Embed Size (px)

Citation preview

�������� ���� ���� ��� :������� ������� ����� �� � � :�����) ���/� ���(

���

��������� ��� ����� � �� ����� �:

������ ��

�������� � ��

������� ������ ���� ������� ��� ������� ������� ���� �������� ����� ���� –���

������� ����� ������

) �� ��� � ���/��/���� �� ��� ���� ����/��/������(

�������. �������� ����� !�"��� ���#�$� %�&#Corporate)

Governance( ���%'� �*� ��+�, -�%,0� ���1�� �� 2�*��� ������� �%���*�� 3��� ���&��4 5� �6#,� 78�� �� �#����

95��: 9�%�%��0� - �#��� ��%$��� �� ��� ���� �; <#�# ��� =>�? 5� @� � ��� �A��B�� �� �%���; �BC ��&4 <�1�� ������ �%��

�%��6��� D*"E�+�F�� ��1����� 9 G� ���#� �� ,#�1� <��14 �%;� �F� ��1�����“Creative Accounting”. 5� �%C� �;��1 ��

��� �������� ����� ��'6� ��# =�: �%���*�� ���H���� �� ���� ���� �'�F ������� G"� EI+9 �%��6���� E�+�F� &%&*#� 9 �� �� G JI�B#1� �%����� ���&0� 5� %&� !�. J�I8��� K?�� 5��

�%6,�� ������ ���'6� =; L�"�� L�B�: =�: �1�� �� K?� D '# %���� 5� �������5%# �%B%�8#��� �%�H�� 9 <���14 =�; D�*#���

�� B#��� �� �� �� -�%,0� ���1�� �� ��'6��� �?� ���#� G��� �9 �M� �� ������ @�� G� ��'6��� �?� �A�; &��4 �N� �*M����� 5

�% �*1�� �%��*�� ������ ���� =; &%��#��� % M��.

�O� ������� ���� ���

5� �#% ��H 5; -���; ������� ����� 54 �1�� �� �%� �� ����� 7��B� �%��� =�: D '%� 9���H��� ������� -�� : P�I,

�'10�9 �'%� -���1���� 9 ��� *�� 7%B�#� 9 � ��� �'�����:� ?��,#�����B��9 � �%��6�� ����*��� �%��#� �"���' � 9�*%�M �' % �#�

�'���B�� �'#��M��� -�� F� QM� L�";4 �%��R1� . ���4 5��� ���'6� ��C� � 5�� �S���� P4 �1�� �� �'%�: �+�# �#�� TA�#��

$: �% �*1�� �A%��� �� ������� ����� - ��M �$����� >�� 54 D%�*#� ��'6��� �?� G����� 2�4 =; PB%�8# ��%�U� . ����4 ���

=�: �1�� �� TA�# 54 ����1��� ������� �� �*M����� 5�M� <�*# V�� � V�'� � �% �*1�� �A%��� �� ��'6��� �?� 7%�8# �� � ���*# �'��

-�� F� QM�� ������ �� �%������ -&'M0� 5%� �+� �B��.

��� :� ���� ��������

��� ��� �� ����

������� �� ����� ���� �� ������ ��� �������� �� ����"Accounting Practices" � ���� ��� ���� !Creative"

"Accounting ��"� � ����� "Environmental Accounting" #����! ��$�% ���$� �& ��$��"Corporate Governance"� � �� #���� '�(�

"The Financial Numbers Game"#�)��*� )�( . +,) �� -�$� �(� ���/� -& 01 #���� ,�� � ���� �"� �� 2����� ����3 ��� �������

����� �4� �� '�� ����3 �� ������30� ������(0 �0����� -� ��$���&� ���5 6�% ��� �� ���� -��%� -�4 �����7� 81 ���91 #������

:� $ ����� �3��� ����� ���� �� � ����� �;�� �� �4� ��<&��� ��$���� ����� ���0� �� ��$�%: �$�% 1 �� � '�$ ���� -���

�� ���� ��4� �� ���� 8�� >9� �$% �)����1 �� ��)�� . -�$�� '��;� -& �� ���� ��$%� ��& �� ?���� @� ��� ��$�% ��$��

)� ( ������� ��� ����9 ��%;� �F� ���1����� “Creative Accounting”9 ���� �������� Q��� 9�����.

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� �O�

��* ����� ���� �� ����� A��( �� B4� �� � ���� +���� 81 #� �� -�� �� ����� A��( 8�� -��"�4 -� ���$ ��9���$ �3�� 0

����� 6�(� ?���� �� �� �/�� B# � 1C, <��3�� ��� -# ,1 ,) -& 0 '��;����3 +�� �� �� ���� ���3� �����( 8�� ���%� �����

� �� '��) #E����FGGF'H&.( C, ���� ���� ������ ?�� '��;� 8��� �����!� ��$�% ��$�� �& ��$�� "Corporate Governance" -�

��4� ��� ����� �����# ,) ��%�� J���� @� �&� ���� �� '��;� <� & ��K$ ��3�� -�3 ��� �%(���� L� J� ���4�� ��� �� �����

'"��� 6�4�� ,)'��;� 8�� <�$��� ���3 ������ �� �� �$��� ���.

��� ����� �� ��

��$�% ��$�� A�9�� '���)0 ��<� -� �����)& ���� +,) �����(Corporate Governance) ����� ���� �� �� -������ -���� � ( -�

���� ������# L���4� � ��� M��� ����� ����N� -� ���� B �� �� ��� ���� ����� ��� 2$� ���4�� ��� ��# C��) �<�� L��

,) �� >9� ���(+�3�0���< �� ��)��� ���� +,) �� ��� ,) '�;� ���$& �$% A�9��#� ���� �� ��)��� 6��9���3;��� �& �� '�� �� B

� ��.�� ������ L�� ��$& �(� ������ -���� ����� �� ���(������(0 (OECD) 8�����)&��$�% ��$�� '����� ���� � ��� �����

#���� '�� �� ��3���O������� ����& ��$ ������ �� �����(! ��%�4���$���&� ���5 �� ��$�% ��$�� ��� ����� � ���& 6�% @��3� �����7

��$�%� ����� ��$�� ����� -& #������ P�3 ���) 8�� ����� ���3 Q�3� ���� '�� R���& ?���� �� ���� :�� '��) '�� � -���& #FGGS'(.

�O� ������� ���� ���

��� ����������

���8,) + �������� ?�)� 6�4�� 81 : T( ��$�% ��$�� '��;� 8�� R�9 R�41# ��%�� J���� @� �&� ,)

'��;����4�� ��� �� ����� ���� ��.

F( ����� ���������� ���3# �����(!�#������ # ?���� �� ��$�� '��;� ��$�%J(� ��& 8�� B4� �� ��;�$� .

U( � & ��K$ ��3�� -�3 ��� �%(���� L� < '"��� 6�4�� ,)'��;� ���3 ����� ��3��� C, �(7�� ��3���� J� �$��� ��� 8�� <�$��

������ �� ��.

V( Q�� �� ��� ����< ���K% -� �� �����4�� ������ �� '�)�;�� ������ �"� @����� A��( �� ����������.

��! ����� ��"#$

����� ���� +,)������ �;�� W��� 8��Analytical Descriptive)

(Approach L�� -� ���$ �� B ����� W��� ,)� #���� A�9��X �� ������3 �)�� ������ �� C�� ���� ����������� �������� 6�� .

'� L�� �(7� B�� �$ � �$� >�� R�31 ������ �� ���� A�9�� ��� >"��� ����� 8�� A7�0 81 ���9!� #������ ����� �73��

������ ����� ����� ��"��� ������ -� ������ �, . ����� +,)��%(���� ������� '� ��9��� �� �� ��� ����� �4��� ���� ?�)& '��� �� .

��% ��&$'� ��(�����

?�)& 6�4�� �3& -����� '��4� '� �4� �;�5 ���1 ��%����� 81 ���"� '��(& ���� : #�����)&� ���� ��$%� ��� � ������ ��� '�4

?�)& 6�4�� �� �� ��3���� #����)&����� . ���� ���� '�4 ������

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� �O�

���� A�9�� ����� ��;����$�% ��$�� '��;� ?���� L�� -� # J���� @� �&�+��������� ���� �� #� �� B���;� ��, � ���3 8

:���� �������� ����(!�Y ��3�� -�3 L�� '�4 M(��� -�� �� ��K$ <� &����$�% ��$�� '"�Y ����� ���� Z�� �4� J � '�4 ��& L�� -�3 -��$�� ������ ������(0 �"� �� ����� ����� ������

�3� �� �� ���� �$��� �� ��3��� ��4� �� J9�� ��� ��� ��-�3� +,� ��� ���������;� �� ')��� -& -$�� ?�$� '��;� 6� �� �$��� �� ��$�% ��$��� #� �������� 2��� '�4� -�9�� E,�

� W"��� ')&� ��7������4�� ������ �� ���K% -� �� �� ��)��� A��( �� ����� @����� '�)�;�� ������ �"� �� ��� ����<�����.

��$�) :�*� �� ��� ��+�(� ,�����

��� -���� � ��� ��#+

B�& 81 ���%! -� � 0 ��� ��'*�� '��;� J�� '����0 -�

(Corporate Governance) ���4�� ��� ��& 01- ��%� ������ L�� B�& 81����� 6�(� ?���� �3�� 0 � �� �� �/�� B1 C, <��3�� ��� -

L��1) -���3 +�� �� 0 '��;� , ���3� �����( 8�� ���%� ����� �� ����� �� '��) #E����FGGF'H&()�(. � �� ?����� -�9 -�

��� �& �� ��3���3��� � ����: ���4 -� ��� � ��$�% ��$�� -& #��$�% E����� #'��� ������ ��$�% C��� B[3�� �� 81 C,$�

�R�3!���4 C�� 6� �� ���� <�<�� 81 ���� ����$� . :��� �� '��;� ,� ���4� -& �) ������R�3! ��� -��9 ��$��

�R�31 �)� �9�& B3� 8�� ��$�% ��� ����� ��4��� -� '��

)�( V�,R� �+�# �%��*�� �W�� G�M� 54 =�: -���F� � M# �) ����� <%�*#� P� ������ �� ( =�:H6� 54" ������� "F� �+Y� ��M�#�� �� ���� Z&%M"Governance" ) 951����[�(.

�O� ������� ���� ���

�"; ����� �9�& '���)0 J� -��)��� ���� -��9�� -� :��� '��;� -�$ -�;���� -�9�4�� -��"� -� ����� @���&�R�3!

��$�� ����� ����� :���� ��$�%����! � �(� 8�� �& ��$�%� ����� ���;� 81 ��$�% � �� �(� ���� 6� ����%! ?�� ��$�% �� ��

�� ����;% ����� -��9 �R�;$ J��� ������� ��(��� <�<��� ��������� ����3� �7����� �4�� @�3� ����! '���� �$�% 8�� ������ �3�� ����� �������0) ; Shahnawaz, 2003 #E����FGGU'(.

