Embed Size (px)

Citation preview

IN THIS LECTURE, YOU WILL LEARN:

Am simple perfect competition production

medium-run model view of what determines the

economy’s total output/income

how the prices of the factors of production are

determined according to this model

how total income is distributed

what determines the demand for goods and

services

how equilibrium in the goods market is achieved

2 theories of consumption0

1CHAPTER 3 National Income

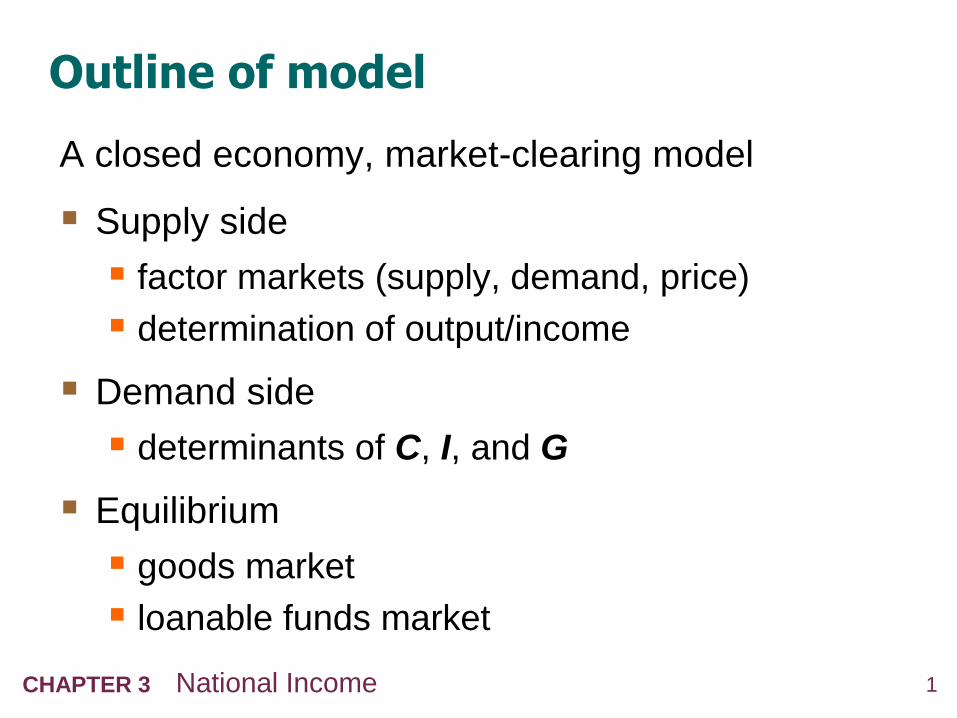

Outline of model

A closed economy, market-clearing model

Supply side

factor markets (supply, demand, price)

determination of output/income

Demand side

determinants of C, I, and G

Equilibrium

goods market

loanable funds market

2CHAPTER 3 National Income

Production Model

Vast oversimplifications of the real world in a

model can still allow it to provide important

insights.

Consider the following model

Single, closed economy

One consumption good

3CHAPTER 3 National Income

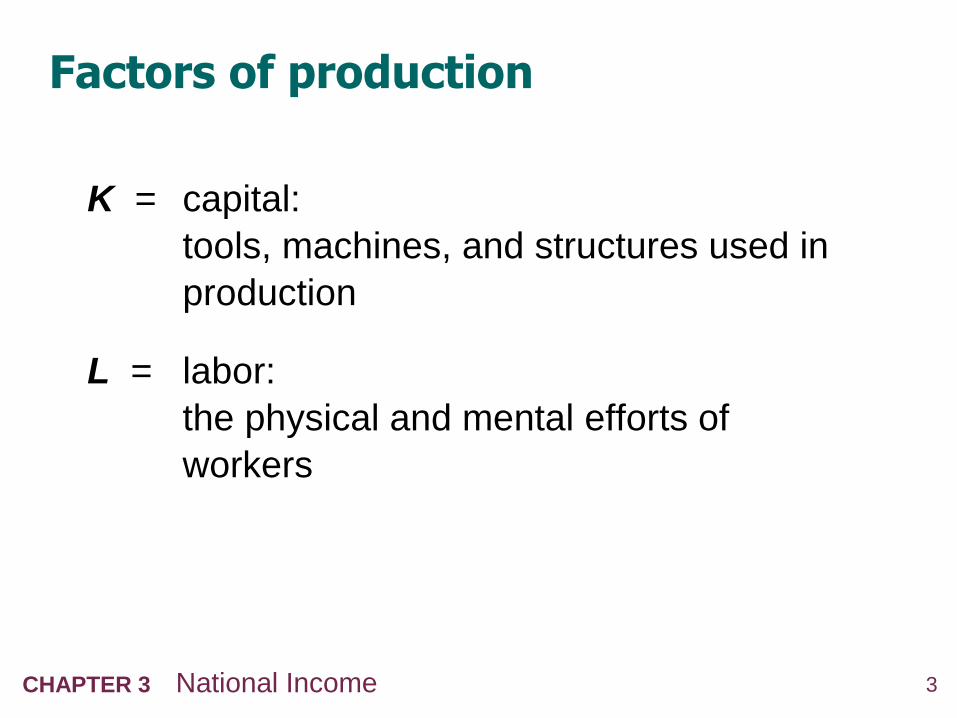

Factors of production

K = capital:

tools, machines, and structures used in

production

L = labor:

the physical and mental efforts of

workers

4CHAPTER 3 National Income

The production function: Y = F(K,L)

shows how much output (Y )

the economy can produce from

K units of capital and L units of labor

reflects the economy’s level of technology

We assume that the production function for the

economy as a whole exhibits constant returns to

scale

5CHAPTER 3 National Income

Returns to scale: a review

Initially Y1 = F (K1 ,L1 )

Scale all inputs by the same factor z:

K2 = zK1 and L2 = zL1

(e.g., if z = 1.2, then all inputs are increased by 20%)

What happens to output, Y2 = F (K2,L2 )?

If constant returns to scale, Y2 = zY1

If increasing returns to scale, Y2 > zY1

If decreasing returns to scale, Y2 < zY1

6CHAPTER 3 National Income

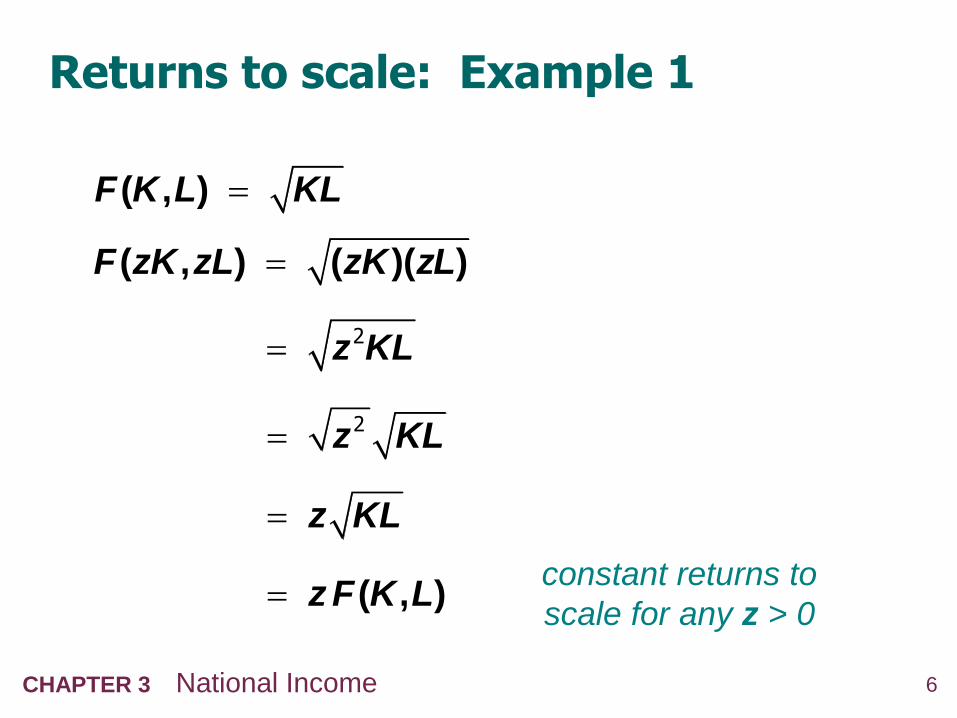

Returns to scale: Example 1

( , )F K L KL

( , ) ( )( )F zK zL zK zL

z KL 2

z KL 2

z KL

( , )z F K Lconstant returns to

scale for any z > 0

7CHAPTER 3 National Income

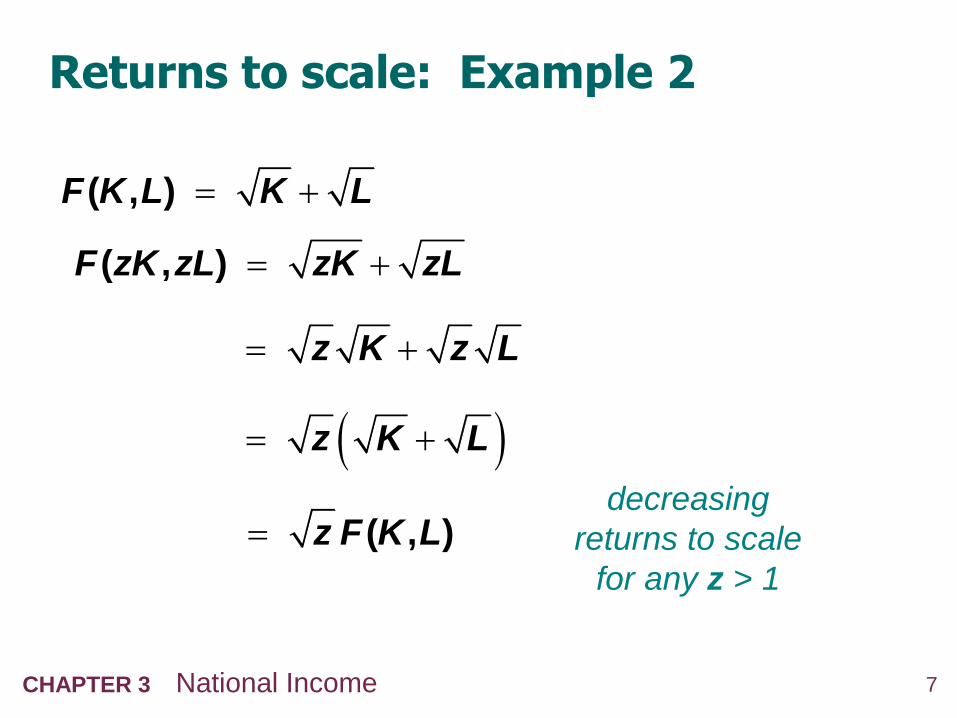

Returns to scale: Example 2

( , )F K L K L

( , )F zK zL zK zL

z K z L

( , )z F K Ldecreasing

returns to scale

for any z > 1

z K L

8CHAPTER 3 National Income

Returns to scale: Example 3

( , )F K L K L 2 2

( , ) ( ) ( )F zK zL zK zL 2 2

( , )z F K L 2 increasing returns

to scale for any

z > 1

z K L 2 2 2

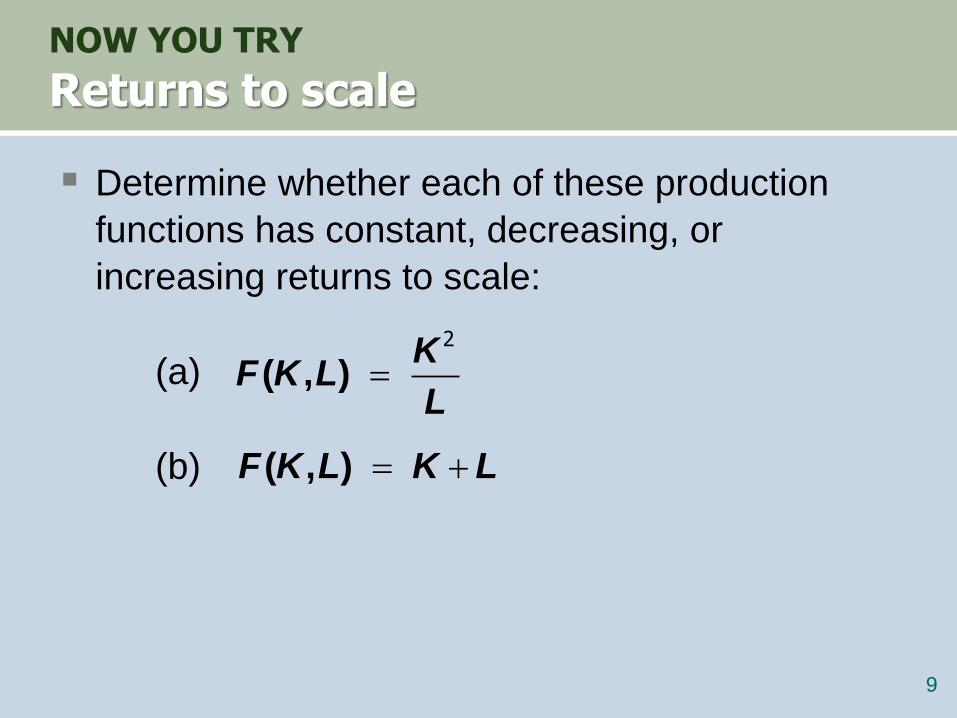

NOW YOU TRY

Returns to scale

Determine whether each of these production

functions has constant, decreasing, or

increasing returns to scale:

(a)

(b)

9

( , )K

F K LL

2

( , )F K L K L

10CHAPTER 1 The Science of Macroeconomics

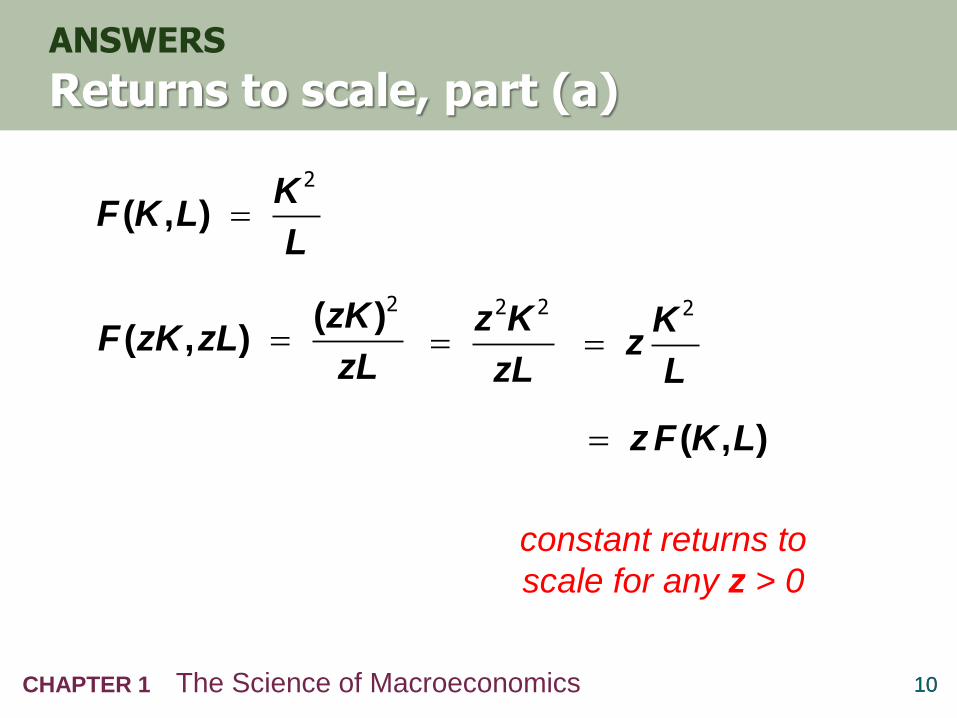

ANSWERS

Returns to scale, part (a)

