Embed Size (px)

Citation preview

Updates/Amendments in Companies Act, 2013

CS DHARMENDRA GANATRA

PRACTISING COMPANY SECRETARY

Saturday- 07.10.2017

CS DHARMENDRA GANATRA

CS DHARMENDRA GANATRA

CS DHARMENDRA GANATRA

CS DHARMENDRA GANATRA

CS DHARMENDRA GANATRA

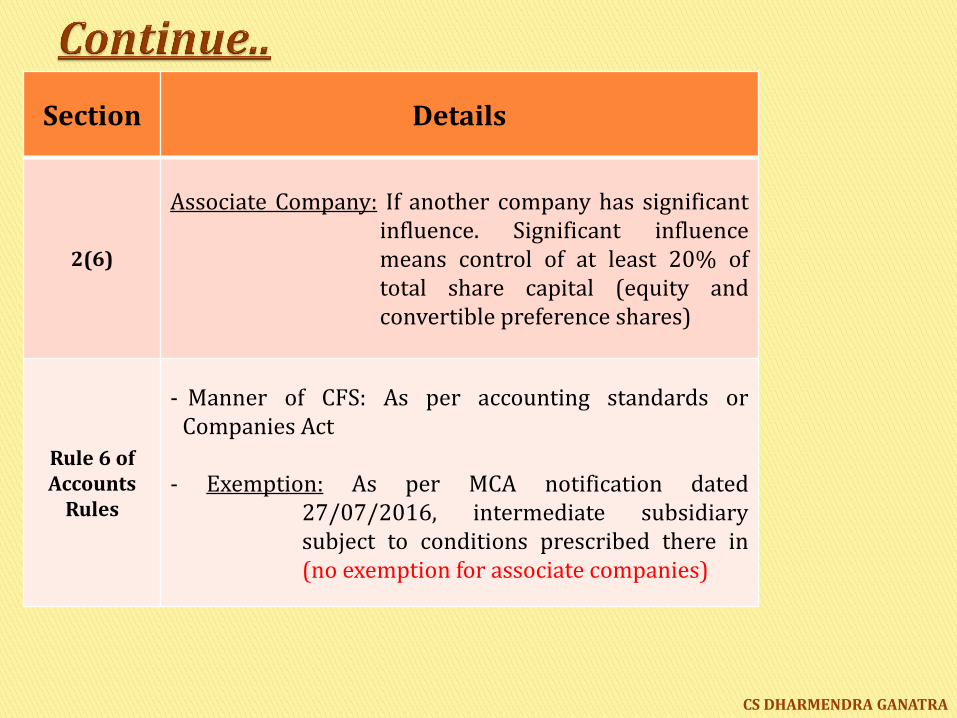

Section Details

2(6)

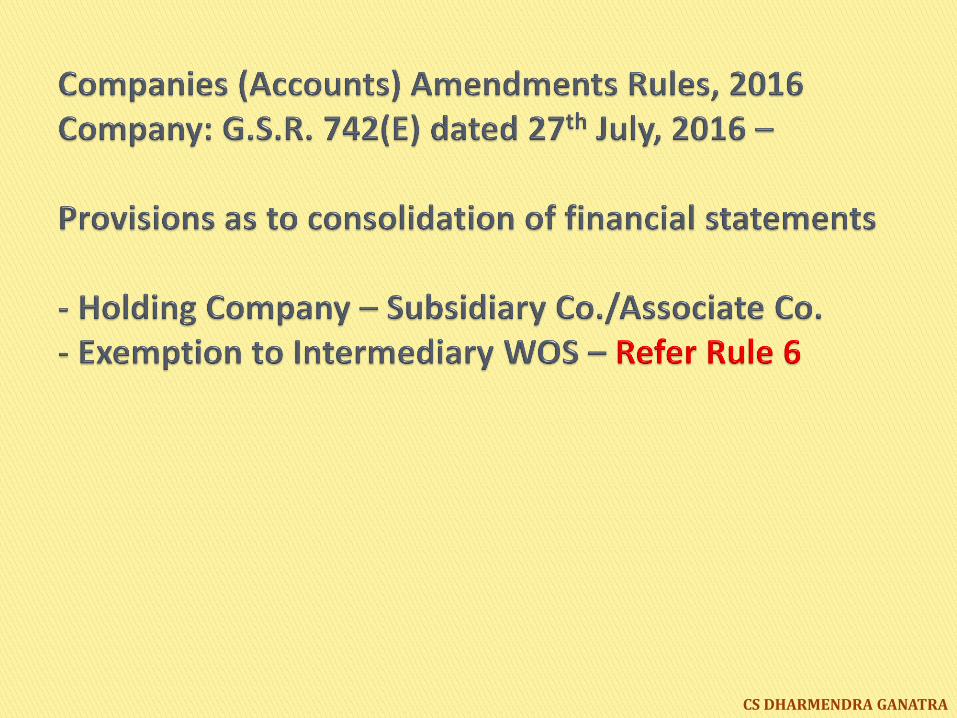

Associate Company: If another company has significant influence. Significant influence means control of at least 20% of total share capital (equity and convertible preference shares)

Rule 6 of Accounts

Rules

- Manner of CFS: As per accounting standards or Companies Act

- Exemption: As per MCA notification dated

27/07/2016, intermediate subsidiary subject to conditions prescribed there in (no exemption for associate companies)

CS DHARMENDRA GANATRA

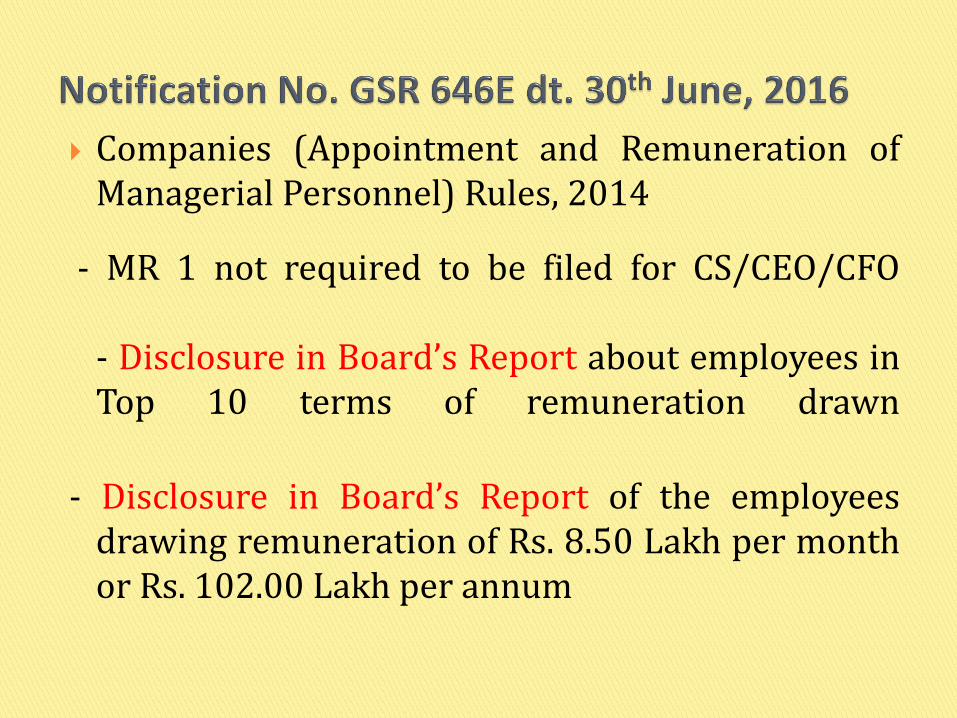

Companies (Appointment and Remuneration of Managerial Personnel) Rules, 2014

- MR 1 not required to be filed for CS/CEO/CFO

- Disclosure in Board’s Report about employees in Top 10 terms of remuneration drawn

- Disclosure in Board’s Report of the employees drawing remuneration of Rs. 8.50 Lakh per month or Rs. 102.00 Lakh per annum

CS DHARMENDRA GANATRA

CS DHARMENDRA GANATRA

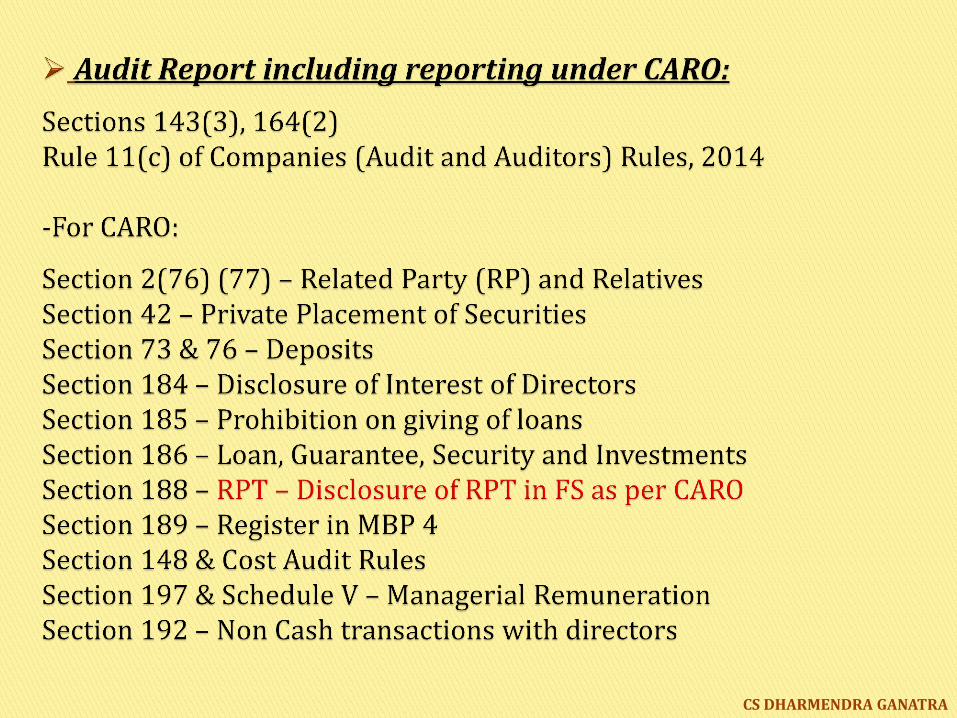

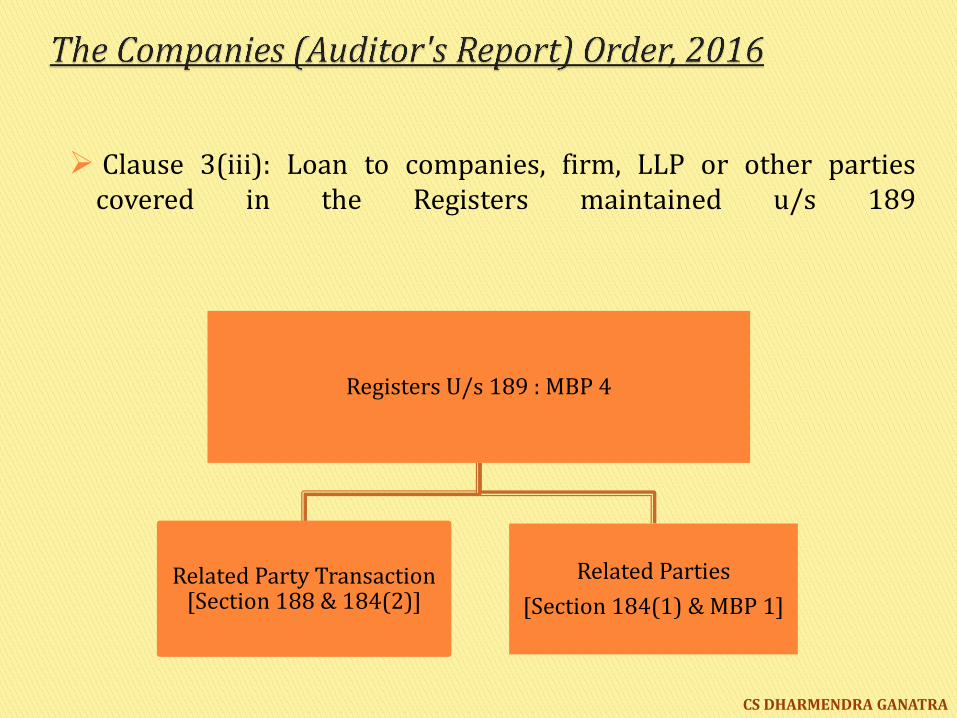

Clause 3(iii): Loan to companies, firm, LLP or other parties covered in the Registers maintained u/s 189

Registers U/s 189 : MBP 4

Related Party Transaction [Section 188 & 184(2)]

Related Parties

[Section 184(1) & MBP 1]

CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

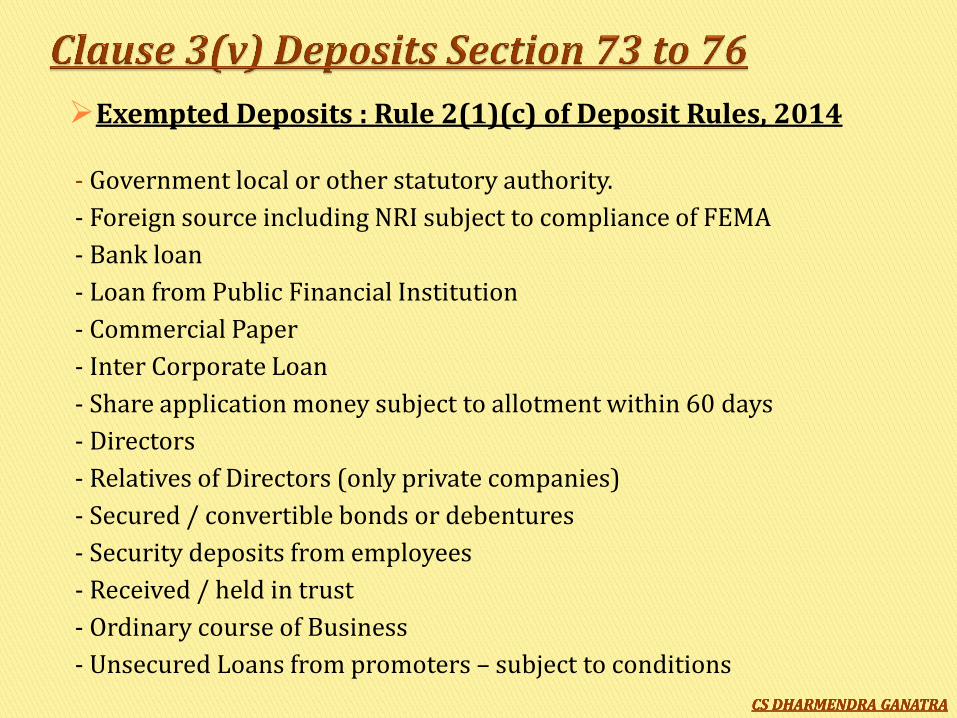

Exempted Deposits : Rule 2(1)(c) of Deposit Rules, 2014

- Government local or other statutory authority.

- Foreign source including NRI subject to compliance of FEMA

- Bank loan

- Loan from Public Financial Institution

- Commercial Paper

- Inter Corporate Loan

- Share application money subject to allotment within 60 days

- Directors

- Relatives of Directors (only private companies)

- Secured / convertible bonds or debentures

- Security deposits from employees

- Received / held in trust

- Ordinary course of Business

- Unsecured Loans from promoters – subject to conditions

CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

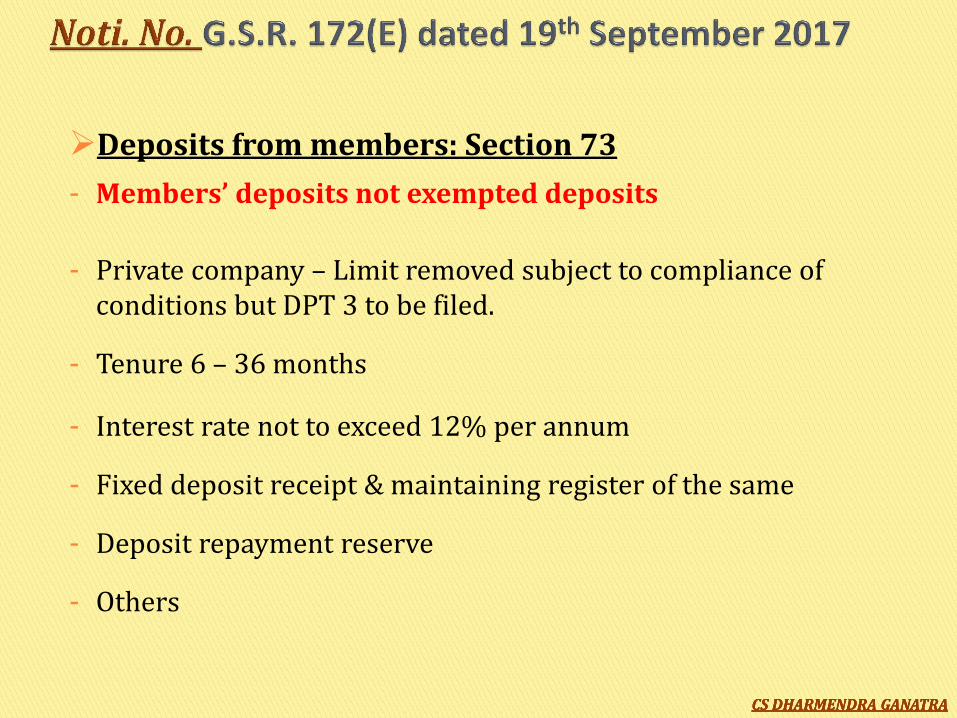

Deposits from members: Section 73

- Members’ deposits not exempted deposits

- Private company – Limit removed subject to compliance of conditions but DPT 3 to be filed.

