Embed Size (px)

DESCRIPTION

M&A exam outline

Citation preview

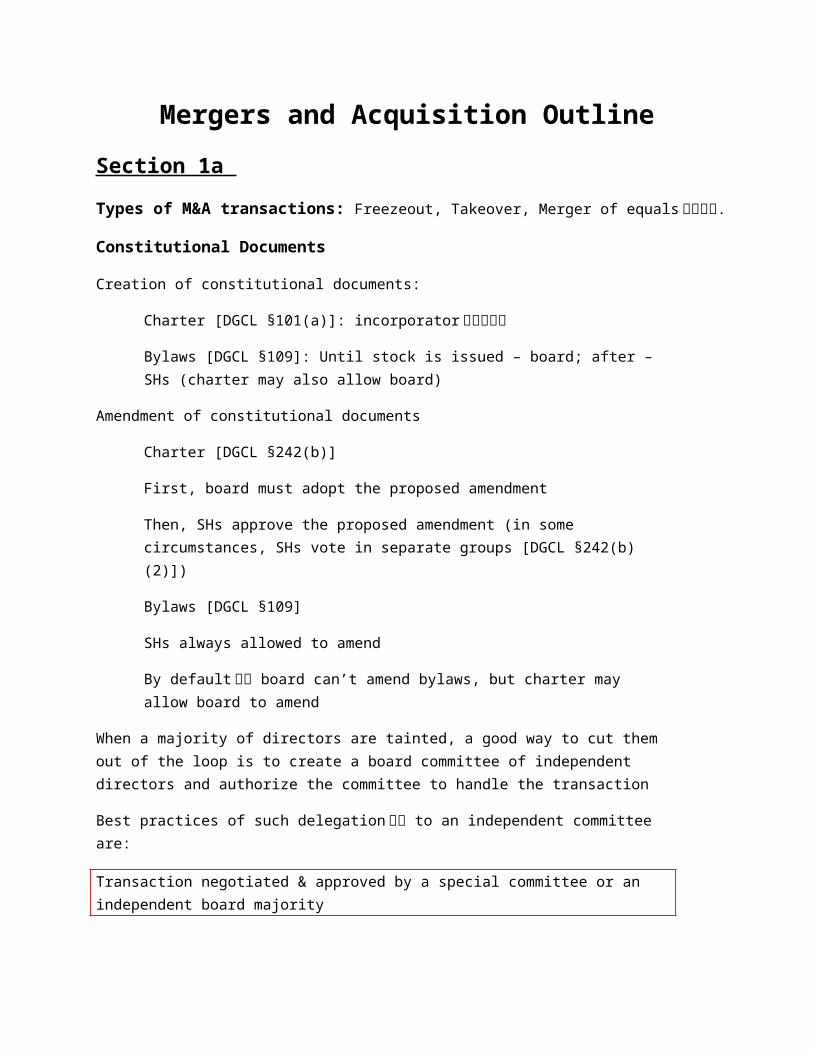

Mergers and Acquisition Outline

Section 1a

Types of M&A transactions: Freezeout, Takeover, Merger of equals对等合并.

Constitutional Documents

Creation of constitutional documents:

Charter [DGCL §101(a)]: incorporator公司创办人

Bylaws [DGCL §109]: Until stock is issued – board; after – SHs (charter may also allow board)

Amendment of constitutional documents

Charter [DGCL §242(b)]

First, board must adopt the proposed amendment

Then, SHs approve the proposed amendment (in some circumstances, SHs vote in separate groups [DGCL §242(b)(2)])

Bylaws [DGCL §109]

SHs always allowed to amend

By default缺席 board can’t amend bylaws, but charter may allow board to amend

When a majority of directors are tainted, a good way to cut them out of the loop is to create a board committee of independent directors and authorize the committee to handle the transaction

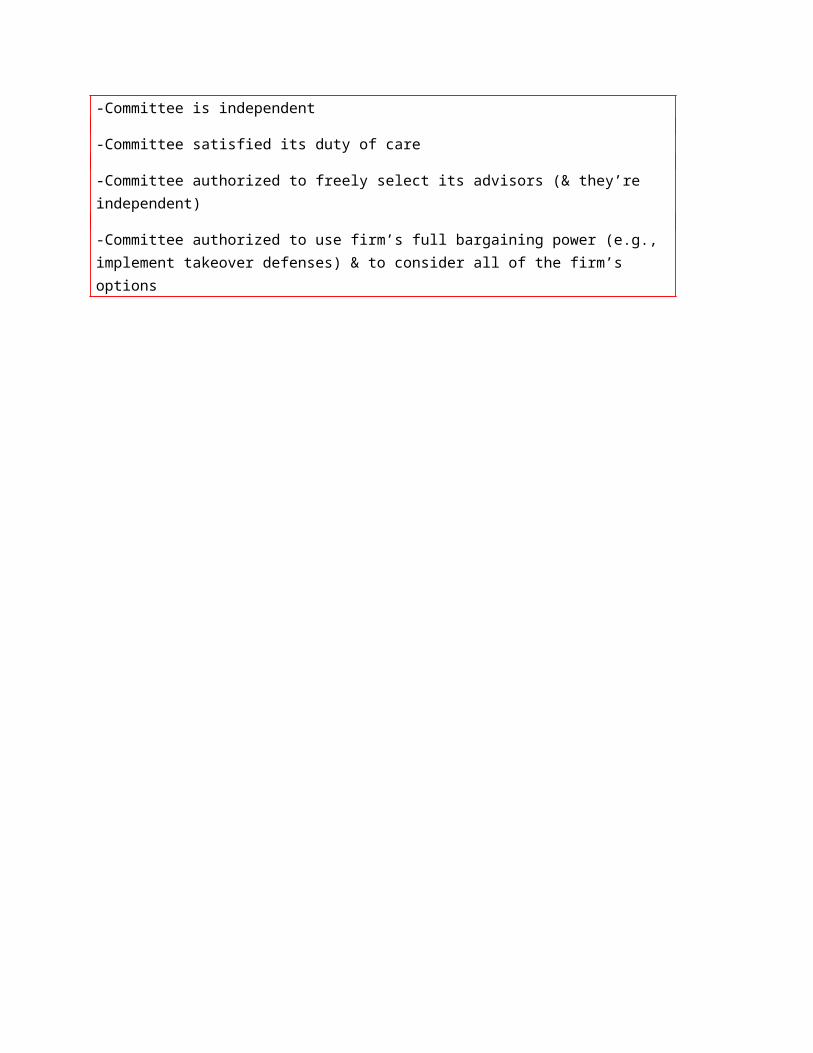

Best practices of such delegation委托 to an independent committee are:

