Embed Size (px)

DESCRIPTION

Â

Citation preview

Paraplanners -Don’t Leave Home Without One

What Low Yields are Really Telling Us

Osborne’s Tradable Annuities

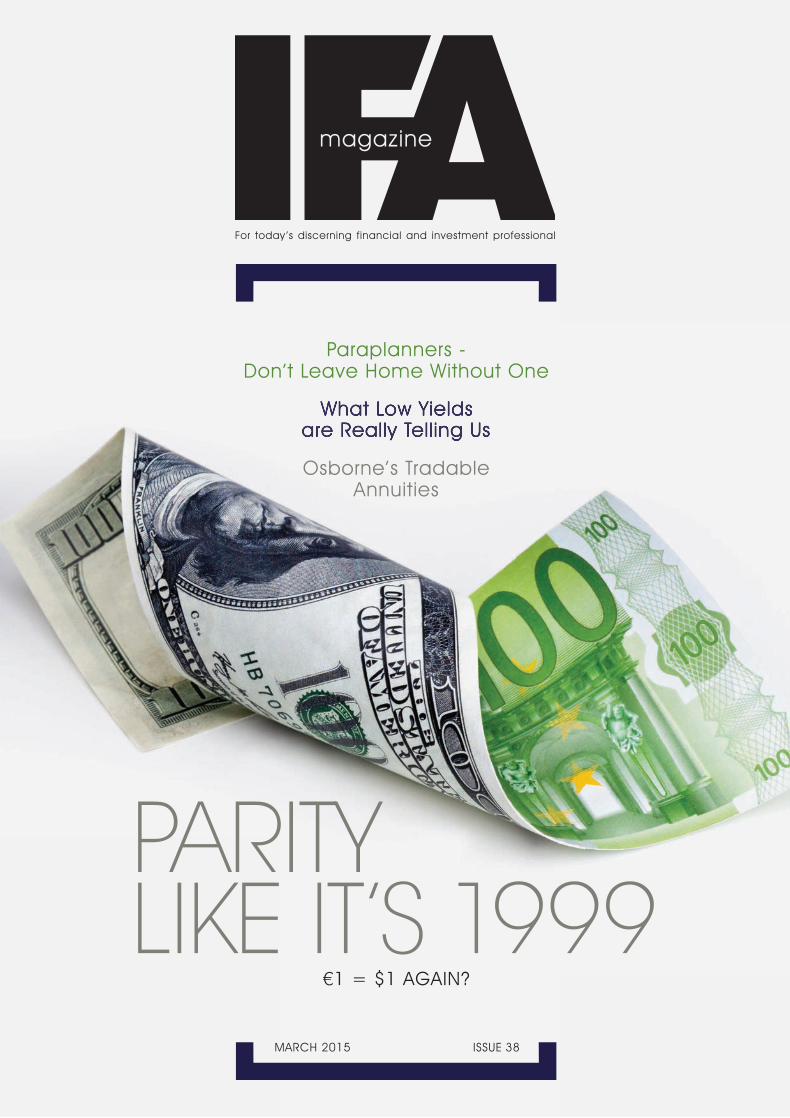

€1 = $1 AGAIN?

PARITY LIKE IT’S 1999

MARCH 2015 ISSUE 38

For today ’s discerning financial and investment professional

Cover.indd 1 19/03/2015 14:35

C O N T E N T S

CONTR I BU TORS

Brian Tora an Associate with investment managers JM Finn & Co.

Lee Werrell a senior compliance consultant and industry adviser.

Richard Harvey a distinguished independent PR and media consultant.

Nick Sudbury known for his columns in many leading financial magazines.

Neil Martin has been covering the global financial markets for over 20 years.

6

News All the big stories that affect what we say, do and think

14Parity and the Euro

It’s been a long time for the undervalued greenback, says Michael Wilson

19

UK Equity Income FundsNick Sudbury says the current popularity of UK plc is entirely rational

25Paraplanners

And why you need one. Sara Arthur, MD at the Parahub, explains

29 It’s All About the Timing Pensions expert Steve Bee takes some lessons from Tom and Jerry

33Landscape Artist

Neil Martin talks to Mike Parsons, of JP Morgan Asset Management, about the joys of the open road

36 Low Yields, Clear Hints There’s a lot you can tell from the current state of risk aversion, says M&G’s Caitlin Hughes

38Indexing Error

Are you sure you know what’s in that index you’re tracking, asks Brian Tora?

41 Rethinking the Adviser Model Neil Martin talks to John Spiers, the head of crossover adviser EQ

Editorial advisory board: Richard Butler, Michael Holder, Ian McIver and Mark Pullinger

03/1

5

Editor: Michael [email protected]

Art Director: Tony [email protected]

Publishing Director: Alex [email protected]

THE FRONTLINE: What goes around, comes around. If you wait long enough, that is. So what happens now?

WHEN BRIAN RETIRED AS SALES DIRECTOR HE NEVER EXPECTED TO GO BACK.

Your clients risk going back to work in retirement unless you make sure they’ve got enough to cover the basics. Things like food, utility bills and running a car.

An enhanced annuity could still be the cheapest* way to secure their basic income needs – and don’t forget, this is guaranteed for life. And with our Target Income Calculator you can give them an indication of how much of their pension fund they will need to set aside to cover the essential living costs, as well as the income they could receive from a Partnership annuity.

That way, once you’ve got their money working, you can rest assured your clients will never have to.

For more details call 0845 108 0443 or visit partnership.co.uk

*Source: Partnership data 2014, Compared to a standard annuity and depends upon individual circumstances. Telephone calls may be recorded for training and monitoring purposes. Local call rates will apply. Partnership is a trading style of the Partnership group of Companies, which includes; Partnership Life Assurance Company Limited (registered in England and Wales No. 05465261). Partnership Life Assurance Company Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. The registered office is 5th Floor, 110 Bishopsgate, London, EC2N 4AY.

For authorised financial advisers only – not for retail clients

PART0068_Golf_Ad_210x297_FAW_AW.indd 1 14/10/2014 16:05Cover.indd 2 19/03/2015 14:35

C O N T E N T S

IFAmagazine.com

March 2015

3

44

Plain Talking Defaqto’s Gill Cardy is back!

46Still the Big Country

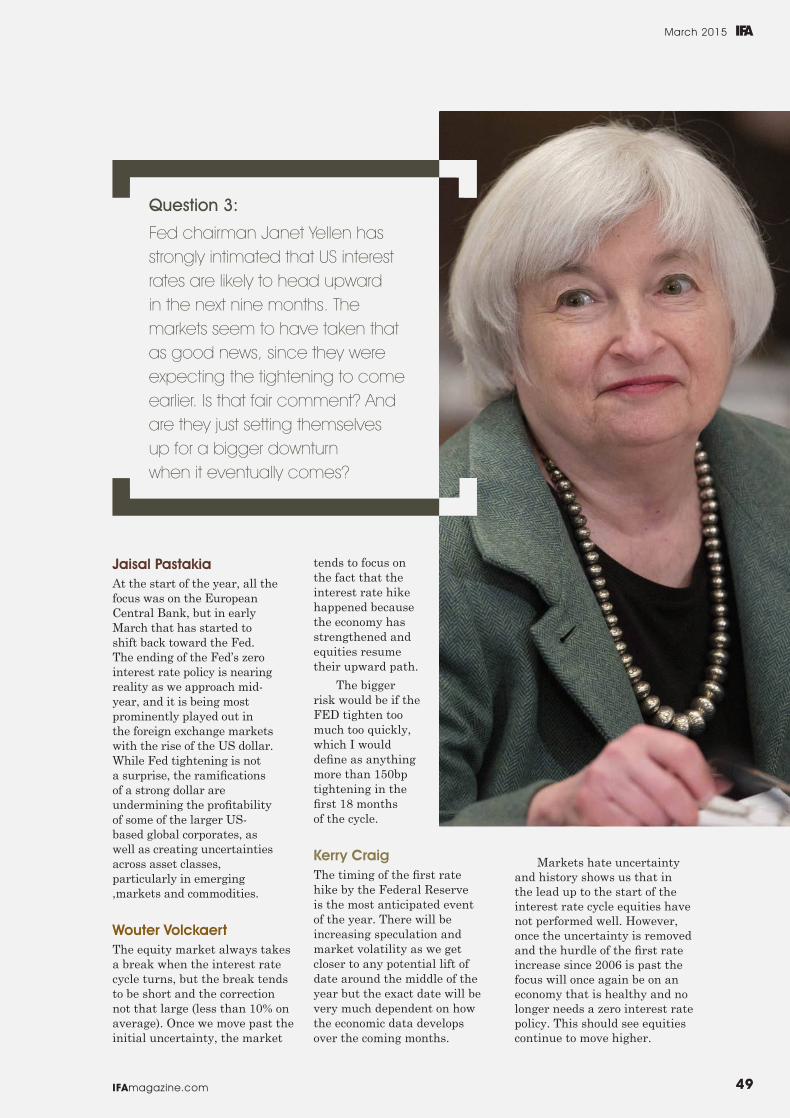

Our panel of senior analysts tells us that America is far from being structurally overvalued

