embed Size (px)

Citation preview

RevenueCASBO Training

Revenue vs. Expenditure

Which do you prefer?Which do you need to manage the

closest?Should you be conservative or liberal in

how you budget?Budget revenue low, expenditures high.

FUNDS

A fund is “a sum of money or other resources whose principal or interest is set apart for a specific objective.”

The districts in the State of Arkansas use what is called the “fund method” of accounting.These funds have revenue and

expenditures.

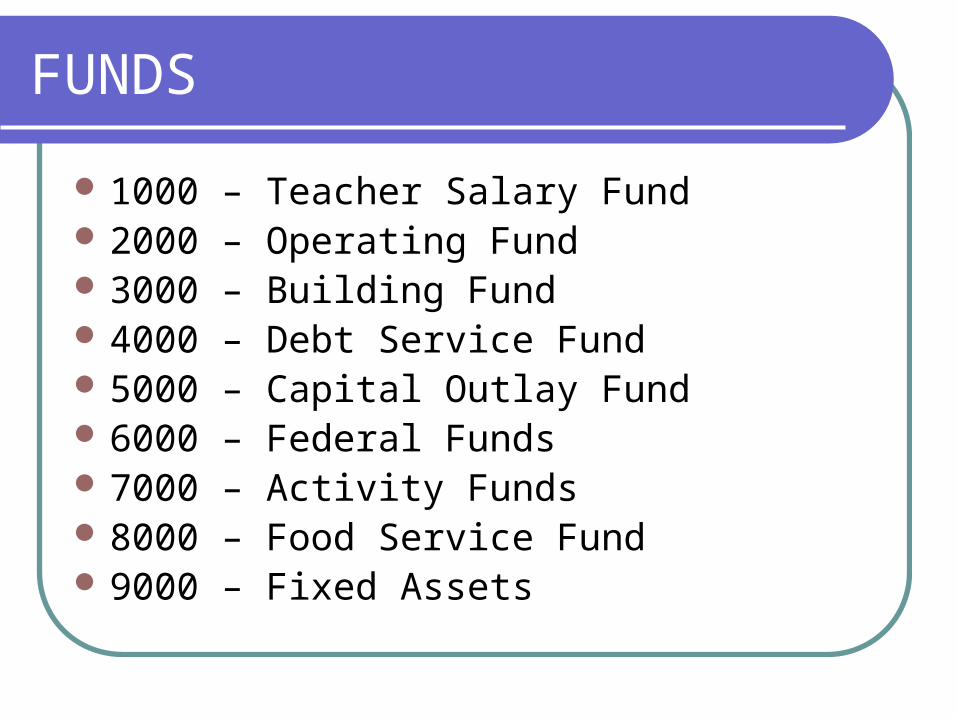

FUNDS

1000 – Teacher Salary Fund 2000 – Operating Fund 3000 – Building Fund 4000 – Debt Service Fund 5000 – Capital Outlay Fund 6000 – Federal Funds 7000 – Activity Funds 8000 – Food Service Fund 9000 – Fixed Assets

Revenue

In business, revenue is the amount of money that a company actually receives from its activities, mostly from sales of products and/or services to customers

Schools do not generally create incomeMost of our revenue comes from taxes.

REVENUE

Four major categories of revenue:StateLocal Property TaxesFederal GrantsOther

There are specific codes we must use for accounting for revenue that we receive. They are found in the Handbook 2R2.

Types of Revenue

Taxes, income, fiduciary money, bond money Taxes – tax collection and state aid Income – sale of goods or services

Activity accounts Cafeteria

Fiduciary funds – money held in trust for a specific purpose

Grants Bond money – the proceeds from the sale of bonds

for the financing of a construction project, etc.

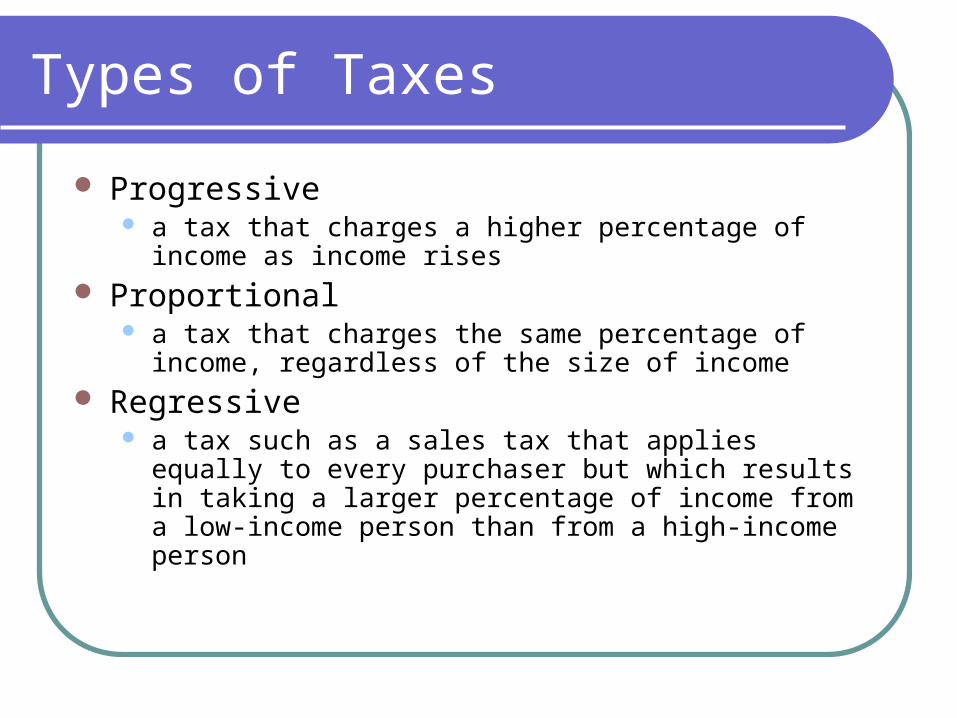

Types of Taxes

Progressive a tax that charges a higher percentage of income as income

rises Proportional

a tax that charges the same percentage of income, regardless of the size of income

Regressive a tax such as a sales tax that applies equally to every

purchaser but which results in taking a larger percentage of income from a low-income person than from a high-income person

Property Tax

HistoryProperty taxes have been around for

centuriesEstablished as a way to tax the wealthy

property ownersTaxes based on ownership of property were

used in ancient times. The modern tax has roots in feudal obligations owed to British and European kings or landlords.

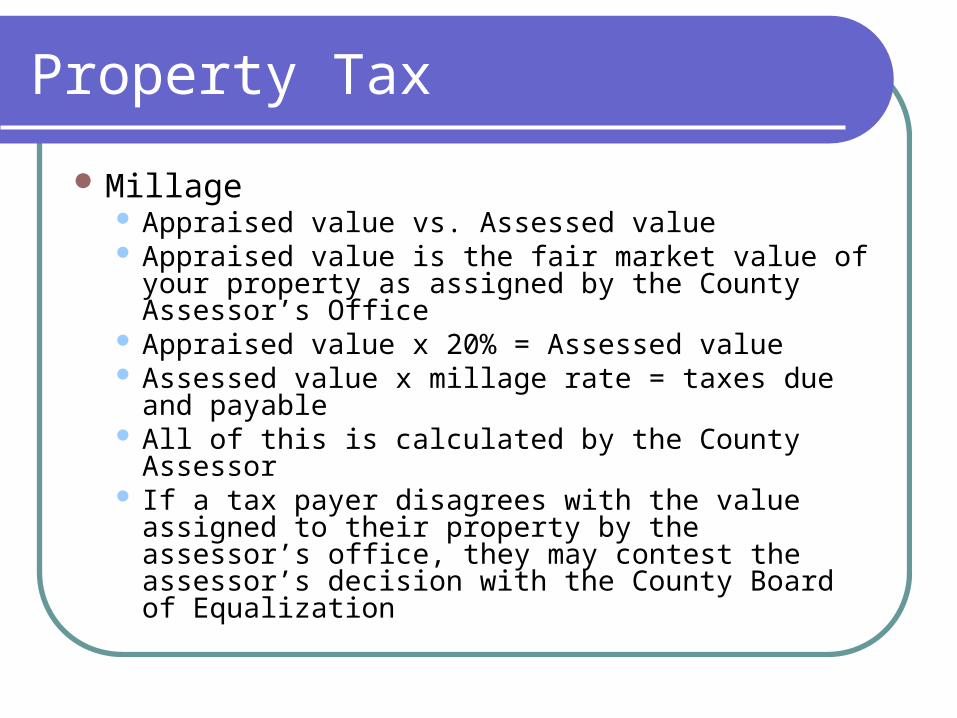

Property Tax

Millage Appraised value vs. Assessed value Appraised value is the fair market value of your

property as assigned by the County Assessor’s Office

Appraised value x 20% = Assessed value Assessed value x millage rate = taxes due and

payable All of this is calculated by the County Assessor If a tax payer disagrees with the value assigned to

their property by the assessor’s office, they may contest the assessor’s decision with the County Board of Equalization

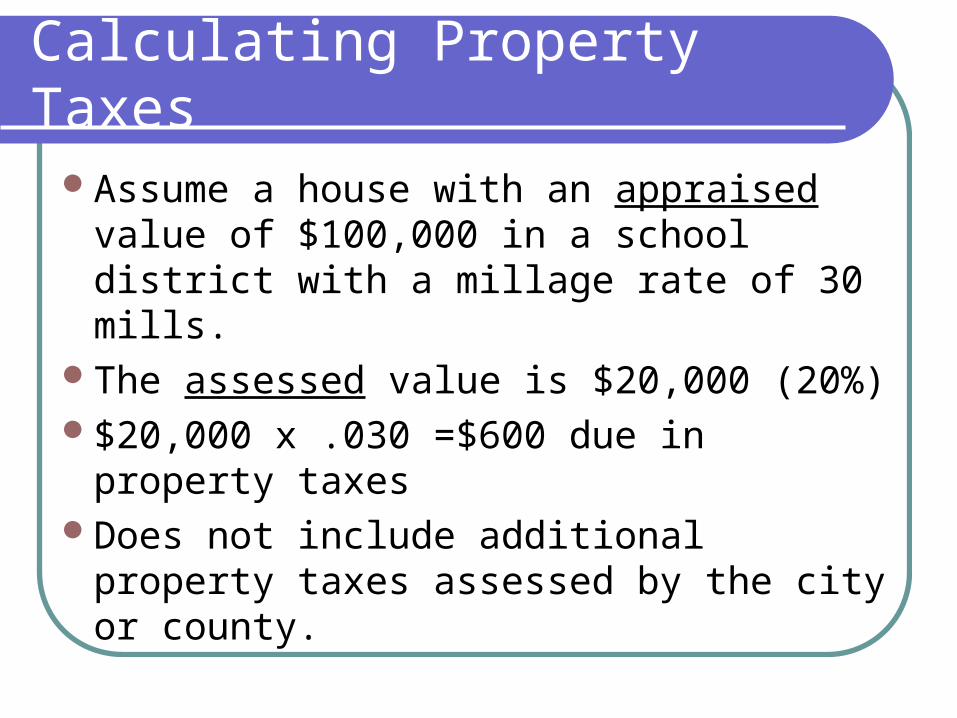

Calculating Property Taxes

Assume a house with an appraised value of $100,000 in a school district with a millage rate of 30 mills.