- Tenure 6 – 36 months

- Interest rate not to exceed 12% per annum

- Fixed deposit receipt & maintaining register of the same

- Deposit repayment reserve

- Others

CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

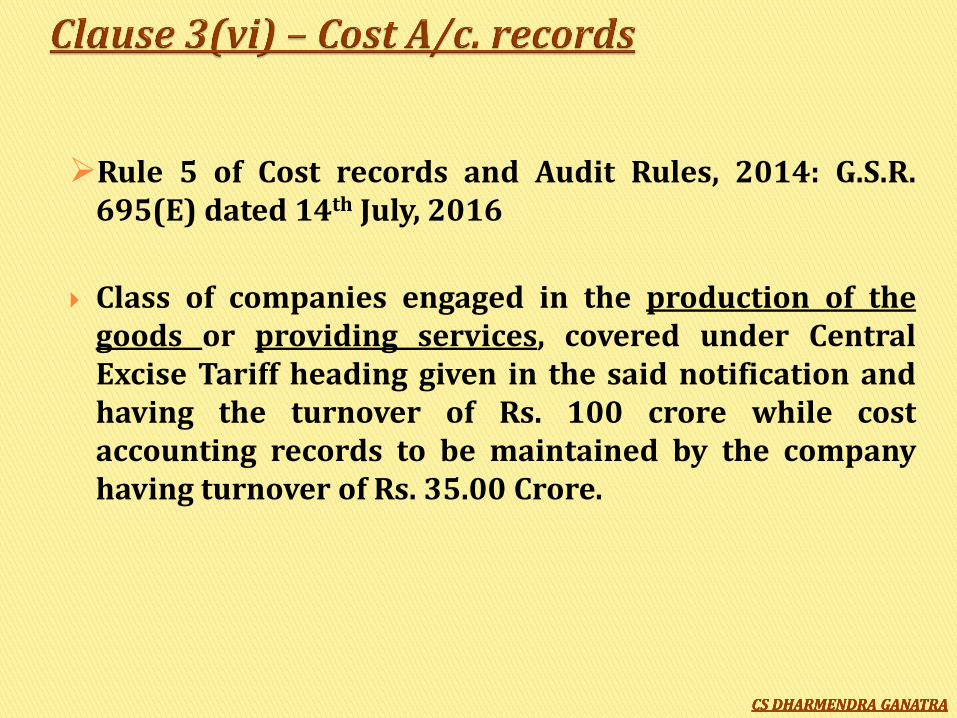

Rule 5 of Cost records and Audit Rules, 2014: G.S.R. 695(E) dated 14th July, 2016

Class of companies engaged in the production of the goods or providing services, covered under Central Excise Tariff heading given in the said notification and having the turnover of Rs. 100 crore while cost accounting records to be maintained by the company having turnover of Rs. 35.00 Crore.

CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

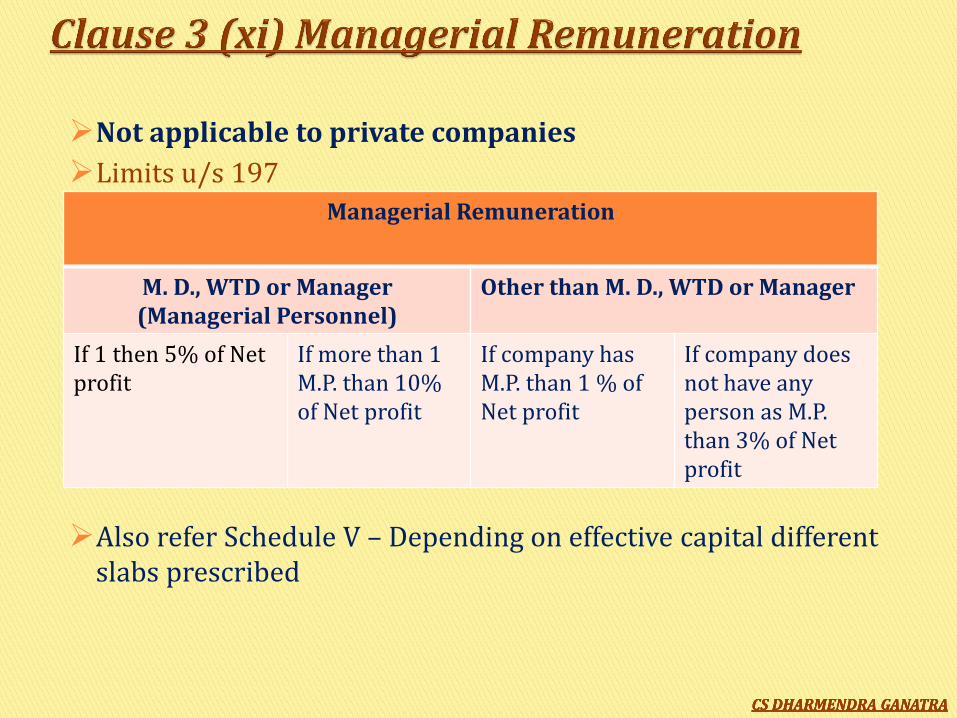

Not applicable to private companies

Limits u/s 197

Also refer Schedule V – Depending on effective capital different slabs prescribed

Managerial Remuneration

M. D., WTD or Manager (Managerial Personnel)

Other than M. D., WTD or Manager

If 1 then 5% of Net profit

If more than 1 M.P. than 10% of Net profit

If company has M.P. than 1 % of Net profit

If company does not have any person as M.P. than 3% of Net profit

CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

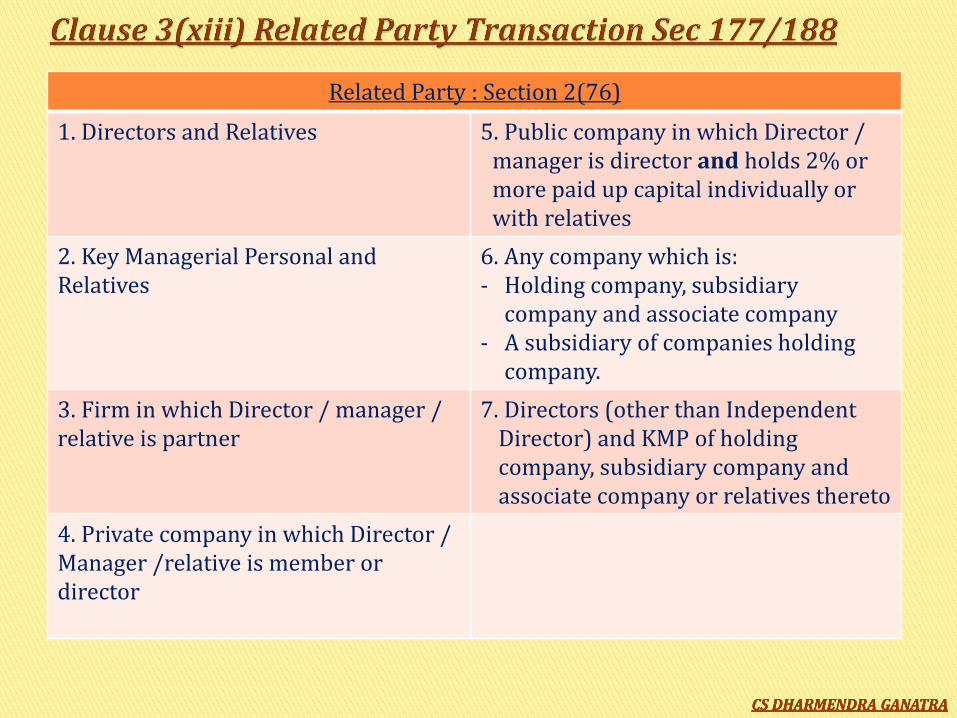

Related Party : Section 2(76)

1. Directors and Relatives 5. Public company in which Director / manager is director and holds 2% or more paid up capital individually or with relatives

2. Key Managerial Personal and Relatives

6. Any company which is: - Holding company, subsidiary

company and associate company - A subsidiary of companies holding

company.

3. Firm in which Director / manager / relative is partner

7. Directors (other than Independent Director) and KMP of holding company, subsidiary company and associate company or relatives thereto

4. Private company in which Director / Manager /relative is member or director

CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

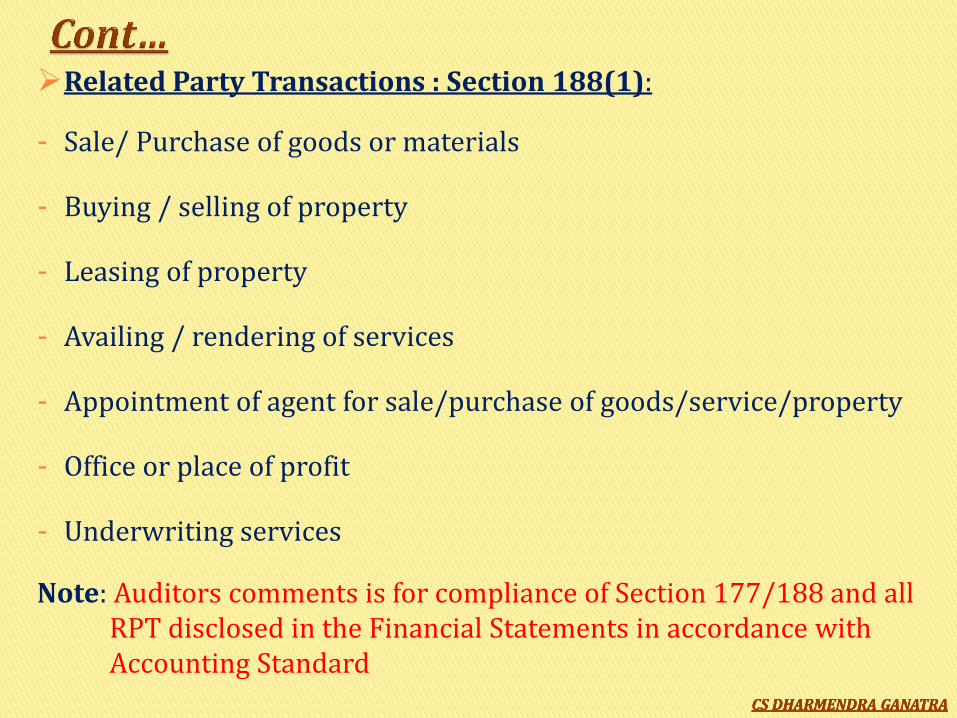

Related Party Transactions : Section 188(1):

- Sale/ Purchase of goods or materials

- Buying / selling of property

- Leasing of property

- Availing / rendering of services

- Appointment of agent for sale/purchase of goods/service/property

- Office or place of profit

- Underwriting services

Note: Auditors comments is for compliance of Section 177/188 and all RPT disclosed in the Financial Statements in accordance with Accounting Standard

CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

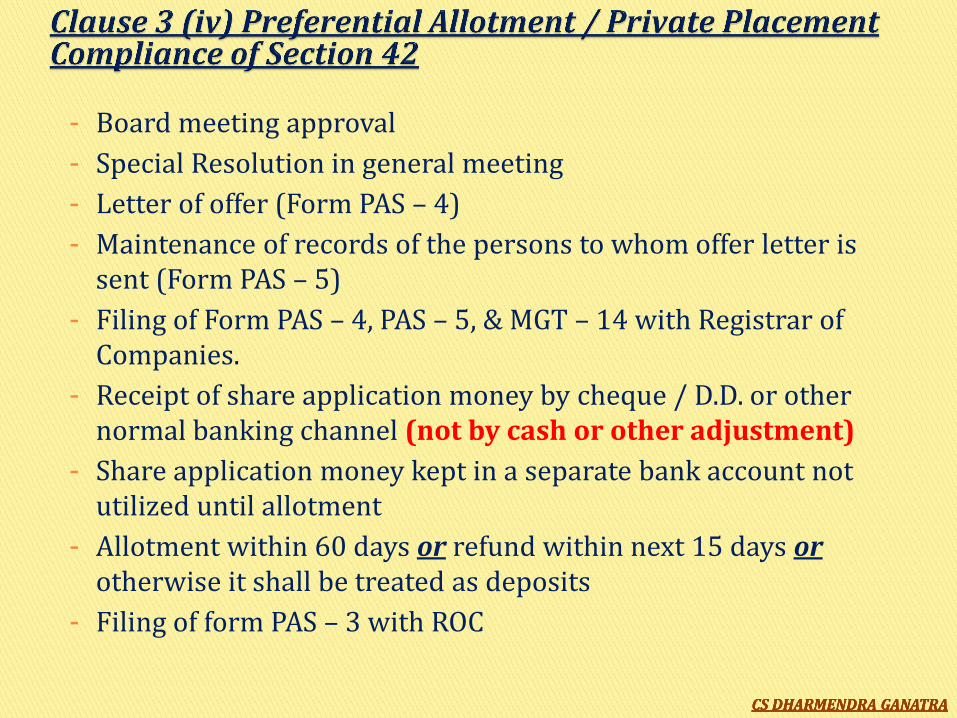

- Board meeting approval

- Special Resolution in general meeting

- Letter of offer (Form PAS – 4)

- Maintenance of records of the persons to whom offer letter is sent (Form PAS – 5)

- Filing of Form PAS – 4, PAS – 5, & MGT – 14 with Registrar of Companies.

- Receipt of share application money by cheque / D.D. or other normal banking channel (not by cash or other adjustment)

- Share application money kept in a separate bank account not utilized until allotment

- Allotment within 60 days or refund within next 15 days or otherwise it shall be treated as deposits

- Filing of form PAS – 3 with ROC

CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA CS DHARMENDRA GANATRA

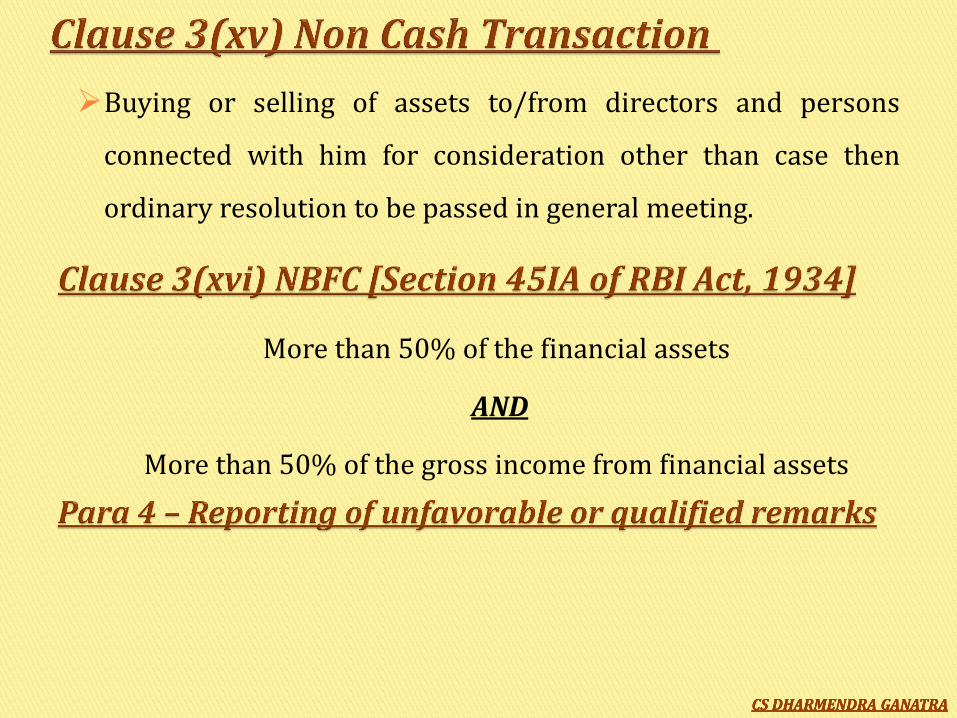

Buying or selling of assets to/from directors and persons

connected with him for consideration other than case then

ordinary resolution to be passed in general meeting.

More than 50% of the financial assets

AND

More than 50% of the gross income from financial assets

CS DHARMENDRA GANATRA

Section / Rules

Details

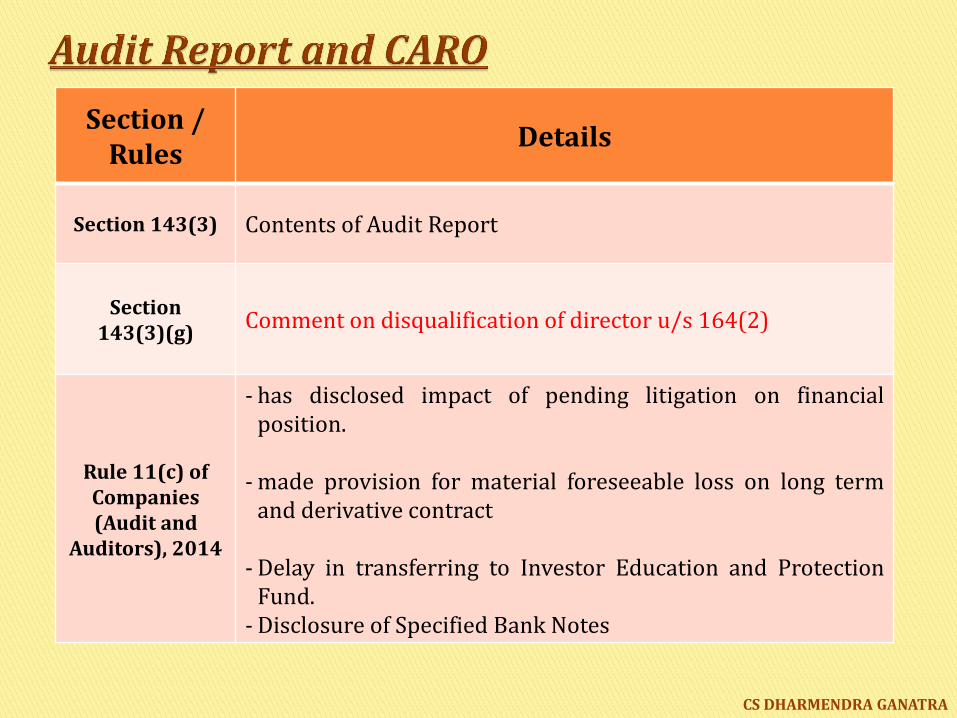

Section 143(3) Contents of Audit Report

Section 143(3)(g)

Comment on disqualification of director u/s 164(2)

Rule 11(c) of Companies (Audit and

Auditors), 2014

- has disclosed impact of pending litigation on financial position.