10

( , )K

F K LL

2

( )( , )

zKF zK zL

zL

2z K

zL

2 2K

zL

2

( , )z F K L

constant returns to

scale for any z > 0

11CHAPTER 1 The Science of Macroeconomics

ANSWERS

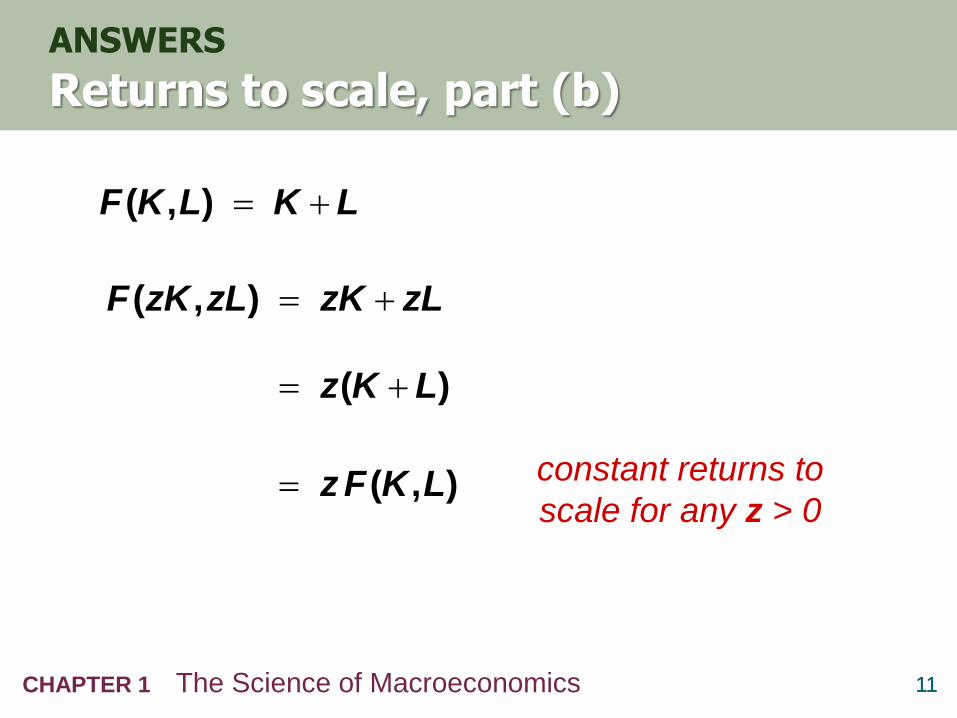

Returns to scale, part (b)

11

( , )F K L K L

( , )F zK zL zK zL

( )z K L

( , )z F K L constant returns to

scale for any z > 0

12CHAPTER 3 National Income

Assumptions

1. Technology is fixed.

2. The economy’s supplies of capital and labor

are fixed at

and K K L L

13CHAPTER 3 National Income

Determining GDP

Output is determined by the fixed factor supplies

and the fixed state of technology:

, ( )Y F K L

14CHAPTER 3 National Income

The distribution of national income

determined by factor prices,

the prices per unit firms pay for the factors of

production

wage = price of L

rental rate = price of K

15CHAPTER 3 National Income

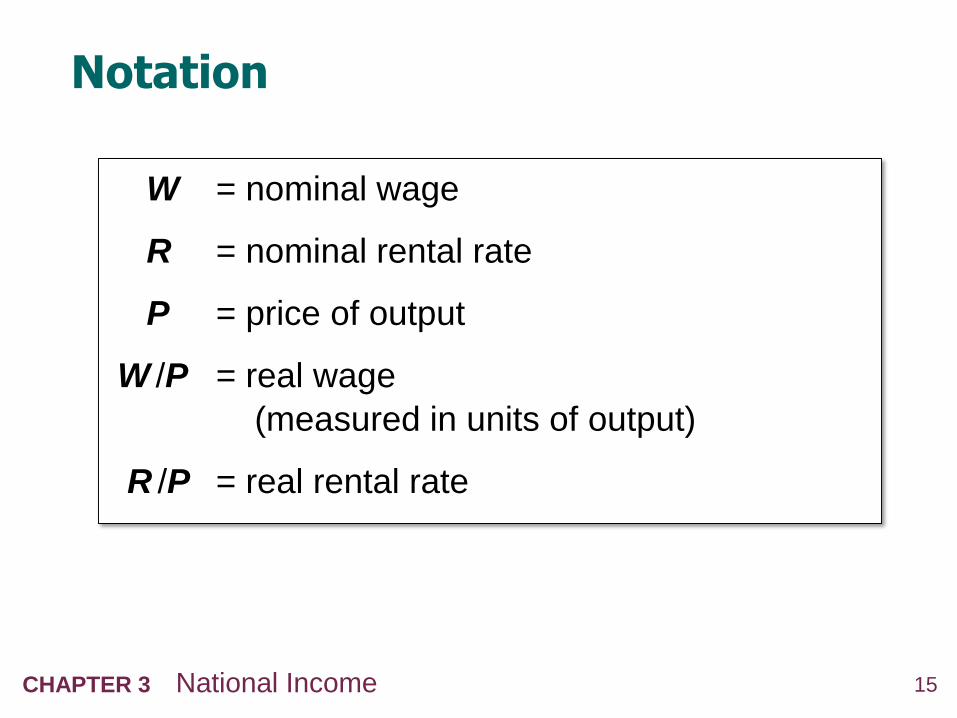

Notation

W = nominal wage

R = nominal rental rate

P = price of output

W /P = real wage

(measured in units of output)

R /P = real rental rate

16CHAPTER 3 National Income

How factor prices are determined

Factor prices determined by supply and demand

in factor markets.

Recall: Supply of each factor is fixed.

What about demand?

17CHAPTER 3 National Income

Demand for labor

Assume markets are competitive:

each firm takes W, R, and P as given.

Basic idea:

A firm hires each unit of labor

if the cost does not exceed the benefit.

cost = real wage

benefit = marginal product of labor

18CHAPTER 3 National Income

Marginal product of labor (MPL)

definition:

The extra output the firm can produce

using an additional unit of labor

(holding other inputs fixed):

MPL = F (K,L+1) – F (K,L)

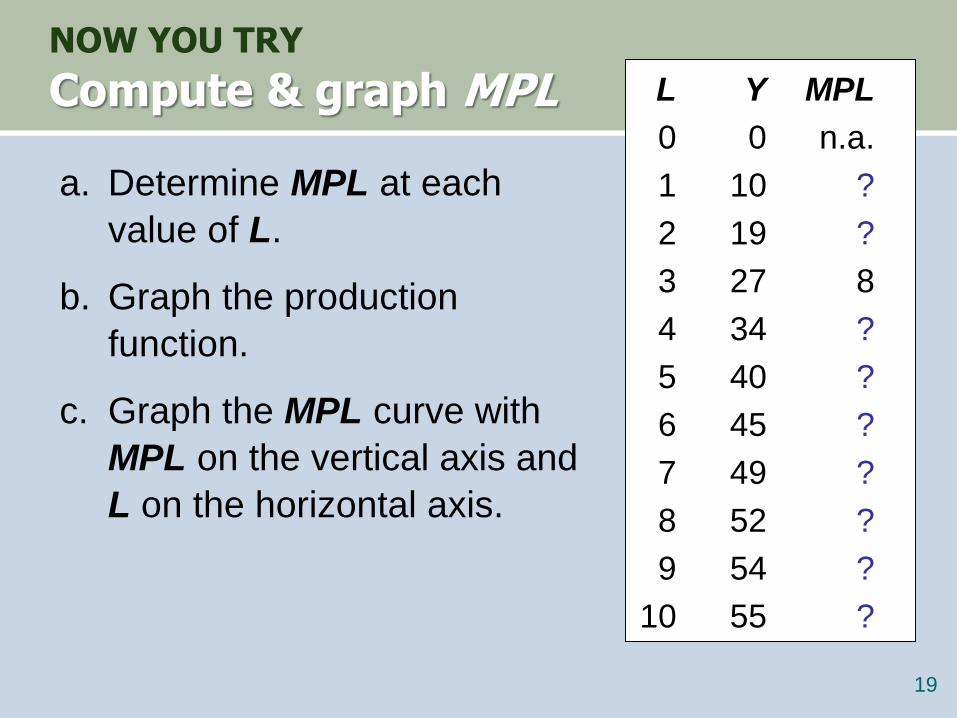

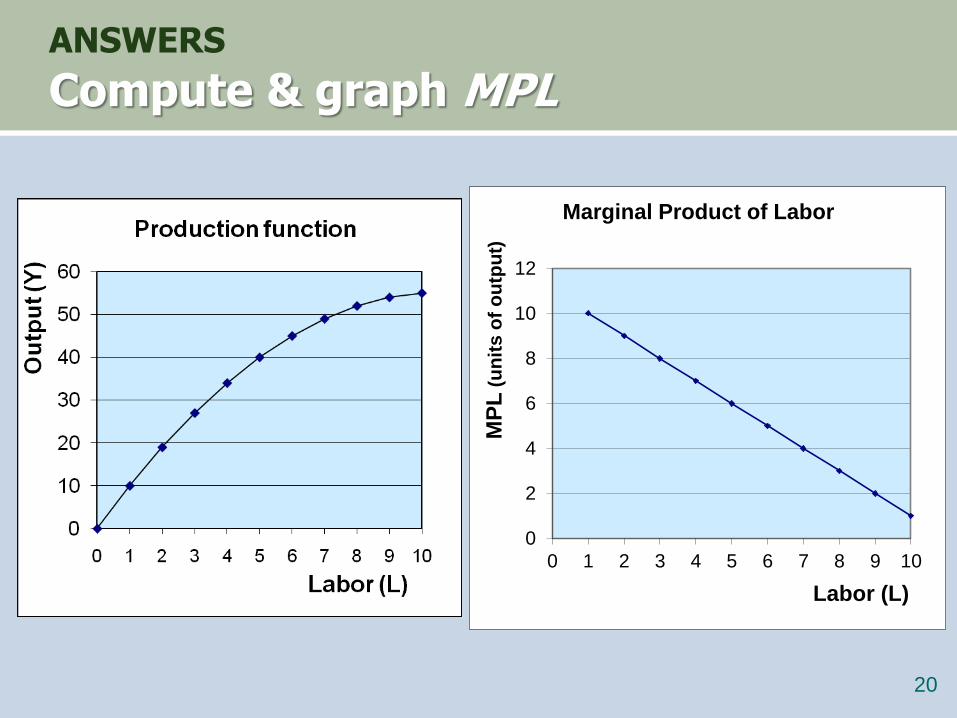

NOW YOU TRY

Compute & graph MPL

a. Determine MPL at each

value of L.

b. Graph the production

function.

c. Graph the MPL curve with

MPL on the vertical axis and

L on the horizontal axis.

19

L Y MPL

0 0 n.a.

1 10 ?

2 19 ?

3 27 8

4 34 ?

5 40 ?

6 45 ?

7 49 ?

8 52 ?

9 54 ?

10 55 ?

ANSWERS

Compute & graph MPL

20

0

2

4

6

8

10

12

0 1 2 3 4 5 6 7 8 9 10

MP

L(u

nit

s o

f o

utp

ut)

Labor (L)

Marginal Product of Labor

21CHAPTER 3 National Income

Y

output

MPL and the production function

Llabor

F K L( , )

1

MPL

1

MPL

1MPL

As more labor is

added, MPL

Slope of the production

function equals MPL

22CHAPTER 3 National Income

Diminishing marginal returns

As an input is increased,

its marginal product falls (other things equal).

Intuition:

Suppose L while holding K fixed

fewer machines per worker

lower worker productivity

NOW YOU TRY

Identifying Diminishing Returns

Which of these production functions have

diminishing marginal returns to labor?

23

a) 2 15F K L K L ( , )

F K L KL( , )b)

c) 2 15F K L K L ( , )

24CHAPTER 1 The Science of Macroeconomics

ANSWERS

Identifying Diminishing Returns

24

a) 2 15F K L K L ( , )

F K L KL( , )b)

c) 2 15F K L K L ( , )

No, MPL = 15 for all L

Yes, MPL falls as L rises

Yes, MPL falls as L rises

25CHAPTER 1 The Science of Macroeconomics

NOW YOU TRY

MPL and labor demand

Suppose W/P = 6.

If L = 3, should firm hire

more or less labor? Why?

If L = 7, should firm hire

more or less labor? Why?

25

L Y MPL

0 0 n.a.

1 10 10

2 19 9

3 27 8

4 34 7

5 40 6

6 45 5

7 49 4

8 52 3

9 54 2

10 55 1

26CHAPTER 1 The Science of Macroeconomics

ANSWERS

MPL and labor demand

If L = 3, should firm hire more or less

labor?

Answer: YES, because the benefit

of the 4th worker (MPL = 7) exceeds

its cost (W/P = 6)

If L = 7, should firm hire more or less

labor?

Answer: NO, the firm should reduce

labor. The 7th worker adds

MPL = 4 units of output but costs the

firm W/P = 6. 26

L Y MPL

0 0 n.a.

