Embed Size (px)

Citation preview

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

ACCA教育领航者

咨询热线:400-6611-069

国际会计师培训基地

2016.09-2017.08 ACCA考纲解析

白皮书

P1-P7

目录

ACCA P1-P7 题型与分值.......................................................................................................... - 2 -

P1:Governance, Risk and Ethics........................................................................................ - 3 -

P2:Corporate Reporting......................................................................................................- 6 -

P3:Business Analysis.......................................................................................................... - 15 -

P4:Advanced Financial Management............................................................................- 19 -

P5:Advanced Performance Management....................................................................- 23 -

P7:Advanced Audit and Assurance ( INT)....................................................................- 29 -

东亚国际各分校联系方式........................................................................................................- 39 -

-1-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

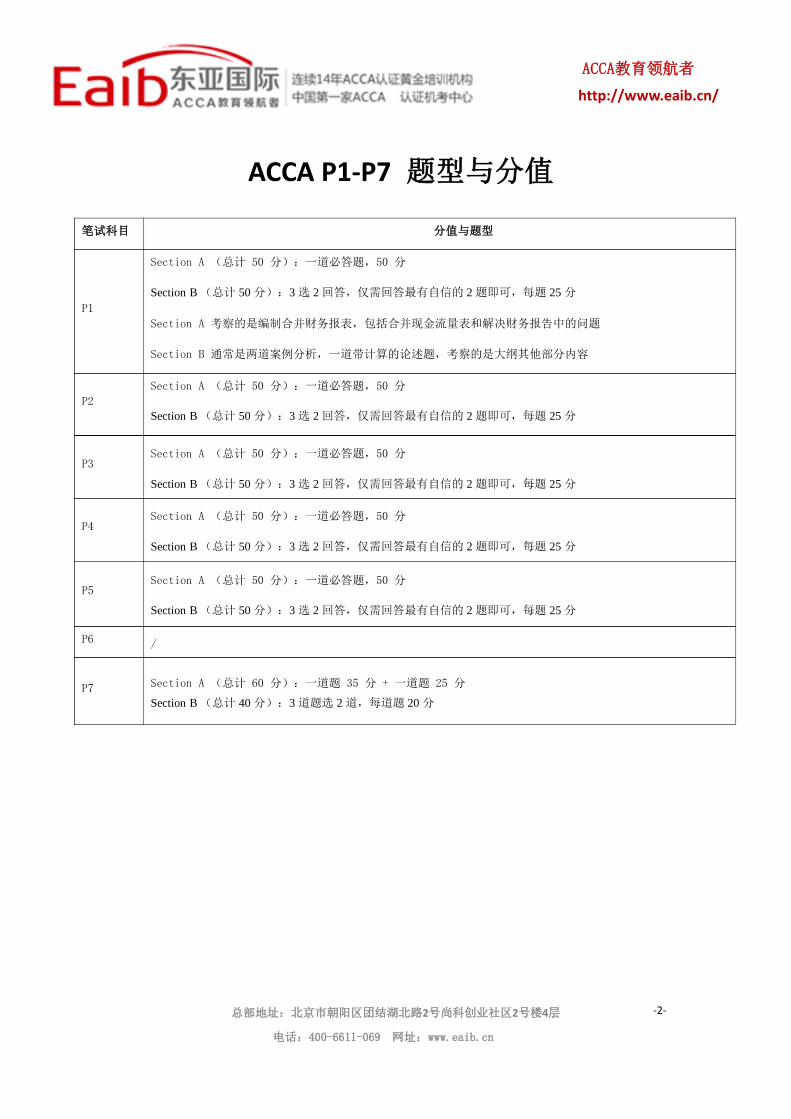

ACCA P1-P7 题型与分值

笔试科目

Section A (总计 50 分):一道必答题,50 分

Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

P1

Section A 考察的是编制合并财务报表,包括合并现金流量表和解决财务报告中的问题

Section B 通常是两道案例分析,一道带计算的论述题,考察的是大纲其他部分内容

Section A (总计 50 分):一道必答题,50 分

P2 Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

Section A (总计 50 分):一道必答题,50 分

Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

P4 Section A (总计 50 分):一道必答题,50 分

Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

P5 Section A (总计 50 分):一道必答题,50 分

Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

P6 /

Section A (总计 60 分):一道题 35 分 + 一道题 25 分

Section B (总计 40 分):3 道题选 2 道,每道题 20 分

分值与题型

P3

P7

-2-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

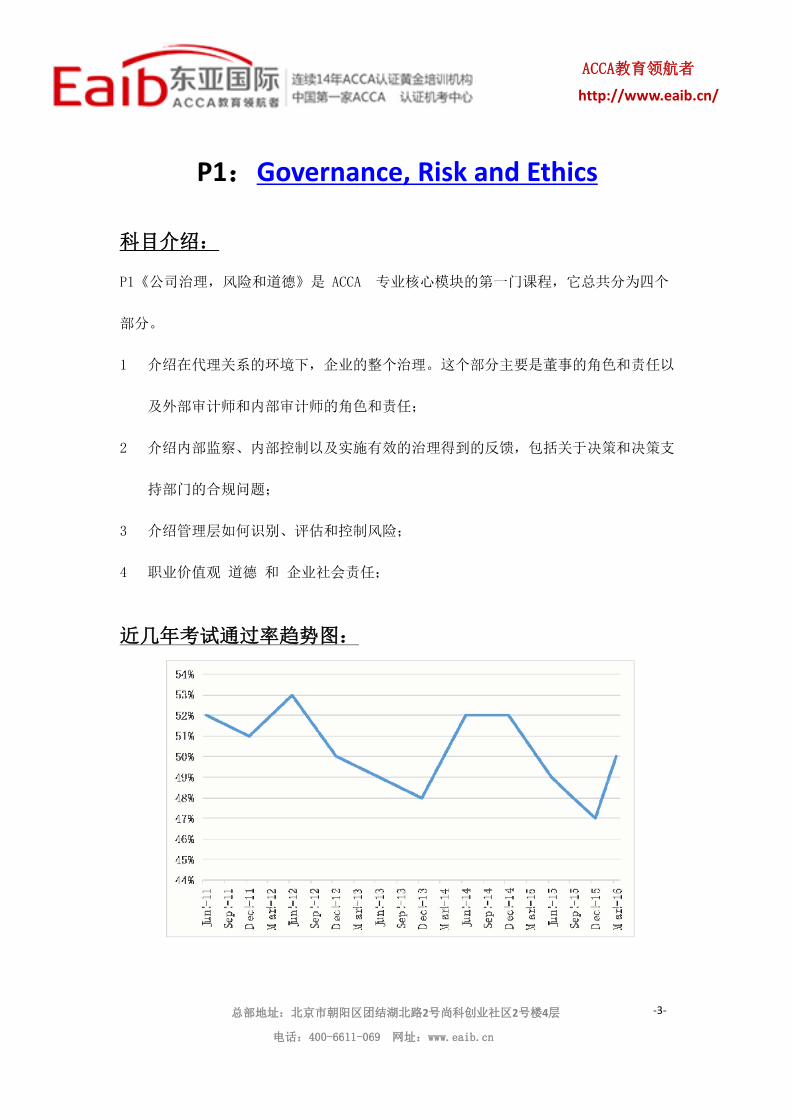

P1:Governance, Risk and Ethics

科目介绍:

P1《公司治理,风险和道德》是 ACCA 专业核心模块的第一门课程,它总共分为四个

部分。

1 介绍在代理关系的环境下,企业的整个治理。这个部分主要是董事的角色和责任以

及外部审计师和内部审计师的角色和责任;

2 介绍内部监察、内部控制以及实施有效的治理得到的反馈,包括关于决策和决策支

持部门的合规问题;

3

4

介绍管理层如何识别、评估和控制风险;

职业价值观 道德 和 企业社会责任;

近几年考试通过率趋势图:

-3-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

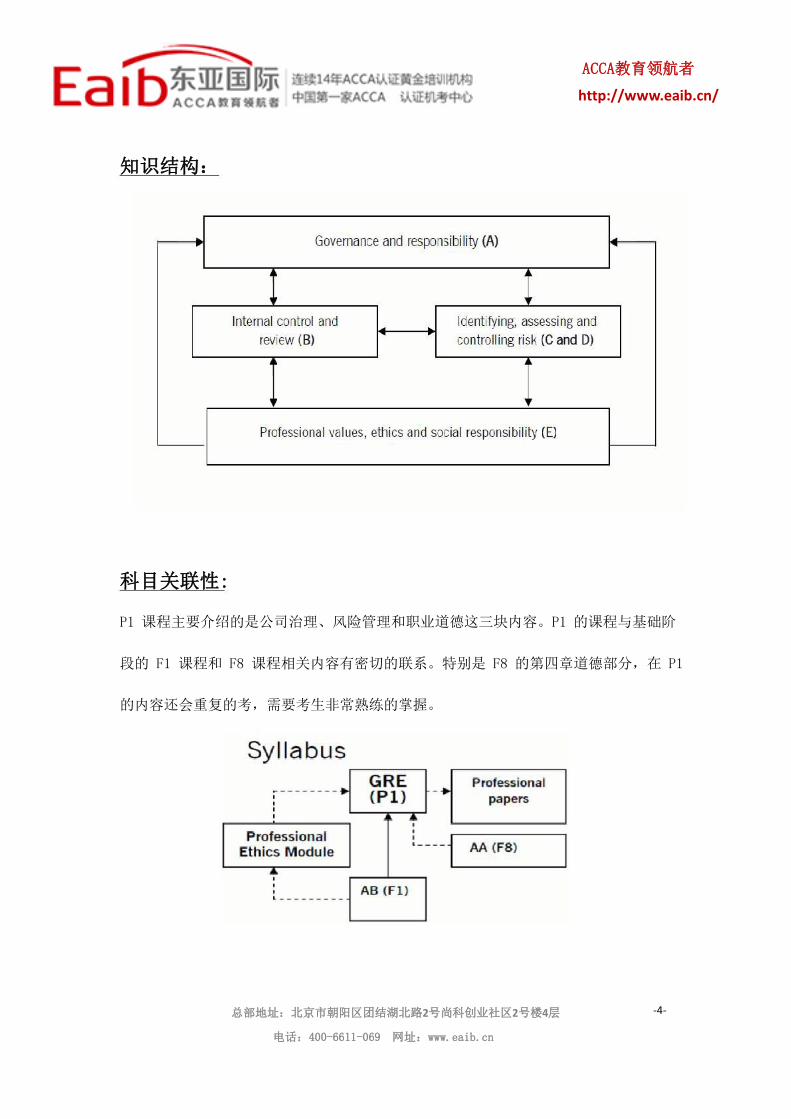

知识结构:

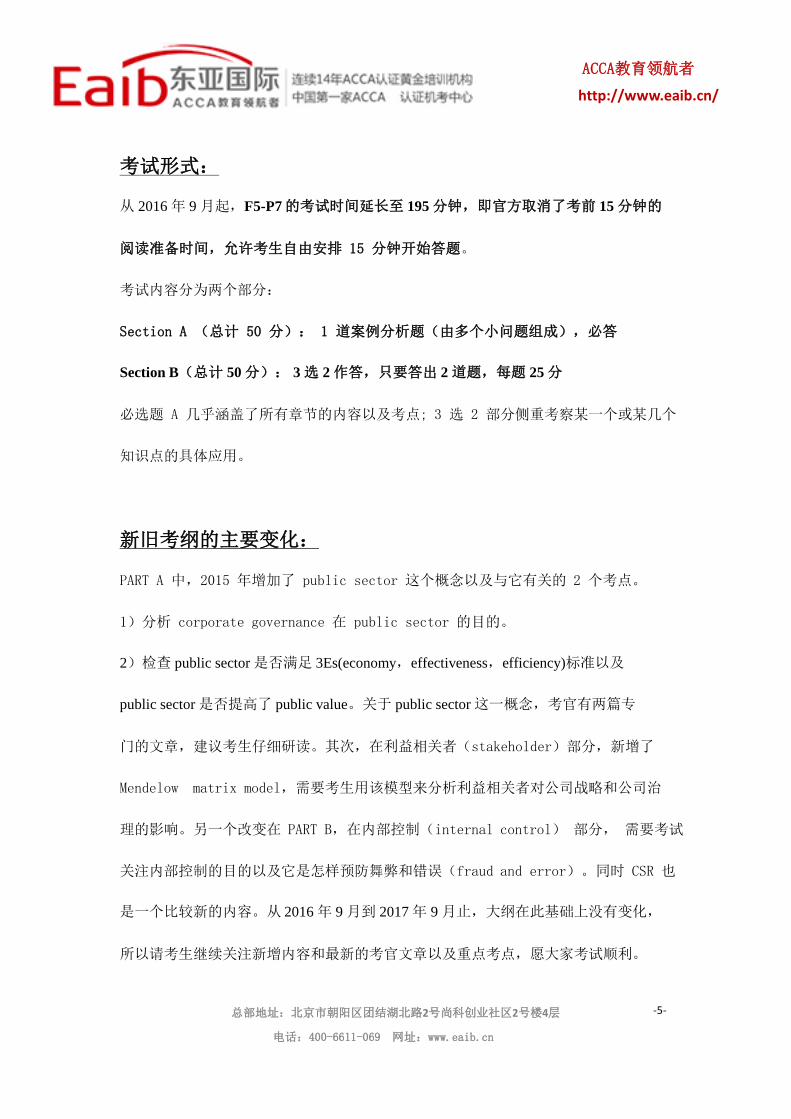

科目关联性:

P1 课程主要介绍的是公司治理、风险管理和职业道德这三块内容。P1 的课程与基础阶

段的 F1 课程和 F8 课程相关内容有密切的联系。特别是 F8 的第四章道德部分,在 P1

的内容还会重复的考,需要考生非常熟练的掌握。

-4-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

考试形式:

从 2016 年 9 月起,F5-P7 的考试时间延长至 195 分钟,即官方取消了考前 15 分钟的

阅读准备时间,允许考生自由安排 15 分钟开始答题。

考试内容分为两个部分:

Section A (总计 50 分): 1 道案例分析题(由多个小问题组成),必答

Section B(总计 50 分): 3 选 2 作答,只要答出 2 道题,每题 25 分

必选题 A 几乎涵盖了所有章节的内容以及考点; 3 选 2 部分侧重考察某一个或某几个

知识点的具体应用。

新旧考纲的主要变化:

PART A 中,2015 年增加了 public sector 这个概念以及与它有关的 2 个考点。

1)分析 corporate governance 在 public sector 的目的。

2)检查 public sector 是否满足 3Es(economy,effectiveness,efficiency)标准以及

public sector 是否提高了 public value。关于 public sector 这一概念,考官有两篇专

门的文章,建议考生仔细研读。其次,在利益相关者(stakeholder)部分,新增了

Mendelow matrix model,需要考生用该模型来分析利益相关者对公司战略和公司治

理的影响。另一个改变在 PART B,在内部控制(internal control) 部分, 需要考试

关注内部控制的目的以及它是怎样预防舞弊和错误(fraud and error)。同时 CSR 也

是一个比较新的内容。从 2016 年 9 月到 2017 年 9 月止,大纲在此基础上没有变化,

所以请考生继续关注新增内容和最新的考官文章以及重点考点,愿大家考试顺利。

-5-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

P2:Corporate Reporting

科目介绍:

P2《公司报告》是 F7《财务报告》的后续课程,它更加深入地考察会计师对会计

准则的掌握以及在商业环境下对财务报告原理和做法的运用与评估。P2 主要分为四大

部分。

1. 根据公认会计原则和相关会计准则,会计师在编制合并财务报表时所要考虑的财务

报告框架;

2.

3.

4.