- made provision for material foreseeable loss on long term and derivative contract

- Delay in transferring to Investor Education and Protection Fund.

- Disclosure of Specified Bank Notes

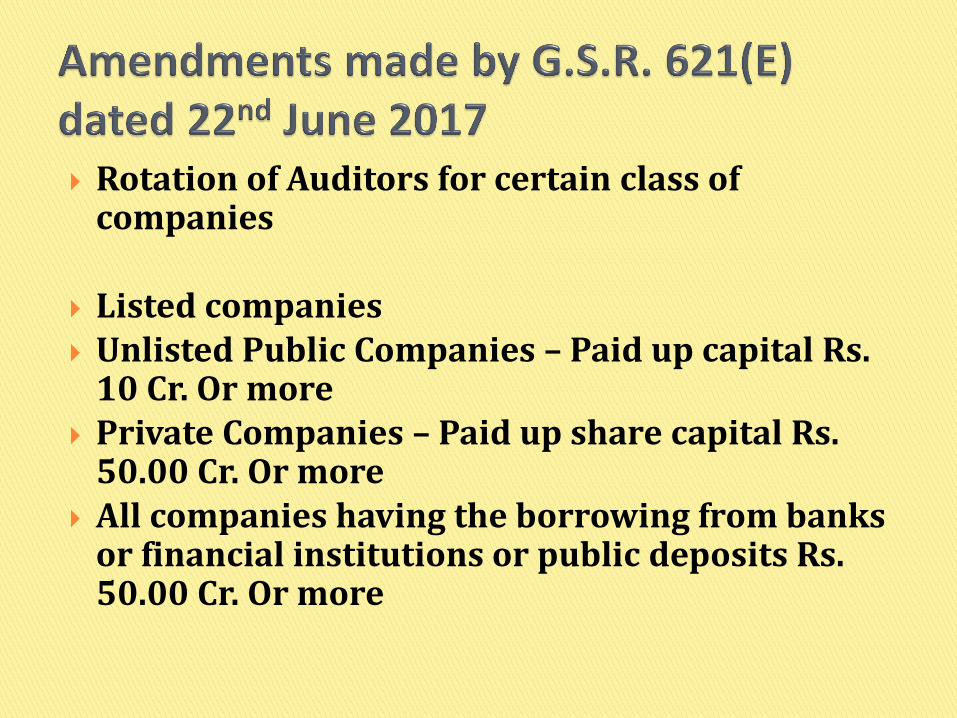

Rotation of Auditors for certain class of companies

Listed companies Unlisted Public Companies – Paid up capital Rs.

10 Cr. Or more Private Companies – Paid up share capital Rs.

50.00 Cr. Or more All companies having the borrowing from banks

or financial institutions or public deposits Rs. 50.00 Cr. Or more

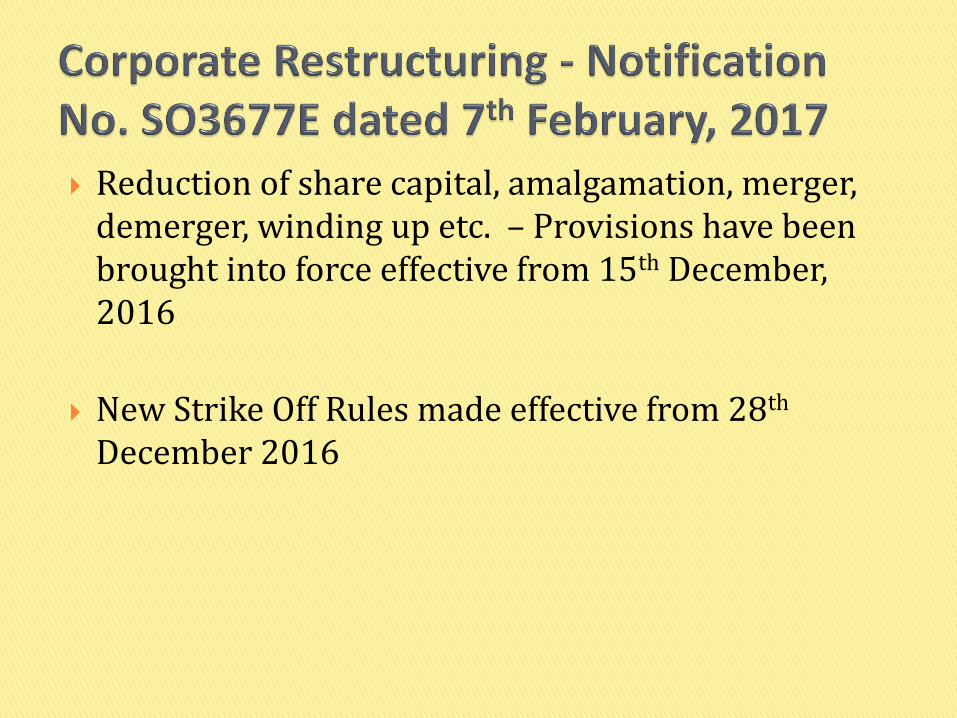

Reduction of share capital, amalgamation, merger, demerger, winding up etc. – Provisions have been brought into force effective from 15th December, 2016

New Strike Off Rules made effective from 28th December 2016

Not more than two layers of subsidiary company – Section 2 (87) notified effective from 20th September, 2017

CS DHARMENDRA GANATRA

THANKS

RAJKOT BRANCH OF WIRC OF ICAI

BY CA VIKASH JAIN

B.com (Hons)., FCA, DISA, IP, Arbitrator

07TH October, 2017

Email Id: [email protected]

Contact No. 9327715892

CA Vikash Jain

ACT CONTAINS :

29 Chapters

470 Clauses

7 Schedules

CA Vikash Jain

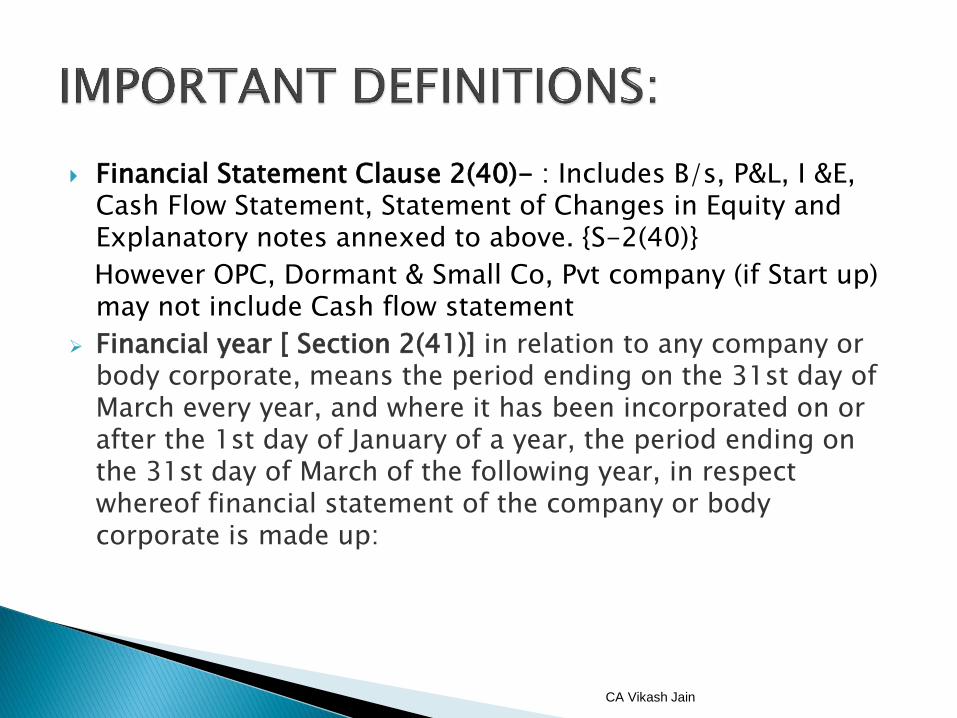

Financial Statement Clause 2(40)- : Includes B/s, P&L, I &E, Cash Flow Statement, Statement of Changes in Equity and Explanatory notes annexed to above. {S-2(40)}

However OPC, Dormant & Small Co, Pvt company (if Start up) may not include Cash flow statement

Financial year [ Section 2(41)] in relation to any company or body corporate, means the period ending on the 31st day of March every year, and where it has been incorporated on or after the 1st day of January of a year, the period ending on the 31st day of March of the following year, in respect whereof financial statement of the company or body corporate is made up:

CA Vikash Jain

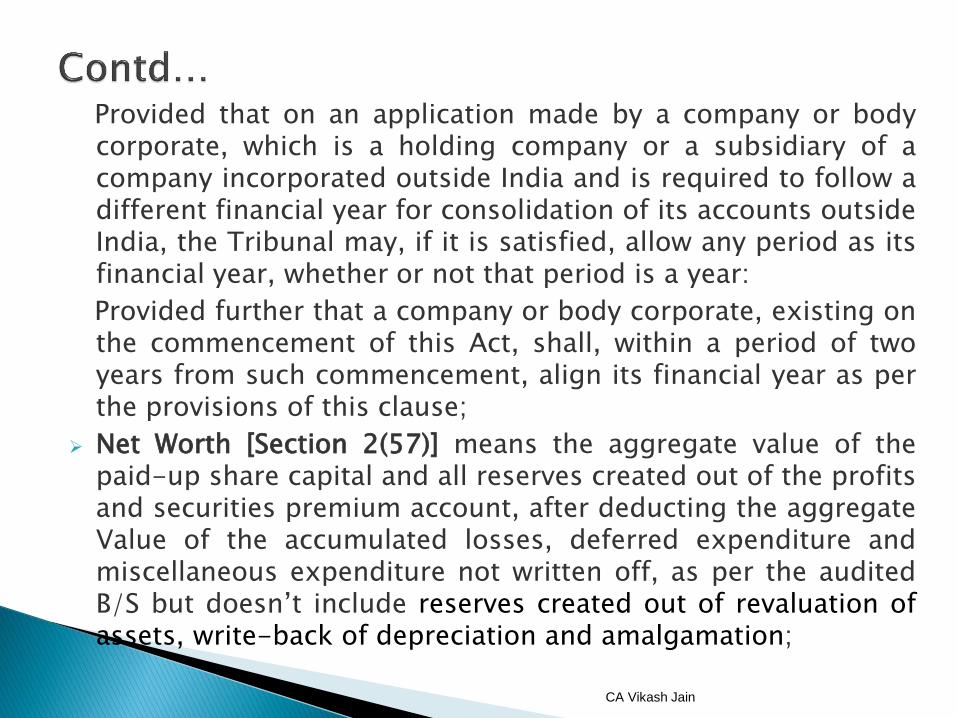

Provided that on an application made by a company or body corporate, which is a holding company or a subsidiary of a company incorporated outside India and is required to follow a different financial year for consolidation of its accounts outside India, the Tribunal may, if it is satisfied, allow any period as its financial year, whether or not that period is a year:

Provided further that a company or body corporate, existing on the commencement of this Act, shall, within a period of two years from such commencement, align its financial year as per the provisions of this clause;

Net Worth [Section 2(57)] means the aggregate value of the paid-up share capital and all reserves created out of the profits and securities premium account, after deducting the aggregate Value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited B/S but doesn’t include reserves created out of revaluation of assets, write-back of depreciation and amalgamation;

CA Vikash Jain

CA Vikash Jain

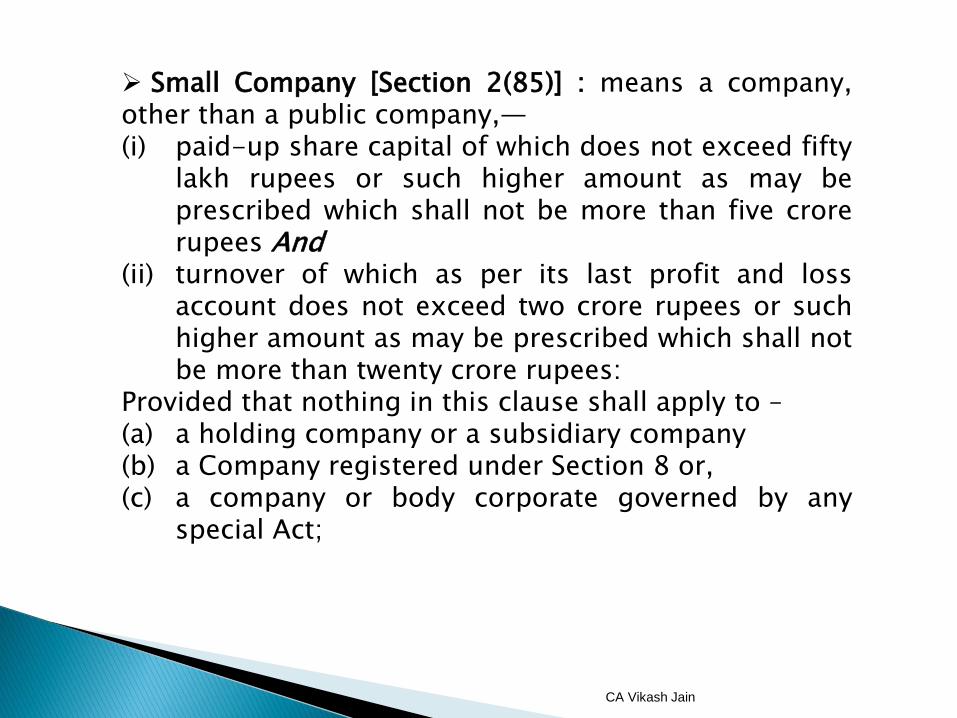

Small Company [Section 2(85)] : means a company, other than a public company,— (i) paid-up share capital of which does not exceed fifty

lakh rupees or such higher amount as may be prescribed which shall not be more than five crore rupees And

(ii) turnover of which as per its last profit and loss account does not exceed two crore rupees or such higher amount as may be prescribed which shall not be more than twenty crore rupees:

Provided that nothing in this clause shall apply to – (a) a holding company or a subsidiary company (b) a Company registered under Section 8 or, (c) a company or body corporate governed by any

special Act;

CA Vikash Jain

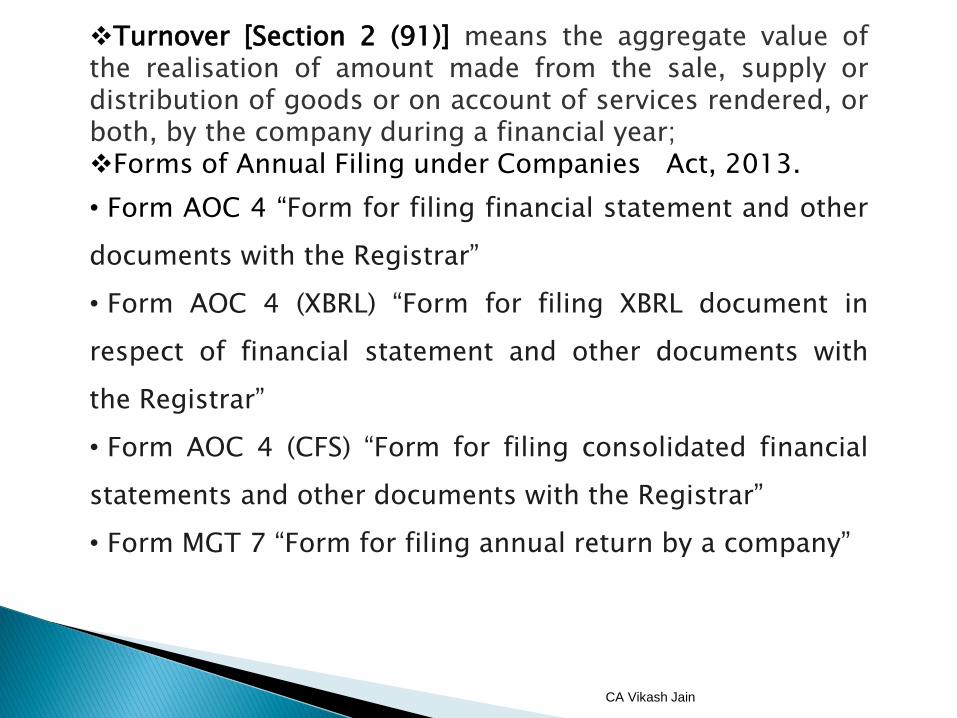

Turnover [Section 2 (91)] means the aggregate value of the realisation of amount made from the sale, supply or distribution of goods or on account of services rendered, or both, by the company during a financial year; Forms of Annual Filing under Companies Act, 2013.