��%��-���� ��& (Estrin, 1998) 81 '���)0 �� 2�"� @ � -& ��$�� A�9�� �;�0 �) ��$�%� ��$�� -� �����! ���9!� @� �& 81

:��&# ���� ��� �� ����� �4 �� ')&� @� �� J��� �$N� ��$�� '��;� �� � ����9� ��$�% � ����� ���� Demirag et al., 2000;)

.Dewing and Russell, 2000; Monks and Minsow, 2002; #E����FGGU'(:

T. � ��$�� -� ��;���!8�� � �(�� R��. F. ������(0 �R�;$ -����. U. B7� -� ���� E, �$�� ��3�1 �$�% ?�)&# C�� 6�4�� �"����

R�� �� ���� ?�)�.

V. ������ ��3�� ����� L�� ��$�% R�& �� ��$�� -���4� -���� 7$ 81 � �(� ���N����)� 2�3����1 -��)���� �$�% �$�%� ������ ����3 �� -�����.

S. ���� '� ��� '��� -� N '���� -��,�;�� -������ ���� ���� 2�3����!��� N���� B"�9�&.

\. R�& '��4����!�4� �3�� J��� �R��� <�<��� ���� . ]. 8�� ���� -� ��$�% -�$�� -� � $& ��� @��3 -� �����

-����� -������� @��3��.

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� �O�

^. ����$�1A7�0� -�9�4�� -��"�� -�;���� -��)��� �$��%�

��$�% R�� � ��� -� (�� ��� .

6 � ��� ��7��: ��$�% ��$�� '��;� -& � 8�� <$� A�9�� � �(� 8�� ���� -��"�4 ������� ��$�% ����� �� '�����N�� # ���)& 8�� �$N��

:��� ?��� �$��%� �_(7� �, -��"�_� -�;��_�� -��)��_��$�*')��# <�<���Q���!���� ����� �� ����;%� .

���#"� �-���� � ��� ��#+ .��+' ����� �

P���3 C��) -& 81 ������ L�� ��%�������� ��9� 8�� ��$�% ��$�� '��;� ���;� 6���� ���� ��� :����# R�� C, -�$ -�

�� �7�� ������ E����(0 -���� �����$ ���� ���OECD C� ���� .����� �� � 8��: ������ E����(0 -���� ����� ���(OECD �� '��T```���a ' ���� b�� � �$�% ��$���� ����� ���c :

T. '��� ���� 6�4� Shareholders Rights

F. ���� ���� ������'���Equitable Treatment of shareholders U. ���@���&>��� Stakeholders Role

V. ���N�� 2�3����! Board Responsibilities S. Q���!����;%� Disclosure & Transparency

��� ���� � ���� b�� � +,) 8�� ��) �$%T ( -$��-&� ��;�� ���%�# L�� ���& ��* ')& @��3 ������ Q�3� E&�$�% . -$�� C,

��4: 1- 8�� b�� � +,) 6� ��& -� ���� B��� @���� ?�� J(� ��! W"���-� �� �3�& )��� '�$�1 2�3� 8�� � �(� ���! E�����

%��$�# �6�4� ����� � -��)������ ����( '��� '��4� � � �$ ������ '��� @���� ���� # R���1� @���& #����� -�;��� -� >���

�O[ ������� ���� ���

� #-�����R7��� ')��*� # �(7� �, ��"; -�P������� �� �$�%# 8�� ��$K� J� ��$�% ����9A� �1 @���� ��������� �� �����

������ �4�� ���� ������Q���!� ����;%.

���)�(. \ ���������� ����� .

������ : ������ ������� ������� ����)OECD( ����� �)������ ������ ����(.

P3���� ��� �4� 6����� ��� C� &� ��$d$��%� �� � '��4� 81 ?��P���( ��� :���� 8�� ��$�% ��$�� ������� 8�� �b�� � -� �����

������ E����(0 -���� �����OECD��� 6���� B '� " ��� ����4� -���4� ��;��� '���(ROSC) " 8�� -���� 8�� C, 6� �� '��c -

��$��� ��� ��))#�(�%FGGF'.(

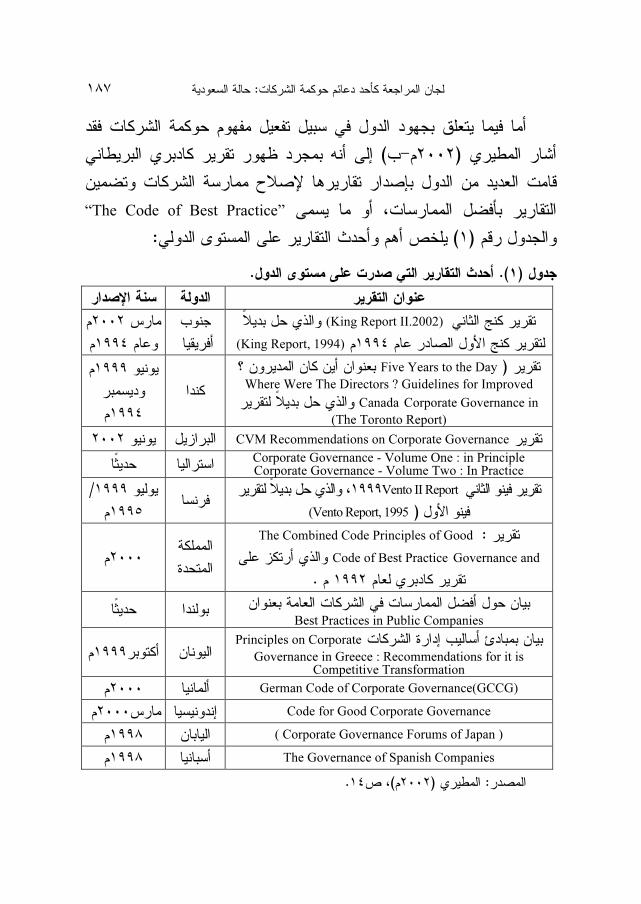

�� �; ���*��'10� ����

<��+4 �� ]��+���

E�+�F��%��6����

��%��R1� QM�-�� F�

��� 7�B��'10�

�����

����� ����

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� �O�

��� ��& �� �� ��� ���3 6��� �� � ���;� '��;��4� ��$�% ��$�� E���� ��%&)FGGF'H@ ( ������ E� ��$ ���4� ���� ��3� B�& 81

��� -� ���� ���(���a �)����4� Q7�! -��9�� ��$�% ������ ������� �9�K ����4�# 8��� �� �& “The Code of Best Practice”

�3� �� '(�)T(��� :���� 8�� ����4� L��&� ')& Z��� :

����)�(.���� ��� � ��� ���� ��� ������� ���� .

������ ���� ���� ���! �

��C�� T� �%�B#(King Report II.2002) JI% � �� Z?��� ��; � �+�� ��0� T� �%�B#������ (King Report, 1994)

<�M �%B%��4

Q�������� ��;������

�%�B# )Five Years to the Day ^ 5��% ��� 5�� 5%4 5��*� Where Were The Directors ? Guidelines for Improved

Corporate Governance in Canada#� JI% � �� Z?��� �%�B (The Toronto Report)

� �

�%�%����� ���1% ������

�%�B#CVM Recommendations on Corporate Governance �%&����� �%�%����

Corporate Governance - Volume One : in Principle Corporate Governance - Volume Two : In Practice �%���#1� JC% ��

��C�� �%� �%�B#Vento II Report ���� �%�B#� JI% � �� Z?��� 9 ��0� �%�)(Vento Report, 1995

�1�� �%��%���� /

�����

�%�B# :The Combined Code Principles of Good

Governance and Code of Best Practice =; &�#�4 Z?��� ��*� Z�� �� �%�B#���� � .

������- �#���

�����

5��*� ���*�� ������� �� ��1������ �"�4 ��� 5�%� Best Practices in Public Companies � ��� JC% ��

<%��14 \ ���� 5�%�-�� : ������� Principles on Corporate Governance in Greece : Recommendations for it is

Competitive Transformation 5��%�� ���#�4�����

German Code of Corporate Governance(GCCG) �%���4 �����

Code for Good Corporate Governance :�%1%� Q��������

( Corporate Governance Forums of Japan ) 5���%�� ���O�

The Governance of Spanish Companies �%��14 ���O�

������ : �����)�����(� ��!.

�OO ������� ���� ���

���#"� �-���� � ��� ��#+ .��+' �� ��/�� �

� ��� �����(! ���3���$�% ��$�� '��;� ���;�# ��4�� C, �� �� �� ��� �� �� �0���� C���� ����� B3� 8�� �� �� �4���

+�3�0 ,) .���%& ���� �� � 8�� -���� )��� � &#R FGGT' ( 81 '� B�&�� '�� FGGT' ��$�% ��$�� '��4� ���4� ��& -� R����0 �� #��� � E,B '�( C� ��� 6�� �"�)� ��3��� ���3� ��<� J� -�����

��$�%� ���� <$�� -� ��� B�� C��%� #���� 6��� ���� � ���-������4� -������(0 -� -������ ��3��� � ���� . ���4� ��%& �(�

81 B��3� 8�&��$�% ��$�� b�� �� '��;� - ����� ��� ��3�� W��� ���)& -�� #���7����� ��,�;�� ���"�� ��$�� -���4 -� ���: 6�� -���(

��� 2&�`S/T``F' ��$�% -���(� TS`/T`^T' ������0 -���(� ^/T``]' A��( -���(� ����� '�� FGU/T``T' Y A��!� ����� -���(�

�;��E<$�� `U/FGGG#' -� �)��*� -���4�� ��$�� � ��� ����� ��$�%#��%� � ��* �& ��%� � ���� R�� .

����� ����� ��$)E<��# FGGU' ( ��$�� '��4� 81 ?��� ���� �� �� �� �� �� ��� ������3 �� ��$�%b�� � ���� ��$�% ��$��

-� ����������� E����(0 -���� ����� 6�� -& 81 ��� �� ���P���� ��% �(d����� #��$�% ��$�� ���( R���1 ��3� �� � @��� ���

���B� #��$��� ���� ������� ���3! '��4� �� -��� '�� �$% 1 ���$ -��c ����� -� �;��� �( -��� �3��.

���F` ����� FGGS -����� ���� 2�"�� ������0 ��<� -��& ' E���(EIOD) �� C,� #��� �� ��$�% ��$�� ���( �%� Q���

��4� �� ����-��� "����� ��$�% ��$���" ��� ���� C��% ���

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� �O�

VGGC��%� ) #���� ���� �����%� <$��FGGS'(. ��<� ���& ��$P��N� ����� ������0 #'�� ����� A��( ��$�% ��$�� ���( ���

� A��( ��$�% ���1 �R�;$� ������ -��9 ����%��� ���( -�9�� E,'�� �����#��$�% ���1 ��74�� -��9 J� C��$ ��� ��� '����� .

������ E����(0 -���� ����� b�� � R��(0 '� �(�OECD ��$�� P�3�� ��;�� ���� �$���� ��$�% J9� ��� �b�� � ��$�% ��$��

��� �� ����� A��(.

81 ���%! ��3�P���3 C��) -& �0����� �� ������ ��� �� $ :��� �� ��-�� �) #����FGGU'()�( -���� @�/���2���� ��

�� �� W��� ��� -���� 2�3� ��� #L�� '� P��N� ��$�� ���� R�%�1

� � ����� �� ��$�%# �������� ��� � � <$�� ����! �������� �� ��#)� �������� B �%� ����Z��� ,) �� .

