Embed Size (px)

Citation preview

Federal Tax Update63rd Annual Institute on TaxationTuesday, November 15, 2016 8:30am - 9:45am

By: Peter X. Bellanti,

CPA Amato, Fox & Company PC

36 Niagara Street

Tonawanda, NY 14150

(716) 694-0336

Email pbellanti@amatofox. com

Federal Tax Update

• Including Highlights of:• Protecting Americans from Tax Hikes Act of 2015 Extended Tax

Provisions

• Depreciation Update

• The Surface Transportation Act of 2015 IRA Rollover Relief

• Congressional Tax Laws passed in 2016 Tax Reform Update

1

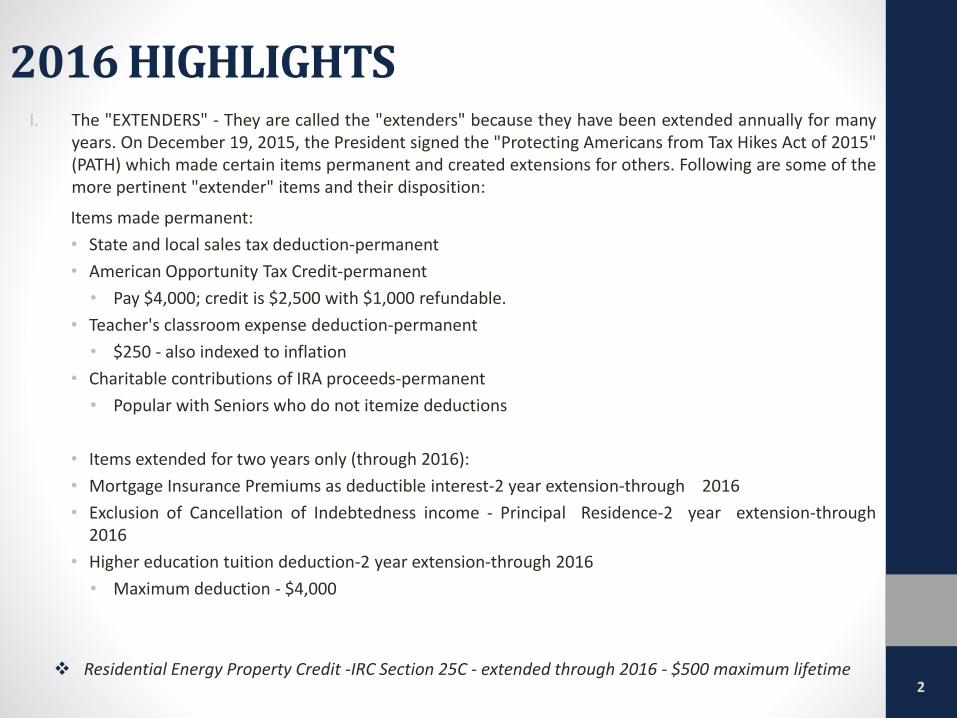

2016 HIGHLIGHTSI. The "EXTENDERS" - They are called the "extenders" because they have been extended annually for many

years. On December 19, 2015, the President signed the "Protecting Americans from Tax Hikes Act of 2015"(PATH) which made certain items permanent and created extensions for others. Following are some of themore pertinent "extender" items and their disposition:

Items made permanent:

• State and local sales tax deduction-permanent

• American Opportunity Tax Credit-permanent

• Pay $4,000; credit is $2,500 with $1,000 refundable.