• Form AOC 4 “Form for filing financial statement and other

documents with the Registrar”

• Form AOC 4 (XBRL) “Form for filing XBRL document in

respect of financial statement and other documents with

the Registrar”

• Form AOC 4 (CFS) “Form for filing consolidated financial

statements and other documents with the Registrar”

• Form MGT 7 “Form for filing annual return by a company”

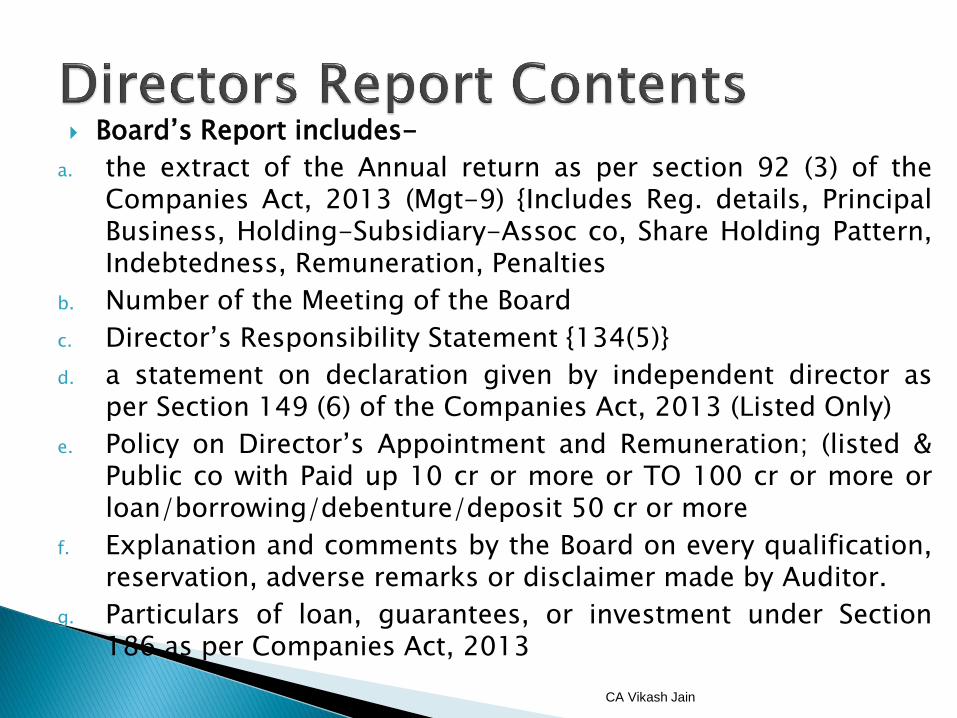

Board’s Report includes-

a. the extract of the Annual return as per section 92 (3) of the Companies Act, 2013 (Mgt-9) {Includes Reg. details, Principal Business, Holding-Subsidiary-Assoc co, Share Holding Pattern, Indebtedness, Remuneration, Penalties

b. Number of the Meeting of the Board

c. Director’s Responsibility Statement {134(5)}

d. a statement on declaration given by independent director as per Section 149 (6) of the Companies Act, 2013 (Listed Only)

e. Policy on Director’s Appointment and Remuneration; (listed & Public co with Paid up 10 cr or more or TO 100 cr or more or loan/borrowing/debenture/deposit 50 cr or more

f. Explanation and comments by the Board on every qualification, reservation, adverse remarks or disclaimer made by Auditor.

g. Particulars of loan, guarantees, or investment under Section 186 as per Companies Act, 2013

CA Vikash Jain

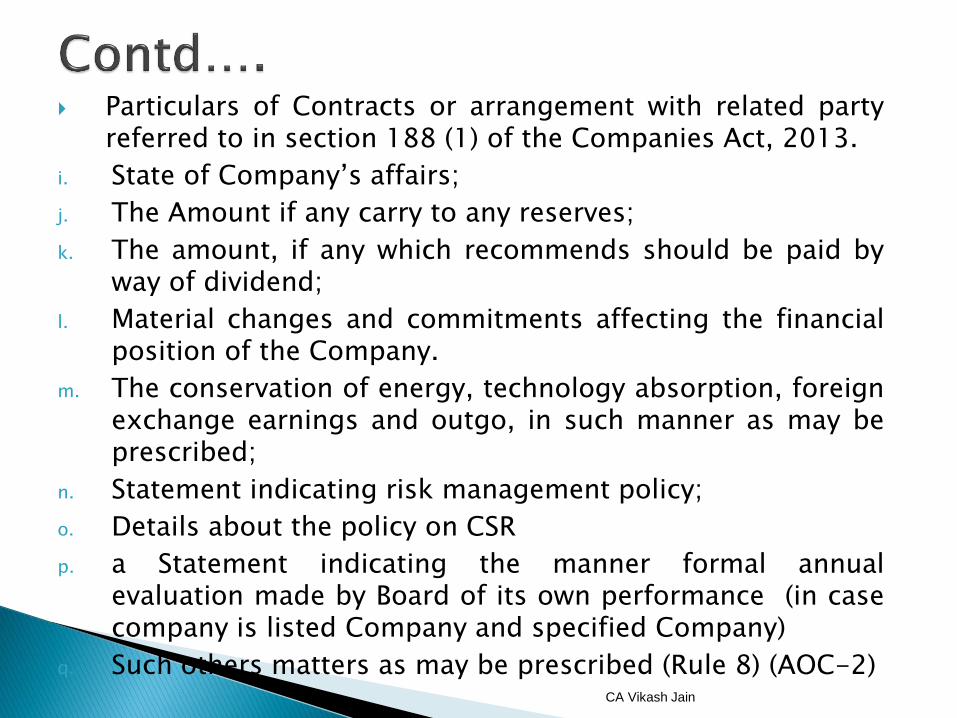

Particulars of Contracts or arrangement with related party referred to in section 188 (1) of the Companies Act, 2013.

i. State of Company’s affairs;

j. The Amount if any carry to any reserves;

k. The amount, if any which recommends should be paid by way of dividend;

l. Material changes and commitments affecting the financial position of the Company.

m. The conservation of energy, technology absorption, foreign exchange earnings and outgo, in such manner as may be prescribed;

n. Statement indicating risk management policy;

o. Details about the policy on CSR

p. a Statement indicating the manner formal annual evaluation made by Board of its own performance (in case company is listed Company and specified Company)

q. Such others matters as may be prescribed (Rule 8) (AOC-2)

CA Vikash Jain

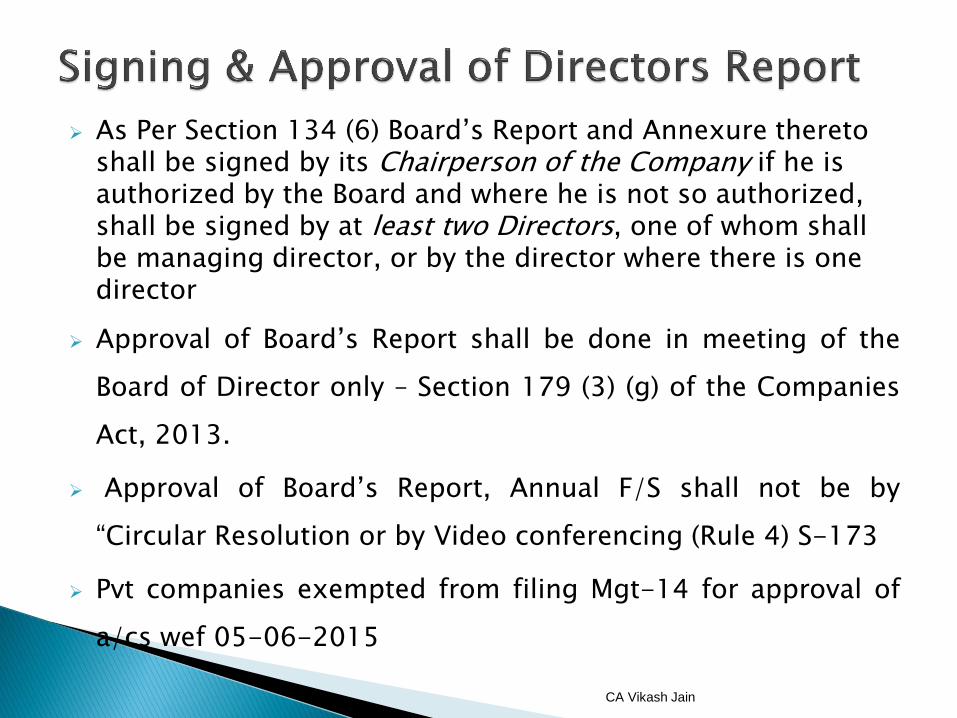

As Per Section 134 (6) Board’s Report and Annexure thereto shall be signed by its Chairperson of the Company if he is authorized by the Board and where he is not so authorized, shall be signed by at least two Directors, one of whom shall be managing director, or by the director where there is one director

Approval of Board’s Report shall be done in meeting of the

Board of Director only – Section 179 (3) (g) of the Companies

Act, 2013.

Approval of Board’s Report, Annual F/S shall not be by

“Circular Resolution or by Video conferencing (Rule 4) S-173

Pvt companies exempted from filing Mgt-14 for approval of

a/cs wef 05-06-2015

CA Vikash Jain

Information and Explanations which to the best of his knowledge and belief for the purpose of his audit.

Proper books of accounts must be as per required by law.

Report on the accounts of any branch office of the Company.

Company’s balance sheet and profit and loss account deal with in the report are in agreement with the books of account and return,

Implementation of financial statement with the accounting standards,

Observations or comments of the auditor on financial transactions or matters,

Any directors is disqualified from being appointed as a director under sub-section (2) of Section 164 (Details later).

CA Vikash Jain

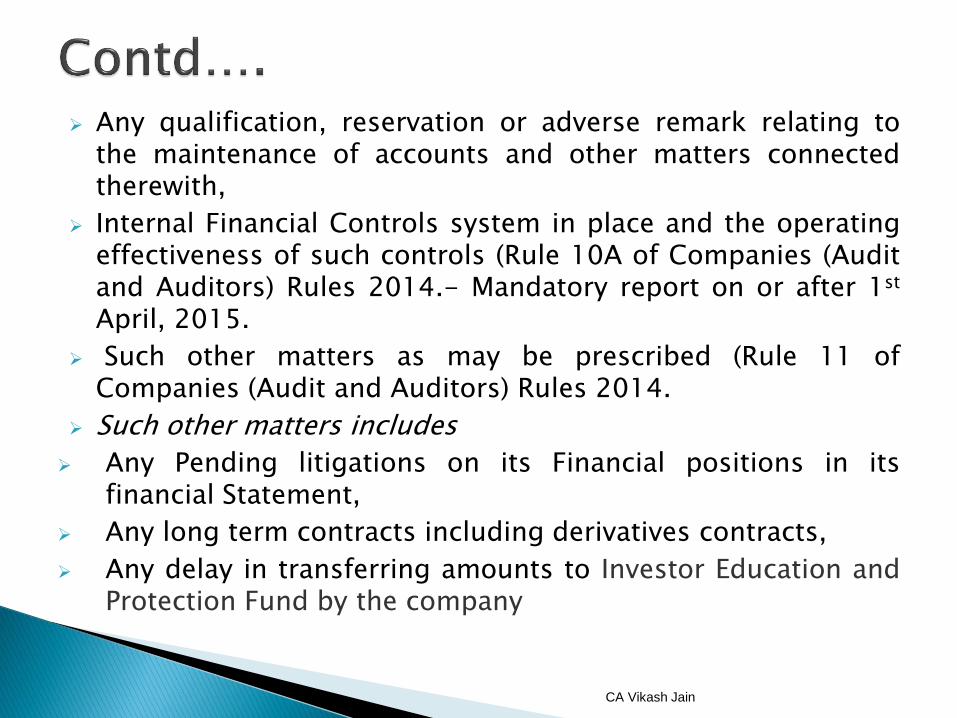

Any qualification, reservation or adverse remark relating to the maintenance of accounts and other matters connected therewith,

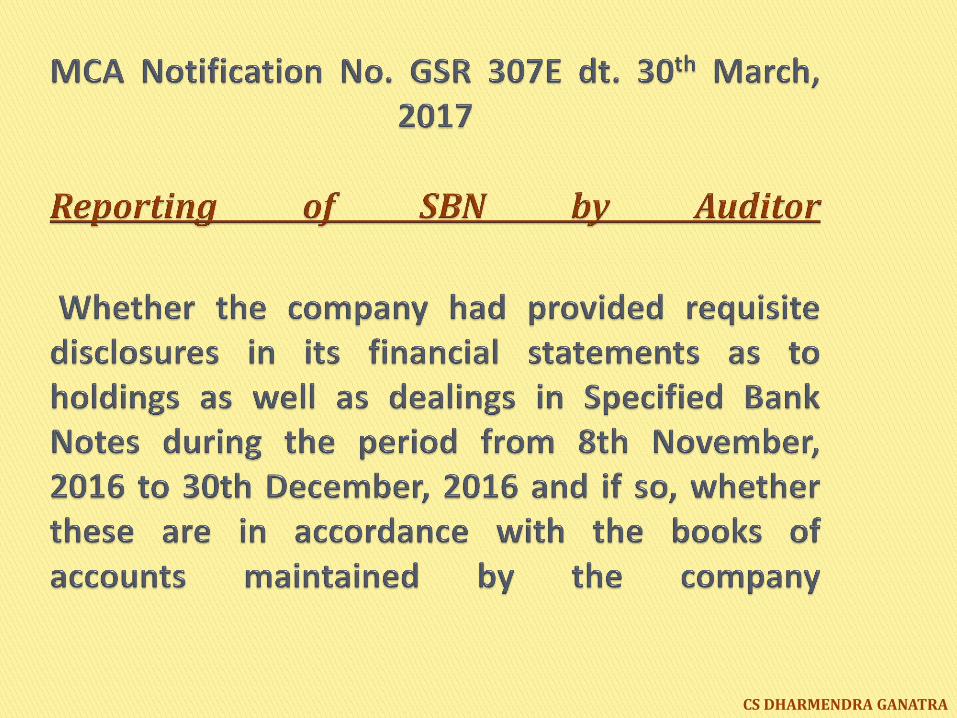

Internal Financial Controls system in place and the operating effectiveness of such controls (Rule 10A of Companies (Audit and Auditors) Rules 2014.- Mandatory report on or after 1st April, 2015.

Such other matters as may be prescribed (Rule 11 of Companies (Audit and Auditors) Rules 2014.

Such other matters includes

Any Pending litigations on its Financial positions in its financial Statement,

Any long term contracts including derivatives contracts,

Any delay in transferring amounts to Investor Education and Protection Fund by the company

CA Vikash Jain

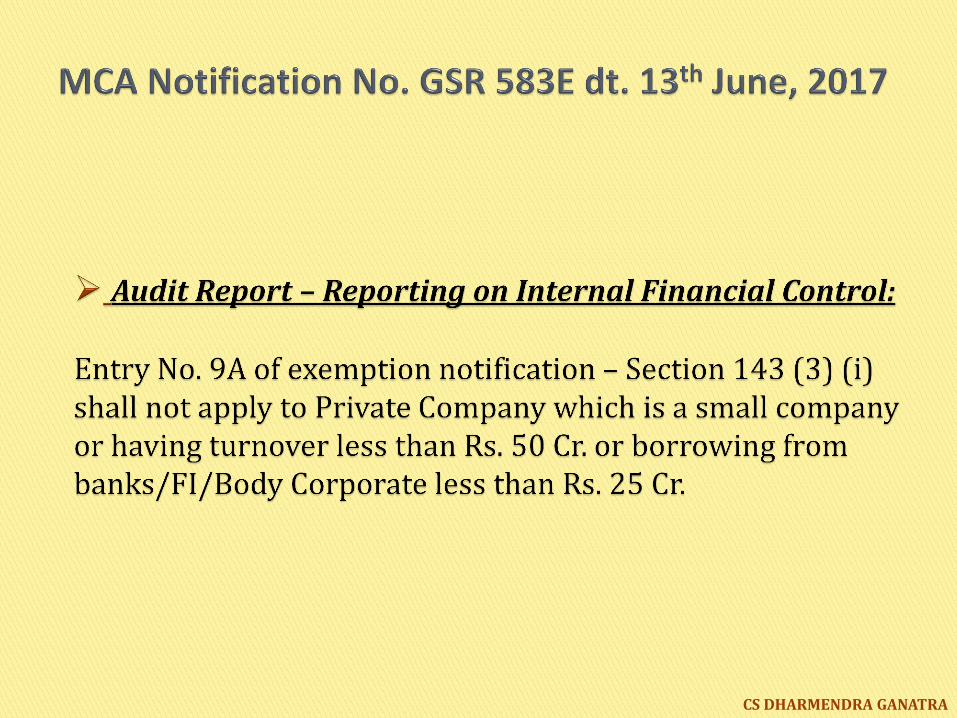

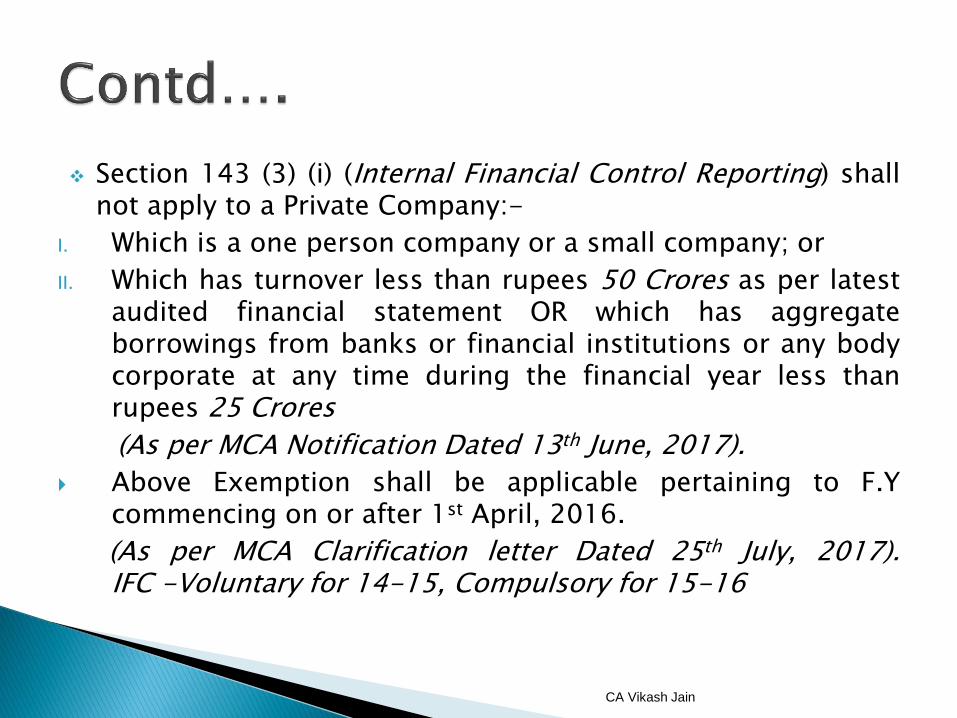

Section 143 (3) (i) (Internal Financial Control Reporting) shall not apply to a Private Company:-

I. Which is a one person company or a small company; or

II. Which has turnover less than rupees 50 Crores as per latest audited financial statement OR which has aggregate borrowings from banks or financial institutions or any body corporate at any time during the financial year less than rupees 25 Crores

(As per MCA Notification Dated 13th June, 2017).