1 10 10

2 19 9

3 27 8

4 34 7

5 40 6

6 45 5

7 49 4

8 52 3

9 54 2

10 55 1

27CHAPTER 3 National Income

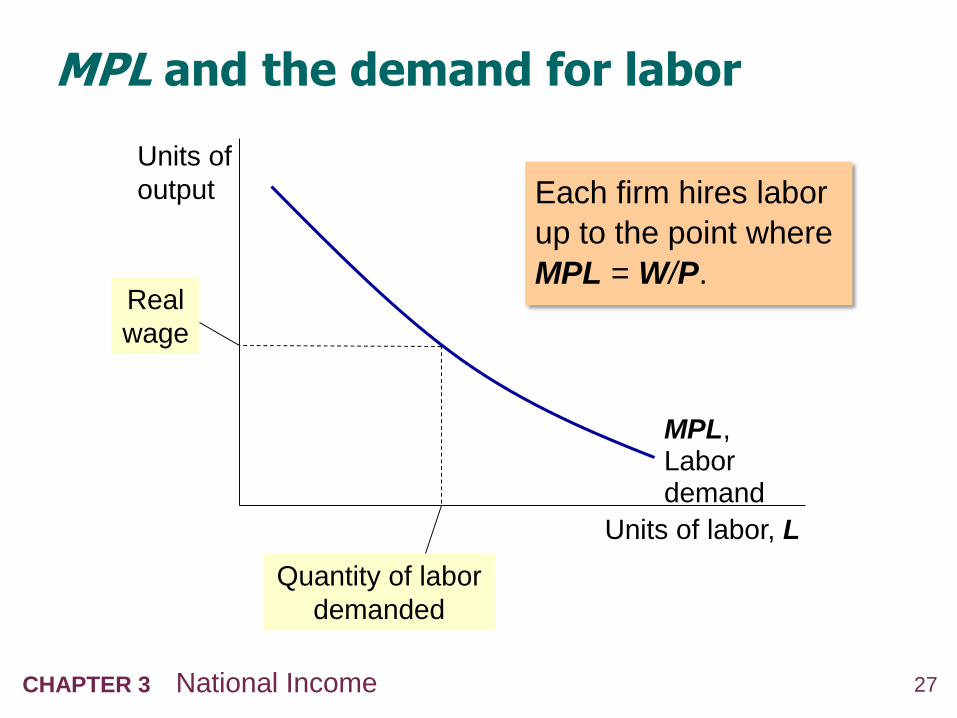

MPL and the demand for labor

Each firm hires labor

up to the point where

MPL = W/P.

Units of

output

Units of labor, L

MPL, Labor demand

Real

wage

Quantity of labor

demanded

28CHAPTER 3 National Income

The equilibrium real wage

The real wage

adjusts to equate

labor demand

with supply.

Units of

output

Units of labor, L

MPL, Labor demand

equilibrium

real wage

Labor

supply

L

29CHAPTER 3 National Income

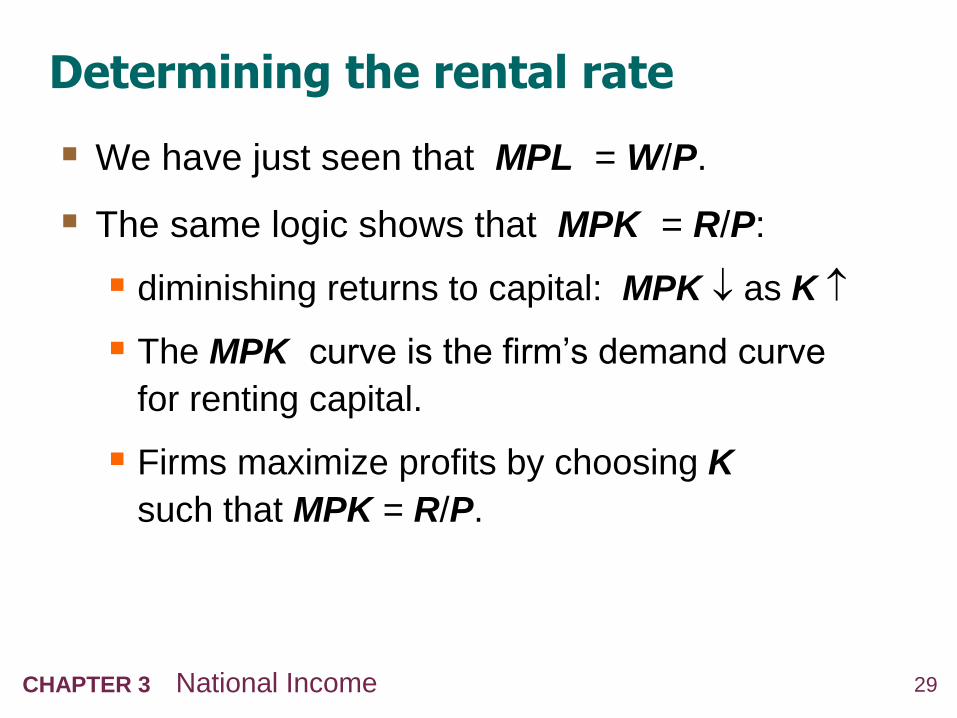

Determining the rental rate

We have just seen that MPL = W/P.

The same logic shows that MPK = R/P:

diminishing returns to capital: MPK as K

The MPK curve is the firm’s demand curve

for renting capital.

Firms maximize profits by choosing K

such that MPK = R/P.

30CHAPTER 3 National Income

The equilibrium real rental rate

The real rental rate

adjusts to equate

demand for capital

with supply.

Units of

output

Units of capital, K

MPK, demand for capital

equilibrium

R/P

Supply of

capital

K

31CHAPTER 3 National Income

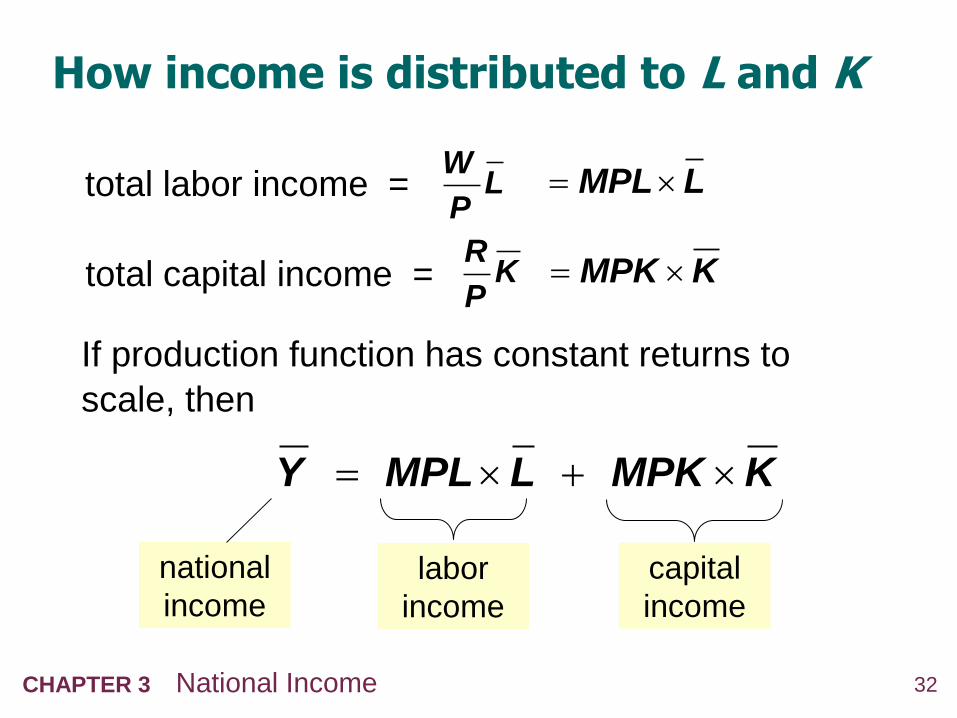

The Neoclassical Theory of Distribution

states that each factor input is paid its marginal

product

a good starting point for thinking about income

distribution

32CHAPTER 3 National Income

How income is distributed to L and K

total labor income =

If production function has constant returns to

scale, then

total capital income =

WL

PMPL L

RK

PMPK K

Y MPL L MPK K

labor

income

capital

income

national

income

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

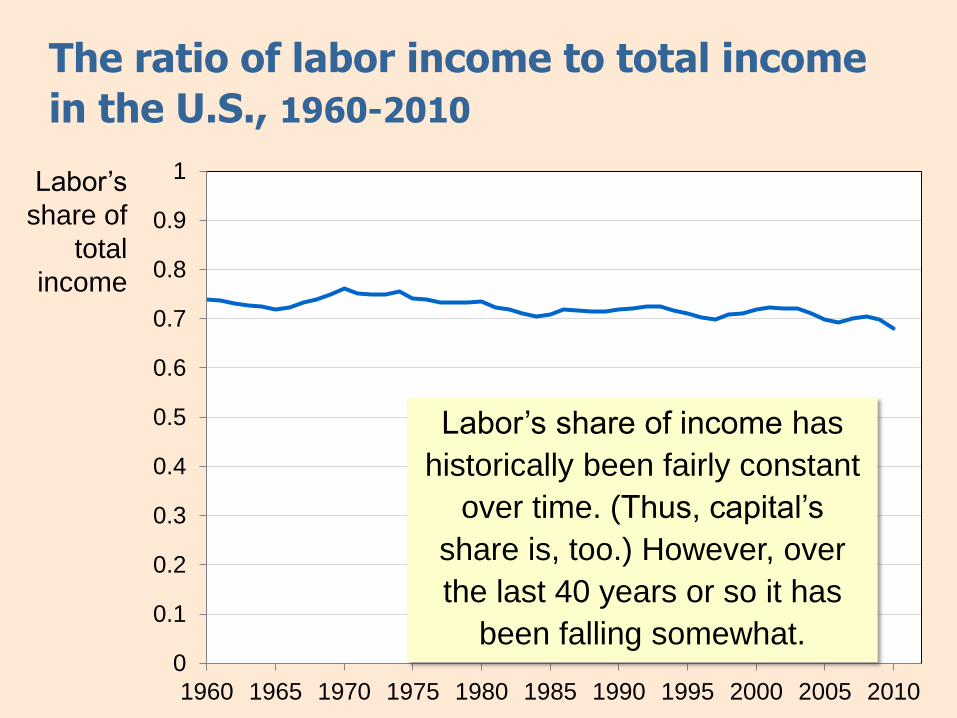

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

The ratio of labor income to total income

in the U.S., 1960-2010

Labor’s

share of

total

income

Labor’s share of income has

historically been fairly constant

over time. (Thus, capital’s

share is, too.) However, over

the last 40 years or so it has

been falling somewhat.

34CHAPTER 3 National Income

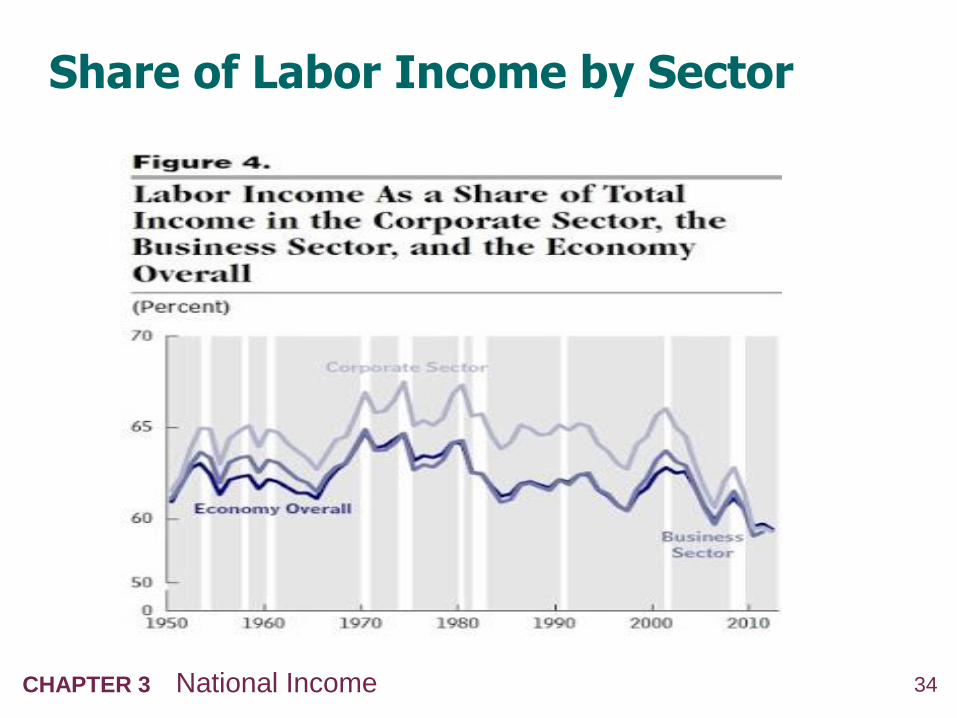

Share of Labor Income by Sector

35CHAPTER 3 National Income

The Cobb-Douglas Production Function

The Cobb-Douglas production function has

constant factor shares:

= capital’s share of total income:

capital income = MPK × K = Y

labor income = MPL × L = (1 – )Y

The Cobb-Douglas production function is:

where A represents the level of technology.

1Y AK L

36CHAPTER 3 National Income

The Cobb-Douglas Production Function

Each factor’s marginal product is proportional to

its average product:

1 1 YMPK AK L

K

(1 )(1 )

YMPL AK L

L

37CHAPTER 3 National Income

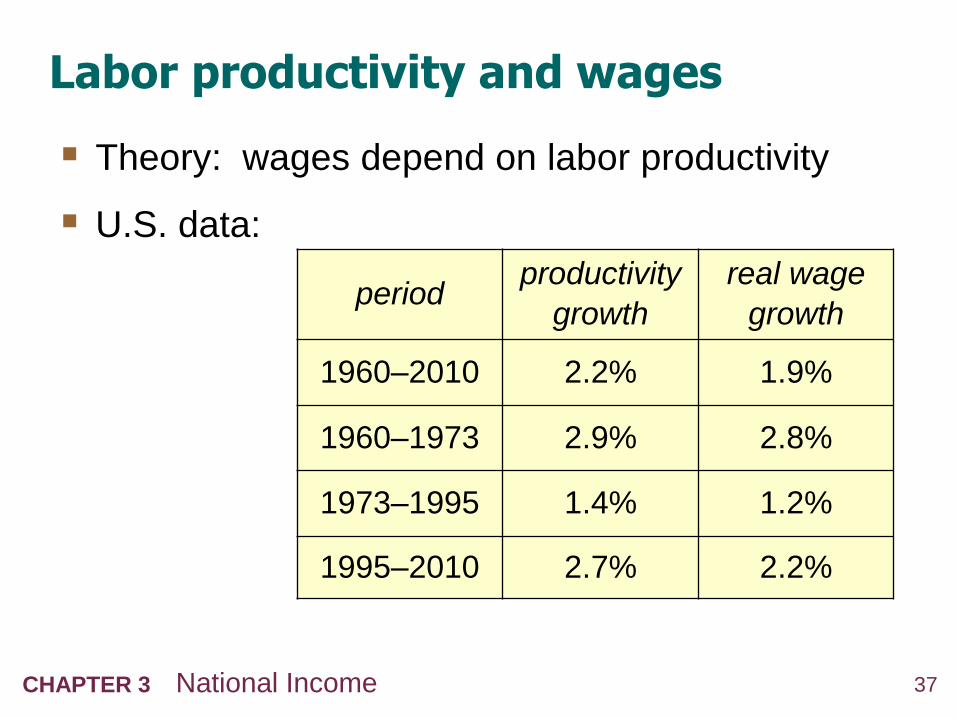

Labor productivity and wages

Theory: wages depend on labor productivity

U.S. data:

periodproductivity

growth

real wage

growth

1960–2010 2.2% 1.9%

1960–1973 2.9% 2.8%

1973–1995 1.4% 1.2%

1995–2010 2.7% 2.2%

38CHAPTER 3 National Income

Analyzing the Production Model

Per capita = per person

Per worker = per member of the labor force.