��� #"��' ���� � �.��+-���� � ��� ��#+

C��) -& ��7� B�& 01 ������ �"� �� '��;� ,) ���� -� '*�� d$����P��3 d7�� � ( -� � -���� ?���� '��;� ,) Q�% ����� -�����

A��( �� B4� �� ��;�$� B ��3 8�������E���� .������� ���� ���P������0���� +,) ')� :

• ��������$��� �� � ���� ����� � � ��%�� � ) ����� ���� ,�� � ��4� -���� �$ �4��T`^T' (��4� ��� ����3 A�� �� ���� C��

-� ���; �� '��4� TVHTS� ��$& FGGU'��"� ����9�� � Q���O)���� ����;%� � ����� ������ ��$�% �� �R���� � �(� '�� �� �

)�( The Second MENA Regional Forum on Corporate Governance, "Improving Transparency

and Disclosure", Hosted by Lebanon Corporate Governance Task Force (LCGTF), Beirut, June 3-5, 2004.

��� ������� ���� ���

��������$�% ��$�� '��;� �%(��� �)����� �7� -� Governance Corporate� :�� ����$�1B4� ���$��� �� . ���&� ���( �� � �����R�31� �(7� E�, -� �� ������ �������� ������ ��(7� '���

-�9� �� �K%��� '����� �R���� ����;%� Q���!� R�� �R�;$ <�<������(� -������� ��"�� �$$ �� .

• '��(������ �"�� -������4 -� ��������a �� A��%� ������� C��� ���(� ����� ��3��# ����� ���4� ���-�3

��)��� ��$�%� ��3��.

• ���� '(� R�<� 2�3� ��( FUS g����� FG/^/TVFS E, _)��� ��4;����� ��3 �$ �� ����� � �(�� ���� 2��K� 8�� B��

� �(� ���%� ����"� � ��� -��� ����N� ����� C,� <��3 �� ��� ���, � �(� ����4�# '�� ���� ��"�(� ������# B������� ��%���

�� R�� ���;$ J�� �� '���!� ����$� �<�3�.

• J� -����� ����! �R�;$ ���! ����� <$�� B��� E, 84���

O �� �� ����3���% ��� 84��� ������! ���3 ���� ���! ���� 2�3�� ���! ?���� 81 ��$�% ��$�� �� ���� ��3�� �� ������N���

��$��� #-�� � 8�� ������$��� ����� '�4� �� 2��� b�� ����1 ����N�� ��$�%. �����& ����� ���� 84��� M(�� �(� �): ��,3

�� �$������ ��� ?��� ���(7�� ��$# �� ���"� ���$� b�� �� '�� ������ ����!#O ���00�� ����� �� ������ �� # ��� h,����

b�� �� h,��� �� �)����� ��$�����!���%� # ���91 W���� 81 ���1��$�% � ��$�� 6� �� ����N�����!�%� ��# ��� ���;��

2�3� ���3���!�� ������� ����N�� ��$�%)�(.

)� ( *�� 2�%��� - %�M� =B#��� Q%A� G� ���B�������� ��1�� ��/�/�����.

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

• �4� '� ����"�R�3!��$�� 6� ��� ����� -� ��$�%� (Corporate Governance) "���( �� �4� ������30 '�� �;���'����

� ��(�% �4���� �9��)�� -� ��� N ��3�� -������� -�������4��� �� ������(0 �$��� .� �( M(�� �� -�$��%���<� & �R�3!

��;�$ �� ������ ���4�� ��� @��3� 81 ���%! J� ��$�%� ��$�� ��4� ��'��;� ,�# +,) ���� :��� �R�3! A��( �� �����E���� )�(.

• ��$ ���( ��3��� �)� � ���� -� ���� ����� J � �������3

� ����� ������ �%(���� Q�% '��;� (Corporate Governance) � ( -�-� ����3� �� -������ -������$� ��3� ��3��� � ���� >�9���

������ �"� �� B4� �� 81 �3�� :��)�.(

• ��� ���4 '(� E�<� ��4FFT] g�����T/TT/TVFU_) 8�� Z�� E,���� �� :TH -&��"� -����� '�4� �P��(1 �$�% �� -� B 3�� -��$N�-& -�9�� 0 �$�%� ���� '"�4 E& �& ����� �& ��� �

� #����� ��* �������& '"�4 +,) -� ?,�� ' B�E&�& ����� ������� ���,� -� W��� i� � �&-&�4 +,) -�$� ���9� '" .FH -&� '�4 ���1 �$�%

B 3�� �$N� #E��� J � ��$K� ���a-&d7$ -� R�9�& 2�3� ���! -� '�"� �(&� '���3�<� �$�% �� -��,�;�� -�;���� -���� -������ '��& ���� ����� ���4� J � ,) �7� ��<� �( #����� �3��

�)��� ��$�%'��� ���� �(7� �, '������ � .UH -& @���� '�4� ���4� ���a �$�% �� ��� ��3�� 8��� E, �����4)���$K� Z�� (

�� ��$,� ��$K� B 3�� ��N�)F (+7�&.

)� (��%�� - %�M9 *�� ����� L�CIC�� [/�/�����. )[( Z�%8���9 �����/4 9�Z�%8���9 �����/ 9<�Z�%8���9 �����/ ��B��� 9`9 �����9

� 5� � ;0��� =�: �[ ��*� �����.

��� ������� ���� ���

��3����%! -& 81 ��4 ,)R�3d,�;�� '��$ ���� B�3�� 89�4� '(�]/@/TS`GV �� g���S/S/TVFU_) ����� 8�� �4���� �9�4

���<� ��3� ������ ������ 8��� E����(0 2�3�� ��"� ��3�'(� ���� ��� @3�� ��$%� UTST g�����\/U/TVFT_) ����

����� ��)��� ��$�% A�9�& : �� ����� � �(� ��� <�<�� ����9��)��� ��$�% � (�� '���� 84�� ���� -��)��� ������ #R�& +,) 6�4��� ��$�%����)& . '"�4 ����9�� �� ������� ���;$ 8�� ��$K�

��$�% -� ����� ������ �� ���� ����# -� -������� -�$�� C,� '��4�R�&��$�% # -� � "�� R�5 81 ����� R�&C�� ,���� #��$�%

'�������� ����� � ���� ���4.

• �4� '� 84���''�)���� ������ ��$�% �� ����� ��3�� ����� '' � ����� ������ ����3 B���� E, ��% E,�P��9�d;��$ ��� <��3� �

SGG� ���� ���� -����� -� #R���� ��3� -� Z�% ��3��� ��3������� ��9� C,� #����� (�� -��� 2�"� ����)�(.

• P��N� ��� 6�� �"�) ����& ��$A��%� -� ��$�� ��"7 ��& :���� J�� 8��� �� ��$�%���! -����� -� � ��� #���� ���%�

R� 1B��� '�����7� . #���� ��%� J�� ��%� @� & ���� A��%� -�9��� ��������� '�$�� ��� @� ����# #���� ����3� -��)��� 6�4� �����

-�� �� #����;%� Q���! L�� @� � ������ J � @� ���N��� 2�3� ?"�������! # '�$�& -�9�� E, 2��� @� � A��%� ������

B����� -� ,�;�� �%� )(. ���%! ��3�P��N� ��� B�& 81 2�3� -� '(� ��4 ��� 6�� �"�))THUTFHFGG\' ( ��FT/TG/TVF] 6��� _)

.م����٣٠/٣/٢٠٠٥ة ا ����د� ���ر�� ) ٧()O( ����٦ة ����ظ ����ر�� ������ق ا�&��ل �$�# ٢٧ ص ،م٢٠٠٦ ��* �+� أو ا�&���0 ا��*�&- �,

.http://www.cma.org.sa/cma :�4567��7 ا3

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

TF/TT/FGG\'# �� �� �$��� �� ��$�% ��$�� ��"0 8�� �4���� ������ . �� R�3 �(� 6���! �"�� J(�� 8�� ��%�� -�� B�& �����$" �(

��"7 ���1 �� ���� ��%���0 '� ��$ #���� ������ -� ��4� b�� ���$�% ��$�� ��3� �� ���( �& -���( -� B��(& ��� ��� @��3� . ��$

�� ����� �����(0� ����7� ��"��� ���/�� �� �)���1 �� ���� �%� �� �"�� ���4���"�� J(�� 8�� ��� A��%�."

�)�) :"$�-���� � ��� �0��� ��1� ��"� �

��� 2 ���'���"� � �$"� ����$ ��3�� ��3� ���4� 81 ������ ���%! @���� -� B��

���� -� R<3 ,�# P���� ?����� ���� 01 ��3�� ��� �& �� B�&������ :��1 ?���� R�;�$0 '�� ?�� ���� +,) ��/������ #

���9!� ?���� 81 � ��5 ��� @��$A�9�� ,� -���� . �� � 8�������: -������4 -� ����� ����$ �"�� ����(1992) The Canadian

Institute of Chartered Accountants (CICA)���K ��3�� ��3 " ���$� ��3���N�� <$��� -�, �$�% R��� -� ����� ���� '"�4 ��3�� �� '��

2�3� 81 ������� � (���! . -� ��� �4��$ ��3�� ��3 ���� 2�3�� -��3�����!# J3�� >�%�� ��3�� �� ������%� Z�����

�3���#��3�� W"���� 6���� # J��3� #�$�%� ����� � �(� C,$� � ���� ��������%�� ��� .�� ������� -����� (Marrian, 1988: 2)���K

" ��,�;�� ����N��� -�;�$� ��* R��� ���� 81 ��7� -� ���$� ��3O������� .')& -������ '"�4 ��3�� �����& C,$� # -� �$K� :��

W"���� #�$�%� �� ����� ����� � �(� '��� ����� � ( -� ��3���3���� ���� J3��# @���& ������ >�%�� -K% ������ R���1�

�3��� J3��" )� <����-��3�)# FGGF'(.

��� ������� ���� ���

��� � ��' �(��'���"� � 3�"�

-& 81 ������ L�� ��%� � ��� ��3�� -�3 '��;� B_��� @��� ����N�� -� ���� ���� ���� 81 ,_�� ��_� ��� +���� ,�� �� $ �$��

-�( ?�� -� ��$& .���� �� � 8��: ��_%& �_�$�� (Birkett, 1986) -& ������7� ���& �� ���� �� &� ��3�� -�3 >����T`UG' ���_��

���� 6��� ���� ��3%(SEC) ���� 6��k C������ ���� C,$� (NYSE) -�3 R�%�1 8�� �$�_% ��_��� ��� L��� �� ��3�� -��_$� <�� ��� (McKesson and Robbins) .81 ��%� ��$-& -�_3 R�%_�1 ��_$�

�_� �_�(��� �_�* 27�1 �0�� L��� ��� '��� �� � �� �( ��3��?��� R�� �3��� ��$�%) � <����-��3�)# FGGF'(.