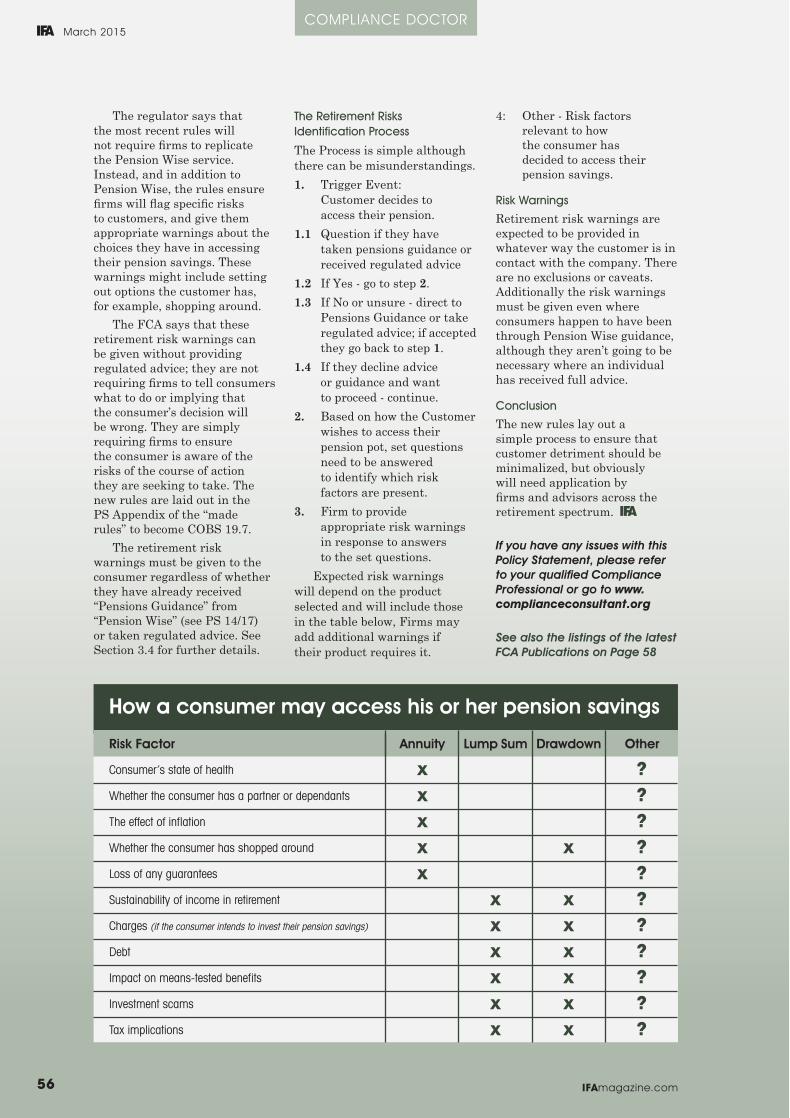

55 Compliance Doctor PS 15/4 is important but it’s been cobbled together at high speed, says Lee Werrell

65FCA Publications and IFA Calendar

In the news, in print and in court. Our monthly listing of what’s new in FCA-land

65Thinkers: Thomas MalthusThe world is not enough, he said. Was he right?

65The Other Side

Life’s a gamble, says Richard Harvey. But has the government rigged the odds?

‘IFA Magazine’ is a trademark of IFA Magazine Publications Limited. No

part of this publication may be reproduced or stored in any printed or

electronic retrieval system without prior permission. All material has been

carefully checked for accuracy, but no responsibility can be accepted

for inaccuracies. Wherever appropriate, independent research and

where necessary legal advice should be sought before acting on

any information contained in this publication.

IFA Magazine is published by IFA Magazine Publications Ltd, The Old Wheelwrights, Ham, Berkeley, Gloucestershire GL13 9QH Tel: +44 (0) 1179 089686 ©2015. All rights reserved

IFA Magazine is for professional advisers only. Full subscription details and eligibility criteria are available at: www.ifamagazine.com

Contents.indd 3 19/03/2015 14:21

Contact us: 0800 41 41 81 • fundsnetwork.co.uk/pension

This advert is for investment professionals only, and should not be relied upon by private investors. *The Investor Fee is not applicable if a client is already paying this on anothersole account held on the platform. Annual ongoing fund charges apply. The value of investments can go down as well as up and clients may get back less than they invest. Issuedby Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. FundsNetworkTM and its logo are trademarks of FIL Limited. CSO6970/0415

No charges fordrawdown with ourpension solutionFundsNetwork.

The world of pension options is dramatically changing, and so

drawdown is on the up. With the FundsNetwork Pension,

however, charges won’t get in the way of offering your clients

choice and flexibility.

So if your clients want to take advantage of the new rules, point

them in the direction of our pension solution.

� No additional charges for capped or flexible drawdown

� Clients pay just 0.25% p.a. and a low annual fee of £45

� An extensive range of over 2,600 clean share classes

� And to help you, full integration with our Adviser Fees service

fundsnetwork.co.uk/support

Endof tax year

upport

fun

EEnEnupport

En5APRIL

Job No: 49694-2 Publication: IFA Magazine Size: 297x210 Ins Date: 01.03.15 Proof no: 1 Tel: 020 7291 4700Ed's Welcome.indd 4 19/03/2015 14:23

Look on the Bright Side

I suppose it’s probably the sunny Fisher grin and the annoyingly perma-bull approach to life that grates slightly on a poor jealous Englishman stuck in Wiltshire on a grey day in March. But the other weekend Mr Fisher came up with something that made me properly sit up and take notice. In fact, I’m still trying to work out now whether he’s onto something eternally profound, or just a long run of historical coincidences? You decide.

We are getting our venerable English knickers in a proper twist, Mr Fisher said (I paraphrase him slightly), about the dire financial prospects that are likely to arise from the forthcoming election. It currently seems next to impossible that any of the major parties can hope to form a government without having to sacrifice its bold autonomy to some sort of a messy coalition that will stop it from doing anything decisive.

Lessons from History

And that will be just terrible for stocks. Won’t it? Actually,

The point, says Fisher, is precisely that a badly hamstrung coalition can’t do much damage through being clumsy. It can’t pitch its economy headlong into a bold new ideology. I’d personally add that it can’t get away with starving the economy into recovery, as George Osborne has tried to do.

nifie , cti e o ernments re li elier to o thin s stoc s

h te, says Fisher. ch s ch n e ro ert ri hts, re r re l tions n re istri te reso rces n c it l...

h rli ments cre te inners n losers

lore, ri in le isl ti e ris ersion n h rtin stoc s.

I wish I’d said that, Oscar. But is he right? We’ll find out soon enough.

Mike Wilson, Editor

It’s not every day that I

acknowledge a profound debt

of gratitude to the inimitable

Ken Fisher, the chief executive

of Fisher Investments, who writes

periodically in the Financial Times

about all things transatlantic

says Mr Fisher, no it won’t. The markets only thin that they hate an indecisive government with no scope for bold innovation. In practice, they absolutely love it. And history provides an endless sequence of incredibly profitable stock market runs that have happened during periods of political gridlock.

There was the infamous Lib/Lab pact of 1977-79, which saw a 60% resurgence in the Footsie. There was the awful second Clinton term in the late 1990s, when a powerless Democrat President presided not just over a Republican Congress, but also over one of history’s longest bull markets. There’s Germany’s toothless grand coalition, which is currently turning in a fantastic Dax performance. There were all those bickering, incompetent European administrations in the 1980s, all of which managed to outperform the UK even though we had Margaret Thatcher running the show.

Bright Side

The point, says Fisher, is

of Fisher Investments, who writes

Financial Times

says Mr Fisher, no it won’t. The that they

hate an indecisive government with no scope for bold innovation.

Contact us: 0800 41 41 81 • fundsnetwork.co.uk/pension

This advert is for investment professionals only, and should not be relied upon by private investors. *The Investor Fee is not applicable if a client is already paying this on anothersole account held on the platform. Annual ongoing fund charges apply. The value of investments can go down as well as up and clients may get back less than they invest. Issuedby Financial Administration Services Limited, authorised and regulated by the Financial Conduct Authority. FundsNetworkTM and its logo are trademarks of FIL Limited. CSO6970/0415

No charges fordrawdown with ourpension solutionFundsNetwork.

The world of pension options is dramatically changing, and so

drawdown is on the up. With the FundsNetwork Pension,

however, charges won’t get in the way of offering your clients

choice and flexibility.

So if your clients want to take advantage of the new rules, point

them in the direction of our pension solution.

� No additional charges for capped or flexible drawdown

� Clients pay just 0.25% p.a. and a low annual fee of £45

� An extensive range of over 2,600 clean share classes

� And to help you, full integration with our Adviser Fees service

fundsnetwork.co.uk/support

Endof tax year

upport

fun

EEnEnupport

En5APRIL

Job No: 49694-2 Publication: IFA Magazine Size: 297x210 Ins Date: 01.03.15 Proof no: 1 Tel: 020 7291 4700

IFAmagazine.com

March 2015

5

W O R D S O F W I L S O N

Ed's Welcome.indd 5 19/03/2015 14:23

Pension Conversions:

The Knives Are Out

We shouldn’t have been surprised, or course.

With the general election barely six weeks

away, and with one of the tightest run-ins

for half a century on the cards, the fighting

was bound to get dirty sooner or later

On the one hand was the UKIP leader Nigel Farage, offering to strike up a ‘support arrangement’ for a future Conservative government - while absolutely ruling out a coalition with the Tories because, Mr Farage said, “most of the people sitting around the cabinet table are ghastly”. And all that on condition that David Cameron, or preferably the chief whip Michael Gove, agreed to hold a referendum on Europe this year. (“Total nonsense” was Chancellor George Osborne’s official line on a Tory deal with UKIP.)

On the other was the fix that shadow chancellor Ed alls got himself into over a collaboration approach from the Scottish Nationalists – an idea that his boss Ed Miliband had already rejected. ut if, as he claimed, the S P wants to break up the nited Kingdom and

cannot stand up for the whole of the K , how did he find himself conceding to the ’s

ndrew Marr that he was “not going to get involved in speculation about post-election deals, because we are fighting for a majority.