• Teacher's classroom expense deduction-permanent

• $250 - also indexed to inflation

• Charitable contributions of IRA proceeds-permanent

• Popular with Seniors who do not itemize deductions

• Items extended for two years only (through 2016):

• Mortgage Insurance Premiums as deductible interest-2 year extension-through 2016

• Exclusion of Cancellation of Indebtedness income - Principal Residence-2 year extension-through2016

• Higher education tuition deduction-2 year extension-through 2016

• Maximum deduction - $4,000

Residential Energy Property Credit -IRC Section 25C - extended through 2016 - $500 maximum lifetime2

2016 HIGHLIGHTS

3

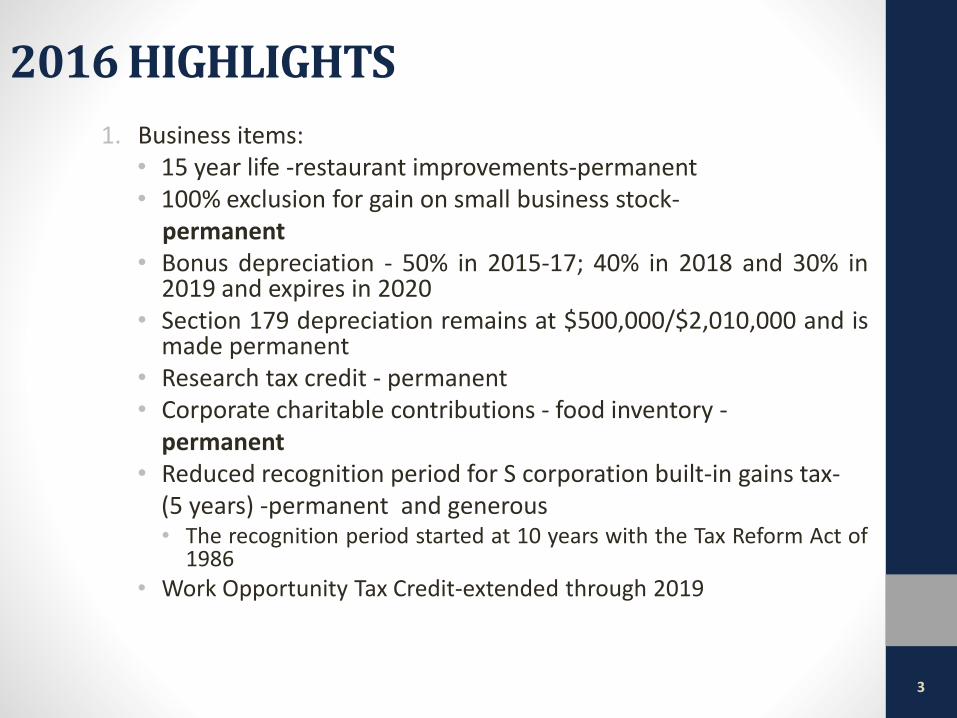

1. Business items:• 15 year life -restaurant improvements-permanent• 100% exclusion for gain on small business stock-

permanent• Bonus depreciation - 50% in 2015-17; 40% in 2018 and 30% in

2019 and expires in 2020• Section 179 depreciation remains at $500,000/$2,010,000 and is

made permanent• Research tax credit - permanent• Corporate charitable contributions - food inventory -

permanent• Reduced recognition period for S corporation built-in gains tax-

(5 years) -permanent and generous• The recognition period started at 10 years with the Tax Reform Act of

1986

• Work Opportunity Tax Credit-extended through 2019

2016 HIGHLIGHTS

4

II. Tax Reform -Update

• "Extenders" - Senate wanted to extend them for a year or two. Housewanted to make selected items permanent. The House got its way.

• Theory was that Tax Reform in 2016 would be easier because certainitems would be "out of the way". Stay tuned. 2017? 2018??

III. DEPRECIATION -be aware:

i. First Year Depreciation -(Section 179 expensing) this has been madepermanent and can be used up to $500,000 to immediately write offeligible assets (tangible personal property and certain qualified realproperty). It begins to phase out as asset purchases for the yearexceed $2,010,000 for 2016.

• Eligible property can be new or used.

• Basically tangible property; not real property

• Net income limitation (from all active businesses of taxpayer) with carryforward of unused depreciation.

• Wages count as income in computation of limitation.

• Section 179 depreciation must be taken before the Bonus depreciationbelow.

2016 HIGHLIGHTS

5

ii. Bonus Depreciation -(Section 168(k)) -this remains at 50% through 2017, but thenbegins to phase out and by 2020, it is scheduled to expire.

