Embed Size (px)

Citation preview

Results of the SYRTO Project

SYstemic Risk TOmography:

Signals, Measurements, Transmission Channels, and Policy Interventions

Roberto Savona - Primary Coordinator of the SYRTO Project University of Brescia

Final SYRTO Conference - Université Paris1 Panthéon-Sorbonne February 19, 2016

Συρτό

Seven Women Dancing

Archaeological Museum of Olympia

0

5,000

10,000

15,000

20,000

25,000

30,000

I II III IV I II III IV I II III IV I II III IV I II III IV I II III

2008 2009 2010 2011 2012 2013

Greek Sovereign CDS 5 yrs

0

5,000

10,000

15,000

20,000

25,000

30,000

I II III IV I II III IV I II III IV I II III IV I II III IV I II III

2008 2009 2010 2011 2012 2013

Greek Sovereign CDS 5 yrs-300

-250

-200

-150

-100

-50

0

50

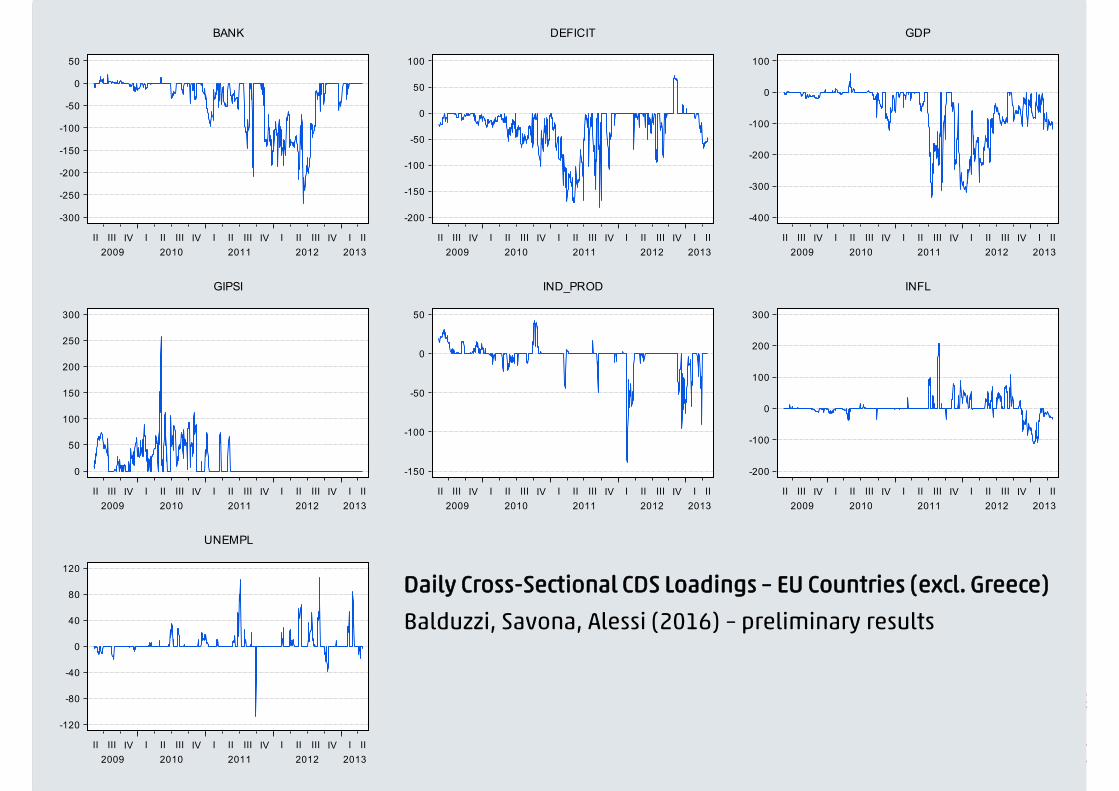

II III IV I II III IV I II III IV I II III IV I II2009 2010 2011 2012 2013

BANK

-200

-150

-100

-50

0

50

100

II III IV I II III IV I II III IV I II III IV I II2009 2010 2011 2012 2013

DEFICIT

-400

-300

-200

-100

0

100

II III IV I II III IV I II III IV I II III IV I II2009 2010 2011 2012 2013

GDP

0

50

100

150

200

250

300

II III IV I II III IV I II III IV I II III IV I II2009 2010 2011 2012 2013

GIPSI

-150

-100

-50

0

50

II III IV I II III IV I II III IV I II III IV I II2009 2010 2011 2012 2013

IND_PROD

-200

-100

0

100

200

300

II III IV I II III IV I II III IV I II III IV I II2009 2010 2011 2012 2013

INFL

-120

-80

-40

0

40

80

120

II III IV I II III IV I II III IV I II III IV I II2009 2010 2011 2012 2013

UNEMPL

Daily Cross-Sectional CDS Loadings – EU Countries (excl. Greece)

Balduzzi, Savona, Alessi (2016) – preliminary results

Results of the SYRTO Project

Paris, 19 February 2016

Roberto Savona Primary and Scientific Coordinator of the SYRTO Project

Department of Economics and ManagementUniversity of Brescia

SYRTO Kick-Out Meeting & First LabEx ReFi Conference on Systemic Risk

Agenda

� Structure, Objectives & Main Deliverables� Research activity� WPs 2-6� WP 7 – EWS� WP 8 – SYRTO Code