特殊行业的报表特点,包括非盈利组织和中小企业;

察会计师的财务分析能力和对公司报告的影响;

一些会计准则当前的发展变化以及它们对财务报告的影响。

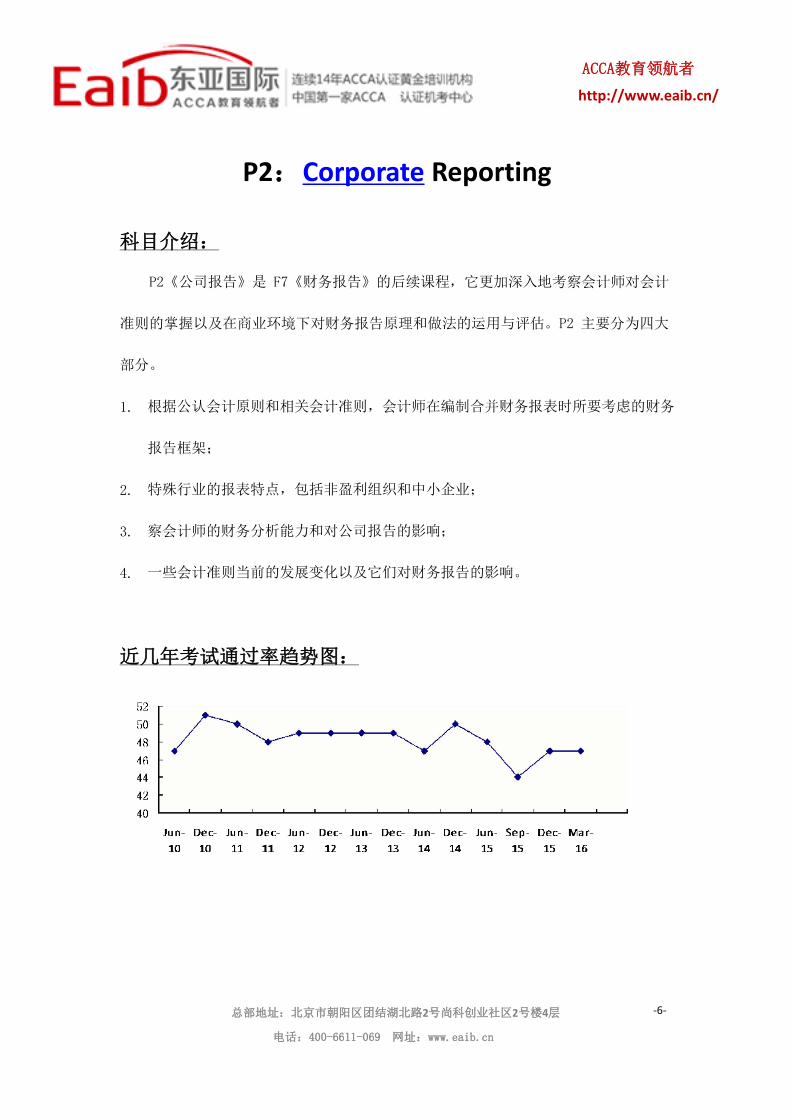

近几年考试通过率趋势图:

-6-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

知识结构:

科目关联性:

P2 课程是 ACCA 财务会计体系下的最后一门

课程,它是前面 F3、F7 课程的后续课程, 在 F3

和 F7 的基础上更加深入地考察考生对会计准则的

掌握程度和运用相关知识进行财务分析的能力。 和

P2 某些内容有些关联的是 ACCA 的最后一门课程

P7《高级审计和鉴证》。

-7-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

考试形式:

从 2016 年 9 月起,F5-P7 的考试时间延长至 195 分钟,即官方取消了考前 15 分

钟的阅读准备时间,允许考生自由安排 15 分钟开始答题。

Section A (总计 50 分):一道必答题,50 分

考察的是编制合并财务报表,包括合并现金流量表和解决财务报告中的问题

Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

通常是两道案例分析,一道带计算的论述题,考察的是大纲其他部分内容

新旧考纲的主要变化:

从 2016 年 9 月的考试开始,考纲内容没有任何增减。

以下表格是去年(即 2015 年 9 月开始)考纲内容相比较再之前一年的一些微调,

这个仍适用于 2016 年 6 月的考试,故总结如下,供大家参考:

考纲章节和主题

新增 C1b) and c))

考纲内容

讨论和应用在企业可以应用收入确认模型至合

同的标准。讨论和应用客户合同所获收入的 5

步模型。

新增 C3d) 应用 和讨 论预期 减值 损失( expected loss

impairment loss)的会计处理。

-8-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

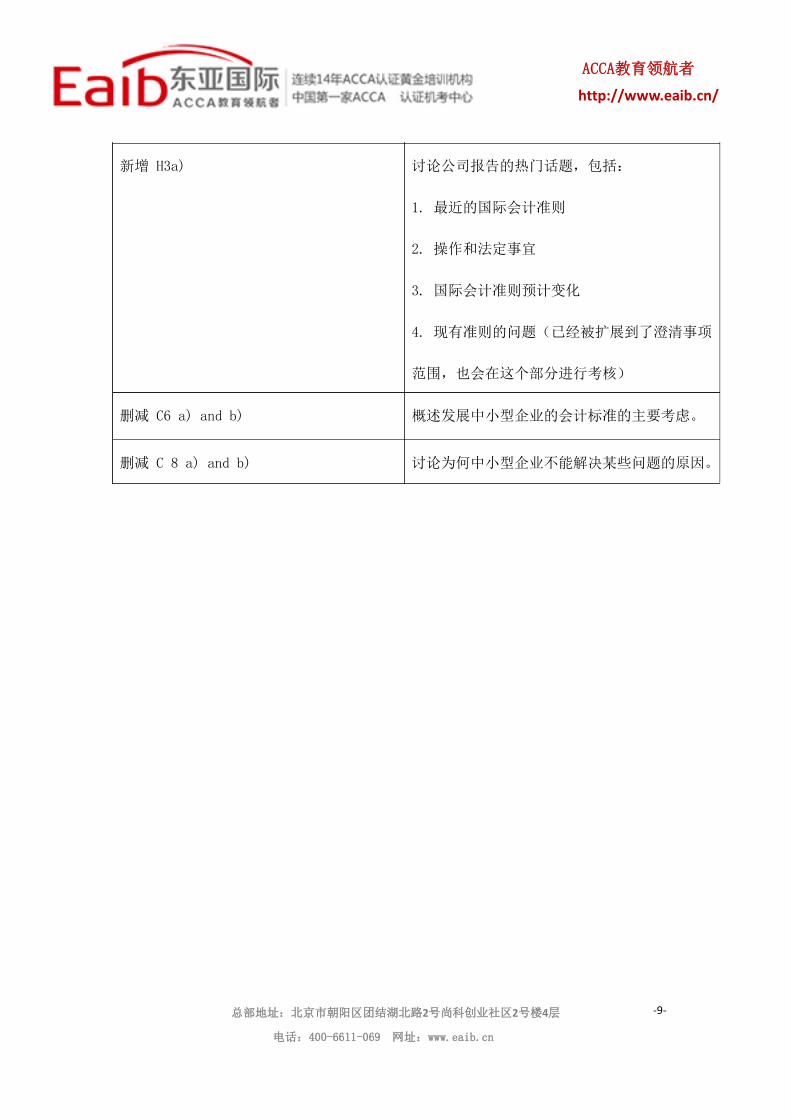

新增 H3a) 讨论公司报告的热门话题,包括:

1. 最近的国际会计准则

2. 操作和法定事宜

3. 国际会计准则预计变化

4. 现有准则的问题(已经被扩展到了澄清事项

范围,也会在这个部分进行考核)

删减 C6 a) and b)

删减 C 8 a) and b)