• Eligible property must be new

• 20 year life or less

• Not allowable for NYS purposes. (e.g. Form IT-398)

iii. Capitalization and Repairs - In addition to Sections 179 and 168, the repair regulationsset up a "safe harbor" and taxpayers with applicable financial statements can expenseamounts up to $5,000. Taxpayers without applicable financial statements can expenseamounts up to $2,500.

iv. The safe harbor is elected by annually attaching a statement to the timely filed federalincome tax return titled, "Section l .263(a)- l (f) de minimus safe harbor election". Theelection is not considered a change in accounting method and, therefore, Form 3115 isnot required.

v. In September, IRS published a 202 page Manual to summarize all of the developmentsin the areas of Capitalization and Repairs, titled, "Capitalization of Tangible Property"and posted it on irs.gov.

VI. Automobiles -the first year depreciation deduction remains at $11,060 for 2016 and2017 due to the extension of the Section 168 bonus depreciation rules for those years.

2016 HIGHLIGHTS

6

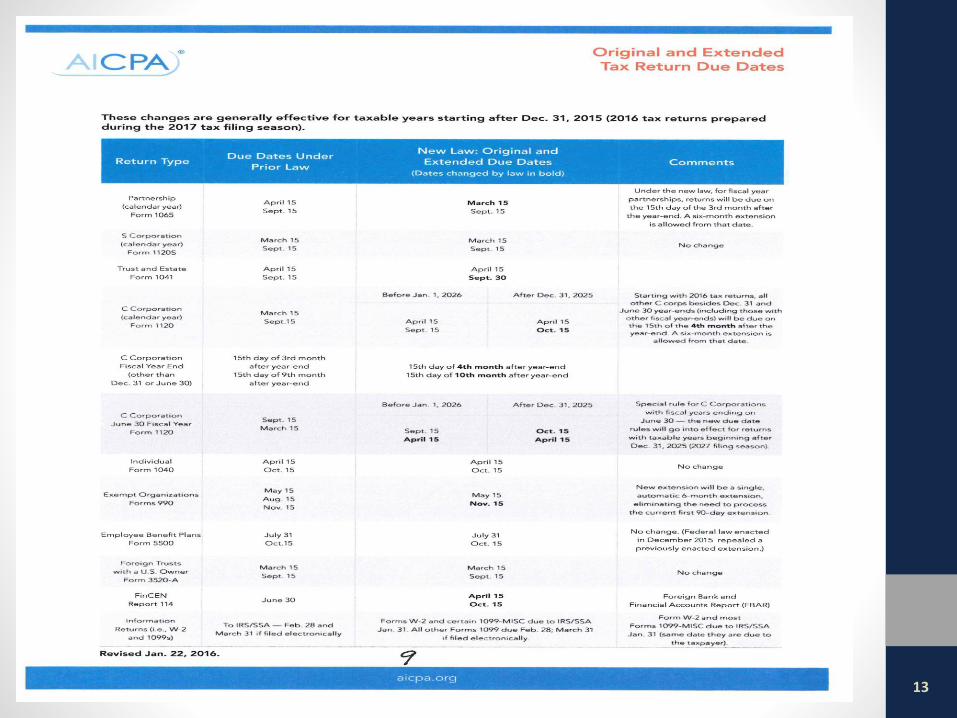

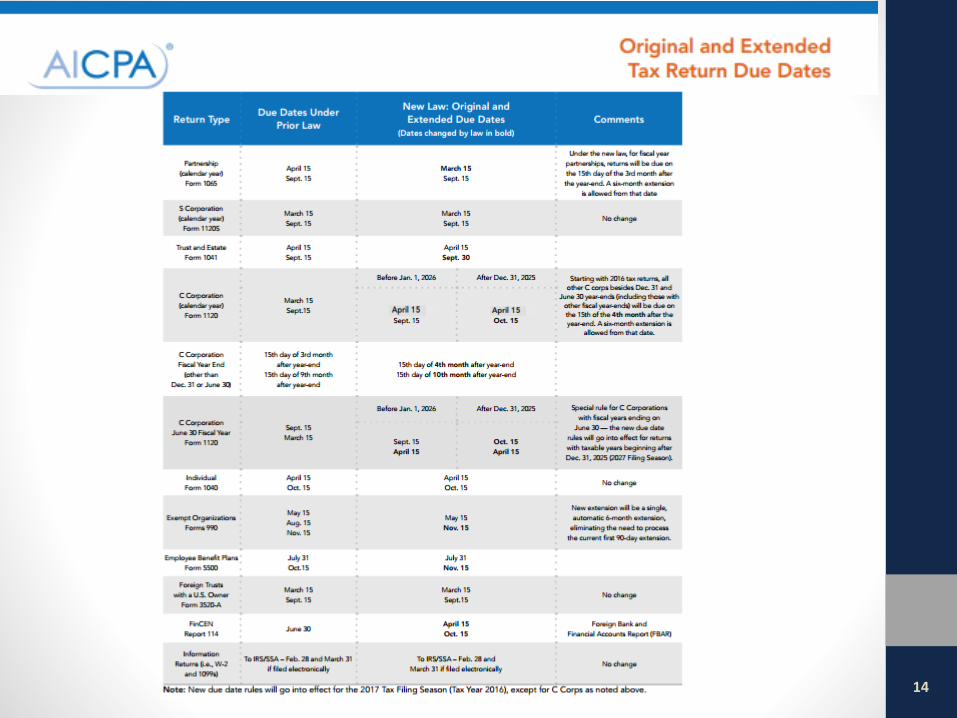

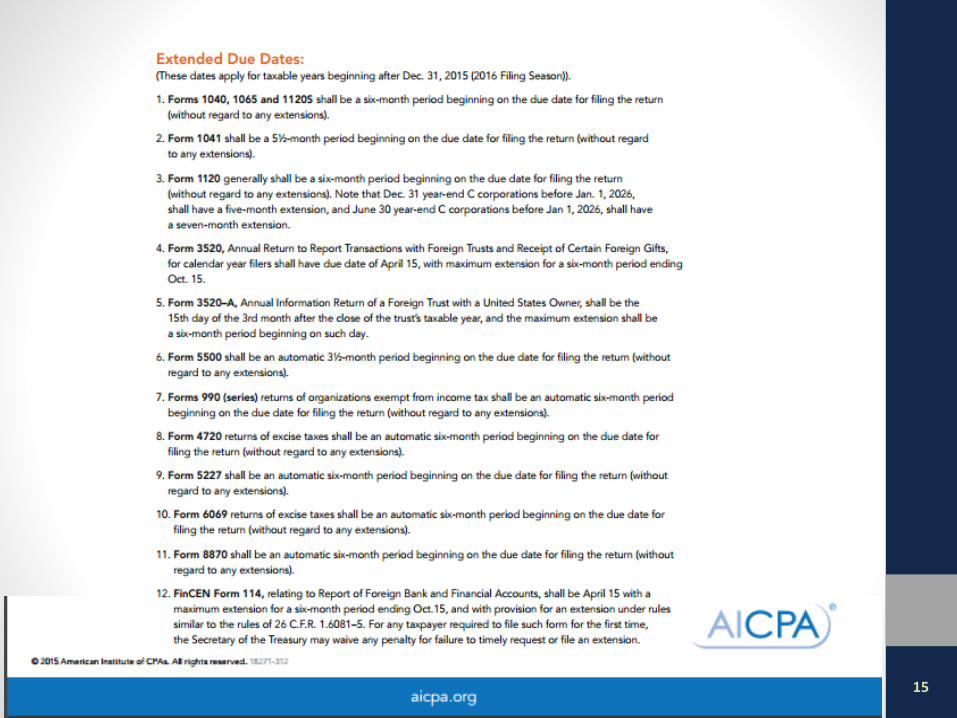

IV. SURFACE TRANSPORTATION ACT of 2015 (7/31/15):

i. Return Due Dates are changing!!

a. Partnership returns will move from 4/15 to 3/15 and can be extendedto 9/15.