The assessed value is $20,000 (20%)$20,000 x .030 =$600 due in property

taxesDoes not include additional property

taxes assessed by the city or county.

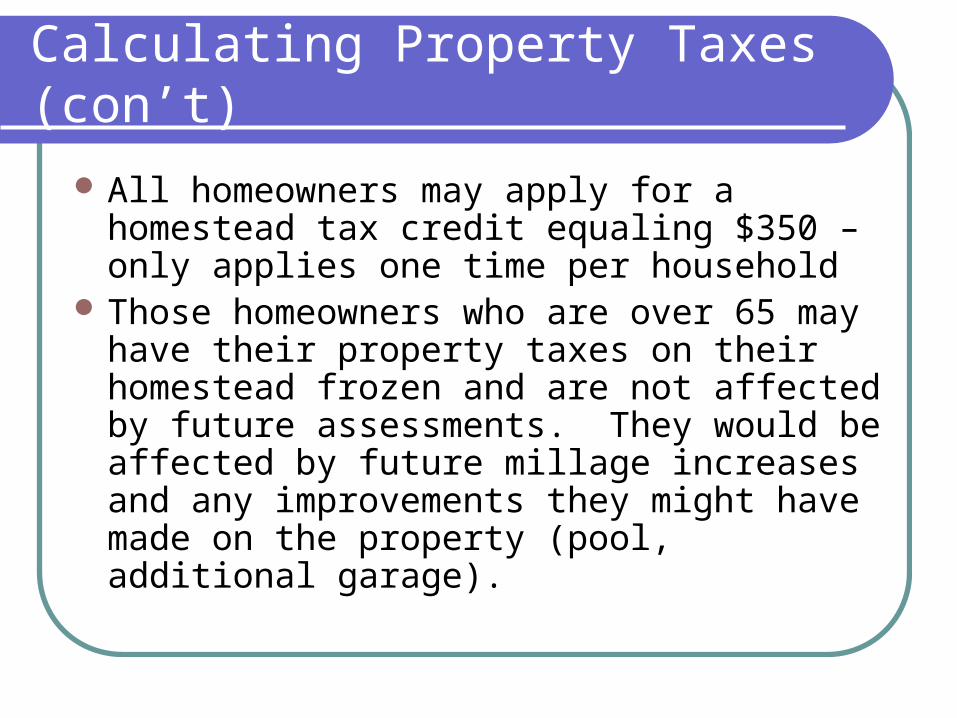

Calculating Property Taxes (con’t)

All homeowners may apply for a homestead tax credit equaling $350 – only applies one time per household

Those homeowners who are over 65 may have their property taxes on their homestead frozen and are not affected by future assessments. They would be affected by future millage increases and any improvements they might have made on the property (pool, additional garage).

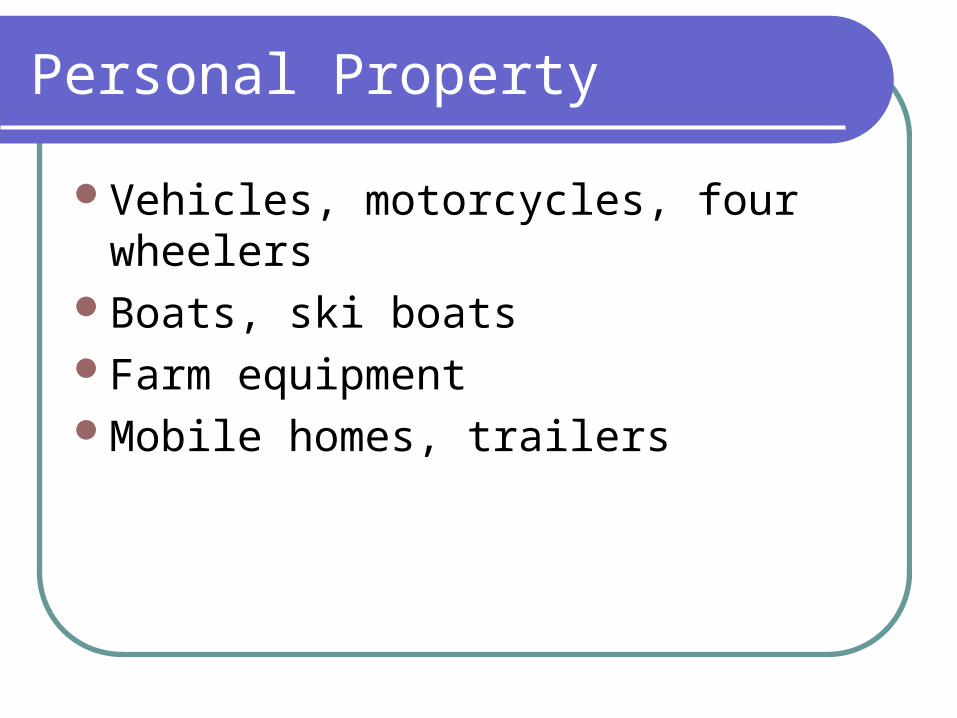

Personal Property

Vehicles, motorcycles, four wheelersBoats, ski boatsFarm equipmentMobile homes, trailers

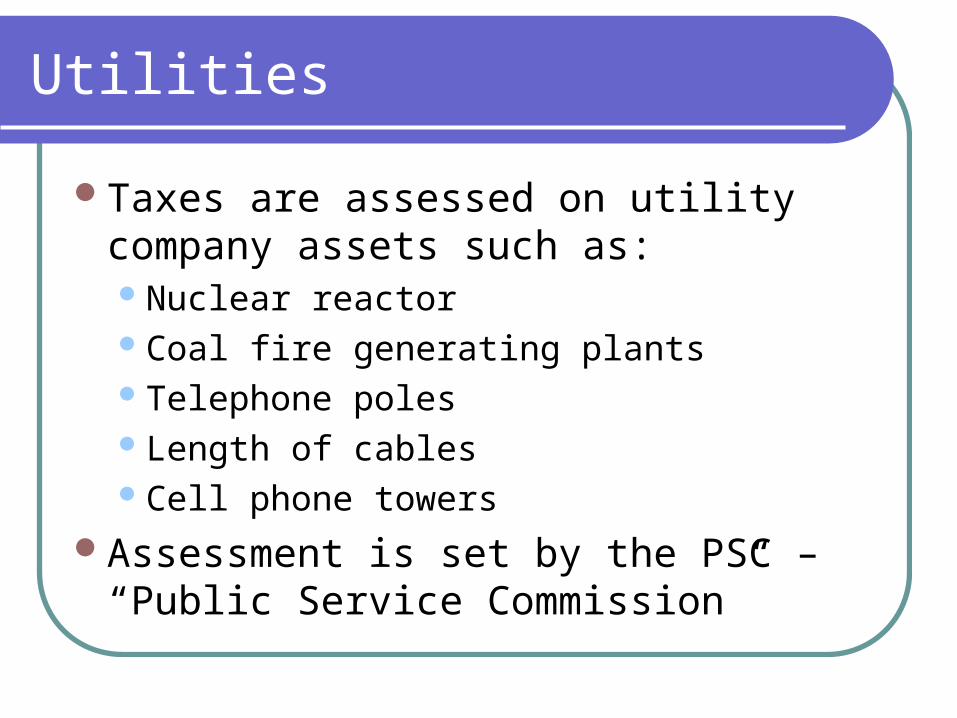

Utilities

Taxes are assessed on utility company assets such as:Nuclear reactorCoal fire generating plantsTelephone polesLength of cablesCell phone towers

Assessment is set by the PSC – “Public Service Commission”

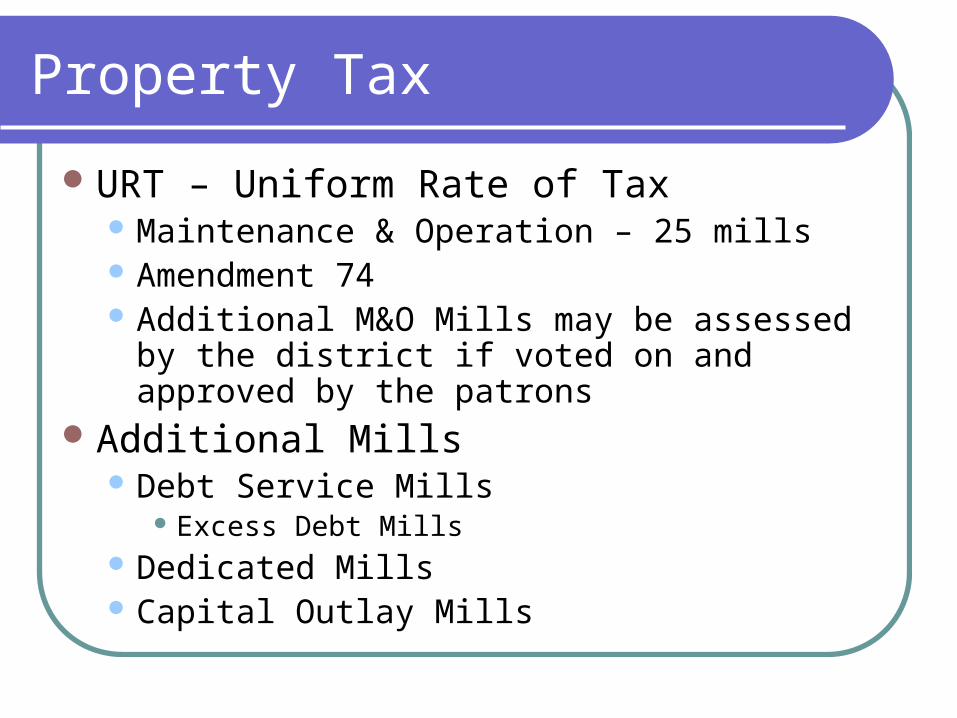

Property Tax

URT – Uniform Rate of Tax Maintenance & Operation – 25 mills Amendment 74 Additional M&O Mills may be assessed by the