Structure, Objectives &

Main Deliverables

SYRTO – SYstemic Risk TOmography

� Funded by the European Union under the 7th Framework Programme. Budget: 2.47 mln €.

� Structure: � Consortium

1. University of Brescia (Italy) – UNIT LEADER2. CNRS & Paris I Sorbonne (France)3. Athens University of Economics and Business – RC (Greece)4. University Cà Foscari Venice (Italy)5. University of Amsterdam Stichting VU-VUMC (Netherlands)

� Advisory BoardI. Scientific DivisionII. Policy Division

ConsortiumOur team (40 full-time researchers)

I. UNIVERSITY OF BRESCIA• Roberto Savona

(Primary and Scientific Coordinator) • Maurizio Carpita• Chiara Carini• Marica Manisera• Marco Sandri• Marika Vezzoli• Flaminio Squazzoni• Paola Zuccolotto• Enrico Ciavolino (University of Salento)• Silvia Figini (University of Pavia)II. CENTRE NATIONAL DE LA RECHERCHE SCIENTIFIQUE• Philippe de Peretti• Jorgen Vitting-Andersen • Peter Addo• Hayette Gatfaoui• Dominique Guégan• Rania Kaffel• Lorenzo Frattarolo• Liu YifangIII. ATHENS UNIVERSITY OF ECONOMICS AND BUSINESS – RC• Petros Dellaportas• Efstathia Agelonidi• Anastasios Plataniotis• Ioannis Vrontos

IV. UNIVERSITY CA’ FOSCARI VENICE• Monica Billio

(Scientific Coordinator)• Loriana Pelizzon• Diana Barro• Roberto Casarin• Michele Costola• Fulvio Corsi• Gloria Gardenal• Martina Nardon• Marcella Lucchetta• Antonio Paradiso• Domenico Sartore• Massimiliano Caporin (University of Padova)V. UNIVERSITY OF AMSTERDAM STICHTING VU-VUMC• Andre Lucas• Arjen Siegman• Siem Jan Koopman• Francisco Blasques• Julia Schaumburg• Dirk Schoenmaker

Advisory BoardI. SCIENTIFIC DIVISION (21 MEMBERS)A. RESEARCH UNIT (6 MEMBERS)A.1. Researchers working with the University of Brescia• Pierluigi Balduzzi (Boston College) • Paolo Manasse (University of Bologna and IGIER Bocconi)A.2. Researchers working with University Cà Foscari Venice• Lorenzo Forni (University of Padua) • Mila Getmansky Sherman (UMass Amherst) • Andrew W. Lo (MIT Sloan)• Roger Stein (MIT Sloan)