-�$� �� �� ��$���� ����� ���0� R�%�a ���� �� ��� �"�& -� ��3��� -�3# L�� ���� 6��� ���� �"�) ����&SEC '�� ��T`]F '

P��( -��)��_� �_���� ��)��_� ��$�%_ �_� �_�3�� -�3 -��$� -��������. � '�� ��T`]\' ����9_ �_$���� 2�3��$ ��3 ���&

�$�% �� ��3��� -�3 R�%�1 ��)��� �. � '�� ��T`]^' ���� ����& ���� 6��k C������NYSE P��� ��$�%_ '<1 ���)& -�$ ������ -�

��3��� -�3 -��$� ���� ��3��. ��� ��$d4�0 � '(� �����\T ��� E, �����4 @����� ��3�� ��3 -� �(7�) � <����-��3�)# FGGF'(.

& ��$%� �� ����� �$��� �� ��3�� -�3 81 J3��� '��T``T' ����� E�� ��$ ��3 ��$%� '� Cadbury � '�� ����� �� ���& ��T``F' -��$�

-�����_4 -���� �7� ��)��� ��$�% �� ��3�� -�3. J_��� �_� �� 1 @� �&�%�R� �� ��3��� -�3 ����� �$��� ��� 0 P���$ ?� �_$���& -_�

��$�% -� ���� 27�1 �3���# ���� ����4� -�������� -��)��� � ����

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

2�3� � *�� ���9� ��*���1 ���� ,�;�� �� ��$�% �_� �_� �$�% �� ��� � �(�� ��� ������� �� ���3 ��� ����� #: '�� ���3�1 C� T`^]' R�%�a

��$�% �� ��3�� -�3 ��)��� ) #E�� FGGU'(.

�0�_� �_� �_�3�� -�_3 -��$� ��/9 �K%� �4� ��$ �� ��&� �$�% 27�1 C, -�� #������� �4� � $� �� 27�!� �����0 C_���7�&

(Acceptance Corporation Limited Atlantic) '��T`\S'# ?_�� E,_� � ���� g���� �� L��� � $& B��$ ��$ �� (Green, 1994; Collier, 1996).

'�� �� ��$ �� ��� '(�;� �(�T`^V'# -� -�$� ����� � � -� -��& ����� ��)� ����$ C�� � $&(Canadian Commercial Bank)� (Northland Bank)

E��$ -������4 -� ���� ���� ��� ���(CICA) �_����$�� ��3 -��$� 81 (Macdonald) ���_( ��� #����$ ��$�% 8�� � �(� ����� � � L� �

'�� �� �)���4�T`^^'# �_��4� ��3�� -�3 -��$� ���)& 8�� �$& E,� ��$�%_ �_�� � �(� �"� (Macdonald Commission, 1988) #) <�_���

�-��3�)# FGGF'.(

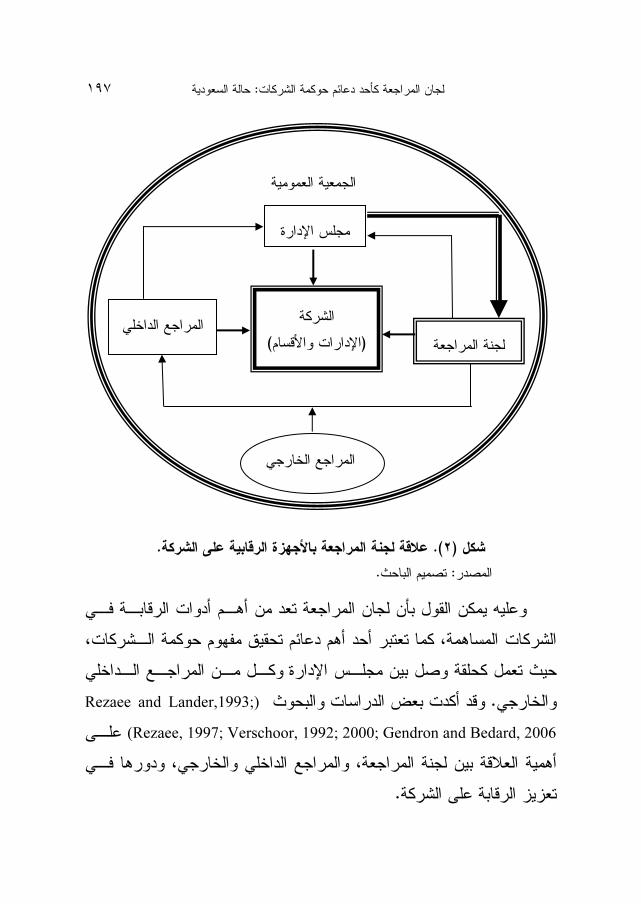

���-���� � ���2 ��"� � 3�" �/��

�4 �� ��4; �� ��9���� ���� �����_� �_� �_�3�� -�_3� ��)��� ��$�%# � #����$%� 81 ��& �� ?���� @� ��� E, �N� ��) B�;� Q����): �� l��$�% ��$�� A�9�� ��3�� -�3 �(7� �)

8�� ?��� -� � 0 �N� ,) 8�� � �3O����c )"���� ( �� -_$�� ��7� -� -� �$K� 6� �� ��$�% ��$�� '��;� J(� ��& 8�� . ��K_��

2�3� ���c +,) ���4� �����! ���� J3��� ## �3��_� J3��� .��$ �_���� ��_�"� ����N�� ��& ��� ���� ����� � �(� '��� ��3� -&

2�3� ���! . �� ��3 ��� ��K�� '�_�� ���;$ -� 64�� �� 2�"� ��3

��[ ������� ���� ���

2�3� ������ E& '��4�� #�����; +,�;��� ����� � �(����! ���K_% -� -��)��_� >��_� ����� �$�% ��*& 64�� �� +������ '��� ���;�

-�������� ��4�� �;�$�� ���� �R�;$ .���4� C, �$& �(�E�� ��$ Cadbury)

(Report �� '�� T``F��� ' -���" �_�$�� �R�_3O �_��� @��3��$�%� " 8�� 2�_3� -�3 -���� ���)&���! �_�3� �_�3�� �_�3�$

��3�� ��3� -�3� ���9� ���4� -&� �m��$�� <��� ��3� ����%��8�� ���� R�9�&�$�% h��� -� -��4��� .��%& ��$� � -���_� Millstein,)

(1999 d(�;� C��) -& 81 � �_ �(� '�_�;� ������ �9�& -& 8�� -c d7��$ ��<$�� ��4� ����$ ��3�� ��3 ��� 8�� @��� ��$�% 8��) ����

<�$��0 ( ���� ����4� ����� �� . +�_$& �_� J_(� �_� ,)� ���<_�� (DeZoort, 1997)�� -�9 B�& 81 ��%& ����� -a_� ��$�% 8�� � �(� ��$

J3�� C,$� #�3��� J3��� #���! � (�� ��� '�4� ��3�� -�3 -��)��� >��� ����� �)���3 -�9 ���� . ��� 6;����� -���5� 2$�

(Pincus et al., 1989)& ����� ��% � 81 ')��� ��� ��3��� ��3 ��3� -& � ���� �� �� �� #�3��� J3��� ���! 2�3� -� �%� 81 ���9!�

��)����� 2_�3�� ���! -� ������� ��* ������� ��$%� -� ?�;�� �� ���; � �(� ��%N� ')& -� ���& 8�� �� ���� ���!) � <����-��3�)#

FGGF' .(���� ���(�-��3 (Green, 1994)7�� -�3 -& 8�� �_�3�� ��3�� ��3 -& 81 ���%&� #���� ����4� ����� �� '�� ��� �� ����$ ���! � (�� �7� -� C,� ���(�� ��3� 67*1 �� ����� -& -$�� ���;

�3��� J3�� �74�� -����� . -�_3 -& 8_1 �_��� W"��� ������ PR<3 ���� �� �& ��3�� ��� � � -� ��$�% ��$�. '_(� �$%_� )F (

�, :�_�� �_� �(� �<�3�� �$�%� ��3�� ��3 -� �(7� >9���(7��$�%� .

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

�"#)$ .(�#� ��� �%�&�� '*+�,�% -���� ��� &��".

������ :������ ����.

�_� �_ �(� ���& '_)& -� ��� ��3�� -�3 -K ��4 -$�� B���� ��)��� ��$�%# ��$�%_ ��$�� '��;� 6�4�� '"��� ')& ��& � ��� ��$ #

L�� 2_�3� -� ��� �4��$ �������! -_� �_$� ����_ J_3���3���� .L�� � ����� �� ��$& �(� Rezaee and Lander,1993;)

(Rezaee, 1997; Verschoor, 1992; 2000; Gendron and Bedard, 2006 8_�� ��3�� ��3 -� �(7� ���)&# �3���� ���� J3��� # �_� �)����

�$�% 8�� � �(� <�<�� .

-�� F� QM�

�*M����� �M�

�,� �� GM�����

������ )��1�0�� ���� F�(

��%���*�� �%*�M�

�M��,�� GM�����

��O ������� ���� ���

��2� :������� ��2�� ��� � ���

-� R<3 ,) �� ������ ?�� �_� �_���� ���_�� ���� �_"� ������ �� �� �$��� �� ������(0# ���$ ��� & ��& �� ���� ')& ��

! ��<� �� ��$�) ����# ����1 �� ���4� �����# -_� �_�� ��( ����9 �� ��3��� -�3 -��$� ��)��� ��$�% M(��� '� # ?��_� �� ���� � �3� +,) � $� �� ���3 A��%� >�7� ')& 81 6���� '�

��)��� ��$�% �� ��3�� -�3 ��� ����� ���4� -�3� -$�� ?�$� # ���3 ���$% ��3��� '�������� �"� �� ��$�% ��$�� '��;� ���;�.

!�� '���� � �4 ����5'/�� �0�2� �4 �)���� -�������� ��2�� ��

�$��� �� ������(0 �"� ���% ����� ���� �� ������ �� ��� ����� ����4 ����� ���� �����0� �"��� ?�� ���,3 ���/�

P����� '��9�7 ����� ����� ���3� E����(0 2�3� R�%�1 ���% 8�������1�� 2�3� ��$%� #-����� ���� � 8�� '��� �����

�"��� #������7 ���� �"�� R�%�1� #���3 � �3� ������0 ������ ����# �0���0 �"�)�# ���� 6�� '��� 8�� R�<� 2�3� �4��� 81 ���9!�

)���� L�� #������ ���� 6�� g���� �� ���) ����� ��4� ��� E,� �� ' ���K% -� ������� ����3 2�n& 8�� �$���� ��� 2&� ��$�) ����1 ���

8�� ������ ���3�� ������ #�� �������0 @,3� 6�� +,� �4� <�<�� @��3 ���$ ��/� �� Z���� 2�n�� b�� � ')& ��%� �� ����$��

6��� �4����Y ��� ��$ ��$�% � (�� '��� '���� #������ -��K����� ��* ����$�. ���F/\/TVFV 6��� #_)UT/]/ FGGU ' 7�� '�

R�%�16�� �"�) ���� 6�� '��� @3�� ���� � B�1 ��%� ���� '(� �$�� '����� )'/UG .(����� ���$� <��3��N�� -� ���1

�� #������ ���� 6�� '�������%� � � �� R�<� 2�3� 2�"� . J�������� �74��0� ���� ��0 ����%� �"�� '���� �"�� ?���� #E��!�

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

���� J9� ��� #�$��� �� ���� 6�� ������ ����� ���4� >"��6�� �� �R�;$� ��� -��9� #-������� ����� 81 ���� 6���.