Desperate Times, Desperate Measures

There were, then, obvious signs of

desperation coming from both camps. ut what should we make of the hancellor’s pre-

udget statement on 15 March, to the effect that pensioners with existing annuity contracts might still be allowed to participate in the April pension freedoms, despite having signed on the line for a lifetime income rather than unlimited capital freedoms

t certainly did look like a late attempt by the Tories to round up the grey vote and stop it running away to

K P. nd it seemed a logical extension of last ecember’s other panic measure, which had allowed efined

N E W S

IFAmagazine.com6

“From April 2016,

the government

will remove the

restrictions on

buying and

selling existing

annuities”

Chancellor, George Osborne

News.indd 6 19/03/2015 14:30

enefit pension holders the prospect of cashing in their benefits for

-style lump sums. ut how might the new

idea work in practice

The government’s statement was confident enough The hancellor has

announced that the government will extend its pension freedoms to around 5 million people who have already bought an annuity, it began. From pril 2016,

the government will remove the restrictions on buying and selling existing annuities to allow pensioners to sell the income they receive from their annuity without unwinding the original annuity contract .. Pensioners will then have the freedom to use that capital as they want just as those

who reach retirement with a pension pot can do under the pension freedoms announced in udget 2014. They can either take it as a lump sum, or place it into drawdown

to use the proceeds more gradually .

Industry Reactions

Tish and pshaah, the industry’s response seemed to say. To sell an existing annuities contract for cash, you’re going to have to find a buyer for it. Which won’t be easy, given that its financial outcome, and

therefore its value, depends entirely on how long you’re likely to live. re annuity holders looking for a conversion really going to have to bare every detail of their health

to the prospective buyers, like slaves in a marketplace

oanne Segars, the hief Executive of the

National Association of Pension Funds, put it a little more subtly. t’s clear to see how this fits with this Government’s agenda for pensions, she said, but what is less clear is how savers will be protected. full consultation will be essential . which would need to look at how the buy-back price of an annuity would be calculated so people selling their annuity could be assured of good value and also consider a prescribed process for introducing buyers and sellers to avoid excess costs, which would inevitably be carried by the consumer.

ot a good start, coming from the country’s biggest federation with over 1,300 pension schemes covering some 17 million people. ut

ndrew Tully, pensions technical director at MGM dvantage, rammed home the point rather more forcibly. t was, he seemed to be saying, nothing less than robbing people twice instead of only once

“There are significant risks, he said, and two wrongs won’t make a right.

eing sold a poor value annuity and then being offered a poor value cash lump sum, which is taxable, will not address the issue of an inappropriate original sale.

uite so. This one’s going to take a bit of sorting out.

IFAmagazine.com 7

UKIP Led

er, N

ige

l Fara

ge

Joa

nne Se

ga

rs, CEO

Na

tiona

l Assoc

iatio

n of Pe

nsion Fund

s

N E W S I N B R I E F

QE Gets Under Way

Quantitative easing in the euro

zone got under way, as the

European Central Bank started

buying in Eurozone government

bonds, often at low or even

negative yields. Greek bonds

are not eligible for support

within the current scheme.

“It’s clear to

see how this

fits with this

Government’s

agenda for

pensions, but

what is less

clear is how

savers will be

protected”

Falling Down

UK construction output fell by

2.6% in January, sharply below

economists’ expectations

of a 1.2% rise. It was the

biggest fall since November

2013, and contrasted with a

0.6% increase in December.

Housebuilding activity fell by 5%

over the month, commercial

building by 6.6% and new

infrastructure work by 2.7%.

News.indd 7 19/03/2015 14:30

N E W S

16 Million Orphans?As if the response to the pension freedoms wasn’t enough,

there was more bad news for the Chancellor, and for the

FCA, from Garry Heath, a former Director General of The IFA

Association and the eponymous founder of the Heath Report.

And half a cheer for the sceptics who had always lamented

the loss of the old commission model.

The true scale of the RDR disaster was only now becoming evident, it seemed. “23 million UK Citizens used to be able to access advice through

banks or the IFA sector,” it thundered. But, “thanks to the regulator’s obsession with creating a commission free market 16 million no longer have access,

and if they persist with removing Trail Commission the 7 million consumers still advised will at best drop to 5.5 million, and at worst 4 million”.

N E W S I N B R I E F

Yakkety Yak

More than a billion smart phones

were sold worldwide in 2014,

according to Gartner research.

Global champion Samsung

faced tightening competition

from Apple after the iPhone 6

was launched.

Fool’s Gold

The FTSE-100 finally beat

its end-1999 record in late

February – in nominal terms,

at least, In real inflation-

adjusted terms it would have

needed to be 53% higher.

IFAmagazine.com8

This advert is for investment professionals only,only,only and should not be relied upon by private investors.The value of investments and the income from them can go down as well as up and clientsmay get back less than they invest. Map contains Ordnance Surveydata © Crown Copyright and database right 2013. Source of performance: Morningstar as at 31.12.2014. Basis: bid-bid with net income reinvested. Launch date is 30.04.2007. Copyright - © 2015 Morningstar,ningstar,ningstar Inc. All Rights Reserved. Past performance is not aguide to the future. *Source Morningstar as at 31.12.2014. Based on multi asset funds from the mixed or flexible investment and unclassified sectors where ‘income’ or ‘distribution’ was included in the fund name. Market index from 01.10.11 – 70% BofA ML SterBrd Mkt NUK; 15% FTSEAll-ShareTR; 10% MSCIWORLD EX UK (NUK); 5% GBP OverNight IndexAverage – full history available from Fidelity.Fidelity.Fidelity Holdings can vary from those in the index quoted. For this reason the comparison index is used for reference only.only.only The fund’stargetyield isbetween4%and6%p.a.onthecapital invested.Theyield isnotguaranteedandwillfluctuate in linewiththeyieldavailable fromthemarketover time.Thefundsshouldonlybeconsideredasalong-terminvestment.Asaresultof theannualmanagementcharge for the income share class being taken from capital, the distributable income may be higher but the fund’s capital value may be eroded which will affect future performance.The investment policies of Fidelity multi asset funds mean they invest mainly in unitsin collective investments schemes. Investments should be made on the basis of the current prospectus, which is available along with the Key Investor Information Document, current and semi-annual reports free of charge on request by calling 0800 368 1732.Issued by FIL Investments International, authorised and regulated by the Financial Conduct Authority.Authority.Authority Fidelity,Fidelity,Fidelity Fidelity Worldwide Investment, the Fidelity Worldwide Investment logo and F symbol are trademarks of FIL Limited. UKM0215/5223/CSO7022/0515

Fidelity Multi Asset Income Fund

Reliable income with low volatility.ty.tyGuide your clients to the right solution.Finding reliable, diversified sources of income for your clients

presents a considerable challenge. Our Multi Asset Income Fund

may hold the solution:

� Currently yielding 4.03%, or 5.02% gross in a SIPP

� Less volatile than the best-selling multi asset income funds*

� Lower capital drawdown than equities

� Outperformed its comparative index over 3 and 5 years, and

since launch in 2007

The fund is one of three Fidelity multi asset income options. All are

guided by our proven multi asset approach. All are independently

risk-profiled by Distribution Technology. And all are available

via FundsNetwork™ Navigator.

So click or call today – and set your clients on

course for reliable income.

News.indd 8 19/03/2015 14:30

The annual cost of is £340 million,

Heath insists - and rising. nd the failure of the regulator to define Simplified dvice’, as it promised the Treasury Select ommittee 4 years ago, means that there is no sign of alternative distributions big enough to take up the 16 million abandoned consumers.

The Heath Report therefore proposes

n New legislation to restore proper Parliamentary accountability in Financial Services

egulation.

n The suspension of the F ’s plans to remove Trail commission in 2016.

n The separate disclosure of the advisers’ compliance and compensation costs so that consumers can see the costs they are paying for - over which the adviser has no control.

n The creation of a oyal ommission to

define what citi ens can reasonably expect from the state and what they should provide for themselves.

theheathreport.com

Wise words or in ammatory rhetoric? Let us have your thoughts please. Email [email protected]

Lord

Gre

en

N E W S I N B R I E F

My Old China

China announced plans to raise the retirement age for both men and women, with effect from 2017. The over-60s are expected to grow from 15% of the population today to 40% by 2050.

Yee Haw

The Nasdaq, a bellwether

for confidence in US tech

stocks, closed above 5,000

for the first time since March

2000. The S&P 500 had long

been in record territory.

Never a man to mince his words, Mr Heath affirmed that 13,500 advisers have left the industry since the announcement of and that nowadays the only consumers likely to receive advice are the seriously wealthy. Which made it a mystery how this could be seen as consumer protection

Institutional Evasion

We have a regulator who derives its power from a statute passed by Parliament but is not responsible to anyone particularly the Parliament that created it, he declared. This allows the F

to embark on this act of vandalism in the sure fire knowledge that no one can stop it. t is an abuse of power

- pure and simple .

