Embed Size (px)

Citation preview

Kiev Retail Market Overview

Q4 2013

Jones Lang LaSalle – Retail Overview – Q 4 2013 2

Content

• Kiev retail market snapshot, Q4 2013

• Supply: Retail real estate development

• Demand: Retail market drivers

• Rent and vacancy rate

• Standard lease terms for retail premises in Kiev

• Summary

Jones Lang LaSalle – Retail Overview – Q 4 2013 3

Kiev Retail Market Snapshot, Q4 2013

Quality shopping centre stock, sq m 728,700

Completions, Q4 2013, sq m 97,500

Completions, Q1-Q4 2013, sq m 112,100

Quality shopping centre stock per 1,000 257.9

Vacancy rate 6.5%

Announced completions, 2014 414,790

Prime shopping centre base rent*, USD/sq m/year 1,200

Operating expenses, USD/sq m/year 90-120

Source: Jones Lang LaSalle

*Rents are given for a single unit of 100 sq m GLA located on the ground floor of a retail gallery. Rents

exclude VAT and OPEX.

Supply: Real Estate Development

Jones Lang LaSalle – Retail Overview – Q 4 2013 5

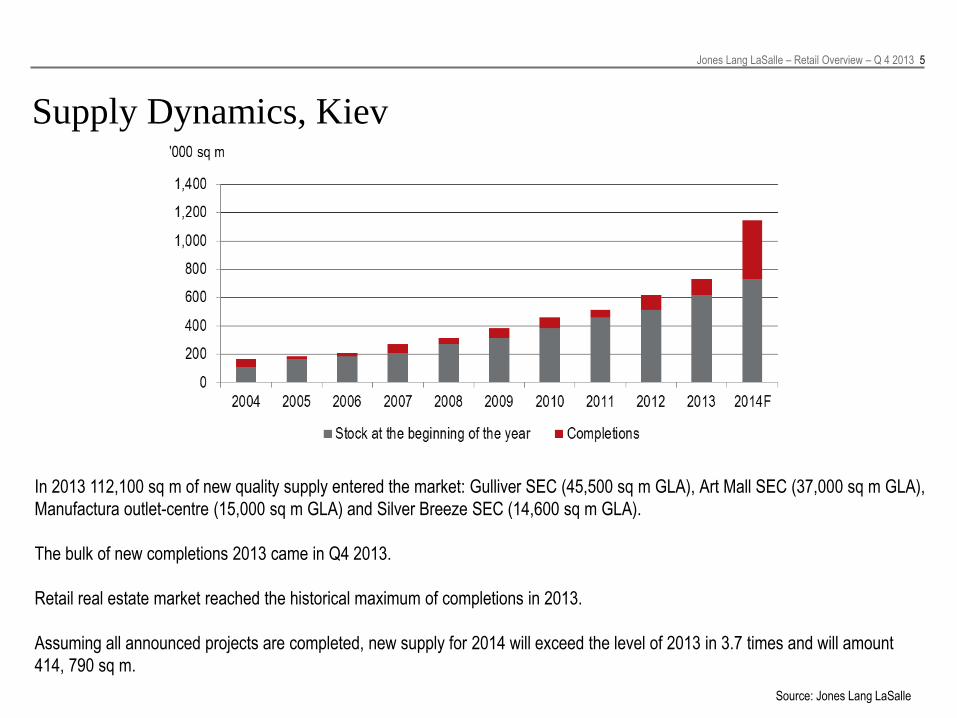

Supply Dynamics, Kiev

Source: Jones Lang LaSalle

In 2013 112,100 sq m of new quality supply entered the market: Gulliver SEC (45,500 sq m GLA), Art Mall SEC (37,000 sq m GLA),

Manufactura outlet-centre (15,000 sq m GLA) and Silver Breeze SEC (14,600 sq m GLA).

The bulk of new completions 2013 came in Q4 2013.

Retail real estate market reached the historical maximum of completions in 2013.

Assuming all announced projects are completed, new supply for 2014 will exceed the level of 2013 in 3.7 times and will amount

414, 790 sq m.

Jones Lang LaSalle – Retail Overview – Q 4 2013 6

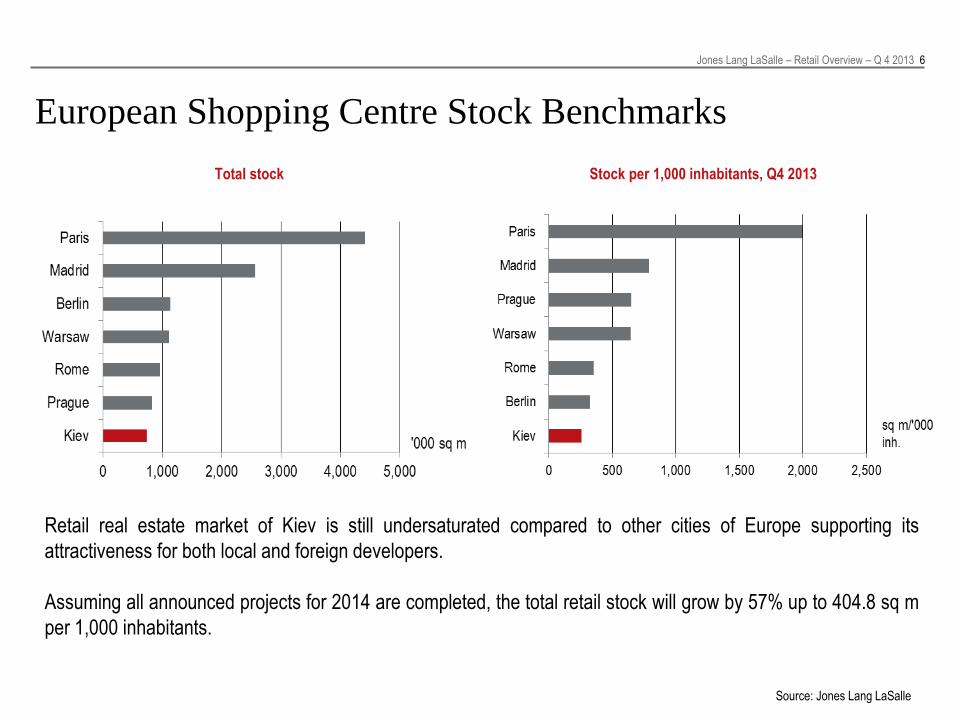

European Shopping Centre Stock Benchmarks

Retail real estate market of Kiev is still undersaturated compared to other cities of Europe supporting its

attractiveness for both local and foreign developers.