$ ������ �� �� �$��� �� ��3��� � ���� ���� A��( ��% ���$�) ����1� ����� ������ ���$� ���� ��� ���PR� ��� -�

����4� ����4� ���� R�31� #���� ���� ����� �� �$�%� ')& Z��%��) �� ���� � -� ���;��0 ?�� ���4�� ��� �� �� ���� #��3� ,

P����'�� Q���!� ��� ������ ���� � ���� '�)�;�� ?�)& ���� ) #���3� ��<�TVG\_)(��3�� ������� ) #���3� ��<�TVG\_)( #

R�����' '(� �$�� '���� ���� /TF g�����TU/S/TVTF _))T``F' (Z� E,� -������4 -� ���� '��� ������ �%� ����� ���� �� � 8��

-������4 -� ����� ������ �"�� R�%�1SOCPA H ���� ����� �"�) �)� ���?�%1 ������ ���3� ��<� – ��3��� � ���� ���� �����

� �$��� �� �)���� R�4��0) #�����FGGV'.(

!�� ���� ��2�� ��� � �4 ��"� � 3�"���

� ��������� �� �� �$��� �"� �� ����� � �3� ��3�� -�3 ��&� @3�� -�$ �� ��$%� '(� E�<� ��4 )`GU ( ��TF/G^/TVTV _)

6���FU/GT/T``V 01 ' B�&d7��� ����� '#�3� L�� � � �3� +,) ��� 6� �� �� ���4��0 �� �9���� �� ��� �� �� � � ( -�

-���� -������) #� �T``\' Y #E��$T``\' Y #<����T```' Y #����� ?���T``^Y'� <���� -��3�)# FGGF' #-���� YFGGF' Y

#E�� FGGU'( ��( ���& �� ��� ����1 ����9 �� �)��� '�4� �$6��� ��$%� �� A�� E, ��� @���� ���Z���� ( -� �"�� �

-�����4 -� ����� �������� ?�� �� �)� #����$�) ����1� �����4�� �������� ��4; �� B9�����.

��� ������� ���� ���

!���� �/ 6�7�� �8�);<� ( >��'���/@/�!�!A�

���� ��K� '(� E�<� ��4 )`GU ( ��TF/G^/TVTV 6��� _)FU/GT/T``V -�3 ��$%� �9�4 ��� �$��� �� ��)��� ��$�%� ��3

���3� ��<� ��, � �� ���3 ���1 �� ������ �� �� ������� �"�� -������4 -� ����� ������SOCPA ����4� �� ����;%� Q���! <�<����$�% -� A�� ,� ����.

��4 ,) C�� �(� E�<����� ����3� �_�3 '�_�� �_���� �$�%�@���� >�%�� '��� +,) -� -� -�$� -& 8�� ��3�� �_���� �����4

@���� ����4� �� ����4�� ����7�. h,�_�� ��_� ��$ E��_%���0 E�<� ��4� 6���� �9 ����� R�9�& �����9� ���� ��3�� ��3

��3� ��� @���&� ) -�9 -�� # �_�� �_� � �9_ +, ) ���_3� ��<� #������TVTV_):(

TH -�$�� �$�% ��)��� -� -�$� -& -� �4� 0 '��� -� ���FG �P��� ��� -�$� L�� � R�9�&P���� ��3� � ��7� -� �4� -& <�3� 0� #R�9�&.

FH -� ��3� �9� -�$� 0& R�9�& 2�3� ���! -�� �& -��,�;�� 4� ���%��0 �� � 8�� �� �$�% �� E��1 �& ��� ��� -���.

UH -&� B -� �9;�� #�� ����� ���� ���4� ��4�� '��1 8�� -�$��3� ,) �� @���� ���� ��)K�.

VH �� ��%� � ��* �& ��%� � ����� ��3� �9� -�$� -& <�3� 0 ������$�% @��� '�� �� ��4�� .

8��� ��3�� ��3 -& 81 E��%���0 h,��� ��%& ��$ :�_� ���� �$�%_� ����� � �(� �R�31 ������� ���;$# ���_��� E& Z7��_��

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

2�3� ������ ����������1 �$�% . 81 ���%! ��3�& ��$�%_ �� -��3 ���� ���( ����� �����4 @���� >�%�� ��3�� �_�$ B����7�

�4� E�<� ��4 �� ��� # �_�3�� ��3 ��� -a� :��& ��$�% �� ��&� '��� +,) :������ ��3� $��� �4�� 2�3� -� ���!� ���! ��,�;��

�$�%� ����� � �(� '��� �� ���� �$�%� +������ B�����# C_, ���%�� J � ���� '"�4 ��3��� ���� ������ 8�� �%(���� �)����� � ( �����

����� ������ ���� '"�4 �� �����4 @���� '�_�� 8_�� B_����7� ����� �$�%� ����� � �(����! J��� �����4�� ����� ��<7 ������

2�3����!�����0 R���1 -���� 8�� �4��� 81 ���91 �) J3�� ����� '��4�� +����4� ����� B��� ���3 ������ B���� ������ ���� �_�$ #B"�&

�_� ���� �� �(� ���3 -� ���� ����7� ��3�� ��3� '�4� �),_�;����� '���� ��$�% '��� �� ���� �K%�� ��4� -� �$K���K%��� ��.

�@���� >�%�� 6���� ���� �����4 �$�% �� ��� ��3��# ���%& ����%���0 � �9 8�� -& 81 ��3� -� ���� -� ���� R���& >�%��

������ �R�;$ �$�% �� ��� ��3�� 8�� ���4 '��� -�� -������4# ��� '� ���1d���4� d0��3 �$�% � ���� ��3�� ��3 81 B����� ���� @��$�

2�3� 8�� ���� ��$,� ��3�� ��3 C, �� ��� -& 8�����! ���� -� � P ���� >%��� ���4� ����� ������� ��7��P�����( � ��3�� ��$& �&

�$�% �� ���##>�%�� B 3�� '� E, 2��� -� �� '�4� '� -�� 2�3����! ��� ��3�� ��3 -� B�1 ������ ����� ���� ����3 8��

�$�%�d�� ��'�9��� ���4� -�, -������4 -� ���� R���& # '� -�� ��3�� @���& -�� � �$�% �� ��� ��3�� ��3� � ( -� '���%��

>�%�� B 3�� '� E, 2����#P ���� ���� ����3 -���� �P�����( � ��$& �& '���� ���� '��m��$� ����� J� �$�% �� ��� ��3��. � �9 +,) �����

��� ������� ���� ���

L� ��3�� ��� 8�� ��$K�� � ��� ����� ���� L7� -� ��<� 0 ���� 2��� #��;�� �����( @���� -� ��$& � ( -� J3�� �� ��$�%�

� J3�� �� ��$�%� � ��� ����������( @���� -� ��$& � ( -.

��7�� 6 � ��� >�%�� 8�� @��� -�$ ��3�� ��3 '��� �3 -& '� E, 2���� ����( ���� ��� �$�% �� ��� ��3�� �����4 @����

3�� B ,)>�%��.

!���� �/ 6�7�� �8� B�2�' -�2��5);<� ( >��'���/@/�!�! A�

� J(� �� '(� E�<� ��4 B3)`GU ( g���_��TF/^/TVTV __) 6� �� ��� �� ��� ��� �$��� �� ��3�� -�3 ��$%� Z��# L��1 -

�_ ���� ����� -�3 C�� ��$%� -� -$��� ' ��$�% �� # �� _� �3��� J3�� >�%�� 8�� �4� B�� ��3� ��� ���( ��� . ��_� �_(�

�� 6��� ?�$� � -� _����� ������_ �_"��� �_�3�� ��3 � ( -� -������4 E�<� ��4 ���� �_��� ��4� �� �� ��� +,) B�1 ��%�

) #-������4 -� ����� ������ �"��FGGV'( :

&H ��3� ��� 6���� '��� Q�9� '��# >�%�� ���� 8�� ��9� R�;�$� @�����4� �����4#'���) E& �$�% �� ����� � �(� A�9�� ��� '� .

@H '��1 '�����1 �� � �$�% R�9�& '���� ?�)K ��3�� -�3 ��3�� -�3.

hH :� �74��0 '��;� Q�9� '�����1 �$�% � �� R�9�& -�3 ��3��.

�H ���$ ����� ���� ��)K� ���� '�� �� :� R�9_�& -�_3 ����� ���� '���� 8�� '���� '��� ��3��# �, ���_�� � $��

�$�% ����K �(7� .

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

_)H E�<� ��4 B 89( �� 6� �� -� 64��� �� �(� ��& ��3� '�� '(�)`GU ( g�����TF/^/TVTV_) .

�H �_���� �����_;� ���( J9� ' ��$�% �� -& -�_3 �_����3��# �_) ��$ E�<� ��4� 6��� E��%���0 h,���� �;�$ ���1�

����� E& -��.

<H �_���$ ���� ���� Z���� @�3� -� � ��<�� � �9 ��3� '�������� ��3� '��4.

!���� ����8� C���"�� ��� � -���� �4 ��"� � 3�" . � � &$ �

8�� R�� � ��_4 �_��� ?�$� ��� 6��� ���1 ���� �� W"��� '(� E�<�)`GU ( g�����TF/^/TVTV _) #�4 �� ��4; �� ���1 ��%��

P���� �_�3�� �_�3 �_��( �/� ���)& -� ��3�� -�3 A�9�� �� �����# 2_�3� -� �4� �� ���; -�3� :��1 �)� ���1 �_"�� # � �_��

'(� E�<� ��4� ����� ��3�� -�3� ����� ���4�)`GU ( g�����TF/^/TVTV -�3� +,) -� ���%�� ��"�; 64�� �� �)������ _)# �_;�$�

��� 6��� ��3� Z���� �(� #���� +,� '��4� -���� ��� 6��� �_� �) � 7� �, ����1� L�� &� ����� -� ���� #��3�� -�3 ����K �(

�����) #-������4 -� ����� ������ �"��FGGV'( :

TH � _���� ���N_� �_� ���4� ��3�� -�3� ��� �, L�� � '�� -������4 -� ����� ������ �"�� B���� E, ���FGGF'.

FH E����� ��3 ���4�Treadway Commission �_� ���� 'T`^] ' -�9� E,�1��: �%� � ��3�� -�3� 6���� ����� # ����9 �)<� & -��

��3�� -�3 ��� '��� ���( ���1# J9� ����� ���%�1 ���4� -�9�� ���4 +,)) Treadway, 1987( .

��� ������� ���� ���

UH �$���� ��� 6�� �"�) -� ����� ���4# �_� ��� '� ��� '��FGGG'# ����� -� ���4� '��4� ��3�� ��3 -� ���4 +,) @�����

�4� <<�� ��� �� ���( �� '���� ��)��� ��$�%� ���� '"�4 ��.

VH '�� �� ���� ���4� -� Z���T``` �_�3 -� ' - ���_� Blue

Ribbon CommitteeA�9�� �;�$� ��$���� ��� 6�� �"�) -� �4� �� ���� �%_� �_�3� ���_(� #��)��� ��$�% �� ��3�� -�3 ������ <�<�� � �

'�� �� ��� '�� ��$���� ��� 6�� �"�) � ( -� ���� � '� ������FGGG' .