IFAmagazine.com 9

Garry Heath

web: fidelity.co.uk/mai

call: 0800 368 1732

Yield

as at 31.12.144.03%

News.indd 9 19/03/2015 14:30

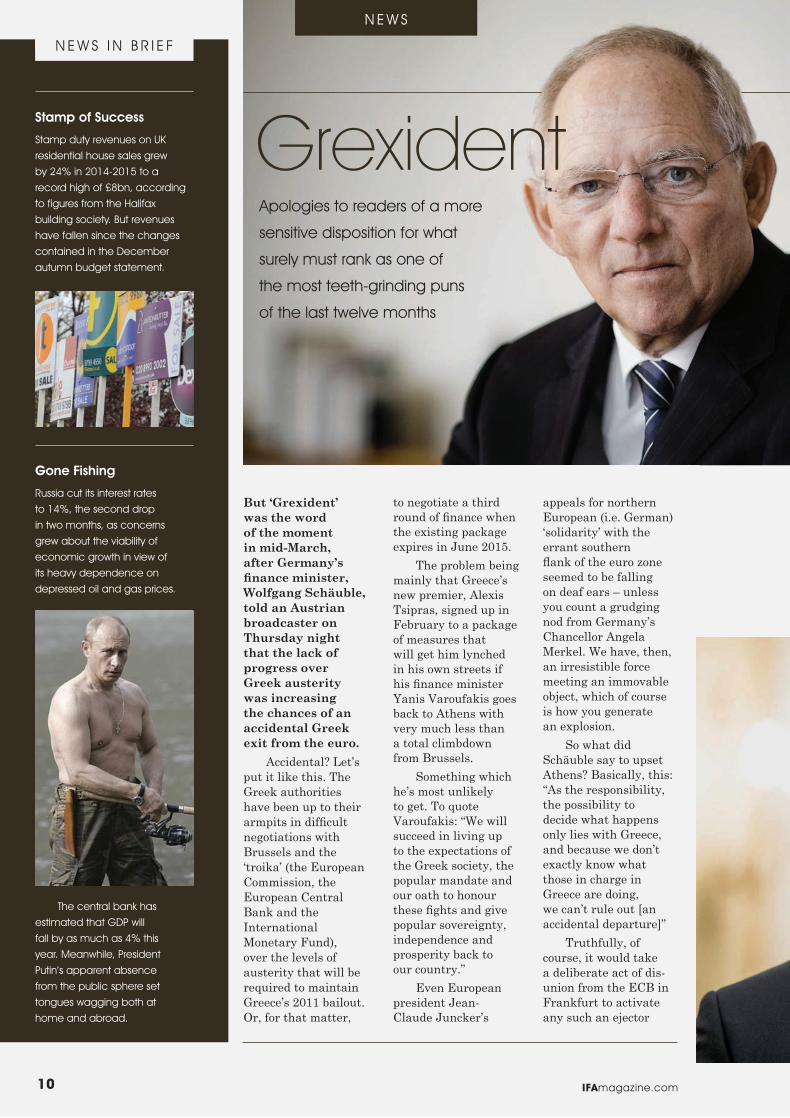

GrexidentApologies to readers of a more

sensitive disposition for what

surely must rank as one of

the most teeth-grinding puns

of the last twelve months

But ‘Grexident’ was the word of the moment in mid-March, after Germany’s finance minister, Wolfgang Schäuble, told an Austrian broadcaster on Thursday night that the lack of progress over Greek austerity was increasing the chances of an accidental Greek exit from the euro.

ccidental et’s put it like this. The Greek authorities have been up to their armpits in difficult negotiations with

russels and the troika’ the European ommission, the

European entral ank and the

International Monetary Fund), over the levels of austerity that will be required to maintain Greece’s 2011 bailout. Or, for that matter,

to negotiate a third round of finance when the existing package expires in une 2015.

The problem being mainly that Greece’s new premier, lexis Tsipras, signed up in February to a package of measures that will get him lynched in his own streets if his finance minister

anis aroufakis goes back to Athens with very much less than a total climbdown from russels.

Something which he’s most unlikely to get. To quote

aroufakis We will succeed in living up to the expectations of the Greek society, the popular mandate and our oath to honour these fights and give popular sovereignty, independence and prosperity back to our country.

Even European president ean-

laude uncker’s

appeals for northern European i.e. German) solidarity’ with the errant southern

ank of the euro one seemed to be falling on deaf ears unless you count a grudging nod from Germany’s

hancellor ngela Merkel. We have, then, an irresistible force meeting an immovable object, which of course is how you generate an explosion.

So what did Sch uble say to upset

thens asically, this s the responsibility,

the possibility to decide what happens only lies with Greece, and because we don’t exactly know what those in charge in Greece are doing, we can’t rule out an accidental departure

Truthfully, of course, it would take a deliberate act of dis-union from the E in Frankfurt to activate any such an ejector

N E W S

IFAmagazine.com10

N E W S I N B R I E F

Gone Fishing

Russia cut its interest rates

to 14%, the second drop

in two months, as concerns

grew about the viability of

economic growth in view of

its heavy dependence on

depressed oil and gas prices.

Stamp of Success

Stamp duty revenues on UK

residential house sales grew

by 24% in 2014-2015 to a

record high of £8bn, according

to figures from the Halifax

building society. But revenues

have fallen since the changes

contained in the December

autumn budget statement.

The central bank has

estimated that GDP will

fall by as much as 4% this

year. Meanwhile, President

Putin’s apparent absence

from the public sphere set

tongues wagging both at

home and abroad.

News.indd 10 19/03/2015 14:30

seat, and there’s surely no reason to suppose that the explosive charges in the release mechanism haven’t been deactivated long ago. ut if you’re looking for the reasons

why the euro has slumped close to dollar parity during the last month, the Grexident factor wouldn’t be a bad place to start.

Taxing the Patience

Meanwhile, a little counter-intuitively, the first signs of a turnaround in the Greek economy seem to have been tentatively happening. Greece’s statistics service E ST T published an initial estimate for G P growth during 2014 last year which it reckons improved by 0.8 , rather better than the 0.6 that its own forecasters had been predicting.

ut don’t hang out the bunting yet. Preliminary estimates showed that the thens government missed its 1.4bn budget surplus

target during the first two months, managing only 1.2 bn because

of a painful shortfall in tax revenues. Tax revenues, the finance ministry said, totalled 7.3bn around 14 below

the targeted 8.5bn.

Undercover Mission?

nd that was what prompted aroufakis’s pretty extraordinary plans for a new network of government-sponsored amateur tax snoopers, each of them wired for sound and video, to seek out Greece’s many millions of serial tax evaders.

aroufakis confessed, in a leaked memo, that the backlog of tax arrears currently stood at 76bn £55bn) about £5,000 for

everyone in the country - but that only 8bn of this was ever likely to be recoverable. Given, he said, that the state’s tax inspection service was demoralised and understaffed, it might be an option to recruit large numbers of hourly-paid non-professional inspectors , including tourists, to check up on his countrymen.

Tourists es indeed, and many of them German, apparently. erlin has already offered to send 500 tax inspectors to

thens if need be but the massed hordes of German tourists who head south every summer would also provide excellent cover for the investigators.

las, as long as ritain’s climate remains coldly northern, alas, George Osborne can only dream of doing the same.

IFAmagazine.com 11

Wo

lfga

ng Sc

häub

le

Alexis Tsip

ras

N E W S I N B R I E F

We Interrupt this Service…

Bitcoin values sulked around the $285 mark in mid-March – a significant improvement on the $175 level of mid-January but still 35% down on the values of last November. Bitcoin miners had been hit by a wave of denial of service attacks during early March.

Germany’s

finance

minister,

Wolfgang

Schäuble,

has hinted

that the

lack of

progress over

Greek austerity

was increasing

the chances of

an accidental

Greek exit from

the euro

Real Pain

The Brazilian real continued

its worsening slide against

foreign currencies, having now

lost more than 40% against

last summer’s dollar rates.

There were riots in many

cities against perceived

corruption and political

incompetence in the

government, which only

began its new term in January.

Meanwhile, the central bank’s

forecasts of a 0.66% economic

shrinkage in 2015 are looking

too rosy for comfort.

News.indd 11 19/03/2015 14:30

ETF Assets head for $3 Trillion

N E W S

IFAmagazine.com12

Only this January, PwC issued a report projecting that global ETF assets under management would double to $5 trillion by 2020. And already, according to Debbie Fuhr’s ETFGI consultancy, we’re looking to break through the $3 trillion milestone for ETFs and ETPs in the first half of .

All of which was rather timely, given that March marked the 25th anniversary of the very first ETF listing, in anada. Pass the birthday cake and the champagne

Total global AUM at the end of February, Ms Fuhr said, came to a colossal 2. 1 trillion some $110 bn more than in ecember 2014. The global ETF ETP industry had 5,632 ETFs ETPs, with 10, 02 listings, from 245 providers listed on 63 exchanges in 51 countries.

ut traffic was also phenomenal.There were 50.7 billion in net new

asset ) in ows during February alone, she said the second largest NNA month on record, after the 61.5 billion recorded

in ecember 2014.

Equity Trackers in Favour

Where was the money invested Equity ETFsETPs accounted for the largest net in ows

30.4 bn, or 60 ), followed by fixed income ETFs ETPs with 15.6 bn 30.7 ) and commodity ETFsETPs with 2. bn in net in ows 5.7 ). On a year to date basis the net new asset ows into all sectors are at record levels - 28.8 bn into fixed income, 8.0 bn into commodities, 2.7 bn into active ETFs and 62.0 bn globally.

iShares gathered the largest net ETF/ETP in ows in February with 1 . bn, followed by anguard with 5. bn and SP ETFs with 4.3 bn net in ows. On a T basis, iShares gathered the largest net ETF/ETP in ows with 26. bn, followed by anguard with 15.7 bn

and WisdomTree with 6.8 bn net in ows.

nvestors allocated the majority of net new assets to equities, said Ms Fuhr, as the

S market rebounded from a difficult anuary to end February with both the S P 500 and the ow up 6 for the month. olatility declined during the month. eveloped markets were up 6 for the month, while emerging and frontier markets were up 3 .

According

to Debbie

Fuhr’s ETFGI

consultancy,

we’re looking to

break through

the $3 trillion

milestone for

ETFs and ETPs

in the first half

of 2015

Debbie Fuhr

Looking Good

Strong US growth was also hinted

at by encouraging employment

statistics. Meanwhile the

Federal Reserve was thought

to have advanced its plans

for a raising of US interest

rates, probably by mid-year.

N E W S I N B R I E F

Free Money

The spring budget, announced

on 18 March, included a new ISA

for first time house buyers which

would attract £50 of government

cash to match every £200 they

saved toward their deposits. It

was expected to be popular.

The government also relaxed the

intra-year withdrawal rules for ISA

accounts, allowing investors to

draw down cash without losing

part of their annual entitlement.