district if voted on and approved by the patronsAdditional Mills

Debt Service Mills Excess Debt Mills

Dedicated Mills Capital Outlay Mills

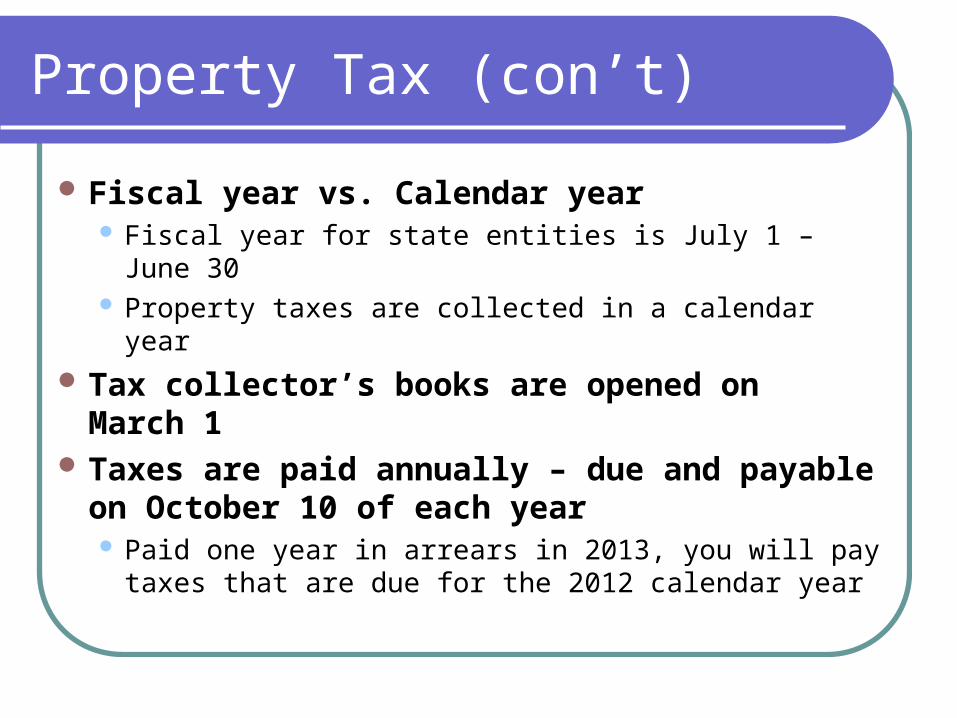

Property Tax (con’t)

Fiscal year vs. Calendar year Fiscal year for state entities is July 1 – June 30 Property taxes are collected in a calendar year

Tax collector’s books are opened on March 1

Taxes are paid annually – due and payable on October 10 of each year Paid one year in arrears in 2013, you will pay taxes

that are due for the 2012 calendar year

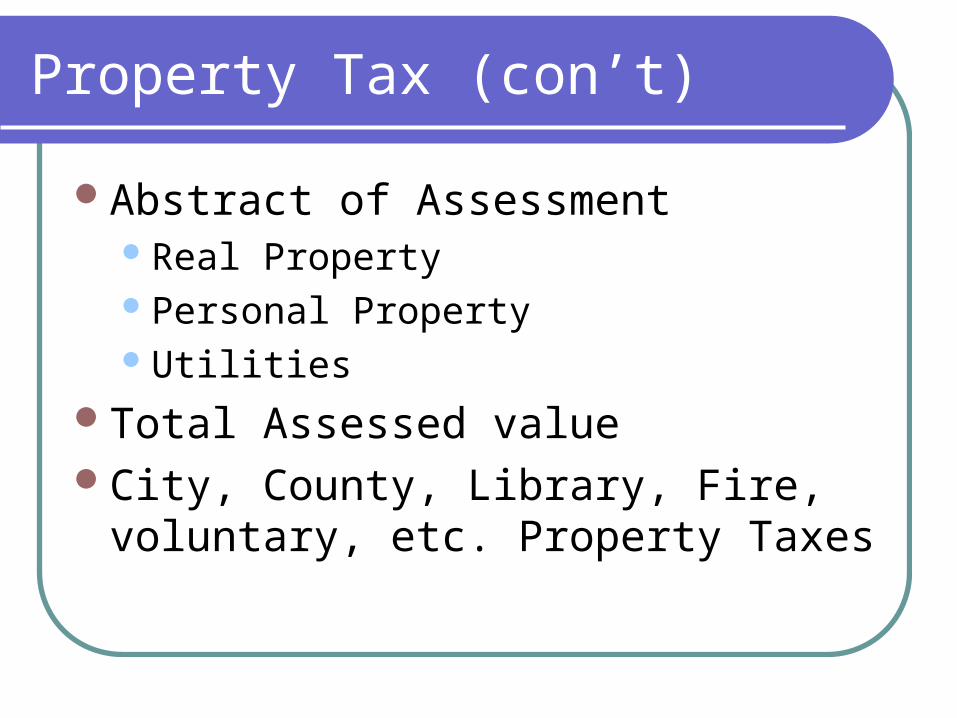

Property Tax (con’t)

Abstract of AssessmentReal PropertyPersonal PropertyUtilities

Total Assessed valueCity, County, Library, Fire, voluntary, etc.

Property Taxes

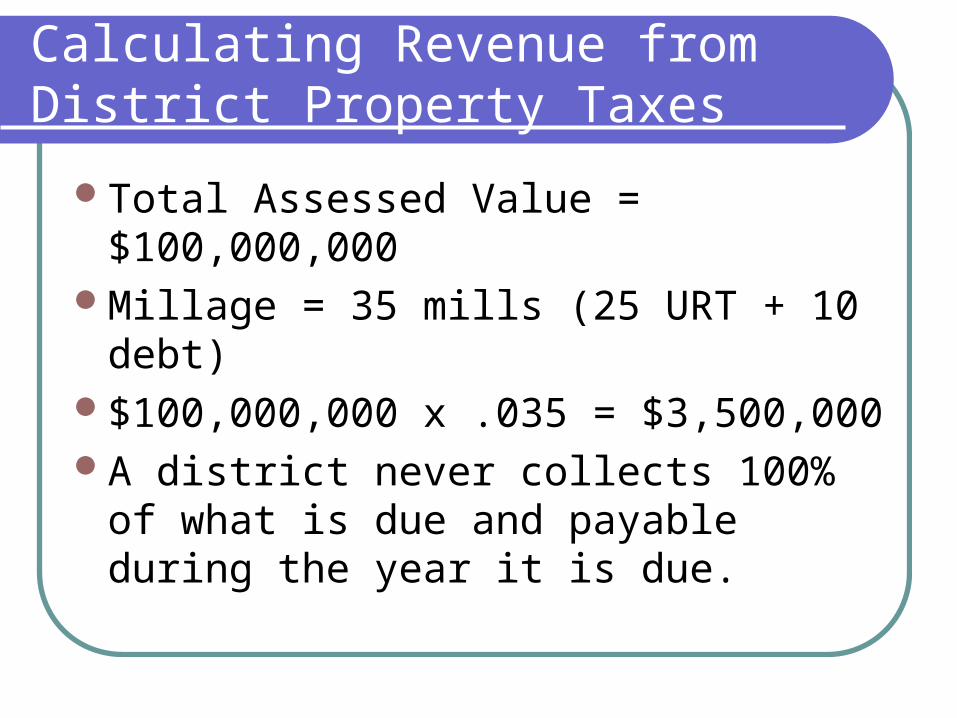

Calculating Revenue from District Property Taxes

Total Assessed Value = $100,000,000Millage = 35 mills (25 URT + 10 debt)$100,000,000 x .035 = $3,500,000A district never collects 100% of what is

due and payable during the year it is due.

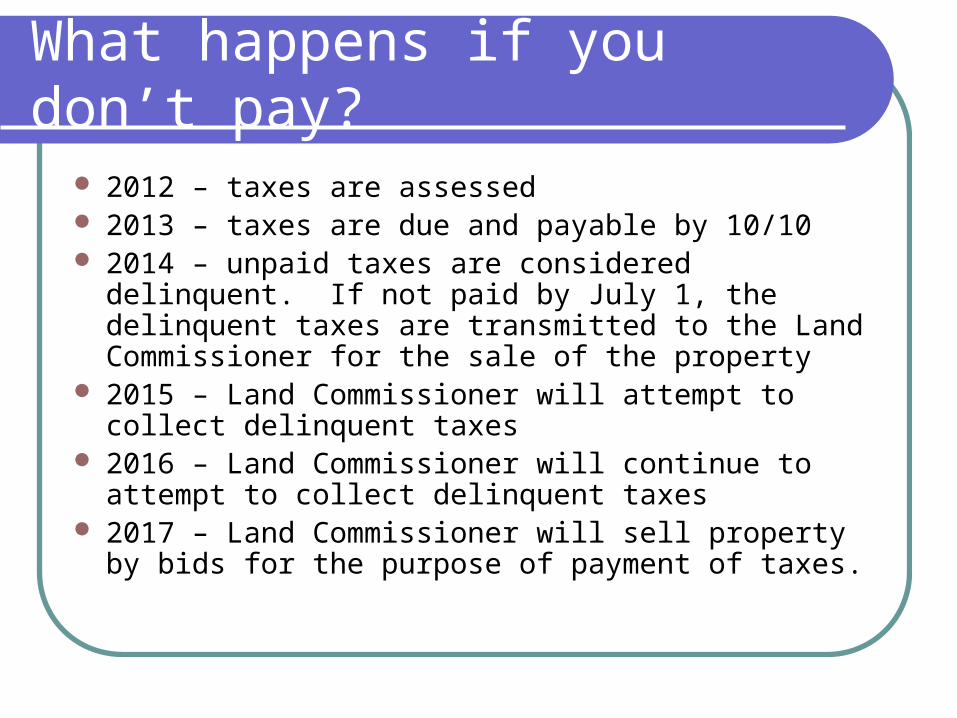

What happens if you don’t pay?

2012 – taxes are assessed 2013 – taxes are due and payable by 10/10 2014 – unpaid taxes are considered delinquent. If not

paid by July 1, the delinquent taxes are transmitted to the Land Commissioner for the sale of the property

2015 – Land Commissioner will attempt to collect delinquent taxes

2016 – Land Commissioner will continue to attempt to collect delinquent taxes

2017 – Land Commissioner will sell property by bids for the purpose of payment of taxes.