SH 2��*& �� �$���� 2�3��$ -� ���� -���4 Z���FGGF ') 2�� ��� -���(H '�� ���$�& FGGF'(#89( E,� 8�� � �(�� �"�) ��$%�

�_��� ��$�%� ���� '"�4 -��3�� -�, -������4 -� ���� R�&# �_�$ ���� �$�% �$ �� ��3�� -�3 R�%�1 @�3� ��$,� -���4 89(.

\H '�� �$���� -����� -��3�� ���� -� ���� @��$FGGG ' -��� )��3�� -�3#�� '�� -��%�� E��� -�4 �� ��3�� -�3 �.(

]H �$���� -����� -��3�� ���� -� ����� ����� ��3�� ������. ^H '�� ���� �$���� ����� � �(� Z�� ���4� �����FGGT'.

'(� E�<� ��4 81 ���9!� FFT] g����� T/TT/TVFU -K% _) �� E, ��$K� ��� ���;$ ��� �$�% +�# �_��� '"�_4� '�� Q���!�

-� ��� ��� #��)��� ��$�%� -������_4 -� ����� ������ �"�� -_��(7� �, ������.

��( -�_3 �_�� �_���� ���4 �� ��� ����a ��� 6��� 8��& '(� E�<� ��4� ������ ��3�� `GU ��� g��TF/^/TVTV)_# 8_��

-�9�� -&��� ��) #-������4 -� ����� ������ �"��FGGV'(:

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

TH 8��� ��3 ��)��� �$�% �$ �� �$%o�)��3�� ��3 ( ���� 2�3� Q��( 8�� PR�� �$�%� ���� ����3 -� ��( ����� ����� ���4�

���!# Y���4 +,) J9� ��� -����� ����� ���4� 8��& ��$ '<�0�4��� ��)��� ��$�% �� ��3�� -�3 ���.

FH '�4����! -� ����� ������ �"�� J� 6����� ��$�%� ���� ��$�% �� ��3�� -�3 ��� ����� ���4 6� �� �� ��� -������4

���$��� ��)����R�3!�<7 P���� ��.

UH 8�� -�������1 +����� E, h,��� 6�� E��� ��$K� ���1 �$�% ���! � �(� '��� ������� ���;$ :�� -� ���3� ��<� ��$�%� ����

�$�% �� �����# ��3�� 8��� E, �$�%� �����4 @���� 8��� �$�%� ���� '"�4 ���4� '�4� -&)�����$K� Z ( �� ���� B�&� B 3�� -� �

-� ���� ��$K� B��9����1 � �(� '��� ������� ���;$ :�� ��� �$�% �$�%� ����� . -� ���� E��� ��$K� �%������1�$�% # ���4��

�����4 @���� -� ���� Z�;# ����3 81 ��3�� ��3 ���4�� �%� ���� �� B�1 �"P�����" 6�� ��3�� -�3 ��� ����� ���4 -�

2�3� ���4����!P���� �)�%� '�� �� ���� '"�4� �.

VH ��3�� �����4 @���� �� '�4� �� ��3�� ��� ��<� 0& -���� -� ��)��� ��$�%� ���� '"�4)U ( � ��� ����� ���� L7� ��$�%�

��;�� �����( @���� � ( -� J3�� ��#� )S ( � �_�� ����� ���� 2�� �����( @���� -� ��$& � ( -� J3�� �� ��$�%� . ����� ���� ����3��

��_� ��_;�� �����_4 @����� �& -� ���� ��K ��;��0 ����9 ��� ��� ��;��0 ��� �� ����� -& 8�� #���& P _���� ��_;�� �����4 @���

P�����(� ��5 # 2_�� -_� �����( @���� E� ��3�� ��� ��<� 0& ��% � ������ ����.

��[ ������� ���� ���

����3 ���4 ���9� �(���)��� ��$�% �� ��3�� -�3� ����� ��9��� ������ ����� ��3� ?�� � �(� '��� ���;$ -� 64��

�� �����E& '��4�� #�����; +,�;� 2�3� ���������! ���;� ���K% -� �$�% ��*& 64�� �� +������ '���# -��)��� >��� �����

��4�� �;�$�� ���� �R�;$ -�������� ��3� ��� 6��� ����� 81 ���9!� Y���� �� �4��) #-������4 -� ����� ������ �"��FGGV'(:

TH ��_/ �)�%�� �)����� � ( ����� ����� ���� '"�4 ���� �_�* ��_����� �& ����� �& ��� � E& -�9�� 0 ���K ����( 81 ����

�� �� ���)& �, �����# ������� �& ����� E& '"�4 +,) -� ?,�� ' B�&� -�$� -& ���,� -� W��� �� �� ���)& �, i� � �&���9� ���� '"�4.

FH ���� E&� �_)����� �_ ( �$�% �)�� �� �� �� ���� ������ ������ +,) �� ���/�# d,�& Y���K% �����4� -� ��3� +�� �� '��4�� �_�

7� :�� �� ��0R 8_�� �)��&� �K%�� ����& ��� � �� ���� ������ ����� �K%��� ��� <$�������& W"� .

UH �K%�� �� �� �(� ��%�� '���� ���;$ -� 64��# ������� R����� M/ A�(� -� �� -� -$�� � ���� �4��� �������# ����%�$�

���3 -� 64�� -� -$�� �4��� �� �(� ��%�� ,�;�� ������� #����(� ���,�;�� �� �� �� �� �(� ��%�� ,�;���) .

VH ?�%! �_� R���� �& M/� �(7� �, ��4� ������ 8�� ����4� ���)& ��3� :�� :��& ���& E& �& #�$�% �� J4�.

SH ���� �����4 @���� ����4� �� ����7�� ����4�# -�_$�� 2�3�� �3��� J3�� -� ��� �4�� ��3����! �� -$�� �� Y J3

2�3� � ( -� ����K� �& ���( E& -� :K�� B��� '��4 -� �3������!

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

����1 �$�% . �_��� �_��� ���� �����4 @���� Q��( ��3� 8���� d4 � �$�%�� ���4 +,� �4��� �����4 @���� ����� �R�3! # 64���

4� �� ����� ����� -& -� 8_�� ����( �$�%� �����4 @���� ���� @���� ����4� �� :��� ����� ������ �$�%� ���� '"�4 ��3��

d,�;�� �$�%� �����4 ����� ������ �� ���� . �<_� �_�3� Q�_�4� �_�$ �����4 @����# @� �� -�� J� # �_� �����4 @���� 6� 8�� ��;��

�� _(� �� ���/� '� ,1 +���/� @ � B ��� ��9 E& -� ������ � � ��� 4� �� � ��/ �& 6"0 ��*.

\H -����� -��3�� ��74�� -� 64�� # ��3�� ��� ��� ����� �$�% �� �����# �_��� ���_� �� ����4�� Z�; 6���� # E& '��_4��

4�� ��$K� ���K% -� �����4� -����� -��3�� ��7D �_� �R�_;$ -� J��� ��4�� �;�$� � ����& -� B -���4� . 2_�3� -� �� ��� �4�� ��3� -�$��

���! -����� -��3��� . �_;��� >�_%�� �� �� ���� ��3� '�4� ��$ _�� �_�<�� �0�_ � �m_��$�� �$�% �� ����� ��3�� ���� :�

��$� Z�% >�%��� B �������"7�# @� �� -�� J� # �_� �_��� ����� ��3�� ���� ��� R���1# R�_;�! �& <3� �& ��4��0 @ � PR�� #

�� J��� 2�3� 81 -K% ,) �� ������ -� B�1 ���� '�����!.

]H �$�% �;��� '�� -� �$K�� '<�� �� ,��� ����k ����� -���4� �$��� ��.

^H -��4��_� -���%��� �3�� ��� ���$ ������0 ��_��� '�_�4�

'� ���& ������ ������ ,�;�� 8�� ��3� ����� ������.

���3 A��%� -�9� ��$ ��3� �9� �� �)���� @3� ���% L�� -� ��3�� ��3 �$%� -& 8�� Z� )V (�9�&R�(� 8�� # -&�

��O ������� ���� ���

-� �4� 0 -&� '��� -� ��� -�$�� �$�% ��)��� -� ���$�)TGG (p0& ����%� '�� -� ��$& C��� )S٪(�$�% '��& -� . ���� :� -�$��

�� �& � ���� �� +���$� �3�� 8�� d7��� -�$� -&� '"7� ���� ��)K�������#�� ��3� �� ����� �� �� J� ����3�� �3��� #��3��� � ��

���� 2�� �� �# 2�����$ ����% 8�� d7��� -�$� -& -$�� C,$� 8�� � ����p0&���� J � -� B�� � �4� ��3� ��#� 8��� �9 p0& J�3�

-� �4� �� :��& ��3 E& ���9� ��3�� ��3 �� B���9� @��3 81 2�3����!#p0&� ��� ��%� �, 2�. ����� � �9 81 A��%� 6����

��)��� ��$�%� �����4 @����# -� ���� ��3�� ��3 >%�� -& 8�� ���4 '��� -�� ��$�% �� ��� ��3�� '� Z��� -������4 -� ���� ���� '� B3�� �$ C,� ������ �R�;$ �$�% �� ��� ��3�� 8��

���$�% �� ��� ��3.

��3 ��3�� -�3 � �9 A��%� -& 81 ���%! ��3�� M(�� � ( -� ��3�� ��3 -� -����� 81 ���& '� ������3 ��� �����$��� -�

����"�� R� ! -������'B��� '�����7�� #��� � R�9 8�� B�*��� ����1 2�3� 81 J�� '� C,���1�"�� #� �"��� �$% +����� B%(�� +��� E, .

) -& ��7�� A��%� ,����$ ��3��� ��&# ���� ���$ ��� ��R�3! �������a 6 �� ��4 2$� ����� ������ .

!�� 3� � ��� ��"� � 3�"� -���� � ��� ��#+ .��+'� ��� �4

������� ��2�� ��� �E

d4 �� ���%&� ���� +,) �� ) ��4;UHU ( -� ����� �(7� C��) -& 81 ���� �;� ��$�% ��$�� '��;�� ��3�� -�3 . ��$& -& 8_1 �9�& ���%

P���3 C��) ?�� ���� :���� 8�� ?���� �� ��$�% ��$�� '��;��"� ������ . �) ��) B�;� Q��� E, �N��: ?_���� -$�� ?�$ +,_)

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

�_� �� �_$��� �_� ��$�% ��$�� '��;� ���;� �� ���3 +,)� �(7�������l. B�� C%0 ��� 8�� 8�� �3��� <$�� ��$�% ��$�� '��;� -&

��$�% �� � �(� @��3# ,_) 6_4�� �_�5 -� L� -� � 0 ���� � #?�� ��)� � ���)& <� ���$ ��3�� -�3 ��� � �(� ���5 ')& ��& ���� �

��$�% ��. & 8_1 �� _ ��%& �(� ��$�%_ 8_�� �_ �(� ��9_( -(Corporate Governance) �_)��� -_� �)��& ���� ��$�% ����� �����$ P9�& ����)��� 81 #� �(�� #��$�%_ ��� �� ���� ������ ����� ��

�_� �_���� ?�)� 6�4�� �� C,$� :(Demirag et al, 2000) #) <�_����-��3�)# FGGF'.( ��$�% ��$�� ��"0 A��%� R�3 �(� ��_� E,_

P��N� �$��� �� ������ �� �� ��� L�� #�(7� +,)� ��� ,) �$N� �%� �� � ����� �_����� �_�3�� -�3 ��$%� �4����� A��%� -� ��c 8�� ������:

&HR�9�& ��* -� ��3 ���! 2�3� �$%� # -��,�;�� ���! 2�3� 0 ��3�� ��3 8��� R�9�& ��7� -� ��"�9�& ��� �4�# Z��� '��� -�

�� ����� ���� -�N%� .