B. SUPERVISORY UNIT (15 MEMBERS)• Viral V. Acharya (NYU Stern)• Yacine Aït-Sahalia (Princeton University)• Herman K. Van Dijk (VU University Amsterdam)• John Doukas (Old Dominion University)• Darrell Duffie (Stanford University)• Mardi Dungey (University of Tasmania and University of Cambridge)• Paul Embrechts (ETH Zurich)• Robert Engle (NYU Stern)• Rajna Gibson Brandon (University of Geneva)• Christian Gourieroux (University of Toronto and CREST)• David Lando (Copenhagen Business School)• Norman S. Matloff (UC Davis)• Alain Monfort (CREST and University of Maastricht)• Sthephen Schaefer (London Business School)• Charles J. Stone (UC Berkeley)

Advisory Board (cont’d)

II. POLICY DIVISION (14 MEMBERS)• Carsten Detken (ECB) • Gianni Amisano (FRB) • Lucia Alessi (EC)• Thilo Liebig (ESRB, Deutsche Bundesbank)• Andrea M. Maechler (IMF) • Simone Manganelli (ECB)• Bernd Schwaab (ECB) • Giovanni Dell’Ariccia (IMF) • Gianni De Nicolò (IMF)• John Berrigan (DG ECFIN)• Sebastian Schich (OECD)• Mario Quagliariello (EBA)• Kostas Tsatsaronis (BIS)• Xin Zhang (Sveriges Riksbank)

Objectives� Thinking and rethinking the

economic and financial system as a system of Sovereigns, Banks with other Financial Intermediaries and Corporations.

Financial NetworksTopology

� Looking at the financial system as a biological entity and try to identify the main risk signals also providing the right measures of prevention and interventions.

HIV infected cell

Banks & Other Fin Int

Corporations

Sovereigns

Main Deliverables - Publications111 Publications ( … but the number is running up):

Bankers, Markets & InvestorsCanadian journal of statisticsComputational Statistics & Data Analysis Economic ModellingEuropean Journal of Operational ResearchEurophysics lettersFinancial Analysts JournalIntelligent Systems in Accounting, Finance and ManagementInternational Journal of ForecastingInternational Review of Financial AnalysisJournal of Advanced EconometricsJournal of Alternative InvestmentsJournal of Applied EconometricsJournal of Banking and FinanceJournal of Business and Economic StatisticsJournal of EconometricsJournal of Econometrics Journal of Empirical FinanceJournal of ForecastingJournal of Money Credit and Banking Journal of Multivariate AnalysisMathematical and Statistical Methods for Actuarial Sciences and FinanceMetronOxford Bulletin of Economics and StatisticsPattern Recognition LettersPLoSONEProcedia Economics and FinanceReview of Economics and StatisticsReview of FinanceStatistical PapersThe North American Journal of Economics and Finance

42 Publications in 34 International Peer Reviewed Journals

Advances in Latent Variables - SpringerCountry and Political Risk - Risk Books

4 Chapters in 2 International Peer Reviewed Books

BancariaComment la régulation financière peut-elle sortir l’Europe de la crise? Statistica & Applicazioni

3 Publications in 3 National Journals

62 Working Papers (under revision & to submit)

http://syrtoproject.eu/publications/

Main Deliverables – Special IssueSpecial Issue on

Systemic RiskMila Getmanky & Roger M. Stein (eds)

Issue: Spring 2016

Contributors:

P. Glasserman, G. Tangiralaz (Columbia)S. Das (Santa Clara)

S. Battiston, M. D’Errico, S. Gurciullo (Zurich)M. Flood, P. Monin (OFR)H. Mamaysky (Columbia)

M. Billio, L. Frattarolo, L. Pelizzon (Ca’ Foscari )E. Ciavolino, R. Savona (Brescia)

A. Lo, R. Stein (MIT)

Note: All papers and co-authors presented at CSRA

Main Deliverables – BookMonograph

Systemic Risk TomographySignals, Measurements and

Transmission ChannelsEditors:

Monica BillioLoriana PelizzonRoberto Savona

June 2016

Main Deliverables – Conferences4 Big Conferences 2 Workshops and 1 Special Session at EFMA Conference:

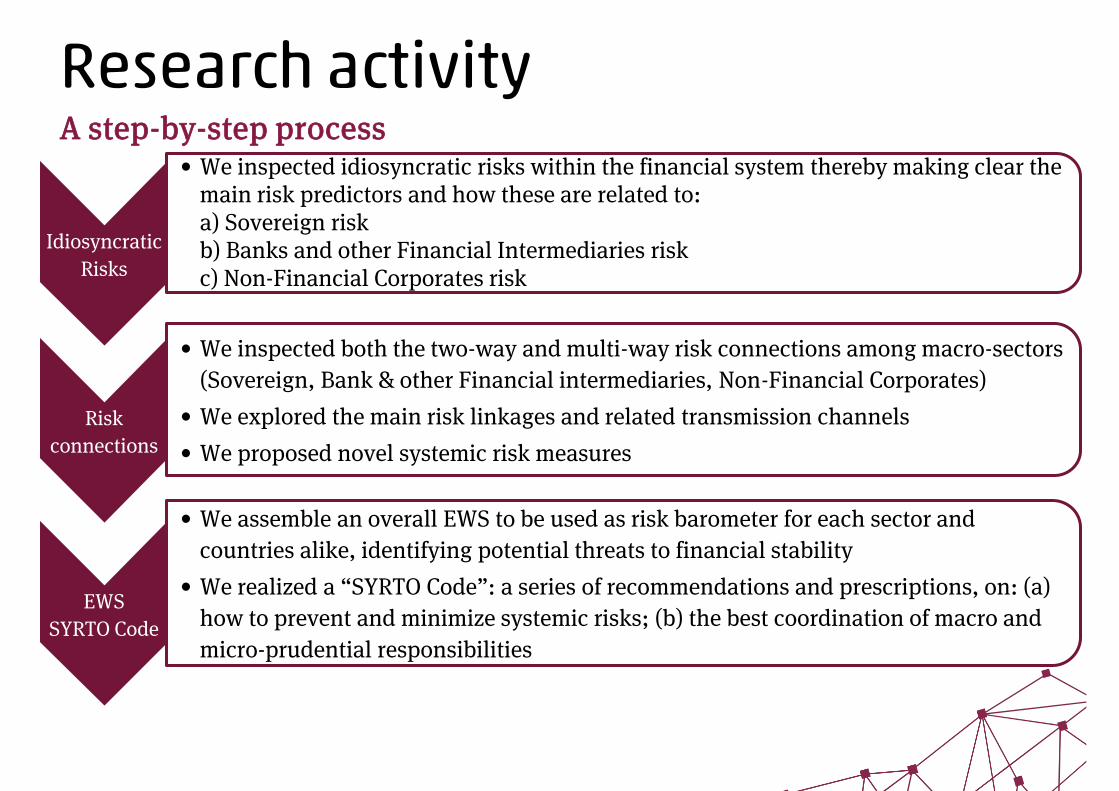

Research activity

Research activityA step-by-step process

Idiosyncratic Risks

• We inspected idiosyncratic risks within the financial system thereby making clear the main risk predictors and how these are related to:a) Sovereign riskb) Banks and other Financial Intermediaries riskc) Non-Financial Corporates risk

Risk connections

• We inspected both the two-way and multi-way risk connections among macro-sectors (Sovereign, Bank & other Financial intermediaries, Non-Financial Corporates)

• We explored the main risk linkages and related transmission channels• We proposed novel systemic risk measures