Property Tax

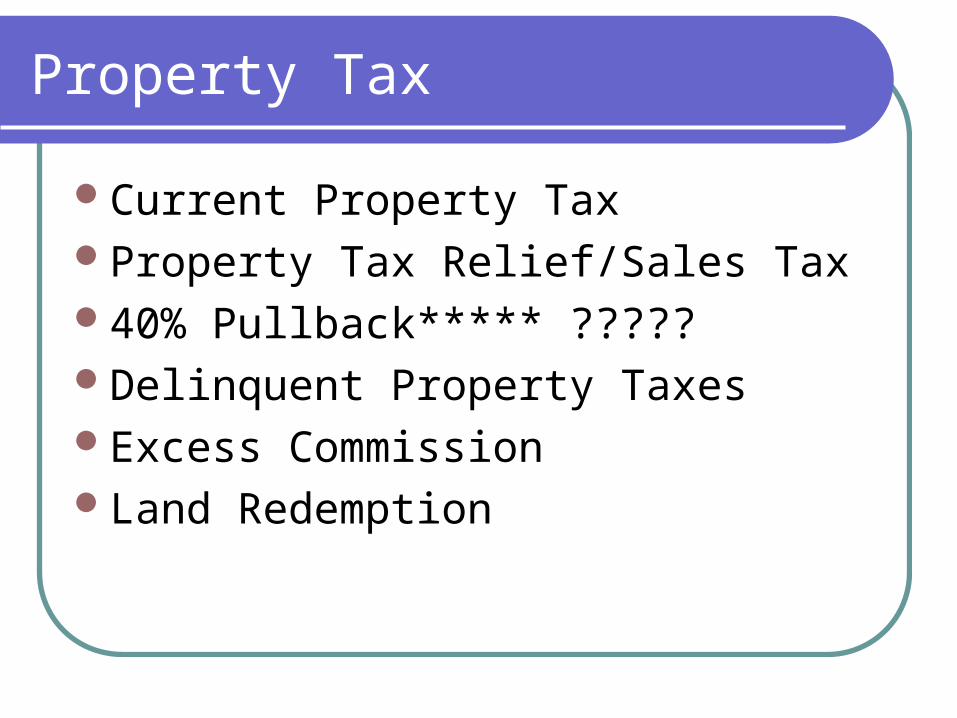

Current Property TaxProperty Tax Relief/Sales Tax40% Pullback***** ?????Delinquent Property TaxesExcess CommissionLand Redemption

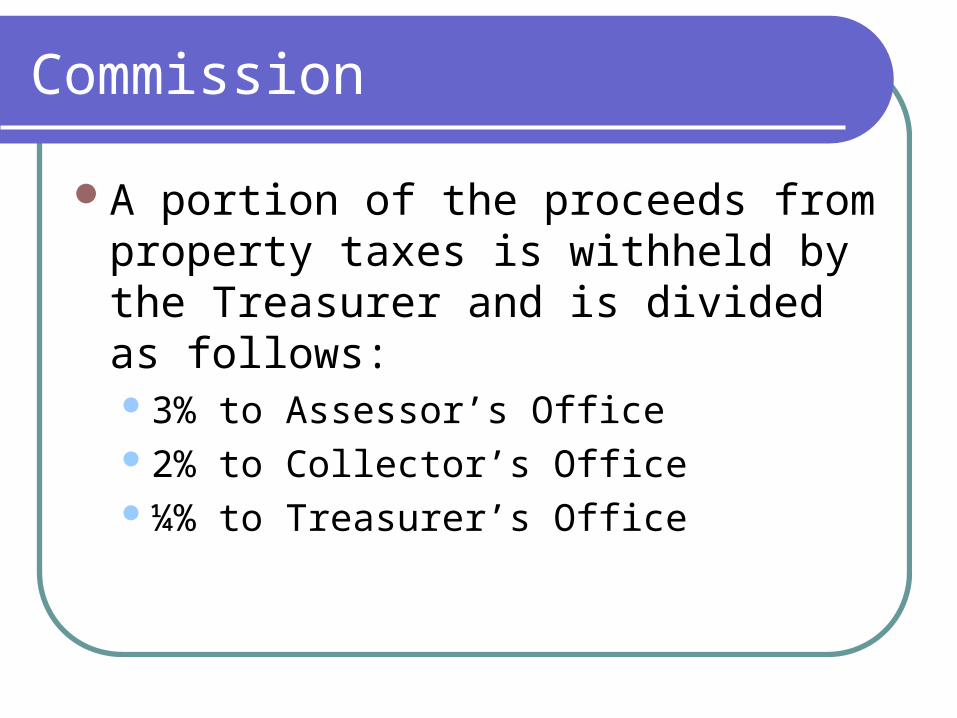

Commission

A portion of the proceeds from property taxes is withheld by the Treasurer and is divided as follows:3% to Assessor’s Office2% to Collector’s Office¼% to Treasurer’s Office

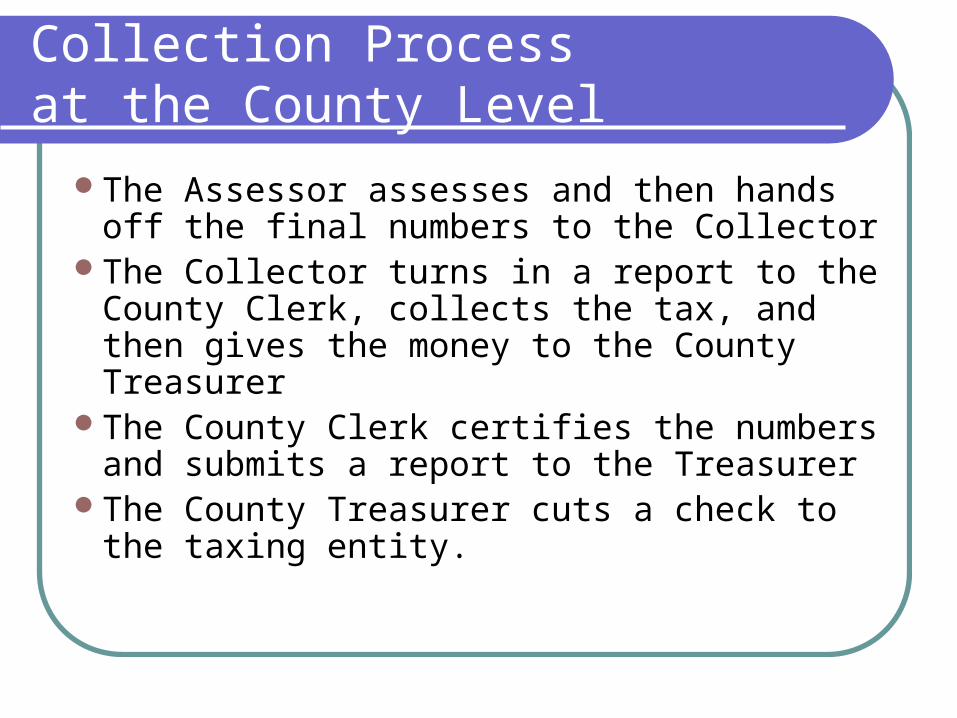

Collection Process at the County Level

The Assessor assesses and then hands off the final numbers to the Collector

The Collector turns in a report to the County Clerk, collects the tax, and then gives the money to the County Treasurer

The County Clerk certifies the numbers and submits a report to the Treasurer

The County Treasurer cuts a check to the taxing entity.

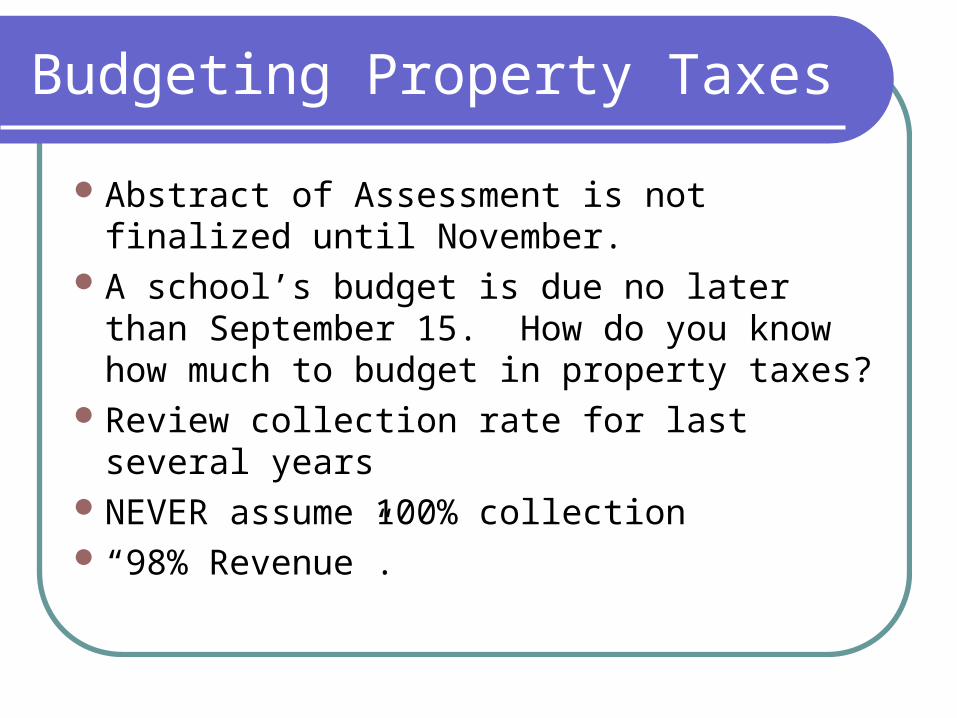

Budgeting Property Taxes

Abstract of Assessment is not finalized until November.

A school’s budget is due no later than September 15. How do you know how much to budget in property taxes?

Review collection rate for last several yearsNEVER assume 100% collection “98% Revenue”.