Sweet Harmony

The Chancellor also announced

various changes to EIS, VCT

and SEIS arrangements, which

basically harmonised the

eligibility rules with the European

rules on state assistance. He

also abolished the rule requiring

SEIS funds to spend 70% of their

start-up cash before they were

eligible to graduate to EIS status.

Clear evidence

that the trend

toward passive

products is

moving faster

than expected

News.indd 12 19/03/2015 14:30

News.indd 13 19/03/2015 14:30

S O A P B OX

First Among Equals?It’s been a long time coming, says

Michael Wilson, but the dollar

is finally reasserting itself

over the upstart euro

We were just getting the March issue of IFA Magazine together when the dread news came over on the radio. For the eleventh day in succession, the euro/dollar exchange rate had slid back (or soared, depending on your viewpoint), and one dollar would now cost you a whole 93 euro cents, compared with 89 euro

cents on 3 March. Yes, in the space of seven days the currency had lost 6% of its value. nd, for the first time since 2003, one American dollar was starting to look like it would buy you a euro.

Five days later, as we got to the finalisation phase for IFA Magazine, the situation had attened out a little but it had in no way improved.

nd you could almost hear the satisfaction coming in across the airwaves from Washington and ew ork.

t’s been a long time coming, Europe, the voices said, but we got there eventually. So you really thought your puny little lashed-together raft could outperform the mighty S battleship in the long term

March 2015

IFAmagazine.com14

Ed's Soapbox.indd 14 19/03/2015 14:30

Even though your crew members have been threatening to push each other overboard for the last five years, and the only one with the keys to the engine, Germany, had been refusing to keep those Greeks on the team if they accepted half rations and paddled twice as hard

ou couldn’t make it up, pal.

ritons are also celebrating. ast summer the pound was

trading at 1.20, meaning that holidaymakers were paying 83 pence for every euro coin in mid-March, however, the rate had soared to 1.40 for the first time since ecember 2007, meaning in effect that

their holiday spending power in the euro one had improved by 15 in nine months. nd what was more, this was happening against a generally negative in ation rate, which meant that their bonan a was even bigger in real terms.

What’s causing this collapse in the euro’s value ou’d have to have been living in a cave to have missed it. On the one

hand, city analysts are saying that

continued fears over

a Greek exit

Grexit ) from the Euro one has put the skids under the common currency. nd on the other, this month’s 60bn commencement of the scheduled 1.1 trillion quantitative easing

has opened up the very real likelihood that in ation will pick up, and that the sheer mass of new money being printed will devalue what’s left. The forward currency markets will have got their calculators round this likelihood some time ago.

E Pluribus Unum

The cynics in Washington do have some pretty good reasons to be feeling smug about all this. The euro and the dollar are both federal’ currencies which are

shared by large-ish groups of states 1 in Europe, 50 in

merica), but that’s where the similarities end. We

could no more think about ew Mexico

being forced out of the union,

or alifornia demanding

a better

IFAmagazine.com

March 2015

15

Ed's Soapbox.indd 15 19/03/2015 14:30

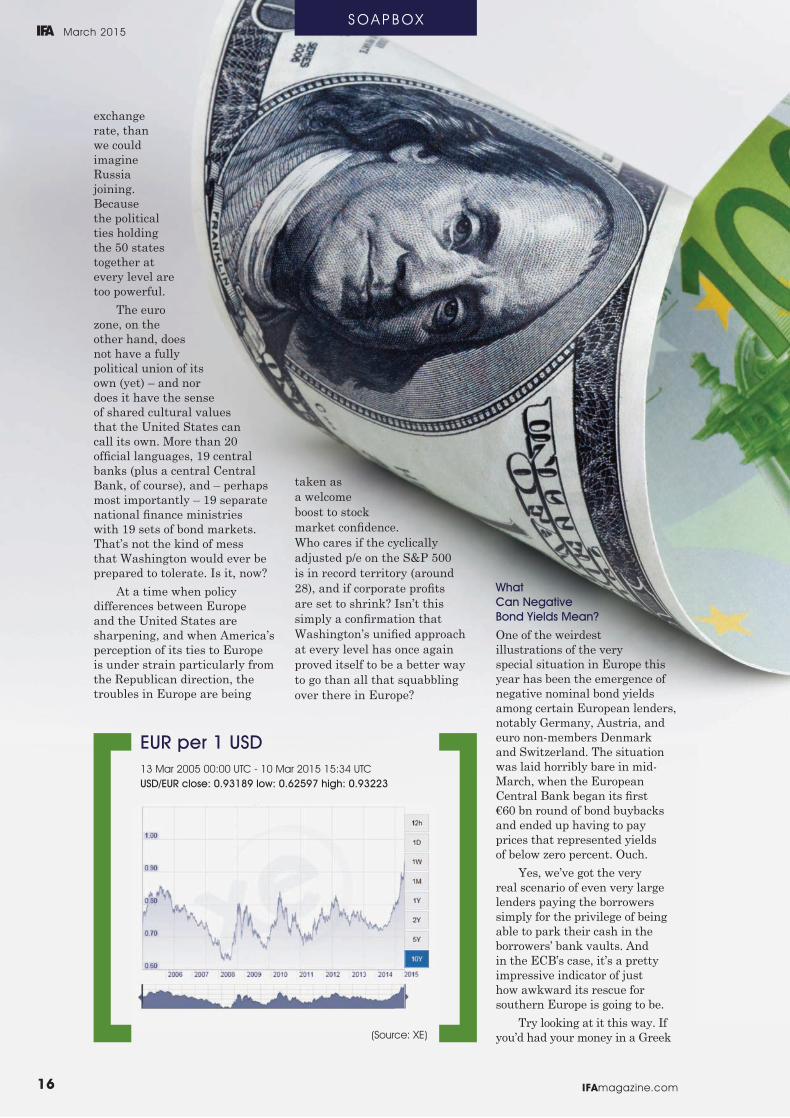

EUR per 1 USD

exchange rate, than we could imagine Russia joining.

ecause the political ties holding the 50 states together at every level are too powerful.

The euro one, on the

other hand, does not have a fully political union of its own yet) and nor does it have the sense of shared cultural values that the nited States can call its own. More than 20 official languages, 1 central banks plus a central entral

ank, of course), and perhaps most importantly 1 separate national finance ministries with 1 sets of bond markets. That’s not the kind of mess that Washington would ever be prepared to tolerate. s it, now

t a time when policy differences between Europe and the nited States are sharpening, and when merica’s perception of its ties to Europe is under strain particularly from the epublican direction, the troubles in Europe are being

What Can Negative Bond Yields Mean?

One of the weirdest illustrations of the very special situation in Europe this year has been the emergence of negative nominal bond yields among certain European lenders, notably Germany, ustria, and euro non-members enmark and Swit erland. The situation was laid horribly bare in mid-March, when the European

entral ank began its first 60 bn round of bond buybacks

and ended up having to pay prices that represented yields of below ero percent. Ouch.

es, we’ve got the very real scenario of even very large lenders paying the borrowers simply for the privilege of being able to park their cash in the borrowers’ bank vaults. nd in the E ’s case, it’s a pretty impressive indicator of just how awkward its rescue for southern Europe is going to be.

Try looking at it this way. f you’d had your money in a Greek

S O A P B OX

taken as a welcome boost to stock market confidence. Who cares if the cyclically adjusted p e on the S P 500 is in record territory around 28), and if corporate profits are set to shrink sn’t this simply a confirmation that Washington’s unified approach at every level has once again proved itself to be a better way to go than all that squabbling over there in Europe

13 Mar 2005 00:00 UTC - 10 Mar 2015 15:34 UTCUSD/EUR close: 0.93189 low: 0.62597 high: 0.93223

(Source: XE)

March 2015

IFAmagazine.com16

Ed's Soapbox.indd 16 19/03/2015 14:30

bank’s vault for the last

six years, the fact that it was in euros

wouldn’t amount to very much consolation if you thought there was even a chance of a default by the Greek Treasury, or even just a delay in getting your money back. Which is also considered a default.) nder these circumstances you might very well be willing to accept a ero return, or even to pay a safe

keeping’ fee to the undesbank for the privilege of knowing that you could get at your cash whenever you needed it.

That’s understandable enough for the Greeks, of course, but this time it’s the E itself that’s the lender. y the way, Greek bonds don’t qualify for the E bond-buying programme because the necessary safeguards aren’t in place.) f even the boys in Frankfurt can’t do a bond buy-back at reasonable rates, that’s a pretty scary measure of how panicky other

small uctuation in yield equates to a 24 uctuation in the value of the bonds themselves.

There are other reasons to worry about the sudden strength of the dollar. t’ll be great for

S tourists in Paris, but bad for anyone hoping to sell cars or computers or Smart watches in Europe. t’ll make this the perfect year to buy a Porsche, if you’re merican, that is, and maybe the iper can wait till next year. t’ll severely damage the merican tourism trade.

The Size of the Slide

ut we digress. ast month, IFA Magazine asked our

urning ssues panel for their views on where the Euro one economy was headed, and the overwhelming sentiment was that most of the bad news was already priced in, and that this might just be an ideal time to make an entrance.

Five weeks on, some of the panel’s confidence has been rewarded. ut only if you happen to be denominated in euros. On the plus side, the FTSE Eurofirst 300 had gained 5 during the month to mid-March, but the sterling euro exchange rate had nearly taken the gloss off the gains for a sterling investor - and much more for a S investor, who’d seen the equivalent of 8 knocked off the dollar value of his Euro one holdings during the month.

Going Forward?