Above Exemption shall be applicable pertaining to F.Y commencing on or after 1st April, 2016.

(As per MCA Clarification letter Dated 25th July, 2017). IFC -Voluntary for 14-15, Compulsory for 15-16

CA Vikash Jain

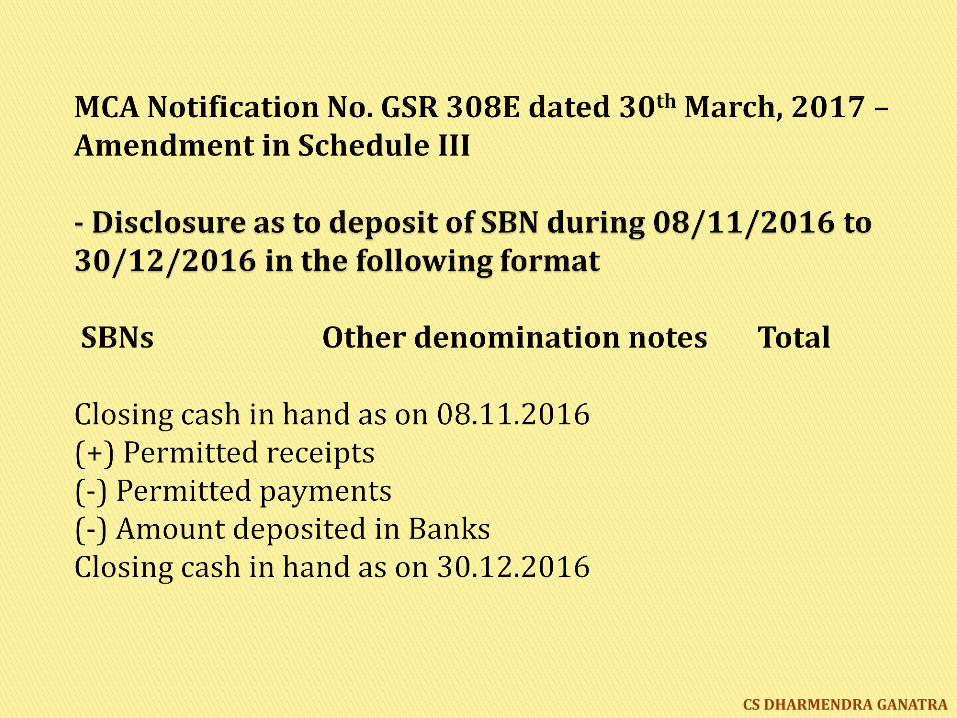

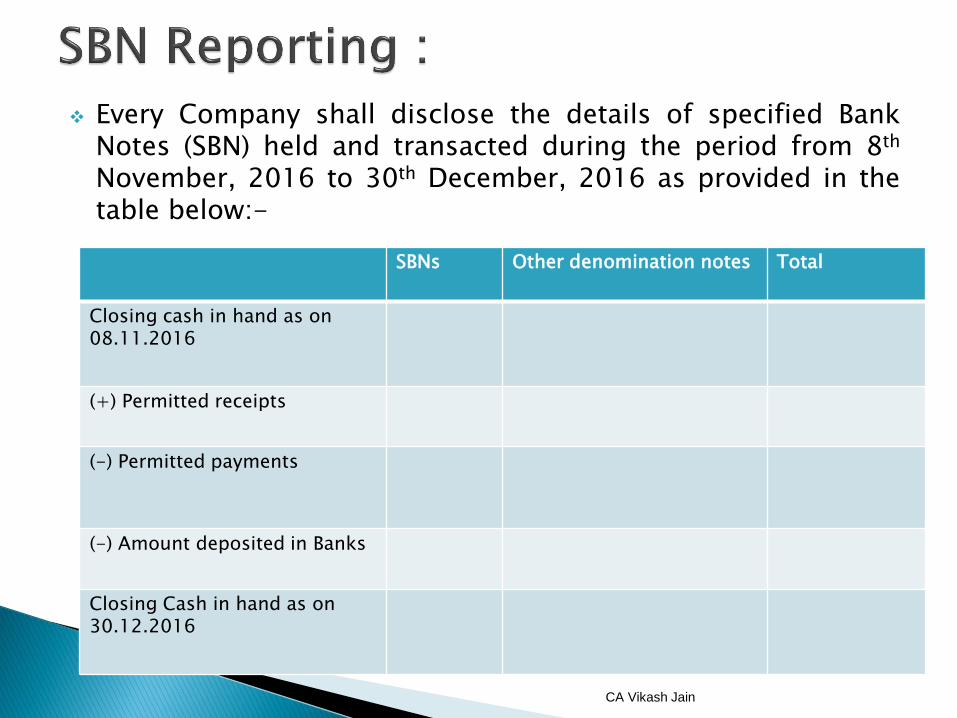

Every Company shall disclose the details of specified Bank Notes (SBN) held and transacted during the period from 8th November, 2016 to 30th December, 2016 as provided in the table below:-

CA Vikash Jain

SBNs Other denomination notes

Total

Closing cash in hand as on 08.11.2016

(+) Permitted receipts

(-) Permitted payments

(-) Amount deposited in Banks

Closing Cash in hand as on 30.12.2016

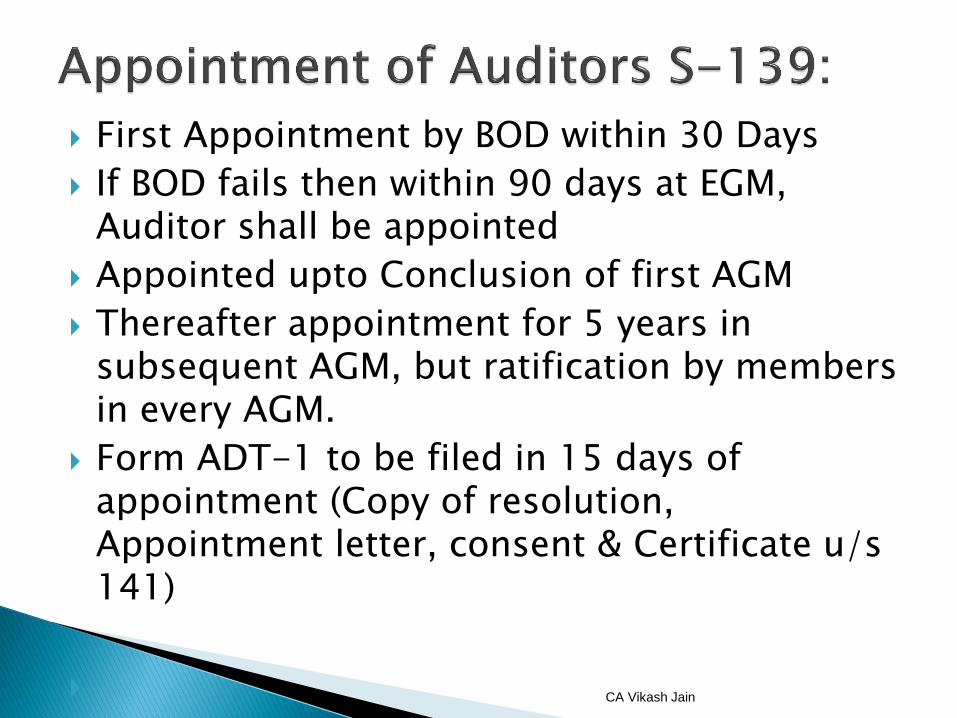

First Appointment by BOD within 30 Days

If BOD fails then within 90 days at EGM, Auditor shall be appointed

Appointed upto Conclusion of first AGM

Thereafter appointment for 5 years in subsequent AGM, but ratification by members in every AGM.

Form ADT-1 to be filed in 15 days of appointment (Copy of resolution, Appointment letter, consent & Certificate u/s 141)

CA Vikash Jain

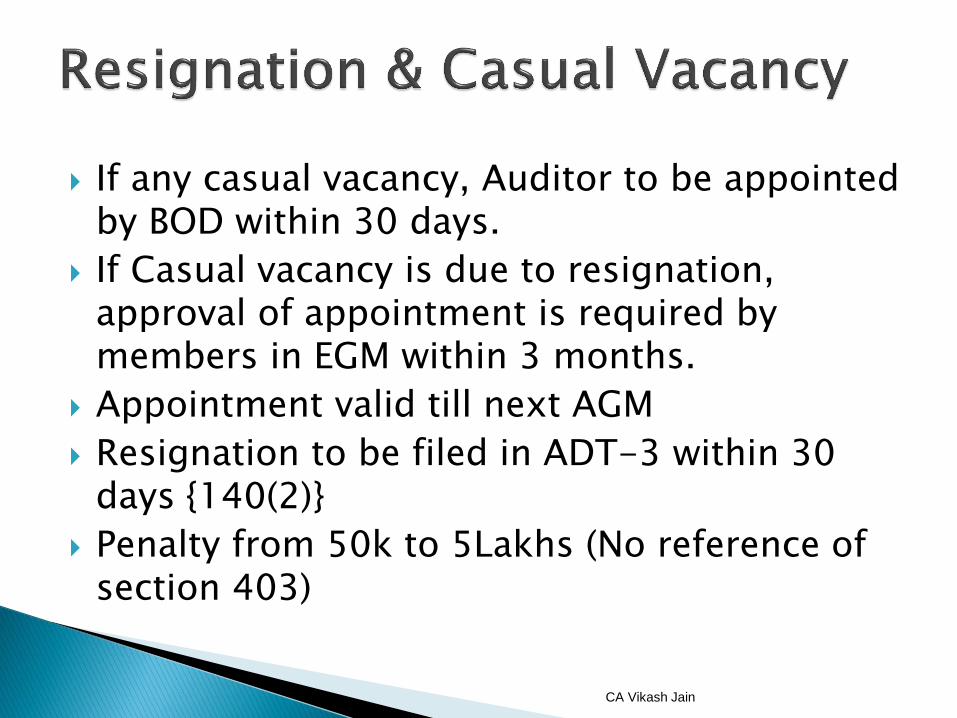

If any casual vacancy, Auditor to be appointed by BOD within 30 days.

If Casual vacancy is due to resignation, approval of appointment is required by members in EGM within 3 months.

Appointment valid till next AGM

Resignation to be filed in ADT-3 within 30 days {140(2)}

Penalty from 50k to 5Lakhs (No reference of section 403)

CA Vikash Jain

MBP-1 in First Board Meeting of FY – Disclosure of Interest by directors (Not to be filed with ROC & for record purpose only. S-184)

FILING OF ADT-1 (Appointment to be compulsorily for 5 years) (15 days of Appointment)

FILING OF MGT-14 (Approval of accounts for Public cos only)

FILING OF AOC-4 (F/S) (30 days of AGM)

FILING OF MGT-7 (A/R) (60 days from AGM)

CA Vikash Jain

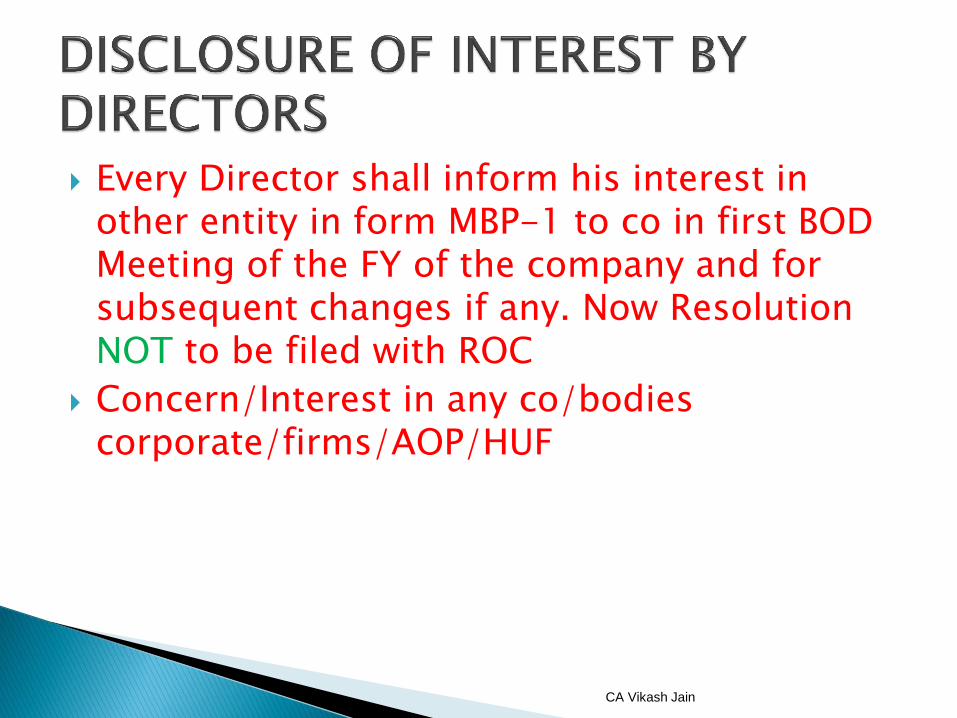

Every Director shall inform his interest in other entity in form MBP-1 to co in first BOD Meeting of the FY of the company and for subsequent changes if any. Now Resolution NOT to be filed with ROC

Concern/Interest in any co/bodies corporate/firms/AOP/HUF

CA Vikash Jain

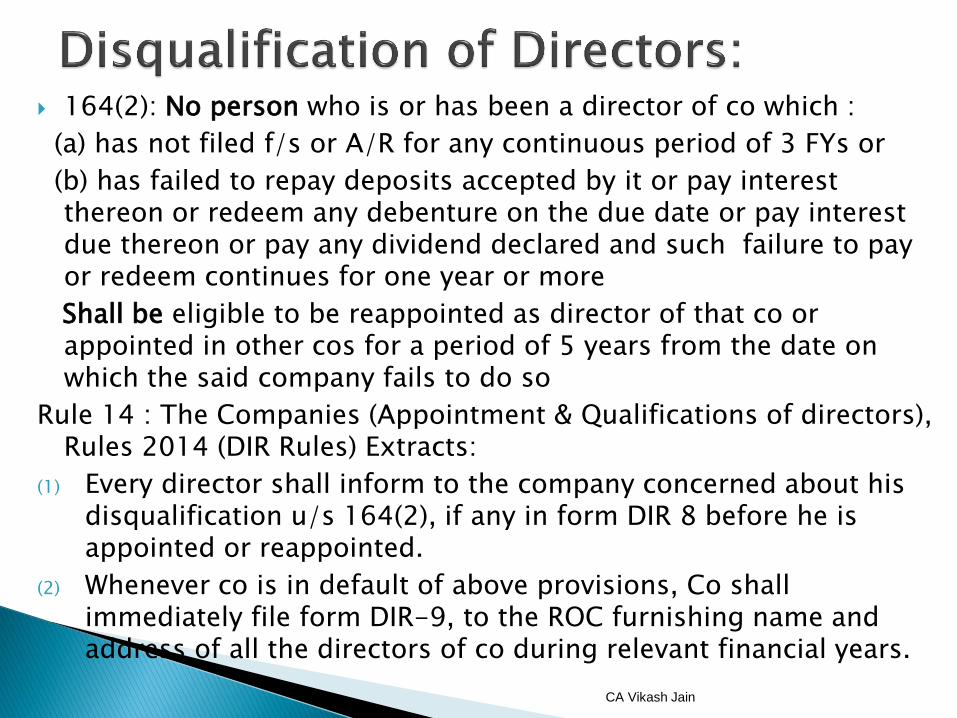

164(2): No person who is or has been a director of co which :

(a) has not filed f/s or A/R for any continuous period of 3 FYs or

(b) has failed to repay deposits accepted by it or pay interest thereon or redeem any debenture on the due date or pay interest due thereon or pay any dividend declared and such failure to pay or redeem continues for one year or more

Shall be eligible to be reappointed as director of that co or appointed in other cos for a period of 5 years from the date on which the said company fails to do so

Rule 14 : The Companies (Appointment & Qualifications of directors), Rules 2014 (DIR Rules) Extracts:

(1) Every director shall inform to the company concerned about his disqualification u/s 164(2), if any in form DIR 8 before he is appointed or reappointed.

(2) Whenever co is in default of above provisions, Co shall immediately file form DIR-9, to the ROC furnishing name and address of all the directors of co during relevant financial years.