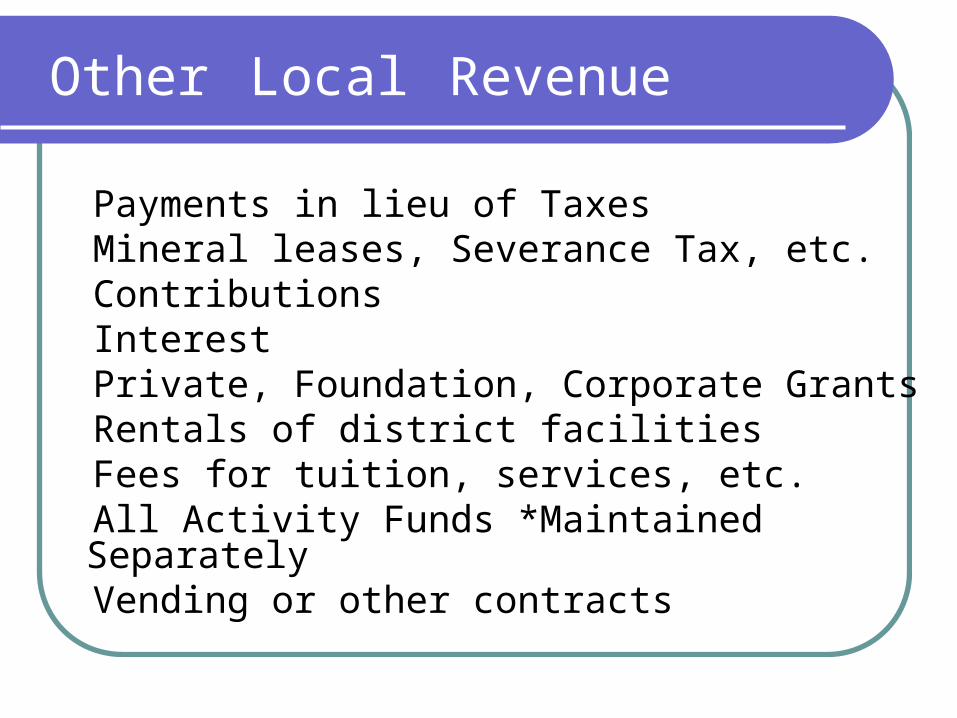

Other Local Revenue

Payments in lieu of TaxesMineral leases, Severance Tax, etc.ContributionsInterestPrivate, Foundation, Corporate GrantsRentals of district facilitiesFees for tuition, services, etc.All Activity Funds *Maintained SeparatelyVending or other contracts

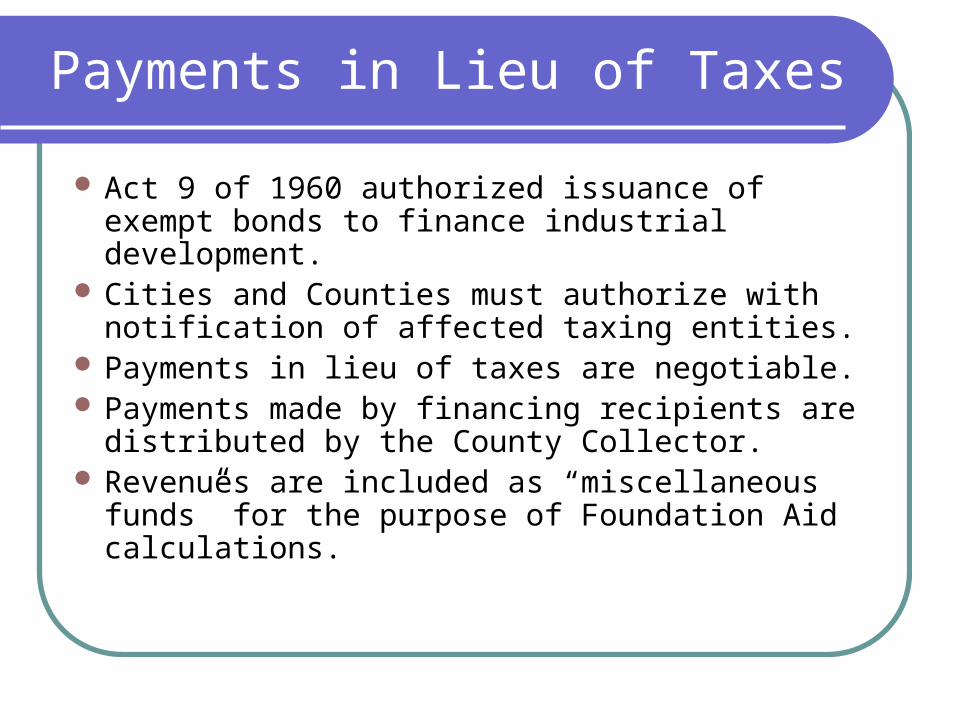

Payments in Lieu of Taxes

Act 9 of 1960 authorized issuance of exempt bonds to finance industrial development.

Cities and Counties must authorize with notification of affected taxing entities.

Payments in lieu of taxes are negotiable. Payments made by financing recipients are

distributed by the County Collector. Revenues are included as “miscellaneous

funds” for the purpose of Foundation Aid calculations.

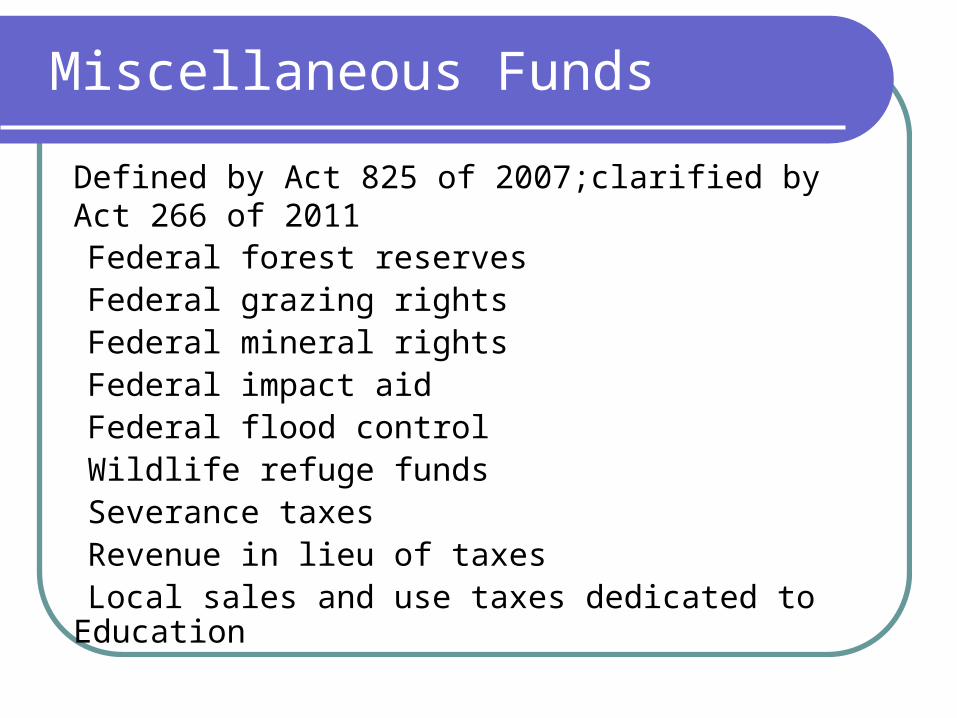

Miscellaneous Funds

Defined by Act 825 of 2007;clarified by Act 266 of 2011Federal forest reservesFederal grazing rightsFederal mineral rightsFederal impact aidFederal flood controlWildlife refuge fundsSeverance taxesRevenue in lieu of taxesLocal sales and use taxes dedicated to Education

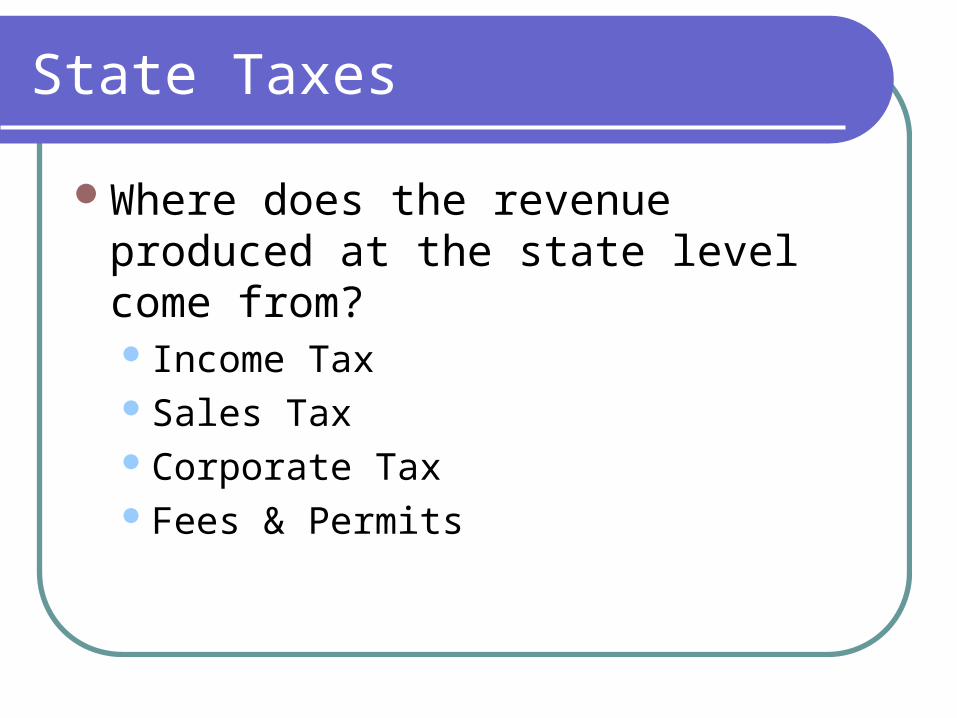

State Taxes

Where does the revenue produced at the state level come from? Income TaxSales TaxCorporate TaxFees & Permits