That, of course, is an overly simplistic view of the situation. n time, the enhanced currency

competitiveness of Euro one manufacturers ought to bring them significant benefits in the export markets, notably to the nited States itself.

nd those benefits won’t be in the figures yet.

s long as a Grexident’ doesn’t take Greece out of the euro and it would take a mighty act of perverseness from Germany to give it a helping shove there is every possibility that Europe may once again outperform. ut the risks are not to be underestimated.

people must be feeling. lready, commentators are wondering just how much of the 1.1 trillion E programme can be achieved if prices are this high.

That’s something that’s been happening not just to the rock-

solid Euro one countries, of course, but also to ritain,

where the competitive overseas pressure for

gilt ownership has kept ritish yields

so pathetically low over the

last few years

much to the

chagrin of pension

annuity buyers, whose

contracts are based on the prevailing

gilt rates at the time they buy their annuities.

nfortunately it’s also been happening in merica, where the ight to quality’ has been driving down Treasury bond yields at just the time when Fed

hairman anet ellen had been talking about raising mid-year interest rates. That puts her in a tricky position should she hold off with the increases to prevent further dollar appreciation, or would she be better advised to restrain further growth ever so gently nd what will happen if S yields then suddenly rebound - because, for instance, the European entral ank suddenly starts to look like it’s got its act together so that demand for S bonds suddenly abates

That’s not such a fanciful scenario as it looks. For the last few weeks, S bond yields have been swooping and switchbacking in a very unsettling manner, as the relative merits of European and merican bond markets have been tested by an endless succession of twitch-making news. s recently as February, 10 year yields were ranging between 1.65 to 2.05 in the space of a day. nd in case you need reminding, that apparently

IFAmagazine.com

March 2015

17

Ed's Soapbox.indd 17 19/03/2015 14:30

Products - UK Equity Income.indd 18 19/03/2015 14:41

P R O D U C T S

UK Equity Income – The Best of All Worlds?Dividend yields in the UK Equity sector can exceed 3.5% per annum, but there

is further upside for investors who can accept more risk. Nick Sudbury reports

UK Equity Income funds have been the best-selling sector of the market for a staggering eight months in a row. The Woodford effect has undoubtedly had a lot to do with it, although the strong demand also re ects the increasingly desperate search for yield.

In spite of its enduring popularity, a number of high profile constituents have recently moved out of the sector including funds

year end. The test is applied over rolling 3-year periods with the current income benchmark being around 3.6 .

There are about 60 funds in the sector that are paying out at least this amount, but the risk is that they are effectively being forced to invest in high yielding blue chips that have been bid up in value. This makes it more important than ever to assess the investment process and to satisfy yourself that the manager is up to the job

run by nvesco Perpetual, Henderson’s and St James’s Place. The reason for this unusual move was the unwillingness to comply with the high income requirement at the cost of compromising on the capital growth.

ll the funds in the sector are required to invest at least 80 in K equities and to achieve an historic yield on the distributable income in excess of 110 of the FTSE All-Share yield at the fund’s

IFAmagazine.com

March 2015

19

Products - UK Equity Income.indd 19 19/03/2015 14:41

holdings such as Game igital and rax have struggled, but have been retained because the business case remains intact.

Woodford is very much his own man and not afraid to be different - which should ensure that the fund is relatively uncorrelated with the rest of the sector. s with his previous mandates, there is a big emphasis on capital preservation, and clients will also appreciate the fact that the new fund is targeting a competitive starting yield of 4 with quarterly distributions.

The F Woodford Equity ncome fund has attracted a

massive amount of capital in a very short space of time, but it is up and running in impressive fashion. Woodford has shown himself to have a safe pair of hands and there is no reason to doubt that he will continue to deliver. t is difficult to see what could go wrong unless something was to seriously undermine the global healthcare sector.

33 allocation comprising holdings such as stra eneca, GlaxoSmithKline and oche. Its other main overweight position is in Industrials, where companies such as apita and

E Systems make up a 17 exposure, which is well in excess of the 10 representation in the benchmark. The main underweights are Oil & Gas, Financials, onsumer Services and asic Materials.

It’s an interesting portfolio, because although the top 10 blue chips make up almost 50 of the fund there are plenty of smaller holdings to provide long-term capital growth. These include several biotech firms, the peer-to-peer investment trust, P2P Global nvestments, and the active investment fund Crystal Amber. Other

n its first months eil Woodford’s new UK Equity Income fund has attracted a staggering £4.7bn in AUM. This remarkable achievement is a testament to his success running a similar mandate at Invesco Perpetual and also re ects one of the highest profile marketing campaigns the investment world has ever seen.

Woodford’s nvesco Perpetual ncome fund generated an annualised cumulative return of 14.3 over his 23-year tenure, which was a full 500 basis points more than the sector average. t will not be easy to replicate this sort of outstanding performance, but he has started well, with his new venture up more than 15 since launch compared to the 2 increase in its FTSE

ll-share benchmark.

The portfolio is massively tilted in favour of the Healthcare sector, with a

The Midas touch

CF Woodford Equity IncomeType: UCITS (UK)

Sector: UK Equity Income

Fund Size: £4.7bn

Launch: June 2014

Yield: 4%

Ongoing Charges: 1%

Manager: Woodford Investment Management

woodfordfunds.com

P R O D U C T SMarch 2015

IFAmagazine.com20

Products - UK Equity Income.indd 20 19/03/2015 14:41

One of the best performing funds in the sector is the little known Evenlode Income, which is up 95% in the last 5 years. It is run by ise nvestment, a firm based in rural Oxfordshire, and has just £252m in AUM. Since it was launched in October 2009 the fund has achieved an annualised return of 13.8%, a full 500 basis points ahead of its FTSE All-Share benchmark.

Hugh Yarrow, the lead manager, who looks remarkably like Hugh Grant, looks for good quality companies that are asset-light. He aims to identify businesses with high returns on capital and strong free cash- ow that can generate sustainable real dividend growth. The portfolio bears very little resemblance to the index with holdings retained for the long-term.

At the end of January there were just 31 positions, with the top 10 accounting

Hidden Gem

Evenlode Income Type: OEIC

Sector: UK Equity Income

Fund Size: £252m

Launch: October 2009

Yield: 3.58%

Ongoing Charges: 0.99%

Manager: Wise Investments

evenlodeinvestment.com

arrow is conscious of the fact that the higher valuations mean that future returns are likely to be lower than in the recent past. He believes that revenue growth is harder to come by, and that this makes it more difficult for companies to grow their dividends. That is why he looks for businesses with sustainable free cash ow, as these have a safety buffer to protect them against a slowdown in the economy or any company or industry specific setback.

The fund offers a decent 3.58 yield with quarterly distributions, and despite its relatively small size it has a competitive ongoing charges figure of 0. for the clean share class. t is an interesting offering and Yarrow’s willingness to move between large caps and small caps differentiates it from many of its peers. Would make a decent diversifier to one of the larger funds in the sector.

for 52.1 of the fund. These included the likes of nilever, GlaxoSmithKline, iageo, Sage Group and stra eneca. The largest sector allocation was the 34.6 weighting in onsumer Goods, followed by 15.7 in Healthcare and 10. in Media stocks. lmost three-quarters of the money is invested in blue chips, with the balance in mid-tier companies, although for most of the period since launch there has been a significant small cap exposure that started off around the 50 mark.

IFAmagazine.com

March 2015

21

Products - UK Equity Income.indd 21 19/03/2015 14:41

and sustainable yields. This is a fairly diversified portfolio with 42 holdings, and with the largest, nilever, only making up 4.1 . The rest of the top 10 include the likes of mperial Tobacco, GlaxoSmithKline,

P and HS , and together they represent just under a third of the fund.

ts largest sector allocation is the 22 exposure to Financials, followed by 21 in onsumer Goods, and 14 in tilities. There is also a holding in cash.

This solid, no nonsense approach, has generated consistent, market beating returns, at a much lower level of volatility than the benchmark. The last 12 months were particularly good, with the 14 gain elevating it into third place in the sector, but it will not always top the table like this. The fund would make an ideal core portfolio holding for income seeking clients with a reasonable level of risk aversion.

every year since it was launched with the annual payments going from just over 4 pence per share in 2005 to around 6.5 pence in 2014. This represents an average annual increase of 5.1 , which is particularly impressive given that it straddles the period encompassing the 2008 0 financial crisis. The fund now has an attractive net yield of 3. , although the distributions are only made twice a year rather than quarterly like some of its peer group.

Francis rooke, the manager, invests in solid businesses with good cash ow

Most of those investing in the sector typically want to be able to rely on a steadily increasing income stream with long-term capital growth and as little volatility as possible. Clients that fit into this profile are likely to find that Tro an ncome from Troy Asset Management ticks all the right boxes.

The £2.15bn Trojan ncome fund was launched in September 2004 and by the end of anuary had achieved a cumulative return of 164.6 , which was comfortably ahead of both the sector average and the FTSE

ll-Share at 117. and 127.3 respectively. ts annualised volatility of .4 was well below the 13 plus recorded by both benchmarks, and the maximum drawdown a full 20 less.

alculations by FE nalytics suggest that it has one of the best risk-adjusted performance records in the sector.

Trojan ncome has successfully raised its dividend

Ticks All the Right Boxes

Trojan IncomeType: UCITS

Sector: UK Equity Income

Fund Size: £2.15bn

Launch: September 2004

Yield: 3.9%

Ongoing Charges: 1.02%

Manager: Troy Asset Management

taml.co.uk

P R O D U C T SMarch 2015

IFAmagazine.com22

Products - UK Equity Income.indd 22 19/03/2015 14:41

Clients who are willing to give up some capital growth in return for additional yield may be interested in an innovative product like the Schroder Income Maximiser fund. This consists of two elements. There is a value-based UK equity portfolio that provides a yield of 3.5% with the potential for long-term capital growth and an option overlay strategy to take the yield up to the target level of 7%.