Assuming all announced projects for 2014 are completed, the total retail stock will grow by 57% up to 404.8 sq m

per 1,000 inhabitants.

Source: Jones Lang LaSalle

Total stock Stock per 1,000 inhabitants, Q4 2013

Jones Lang LaSalle – Retail Overview – Q 4 2013 7

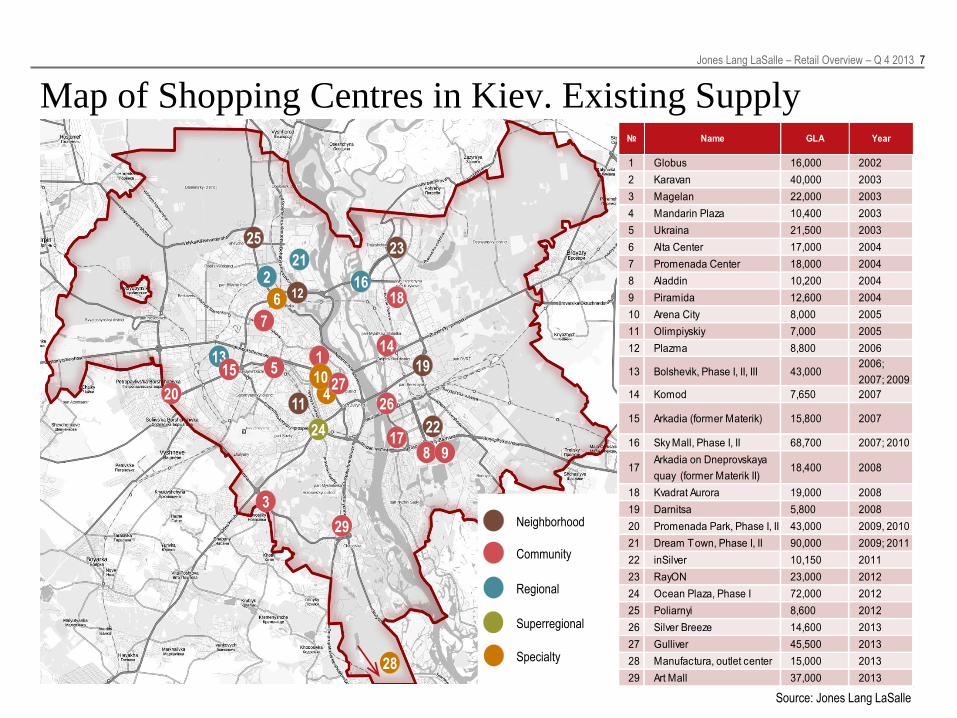

Map of Shopping Centres in Kiev. Existing Supply

Source: Jones Lang LaSalle

Neighborhood

Community

Regional

Superregional

Specialty

1

2

3

4

5

6

7

8 9

10

11

13 14

15

16

17

18

19

20

21

22

23

24

25

26

12

27

28

29

№ Name GLA Year

1 Globus 16,000 2002

2 Karavan 40,000 2003

3 Magelan 22,000 2003

4 Mandarin Plaza 10,400 2003

5 Ukraina 21,500 2003

6 Alta Center 17,000 2004

7 Promenada Center 18,000 2004

8 Aladdin 10,200 2004

9 Piramida 12,600 2004

10 Arena City 8,000 2005

11 Olimpiyskiy 7,000 2005

12 Plazma 8,800 2006

13 Bolshevik, Phase I, II, III 43,0002006;

2007; 2009

14 Komod 7,650 2007

15 Arkadia (former Materik) 15,800 2007

16 Sky Mall, Phase I, II 68,700 2007; 2010

17Arkadia on Dneprovskaya

quay (former Materik II)18,400 2008

18 Kvadrat Aurora 19,000 2008

19 Darnitsa 5,800 2008

20 Promenada Park, Phase I, II 43,000 2009, 2010

21 Dream Town, Phase I, II 90,000 2009; 2011

22 inSilver 10,150 2011

23 RayON 23,000 2012

24 Ocean Plaza, Phase I 72,000 2012

25 Poliarnyi 8,600 2012

26 Silver Breeze 14,600 2013

27 Gulliver 45,500 2013

28 Manufactura, outlet center 15,000 2013

29 Art Mall 37,000 2013

Jones Lang LaSalle – Retail Overview – Q 4 2013 8

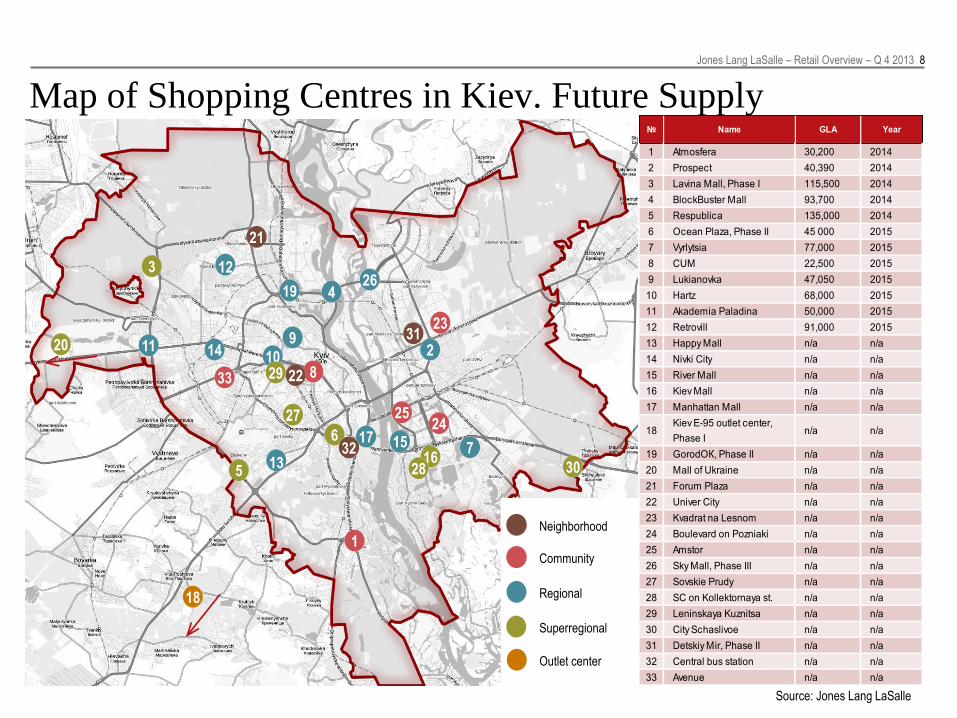

Map of Shopping Centres in Kiev. Future Supply

Source: Jones Lang LaSalle

3

9 6

22

33

1

2

3

15

24

25

27