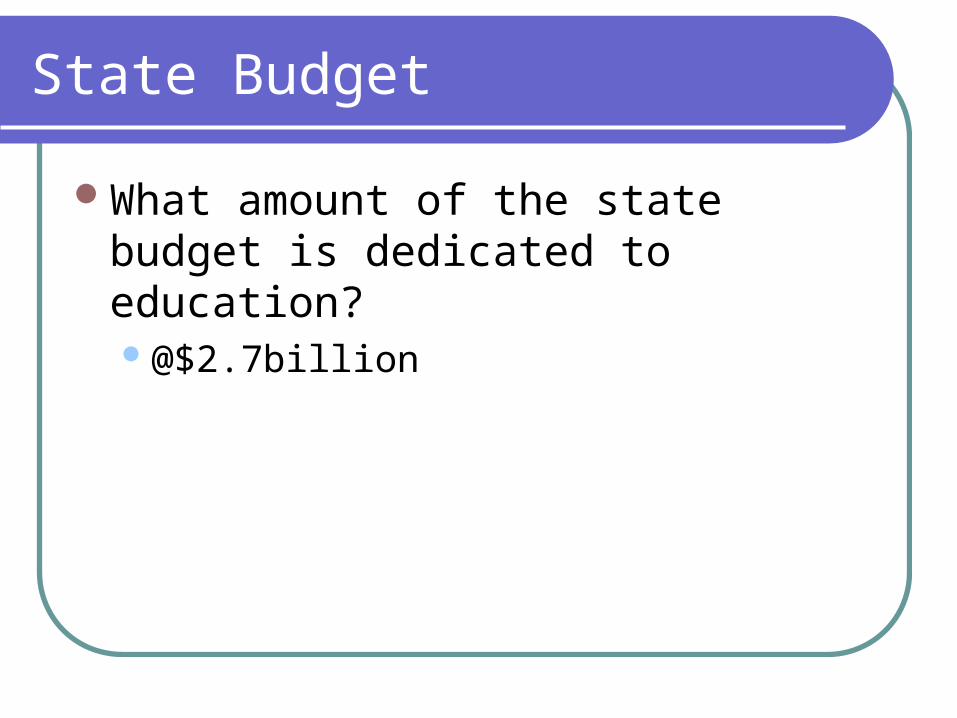

State Budget

What amount of the state budget is dedicated to education?@$2.7billion

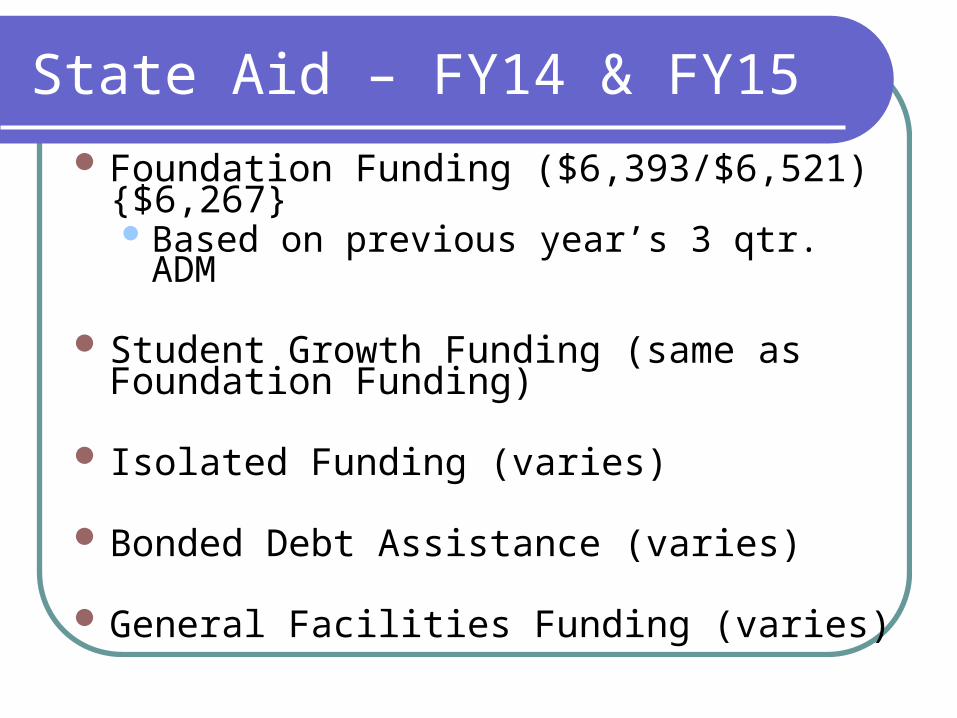

State Aid – FY14 & FY15

Foundation Funding ($6,393/$6,521) {$6,267} Based on previous year’s 3 qtr. ADM

Student Growth Funding (same as Foundation Funding)

Isolated Funding (varies)

Bonded Debt Assistance (varies)

General Facilities Funding (varies)

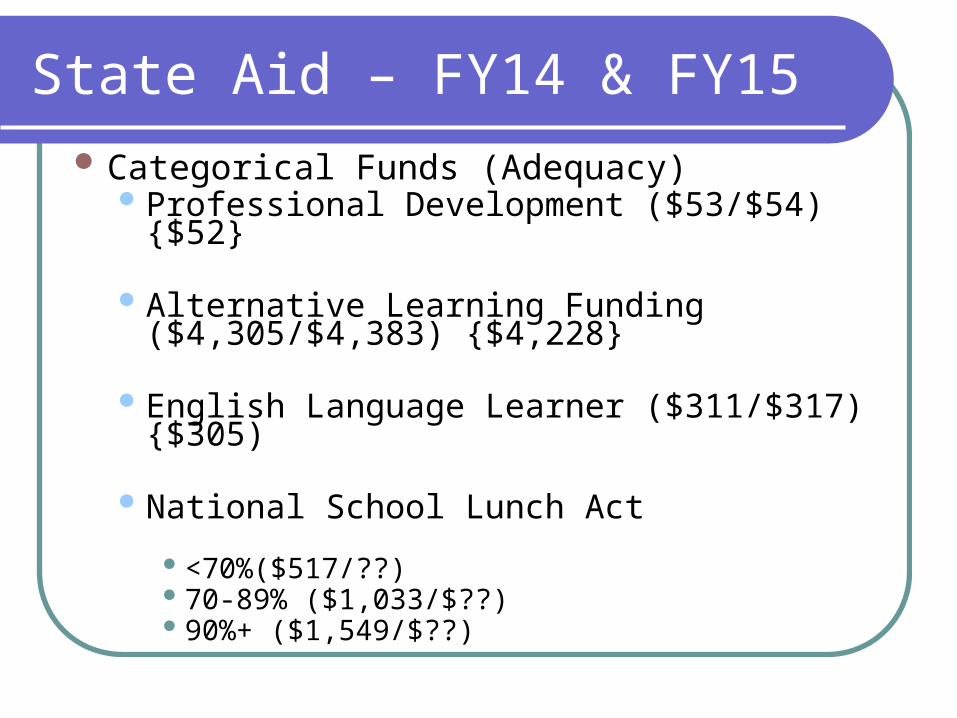

State Aid – FY14 & FY15

Categorical Funds (Adequacy) Professional Development ($53/$54) {$52}

Alternative Learning Funding ($4,305/$4,383) {$4,228}

English Language Learner ($311/$317) {$305)

National School Lunch Act <70%($517/??) 70-89% ($1,033/$??) 90%+ ($1,549/$??)

Calculating State Aid

Printout http://arkansased.org

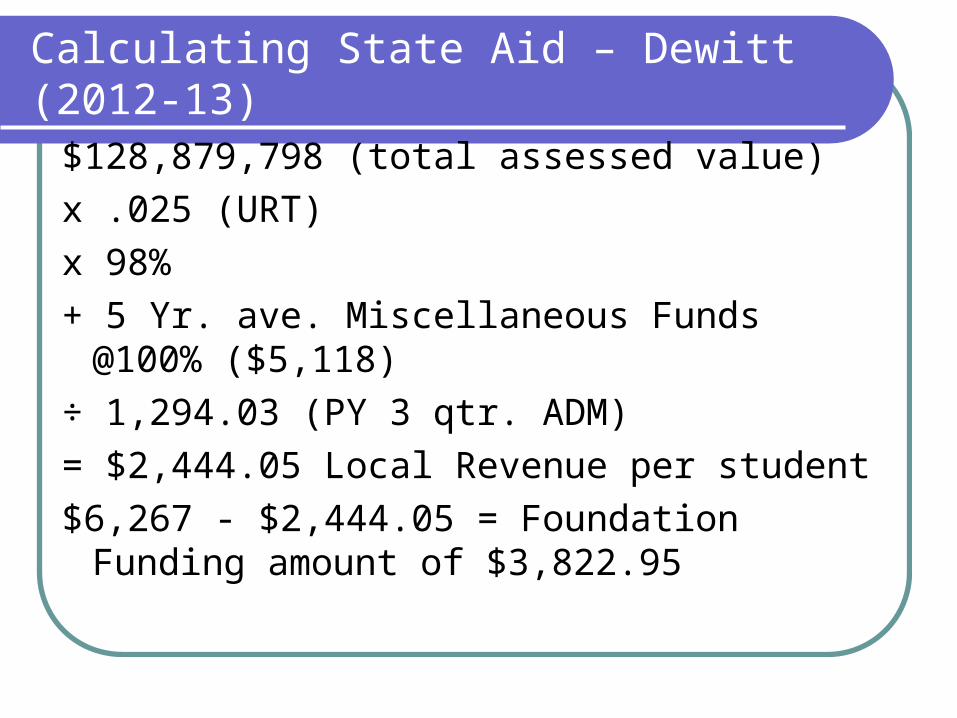

$128,879,798 (total assessed value)

x .025 (URT)

x 98%

+ 5 Yr. ave. Miscellaneous Funds @100% ($5,118)

÷ 1,294.03 (PY 3 qtr. ADM)

= $2,444.05 Local Revenue per student

$6,267 - $2,444.05 = Foundation Funding amount of $3,822.95

Calculating State Aid – Dewitt (2012-13)

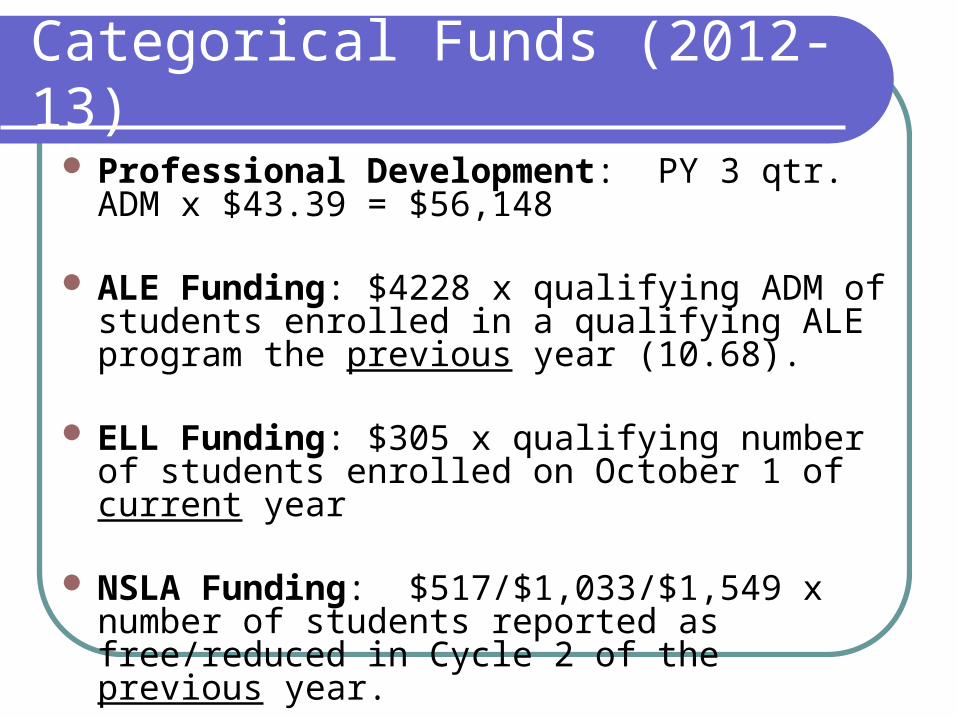

Categorical Funds (2012-13)

Professional Development: PY 3 qtr. ADM x $43.39 = $56,148

ALE Funding: $4228 x qualifying ADM of students enrolled in a qualifying ALE program the previous year (10.68).