In this model, the two are equal.

We can perform a change of variables to define

output per capita (y) and capital per person (k).

39CHAPTER 3 National Income

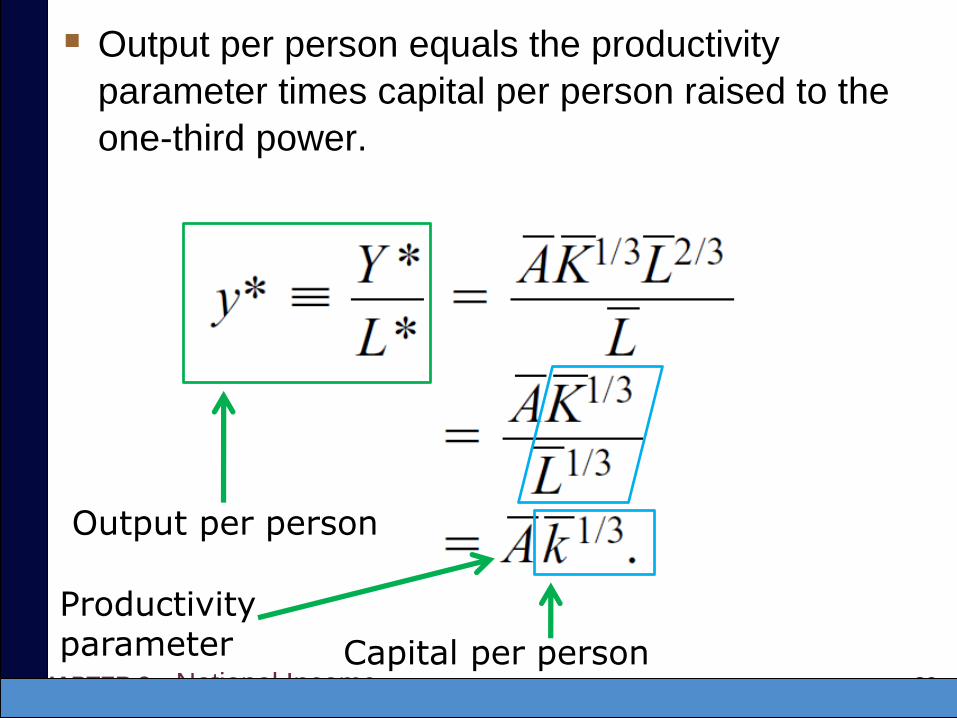

Output per person equals the productivity

parameter times capital per person raised to the

one-third power.

Output per person

Capital per person

Productivity parameter

40CHAPTER 3 National Income

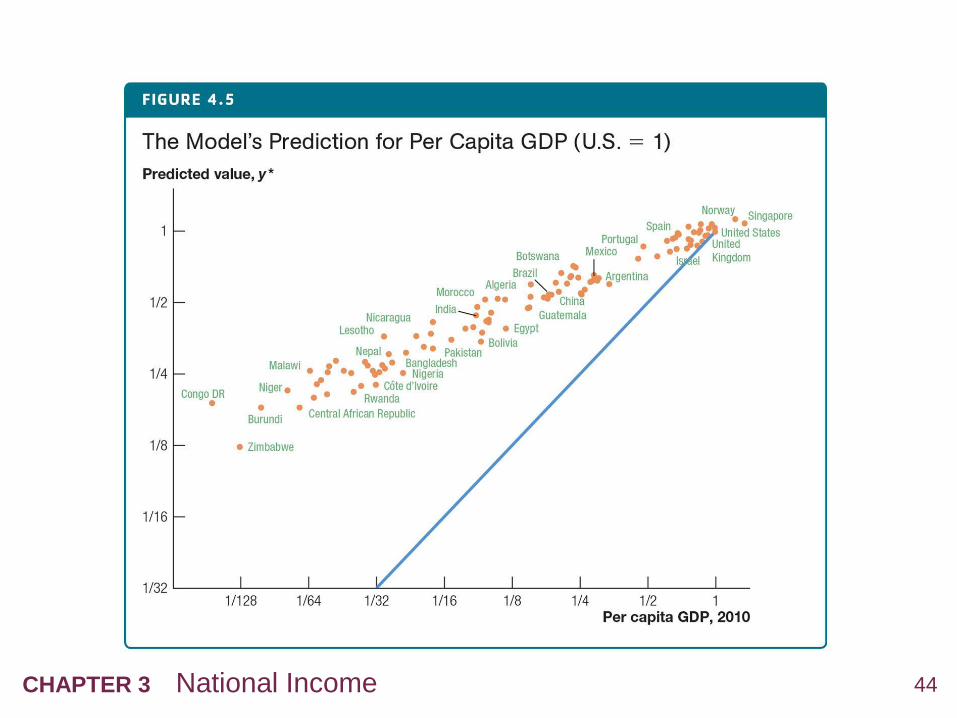

What makes a country rich or poor?

Output per person is higher if the productivity

parameter is higher or if the amount of capital

per person is higher.

What can you infer about the value of the

productivity parameter or the amount of capital

in poor countries?

41CHAPTER 3 National Income

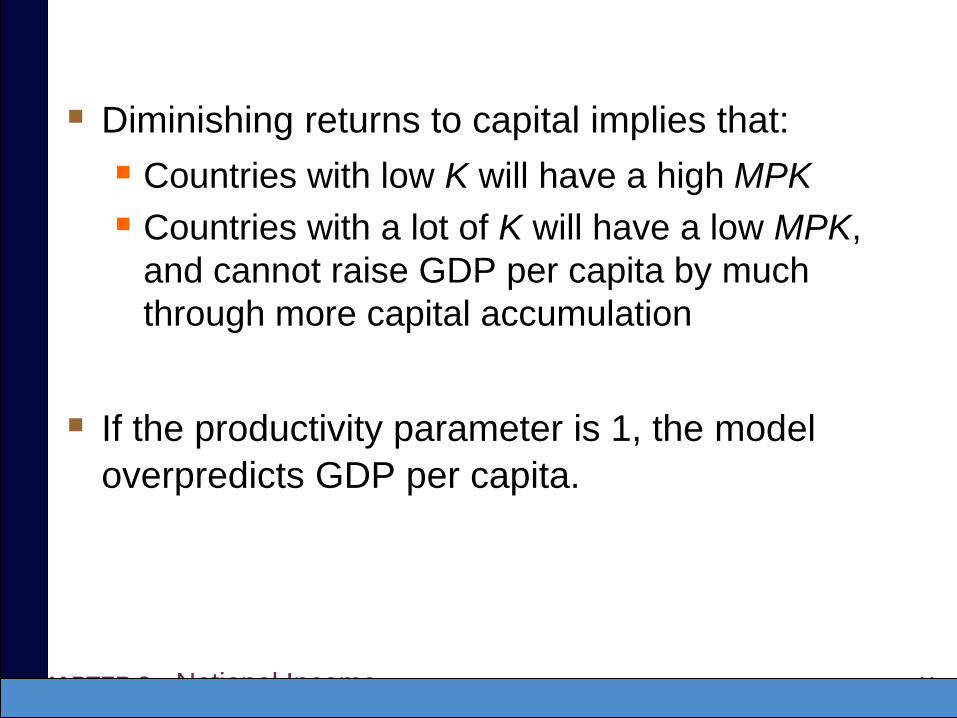

Diminishing returns to capital implies that:

Countries with low K will have a high MPK

Countries with a lot of K will have a low MPK,

and cannot raise GDP per capita by much

through more capital accumulation

If the productivity parameter is 1, the model

overpredicts GDP per capita.

42CHAPTER 3 National Income

43CHAPTER 3 National Income

44CHAPTER 3 National Income

45CHAPTER 3 National Income

Case Study: Why Doesn’t Capital Flow

from Rich to Poor Countries?

If MPK is higher in poor countries with low K,

why doesn’t capital flow to those countries?

Short Answer: Simple production model with

no difference in productivity across countries is

misguided.

We must also consider the productivity

parameter.

46CHAPTER 3 National Income

Productivity Differences:

Improving the Fit of the Model

The productivity parameter measures how

efficiently countries are using their factor

inputs.

Often called total factor productivity (TFP)

If TFP is no longer equal to 1, we can obtain

a better fit of the model.

47CHAPTER 3 National Income

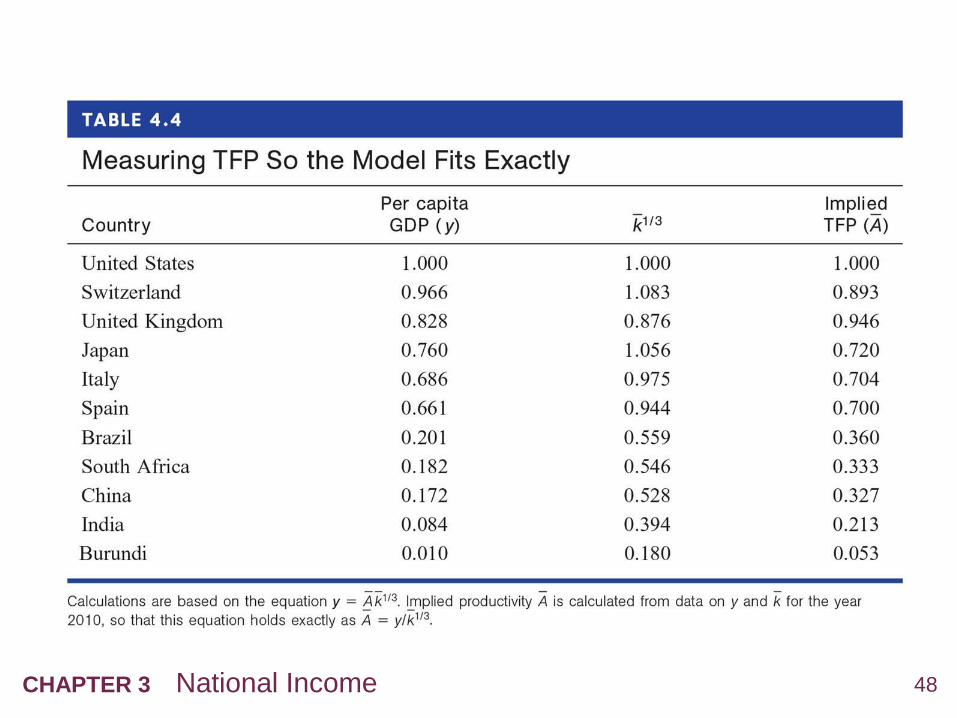

However, data on TFP is not collected.

It can be calculated because we have data on

output and capital per person.

TFP is referred to as the “residual.”

A lower level of TFP

Implies that workers produce less output for any

given level of capital per person

48CHAPTER 3 National Income

49CHAPTER 3 National Income

50CHAPTER 3 National Income

51CHAPTER 3 National Income

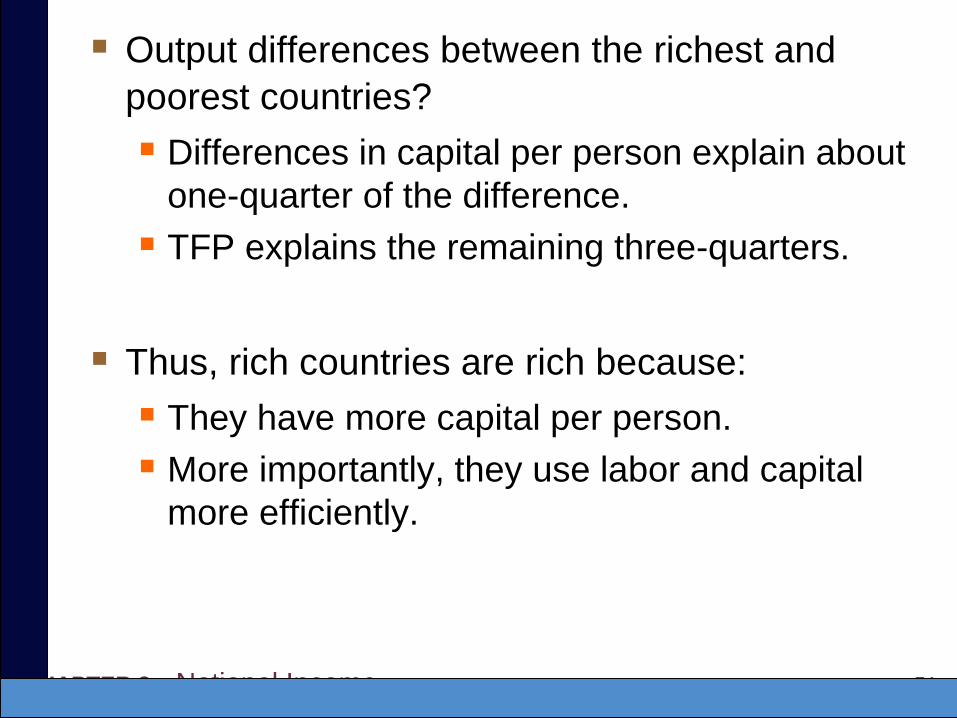

Output differences between the richest and

poorest countries?

Differences in capital per person explain about

one-quarter of the difference.

TFP explains the remaining three-quarters.

Thus, rich countries are rich because:

They have more capital per person.

More importantly, they use labor and capital

more efficiently.

52CHAPTER 3 National Income

Outline of model

A closed economy, market-clearing model

Supply side

factor markets (supply, demand, price)

determination of output/income

Demand side

determinants of C, I, and G

Equilibrium

goods market

loanable funds market

DONE

DONE

Next

53CHAPTER 3 National Income

Demand for goods and services

Components of aggregate demand:

C = consumer demand for g & s

I = demand for investment goods

G = government demand for g & s

(closed economy: no NX )

54CHAPTER 3 National Income

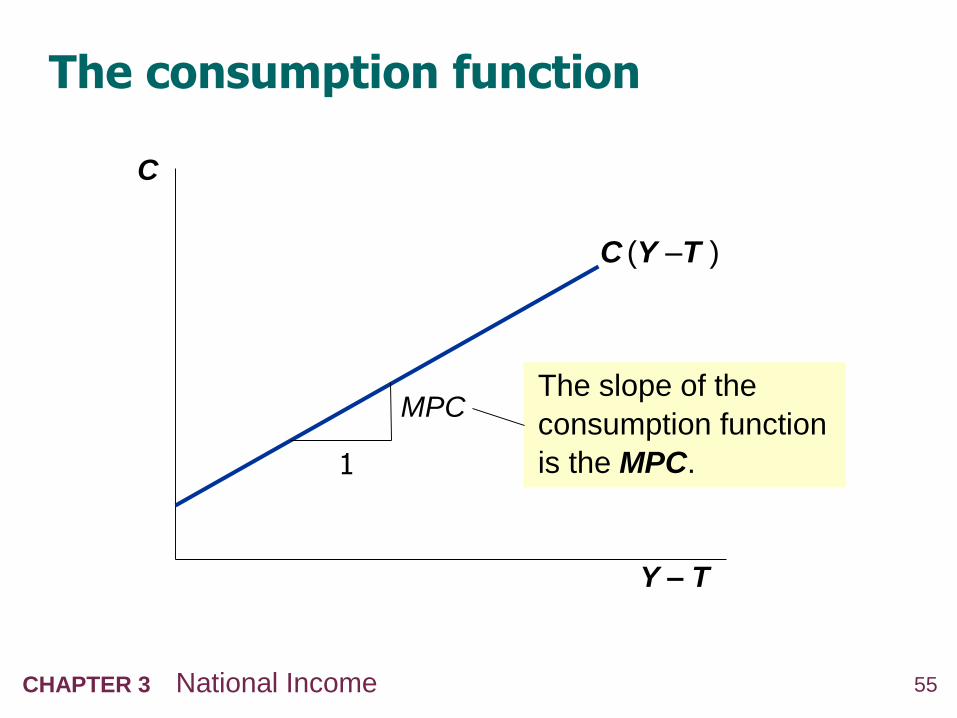

Consumption, C

def: Disposable income is total income minus

total taxes: Y – T.