28

30

31

32

29

1

2

3

4

5

14

16 15 6

7

8

9

17

10 11

18

19

20

21

22

23

24 25

26

27

28

29

30

31

32

33

Neighborhood

Community

Regional

Superregional

Outlet center

12

13

№ Name GLA Year

1 Atmosfera 30,200 2014

2 Prospect 40,390 2014

3 Lavina Mall, Phase I 115,500 2014

4 BlockBuster Mall 93,700 2014

5 Respublica 135,000 2014

6 Ocean Plaza, Phase II 45 000 2015

7 Vyrlytsia 77,000 2015

8 CUM 22,500 2015

9 Lukianovka 47,050 2015

10 Hartz 68,000 2015

11 Akademia Paladina 50,000 2015

12 Retrovill 91,000 2015

13 Happy Mall n/a n/a

14 Nivki City n/a n/a

15 River Mall n/a n/a

16 Kiev Mall n/a n/a

17 Manhattan Mall n/a n/a

18Kiev Е-95 outlet center,

Phase In/a n/a

19 GorodОК, Phase II n/a n/a

20 Mall of Ukraine n/a n/a

21 Forum Plaza n/a n/a

22 Univer City n/a n/a

23 Kvadrat na Lesnom n/a n/a

24 Boulevard on Pozniaki n/a n/a

25 Amstor n/a n/a

26 Sky Mall, Phase III n/a n/a

27 Sovskie Prudy n/a n/a

28 SC on Kollektornaya st. n/a n/a

29 Leninskaya Kuznitsa n/a n/a

30 City Schaslivoe n/a n/a

31 Detskiy Mir, Phase II n/a n/a

32 Central bus station n/a n/a

33 Avenue n/a n/a

Jones Lang LaSalle – Retail Overview – Q 4 2013 9

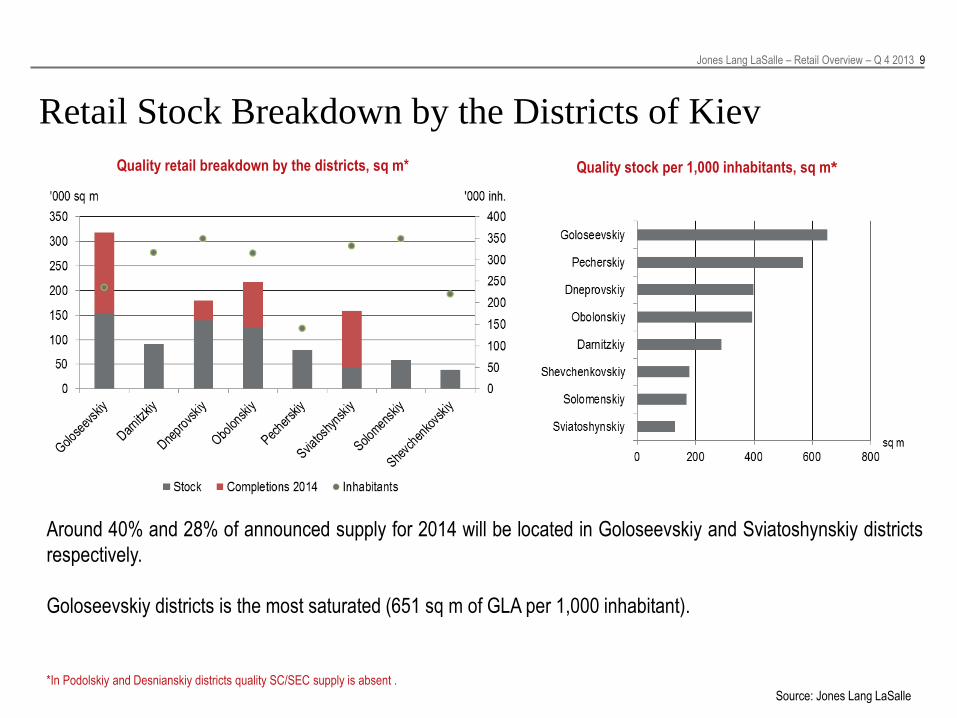

Retail Stock Breakdown by the Districts of Kiev

Source: Jones Lang LaSalle

Around 40% and 28% of announced supply for 2014 will be located in Goloseevskiy and Sviatoshynskiy districts

respectively.

Goloseevskiy districts is the most saturated (651 sq m of GLA per 1,000 inhabitant).

Quality stock per 1,000 inhabitants, sq m* Quality retail breakdown by the districts, sq m*

*In Podolskiy and Desnianskiy districts quality SC/SEC supply is absent .