CA Vikash Jain

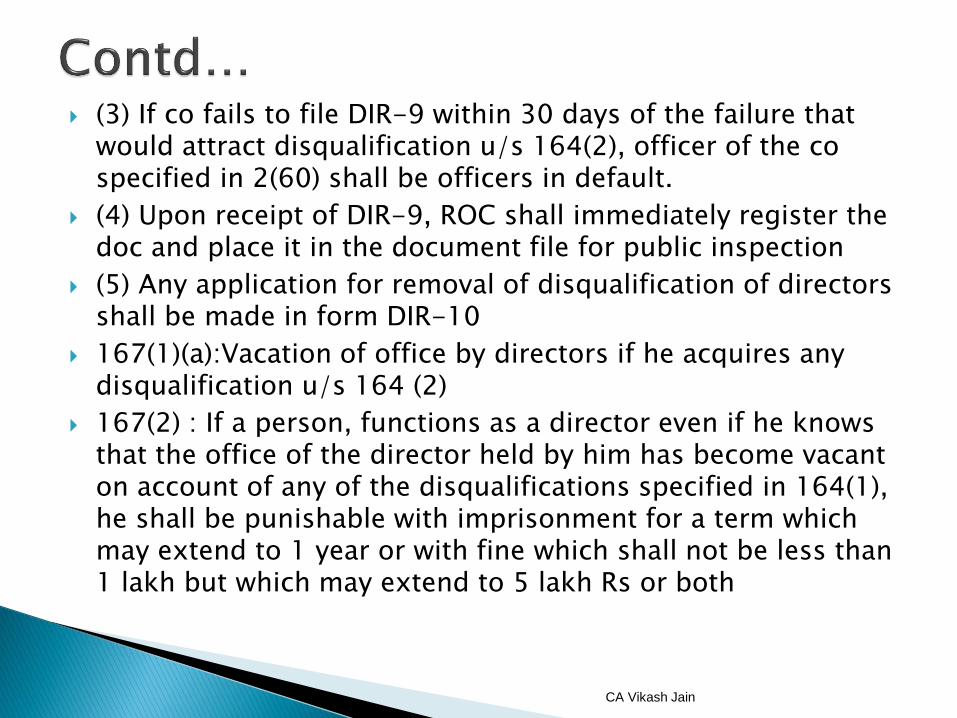

(3) If co fails to file DIR-9 within 30 days of the failure that would attract disqualification u/s 164(2), officer of the co specified in 2(60) shall be officers in default.

(4) Upon receipt of DIR-9, ROC shall immediately register the doc and place it in the document file for public inspection

(5) Any application for removal of disqualification of directors shall be made in form DIR-10

167(1)(a):Vacation of office by directors if he acquires any disqualification u/s 164 (2)

167(2) : If a person, functions as a director even if he knows that the office of the director held by him has become vacant on account of any of the disqualifications specified in 164(1), he shall be punishable with imprisonment for a term which may extend to 1 year or with fine which shall not be less than 1 lakh but which may extend to 5 lakh Rs or both

CA Vikash Jain

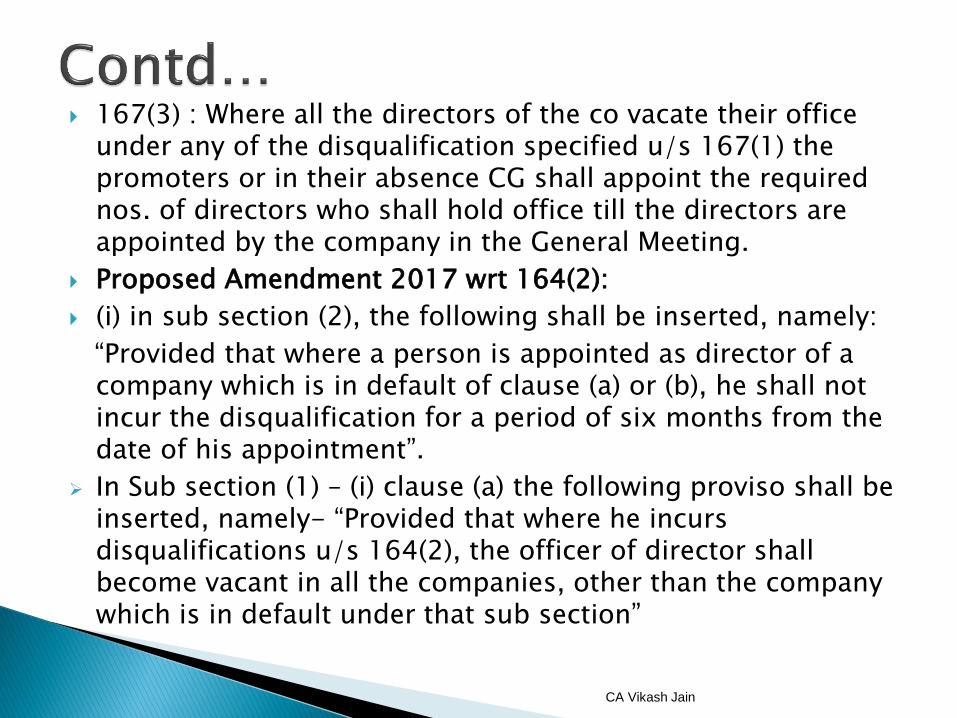

167(3) : Where all the directors of the co vacate their office under any of the disqualification specified u/s 167(1) the promoters or in their absence CG shall appoint the required nos. of directors who shall hold office till the directors are appointed by the company in the General Meeting.

Proposed Amendment 2017 wrt 164(2):

(i) in sub section (2), the following shall be inserted, namely:

“Provided that where a person is appointed as director of a company which is in default of clause (a) or (b), he shall not incur the disqualification for a period of six months from the date of his appointment”.

In Sub section (1) – (i) clause (a) the following proviso shall be inserted, namely- “Provided that where he incurs disqualifications u/s 164(2), the officer of director shall become vacant in all the companies, other than the company which is in default under that sub section”

CA Vikash Jain

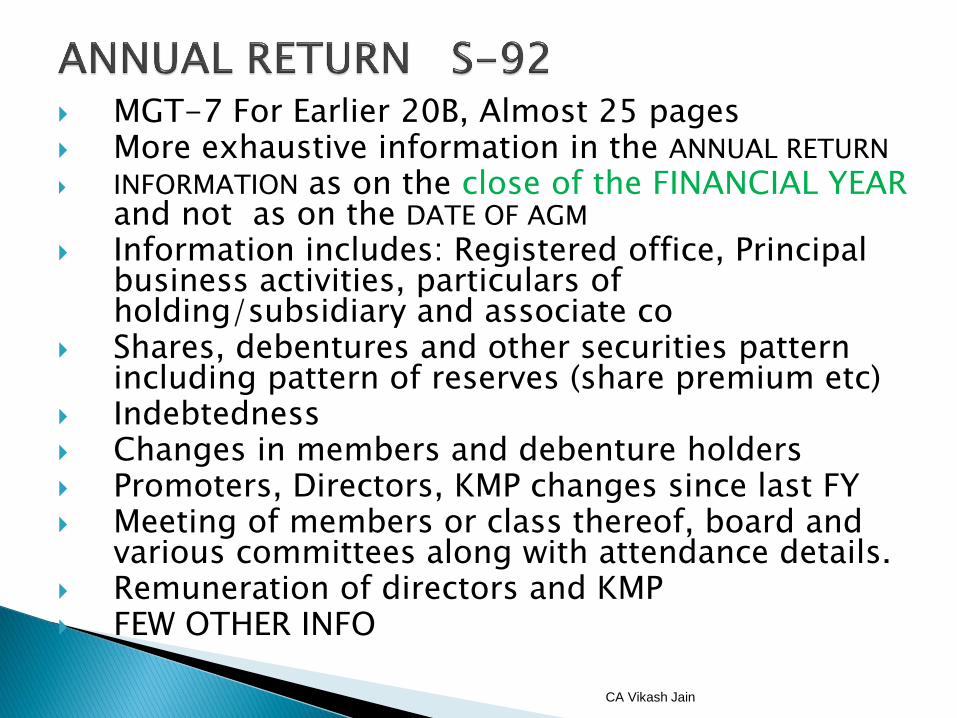

MGT-7 For Earlier 20B, Almost 25 pages More exhaustive information in the ANNUAL RETURN

INFORMATION as on the close of the FINANCIAL YEAR and not as on the DATE OF AGM

Information includes: Registered office, Principal business activities, particulars of holding/subsidiary and associate co

Shares, debentures and other securities pattern including pattern of reserves (share premium etc)

Indebtedness Changes in members and debenture holders Promoters, Directors, KMP changes since last FY Meeting of members or class thereof, board and

various committees along with attendance details. Remuneration of directors and KMP FEW OTHER INFO

CA Vikash Jain

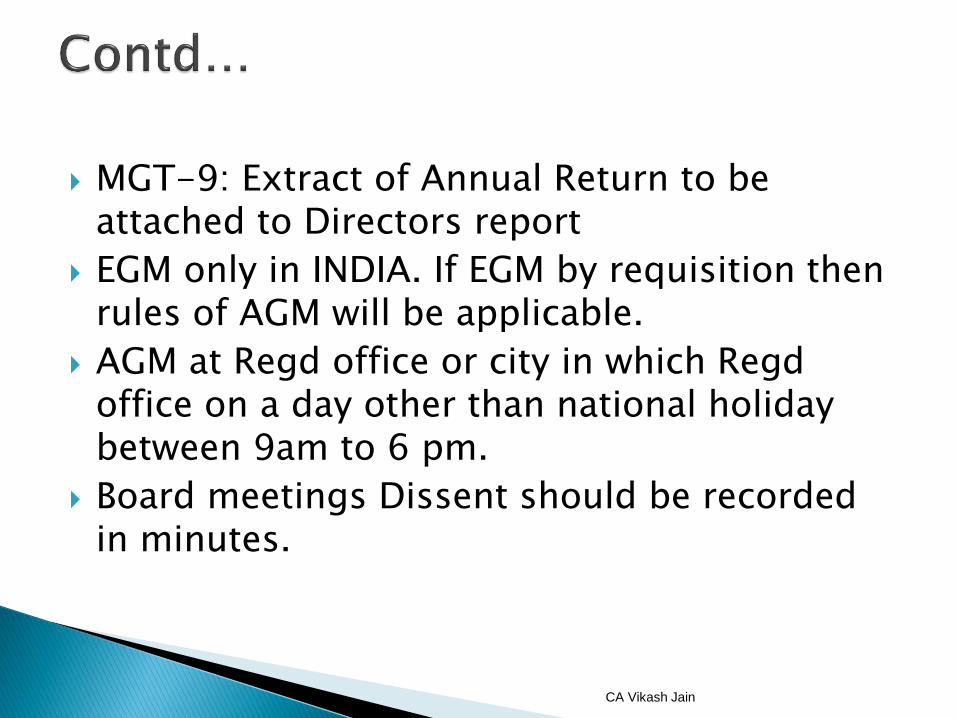

MGT-9: Extract of Annual Return to be attached to Directors report

EGM only in INDIA. If EGM by requisition then rules of AGM will be applicable.

AGM at Regd office or city in which Regd office on a day other than national holiday between 9am to 6 pm.

Board meetings Dissent should be recorded in minutes.

CA Vikash Jain

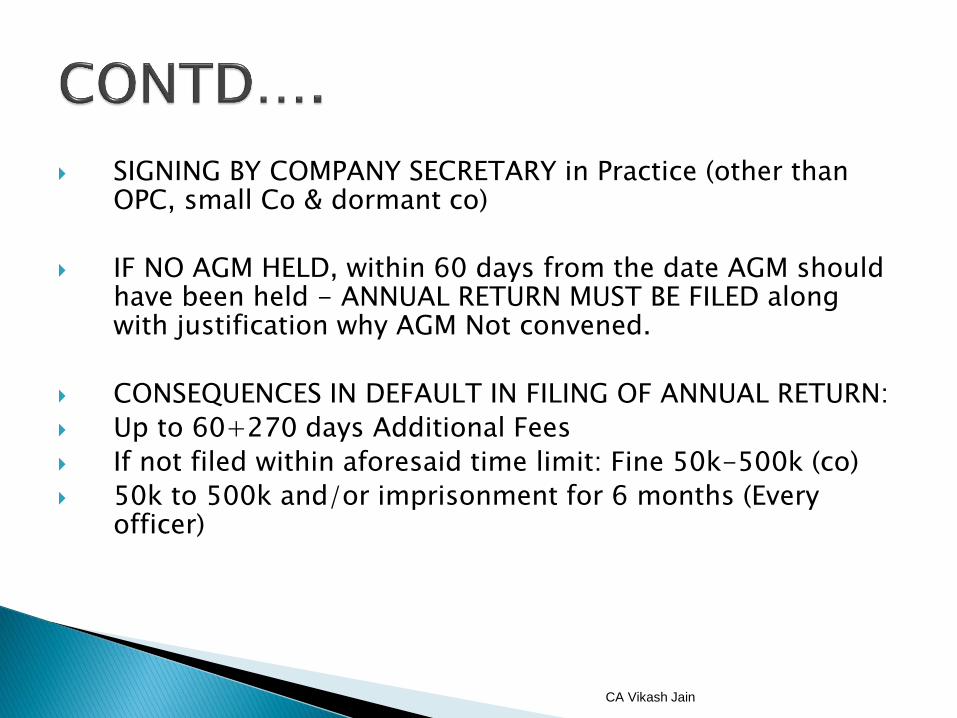

SIGNING BY COMPANY SECRETARY in Practice (other than OPC, small Co & dormant co)

IF NO AGM HELD, within 60 days from the date AGM should have been held - ANNUAL RETURN MUST BE FILED along with justification why AGM Not convened.

CONSEQUENCES IN DEFAULT IN FILING OF ANNUAL RETURN:

Up to 60+270 days Additional Fees

If not filed within aforesaid time limit: Fine 50k-500k (co)

50k to 500k and/or imprisonment for 6 months (Every officer)

CA Vikash Jain

CA Vikash Jain

Presented By:

CA Vikash Jain

B.Com(Hons.), FCA, DISA, IP, Arbitrator

07TH Oct, 2017, Rajkot

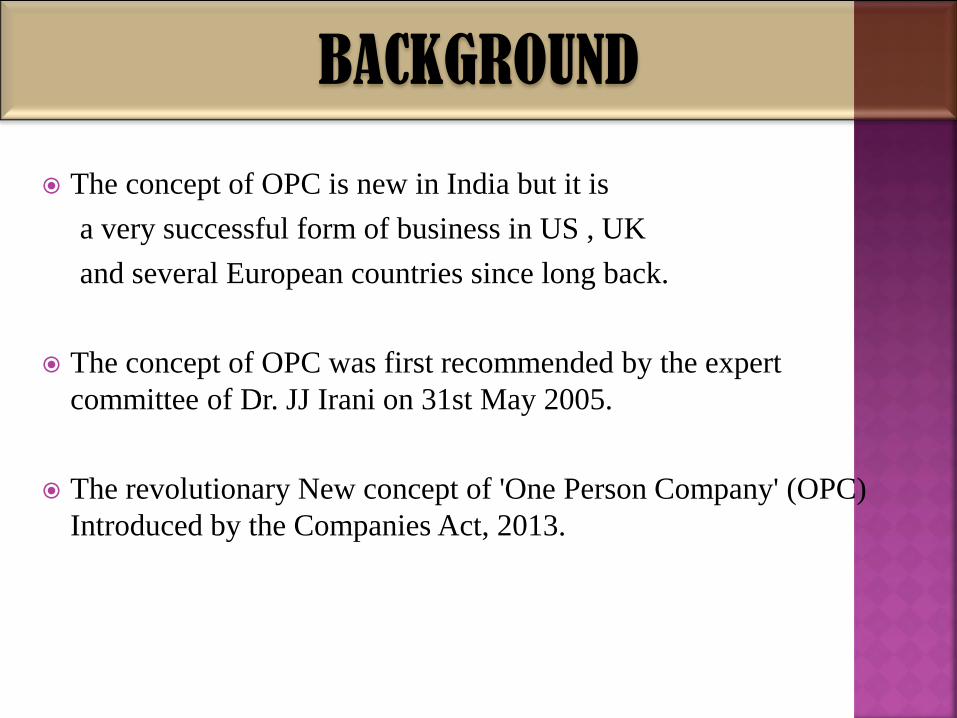

The concept of OPC is new in India but it is

a very successful form of business in US , UK

and several European countries since long back.

The concept of OPC was first recommended by the expert

committee of Dr. JJ Irani on 31st May 2005.

The revolutionary New concept of 'One Person Company' (OPC)

Introduced by the Companies Act, 2013.

BACKGROUND

OPC in India sounds interesting and may serve as new form of doing

business for those who look forward to start their own ventures with a

structure of organized business.

OPC will give the young businessman all benefits of a private limited

company which categorically means they will have access to

credits,

bank loans,

Limited liability,

legal protection for business,

access to market etc all in the name of a separate legal entity.

The OPC can not carry business of Non Banking Financial Investment

activity including investment in security of any body corporate.