Consumption function: C = C (Y – T )

Shows that (Y – T ) C

def: Marginal propensity to consume (MPC)

is the change in C when disposable income

increases by one dollar.

55CHAPTER 3 National Income

The consumption function

C

Y – T

C (Y –T )

1

MPCThe slope of the

consumption function

is the MPC.

56CHAPTER 3 National Income

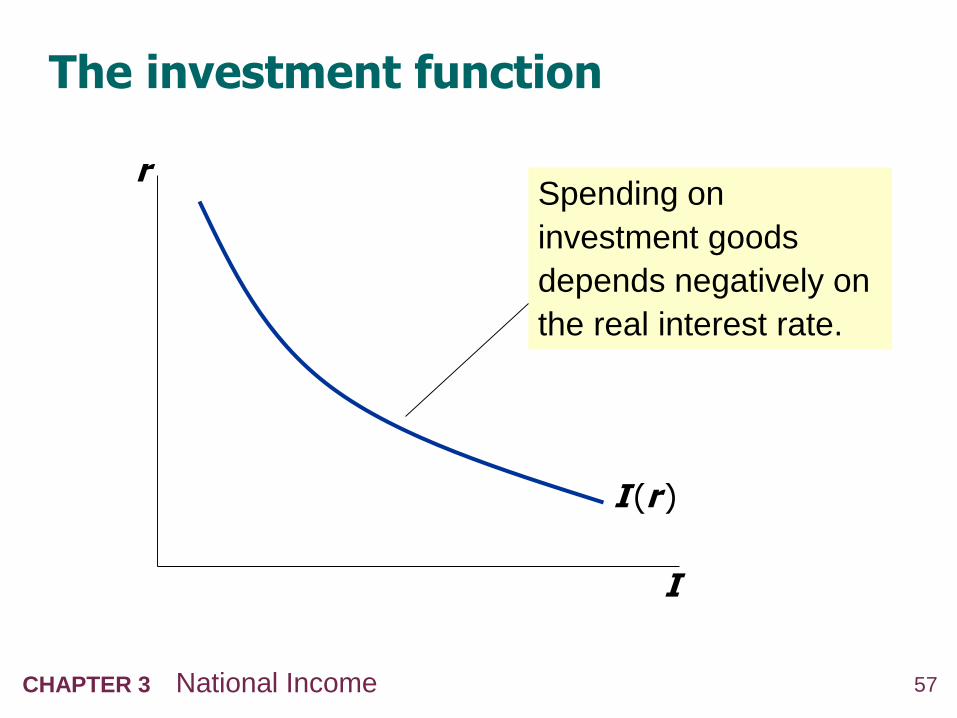

Investment, I

The investment function is I = I (r )

where r denotes the real interest rate,

the nominal interest rate corrected for inflation.

The real interest rate is

the cost of borrowing

the opportunity cost of using one’s own

funds to finance investment spending

So, r I

57CHAPTER 3 National Income

The investment function

r

I

I (r )

Spending on

investment goods

depends negatively on

the real interest rate.

58CHAPTER 3 National Income

Government spending, G

G = govt spending on goods and services

G excludes transfer payments

(e.g., Social Security benefits,

unemployment insurance benefits)

Assume government spending and total taxes

are exogenous:

and G G T T

59CHAPTER 3 National Income

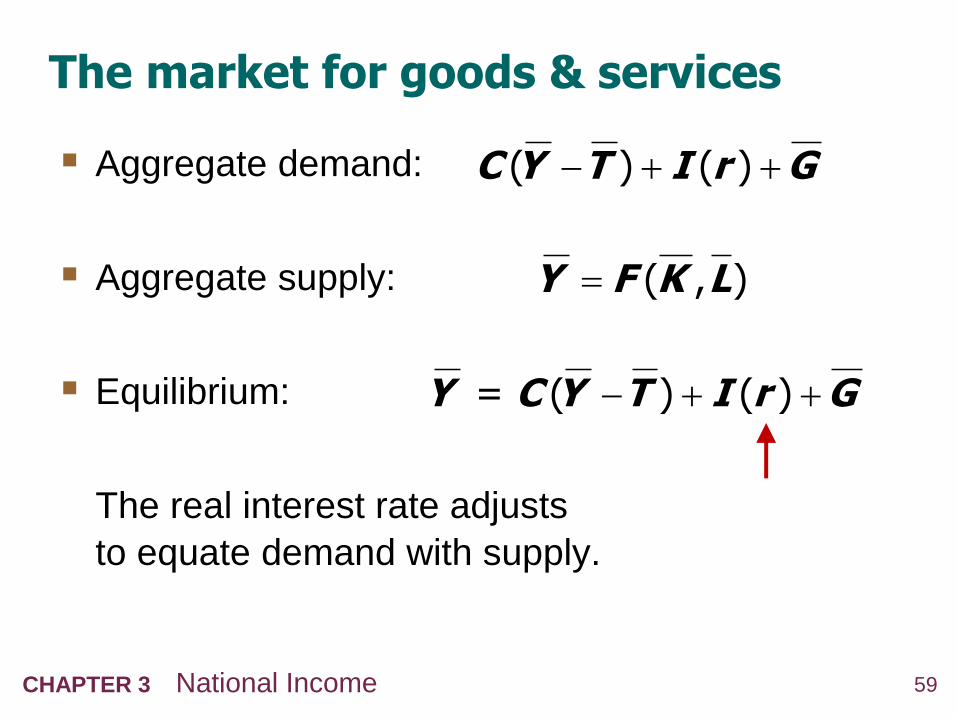

The market for goods & services

Aggregate demand:

Aggregate supply:

Equilibrium:

The real interest rate adjusts

to equate demand with supply.

( ) ( )C Y T I r G

( , )Y F K L

= ( ) ( )Y C Y T I r G

60CHAPTER 3 National Income

The loanable funds market

A simple supply–demand model of the financial

system.

One asset: “loanable funds”

demand for funds: investment

supply of funds: saving

“price” of funds: real interest rate

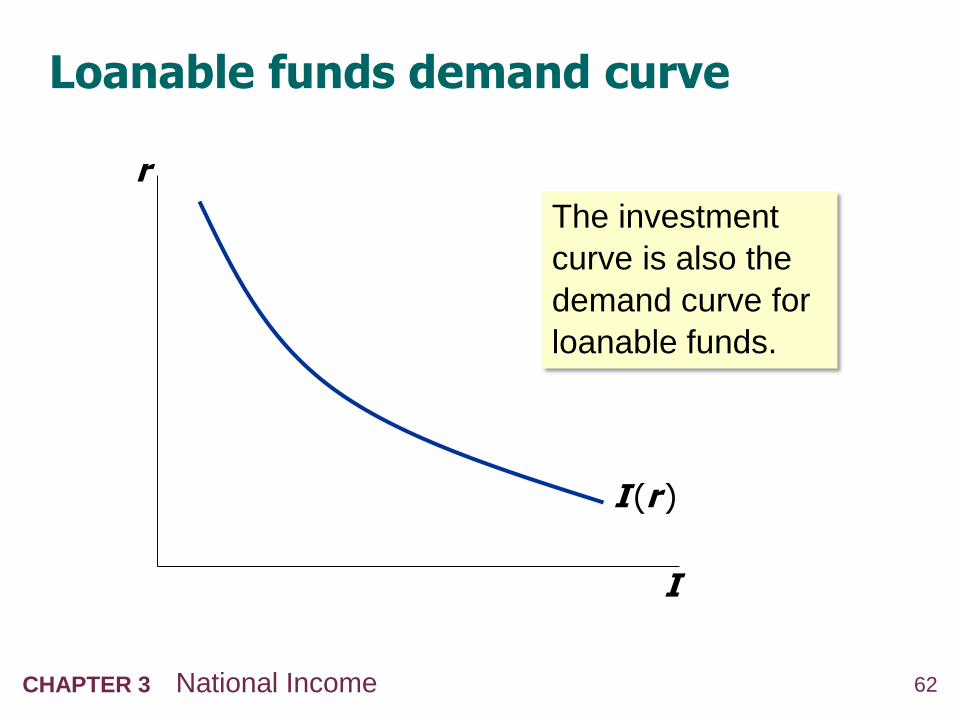

61CHAPTER 3 National Income

Demand for funds: Investment

The demand for loanable funds…

comes from investment:

Firms borrow to finance spending on plant &

equipment, new office buildings, etc.

Consumers borrow to buy new houses.

depends negatively on r,

the “price” of loanable funds

(cost of borrowing).

62CHAPTER 3 National Income

Loanable funds demand curve

r

I

I (r )

The investment

curve is also the

demand curve for

loanable funds.

63CHAPTER 3 National Income

Supply of funds: Saving

The supply of loanable funds comes from

saving:

Households use their saving to make bank

deposits, purchase bonds and other assets.

These funds become available to firms to

borrow to finance investment spending.

The government may also contribute to saving

if it does not spend all the tax revenue it

receives.

64CHAPTER 3 National Income

Types of saving

private saving = (Y – T ) – C

public saving = T – G

national saving, S

= private saving + public saving

= (Y –T ) – C + T – G

= Y – C – G

65CHAPTER 3 National Income

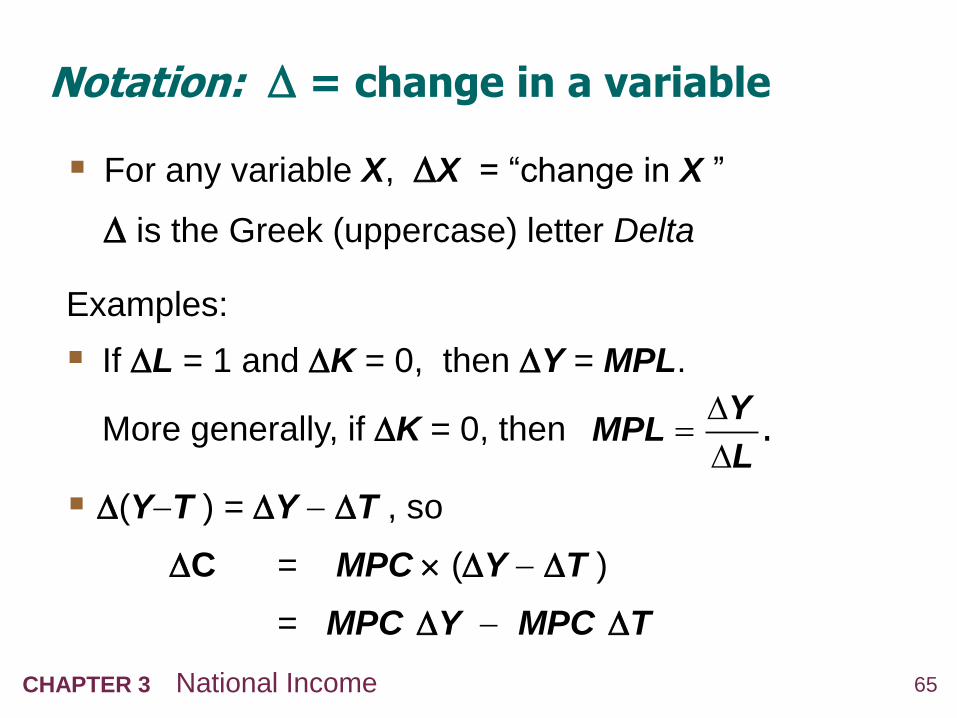

Notation: = change in a variable

For any variable X, X = “change in X ”

is the Greek (uppercase) letter Delta

Examples:

If L = 1 and K = 0, then Y = MPL.

More generally, if K = 0, thenY

MPLL

.

(YT ) = Y T , so

C = MPC (Y T )

= MPC Y MPC T

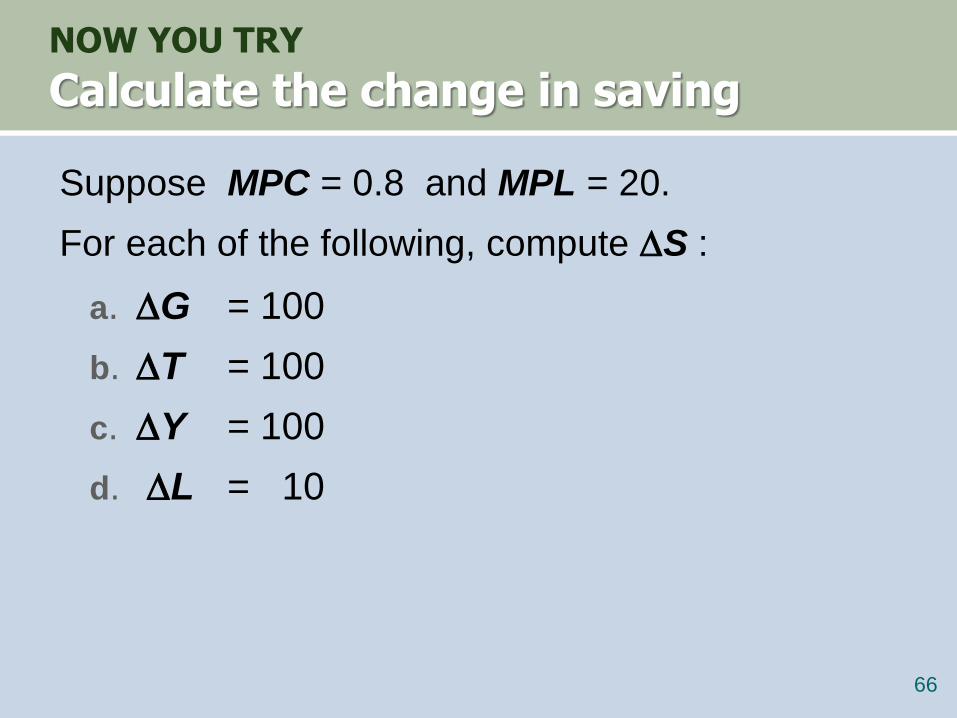

NOW YOU TRY

Calculate the change in saving

Suppose MPC = 0.8 and MPL = 20.