The fund was launched in ovember 2005 and has attracted a creditable £1.2bn in M. Over the intervening years the accumulation units

are up around 100 , which is well in excess of the FTSE ll-Share, but the income units are broadly unchanged. These have paid out the target yield of 7 each year with the dividends distributed on a quarterly basis.

Thomas See, the manager, has put together a predominantly large cap

Keeping Up Appearances

Schroder Income MaximiserType: Unit Trust

Sector: UK Equity Income

Fund Size: £1.2bn

Launch: November 2005

Yield: 6.98%

Ongoing Charges: 1.66%

Manager: Schroder Unit Trusts Limited

schroders.com

on securities or indices not held by the fund, which is another way of boosting the income.

It is interesting to note that although the way derivatives are used should reduce the risk, the fund has in fact recorded an annualised volatility of 10.5 , which is slightly above the sector average. ess surprising is the higher than usual ongoing charges of 1.66 . This is most likely because of the extra cost of buying and selling the options.

The manager invests in robust businesses with the prospect of sustainable dividend growth. His aim is to sell just enough capital growth across the portfolio to meet the high income requirement, while still benefitting from the first part of any share price appreciation. t is a tough balancing act,

but income investors should be pretty pleased with the performance to date as it is hard to think of any other sustainable way of earning a 7 yield.

portfolio of 46 holdings of which the 10 most significant make up 45.6 of the fund. These include companies such as GlaxoSmithKline, Friends

ife, odafone and P. The key sector exposures are 2 .8 Financials, 20 onsumer Services and 17.4 Healthcare.

n order to increase the yield he is allowed to sell short dated call options in the underlying securities. This covered call strategy generates upfront premiums from the sale of the options, but limits the potential capital gains. He can also sell out-of-the-money put options

IFAmagazine.com

March 2015

23

Products - UK Equity Income.indd 23 19/03/2015 14:41

Products - UK Equity Income.indd 24 19/03/2015 14:41

Paraplanners

G U E S T F E AT U R E

What is your role? What part of your job do you love the most? For the majority of advisors, this will be sitting in front of a client and aiding them in securing their future, not sitting in front of a computer screen writing letters, and chasing providers for information. Would you like the time to focus more on

building client relationships and gaining new business?

The Right Skills in the Right Places

Step forward, the Paraplanner. The very name means that these people are there to come alongside you and share the burden. The role of a Paraplanner has arisen because advisers saw the need

Can you afford not to have one, asks Sara Arthur, MD at the Parahub?

We have all been there: those days when the mountain of paperwork never goes down, and you are sat tackling your administration in frustration, bemoaning the workload before you. Or perhaps you have a queue of leads, which you need to follow up, but you are too busy writing reports to do so.

IFAmagazine.com

March 2015

25

Guest Feature - Parahub.indd 25 19/03/2015 14:43

to delegate important parts of their workload in order to maximise profit making ability and make the best use of their resources. A Paraplanner can use their analytical strengths and abilities to write clear, compliant, documents which back up the strategies you have constructed with your clients. The time they spend writing reports is ultimately time you can spend in front of clients. Think of using a Paraplanner as a business strategy tool: making your processes more streamlined and efficient and making that return work for you.

For small F firms, this can be a life-saver. One man band F firms can find it hard to take the strain of servicing clients, attracting new business and dealing with the administration that the process entails. There are a finite amount of hours in a day, after all! So, where do you start?

How To Use a Paraplanner?

There are a great many ways to use paraplanning services, depending on the size of your firm and your requirements. In-house paraplanning is a great way of building a relationship with a Paraplanner, and crafting a strong team with the option of the Paraplanner being the point of contact in-house. This lubricates the process and frees up your time from dealing with clients’ day-to-day contact.

“Paraplanning is an integral part of our process,” says Mark Jeffs, a Financial Planner from Citimark. “It’s a benchmark of our company ethos, and the Paraplanners are more than qualified to deal with any queries that come their way from clients When I was a

train and nurture staff in the ways of financial planning but also save expense by spotting errors”. Having a chain of responsibility to reduce risks can only be a positive step.”

The Outsourcing Alternative

Outsourcing paraplanning is an alternative that may suit smaller firms who aren’t ready for the commitment of a full time member of staff, or the expense. Outsourcing is a major factor in the paraplanning industry, and a bevy of very talented paraplanning firms have sprung up to take the burden off your shoulders. Where do you look for them?

The ParaHub is a network of Paraplanners and financial administrators that serves as a basis for facilitating networking, educational resources and job prospects. You can advertise for a Paraplanner in the place where they congregate, bridging the gap between Advisers and the people they need.

Whichever way you look at it, maximising your resources has the potential for exponential success. Be kind to yourself and make your life easier; paraplanning is the way forward. Having been elected on the Government steering group for the Paraplanner Apprentice scheme, I can see that the role is growing more defined and being honed into a destination in it’s own right. Taking on an apprentice Paraplanner may be a more cost effective way forward, being helped by government grants of £10,000 per Paraplanner.

Help yourself maximise time for profit. Sit in front of a client, and leave the paraplanning to the people who do it best.

Paraplanner, I was always the secondary point of contact for clients. If ever clients couldn’t get hold of the financial planner, they would contact me. It was reassuring for clients to know there was someone else who knew their circumstances and was there to help”.

Dan Atkinson, senior Paraplanner at EQ Investors and IFP Paraplanner of the

ear, adds The reason we find Paraplanners so useful at EQ is objectivity around advice, and the ability to spot new business opportunities. It’s a virtuous circle, where we can

G U E S T F E AT U R E

Help yourself maximise time for profit. Sit in

front of a client, and leave the

paraplanning to the people who

do it best.

March 2015

IFAmagazine.com26

Guest Feature - Parahub.indd 26 19/03/2015 14:43

At Octopus we’re a big admirer of bright ideas. That’s why we love the Enterprise Investment Scheme (EIS), a government-backed initiative which gives investors a number of ways to save on their tax bills. We also love the investment potential of the UK energy sector, which is undergoing a huge transformation. So why not combine these two bright ideas into one? We have. It’s called Octopus EIS. To find out more, talk to your Business Development Manager on 0800 316 2067 or visit octopusinvestments.com

Important InformationFor professional advisers only and not to be relied upon by retail clients. This financial promotion has been issued by Octopus Investments Limited which is authorised and regulated by the Financial Conduct Authority. Your capital is at risk and you may not get back the full amount invested. Tax treatment depends on the individual circumstances of each investor and may be subject to change. Past performance is not a reliable indicator of future results and any forecast is not a reliable indicator of future performance. The availability of tax reliefs also depends on the investee companies maintaining their qualifying status. Octopus EIS invests into small unquoted companies which are likely to have higher volatility and liquidity risk than shares quoted on the London Stock Exchange Official List. This promotion does not offer investment or tax advice and as this product is not suitable for everyone we recommend you seek independent investment and tax advice before investing in our products.

Invest in energy companies through an EIS. Another bright idea from Octopus.

EIS Ad 2015 297x210.indd 1 23/01/2015 16:39Steve Bee.indd 27 19/03/2015 14:50

The About Us page is the second most important page on your website – only behind the home page. This is your one chance to talk about yourself, and not about your customers. This is the opportunity they give you to impress them. Your “About Us” is your audition - Seems self-evident to make it quality, right?

1 – Make your Branding Message

Who are you? What do you do? Clients want to have a deeper understanding of the people who they will be dealing with if they select your company. And remember, it’s also a chance for you to talk about areas of speciality and identify who your ideal client is – this can be a good way of weeding out the unsuitable clients at an early stage.

2 – For Potential Employees

When people hear about your company’s job openings, they will almost assuredly visit your website and check out your About Us page. Having a video that prospective applicants can watch is a great idea. They can get a feel for who you are and who you serve. They should also gain a greater understanding of your values and your mission. It’s also a great idea to include your staff in the video so that the job seekers get a feel for your company’s diversity and the attitude and demographics of the people working there.

Prospective clients and job seekers should also learn the history of the company. Through all of this subtle information, the applicant finds out whether they might be a good fit for your company and whether your company is a good fit for them. Today’s employers realize the value of recruiting someone who feels at home and will stay. The About Us video is another tool for engaging prospects and helping to reduce the wasted time of interviewing someone who really wouldn’t be a good fit and doesn’t realize it until they show up at your office.

ADVERTORIAL

3 – For Current Employees

Having an About Us page isn’t just about new employees. It’s to help focus and align your current ones as well. A good About Us page gives your employees identity and a sense of proudness to be working for this company. It’ll also help your employees explain who they work for and what they do.

For more information on how we can help with a home page video, or any other aspect of video marketing, please get in touch: phone: 01453 810914 email: [email protected]

You can also view examples of our work at: www.halofilms.co.uk

Peter Georgi of Halo Films talks about why IFAs need an “About Us” Video

With thanks to Kirstie of WarroomInc.com

Steve Bee.indd 28 19/03/2015 14:50

Comic TimingKapow! Steve Bee reaches for the popcorn

I have a bunch of grandchildren these days who, I am glad to say, share some of my interests. Two of them are just as keen to watch old Tom and Jerry films as was when was young. Mind you, they both watch them in colour on their own iPads, whereas I used to watch them in

ickering -line black and white on our TV at home (as long as it didn’t overheat of course, in which case the screen went completely grey - but on the plus side you could still hear the soundtrack). I did get to see them in glorious Technicolor once a week, more often

S T E V E B E E

IFAmagazine.com

March 2015

29

Steve Bee.indd 29 19/03/2015 14:50

than not at the Saturday morning pictures (I was a Junior of the ABC, and I still have the badge to prove it). Quite unsurprising really.

The humour in Tom and Jerry is apparently timeless: the little chaps who are the latest in our family to appreciate slapstick laugh in all the right places and absolutely howl when things go badly awry for Tom.