Transaction negotiated & approved by a special committee or an independent board majority

-Committee is independent

-Committee satisfied its duty of care

-Committee authorized to freely select its advisors (& they’re independent)

-Committee authorized to use firm’s full bargaining power (e.g., implement takeover defenses) & to consider all of the firm’s options

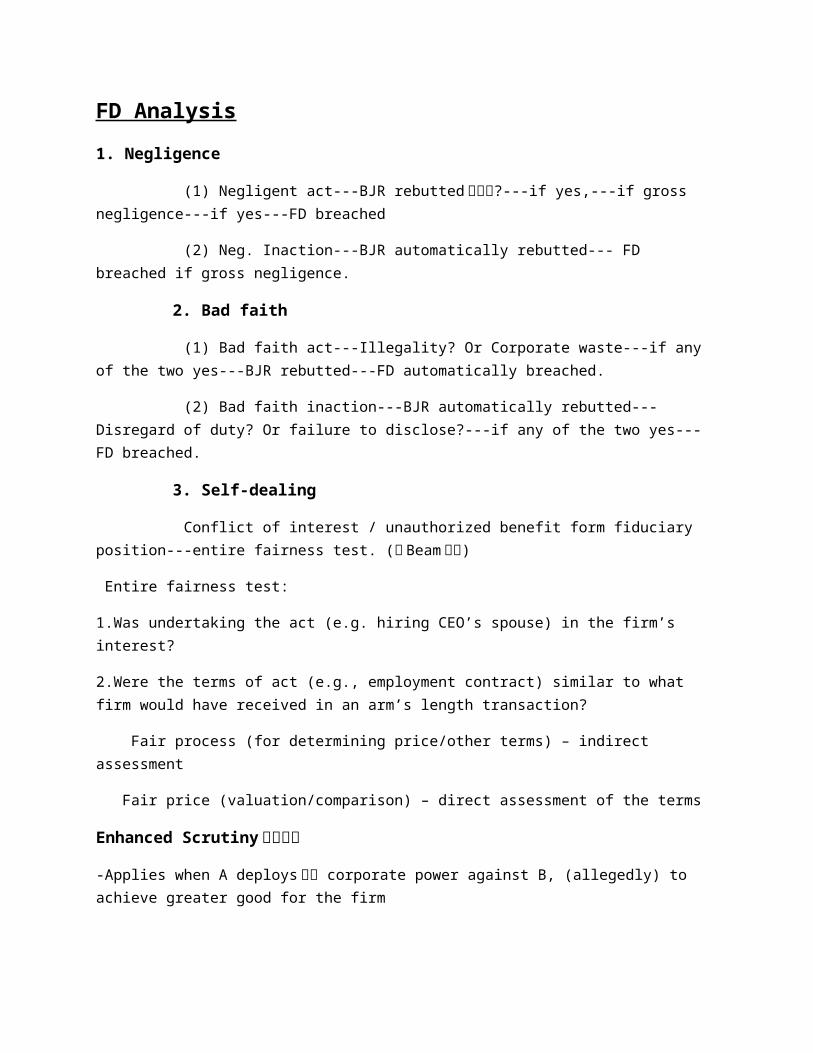

FD Analysis

1. Negligence

(1) Negligent act---BJR rebutted被指控?---if yes,---if gross negligence---if yes---FD breached

(2) Neg. Inaction---BJR automatically rebutted--- FD breached if gross negligence.

2. Bad faith

(1) Bad faith act---Illegality? Or Corporate waste---if any of the two yes---BJR rebutted---FD automatically breached.

(2) Bad faith inaction---BJR automatically rebutted---Disregard of duty? Or failure to disclose?---if any of the two yes---FD breached.

3. Self-dealing

Conflict of interest / unauthorized benefit form fiduciary position---entire fairness test. (看 Beam案例)

Entire fairness test:

1.Was undertaking the act (e.g. hiring CEO’s spouse) in the firm’s interest?

2.Were the terms of act (e.g., employment contract) similar to what firm would have received in an arm’s length transaction?

Fair process (for determining price/other terms) – indirect assessment

Fair price (valuation/comparison) – direct assessment of the terms

Enhanced Scrutiny加强审查

-Applies when A deploys配置 corporate power against B, (allegedly) to achieve greater good for the firm

A adopts takeover defenses (Unocal)

A limits ability to sell shares, to preserve tax benefits (Selectica)

A runs SH meeting in way that interferes with SHs’ vote (Blasius)

-The test: quasi-BJR (did actor make a business judgment, was actor independent & did actor act in good faith?) + reasonableness (is act a reasonable way to address threat?)