b. S Corporation returns will remain at 3/15 and can be extended to9/15.

c. Calendar year C Corporation returns will go from 3/15 to 4/15 and can be extended only to 9/15. Fiscal year C Corporations will be due on the fifteenth day of the fourth month after year end and a six month extension will be allowed. Special rule for 6/30 year ends.

d. Form 1040 will remain at 4/ 15 and can be extended to 10/15.

e. Fiduciary Form 1041 will remain at 4/15 and can be extended to 9/30.

f. Exempt Organizations will remain at 5/15, but only one extension will be necessary (to 11/15).

g. FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR) will go from 6/30 to 4/15. Extension permitted to October 15th.

h. See attached schedule.

i. New due dates are for years beginning after 2015. We will first see them in the 2017 tax season which is just around the comer.

2016 HIGHLIGHTS

7

ii. Stepped-Up Basis Conformity

a. IRS is very interested in gaining assurance that the value of an asset for estate tax purposes is the same value used by a beneficiary for purposes of gain or loss computation. Section 1014 is amended to provide for this. Inconsistent treatment could be subject to the Section 6662 accuracy-related penalty.

b. New law imposed immediate estate basis and reporting requirements. Statements were due for returns filed after August 1, 2015.

c. The executor must furnish a statement to the IRS and to each person acquiring property included in the decedent's gross estate.

d. The statement must be furnished within the earlier of 30 days after the Estate Tax Return was due (including extensions) or 30 days after the return was actually filed. There are penalties for non filing.

e. EXTENSION (Notice 2015-57) -For any statement required to be filed before February 29, 2016, the due date is postponed until February 29, 2016. IRS will issue additional guidance. IRS said do not file anything until Forms or additional guidance are issued.

f. f. Early in 2016, Form 8971- (Information Regarding Beneficiaries Acquiring Property from a Decedent) is created by IRS.

g. Due date again extended to March 31, 2016.

h. Due date extended for 3rd and final time to June 30, 2016.

2016 HIGHLIGHTS

8

i. The filing requirement does not apply to estate tax returns that are filed simply toclaim portability of a deceased spouse's estate tax exemption (the instructions toForm 8971 do not mention this exception - be aware!) or to make certain allocationsor elections re: the generation-skipping transfer tax.