Demand: Consumer Sector and Retailers

Activity

Jones Lang LaSalle – Retail Overview – Q 4 2013 11

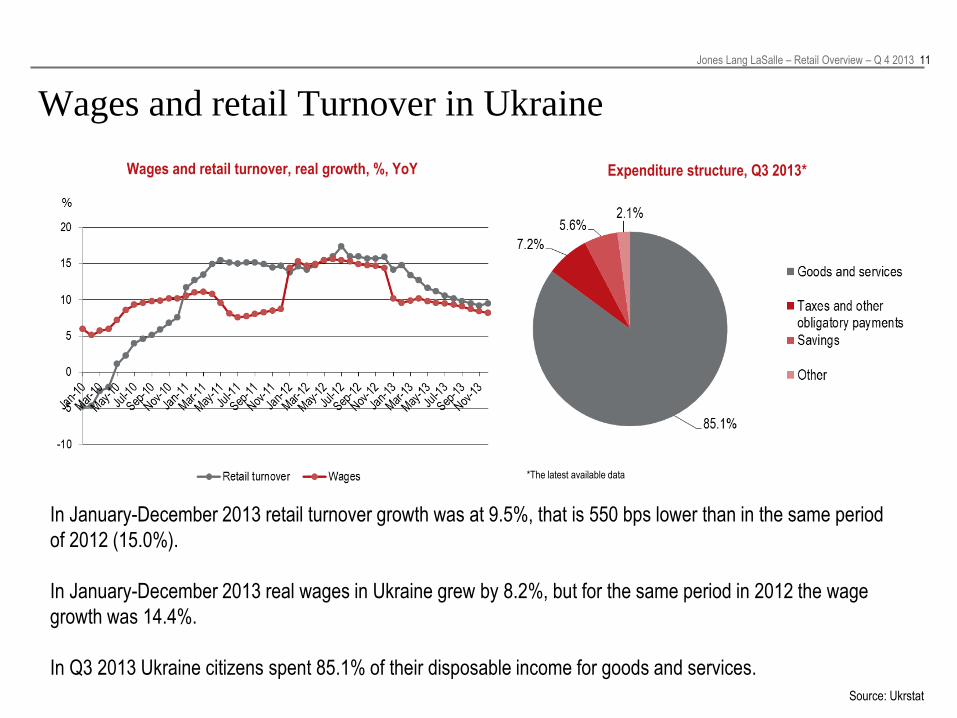

Wages and retail Turnover in Ukraine

In January-December 2013 retail turnover growth was at 9.5%, that is 550 bps lower than in the same period

of 2012 (15.0%).

In January-December 2013 real wages in Ukraine grew by 8.2%, but for the same period in 2012 the wage

growth was 14.4%.

In Q3 2013 Ukraine citizens spent 85.1% of their disposable income for goods and services.

Source: Ukrstat

Wages and retail turnover, real growth, %, YoY Expenditure structure, Q3 2013*

*The latest available data

Jones Lang LaSalle – Retail Overview – Q 4 2013 12

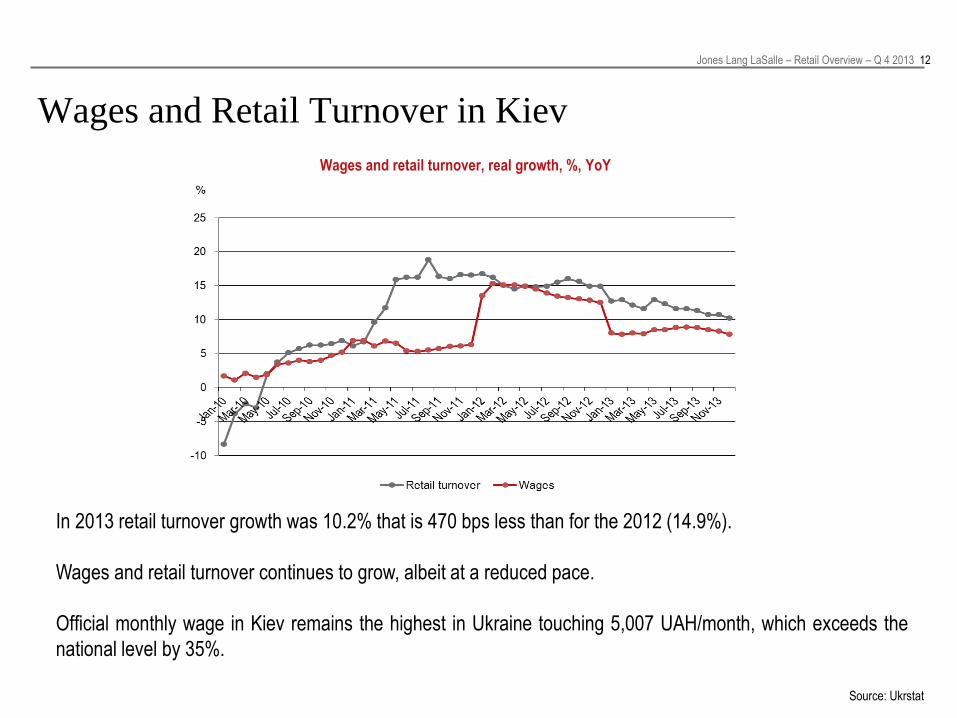

Wages and Retail Turnover in Kiev

In 2013 retail turnover growth was 10.2% that is 470 bps less than for the 2012 (14.9%).

Wages and retail turnover continues to grow, albeit at a reduced pace.

Official monthly wage in Kiev remains the highest in Ukraine touching 5,007 UAH/month, which exceeds the

national level by 35%.