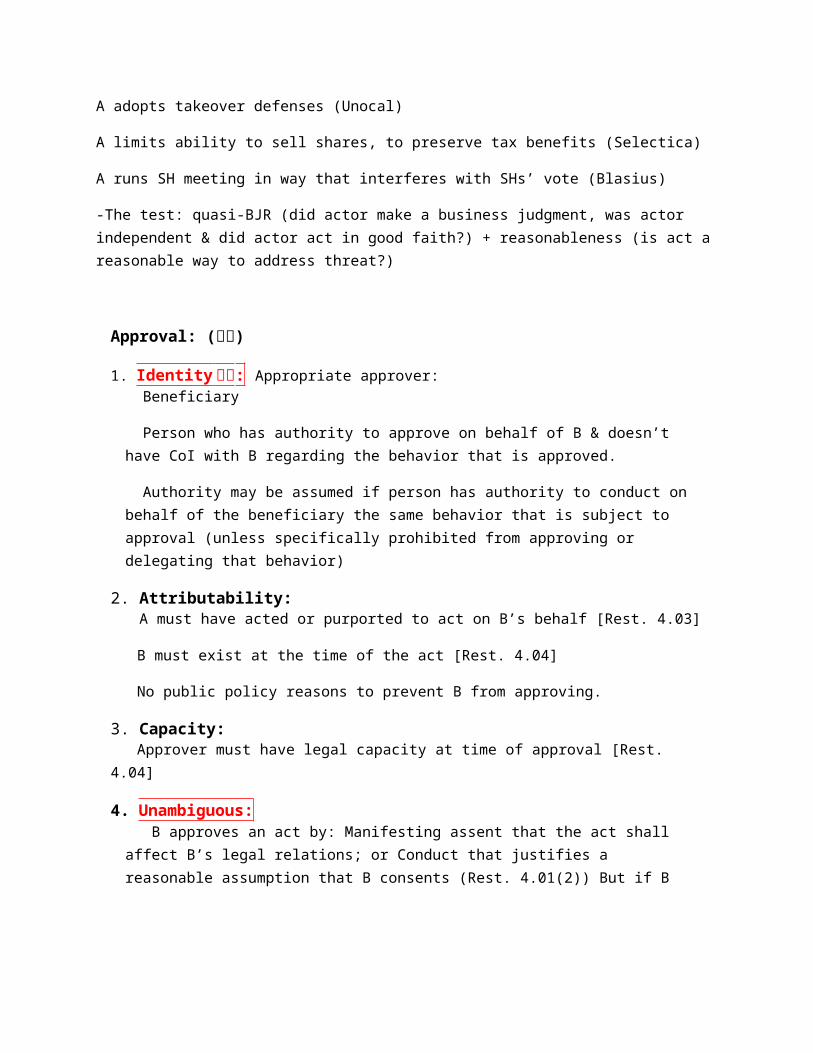

Approval: (要素)

1. Identity身份: Appropriate approver: Beneficiary

Person who has authority to approve on behalf of B & doesn’t have CoI with B regarding the behavior that is approved.

Authority may be assumed if person has authority to conduct on behalf of the beneficiary the same behavior that is subject to approval (unless specifically prohibited from approving or delegating that behavior)

2. Attributability: A must have acted or purported to act on B’s behalf [Rest. 4.03]

B must exist at the time of the act [Rest. 4.04]

No public policy reasons to prevent B from approving.

3. Capacity: Approver must have legal capacity at time of approval [Rest. 4.04]

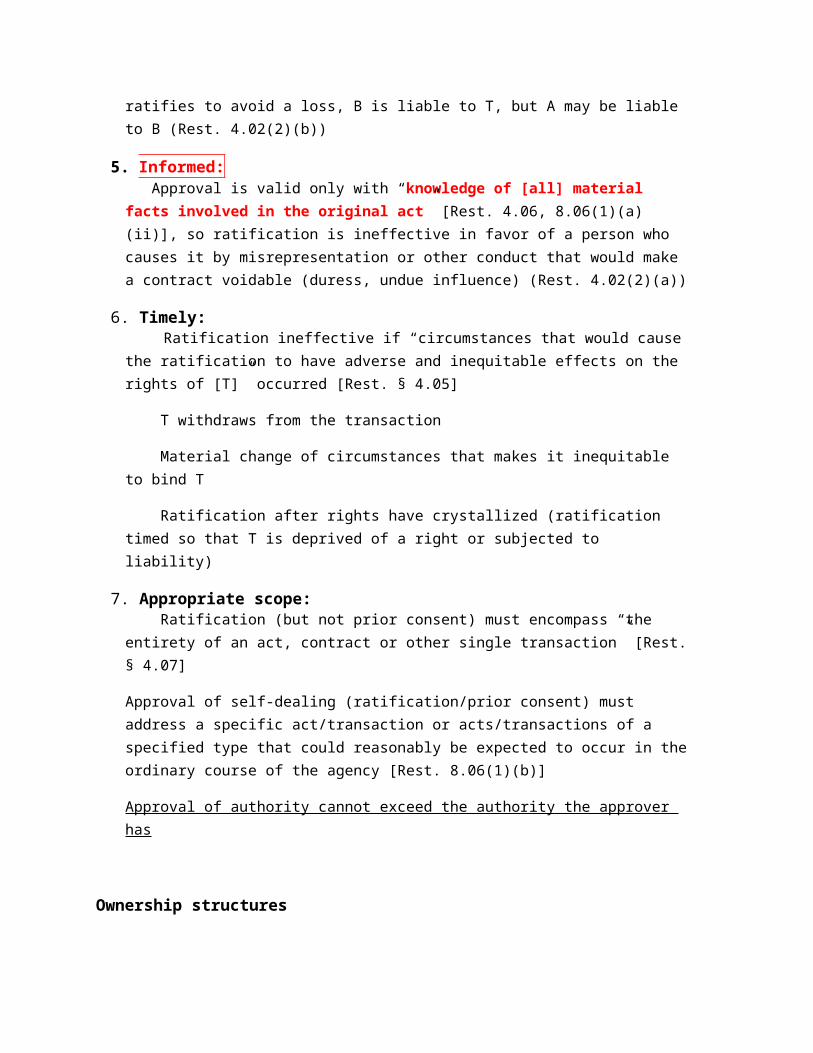

4. Unambiguous: B approves an act by: Manifesting assent that the act shall affect B’s legal relations; or Conduct that justifies a reasonable assumption that B consents (Rest. 4.01(2)) But if B ratifies to avoid a loss, B is liable to T, but A may be liable to B (Rest. 4.02(2)(b))

5. Informed: Approval is valid only with “knowledge of [all] material facts involved in the original act” [Rest. 4.06, 8.06(1)(a)(ii)], so ratification is ineffective in favor of a person who causes it by misrepresentation or other conduct that would make a contract voidable (duress, undue influence) (Rest. 4.02(2)(a))

6. Timely: Ratification ineffective if “circumstances that would cause the ratification to have adverse and inequitable effects on the rights of [T]” occurred [Rest. § 4.05]