Punch Lines

The problem that Tom has - as I said when trying to explain the essence of humour to them (absolutely pointless as it turns out) - is that he’s always in the wrong place at the wrong time. In his world, that means that he will more often than not turn a corner, only to tread on a rake that immediately whips up and smashes him in the face as Jerry makes his getaway.

Even when things seem to be going his way, Tom’s luck always seems to run out. He is often just seconds away from finally hitting erry on the head with a massive mallet or something, only to find that, when he brings it crashing down on what he supposes to be Jerry, it turns out to be the foot of Spike the bulldog. And once Spike has Tom by the neck, even his over-the-top charm

cannot ever save him from the most dire consequences.

And I’ve simply lost count of the times that Tom eventually catches Jerry and holds him gleefully while looking directly at the camera, without the slightest clue that the anvil all we viewers had earlier seen launched skyward in a freak accident at the nearby Acme building site is, even at his moment of glory, heading straight for the very spot where he has chosen to stop and savour his triumph.

Wrong place, wrong time. Always.

Jerry, on the other hand, has the knack of usually being in the right place at the right time, or at least being in the wrong place at the right time when he might see the trap Tom may well fall into if he simply stops to either whistle to him or poke his tongue out while waving his hands with his thumbs in his ears.

S T E V E B E EMarch 2015

IFAmagazine.com30

Steve Bee.indd 30 19/03/2015 14:50

Being in the right place at the right

time, or even being in the wrong place at the right

time is clearly preferable to being in the wrong

place at the wrong time

Stage Fright

Being in the right place at the right time, or even being in the wrong place at the right time is clearly preferable to being in the wrong place at the wrong time. I’ve been thinking about that a lot lately, while thinking about the million or so smaller employers who are soon about to reach their staging dates.

All the experience thus far, as the larger employers

have staged, has shown that auto-enrolment, while hard enough to comply with, is doubly difficult if firms do not leave themselves enough time to prepare for things.

million or more firms are right now rushing at headlong speed into auto-enrolment. Some are well aware of that, and are well prepared for what they must do. For others though, auto-enrolment might well turn

out to be the rake on the oor just around the next corner.

And that’s not funny.

I don’t think it is yet too late for people to help such firms, but can’t help wondering whether a Government advertising campaign warning employers to watch out might be more appropriate than the current ads that focus on employees being ‘in’.

Perhaps Tom and Jerry could even star in the ads?

IFAmagazine.com

March 2015

31

Steve Bee.indd 31 19/03/2015 14:50

Welcome to London Capital ClubYour space in the heart of the City for

meeting, dining and networking

We look forward to welcoming you to London Capital Club

A Space for MeetingLondon Capital Club is the perfect location formeeting with clients over an informal coffee, a spot of lunch, or in one of our sumptuous privatemeeting spaces.

Restaurant Fine Dining

Events & NetworkingWe host a range of networking events, as well as keynote speaker events. We have spaces for members’ events and can accommodate up to 150 delegates in a variety of room set-ups.

London and Beyond

T: 0207 717 0088E: [email protected]: 15 Abchurch Lane, London EC4N 7BWW: www.londoncapitalclub.com

Enjoy the brasserie-style ambience in our public bar and restaurant, @15, formal dining in our members’ restaurant The Walbrook Grill, or hold a private function in one of our historic rooms for an outstanding fine dining experience.

Club members receive the same exceptional service in over 250 clubs worldwide, which make up the IAC network, as well as access to further benefits, such as discounts at some of the country’s best golf courses and hotels.

Follow us @LondonCapClub

Find Us: Bank Cannon Street Monument

Steve Bee.indd 32 19/03/2015 14:50

I N S I D E T R A C K

All Mapped OutNeil Martin talks to Mike Parsons, Managing Director,

JPMorgan Asset Management

“You absolutely get to understand, and it’s the one thing that’s drilled into us here at JP Morgan, that this is a fiduciary business. That we are managing other people’s money, and we put their interests first.

ou can never lose sight of the fact that there is an end-investor, and we’re investing their money and we’re entrusted to look after their money, and generate returns for them.

Get With the Programme

Whilst at Fidelity, Parsons moved from the consumer end of the business to dealing with F s. Some 20 years later, he

throughout his career, as he progressed from Fidelity, into Schroders and then landing at P Morgan in 2007.

He had three interviews when he left university, he says, and he decided that the job in financial services looked the most interesting.

nd he actually started in a Fidelity call centre, dealing directly with clients and getting what he described as a fantastic start in the sector.

Managing Director Mike Parsons, who is Head of UK Sales at JPMorgan Asset Management, provides a quick and somewhat concise snapshot of his abilities after studying geography at Exeter University.

could read maps, do the colouring-in and add-up in numbers, he says. Skills which have obviously stood him well

IFAmagazine.com

March 2015

33

Inside Track - JP Morgan Chase.indd 33 19/03/2015 14:49

currently P Morgan’s chief market strategist for the K and Europe. She and her team produce market research and issue bulletins to advisers about key market developments, aiming to place investment implications into context.

Parsons is a firm believer in their guides and road shows. We give our insights into capital markets, and that really is one of the best ways to help IFAs, interpreting the key trends and nuances of capital markets.

We are able to articulate what’s going on in a relatively simple format which is useful for their end-consumer. Obviously markets move very quickly and they are incredibly complex. So what we’re trying to do is bring clarity to the markets, so advisers can a. formulate their own thinking about asset allocation and b. articulate that to their clients.

There is no shortage of comment and information that

its around from fund groups and the internet - the idea of this is that we can bring it all together in one place.

now heads up a number of teams that deal with F firms, life companies and stockbrokers.

ndependent financial advisors are taken very seriously indeed. We have very strong relationships with the larger regional F s, where we look to have regular meetings, and very in-depth, one-on-one relationships.

would expect my team to see their client base at least every quarter and sometimes it’s once a month, where the firms are sophisticated in their needs. They might have five or six people doing fund selection within that firm, so we have to go and see a lot of people to understand their business.

Parsons says that a great deal of contact comes at the quarterly roadshows which form part of the P Morgan sset Management Market Insights Programme. This programme is a framework of research and current market analysis that is delivered to K advisers. The idea is to illustrate an array of market and economic histories, trends and statistics through clear, compelling charts and graphs that advisers can share with their clients.

Started some ten years ago, Parsons says that the programme has gone from strength to strength. nd at the core of it all is what’s known as the Guide to Market. This is a markets-based chart book, of which there are five regional versions. t is translated into 12 local languages distributed in 25 countries.

Hit The Road

The roadshows, held in more than 20 cities held each quarter, allow P Morgan

I N S I D E T R A C K

then also talk about a product, a fund that we think is topical, or interesting, and relevant to the audience. So that should help to make it a commercial success for both parties.

RDR and Afterwards

s for how the F industry has moved on after , Parsons is upbeat: “I think that almost all of the firms we talk to, are saying that business has never been better. Obviously there are fewer advisers these days, so the simple economics of supply and demand indicates that those that are still trading should be in a better position.

nd pretty much everybody we’re talking to is saying that there are issues about capacity. ’m not saying that all F firms

want to grow their capacity, but they can afford to be choosy about the clients they bring on board, which is a phenomenally strong position to be in.

n terms of F s’ development during the 20 years that Parsons has worked in the sector, he is also very

Having someone of Stephanie Flanders’s standing and reputation must surely prove a big draw for P Morgan

es, without doubt. ut we also have another group, within Stephanie’s team, who are bright and really good strategists, and are good at articulating the message.

The thing with Stephanie is that she’s asked to speak all over the world, so it’s not always possible to get her out to every venue, every quarter. ut we try to make sure that she gets good air time with all of our clients over the course of the year.

s you’d expect, the roadshows are also an important channel for selling the house’s products So whenever we take one of the strategists out, we

to meet thousands of F s throughout the year and are each built around the particular insights of one of P Morgan’s global strategists.

Perhaps the best well known of the current roster is former Economics Editor Stephanie Flanders, who’s

March 2015

IFAmagazine.com34

Inside Track - JP Morgan Chase.indd 34 19/03/2015 14:49

impressed. t has moved from a very transactional industry to a much more relationship-based profession, he says.

ust from a simple point of view, the questions we are getting asked and the analysis that is done on our funds is so much more advanced than it was five years ago, and very much better that ten years ago - and almost unrecognisable from 20 years ago.

Developing the Adviser Market Further

s to the future, Parsons is also upbeat. ut, he adds, the one thing we will all have to do - and this is not just specific to F s but everyone in the industry - is work on consumer trust. nd while that sounds simple, it’s phenomenally hard for an industry, or a

profession, to rebuild trust. t’s very clear that the clients

who use an F , must be able to trust them implicitly. One of the reasons why people don’t use an F is cost of course, but the other is trust.

The key question for Parsons is how collectively the industry can get consumers engaged with the financial services industry and how it properly demonstrates its ability to add value.

Market Direction

sked what advisers are currently focusing on, Parsons says that Europe and the

S loom large. Particularly important is how the new QE programme in Europe will affect the long term prospects of the euro currency and certain asset classes.

He added that IFAs are currently most nervous about the fixed interest market, as rates are at incredibly low

levels which will obviously need to rise in the future.

also think you can expect that capital markets will be a bit more bumpy going forward than they have been.

dvisors are aware of this and are positioning in diversified funds to mitigate what might happen in the future.

Spare Time?

The interview finishes with the inevitable question about how Parsons spends his leisure time. ou might think that given the intensity of his job, winding down with a gentle pastime might be in order, but Parsons says his favourite sports are those that require a liberal squirt of adrenaline.

lthough he admits, as a father of three young children, he gets less time to indulge in such activities than he used to. He now has to settle for a single mountain bike ride every week.

nd that, together with heading up the team of intelligent people who sit within JP Morgan, ought to be enough adrenaline for anyone.

“There is no shortage

of comment and

information that flits

around from fund