Source: Ukrstat

Wages and retail turnover, real growth, %, YoY

Jones Lang LaSalle – Retail Overview – Q 4 2013 13

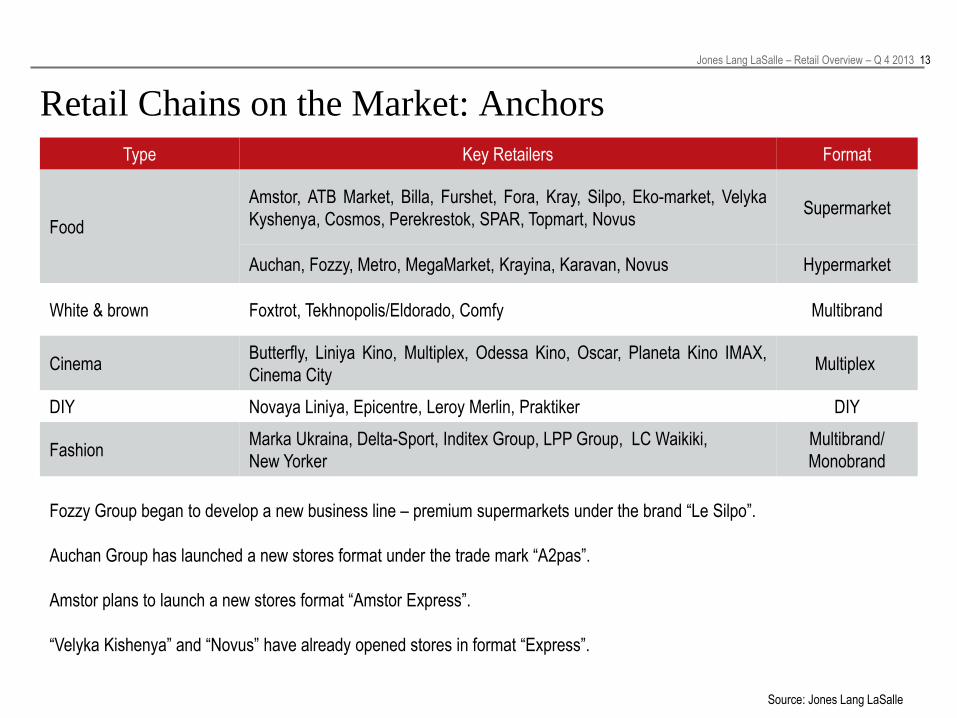

Retail Chains on the Market: Anchors

Source: Jones Lang LaSalle

Type Key Retailers Format

Food

Amstor, ATB Market, Billa, Furshet, Fora, Kray, Silpo, Eko-market, Velyka

Kyshenya, Cosmos, Perekrestok, SPAR, Topmart, Novus Supermarket

Auchan, Fozzy, Metro, MegaMarket, Krayina, Karavan, Novus Hypermarket

White & brown Foxtrot, Tekhnopolis/Eldorado, Comfy Multibrand

Cinema Butterfly, Liniya Kino, Multiplex, Odessa Kino, Oscar, Planeta Kino IMAX,

Cinema City Multiplex

DIY Novaya Liniya, Epicentre, Leroy Merlin, Praktiker DIY

Fashion Marka Ukraina, Delta-Sport, Inditex Group, LPP Group, LC Waikiki,

New Yorker

Multibrand/

Monobrand

Fozzy Group began to develop a new business line – premium supermarkets under the brand “Le Silpo”.

Auchan Group has launched a new stores format under the trade mark “A2pas”.

Amstor plans to launch a new stores format “Amstor Express”.

“Velyka Kishenya” and “Novus” have already opened stores in format “Express”.

Jones Lang LaSalle – Retail Overview – Q 4 2013 14

Retail Chains on the Market: Retail Gallery

Source: Jones Lang LaSalle

Type Key retailers Format

Fashion

Benetton, Bershka, Cacharel, Calvin Klein, Colin's, Cropp Town, Diesel, Gant,

Guess, House, Lacoste, Lerros, Mango, Massimo Dutti, Mohito, Motivi, Noa Noa,

OGGI, O’stin, Oysho, Phard, Promod, Pull&Bear, Stradivarius, Tommy Hilfiger,

Topshop/Topman, US Polo Assn.

Monobrand

Perfume and cosmetics Kosmo, Eva, Watsons, proStor, L’Etoile, Bonjour, Brocard, L’Occitane, MAC,

Bomond, Yves Rocher, Glossary Monobrand/Multibrand

Sports goods Arena, Adidas, Columbia, Nike, Puma, Reebok, Sportmaster, Sportland,

Megasport, New Balance, Northland, Marafon Monobrand/Multibrand

Shoes Aldo, Antonio Biaggi, Carlo Pazolini, Centro, Chester, Ecco, Egle, Geox, Luciano

Carvari, Respect, Tosca Blu, Welfare, Intertop, TsentrObuv Monobrand/Multibrand

Goods for children Antoshka, Budynok Igrashok, Planeta Igrushek, Pelican, SMYK, Tigres, Chicco,

Mothercare Monobrand/Multibrand

Books, music Eurostar, KS, Chitay-gorod, Empik Multibrand

Accessories, jewelry, gifts Accessorize, Almaz, Attributes, Clair’s, DEKA, Diva, I am, LuxOptika, Pandora,

Seta Décor, SIX, Swarovski, Swatch, WOW shop, Sekunda Monobrand/Multibrand

Food-court Coffee House, Pechena Kartoplya, SushiYa, Shokoladnitsa, Yapona Hata,

Coffee Life, L’kafa, Mafia, McDonald's, McFoxy, Kredens Multibrand

Mobile phone Ringoo, Allo Monobrand/Multibrand

Jones Lang LaSalle – Retail Overview – Q 4 2013 15

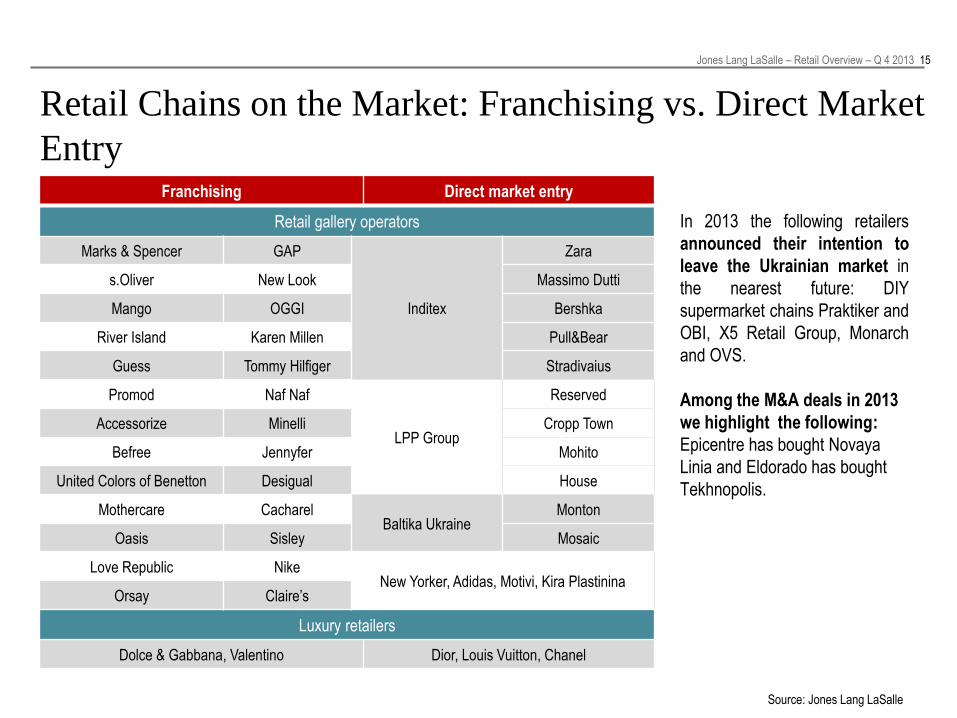

Retail Chains on the Market: Franchising vs. Direct Market

Entry

Source: Jones Lang LaSalle

In 2013 the following retailers

announced their intention to

leave the Ukrainian market in

the nearest future: DIY

supermarket chains Praktiker and

OBI, X5 Retail Group, Monarch

and OVS.