T withdraws from the transaction

Material change of circumstances that makes it inequitable to bind T

Ratification after rights have crystallized (ratification timed so that T is deprived of a right or subjected to liability)

7. Appropriate scope: Ratification (but not prior consent) must encompass “the entirety of an act, contract or other single transaction” [Rest. § 4.07]

Approval of self-dealing (ratification/prior consent) must address a specific act/transaction or acts/transactions of a specified type that could reasonably be expected to occur in the ordinary course of the agency [Rest. 8.06(1)(b)]

Approval of authority cannot exceed the authority the approver has

Ownership structures

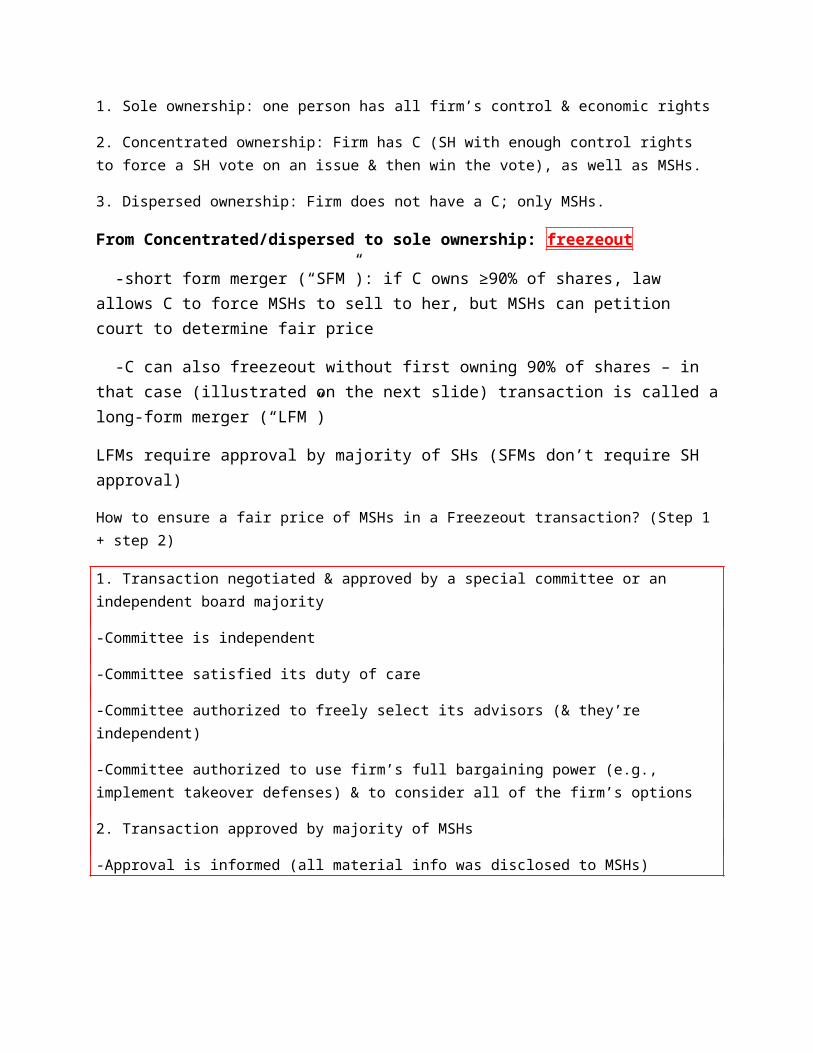

1. Sole ownership: one person has all firm’s control & economic rights

2. Concentrated ownership: Firm has C (SH with enough control rights to force a SH vote on an issue & then win the vote), as well as MSHs.

3. Dispersed ownership: Firm does not have a C; only MSHs.

From Concentrated/dispersed to sole ownership: freezeout

-short form merger (“SFM”): if C owns ≥90% of shares, law allows C to force MSHs to sell to her, but MSHs can petition court to determine fair price

-C can also freezeout without first owning 90% of shares – in that case (illustrated on the next slide) transaction is called a long-form merger (“LFM”)

LFMs require approval by majority of SHs (SFMs don’t require SH approval)

How to ensure a fair price of MSHs in a Freezeout transaction? (Step 1 + step 2)

1. Transaction negotiated & approved by a special committee or an independent board majority

-Committee is independent

-Committee satisfied its duty of care

-Committee authorized to freely select its advisors (& they’re independent)

-Committee authorized to use firm’s full bargaining power (e.g., implement takeover defenses) & to consider all of the firm’s options

2. Transaction approved by majority of MSHs

-Approval is informed (all material info was disclosed to MSHs)

-There is no coercion of the minority (specifically, MSH approval must be an unwaivable condition to the transaction)

-Majority of all MSHs, not just those present at the meeting

Controller

SH owes a FD “only if it owns a majority interest in or exercises control over the business affairs of the corporation” (Ivanhoe Partners v. Newmont Mining Corp. [Del. 1987]),that means, this kind of SH is considered as Controllers.

C’s unilateral act: (C’s self-dealing is allowed)

1. C votes her shares

-No duty to MSHs

2. C buys shares from MSHs

-Solomon v. Pathe Comm. Corp. [Del. 1996]: no duty to offer a fair price; duty only to provide full disclosure & not coerce the sellers

In re Siliconix Inc. Shareholders Litigation [Del.Ch. 2001]: court confirms entire fairness does not apply to freeze-out via tender offer

3. C executes a SFM (freezes out MSHs)

Glassman [Del. 2001]: No duty to offer fair price in a SFM; only duty is to provide full disclosure of facts required for MSHs to decide if they should opt for appraisal

4. C sells her shares

Harris case:

C breaches DoC to MSHs when selling to a looter, if C knew of looting plans or if a reasonably prudent person would have suspected buyer is dishonest & C didn’t conduct a sufficient investigation

But when firm’s charter has a §102(b)(7) exculpatory provision, DoC breached only if C knew of looting plans (otherwise, no liability for negligence)

C act on behalf of the firm (C’s self-dealing is not allowed)

Most common cases are:

1. Transactions in which C is on both sides of the deal (Kahn)

2. Transactions in which C receives different terms than MSHs (Frank)

In either of these cases:

- If “robust procedural protections” (RPP) is implemented, BJR applies

- otherwise, entire fairness applies.