INTRODUCTION

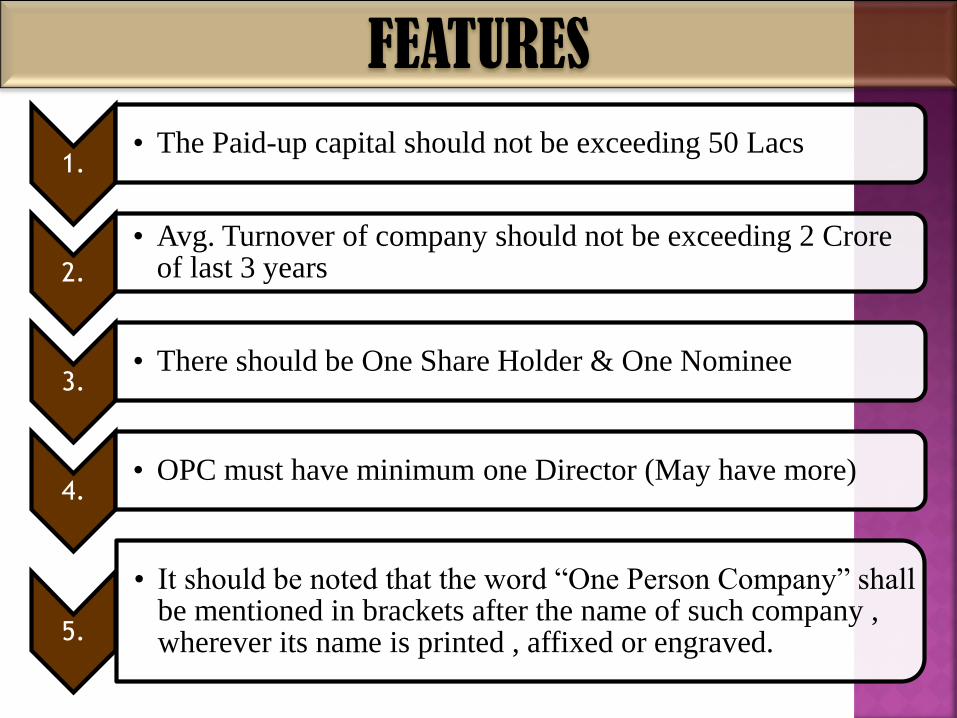

1. • The Paid-up capital should not be exceeding 50 Lacs

2.

• Avg. Turnover of company should not be exceeding 2 Crore of last 3 years

3. • There should be One Share Holder & One Nominee

4. • OPC must have minimum one Director (May have more)

5.

• It should be noted that the word “One Person Company” shall be mentioned in brackets after the name of such company , wherever its name is printed , affixed or engraved.

FEATURES

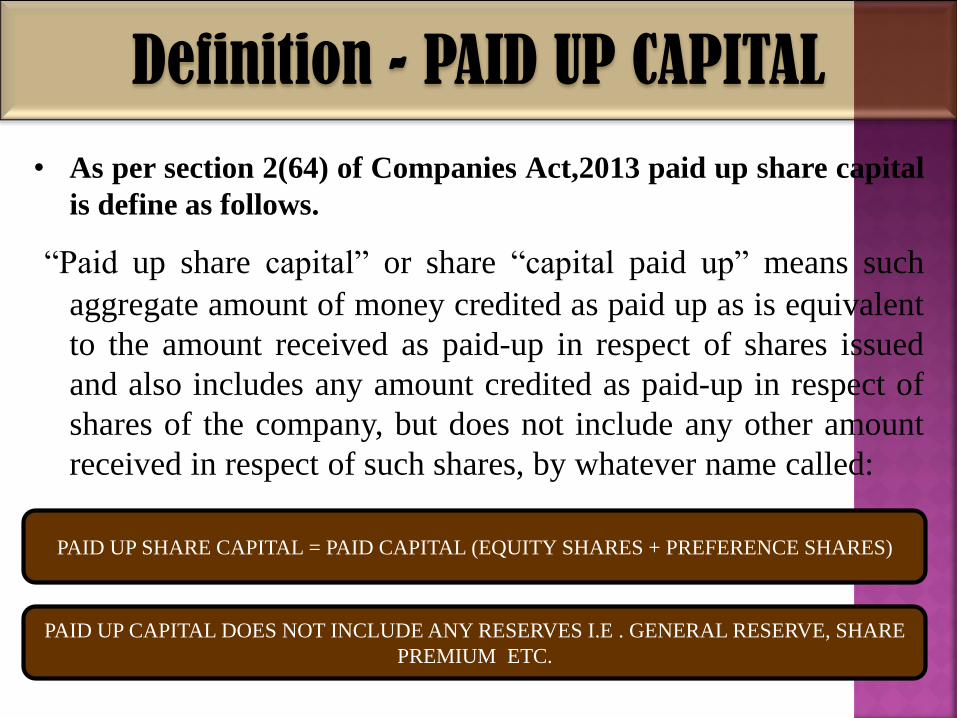

• As per section 2(64) of Companies Act,2013 paid up share capital

is define as follows.

“Paid up share capital” or share “capital paid up” means such

aggregate amount of money credited as paid up as is equivalent

to the amount received as paid-up in respect of shares issued

and also includes any amount credited as paid-up in respect of

shares of the company, but does not include any other amount

received in respect of such shares, by whatever name called:

PAID UP SHARE CAPITAL = PAID CAPITAL (EQUITY SHARES + PREFERENCE SHARES)

Definition - PAID UP CAPITAL

PAID UP CAPITAL DOES NOT INCLUDE ANY RESERVES I.E . GENERAL RESERVE, SHARE

PREMIUM ETC.

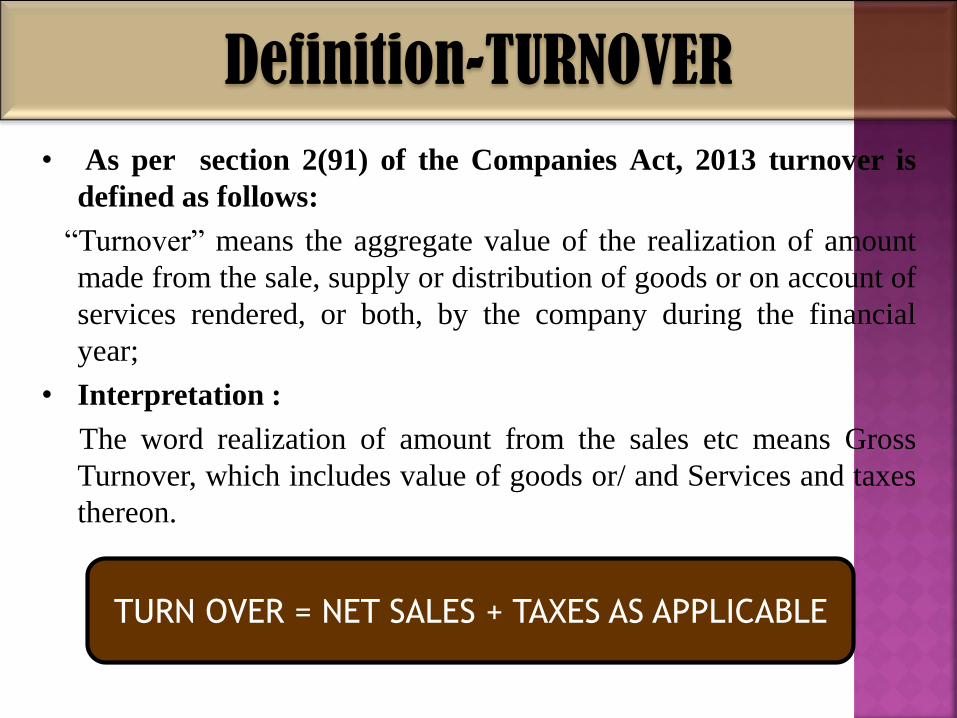

• As per section 2(91) of the Companies Act, 2013 turnover is

defined as follows:

“Turnover” means the aggregate value of the realization of amount

made from the sale, supply or distribution of goods or on account of

services rendered, or both, by the company during the financial

year;

• Interpretation :

The word realization of amount from the sales etc means Gross

Turnover, which includes value of goods or/ and Services and taxes

thereon.

TURN OVER = NET SALES + TAXES AS APPLICABLE

Definition-TURNOVER

ONE SHARE HOLDER

ONE DIRECTOR (May have more)

NOMINEE

CONCEPT

Only a natural person who is a resident of India and also a citizen of India can form a one person company

No minor shall become member or nominee of the One Person Company or can hold share with beneficial interest .

It means that other legal entities like companies or societies or other corporate entities cannot form a one person company.

It also means that Non resident Indians or Foreign citizens can not form a One person company.

It simply means an individual cannot have two different one person companies in his name.

ONE SHAREHOLDER

One Person Company may have minimum only one

director.

However, as per the Act, the total number of directors

shall not be more than 15.

As per the Companies Act, if nothing is mentioned in

the incorporation document, it would be assumed the

sole shareholder shall also be the sole director in the

one person company and which shall be practically the

case in most One Person Companies incorporated.

ONE DIRECTOR

The One Person Company has to nominate a Nominee with his

written consent who, in the event of death or inability to contract of

the owner of the One Person Company, shall come forward and

take over the reins of the one person company.

Requirements of being a resident Indian and citizen of India also

apply to the nominee.

Further if the person so nominated becomes the member of such a

One Person Company and is already a member of another One

Person Company, at the same time, by virtue of rules has to decide

within 6 months which one person company he has to continue.

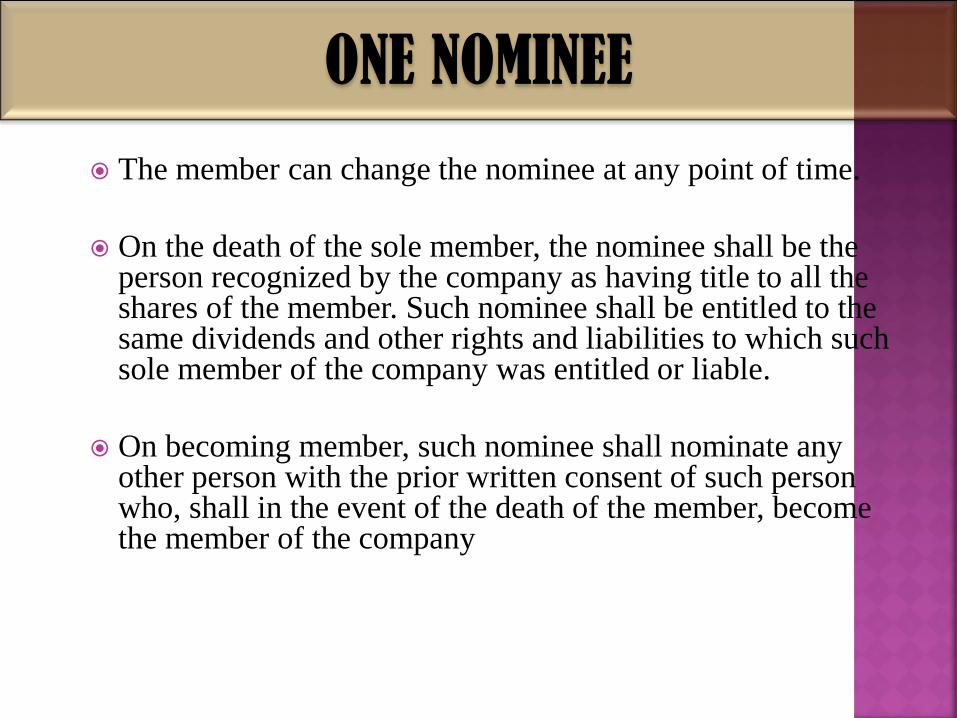

ONE NOMINEE

The member can change the nominee at any point of time.

On the death of the sole member, the nominee shall be the person recognized by the company as having title to all the shares of the member. Such nominee shall be entitled to the same dividends and other rights and liabilities to which such sole member of the company was entitled or liable.

On becoming member, such nominee shall nominate any other person with the prior written consent of such person who, shall in the event of the death of the member, become the member of the company

ONE NOMINEE

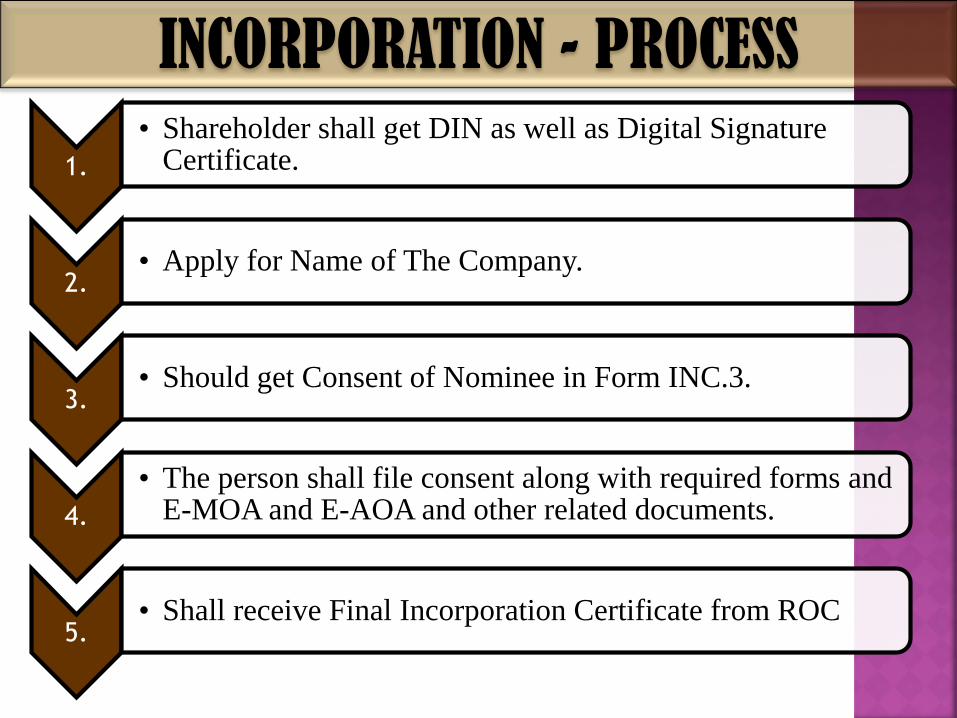

1.

• Shareholder shall get DIN as well as Digital Signature Certificate.

2. • Apply for Name of The Company.

3. • Should get Consent of Nominee in Form INC.3.

4.

• The person shall file consent along with required forms and E-MOA and E-AOA and other related documents.

5. • Shall receive Final Incorporation Certificate from ROC

INCORPORATION - PROCESS

Sr No. Nature of Forms Form No. Due Date of Filing

1. Application for reservation of

Name

INC.1 Not Applicable

2. Application for Incorporation INC.2 60 Days

3. Nominee- Consent Form INC.3 15 Days

4. Change in Member/ Nominee INC.4 30 Days

5. Intimation of Exceeding

Threshold i.e. Ceased to be

OPC

INC.5 60 Days

6. OPC – Application for

Conversion

INC.6 Not Applicable

7. Filing of Special Resolution MGT. 14 30 Days

DUE DATE OF FILING DOCUMENTS

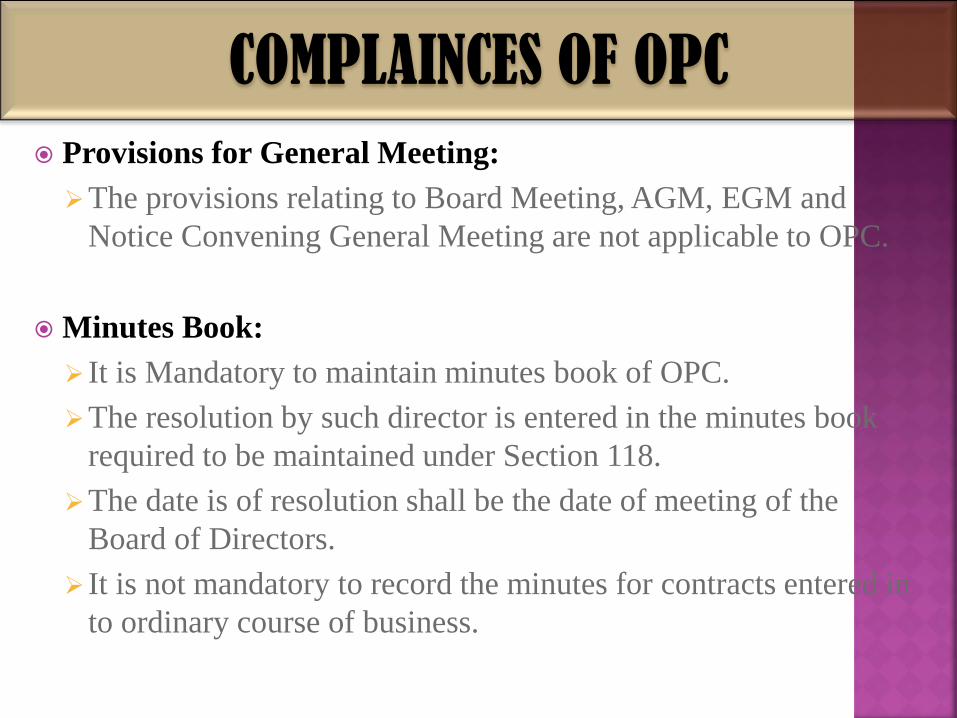

Provisions for General Meeting:

The provisions relating to Board Meeting, AGM, EGM and

Notice Convening General Meeting are not applicable to OPC.

Minutes Book:

It is Mandatory to maintain minutes book of OPC.

The resolution by such director is entered in the minutes book

required to be maintained under Section 118.

The date is of resolution shall be the date of meeting of the

Board of Directors.

It is not mandatory to record the minutes for contracts entered in

to ordinary course of business.