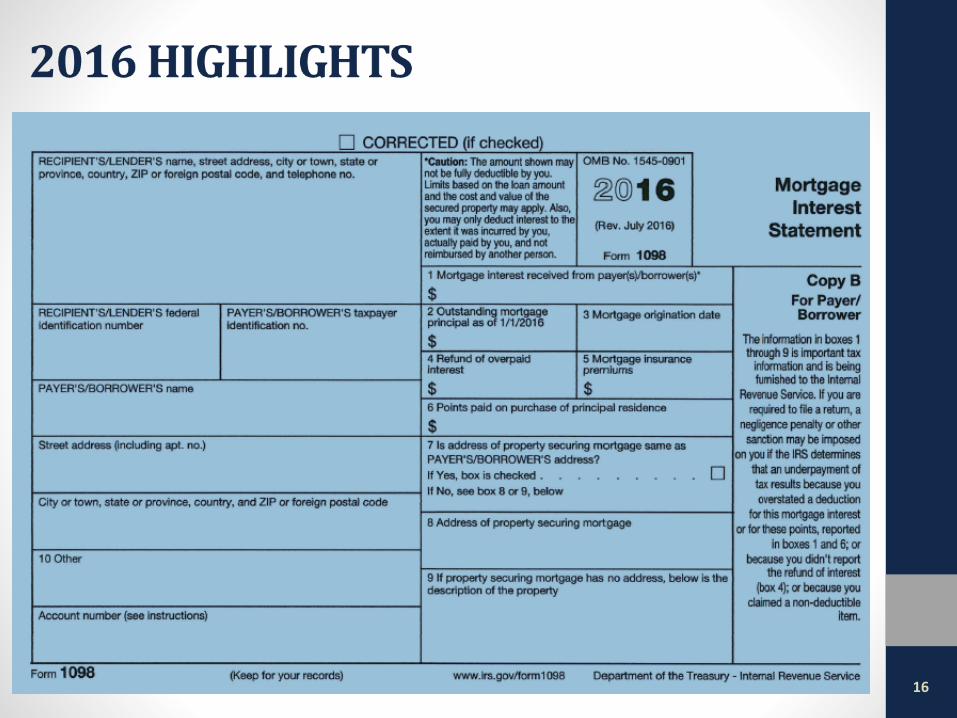

iii. Mortgage Reporting - Form 1098

a. After 2016; Mortgage Interest Statement must show more information:

b. Amount of outstanding principal balance

c. Address of the property

d. Loan origination data

e. See draft of form attached

2016 HIGHLIGHTS

9

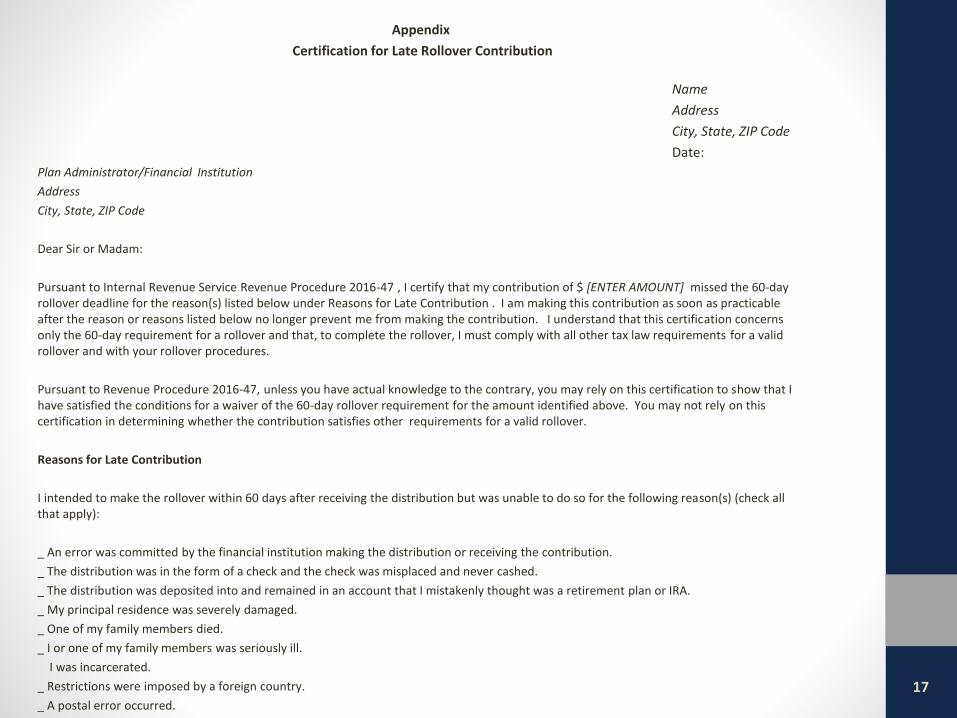

V. Self-Certification for IRA Rollover Relief

• Normally, a distribution from an IRA or qualified retirement plan is taxableto the recipient, unless the distribution is rolled over into another suchaccount within a 60 day period beginning with the date of the distribution.If the deadline is missed, the recipient is taxable on the distribution.

• Sections 402(c)(3)(B) and 408(d)(3)(I) provide that the Secretary may waivethe 60-day rollover requirement "where the failure to waive suchrequirement would be against equity or good conscience, including casualty,disaster, or other events beyond the reasonable control of the individualsubject to such requirement."

• In the past, the taxpayer had to use a private letter ruling request to obtainthe waiver.

• Rev Proc 2016-47 establishes a new "self certification" procedure to extendthe 60-day period. The appendix to this Rev Proc gives the format of a letterto be sent to the Trustee of the Plan. The letter lists 11 specific reasons in a"check the box" format as to why the 60-day period was missed. A copy ofthis letter is attached.