In some cases a firm’s act isn’t a transaction in which C can be on the other side or receive different terms than MSHs, (Sinclair)

if C receives something to the exclusion of & detriment to MSHs --- entire fairness

otherwise --- BJR

Frank case has two practical meanings:

1. Multiple SHs considered as a single control group when connected in some legally meaningful way (e.g., contract to work together towards a shared goal)

2. When an acquirer who is not affiliated with C gives different terms to C and to the MSHs

- RPP: BJR

- otherwise: entire fairness

Either in Kahn or in Frank: if the C can show that special committee element or majority of MSHs is met, the BoP are shifted to the plaintiff.

Section 1b: SH Voting

Mechanics of SH voting

- Call

Who has authority to call a SH meeting

Appropriate notice

- Quorum

If a share is present for any issue at the meeting, it counts towards the quorum for the entire meeting

Who is entitled to vote --- depends on the record date

By default: Notice --- Day before notice is given to the SHs; If notice was waived by SHs, record date is day before meeting

Voting --- Same date as notice record date

- Voting

Vote required to pass (see ppt 1b page 12)

An abstention counts as part of the “voting power present”

*Special voting rules:

1. When an issue is aiming at certain group of SHs, this group of SHs is entitled to vote in their group. Both groups (all SHs and certain SH) need majority favor.

2. Cumulative voting

3. Staggered boards

Board influence on SH voting

Blasius case

Enhanced scrutiny SoR applies when the board deploys corporate power against SHs to achieve greater good for the corporation. When the BoD runs SH meeting in way that interferes with SHs’ vote like in Blasius, the enhanced scrutiny applies:

Quasi BJR (in good faith + investigation) + reasonableness

Purpose: board must identify a legitimate threat/purpose justifying its act

Good faith: duty of loyalty analysis (no self-dealing or bad faith)

Reasonable investigation: duty of care analysis (no negligence)

In Blasius case, the reasonableness standard is the BoD has a compelling justification. But in other enhanced scrutiny cases, the standard for reasonableness is reasonable justification.

Proxy solicitation

Rules (see ppt 1b from page 40~43)

Exchange Act §14(a)-9: prohibits false or misleading statements in connection with soliciting proxies

Elements:

1. Violation

For Rule 14a-9: Material misleading statement or material omission

Standard for materiality (TSC Industries [US 1976]): Substantial likelihood that a reasonable shareholder would consider the statement/omission important in deciding how to vote

2. Injury

3. Causation

Causation exists if:

There was a material misrepresentation; and

The solicited proxies were essential to approve the merger

Controlling the agenda

Proxy contest: solicit from other SHs proxies to vote their shares on the desired issue or for the desired candidate --- too expensive

Proxy access: ask the board to include the desired issue/candidate on the agenda (and on the board’s proxy card)

Meeting showdown: attend SH meeting, make a motion to amend the agenda, get another SH to second the motion, then win a SH vote on amending the agenda

Proxy access:

Electing directors (proxy access) – limited access

DGCL §112: Bylaws may contain a proxy access provision, allowing SHs to nominate their candidates for directors on the board’s proxy card, and create certain limitations on this right

Other SH decisions (SH proposals) – broader access

The BoD must contain the SH proposal into its proxy card as long as it is a legitimate proposal. But BoD may write an objection to the proposal (exclusion).

Procedure: see page 56

Grounds:

1. Improper under state law (SHs can recommend)

2. Relevance (issue has very minor impact on the firm) --- relates to operations which account for <5% of total assets, net earnings & gross sales, and is “not otherwise significantly related to the company’s business”

3. Absence of power/authority

4. Management functions (Proposal deals with a matter relating to the firm’s ordinary business operations).

Section 1c

Litigation procedure

Plaintiff’s complaint commences the lawsuit; must allege:

-Jurisdiction

-Claim (facts showing that plaintiff is entitled to relief)

-Relief (a demand for an appropriate remedy)

Remedy

-TRO (temporary restraining order): issued before opponent can respond

-Preliminary injunction: issued after opponent responds (but before trial)

Standard (for both): (a) reasonable probability of success on the merits; (b) reasonable likelihood moving party will suffer irreparable harm absent the provisional remedy & that harm outweighs harm to non-moving party from granting the provisional remedy.

• Pre-answer motions (motion to dismiss)

– Can be based on procedural flaw (lack of jurisdiction, improper venue, faulty process or service) or substantive flaw (failure to state a claim)

– Standard for dismissal for failure to state a claim (Rule 12(b)(6))

• Federal courts: “a complaint must contain sufficient factual matter, accepted as true, to state a claim to relief that is plausible on its face” (Twombly [US 2007], Iqbal [US 2009])

• Delaware: complaint dismissed for failing to state a claim only if, accepting plaintiff’s factual allegations as true, “plaintiff would not be entitled to recover under any reasonably conceivable set of circumstances” (Central Mortgage [Del. 2011])

Derivative suits

Rules:

1. contemporaneous ownership requirement: Plaintiff must have been a SH at time of the alleged wrong & maintained that status throughout the litigation. (exception: if a transaction was made merely to destroy a plaintiff’s derivative standing, court will not recognize the loss of ownership resulting from that transaction. )

2. demand requirement: SH must ask board to sue before suing derivatively

Standards:

-Derivative: Looking at the body of the complaint and considering the nature of the wrong alleged and the relief requested, has the plaintiff demonstrated that he or she can prevail without showing an injury to the corporation?