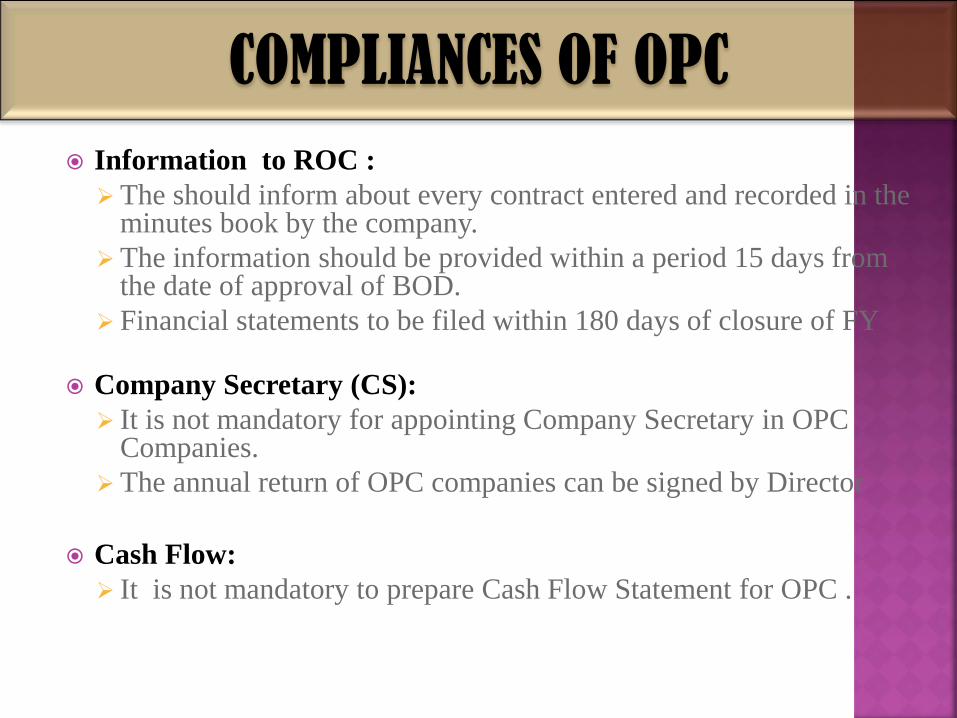

COMPLAINCES OF OPC

Information to ROC :

The should inform about every contract entered and recorded in the minutes book by the company.

The information should be provided within a period 15 days from the date of approval of BOD.

Financial statements to be filed within 180 days of closure of FY

Company Secretary (CS):

It is not mandatory for appointing Company Secretary in OPC Companies.

The annual return of OPC companies can be signed by Director

Cash Flow:

It is not mandatory to prepare Cash Flow Statement for OPC .

COMPLIANCES OF OPC

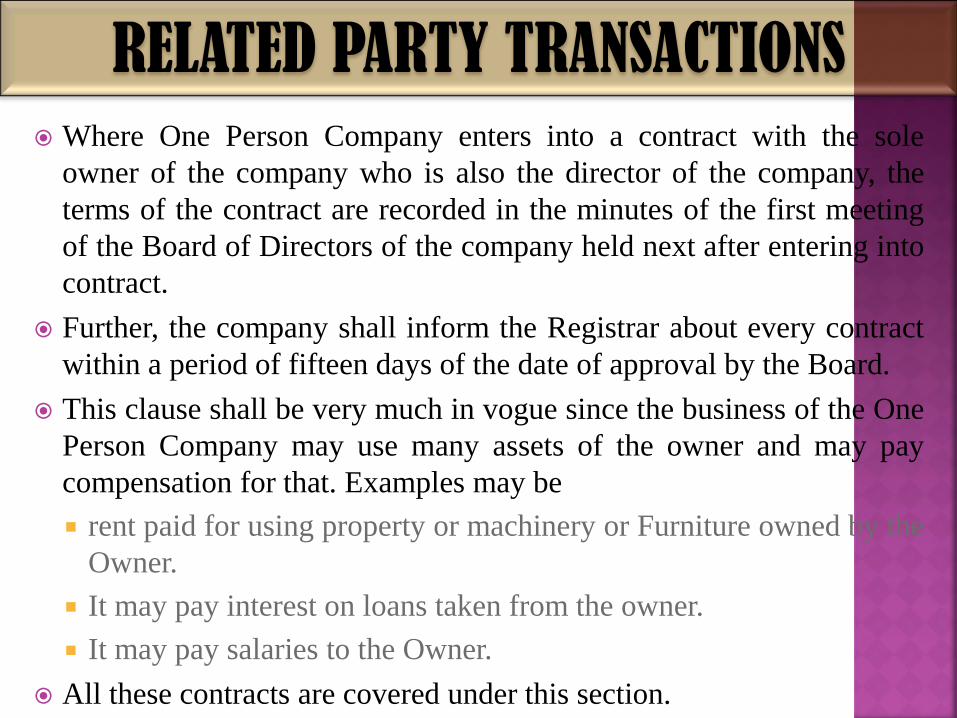

Where One Person Company enters into a contract with the sole

owner of the company who is also the director of the company, the

terms of the contract are recorded in the minutes of the first meeting

of the Board of Directors of the company held next after entering into

contract.

Further, the company shall inform the Registrar about every contract

within a period of fifteen days of the date of approval by the Board.

This clause shall be very much in vogue since the business of the One

Person Company may use many assets of the owner and may pay

compensation for that. Examples may be

rent paid for using property or machinery or Furniture owned by the

Owner.

It may pay interest on loans taken from the owner.

It may pay salaries to the Owner.

All these contracts are covered under this section.

RELATED PARTY TRANSACTIONS

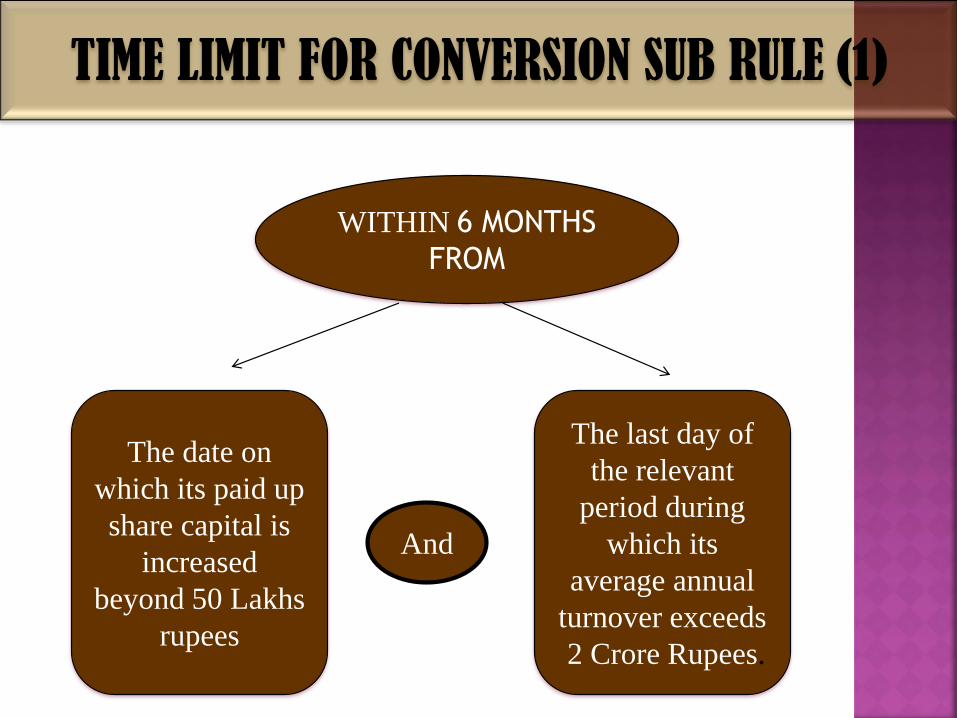

Where the paid up share capital of an OPC exceeds Rs 50 Lacs

And

Average annual turnover during the relevant period exceeds

2 Crore rupees, it shall cease to be entitled to continue as a OPC

(Relevant period means immediately preceding 3 Consecutive

Financial years )

CONDITIONS

WITHIN 6 MONTHS

FROM

The date on

which its paid up

share capital is

increased

beyond 50 Lakhs

rupees

The last day of

the relevant

period during

which its

average annual

turnover exceeds

2 Crore Rupees.

And

TIME LIMIT FOR CONVERSION SUB RULE (1)

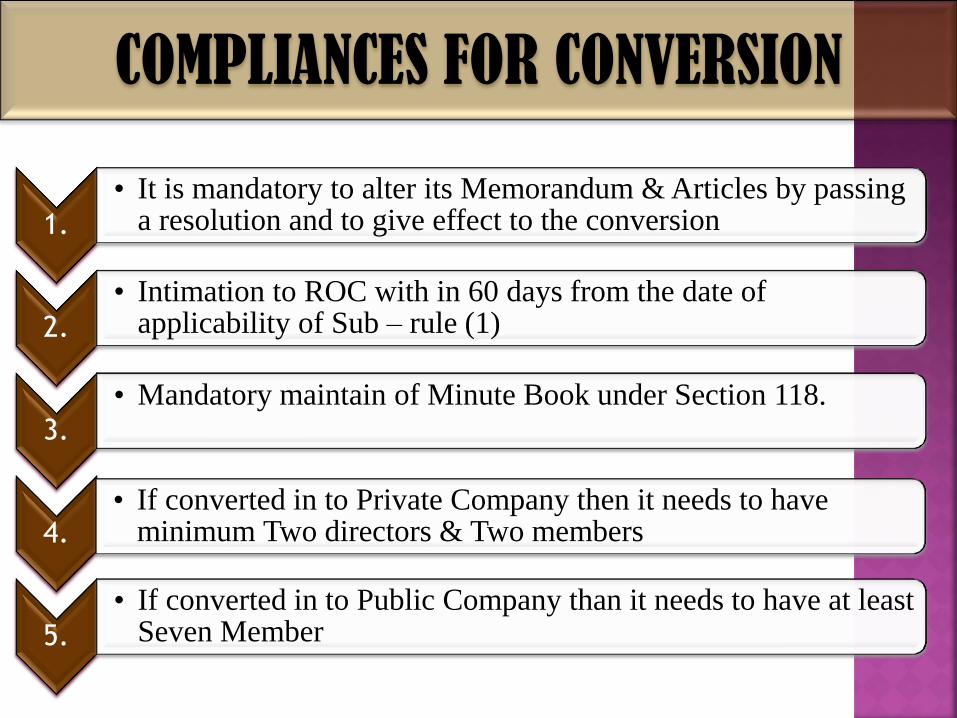

1.

• It is mandatory to alter its Memorandum & Articles by passing a resolution and to give effect to the conversion

2.

• Intimation to ROC with in 60 days from the date of applicability of Sub – rule (1)

3.

• Mandatory maintain of Minute Book under Section 118.

4. • If converted in to Private Company then it needs to have

minimum Two directors & Two members

5.

• If converted in to Public Company than it needs to have at least Seven Member

COMPLIANCES FOR CONVERSION

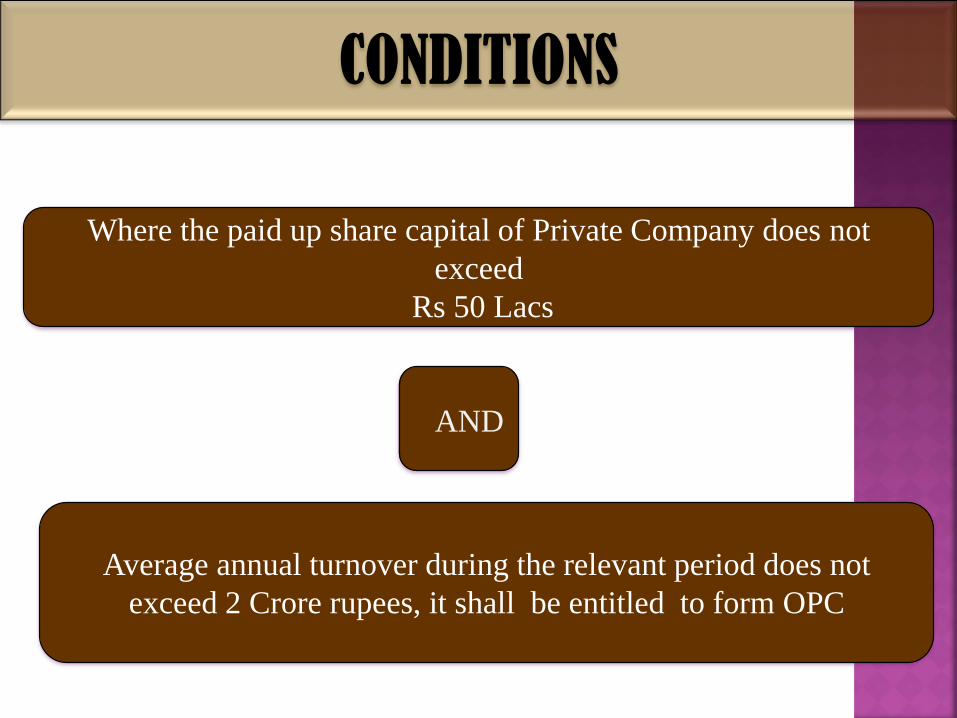

Where the paid up share capital of Private Company does not

exceed

Rs 50 Lacs

AND

Average annual turnover during the relevant period does not

exceed 2 Crore rupees, it shall be entitled to form OPC

CONDITIONS

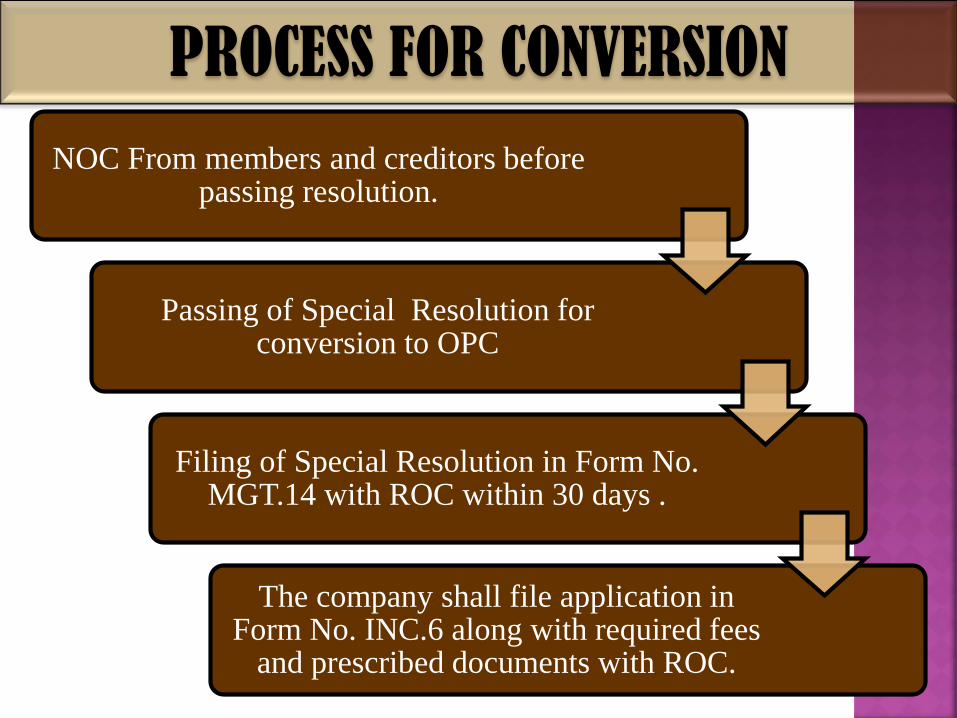

NOC From members and creditors before passing resolution.

Passing of Special Resolution for conversion to OPC

Filing of Special Resolution in Form No. MGT.14 with ROC within 30 days .

The company shall file application in Form No. INC.6 along with required fees

and prescribed documents with ROC.

PROCESS FOR CONVERSION

Declaration by Directors by way of affidavit.

The list of members and creditors.

The latest audited balance sheet and profit and loss

account.

The copy of No Objection Letter of Secured Creditors.

DOCUMENTS TO BE FILED

Limited liability Protection to Directors and Shareholder.

Legal Status and Social Recognition for business.

Complete control of company with the single owner.

Help for testing of business model and enable funding.

Easy to get Loan from bank.

Tax Flexibility and savings .

Easy to manage and Freedom of Compliances.

ADVANTAGES OF OPC

Mitigating Capital Gains

Key Man insurance policy

Mitigating Stamp Duty .

Goods & Services Tax

OPC – A TOOL FOR PLANNING

A One Person Company Purchased One Capital Asset

(meant for sale may be after 1 Year).

As per capital gains the Capital Asset is termed as Long Term

if it is held for 3 years or 36 months (Sec.2 (42A)of I T Act.)

But for Shares to classify as Long Term it is to be held for

12 months (Proviso to Sec 2(42A) of I T Act).

MITIGATING CAPITAL GAINS

So to transfer asset from one person to another, one can

transfer shares of OPC to that person after 12 months to

classify as Long Term.

As per Income Tax Act an Individual can claim deduction for

Insurance Premium in computation of Total Income under

Section 80C up to Rs.1 Lakh Only.

A company whereas can claim deduction for insurance

premium paid for Key man Insurance beyond 1 Lakh

(Actual Amount spent) under section 37 of the Income Tax

Act .

So if a Sole Proprietor converts in to OPC it can avail the

benefit of Higher Insurance premium paid by him.

However the maturity/ Claim benefit of Section 10(10D) will

not be available.

KEY MAN INSURANCE POLICY

An Individual has to pay Stamp duty on transfer of Capital

Asset.

But if , Property proposed to be transfer by form One

person company then Shareholder can transfer the shares of

OPC instead of Transfer of Capital Asset.

STAMP DUTY (State Subject)

On transfer of shares there is lower Stamp Duty applicable

and hence we can mitigate payment of Stamp Duty.

For payment of GST threshold limit is Rs.20 Lakhs for per

Individual or Entity.

Person can Split its income /business (if possible) between

Individual & OPC

GOODS & SERVICES TAX

Thus, The basic slab may be enhance to (20+20) 40 Lacs