EWS SYRTO Code

• We assemble an overall EWS to be used as risk barometer for each sector and countries alike, identifying potential threats to financial stability

• We realized a “SYRTO Code”: a series of recommendations and prescriptions, on: (a) how to prevent and minimize systemic risks; (b) the best coordination of macro and micro-prudential responsibilities

ManagementThe management structure of SYRTO

Exploitation and Dissemination Group

Primary CoordinatorRoberto SavonaEuropean Commission

Executive Board(Project Manager +

WP leaders)

WP 2leader

WP 3leader

WP 5leader

WP 6leader

WP 7leader

WP 1leader

WP 8leader

WP 4leader

WP 9leader

Advisory BoardI. ScientificII. Policy

Scientific CoordinatorsRoberto Savona

Monica Billio

WPs 2-6

WP 2 – Data Collection

Data CenterWe collect data in order to:(i) Collect relevant information to monitor markets, financial institutions and the economy(ii) Evaluate the severity of the risks impact, both considering individual and systemic risks (iii) Realize a data management infrastructure where data are downloaded for empirical

analysis and model calibration

Data Management InfrastructureThe SYRTO data process is developed using the Konstanz Information Miner Platform (KNIME) (www.knime.org). KNIME is an open-source platform based on the Eclipse Platform, which allows the user to easily and intuitively manage modular data analysis environments.

WP 3 – Idiosyncratic Risk MappingHaving the objective to detect the fundamental risk sources, we focused on:

Idiosyncratic Risks

Sovereign risk

• Market’s reaction following bad credit event

• Transmission shocks within the European CDSs, stock exchange markets, and also between the two

Banks & other FI risk

• Credit risk in a large banking system

• Importance of the interbank market

• Hedge fund market• dark pools trading

Corporate risk

• Data mining tools on corporate balance sheet data with the main aim to detect the best tools to predict corporate defaults

WP 4-6 – Risk ConnectionsRisk connections among the system Sovereigns-Banks and other Financial Intermediaries-Corporates (S-B&FI-C)

Two-way risk connections

Factor models with constant, time-varying and stochastic coefficients

Multivariate stochastic volatility, to be used a synthesis of bi-variate risk

Quantile regressions to equity premium prediction

Multi-way risk connections

Multi-equation system with latent variables

Network analysis

Data-mining techniques

WP 5 – Systemic Risk IndicatorsMicro

Financial InstitutionsMacro

Financial SystemAggregate/Disaggregate

Institutions↔ System

Standard Measures

• Equity-side (CoVaR, …)• Bond-side (CoRisk, ...)

New Measures

• Risk Ranking • Markov-Switching• Multivariate Stochastic

Volatility Model

Standard Measures

• Dynamic Granger Causality• Principal Component Analysis

New Measures

• Normalized Ranking• Joint Default Probs, Cycles• Dynamic PCA & Factor Model• Leading Indicators

Institutions→ System

• Entropy Measures• Stress indices & Panels

Institutions ← System

• Graphical Models• Network Analysis• Dynamic PCA & Factor Model• Leading Indicators

WP 7 – EWS

EWS� A web platform is realized to visualize our systemic risk measures for Sovereigns,

B&FIs and Corporations

EWS (cont’d)� … monitor their risk signals

EWS (cont’d)� … and providing risk maps (Banks)

WP 8 – SYRTO Code

SYRTO Code

SYRTO Code – 6 Take Aways

1. Models to give early warning signals of systemic crisis

2. Low financial stress levels are not synonymous of financial stability

3. Make hard decisions based on soft information

4. Manage the complexity of the financial system

5. There is evidence for a country specific financial role

6. Systemically important institutions are correctly identified

www.syrtoproject.eu

This project has received funding from the European Union’s

Seventh Framework Programme for research, technological

development and demonstration under grant agreement n° 320270

www.syrtoproject.eu

This document reflects only the author’s views.

The European Union is not liable for any use that may be made of the information contained therein.