ELL Funding: $305 x qualifying number of students enrolled on October 1 of current year

NSLA Funding: $517/$1,033/$1,549 x number of students reported as free/reduced in Cycle 2 of the previous year.

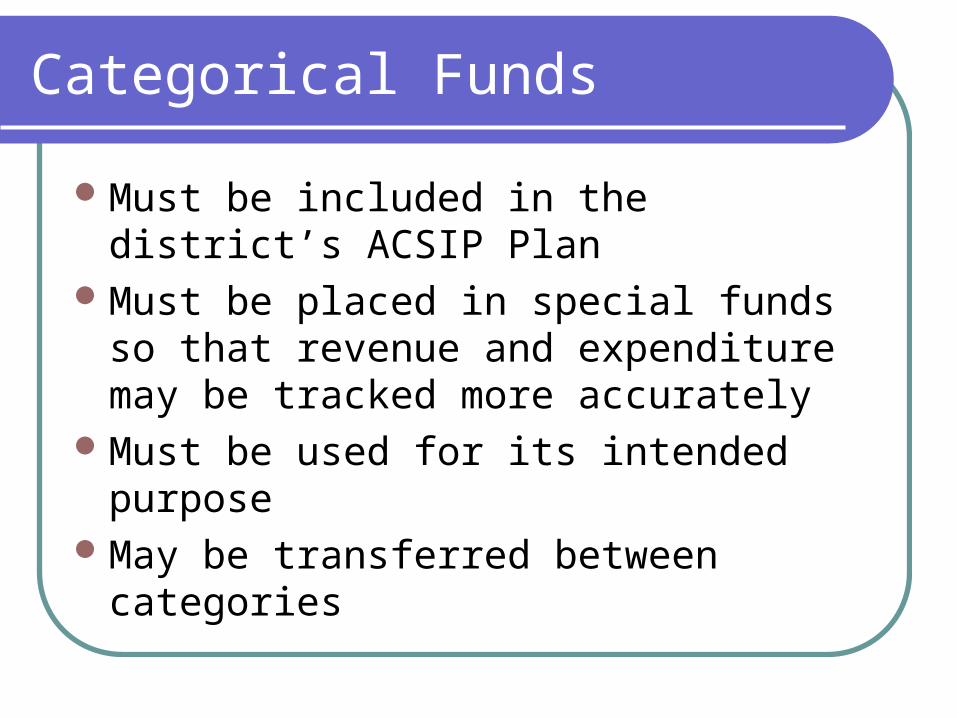

Categorical Funds

Must be included in the district’s ACSIP Plan

Must be placed in special funds so that revenue and expenditure may be tracked more accurately

Must be used for its intended purposeMay be transferred between categories

Funds

Restricted vs. Non-Restricted

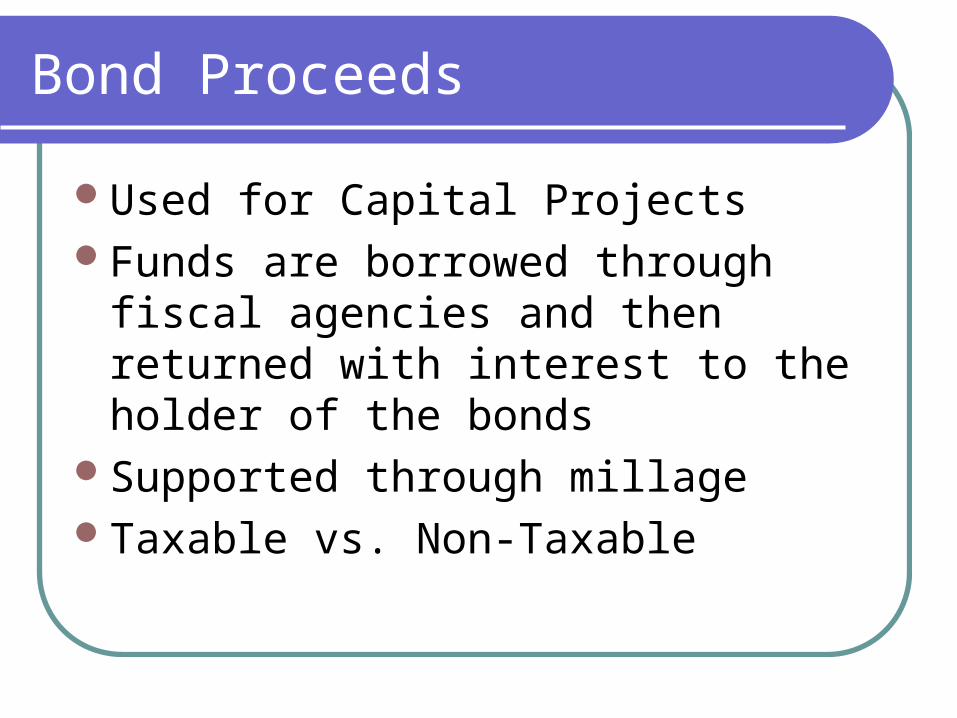

Bond Proceeds

Used for Capital ProjectsFunds are borrowed through fiscal

agencies and then returned with interest to the holder of the bonds

Supported through millageTaxable vs. Non-Taxable

Bond Proceeds

Like your personal banker, you can only borrow what the bond holder believes you can pay back

Bond holders will base their projections on numbers other than your actual budget

You will be able to borrow more money than you can actually afford to pay back.

Bond Proceeds

How does the local property wealth of a district affect your ability to borrow?What about proceeds from a district with

Low millage, low property value?Low millage, high property value?High millage, low property value?High millage, high property value?

Bond Proceeds Used For:

ConstructionRenovationEquippingArchitectural FeesLandOther legal purchases.

?

Should you issue bonds for the purchase of computers?

Federal Programs

Title I – Improving Achievement of Disadvantaged Children

Title II IIA – Improving Teacher Quality

Title III LEP Migrant

Title VI VIB – Special Ed

Federal Programs

Block Grants distributed from the Federal level to the SEA and then by the ADE to the LEA

Federal Programs Coordinator is key Must be a part of the ACSIP Plan May transfer between funds on a limited

basis

Federal Programs

How is your district using these funds? Title I – Improving Achievement of Disadvantaged

Children Title II

IIA – Improving Teacher Quality Title III Title VIB

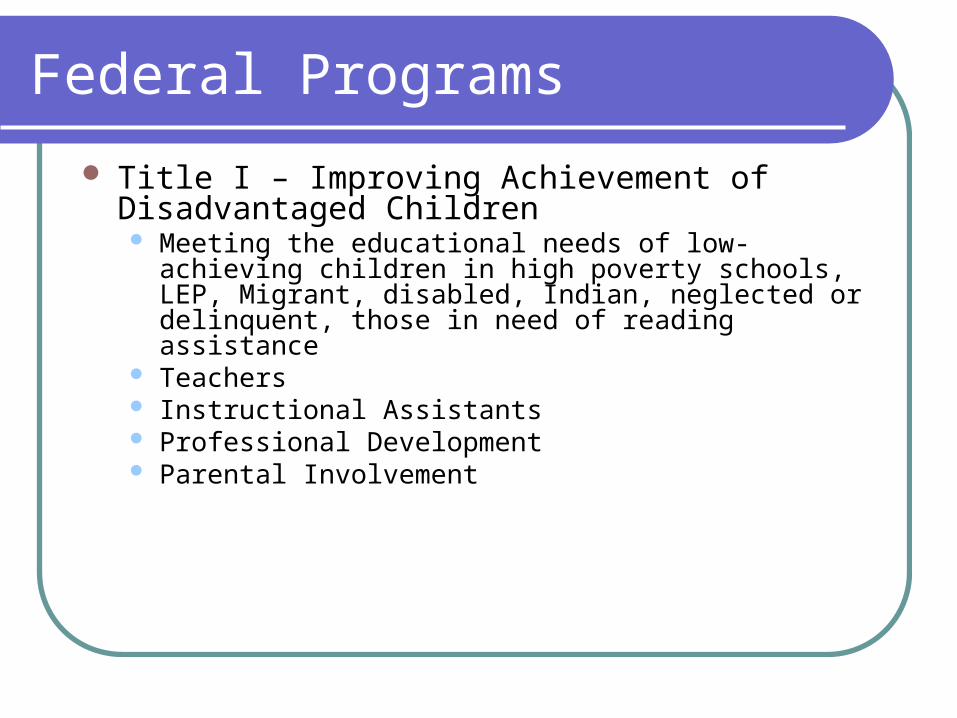

Federal Programs

Title I – Improving Achievement of Disadvantaged Children Meeting the educational needs of low-achieving children in

high poverty schools, LEP, Migrant, disabled, Indian, neglected or delinquent, those in need of reading assistance