• Who can sue derivatively? –

-Common SHs - Yes

-Preferred SHs – Yes, unless this right was specifically limited in charter or another “appropriate document” [Maginn (Del. Ch. 2010)]

-Creditors [Gheewalla (Del. 2007)]

– Yes, when firm is insolvent

– Unclear, when firm is in the “zone of insolvency”

– No, in all other situations

-Directors – No (though courts may allow in future if needed to prevent “complete failure of justice”) [Schoon (Del. 2008)]

Demand:

MBCA (universal demand): see page 25 of 1c

Delaware (excusable demand): demand must be made unless it is futile

• -Primary test: Aronson v. Lewis [Del. 1984]: Demand requirement is excused if plaintiff shows reasonable doubt that either:

– Majority of the board is independent for purpose of responding to the demand (@ time complaint is filed)

– Challenged action is protected by the BJR

• Alternative test: Rales v. Blasband [Del. 1993]: test includes only 1st prong (board independence in responding to demand); applies when:

– P’s claim arises out of board inaction

– P’s claims arise out of transaction not involving a board decision

– A majority of directors that decided on underlying transaction was replaced by independent directors

When a majority of the BoD is not independent while the firm has to make decision on this time, the Firm could form a Special Litigation Committee (SLC) to avoid get involved in the futile test:

Firm asks court to apply BJR (i.e., defer) to a decision of an SLC (composed of disinterested directors) that the derivative action lacks merit - Unlike demand futility litigation, in SLC litigation plaintiff is entitled to limited discovery (as to the independence of the SLC members)

Delaware applies two steps (Zapata Corp. v. Maldonado [Del. 1981]) in SLC litigation:

– Quasi-BJR analysis to SLC’s decision

• SLC independence

• SLC good faith

• Reasonable bases for the SLC’s recommendations

– Court may apply its own “independent business judgment” as to whether to dismiss the suit

SH inspection rights

• Proper purpose (DGCL §220(b))

– SH must make a written demand, presenting a “proper purpose” (i.e., a purpose “reasonably related to such person’s interest as a stockholder”)

• Who has BoP whether purpose is proper? (DGCL §220(c))

– If SH seeks access to the SH list, BoP on the firm to show that SH does not have a “proper purpose”

– If SH seeks access to other corporate records, BoP on the SH to prove “proper purpose”

Conditions for SH inspection right:

1. Written demand from a shareholder (record owner or beneficial owner)

2. Proper purpose

-Purpose is proper if it is reasonably related to one’s interest as a SH

-That purpose must be SH’s true/primary purpose

-SH must have evidence establishing a credible basis for that purpose

3. Proper records

-Requested records are necessary & essential for the purpose

-Safeguards may be imposed to protect confidentiality of the records

Section 2a Acquisition mechanics

Share acquisition methods

• Y buys X’s shares from XS, until Y accumulates enough shares to control X

– Market share acquisition: Y buys X shares on the stock exchange

– Bilateral share acquisition: Y negotiates with individual XS to purchase X shares

– Tender offer: Y makes public offer to XS to buy their shares

Share acquisitions are regulated under federal law by the Williams Act which apply only to registered securities.

- Disclosure of share holdings

- Beneficial owner of 5% of a registered security must file a disclosure (Schedule 13D) within 10 days of crossing the 5% threshold [§13(d)(1)]. 5% threshold includes aggregate purchases by several people as part of a single plan [§13(d)(3)]

Changes in holdings: Schedule 13D must be amended promptly in the event of any material change in the facts set forth in the statement (Rule 13d-2)

Acquisition/disposition of at least 1% of a class of securities is material

Enforcement: X can sue a 5% beneficial owner for failing to file a Schedule 13D or for filing a misleading statement

Has standing to seek equitable relief (injunction, rescission of securities purchases, divestiture of the securities, suspension of voting rights), but not damages.

- Disclosure/process of tender offers

Rules triggered when a tender offer is made for more than 5% of X’s equity securities

An offer commences when the bidder provides security holders with means to tender their securities

- A transmittal form; or

- Information regarding how the transmittal form may be obtained

Bidder may communicate intent to acquire shares without commencing the tender offer if communication

- does not include means to tender the securities, and

- all written communications re tender offer are publicly filed

[Rule 14d-2(b)]

By the date tender offer commences, Y must file a Schedule 14D-1 disclosure statement

Same info must be disseminated to SH via newspaper publication or mailing

XB must then file a Schedule 14D-9 form, in which the management states, with reasons, whether they:

- Support the offer

- Oppose it

- Are unable to take a position

Tender offer must be open for at least 20 biz days [Rule 14e-1(a)]

If Y changes amount of shares acquired or price offered, offer must be open for 10 biz days after change [Rule 14e-1(b)]

If tender is over-subscribed (i.e., more shares are tendered than Y offered to purchase), Y must accept shares on a pro-rata basis [§14(d)(6)]

Any Y who raises his price during the term of the tender offer must raise it for any shares already tendered [§14(d)(7)]

Structural acquisition methods

- Long-form merger (LFM)- Short-form merger (SFM)- Asset sale

LFM procedure

- Parties sign a merger agreement

- Board approval of merger agreement (each party) [DGCL §251(b)]

- SH approval of merger agreement (each party) [DGCL §251(c)]

- Approval by majority of shares entitled to vote

- No vote required (subject to some conditions) in mergers preceded by tender offer, after which Y owns enough shares to approve the merger [DGCL §251(h)]

- Filing [DGCL §251(c)]

-Merger becomes effective when Articles of Merger are filed

-At that point, all merging parties cease to exist except for one surviving entity; all property & liabilities of merging parties vest in/attach to surviving entity [DGCL §259(a)]

- Appraisal [DGCL §262]

- SH who opposed the merger (but lost) may petition the court to determine the fair price to be paid to them (rather than accept the price Y offered)

- DGCL §262(h): Appraisal value is the fair value “exclusive of any element of value arising from the accomplishment or expectation of the merger…”

SFM procedure

- Y notifies all other SHs that it is merging with X in a SFM, specify the terms of the merger & provide all info material to a decision whether to seek appraisal

- Only allowed if Y owns ≥90% of X’s shares

- Filing

- Merger becomes effective when owner files a certificate of merger (certifying that Y owns ≥90% of X’s shares & that Y’s board approved a SFM

- Appraisal [DGCL §262]

- Any MSH may petition the court to determine the fair price to be paid to them

Statutory authority

DGCL §253 allows SFM with corporation

DGCL §267 (2010 amendment) allows SFM with non-corporate entities (partnerships, LLCs, and other unincorporated associations)