Among the M&A deals in 2013

we highlight the following:

Epicentre has bought Novaya

Linia and Eldorado has bought

Tekhnopolis.

Franchising Direct market entry

Retail gallery operators

Marks & Spencer GAP

Inditex

Zara

s.Oliver New Look Massimo Dutti

Mango OGGI Bershka

River Island Karen Millen Pull&Bear

Guess Tommy Hilfiger Stradivaius

Promod Naf Naf

LPP Group

Reserved

Accessorize Minelli Cropp Town

Befree Jennyfer Mohito

United Colors of Benetton Desigual House

Mothercare Cacharel Baltika Ukraine

Monton

Oasis Sisley Mosaic

Love Republic Nike New Yorker, Adidas, Motivi, Kira Plastinina

Orsay Claire’s

Luxury retailers

Dolce & Gabbana, Valentino Dior, Louis Vuitton, Chanel

Jones Lang LaSalle – Retail Overview – Q 4 2013 16

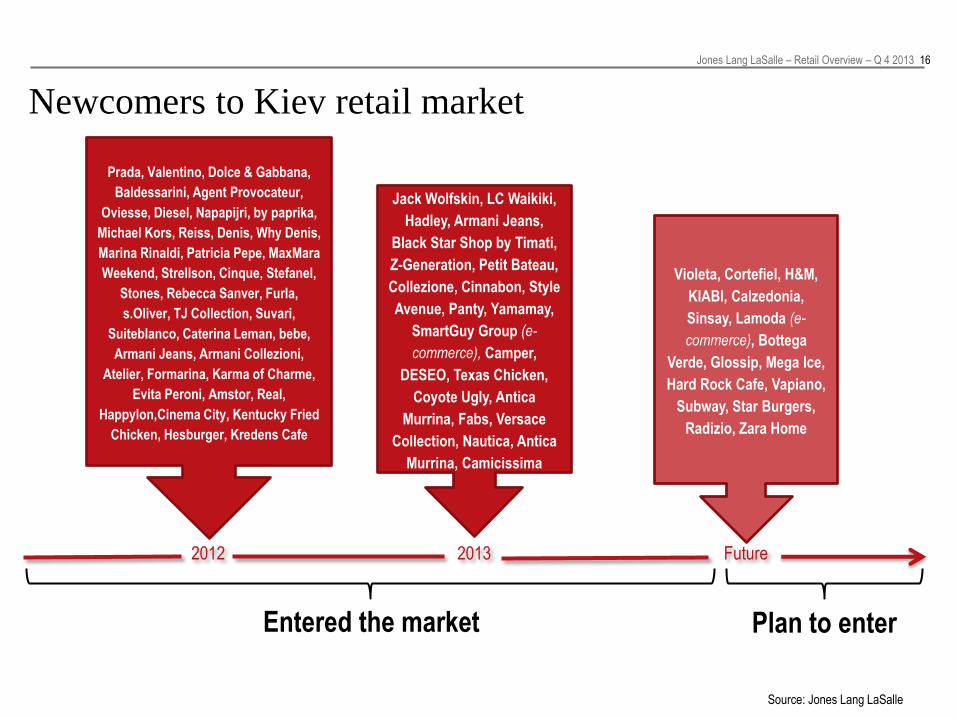

Newcomers to Kiev retail market

2013 Future 2012

Jack Wolfskin, LC Waikiki,

Hadley, Armani Jeans,

Black Star Shop by Timati,

Z-Generation, Petit Bateau,

Collezione, Cinnabon, Style

Avenue, Panty, Yamamay,

SmartGuy Group (e-

commerce), Camper,

DESEO, Texas Chicken,

Coyote Ugly, Antica

Murrina, Fabs, Versace

Collection, Nautica, Antica

Murrina, Camicissima

Entered the market Plan to enter

Violeta, Cortefiel, H&M,

KIABI, Calzedonia,

Sinsay, Lamoda (e-

commerce), Bottega

Verde, Glossip, Mega Ice,

Hard Rock Cafe, Vapiano,

Subway, Star Burgers,

Radizio, Zara Home

Prada, Valentino, Dolce & Gabbana,

Baldessarini, Agent Provocateur,

Oviesse, Diesel, Napapijri, by paprika,

Michael Kors, Reiss, Denis, Why Denis,

Marina Rinaldi, Patricia Pepe, MaxMara

Weekend, Strellson, Cinque, Stefanel,

Stones, Rebecca Sanver, Furla,

s.Oliver, TJ Collection, Suvari,

Suiteblanco, Caterina Leman, bebe,

Armani Jeans, Armani Collezioni,