• Upon receiving such a letter, the Trustee must treat the distribution as arollover. The taxpayer then treats the distribution as a rollover on his taxreturn.The rollover can be challenged by IRS upon a future audit of thetaxpayer's tax return.

2016 HIGHLIGHTS

10

VI. Social Security - 2017 COLA likely to be small or non-existent.

VII. IRS Audits -IRS Employees must initiate all future audits by mail; never by telephone -effective May 20, 2016. (TRC IRS 18,000)

• Due to the large number of "phone scams, phishing and identity theft", IRS is changing a long standing policy. All audits will be initiated by mail.

VIII. Medical Expense Exclusion - In 2017, the reduction of medical expenses will go to 10% of AGI for all taxpayers. There was a reprieve for persons over 65 years of age from 2013 to 2016; they could continue to use the old 7 Yi% rule.

In September, Congress was attempting to fight this increase with HR 3590, the "Halt Tax Increases on Middle Class and Seniors Act". This Bill takes all taxpayers back to the old 7 Yi % rule.

IX. Taxpayer Advocate

• Buffalo office - good people to work with

• Normally, we must demonstrate a "hardship" in order to have the Advocate's office become involved

• Contact data of Buffalo Tax Advocate can be obtained online (Buffalo - 961-5300)

2016 HIGHLIGHTS

11

• PROPOSED: Section 2704 Regulations - PROPOSED

• IRS has been waiting for Congress to take action to limit discounts on gifts or bequests of interests in Family Limited Partnerships and Family LLC's.

• Since Congress has taken no action, IRS has decided to produce regulations which would severely limit the use of valuation discounts for any type of family limited partnership or other family business transfer, where the family will retain control before and after the gift or bequest occurs.

• Regulations have been proposed which may go into effect in 2017.

• However, the ink did not even dry on the above proposed regulations, before Congress began to attack them.

• Personal Tax Due Date -2017

• In 2017, April 15th falls on a Saturday.

• April 16th is Easter Sunday.

• Apri117th marks the observation of Emancipation Day in Washington DC.

• This pushes the Tax Due Date to Tuesday, April 18th and we have more time to work on tax returns.

2016 HIGHLIGHTS

12

X. PROPOSED: Section 2704 Regulations - PROPOSED

• IRS has been waiting for Congress to take action to limit discounts on gifts or bequests of interests in Family Limited Partnerships and Family LLC's.

• Since Congress has taken no action, IRS has decided to produce regulations which would severely limit the use of valuation discounts for any type of family limited partnership or other family business transfer, where the family will retain control before and after the gift or bequest occurs.

• Regulations have been proposed which may go into effect in 2017.

• However, the ink did not even dry on the above proposed regulations, before Congress began to attack them.

XI. Personal Tax Due Date -2017

• In 2017, April 15th falls on a Saturday.

• April 16th is Easter Sunday.

• Apri117th marks the observation of Emancipation Day in Washington DC.

• This pushes the Tax Due Date to Tuesday, April 18th and we have more time to work on tax returns.

13

14

15

16

17

Appendix

Certification for Late Rollover Contribution

Name

Address

City, State, ZIP Code

Date:

Plan Administrator/Financial Institution

Address

City, State, ZIP Code

Dear Sir or Madam:

Pursuant to Internal Revenue Service Revenue Procedure 2016-47 , I certify that my contribution of $ [ENTER AMOUNT] missed the 60-day rollover deadline for the reason(s) listed below under Reasons for Late Contribution . I am making this contribution as soon as practicable after the reason or reasons listed below no longer prevent me from making the contribution. I understand that this certification concerns only the 60-day requirement for a rollover and that, to complete the rollover, I must comply with all other tax law requirements for a valid rollover and with your rollover procedures.

Pursuant to Revenue Procedure 2016-47, unless you have actual knowledge to the contrary, you may rely on this certification to show that I have satisfied the conditions for a waiver of the 60-day rollover requirement for the amount identified above. You may not rely on this certification in determining whether the contribution satisfies other requirements for a valid rollover.