Teachers Instructional Assistants Professional Development Parental Involvement

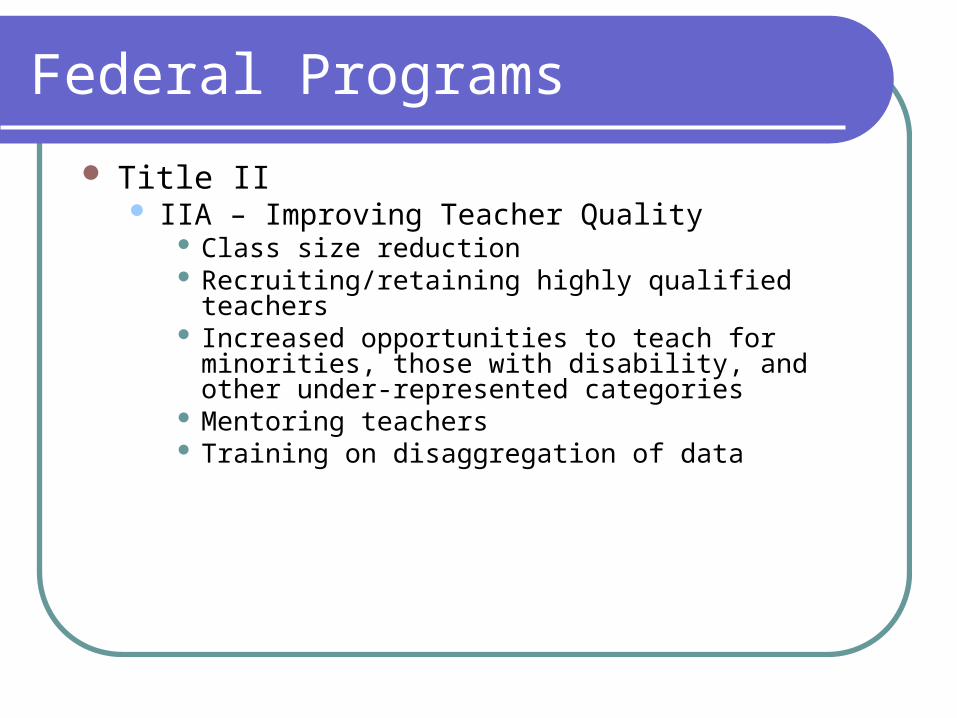

Federal Programs

Title II IIA – Improving Teacher Quality

Class size reduction Recruiting/retaining highly qualified teachers Increased opportunities to teach for minorities, those

with disability, and other under-represented categories Mentoring teachers Training on disaggregation of data

Federal Programs

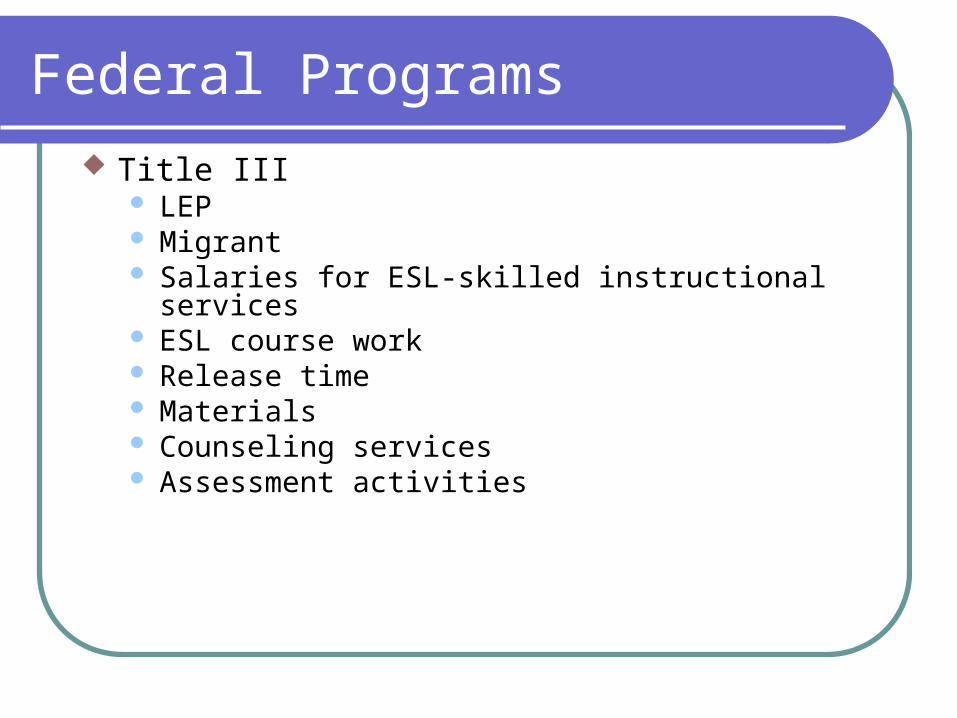

Title III LEP Migrant Salaries for ESL-skilled instructional services ESL course work Release time Materials Counseling services Assessment activities

Federal Programs

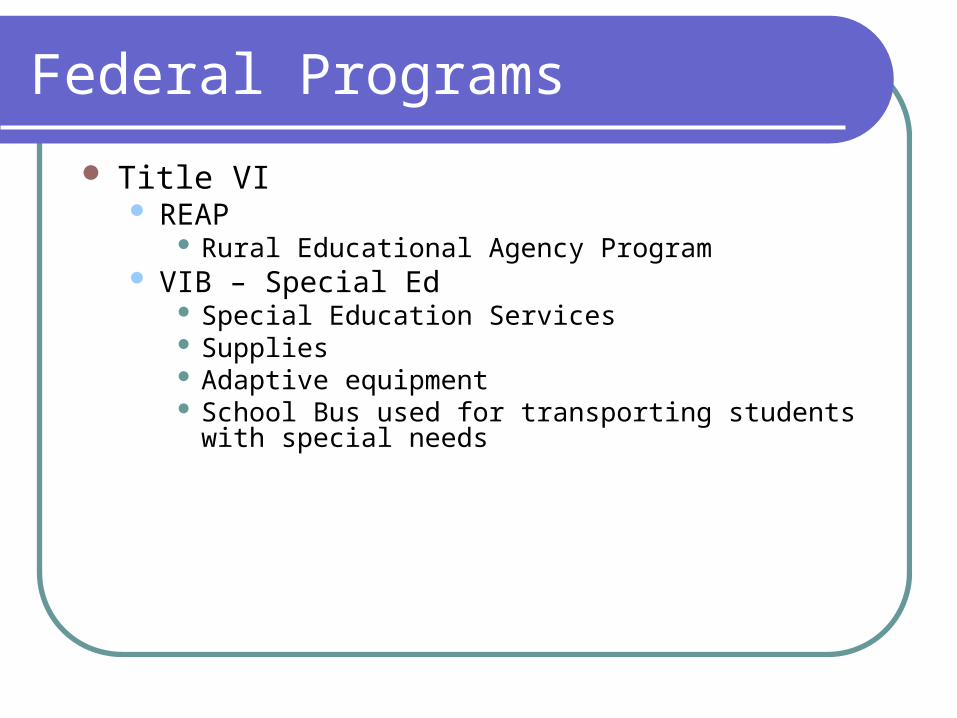

Title VI REAP

Rural Educational Agency Program VIB – Special Ed

Special Education Services Supplies Adaptive equipment School Bus used for transporting students with special

needs

Federal Programs

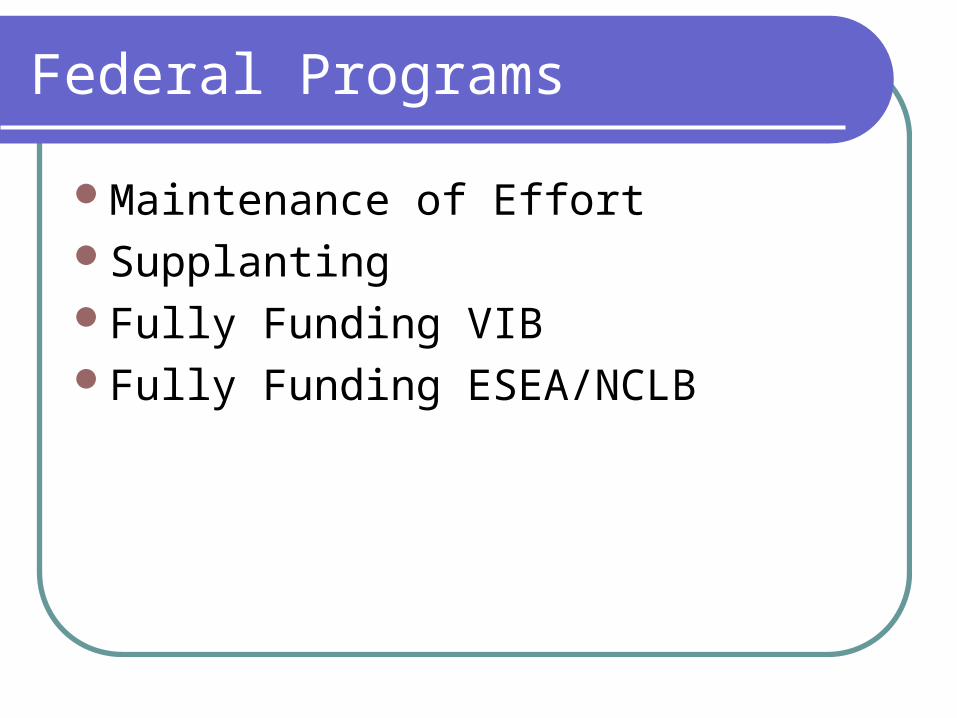

Maintenance of EffortSupplantingFully Funding VIBFully Funding ESEA/NCLB

Activity Funds

Revenue from?

Fiduciary Funds

ScholarshipsFoundations 501(c)3 ???

Grants

You may only use the proceeds from a grant for the purpose for which it was granted.

Be aggressive about seeking grants – every little bit helps.

Food Service - Revenue

SalesNSLA (free/reduced program) * Don’t

confuse this with the state’s Categorical Funds!

Food Service - Expenses

Food commoditiesEquipmentPersonnelProfessional Development

Food Service

How to qualify for Free/Reduced Meals Income Eligibility GuidelinesWhat income must a family of four receive

in order to qualify for free meals? Reduced meals?

Income Eligibility Guidelines

Below are the Department's annual adjustments to the Income Eligibility Guidelines, to be used in determining eligibility for free and reduced price meals or free milk. These guidelines are used by schools, institutions, and facilities participating in the National School Lunch Program (and Commodity School Program), School Breakfast Program, Special Milk Program for Children, Child and Adult Care Food Program and Summer Food Service Program. The annual adjustments are required by section 9 of the National School Lunch Act. The guidelines are intended to direct benefits to those children most in need and are revised annually to account for changes in the Consumer Price Index. They are effective from July 1 through June 30 every year.

http://www.fns.usda.gov/cnd/governance/notices/iegs/iegs.htm

![Which Outbound Marketing Program Is Right For You? [PPT]](https://img.pdfslide.tips/doc/110x75/58731fc61a28ab673e8b730d/which-outbound-marketing-program-is-right-for-you-ppt.jpg)