For each of the following, compute S :

a. G = 100

b. T = 100

c. Y = 100

d. L = 10

66

67CHAPTER 1 The Science of Macroeconomics

NOW YOU TRY

Answers

67

S Y C G 0.8( )Y Y T G

0.2 0.8Y T G

1. 0a 0S

0.8 0 0b. 10 8S

0.2 0 0c. 10 2S

MPL 20 10 20 ,d. 0Y L

0.2 0.2 200 40.S Y

68CHAPTER 3 National Income

Budget surpluses and deficits

If T > G, budget surplus = (T – G)

= public saving.

If T < G, budget deficit = (G – T)

and public saving is negative.

If T = G , balanced budget, public saving = 0.

The U.S. government finances its deficit by

issuing Treasury bonds–i.e., borrowing.

U.S. Federal Government Surplus/Deficit, 1940–2016

pe

rce

nt

of

GD

P

-35

-30

-25

-20

-15

-10

-5

0

5

10

1940 1950 1960 1970 1980 1990 2000 2010

U.S. Federal Government Debt, 1940–2016

pe

rce

nt

of

GD

P

0

20

40

60

80

100

120

140

1940 1950 1960 1970 1980 1990 2000 2010

71CHAPTER 3 National Income

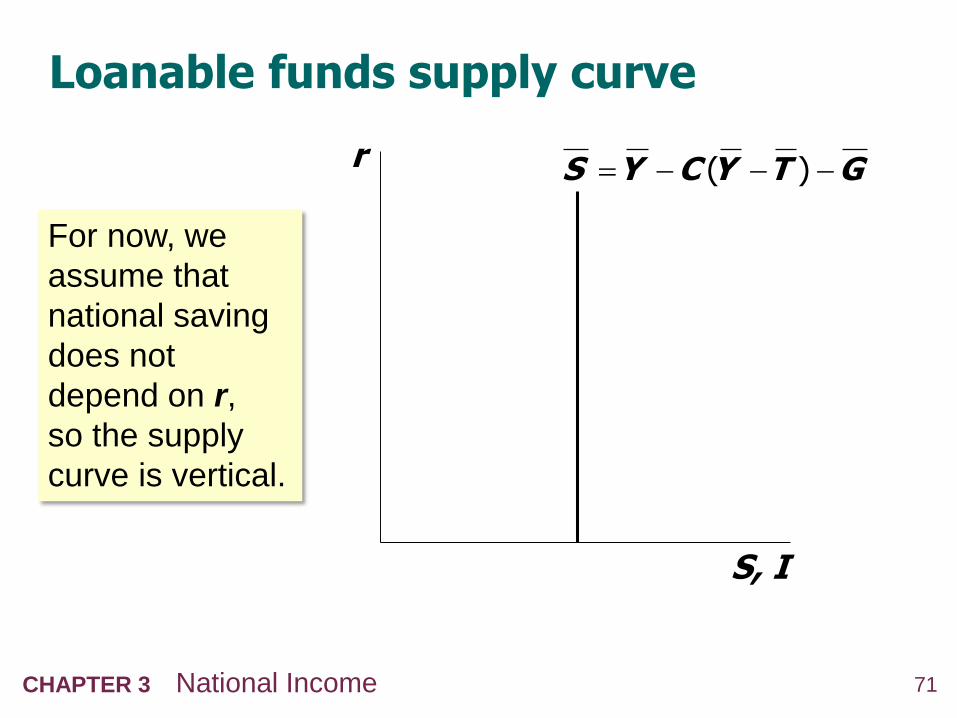

Loanable funds supply curve

r

S, I

( )S Y C Y T G

For now, we

assume that

national saving

does not

depend on r,

so the supply

curve is vertical.

72CHAPTER 3 National Income

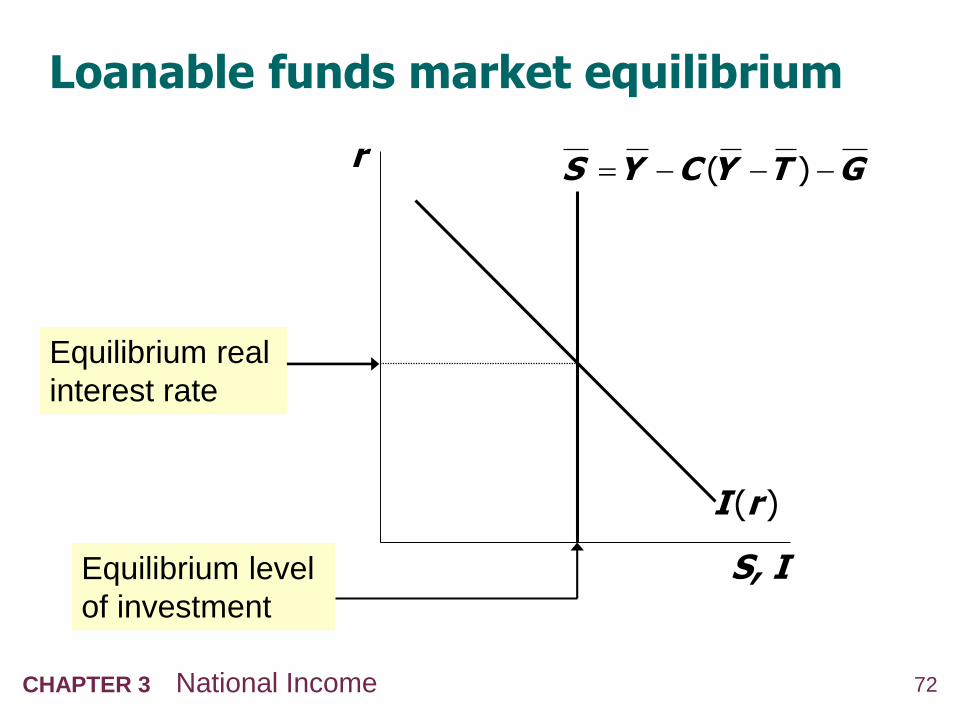

Loanable funds market equilibrium

r

S, I

I (r )

( )S Y C Y T G

Equilibrium real

interest rate

Equilibrium level

of investment

73CHAPTER 3 National Income

The special role of r

r adjusts to equilibrate the goods market and the

loanable funds market simultaneously:

If L.F. market in equilibrium, then

Y – C – G = I

Add (C +G ) to both sides to get

Y = C + I + G (goods market eq’m)

Thus, Eq’m in L.F.

market

Eq’m in goods

market

74CHAPTER 3 National Income

Digression: Mastering models

To master a model, be sure to know:

1. Which of its variables are endogenous and

which are exogenous.

2. For each curve in the diagram, know:

a. definition

b. intuition for slope

c. all the things that can shift the curve

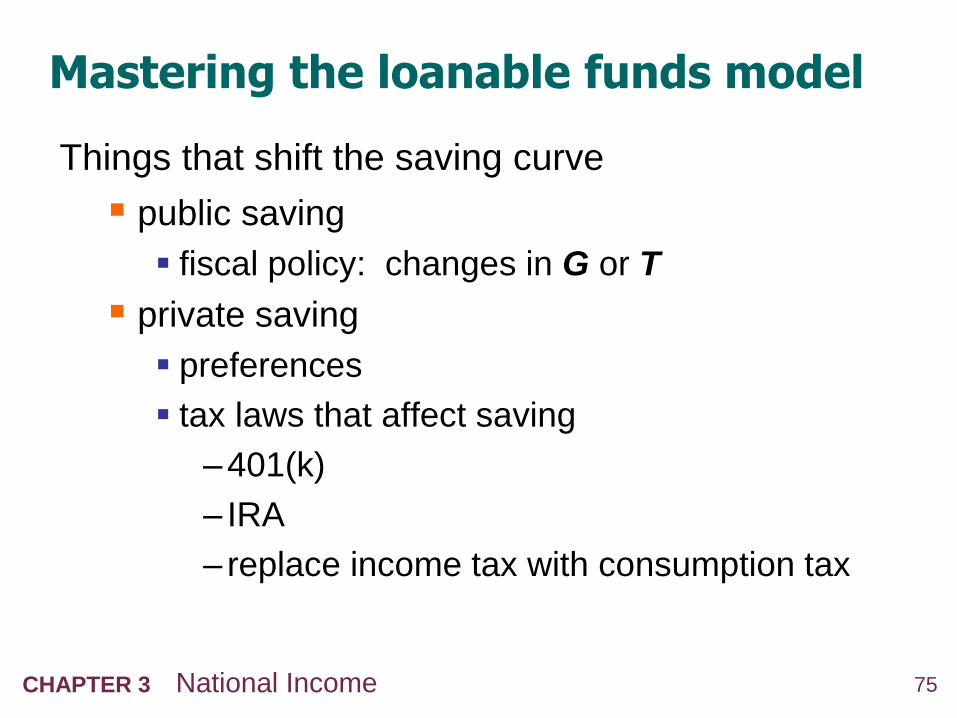

75CHAPTER 3 National Income

Mastering the loanable funds model

Things that shift the saving curve

public saving

fiscal policy: changes in G or T

private saving

preferences

tax laws that affect saving

–401(k)

– IRA

– replace income tax with consumption tax

76CHAPTER 3 National Income

CASE STUDY:

The Reagan deficits

Reagan policies during early 1980s:

increases in defense spending: G > 0

big tax cuts: T < 0

Both policies reduce national saving:

( )S Y C Y T G

G S T C S

77CHAPTER 3 National Income

CASE STUDY:

The Reagan deficits

r

S, I

1S

I (r )

r1

I1

r22. …which causes

the real interest

rate to rise…

I2

3. …which reduces

the level of

investment.

1. The increase in

the deficit

reduces saving…

2S

78CHAPTER 3 National Income

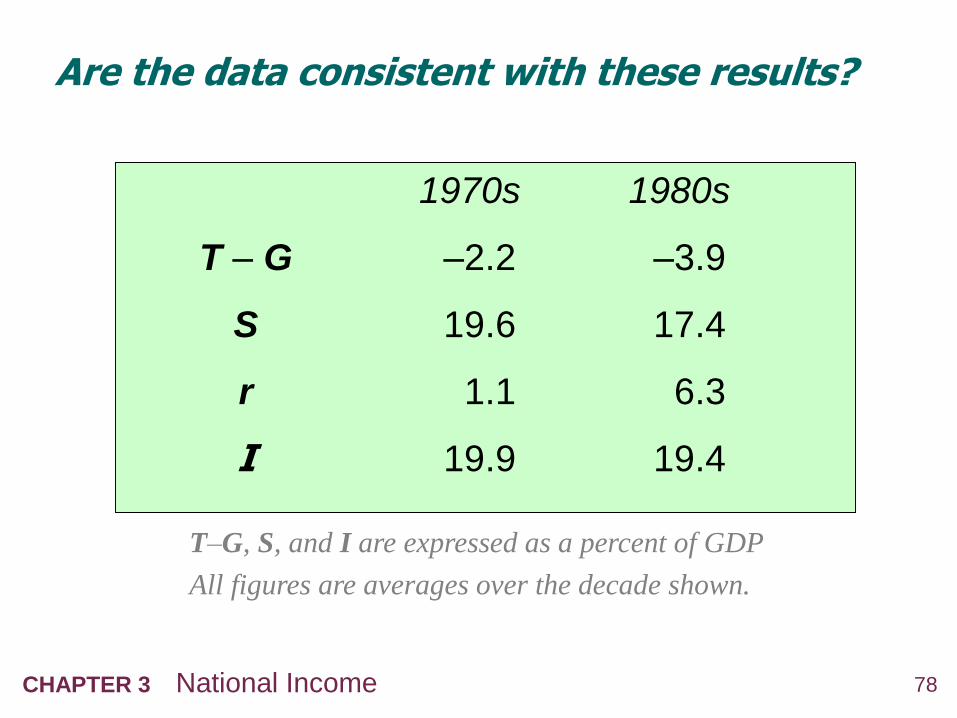

Are the data consistent with these results?

1970s 1980s

T – G –2.2 –3.9

S 19.6 17.4

r 1.1 6.3

I 19.9 19.4

T–G, S, and I are expressed as a percent of GDP

All figures are averages over the decade shown.

79CHAPTER 3 National Income

Mastering the loanable funds model, continued

Things that shift the investment curve:

some technological innovations

to take advantage some innovations,

firms must buy new investment goods

tax laws that affect investment

e.g., investment tax credit

80CHAPTER 3 National Income

An increase in investment demand

An increase in desired investment…

r

S, I

I1

S

I2

r1

r2

…raises the

interest rate.

But the equilibrium

level of investment

cannot increase

because the

supply of loanable

funds is fixed.

81CHAPTER 3 National Income

Another look at Consumption, Saving

and the interest rate Why might saving depend on r ?

How would the results of an increase in

investment demand be different?

Would r rise as much?

Would the equilibrium value of I change?

82CHAPTER 3 National Income

An increase in investment demand when

saving depends on r

r

S, I

I(r)

( )S r

I(r)2

r1

r2

An increase in

investment demand

raises r,

which induces an

increase in the

quantity of saving,

which allows Ito increase.