Atelier, Formarina, Karma of Charme,

Evita Peroni, Amstor, Real,

Happylon,Cinema City, Kentucky Fried

Chicken, Hesburger, Kredens Cafe

Source: Jones Lang LaSalle

Rents

Jones Lang LaSalle – Retail Overview – Q 4 2013 18

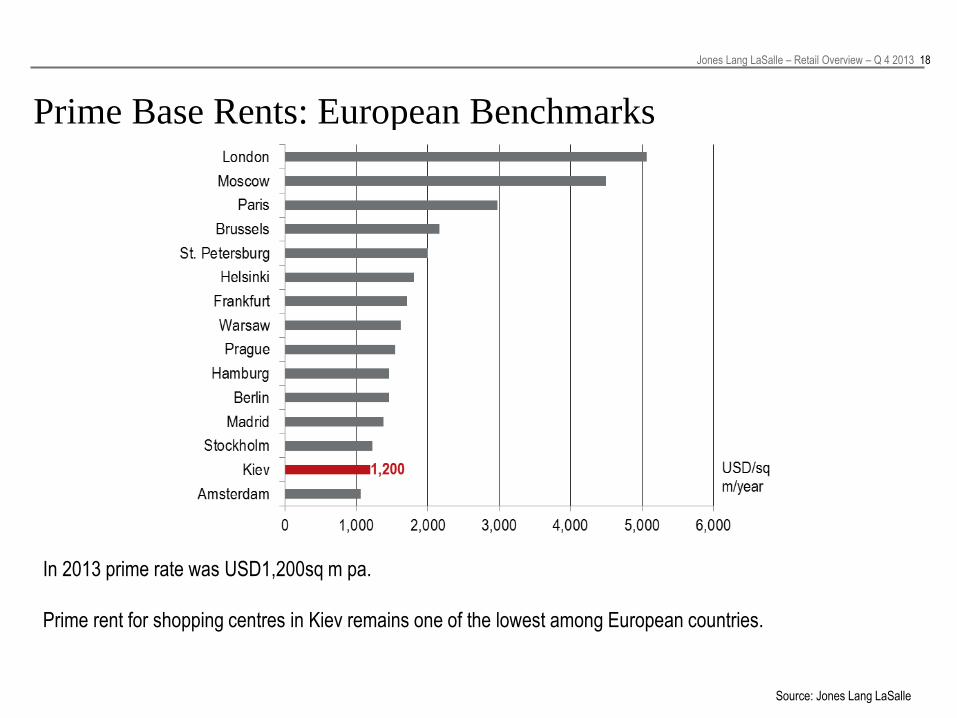

Prime Base Rents: European Benchmarks

Source: Jones Lang LaSalle

In 2013 prime rate was USD1,200sq m pa.

Prime rent for shopping centres in Kiev remains one of the lowest among European countries.

Jones Lang LaSalle – Retail Overview – Q 4 2013 19

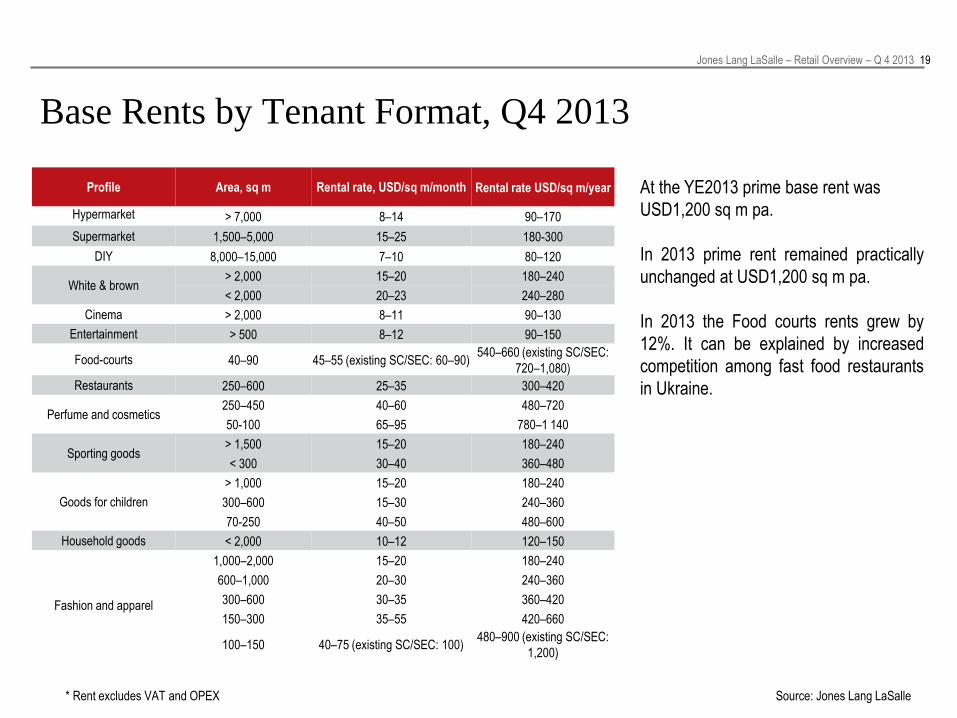

Base Rents by Tenant Format, Q4 2013

Source: Jones Lang LaSalle

At the YE2013 prime base rent was

USD1,200 sq m pa.

In 2013 prime rent remained practically

unchanged at USD1,200 sq m pa.

In 2013 the Food courts rents grew by

12%. It can be explained by increased

competition among fast food restaurants

in Ukraine.

* Rent excludes VAT and OPEX

Profile Area, sq m Rental rate, USD/sq m/month Rental rate USD/sq m/year

Hypermarket > 7,000 8–14 90–170

Supermarket 1,500–5,000 15–25 180-300

DIY 8,000–15,000 7–10 80–120

White & brown > 2,000 15–20 180–240

< 2,000 20–23 240–280

Cinema > 2,000 8–11 90–130

Entertainment > 500 8–12 90–150

Food-courts 40–90 45–55 (existing SC/SEC: 60–90) 540–660 (existing SC/SEC:

720–1,080)

Restaurants 250–600 25–35 300–420

Perfume and cosmetics 250–450 40–60 480–720

50-100 65–95 780–1 140

Sporting goods > 1,500 15–20 180–240

< 300 30–40 360–480

Goods for children

> 1,000 15–20 180–240

300–600 15–30 240–360

70-250 40–50 480–600

Household goods < 2,000 10–12 120–150

Fashion and apparel

1,000–2,000 15–20 180–240

600–1,000 20–30 240–360

300–600 30–35 360–420

150–300 35–55 420–660

100–150 40–75 (existing SC/SEC: 100) 480–900 (existing SC/SEC:

1,200)