概述发展中小型企业的会计标准的主要考虑。

讨论为何中小型企业不能解决某些问题的原因。

-9-

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

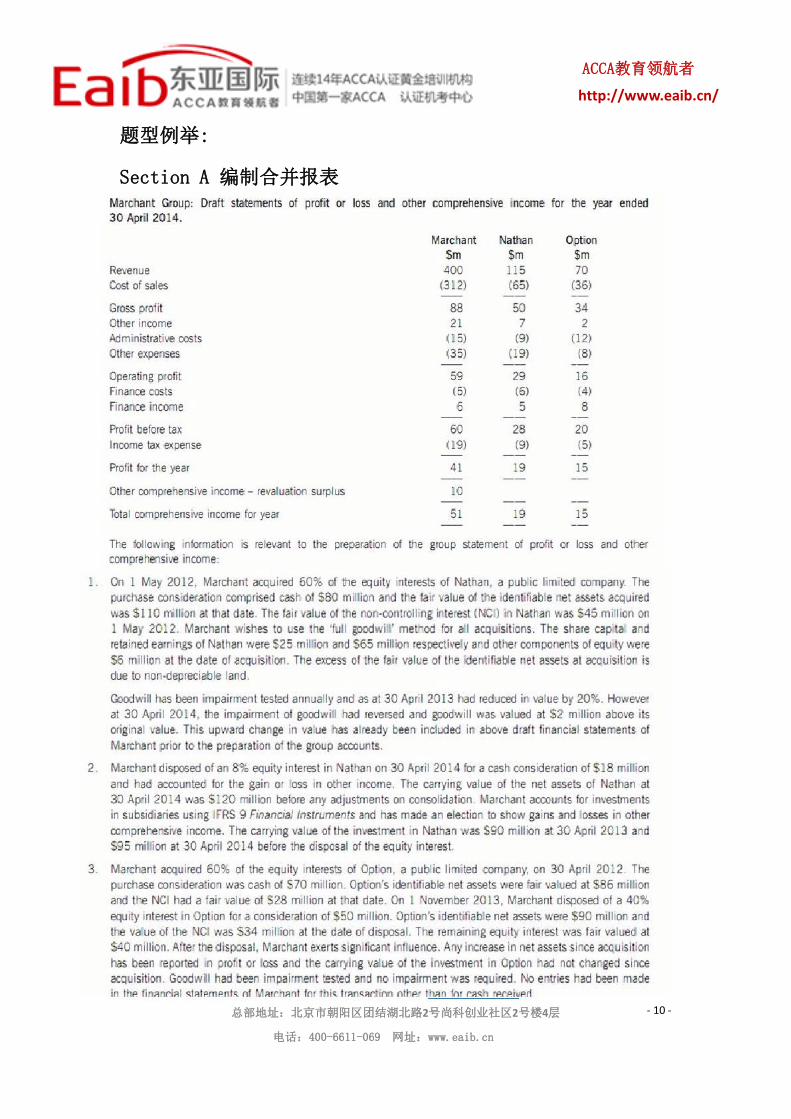

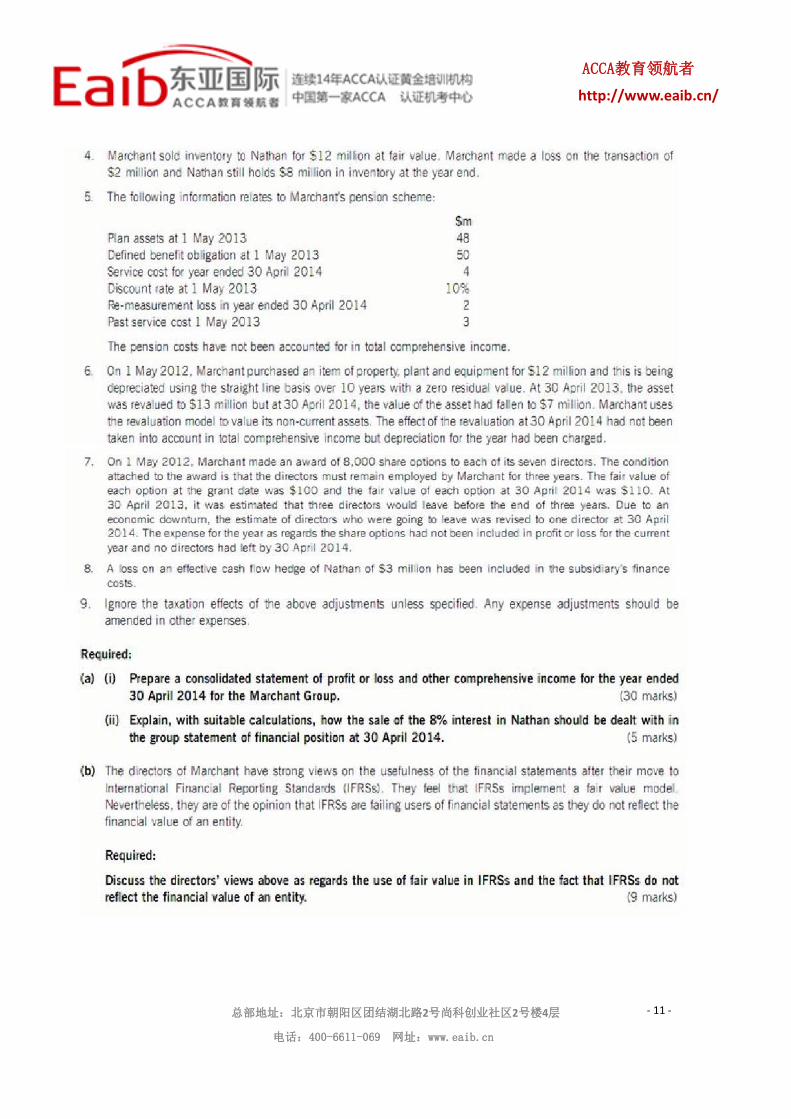

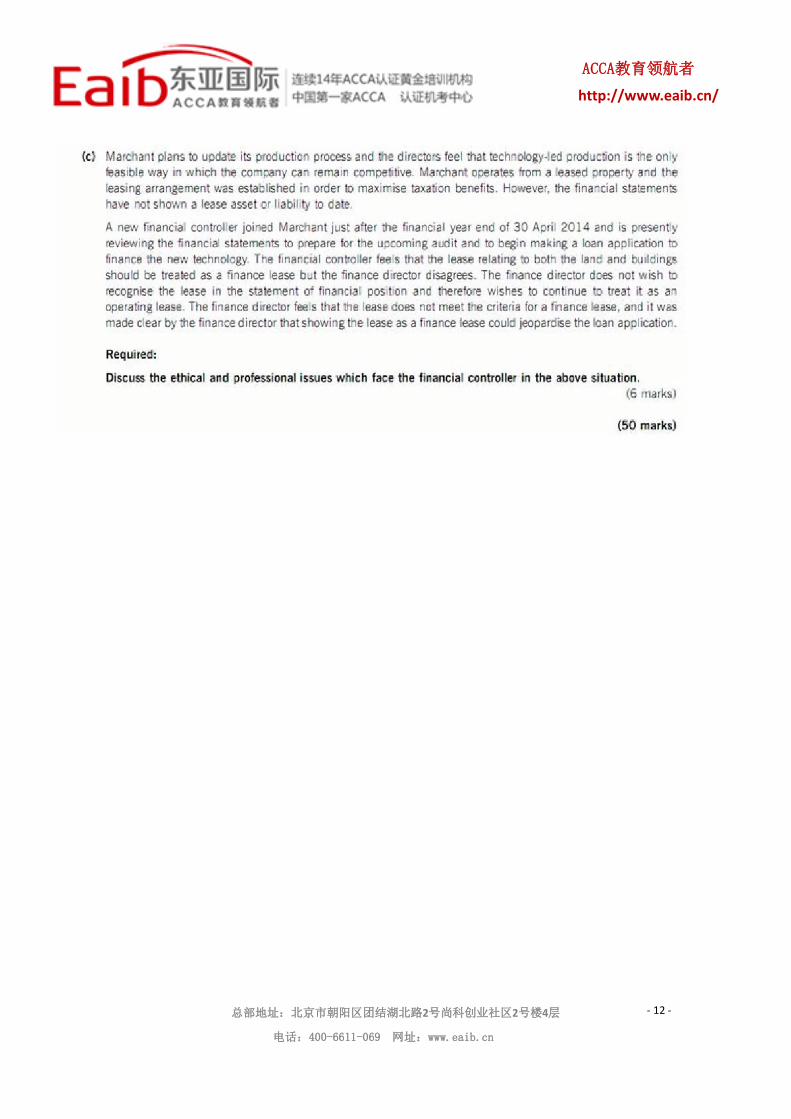

题型例举:

Section A 编制合并报表

- 10 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

- 11 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

- 12 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

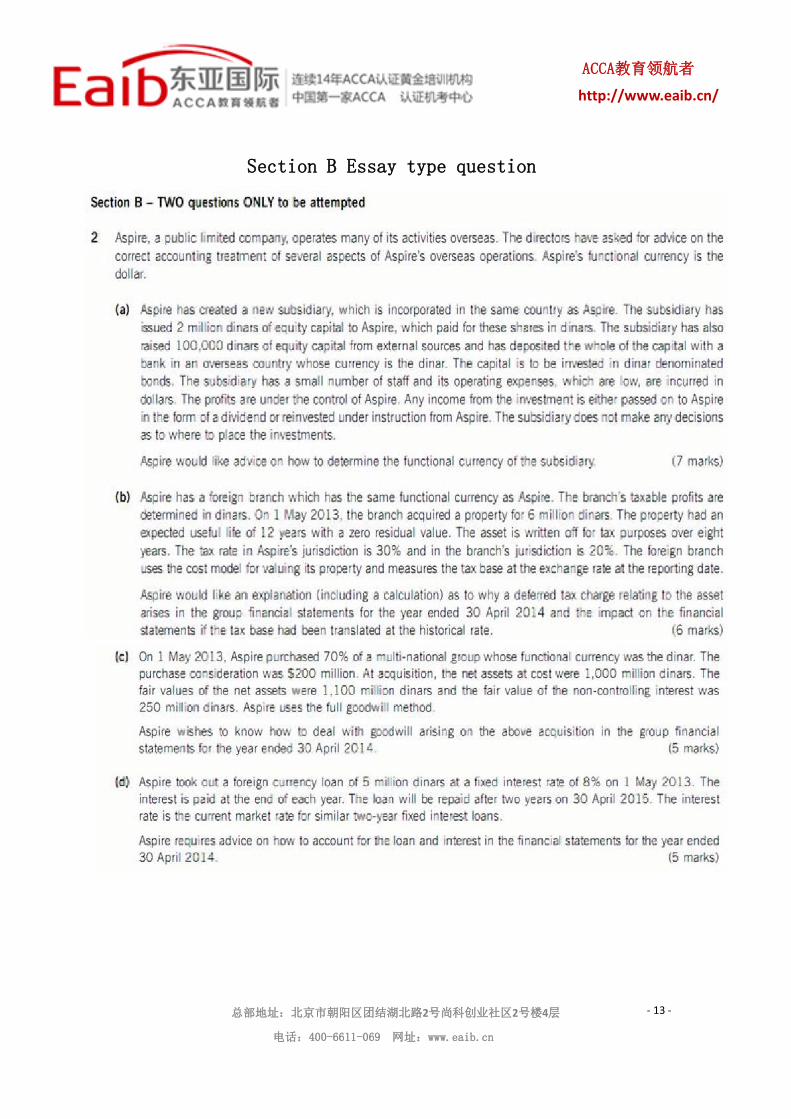

Section B Essay type question

- 13 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

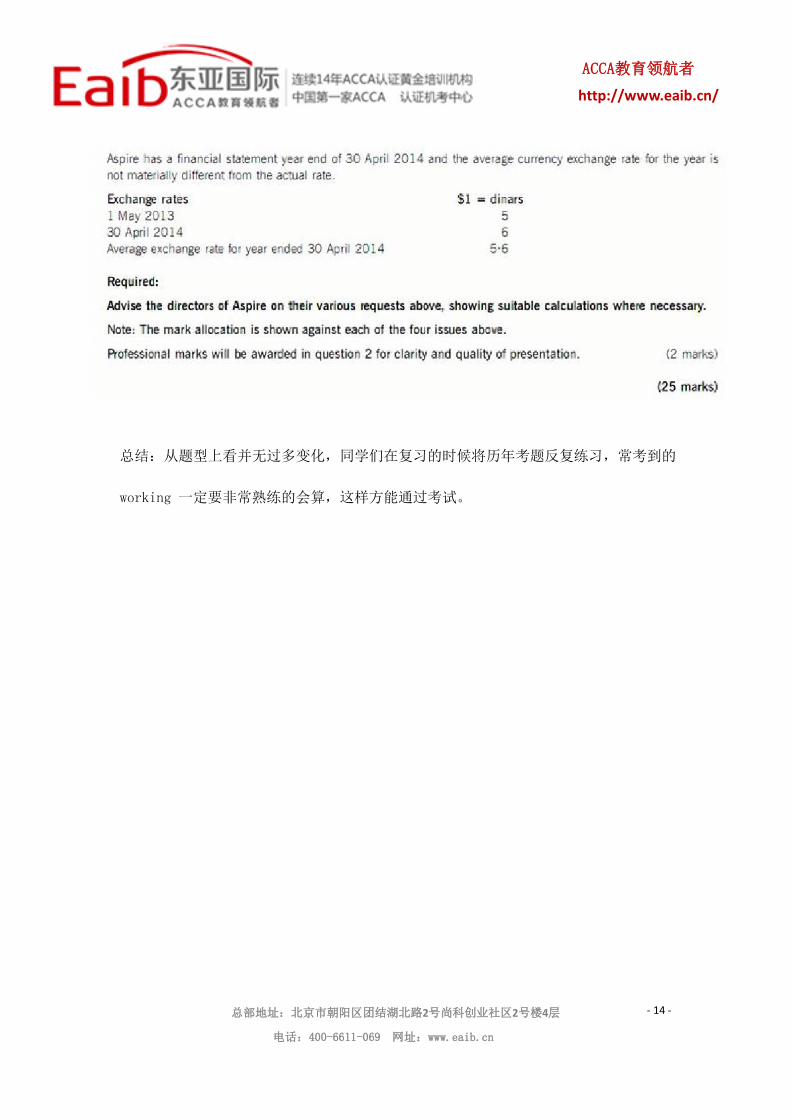

总结:从题型上看并无过多变化,同学们在复习的时候将历年考题反复练习,常考到的

working 一定要非常熟练的会算,这样方能通过考试。

- 14 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

P3:Business Analysis

相关资源下载:

P3 2012 syllabus and study guide

P3 Pilot Paper Questions and Answers (Up to 2010 Dec)

P3 Pilot Paper Questions and Answers (Up to 2010 Jun)

P3 2013 Dec Exam Question

P3 2013 Dec Exam Answer

P3 2014 June Exam Question

P3 2014 June Exam Answer

科目介绍:

P3《商业分析》主要围绕的是三个部分进行讲述:

1. 战略定位。运用相关预测技巧对现有环境和将来环境的战略定位进行分析;主要关

注的是企业的外部环境、内部能力和期望;

2. 战略选择。战略选择关注的是企业未来的决策,以及应对现有和将来战略定位影响

和压力的方式;

3. 战略实施。战略实施关注的是战略选择的实施和转变战略选择为公司行为。这些行

为包括在业务过程重组、信息技术、项目管理、财务分析和人力资源这几个方面。

- 15 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

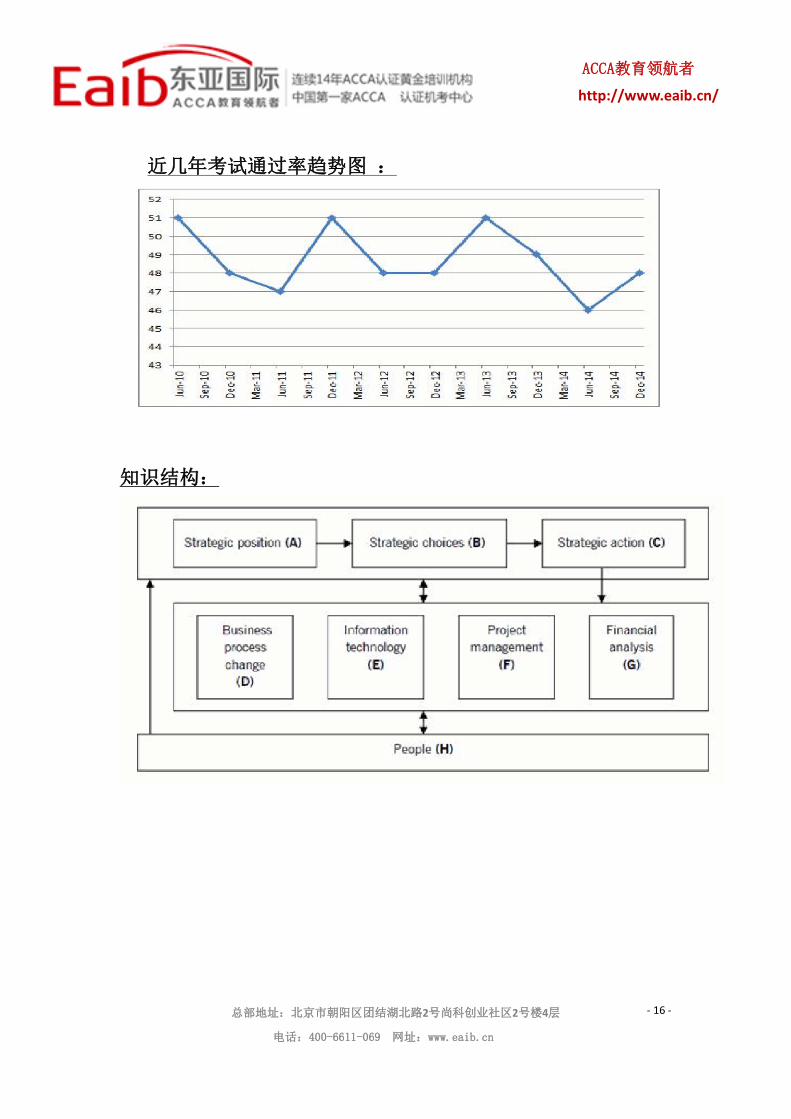

近几年考试通过率趋势图 :