I1 I2

83CHAPTER 3 National Income

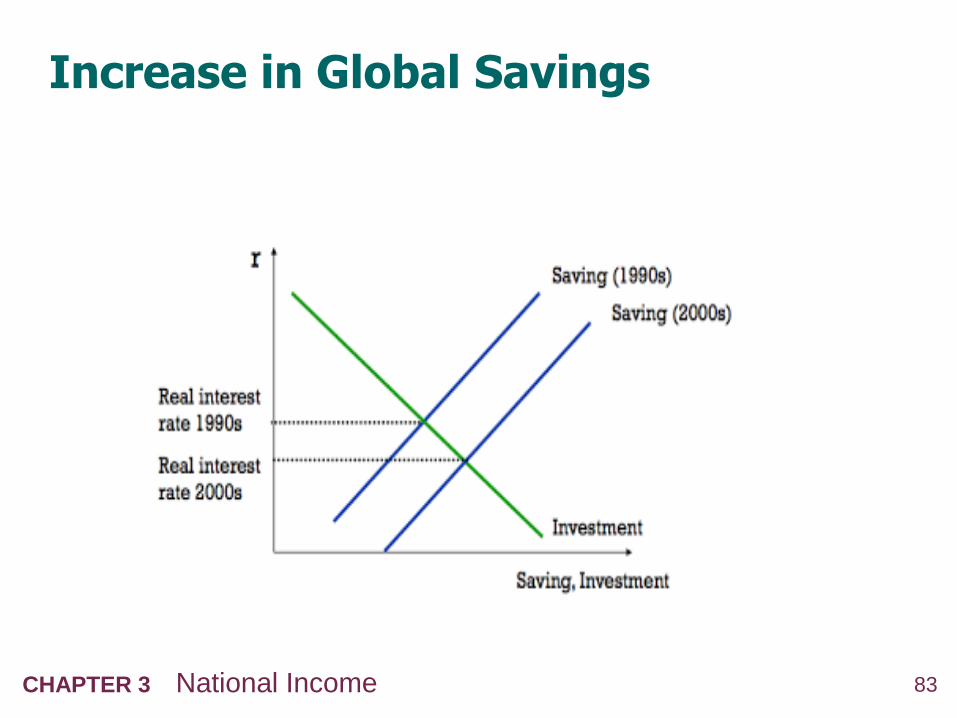

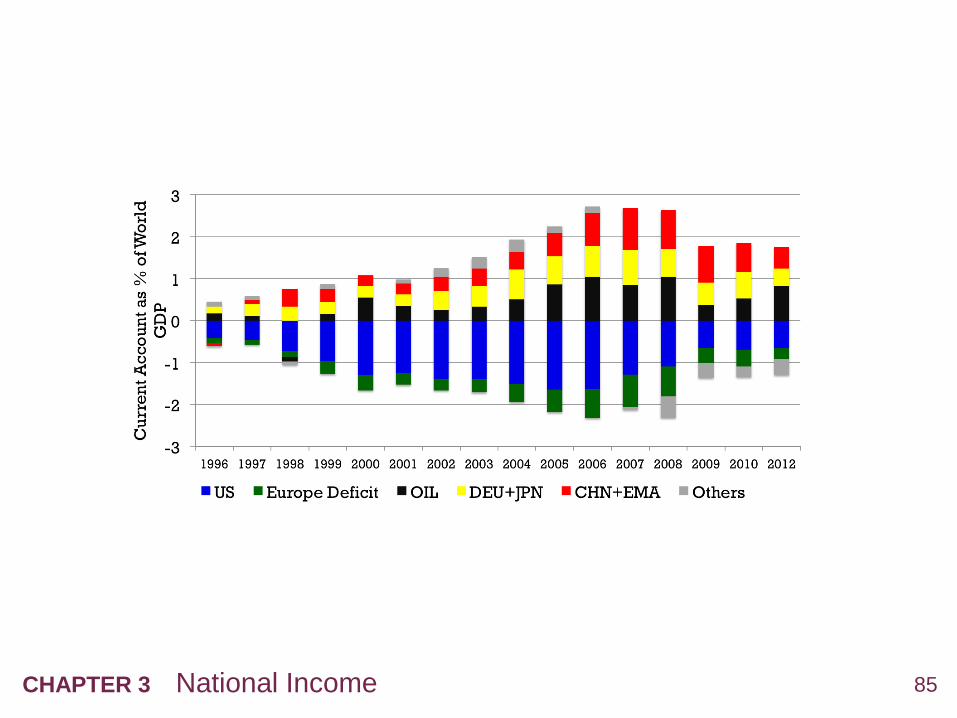

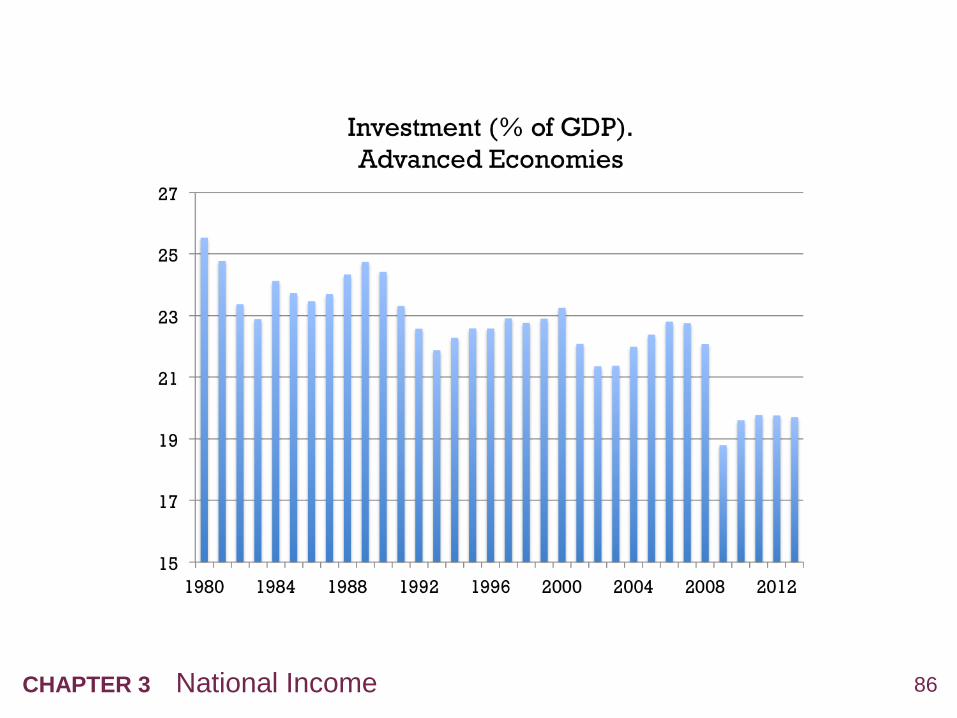

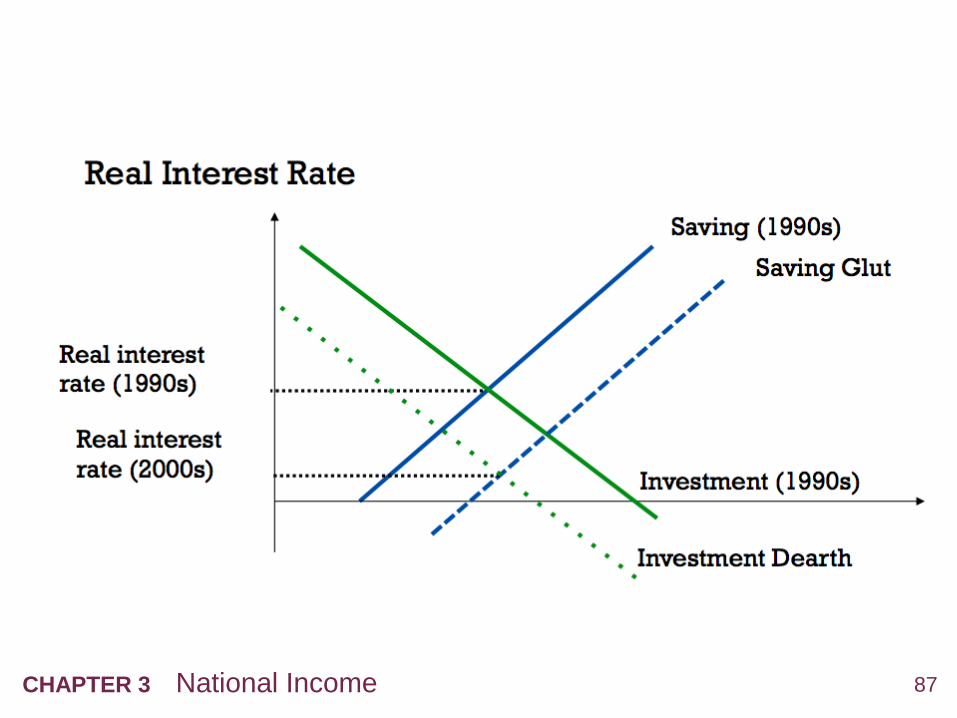

Increase in Global Savings

84CHAPTER 3 National Income

Effect on Global Balances

85CHAPTER 3 National Income

86CHAPTER 3 National Income

87CHAPTER 3 National Income

88CHAPTER 3 National Income

Consumption

How do you decide how much to spend on

consumption?

89CHAPTER 3 National Income

Consumption

2 competing views of consumption

1. Consumption depends primarily on current

income (Keynesian consumption function).

2. People prefer a smooth path for consumption

compared to a path that involves large

movements (Permanent Income/Life Cycle

Hypothesis).

90CHAPTER 3 National Income

The Keynesian consumption function

C

Y

C C cY

slope = APC

As income rises, consumers save a bigger

fraction of their income, so APC falls.

C Cc

Y Y APC

91CHAPTER 3 National Income

Early empirical successes: Results from early studies Households with higher incomes:

consume more, MPC > 0

save more, MPC < 1

save a larger fraction of their income,

APC as Y

Very strong correlation between income and

consumption:

income seemed to be the main

determinant of consumption

92CHAPTER 3 National Income

Problems for the

Keynesian consumption function

Based on the Keynesian consumption function,

economists predicted that C would grow more

slowly than Y over time.

This prediction did not come true:

As incomes grew, APC did not fall,

and C grew at the same rate as income.

Simon Kuznets showed that C/Y was

very stable from decade to decade.

93CHAPTER 3 National Income

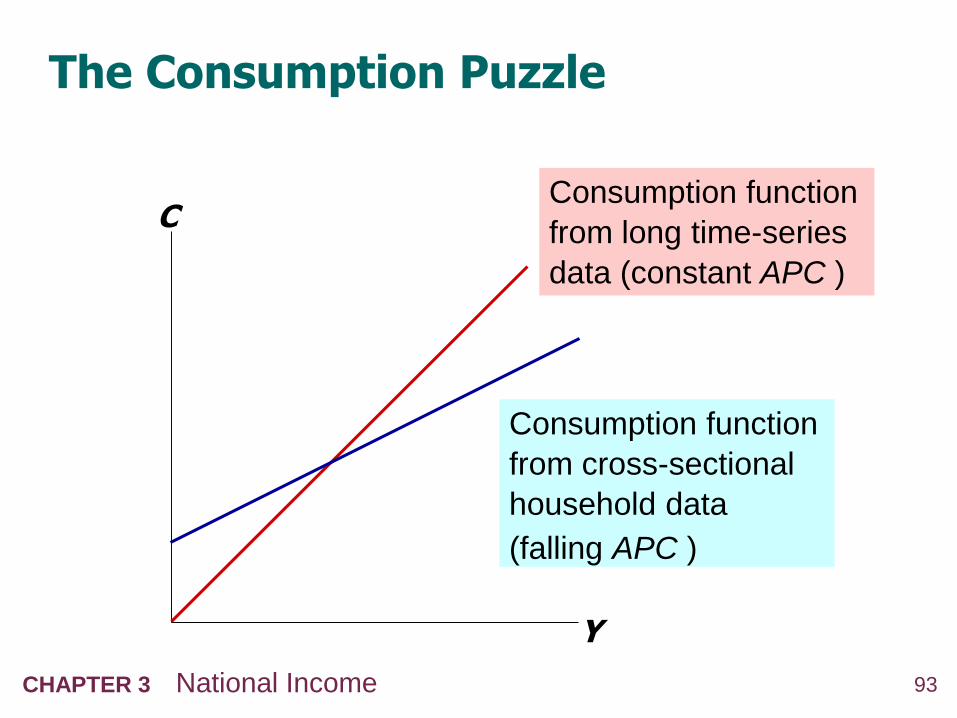

The Consumption Puzzle

C

Y

Consumption function

from long time-series

data (constant APC )

Consumption function

from cross-sectional

household data

(falling APC )

94CHAPTER 3 National Income

Irving Fisher and Intertemporal Choice

The basis for much subsequent work on

consumption.

Assumes consumer is forward-looking and

chooses consumption for the present and future

to maximize lifetime satisfaction.

Consumer’s choices are subject to an

intertemporal budget constraint,

a measure of the total resources available for

present and future consumption.

95CHAPTER 3 National Income

The basic two-period model

Period 1: the present

Period 2: the future

Notation

Y1, Y2 = income in period 1, 2

C1, C2 = consumption in period 1, 2

S = Y1 C1 = saving in period 1

(S < 0 if the consumer borrows in period 1)

96CHAPTER 3 National Income

Deriving the intertemporal

budget constraint

Period 2 budget constraint:

2 2 (1 )C Y r S

2 1 1(1 )( )Y r Y C

Rearrange terms:

1 2 2 1(1 ) (1 )r C C Y r Y

Divide through by (1+r ) to get…

97CHAPTER 3 National Income

The intertemporal budget constraint

2 21 1

1 1

C YC Y

r r

present value of

lifetime consumption

present value of

lifetime income

98CHAPTER 3 National Income

The intertemporal budget constraint

The budget

constraint shows

all combinations

of C1 and C2 that

just exhaust the

consumer’s

resources.C1

C2

1 2 (1 )Y Y r

1 2(1 )r Y Y

Y1

Y2

Borrowing

SavingConsump =

income in

both periods

2 21 1

1 1

C YC Y

r r

99CHAPTER 3 National Income

The intertemporal budget constraint

The slope of

the budget

line equals

(1+r )

C1

C2

Y1

Y2

1

(1+r )

2 21 1

1 1

C YC Y

r r

100CHAPTER 3 National Income

Consumer preferences

An indifference

curve shows

all combinations

of C1 and C2

that make the

consumer

equally happy.

C1

C2

IC1

IC2

Higher

indifference

curves

represent

higher levels

of happiness.

101CHAPTER 3 National Income

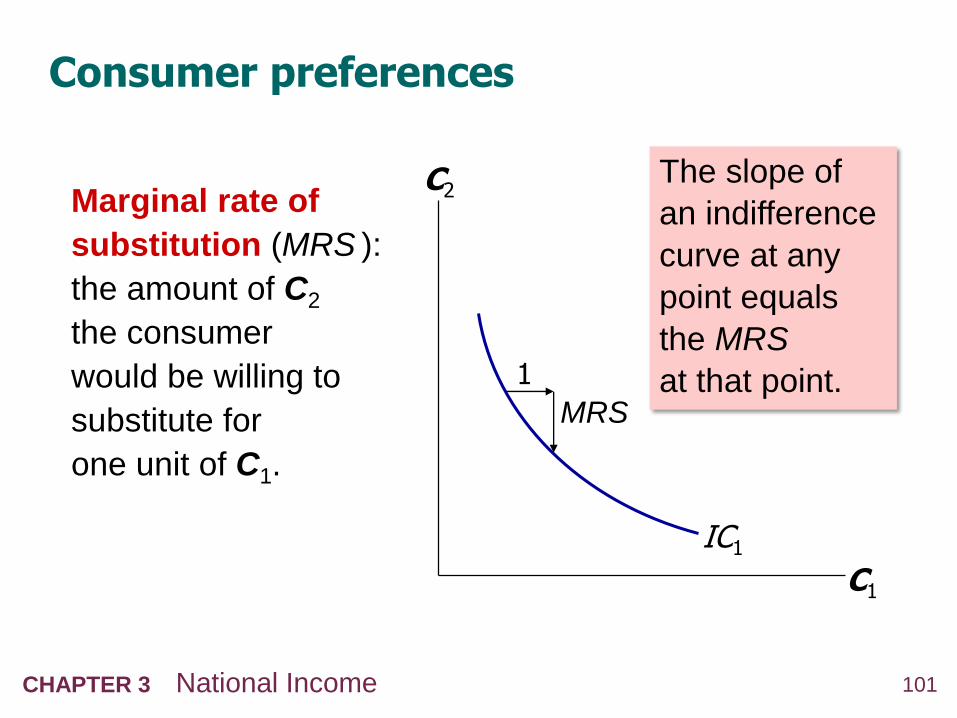

Consumer preferences

Marginal rate of

substitution (MRS ):

the amount of C2

the consumer

would be willing to

substitute for

one unit of C1.