@H�$�%� ���� ����3 ���� # ���! 2�3� -� Q��( 8�� R�� �� ��3�� ��3 R�9�& ����� ���( '����9� ��@���&���3� ��� .

hH��� �� ������N��� ��3�� ��3 ����� ��%� : TH�$�%� ����� ��3�� ���1 8�� ?�%! # -� 64�� ��/

���! 2�3� � ( -� �� ����� ������ ����� ,�;�� �� �������� :��.

FH����� � �(� '��� ���� #���4� J9�� ���&� -� @��$� B�K% �� ���������.

UH �R�3! J9�� ����� ��3�� ����4� ���� ��������� .

��� ������� ���� ���

VH���! 2�3� ����� -������4 -� ���� -���� #'����� # ������ '� ���&#'���74�� -� �$K� -����� ����� ��� 8���� .

SH �� ��� ����& -� ���� 8�� �4���� -������4'� ���&����� C�� -� . \H�3��� J3�� J� ��3�� ��� ���� # R� 1������ ��������� .

]H '� �� �� ���� ���� '"�4 8�� �3��� J3�� ������� ���� ���K% ��.

^H ���� '"�4 ���������! 2�3� 8�� ��9�� � ( ������ ��# R� 1����K% �� ������ E&� .

`H�� �� �� ���� ������ ���� # R� 1� 2�3� ������ E&� ���K% �� ���!.

�$��� �� ��$�% ��$�� ��"0 A��%� -K 6 � ��� >9��� 8�� <$�-� ��3 -���� :��� @��3 -�$� L�� ��3�� -�3 �74�� ���)& �9�&N� �)��,�;�� ��* ���! 2�3� -- �$ ������ -�3� +,) J�����

����9��� ���� �$ �)����4� '�4�� ������P��� ���! ��/9 -� . �� ,)� B��$& �� J(��� #������ L�� ���� �� � 8�� ��%& #)O'Sullivan,

1999($�% 8�� � �(� 6�4�� �"��� ')& -� -& 81 ���� ������ �� �� #���! ������� C��� � (�� ��� '�4� -��,�;�� ��* R���� ������0 -� ��3�� -�3 -��$� 8� �� ������ ����� ���3 ��� E, ��� �)�

-��,�;�� ��* R�9�&.��$ ��%W��� ��� )Weir and Laing, 2000( ���)& 8�� '�4� E, �����* R��� B ��"� �;��� -�$ -��,�;�� ��* R���� �

�) -��,�;��: ������ 6� �� -���4� -��,�;�� R��� -& -� � ��� �$K� -��)��� >��� J� �4;�� . -��;� -�$���� -��,�;�� ��* R��� -a� C,$�

#� �(� ')��� R�& -� '��$��� ���� :74�� #'�� #�$�)� : ���% '�����)

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

6�� �� ')<$��� '����� )� <����-��3�) #FGGF'.( ��& F$�"��$�)� ��$�% �� ��3�� -�3 8��& A��%� -& �)���� ����7� ��3� ��

8�� � �(� ��%�&� ����&��$�%� ) �� J(� �� ,� '��� '��;� ���;� <<��� ��$�% ��$�������� �"� �.

�� �( :-��5�'�� G0�'$� ���� �5�(�

?����,)+ ���� �%(���� ����� A�9��" ��$�% ��$�� " E,_� ���)� ���* �� ��� L�� ��_$� '�_��) 8_�� ,������� -� -�_������

�)��*� ����� ���3� ����� ������� ����� ���� �� ����# J��� '"��� ')& ��K$ ��3�� -�3 8�� <�$ ���;� '��;� ,) 6� �� �_"� ��

������ �� �� �$��� . ���� ��� �(� �_� ?7�_�0 -_� '*�� B�& ��$�% ��$�� '��;� ?����(Corporate Governance) B _% C�_�) -& 01

,) �� � ���)K ���� �� ?���� @� �� ��� A��31 B_4� ��� '�_�;� J(� ��& 8��. � 81 ���� ���%& -& -_� ���� '�_� ��� �_��4��

����� �� � ��'��;� �� ��$�% ��$ �� _ ���� �� ������0 �� $ :� $ ����� ��$�%a '$ ���� -��� ��� �_�$���� ��_��� ���0

�)��* �� ������ �0��� ��� -� *� ��_� R�� -��_�� �� ���� ���� ��$�%� E��!�J������ ���� ���<� C�� -� ��<� A�(� .

�_��� -_� '*��_ B�& ���� ��� �4� �$��� �� J9�� � ��� ��& d$��� C��) -& ��7� B�& 01 ������ �"� �� ��$�% ��$�� '��;�� P��_3

� -����� � ( -� B4� �� ��;�$� B ��3 8�� ?���� '��;� ,) Q�% ���� A��( ������� E���� # �_4���� ���4 �� ���1 �7� -� C,�

'�� <�<��� �� ����;%� Q���! ���� ����4� ��)��� ��$�%�# �_4�� _� �_���� L� � '��;� ,� ?���� ?�� ���4���� ���� �� :�

������ �"� �� B4� ��.

��� ������� ���� ���

����;%� Q���! <<�� ��$�% ��$�� '��;� �� � -& ���� ��$&�. ������_�0 @�3 ���3 �"� ����� 8�� ����� E, ��� �_� �����_��

���� ������0� ���<� J��� ���; � ���� . ���� +,) �%(�� ��$ -�3 �$�% �� ��3�� ��)��� �# ����� � �3� ��� -�3� +,) -��$� -& ��� �

E�<�_ ��_4 @3�� 8�� ���� ���� L�� �$��� �� '_(�`GU g�����TF/^/TVTV)_ )T``V' (01 �3� ���& � �$�%� �� �� ����

'���� �����( 8�� ���& �)��� �� '�_� C, -�� #���1 ��$�� Q�_9� �� ?�)& ��� 6���� '�� C��3��- 6��� ��$%� 81 E�& E, ��� �_��

������ 8��� �����4�� ������ �� ��� ����a -�3 ��� ����� ���4 '(� E�<� ��4� ������ ��3��`GU ���� ������ �%(��� ���� ��

��� 6��� B�1 Z��� ,) �� ������ -� . �� ���%&� -& 8_1 �_� ')��_� ?�_� ��)��� ��$�% �� ��3�� -�3� ����3 ���4 6� ��

1 ��$�% -� A�� ,) 8�� � �(� �� �� �3�# '_�� 8�� 2$��� E, ��� ������ �"� �� ��$�% ��$�� '��;� ���;��.

'� �� 8�� R�� � -a� W"��� -� B�1 ���� ���� ������ �� �:

T. 8�� ��� ����9R�%�1 ��� ���� <$�� � ���" ����_ <$�� ��$�% ��$��" ���� B���$� �� C��%�� -� �$ -� - ���� � (�� -���#

� -������4 -� ����� ������ �"��# ��� 6�� �"�)� # �����_�0 �_"�)� # ����3� ?�/ -� -����� 81 ���9!� ���������� �_(7� B_ �� �$ 8

����N_�� ���� �4�� #�$��� �� ��$�% ��$�� '��;� 6� �� ���;� ���K% -� �� ����� B���)& 8�� ��$K�� '��;� ,) �%�# ! W"���� �_� �3�

8�� @���� �� ,�� B :���� 8�� Z�_�� '�� -����4 �_"� �_� ������.

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

F. A��! �3�� �� >"��� ����� �) ��$�% '���� �4���� C�� ���� C�� � (��)���� ���; �� ���� J� 'R7�� �� �� ��� 4���� ���# � <<_�� �_�

����;%� Q���!���� ����� �� # �;$� � ����� 6�4�-��)��� ��/�.

U. �, ��"�� -� 6����� -���� ���)& 8�� ��$K� �_"� �_(7������ �$��� ��$ -������4 -� ����� ������ �"���# ��_� 6�� �"�)�

� �"�� ����������7.

V. _ ,�;�� �� ���� ?�%O ������ ��9� ��5 ��3�1 ����9 � �9 �3 ��$%� ����3- �_�� �� ����� 0 8�� ��)��� ��$�% �� ��3��

���4 ��$.

S. �$� ��)��� ��$�%� ��3�� ��3 -� -���� ���)& 8�� ��$K� �3��� J3��� ���� J3�� -�. <<�� E, ��� ����� 8_�� � �(�

��$�% +,).

\. ��_��� W)�_�� ��� �� ��$�% ��$�� '��;� ����1 ����9 � <�$�� J� ������ �����3 �� � ���� '��(K �_�� M�� �_4� 8_�

����� ����� �0���(Case Studies) ,_� �_�4� �� @_��3 Q�%������ �"� �� '��;�.

H"� �

/�� :�%�-� 0����

����� 1�2-� �%�) �����" ( � B#�� �%�1 ������� ����� .. ���M#�� =; L�"�� L�B�: G��%�+���"9 ����� ������� � ������� ���%��*�� �+� �%��'�M 9-���B�� 9. *���#� 1�����13��%� 1����) �����" (�%#������ ������� :Z��#�� Z �#��"9

E-JournalUSA ������� ���� ������� ���� �� ��� ����� ��%���� 99 �%��*�� �,1��.

��� ������� ���� ���

*�*-��%� ���� 14��%) �����" (�*M����� 5�M� :�*1�� ���M#�% " �%�8# ��1� -���*�� -� �� ��1������� �� �� ��������� ������ !�� �� �"��� ����#��� $���%� ����&��� 9

�*1 >��� �*��M– �%+B�� a�� –� �+#�$� �%� -�� F� –��1����� �1� . 5��� ���� 6��� ���� 1� �) ���[�" ( �16�� ������ �� ������� ����� �� :�'M�

�%�1��� �H" 9'����� (����� ������ ��)��� *�� !�+� ,-�. /����� ����0�1

��&��� 2����� �% �0� ��#%&�� �*��M 9– 9�%�� F� ��*��� �+#�$� �%� ��b�� 5��; 9�%��4–5 �0� .

�� ��� 1������) �����( �%;� �F� ��1����� “Creative Accounting” 9����

���������Q��� 9. �� ��� 1������) �����" (�*M������ ��1����� �'� �� �C% ��� ����8#�� ��

�% �*1�� �%��*�� ������" � ����-��� �������3����4���� *�� 978 &�'M 9 -��M#�� �%� 9@������ �%*�� ��1�� ��–-���B�� �*��M c c 9: ���b���.