Asset sale procedure

- Parties sign an asset sale agreement

- Buyer receives all of seller’s assets, pays seller agreed consideration

- Board approval of agreement (each party)

- SH approval of agreement (seller only) [DGCL §271]

- Required if seller is selling “all or substantially all of its property and assets”

- Approval by majority of shares entitled to vote

- Seller dissolves, giving its SHs the consideration it received

- Appraisal rights to seller’s SHs (in some jurisdictions; e.g., MBCA)

- DGCL does not provide appraisal rights to SHs of seller

Triangular merger

• Mergers generally require SH approval of both parties, and create appraisal rights for SHs of both parties

• However, a form of merger called a triangular merger allows Y to bypass these SH rights

– The trick: Y forms S, and S merges with X

– S’s SHs get voting & appraisal rights, but S has just one SH: Y, which is controlled by YB (who supports the deal)

• Called triangular merger because there are three parties: Y, S, X

Appraisal rights

- Conditions

- SH must perfect his appraisal right by sending a written notice to the firm prior to the SH vote, informing that he intends to exercise his appraisal rights [DGCL §262(d)]

- SH must not vote in favor of merger, consent to it in writing or accept the benefits of the transaction

- SH must hold shares continuously through merger’s effective day

If: stock is publicly traded or held by over 2,000 SHs [DGCL §262(b)(1)]; and

the consideration to the SH is publicly held stock [DGCL §262(b)(2)]---no appraisal rights.

No class procedure for appraisal rights

Remedies for faulty LFMs

Remedy for breach of FD in a LFM is usually limited to appraisal (receiving the fair value of plaintiff’s shares)

Reason: if merger was approved by majority of SHs, plaintiff did not have the power to block the merger, and shouldn’t get this power as a remedy

However, in cases of fraud, misrepresentation & corporate waste other remedies are available, such as rescission of the merger or rescissory damages

Remedies for faulty SFMs

Glassman : appraisal is exclusive remedy for a faulty SFM

Exceptions: fraud, illegality & inadequate disclosure

Remedy?: not clear, hahaha~~~

Section 2b Acquisition Interactions

• M&A is a complex game between YB, XB & XS

– Y + XB alliance: friendly deal (one that is supported by XB)

– Y + XS alliance: hostile deal (a transaction that doesn’t require XB‘s approval)

– XB + XS alliance: no deal

Arbs are investors who identify companies that they expect will be taken over, buy shares, and sell to Y @ premium.

leveraged buyout (LBO) – borrow the cash used to pay XS

Financing the LBO:

- Bridge financing: creditor lends to Y for short time & at high interest rate (at same time, parties may agree on terms of long-term loan (step 3))

- Y uses bridge financing to pay XS for 100% of X

- Once Y owns 100% of X, Y either:

- Negotiates long-term loan using X’s assets as collateral (lower interest rate)

- Causes X to take a long-term loan & transfer the money to Y as dividend

(Either way, Y uses new money to repay the bridge financing)

Friendly Approach (Nothing to talk about, just see the slides)

Hostile Approach

Why would XB resist?- Entrenchment: XB resists either because they think Y will fire them, or they want to force Y to give them a side-payment to allow the deal to go through: If this is XB’s motivation, it’s not in XS‘s interest.

- Long-term plans: Allow contrarian, innovative strategies (but also inefficient ones)

- Holding out for a better offer: XB resists to force Y to offer a better price – which is in XS’s interest.

Common takeover defenses

• Takeover defenses reduce Y’s ability to acquire X without support of XB (even if XS support Y)

– PR / appeasing SH dissent

– Leveraged recapitalization

– Voting plans

– Staggered board

– Statutory defense

– White knights (lock-ups)

– Poison pills

PR / appeasing SH dissent

This defense changes allies/enemies tally by reducing the # of shares in “weak hands” (SHs who are most likely to sell to Y)

Arbs & other short-term investors

SHs who think XB can’t increase X’s value above Y’s offer

PR campaign aims to persuade SHs that:

- Y’s takeover attempt will fail (so arbs don’t buy shares)

- X will be worth more in foreseeable future than Y’s offer

XB may also reach out to activist SHs and take steps these SHs would like to see

- Pay dividends

- Make corporate governance changes

- Sell unattractive businesses

- Cancel unpopular business plans

Leveraged recapitalization

X borrows money & eliminates low-profit assets (less profitable operations & excessive cash)

X then uses this money to repurchase shares (Raises share price (increasing cost of share acquisition & makes XS happier), Takes shares away from weak hands, Makes X less attractive for LBO (less cash & more debt))

Voting plans

Voting rules or share rights that hinder a takeover; examples:

Limiting voting rights of large SHs, Limiting voting rights of new SHs (“tenure voting plan”), Supermajority voting provision.

Staggered boards

Takes longer to control XB

Statutory defense

- Business combination statutes (DGCL §203)

• Y is prohibited from having a “business combination” with X for 3 years after Y owns 15% or more of X

• Exceptions

• Y has 85%+ interest in X

• Not counting shares owned by directors/officers/employee stock plans

• Prior approval by XB

• Subsequent approval by XB + 2/3 majority of disinterested SHs (written consent not allowed)

• Opting out of the statutory defense

• Original charter rejects the statutory takeover defense

• Subsequent opt-out via charter or SH bylaw amendment by majority of shares entitled to vote (usually only effective after 12 months)

• DGCL §203 doesn’t apply to close corporations (no shares listed & fewer than 2,000 SHs), unless

• The interested SH caused the corporation to “go private”; or

• Charter specifically adopts the statutory takeover defense

White knights

• In a white knight defense, XB gets potential acquirer (Y2) to outbid Y, and signs an acquisition agreement selling X to Y2

– Variation of this is a “white squire”: Y2 (who supports XB) buys a minority position in X, thwarting majority SH support for Y’s hostile bid

– Purchases of X’s stock by X’s Employee Stock Ownership Plan (ESOP) has the effect of a white squire

• XB can encourage Y2 to outbid Y by –

– Preferential access to info about X (XB allows Y2 to conduct due diligence), resulting in Y2 having more certainty than Y regarding X’s value