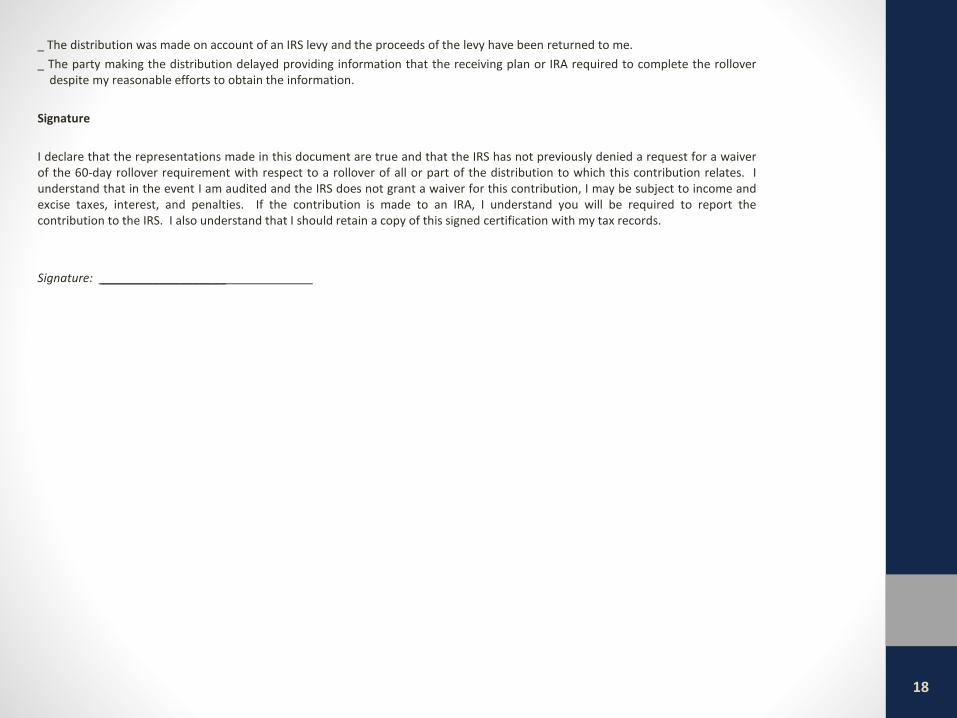

Reasons for Late Contribution

I intended to make the rollover within 60 days after receiving the distribution but was unable to do so for the following reason(s) (check all that apply):

_ An error was committed by the financial institution making the distribution or receiving the contribution.

_ The distribution was in the form of a check and the check was misplaced and never cashed.

_ The distribution was deposited into and remained in an account that I mistakenly thought was a retirement plan or IRA.

_ My principal residence was severely damaged.

_ One of my family members died.

_ I or one of my family members was seriously ill.

I was incarcerated.

_ Restrictions were imposed by a foreign country.

_ A postal error occurred.

18

_ The distribution was made on account of an IRS levy and the proceeds of the levy have been returned to me.

_ The party making the distribution delayed providing information that the receiving plan or IRA required to complete the rolloverdespite my reasonable efforts to obtain the information.

Signature

I declare that the representations made in this document are true and that the IRS has not previously denied a request for a waiverof the 60-day rollover requirement with respect to a rollover of all or part of the distribution to which this contribution relates. Iunderstand that in the event I am audited and the IRS does not grant a waiver for this contribution, I may be subject to income andexcise taxes, interest, and penalties. If the contribution is made to an IRA, I understand you will be required to report thecontribution to the IRS. I also understand that I should retain a copy of this signed certification with my tax records.

Signature: ___________________

![korean tax update...Korean Tax Update July 2020, Issue 73 [조세뉴스] 기획재정부, 「 2020 년 세법개정안」 주요 내용 [전문보기] 1. 코로나 19 피해 극복](https://img.pdfslide.tips/doc/110x75/5fec9dc31c5ac477976510a6/korean-tax-update-korean-tax-update-july-2020-issue-73-e-ee.jpg)