C1

C2

IC1

The slope of

an indifference

curve at any

point equals

the MRS

at that point.1

MRS

102CHAPTER 3 National Income

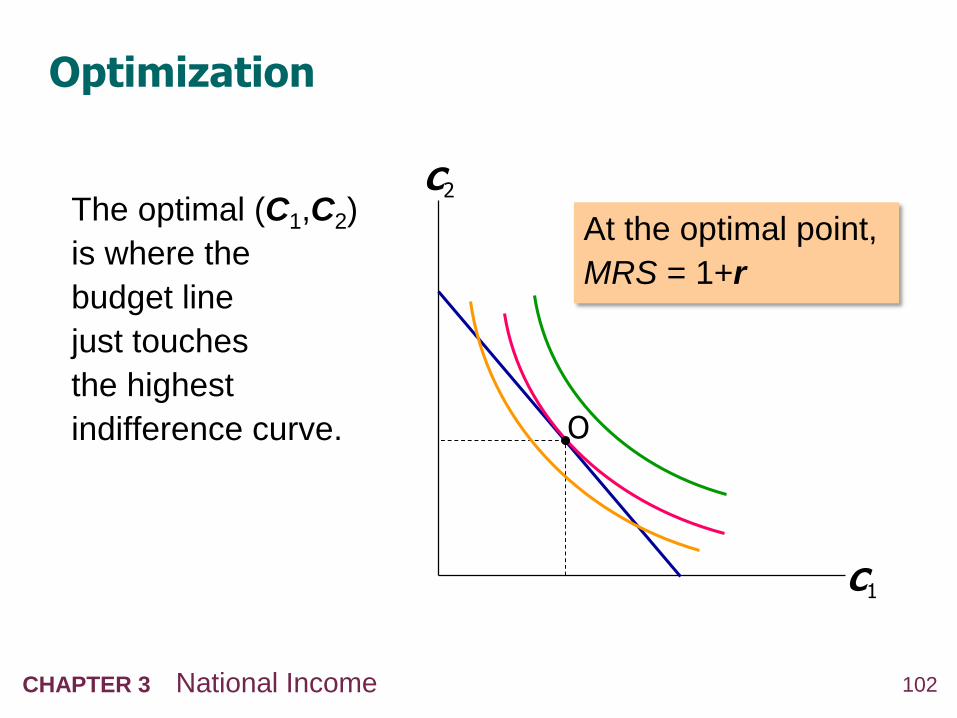

Optimization

The optimal (C1,C2)

is where the

budget line

just touches

the highest

indifference curve.

C1

C2

O

At the optimal point,

MRS = 1+r

103CHAPTER 3 National Income

How C responds to changes in Y

An increase

in Y1 or Y2

shifts the

budget line

outward.

C1

C2Results:

Provided they are

both normal goods,

C1 and C2 both

increase,

…whether the

income increase

occurs in period 1

or period 2.

104CHAPTER 3 National Income

Keynes vs. Fisher

Keynes:

Current consumption depends only on

current income.

Fisher:

Current consumption depends only on

the present value of lifetime income.

The timing of income is irrelevant

because the consumer can borrow or lend

between periods.

105CHAPTER 3 National Income

A

How C responds to changes in r

An increase in r

pivots the budget

line around the

point (Y1,Y2 ).

C1

C2

Y1

Y2

A

B

As depicted here,

C1 falls and C2 rises.

However, it could

turn out differently…

106CHAPTER 3 National Income

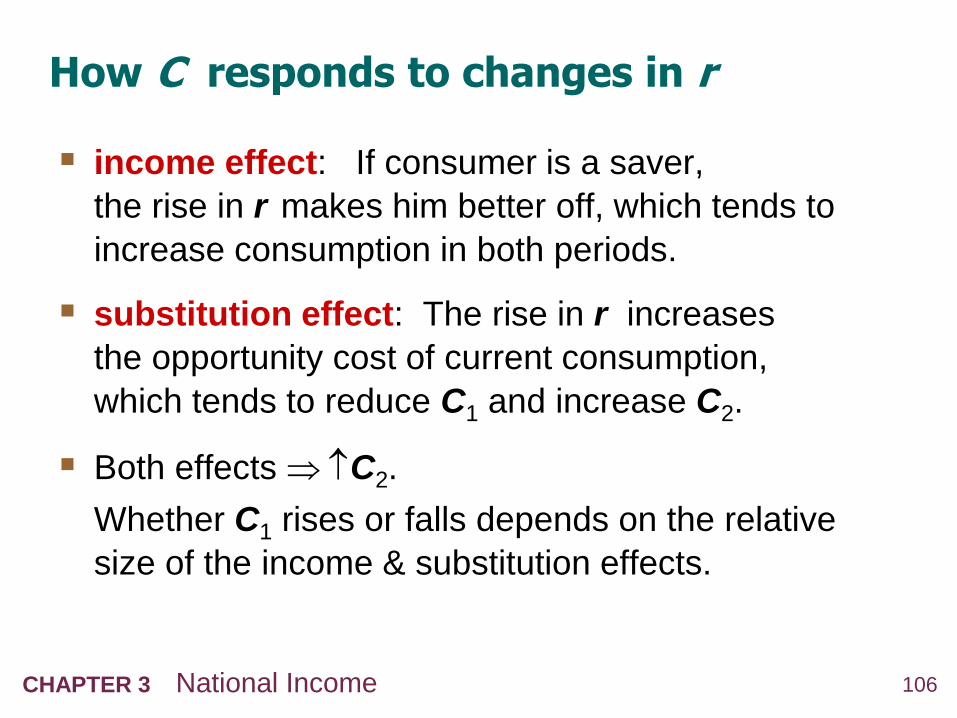

How C responds to changes in r

income effect: If consumer is a saver,

the rise in r makes him better off, which tends to

increase consumption in both periods.

substitution effect: The rise in r increases

the opportunity cost of current consumption,

which tends to reduce C1 and increase C2.

Both effects C2.

Whether C1 rises or falls depends on the relative

size of the income & substitution effects.

107CHAPTER 3 National Income

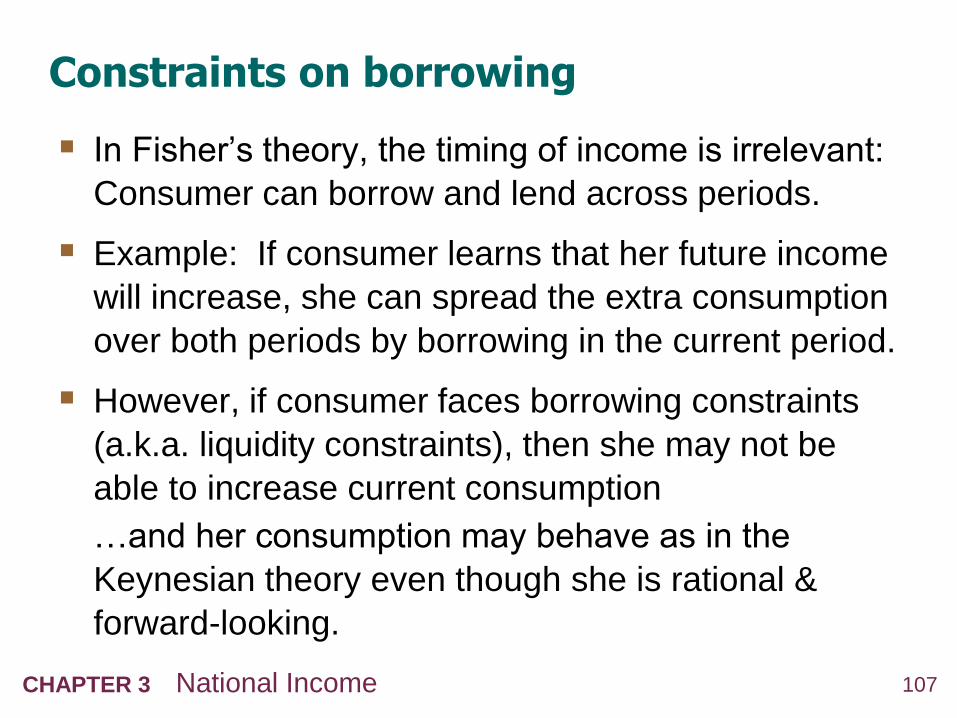

Constraints on borrowing

In Fisher’s theory, the timing of income is irrelevant:

Consumer can borrow and lend across periods.

Example: If consumer learns that her future income

will increase, she can spread the extra consumption

over both periods by borrowing in the current period.

However, if consumer faces borrowing constraints

(a.k.a. liquidity constraints), then she may not be

able to increase current consumption

…and her consumption may behave as in the

Keynesian theory even though she is rational &

forward-looking.

108CHAPTER 3 National Income

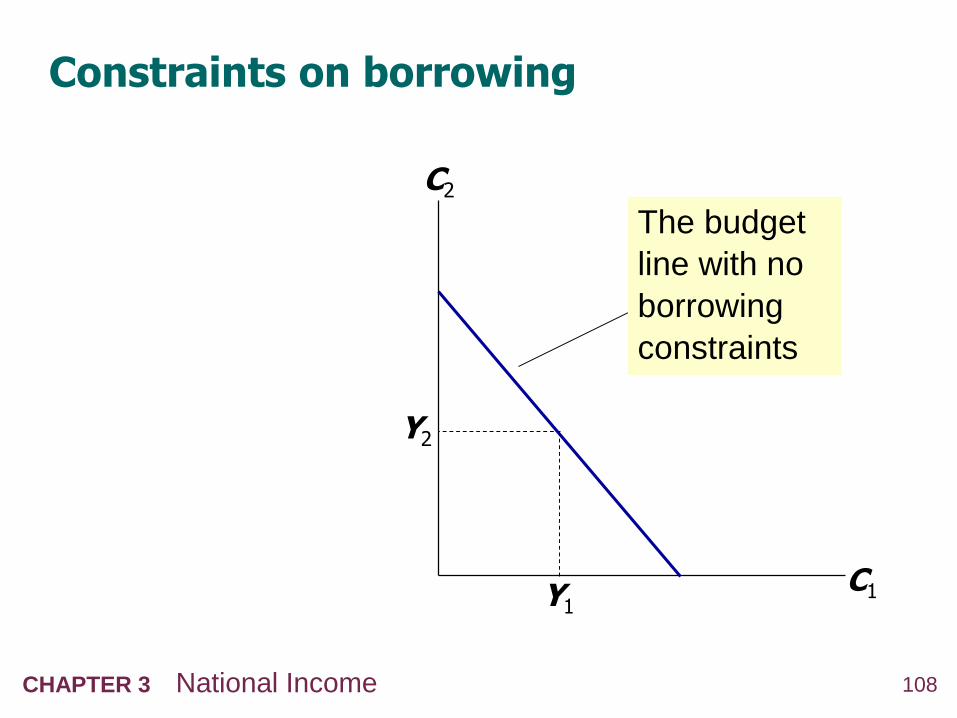

Constraints on borrowing

The budget

line with no

borrowing

constraints

C1

C2

Y1

Y2

109CHAPTER 3 National Income

Constraints on borrowing

The borrowing

constraint takes

the form:

C1 Y1

C1

C2

Y1

Y2

The budget

line with a

borrowing

constraint

110CHAPTER 3 National Income

Consumer optimization when the

borrowing constraint is not binding

The borrowing

constraint is not

binding if the

consumer’s

optimal C1

is less than Y1.

C1

C2

Y1

111CHAPTER 3 National Income

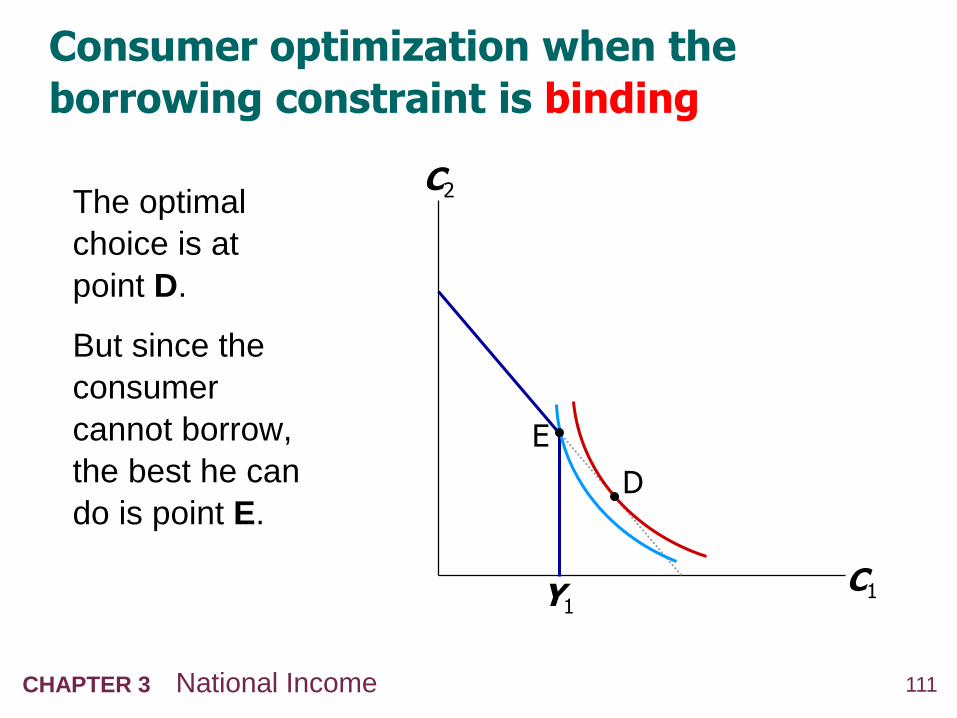

Consumer optimization when the

borrowing constraint is binding

The optimal

choice is at

point D.

But since the

consumer

cannot borrow,

the best he can

do is point E.

C1

C2

Y1

D

E

L E C T U R E S U M M A R Y

Total output is determined by:

the economy’s quantities of capital and labor

the level of technology

Competitive firms hire each factor until its marginal

product equals its price.

If the production function has constant returns to

scale, then labor income plus capital income

equals total income (output).

112

L E C T U R E S U M M A R Y

A closed economy’s output is used for

consumption, investment, and government

spending.

The real interest rate adjusts to equate

the demand for and supply of:

goods and services.

loanable funds.

113

L E C T U R E S U M M A R Y

A decrease in national saving causes the interest

rate to rise and investment to fall.

An increase in investment demand causes the

interest rate to rise but does not affect the

equilibrium level of investment if the supply of

loanable funds is fixed.

114

115CHAPTER 1 The Science of Macroeconomics

L E C T U R E S U M M A R Y

Alternative Views of Consumption

1. Keynesian consumption theory

Keynes’s conjectures

MPC is between 0 and 1

APC falls as income rises

current income is the main determinant of

current consumption

Empirical studies

in household data & short time series:

confirmation of Keynes’s conjectures

in long-time series data:

APC does not fall as income rises115

116CHAPTER 1 The Science of Macroeconomics

L E C T U R E S U M M A R Y

2. Fisher’s theory of intertemporal choice

Consumer chooses current & future

consumption to maximize lifetime satisfaction of

subject to an intertemporal budget constraint.

Current consumption depends on lifetime

income, not current income, provided consumer

can borrow & save.

116