– “Lock-ups” in the acquisition agreement (terms that shift value from X to Y2 if Y2 does not acquire X)

lock-ups:

• Termination fee

– X pays Y2 specified liquidated damages if X terminates acquisition agreement

– So if Y acquires X, X has to pay damages to Y2 reducing X’s value to Y

• “Crown jewels” provision

– Allows Y2 to acquire (at an attractive price) assets of X that Y particularly wants, if X terminates acquisition agreement

– Shifts value from X to Y2 like a termination fee, plus possibly eliminating the reason Y wants to acquire X

Similar defense: when Microsoft bid for Yahoo (wanting to consolidate search engines to counter Google), Yahoo negotiated with Google a joint venture providing Google with control of Yahoo’s search operations

Poison pills

“Poison pills” are contingent rights given to XS or T (third party), which if exercised make takeover less feasible.

Types:

1. flip-over plans (p38)

• Vehicle: equity securities (e.g., blank-check preferred shares)

• Trigger: executing a freezeout merger

• Poison: right to purchase common stock of the merged firm (either Y or S, merged with X) at below market price

– How can X cause S (controlled by Y) to issue shares?

• Antidote: usually, shares are redeemable by board for a nominal amount (e.g., 1¢)

2. flip-in plans (p40)

• Similar to flip-over plans, except:

– Trigger: exceeding a certain share ownership threshold (rather than freezeout)

– Poison: right to purchase shares in X (rather than in S)

3. back-end plans (p41)

• Vehicle: equity securities (e.g., blank-check preferred shares)

• Trigger: executing a freezeout

• Poison: XS may convert X’s shares into X’s bonds

– Bonds can include terms (covenants) that make it difficult to shift bridge financing to X (see “poison debt” in a later slide)

• This sets a minimum price for the acquisition

– Y has to offer higher back-end price (if Y offers a freezeout price lower than the value of the bonds, SHs will convert & receive the bonds)

– Higher back-end requires Y to also offer a higher front-end

4. poison debt (p43)

• Vehicle: debt securities

• Trigger: change of control (“CoC”) – covers various method to change control of the firm

• Poison: vehicle includes terms (covenants) that make it difficult to shift Y’s bridge financing to X

– Forbidding X from assuming additional debt

– Forbidding X from selling/mortgaging its assets

– Restricting ability to distribute dividends

– Macaroni defense: upon change of control, X must redeem bonds at premium price (e.g., 200% of face value)

• Called macaroni defense because debt expands like macaroni

– Antidote: XB allowed to waive covenants or redeem debt (before CoC occurs) for a nominal price

5. poison contracts (p44)

• Vehicle: contract with a third party (e.g., employees)

• Trigger: CoC

• Poison: transfer of value from X to third party

FD in the M&A context

Fiduciary duties: same analysis as any board/controller FD challenge

– Challenges to board behavior: framework in Section 1a1 (e.g., Van Gorkom)

– Challenges to controller behavior: framework in Section 1a3 (e.g., Kahn)

• Special rules for XB’s FD analysis in the M&A context

– When XB deploys corporate power against XS to achieve greater good for the firm (e.g., by deploying takeover defenses), use enhanced scrutiny SoR rather than BJR (Unocal)

Conditions

• Interference in SH voting (Blasius)

• Board implements takeover defenses (Unocal)

• Board implements poison pill designed to prevent any SH from owning >15%, to preserve tax advantages for firm (Selectica [Del. 2010])

• Board embarks on a transaction that will result in a change of control (Revlon)

Unocal analysis

1. Did the board find, in good faith & after a reasonable investigation, that the firm faced a threat that warranted the defensive action?

– Good faith: DoL analysis (similar to BJR)

– Reasonable investigation: DoC analysis (similar to BJR)

– Purpose/threat: what constitutes a legitimate threat? [Airgas, Del. Ch. 2011]

• Structural coercion (e.g., 2-tier front-loaded tender offer)

• Opportunity loss: offer preempts other offers that are better for SHs

• Substantive coercion: essentially, a price that the board deems inadequate (justification: subject to Revlon, board gets to choose long-term plans)

– Losing the “corporate culture” as result of takeover may be an acceptable threat (Paramount)

2. Was defensive action a reasonable response proportionate to the threat posed?

• Unitrin [Del. 1995]: presumed unreasonable if coercive/preclusive

– Coercive: “[A]ctions which have the effect of causing [SHs] to vote in favor of the proposed transaction for some reason other than the merits of that transaction” [Williams v. Geier, Del. 1996]

– Preclusive: making an acquisition by Y realistically unattainable

• Selectica [Del. 2010]: preclusive if Y’s ability to wage a successful proxy contest & gain control is realistically unattainable; but a combo of staggered board + poison pill is not inherently preclusive

• Airgas [Del. Ch. 2011]: defense is not preclusive as long as election process (proxy contests) would allow bidder to get the deal done

• Evaluate threat-response proportionality even if response is not coercive or preclusive

Revlon analysis:

• Condition: When the Board embarks on a transaction that will result in a change of control, Revlon applies. [Lyondell Chem. Co. v. Ryan, Del. 2009]

• When does Revlon not apply?

- Board does not support a sale (“just say no” defense)

- Board decision not to sell T analyzed under BJR

• - But if board negotiates with Y1, it has “embarked on a transaction… that will result in [CoC]”, so Revlon applies

• - Stock transaction that does not create change of control (Paramount)

• - under this circumstance: 1. If it’s a stock transaction, Revlon doesn’t apply. 2. Cash transaction, Revlon applies. 3. Half cash half stock: Revlon applies. (In re Smurfit-Stone)

Revlon duties:

1. enhanced scrutiny applies2. Board must act to maximize SHs’ short-term wealth (e.g. takeover defenses allowed only if they

increase the expected offer to XS) See: In re Dollar Thrifty [Del. Ch. 2010]

a. Process needs to be a reasonably way to achieve the interest, not necessarily the best way the court would have picked

b. Need to pick offer that’s best for XS in short-term, but not necessarily highest price