Jones Lang LaSalle – Retail Overview – Q 4 2013 20

Source: Jones Lang LaSalle

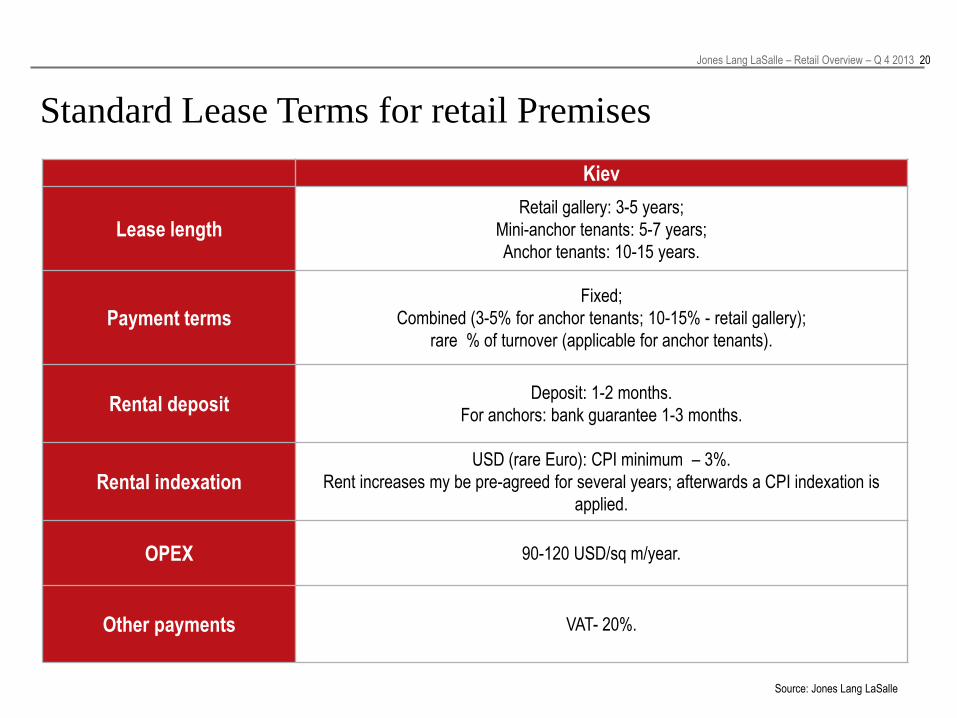

Standard Lease Terms for retail Premises

Kiev

Lease length Retail gallery: 3-5 years;

Mini-anchor tenants: 5-7 years;

Anchor tenants: 10-15 years.

Payment terms Fixed;

Combined (3-5% for anchor tenants; 10-15% - retail gallery);

rare % of turnover (applicable for anchor tenants).

Rental deposit Deposit: 1-2 months.

For anchors: bank guarantee 1-3 months.

Rental indexation USD (rare Euro): CPI minimum – 3%.

Rent increases my be pre-agreed for several years; afterwards a CPI indexation is

applied.

OPEX 90-120 USD/sq m/year.

Other payments VAT- 20%.

Jones Lang LaSalle – Retail Overview – Q 4 2013 21

Summary

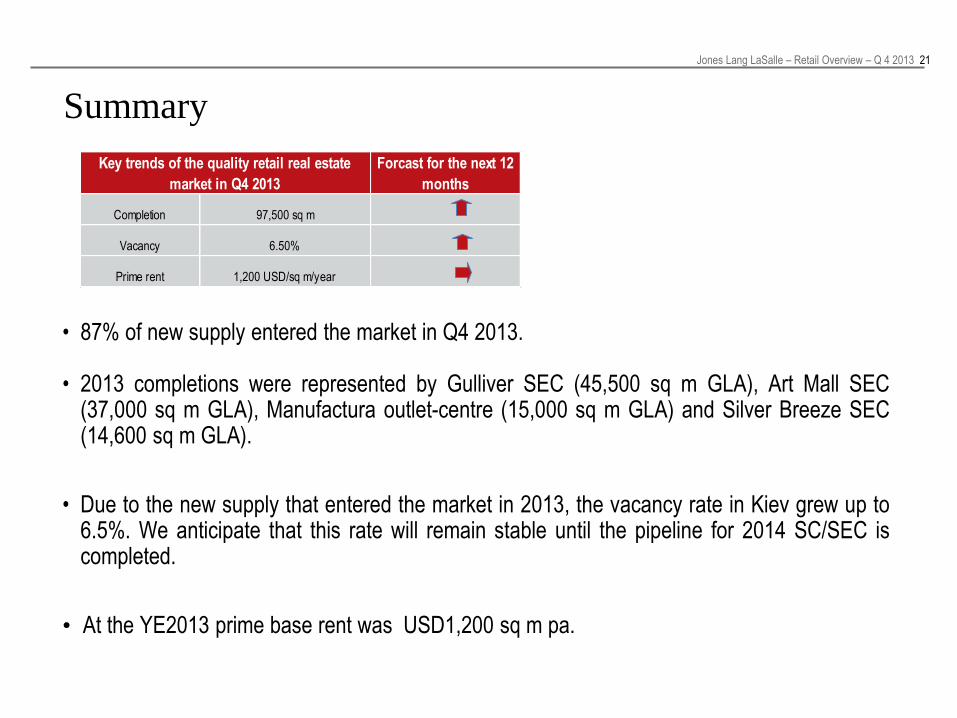

• 87% of new supply entered the market in Q4 2013.

• 2013 completions were represented by Gulliver SEC (45,500 sq m GLA), Art Mall SEC (37,000 sq m GLA), Manufactura outlet-centre (15,000 sq m GLA) and Silver Breeze SEC (14,600 sq m GLA).

• Due to the new supply that entered the market in 2013, the vacancy rate in Kiev grew up to

6.5%. We anticipate that this rate will remain stable until the pipeline for 2014 SC/SEC is completed.

• At the YE2013 prime base rent was USD1,200 sq m pa.

Forcast for the next 12

months

Completion 97,500 sq m

Vacancy 6.50%

Prime rent 1,200 USD/sq m/year

Key trends of the quality retail real estate

market in Q4 2013

Thank you!

© COPYRIGHT © JONES LANG LASALLE IP, INC. 2013. No part of this publication may be reproduced or transmitted in any form or by any means without prior written

consent of Jones Lang LaSalle. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty

that it contains no factual errors. We would like to be told of any such errors in order to correct them.