���� 1�&�#) ����� ( ������������ : �� B#��� 7��1Y� ��1��� ����� �'1�� ��*+ ^�A���� 7��1Y� ��1��� �����" 9������ ������� ������� � � 9-���B�� 9

�%��*�� �+� �%��'�M. ��� 14*�9) �����" (�%��*�� �+� �%��'�M �� ������� ����� �%%B#" ��; ���� 9

���)O�( 9(���� � ���������� �������%� 9�%��*�� �+� �%��'�M 9-���B�� . ;��<��%� ���= 14��") ���[� ( ^5� �� D��+���� ����1��� ������� �� �����������

����-��� *�� 2�%��� 9��1���� �% �*1�� �%*�M�� 9)>(c c 9: �[ b��. 1������3�?�%@������%� ) �����" (�%���*�� ������� QI�: *�..� ��B#1� 5; �?�

�*M����� 5�M�" 9����-��� ���� *�� 92�%��� 9��1����� �% �*1�� �%*�M�� 9)8A( 9c c: �� b�O.

�- ��%� 14��2��) �����/4( "Corporate Governance: ������� �� �BC�� %*% �� ���*��"����-��� ���� .�%��� 9��1����� �% �*1�� �%*�M�� 9 *�� 92)8A(c c 9:

��b�[. �- ��%� 14��2��) �����/<( "��'6� �*6 54 5��% D%�: Corporate Governance

�% �*1�� ������� ��"����-��� ���� . *�� 92�%��� 9��1����� �% �*1�� �%*�M�� 9)8B(c c 9: �� b�� .

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

�- ��%� 14��2��) �����/`(" 7%�8#� � ;F �% �*1 �A%� Q%1N#� -�; Saudi

Corporate Governance" 9����-��� ���� 92�%��� 9��1����� �% �*1�� �%*�M�� 9 *�� )87(c c 9: �� b��.

�- ��%� 14��2��) �����" ( 7%�8#��L��MF��% �*1�� �%��*�� ������ �� ������ ������� " 9����3� !��&�� ���&�� ������ M� 9�%���� �*��M 9�C ; 9)8(9 c c:�O�b���.

D�%� ���� 1�%���) �����" (��I*�� Z�? G� �I��*#��� ������� ��%'�" 9����

����-��� *�� 92�%��� 9��1����� �% �*1�� �%*�M�� 9 )87(c c 9: �[ b��. �� �@ 1*��-�� E���) ����� ( ������� �� GM����� �%%W#� ��%#,� �� -�CR��� ����*������1��� �% �*1�� :%� �1�� 9-���� �%S �%#1M�� ���1� 9�%� ��1����� �1�b

� �+#�$� �%�-�� F�- M 9&%&*�� �; >��� �*��M 9. *��-��E��� �� �@ 1� ����� 1�� ��?) �����" ( �*M����� 5�M� �%��*� 3 � ������� ��

�% �*1�� ����1��� :�%� %� �1�� " 9 ��0� ��1����� ��#R�� � B� @��" ��6� ��

�6������ ����7��%� ����- �� ����-���". 5��H��� : 5%�1���� �% �*1�� �A%'�� 5� -�#6�� �� 981�0� 7���� 5%%�� �� 5%%���#1$� G� 5��*#��� 5%%��B���b� 5��*�

������ b 7������ �b� ���#�4 ���� 2�%��� 9�–�% �*1�� �%��*�� ������ . ��=� ����� �����#�� *"��) �����" (������� ����� ;��� �� +: 5*# �+�" 9

�� �� �� �- :�"����� ���8��!��� ��+��1 /��� 9���� ;�� �� ���� .

.9���� ;�� � � ����� �� *��)>(Q81S4 99c �. ��� D�%� 1F����13�?�%@ ������%� 1������ ) ���O� ( �%%�*�� �*M����� 5�M� ��'�

��'A�";4 ��%#, : 9�% �*1�� �%��*�� ������ �� �%B%�8# �1�� <���� �&��� ����

���&����� =���3�� �����%� ����� - M 99c c :�� – [O . ��������� ��% ����� ���- � G�+�9 �������+�� �����-��� !�>� 9����� � �+�� ��1�� 9���

� ���/��9d%��#� ��/�/������9 �%����% �*1�� �%��*�� ������ 92. ��������� ��% ����� ���- � G�+� )�����( 9�*M����� �M� ������ ����+�����>����

� ����� �� �&����� ���� /�&��% �*1�� �%��*�� ������ 92�%��� 9. '����� '�*�) ���[�� (�� $���3�� ?&�� ��&�� ������� ����-��� !�"�#�� @��"1!�& 9

��� Z��&��� ���B��[�� �O/�/���[ ��� Z��&��� ���B��� 9 ���#1I� ��O�� d%��#��/��/�����% �*1�� �%��*�� ������ 92�%��� 9��&�F�� �� .

��[ ������� ���� ���

'����� '�*�) ���[�� (�&����� ���&� ��� Z��&��� ���B�� 9[�� �O/�/���[ �� ��� Z��&��� ���B��� 9 ���#1I�O�� d%��#� �/��/���� 92�%��� 9��&�F�� ��

�% �*1�� �%��*�� ������ . '����� '�*�) ������ ( ��� Z��&��� ���B����� 9��/O/�����"�B�� �� ���� /� ��

�������+�� �����-��� ����� 9���8 ���-�� �&����% �*1�� �%��*�� ������ 92�%��� 9 . �%�-� ��� ���+�� 1���H� / '�*� )���[�( 9A�9� �� �� �- �(���� /���

���&�� �� ���6��� /����� . ��� �% �%� 1�%��) ���[� ( �� ����1��� ������� �� �*M����� 5�M� �%��*� �� ��

�% �*1�� �%��*�� ������ : 9�%� %� �1�� ����&�� ,�-��� ������ ��� ���� 9�%� �1F� M��� 9 88 9 *��) �(9c c :���b �O�.

59�� 1�9���) �����" (5��� �� ������� ����� &%&*# �M4 5� "������� � �

������ ��������%��*�� �+� �%��'�M 9-���B�� 9.

����H :�*����! 0���� Birkett, B.S. (1986) “The recent history of corporate audit committees”, Accounting Historians

Journal, 13(2): 109-124.

Blue Ribbon Committee (1999) “Report and recommendations of the Blue Ribbon Committee

on improving the effectiveness of corporate audit committees”, The Business Lawyer

54(3): 1067-1095.

Cadbury Committee (1992) Report of the Committee on The Financial Aspects of Corporate

Governance. London, Gee and Co. Ltd.

Collier, P. (1996) “The rise of audit committee in UK quoted companies: a curious

phenomenon?” Accounting, Business and Financial History, 6(2): 121-140.

Demirag, I., Sudarsanam, S. and Wright, M. (2000) “Corporate governance: overview and

research agenda.” British Accounting Review, 32: 341-354.

Dewing, I. and Russell, P. (2000) “Cadbury and beyond: perceptions on establishing a permanent

body for corporate governance regulation.” British Accounting Review, 32: 355-374.

DeZoort, F.T. (1997) “An investigation of audit committees' oversight responsibilities”,

ABACUS, 33(2): 208-227.

Estrin, S. (1998) Corporate governance, state-owned enterprises and privatisation. In: Corporate

Governance, State-Owned Enterprises and Privatisation. Paris, OECD proceedings, pp:

11-27.

Gendron, Y. and Bédard, J. (2006) "On the constitution of audit committee effectiveness",

Accounting, organization and Society, 31(3): 211-239.

Green, D.L. (1994) “Canadian audit committees and their contribution to corporate governance.”

Journal of International Accounting, Auditing and Taxation, 3(2): 135-151.

Macdonald Commission (1988) Report of the Commission to Study the Public's Expectations of

Audits. Canada, The Canadian Institute of Chartered Accountants.

Marrian, I.F. (1988) Audit Committees. Edinburgh, The Institute of Chartered Accountants of

Scotland.

��!�"�� ��!�� �#��$ $�%! �&'����� *�'� :��$�&��� ���� ���

Millstein, I.M. (1999) “Introduction to the report and recommendations of the Blue Ribbon

Committee on improving the effectiveness of corporate audit committees”, The Business

Lawyer, 54(3): 1057-1066.

Monks, R. and Minow, N. (2002) Corporate Governance, 2th Edition, Blackwell Publishing.

O' Sullivan, N. (1999) “Board characteristics and audit pricing post-Cadbury: a research note”,

The European Accounting Review, 8(2): 253-263.

OECD (1999) OECD Principles of Corporate Governance, Organization for Economic Co-

operation and Development (OECD), www.Oecd.org

Pincus, K., Rusbarsky, M. and Wong, J. (1989) “Voluntary formation of corporate audit committees

among NASDAQ firms.” Journal of Accounting and Public Policy, 8(4): 239-265.

Rezaee, Z. (1997) “Corporate governance and accountability: the role of audit committees”,

Internal Auditing, 13(1): 27-41.

Rezaee, Z. and Lander, G.H. (1993) “The internal auditor's relationship with the audit

committee.” Managerial Auditing Journal, 8(3): 35-40.

Shahnawaz, M. (2003) "Development of Corporate Governance Framework in Pakistan: Lessons

for Saudi Arabia", in the 10th Accounting Conference “Accounting Disclosure and

Transparency: their role in Strengthening Corporate Governance & Accountability in the

Saudi Corporate Sector”, Organized by Department of Accounting, College of Business

& Economics, King Saud University – Qasseem, 14-15 October, Saudi Arabia.

The Canadian Institute of Chartered Accountants (CICA) (1992) Terminology for Accountants.

4th Edition Canada.

Treadway Commission (1987) Report of the National Commission on Fraudulent Financial

Reporting. USA, National Commission on Fraudulent Financial Reporting.

Verschoor, C.C. (1992) “Internal auditing interactions with the audit committee”, Internal

Auditing, 7(4): 20-23.

Verschoor, C.C. (2000) “New audit committee responsibilities provide governance opportunities

for internal auditing”, Internal Auditing, 15(5): 35-38.

Weir, C. and Laing, D. (2000) "The performance-governance relationship: the effects of Cadbury

compliance on UK-quoted companies", Journal of Management and Governance, pp:

265-81.

��O ������� ���� ���

Audit Committees as a Cornerstone of Corporate

Governance: Saudi Case Study

Awad Salamah F. Al-Rehaily

Associate Professor of Accounting

King Abdulaziz University, Jeddah, Saudi Arabia

Abstract. The importance of Corporate Governance has been

increasingly recognized in recent years, particularly after the collapse

of large public companies such as "Enron" and "WorldCom" in the

USA. The study aims to clarify the reasons and motives behind the

sudden popularity of the Corporate Governance concept in the last few

years, shedding light on the theoretical and practical aspects of the

concept, along with searching and discussing the role of audit

committees as a cornerstone in the process of its implementation, with

focus on the Saudi environment.

The study indicates that the Corporate Governance is a system

by which organizations are directed and controlled. It aims to protect

shareholders' rights, enhance disclosure and transparency, facilitate

effective functioning of the board, and provide an efficient legal and

regulatory enforcement framework. The study also indicates that

despite the Corporate Governance concept being new in the Saudi

environment, increasing efforts took place to publicize this concept.

The study also provides evidence that the audit committees have

an important role yet to play in the implementation of Corporate

Governance in Saudi Arabian financial reporting environment. This

role is a characteristic function of audit committees being a control

channel between internal and external auditors and the corporation's

board.