知识结构:

- 16 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

科目关联性:

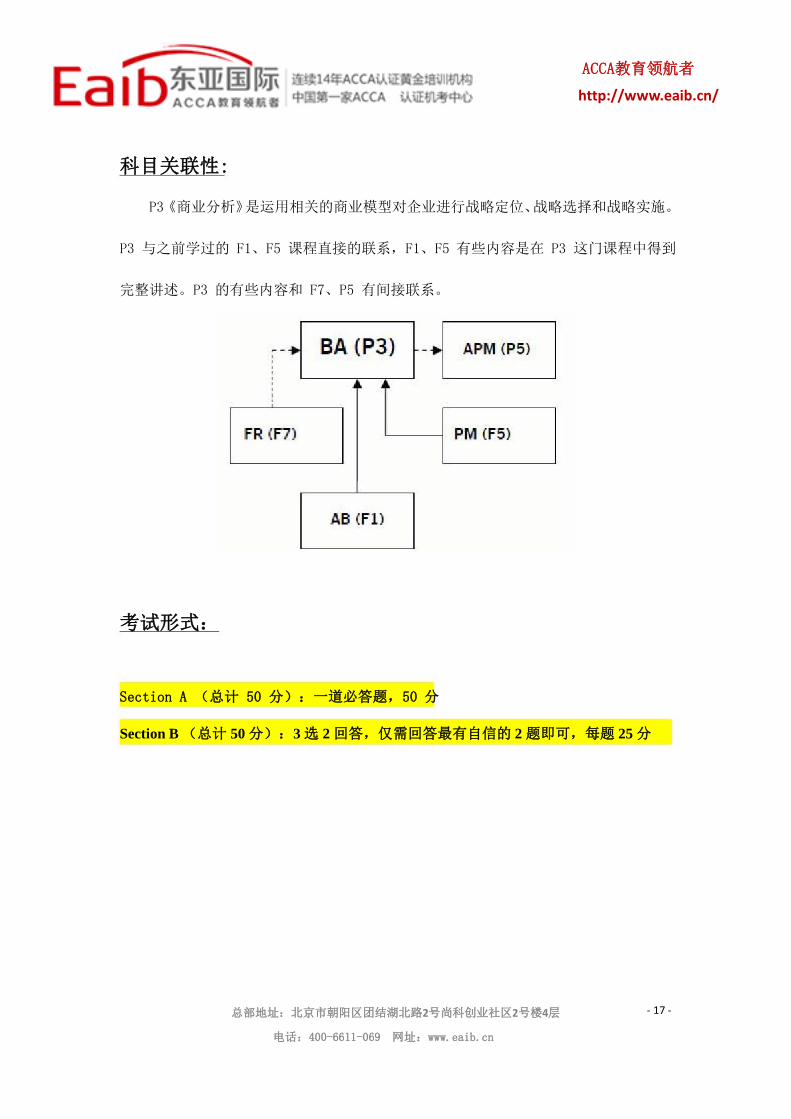

P3 《商业分析》 是运用相关的商业模型对企业进行战略定位、 战略选择和战略实施。

P3 与之前学过的 F1、F5 课程直接的联系,F1、F5 有些内容是在 P3 这门课程中得到

完整讲述。P3 的有些内容和 F7、P5 有间接联系。

考试形式:

Section A (总计 50 分):一道必答题,50 分

Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

- 17 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

新旧考纲的主要变化:

P3 的考纲在 2011 年 6 月考试开始,进行了重大调整。

在 P3 的新大纲下,新的准则规定等会加入到考察范围,并且管理会计的知识会大

量加入到案例分析中。 过往的 P3 考试强调了战略方面的考虑而忽略了管理会计的知

识, 导致有些题目脱离了实际。 这次大纲的改变为考官提供了一个更"真实"的出题平台,

要求考试不仅仅能从战略层面进行商业分析,同时运用财务分析,例如预测预算,成本

会计等数量化的分析技巧来综合的进行决策。 这些变化将对整个科目产生一个较根本的

影响,所以 P3 会对 Pilot paper 进行全面的更新,让大家了解新的考试方向和模式。

2015 年考纲变化如下(2016 年 P3 考纲无明显变化):

考纲章节和主题

新增 C1e

新增 G1b

考纲内容

讨论如何使用大数据通知和执行企业战略

讨论财务部如何转变使得会计在从战略拟

定和执行到影响企业业绩这些决策过程中

扮演重要角色

G1 名称变化

重述 G2 a 和 b

财务

在支持战略企划和决策制定中,评估预算,

标准成本和差异分析

重述 G2 c 考虑风险和不确定性,评估战略和操作决

策(包括使用决策树)

- 18 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

P4:Advanced Financial Management

科目介绍:

P4《高级财务管理》是 F9《财务管理》的后续课程,更加注重一些复杂的战略财

务管理问题的解决。大纲分为四大部分,主要考察:

1. 在跨国企业的环境下,高级行政人员或咨询人员在满足不同利益相关者需求时

扮演的角色和责任;

2.

3.

在本国和国际环境下,投资决策和融资决策对战略结果的影响;

在复杂的公司结构下,财产管理部门的角色,其中包括企业存在的风险和管理

这些风险的战略;

4. 财务问题的影响。

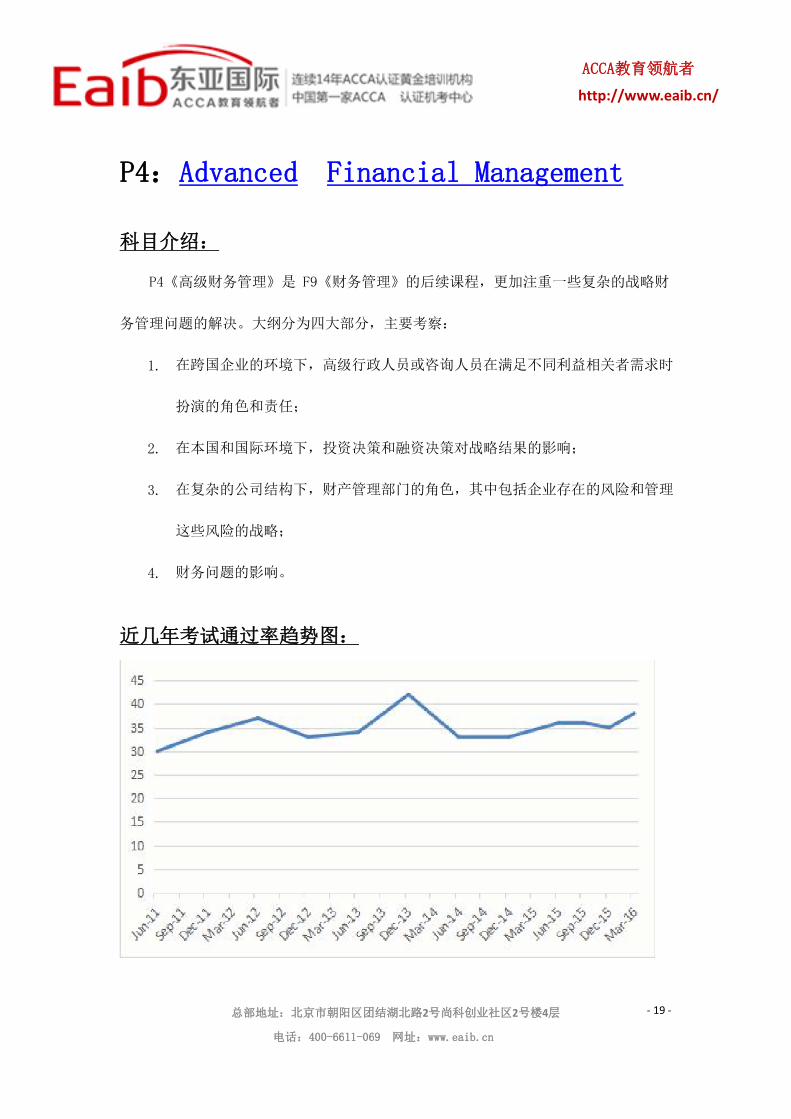

近几年考试通过率趋势图:

- 19 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

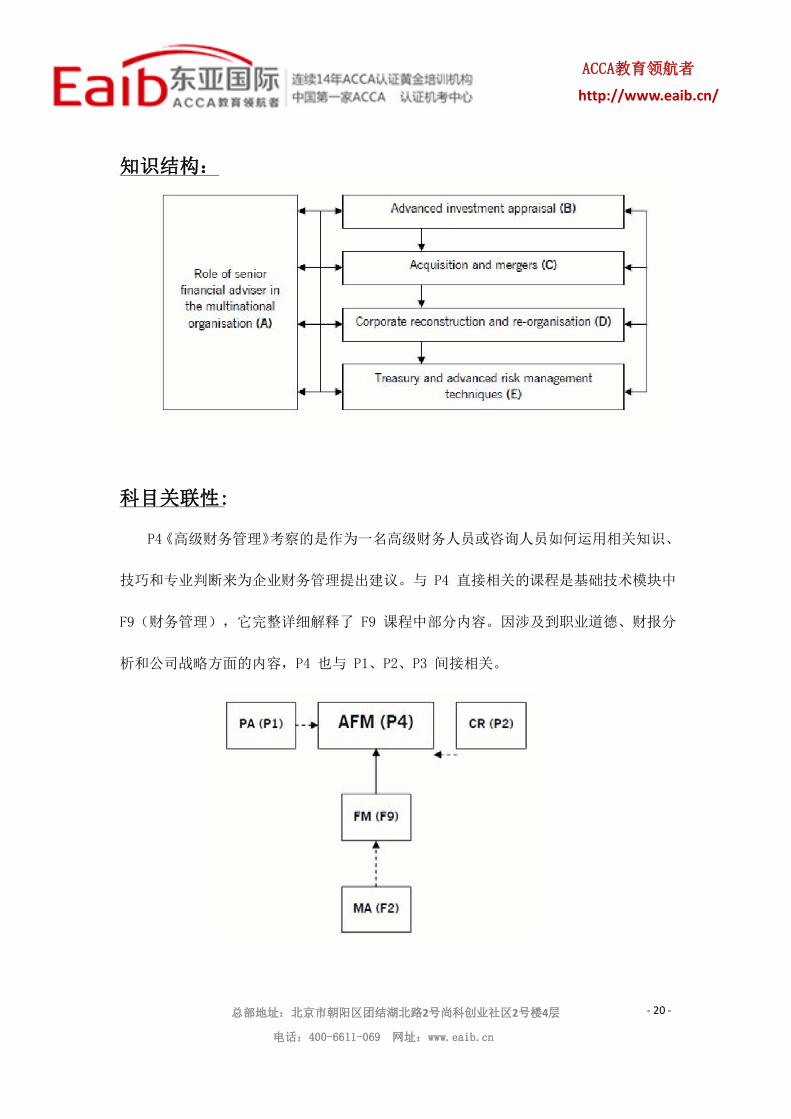

知识结构:

科目关联性:

P4 《高级财务管理》 考察的是作为一名高级财务人员或咨询人员如何运用相关知识、

技巧和专业判断来为企业财务管理提出建议。与 P4 直接相关的课程是基础技术模块中

F9(财务管理),它完整详细解释了 F9 课程中部分内容。因涉及到职业道德、财报分

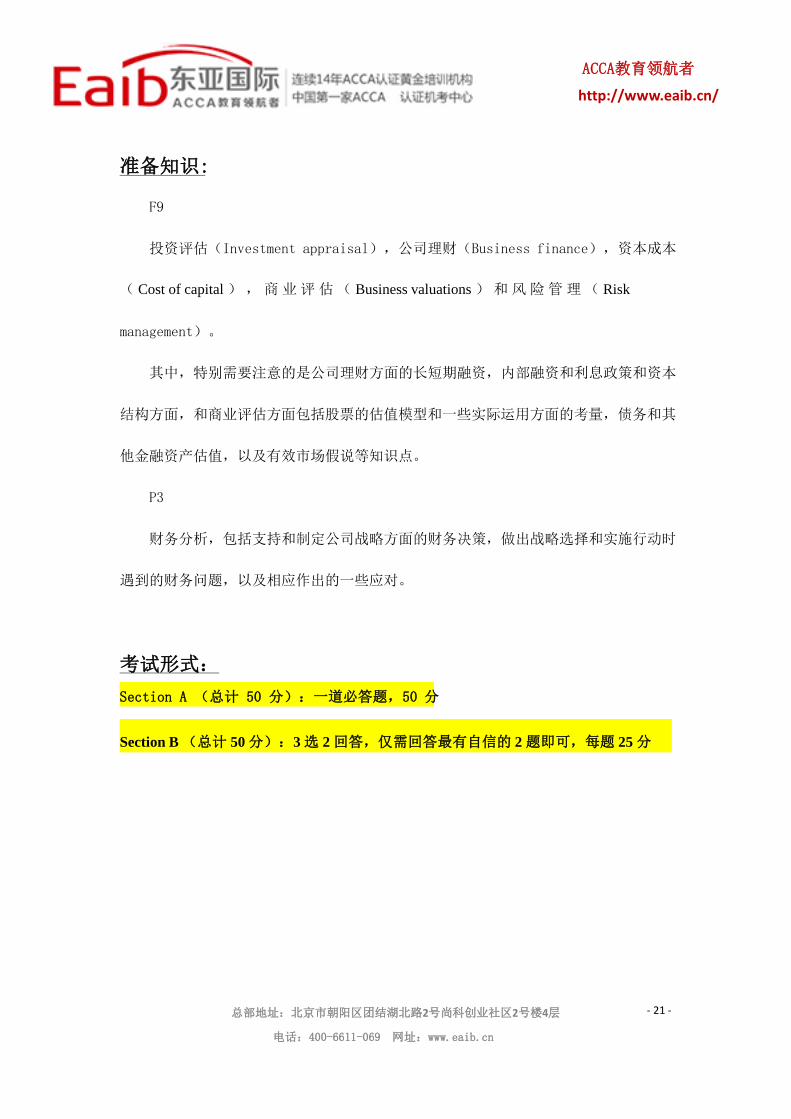

析和公司战略方面的内容,P4 也与 P1、P2、P3 间接相关。

- 20 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

准备知识:

F9

投资评估(Investment appraisal),公司理财(Business finance),资本成本

( Cost of capital ) , 商 业 评 估 ( Business valuations ) 和 风 险 管 理 ( Risk

management)。

其中,特别需要注意的是公司理财方面的长短期融资,内部融资和利息政策和资本

结构方面,和商业评估方面包括股票的估值模型和一些实际运用方面的考量,债务和其

他金融资产估值,以及有效市场假说等知识点。

P3

财务分析,包括支持和制定公司战略方面的财务决策,做出战略选择和实施行动时

遇到的财务问题,以及相应作出的一些应对。

考试形式:

Section A (总计 50 分):一道必答题,50 分

Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

- 21 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

新旧考纲的主要变化:

2016 September-2017 Jun 考纲内容有不同程度的删减与变化, 以前 15 年考纲的

B 部分内容 Economic environment for multinational organisations 的主要内容全

部合并入新考纲 A 部分,以前考纲 G 部分内容 Emerging issues in financial

management 整体做了删减,使得 P4 考核重点更加突出。 其他考纲的细微的调整包

括 dividend policy in multinationals and transfer pricing 从 以 前 考 纲 内 容

Treasury and advance risk management techniques 移动到新考纲 A 部分 Role

and responsibility 下进行考核。 部分加入的新内容还包括 behavioural finance 行 A

为金融学这一新增内容, 而对 conflict of stakeholder interest 不再考核。 新考纲 B 部

分 Advanced investment appraisal 难度减低,不再要求 simple model design of

Monte Carlo simulation 这一简单建模的考核, 但加入 project duration 久期的计算。

同时新考纲对 Mergers and acquisition 这部分难度稍有降低,删减了 compare

various source of finance 以及 evaluate acquisition proposal 这种应用难度高的要

求,但增加了对 reverse acquisition 内容的考察 ,总体来说考官考核目标更清晰和切

合实际,对部分难点和对应用能力要求很高的内容不再做要求。

- 22 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

P5:Advanced Performance Management

科目介绍:

P5《高级业绩管理》是 F5《业绩管理》的后续课程,是对 F5 的扩展和深入,需要学员

在学习之前,对 F5 的大纲有深刻地理解,除此之外,也要求学员能够灵活应用 F2《管

理会计》的中学到的知识和技巧,同时也涉及 P3《商业分析》中有关战略计划与控制

和业绩评估的内容。

最新版的大纲分为五大部分:

1. 利用战略规划和控制模型来计划和监控组织的业绩

2. 评估和确定相关宏观经济,财政和市场因素以及主要外部环境对企业的影响

3. 确定与评价有效的业绩管理信息和监控系统

4. 运用恰当的战略业绩评估方法来评价并且提升企业的业绩

5. 确定和评估当前管理会计和业绩评估的发展对衡量,评估和提高企业业绩的影响,

以及向客户及管理层就企业的战略业绩评价和企业失败的致命性提出一定的建议

- 23 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

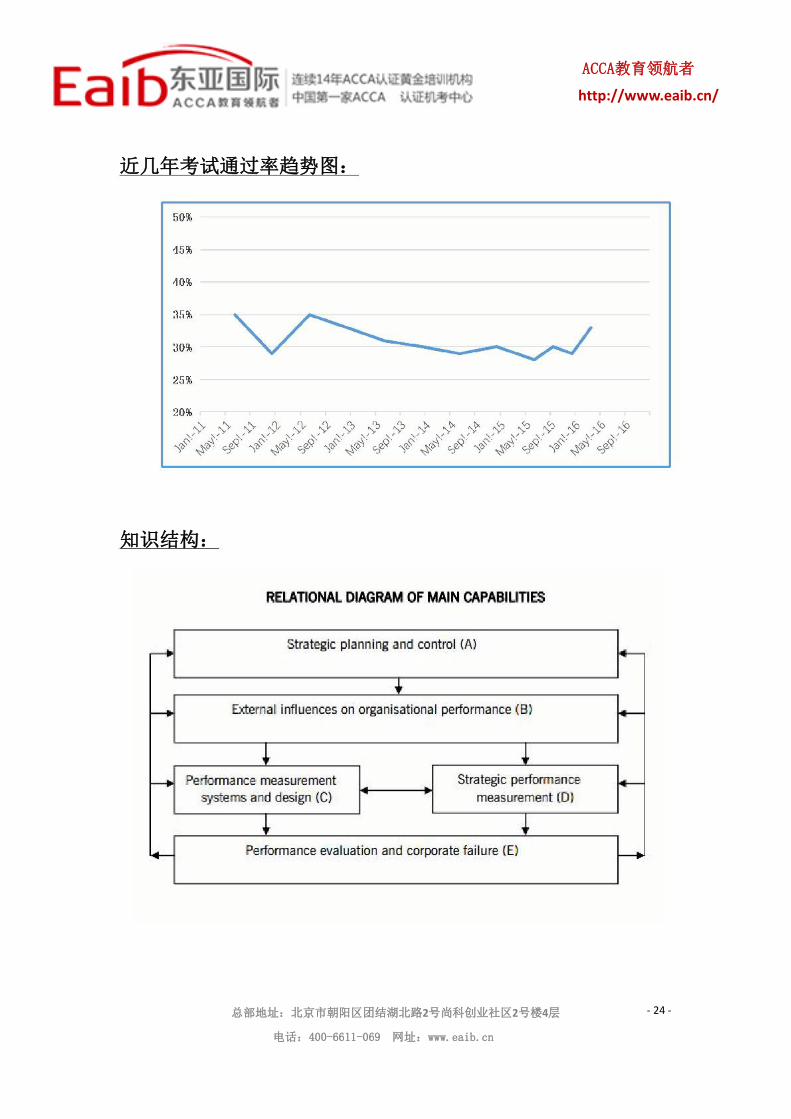

近几年考试通过率趋势图:

知识结构:

- 24 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

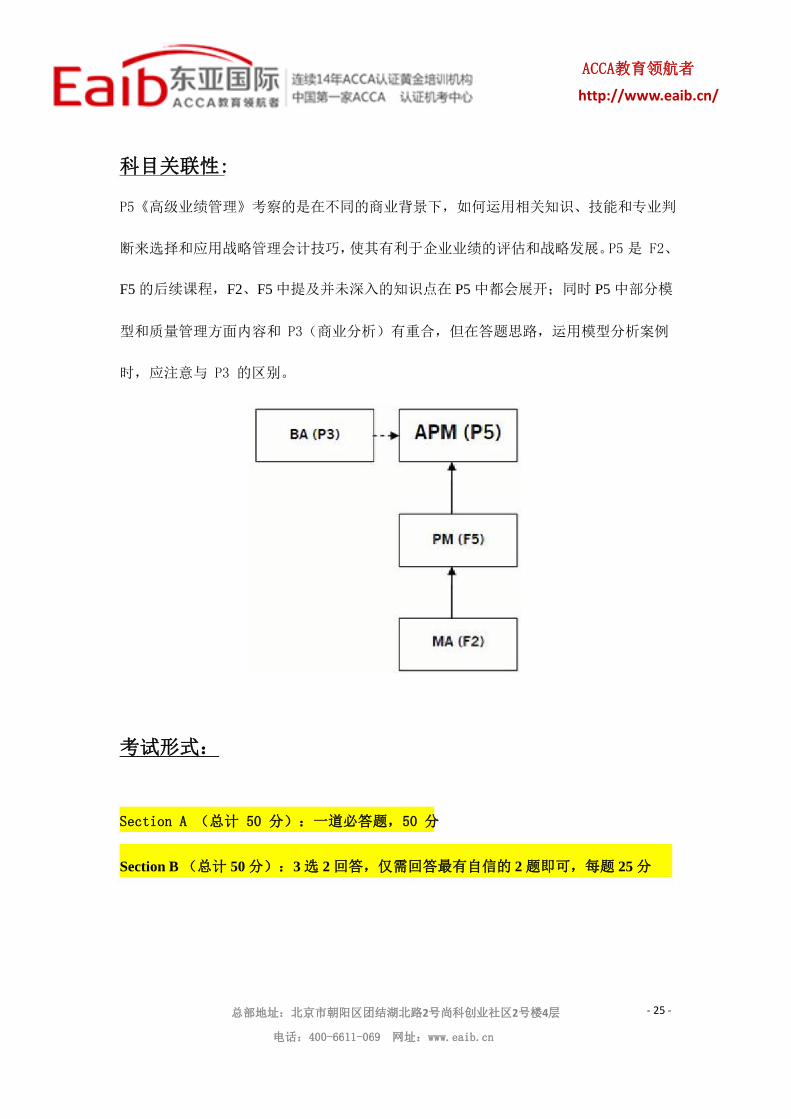

科目关联性:

P5《高级业绩管理》考察的是在不同的商业背景下,如何运用相关知识、技能和专业判

断来选择和应用战略管理会计技巧, 使其有利于企业业绩的评估和战略发展。 是 F2、 P5

F5 的后续课程,F2、F5 中提及并未深入的知识点在 P5 中都会展开;同时 P5 中部分模

型和质量管理方面内容和 P3(商业分析)有重合,但在答题思路,运用模型分析案例

时,应注意与 P3 的区别。

考试形式:

Section A (总计 50 分):一道必答题,50 分

Section B (总计 50 分):3 选 2 回答,仅需回答最有自信的 2 题即可,每题 25 分

- 25 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

新旧考纲的主要变化:

在 2016 年 9 月至 2017 年 6 月的考纲中,内容发生了较大调整,具体如下:

1. In Part A, (1)重点强调不同种类的 budget variances 以及 它们在计划过程 和

控制企业中的作用; (2) 删 掉 了 对 beyond budgeting and input/ output

analysis 的考察, 同时,IT 系统对管理信息的影响部分结合调整后的最新内容,综

合理解。

2. In Part B , 删 掉 了 几 个 零 碎 的 知 识 点 , 分 别 是 traditional management

accounting techniques 的评价,商业分析模型在 funding 中的应用和政府的相

关法规和政策对 performance measurement 的影响。

3. In part C, 不再对责任会计的相关知识点进行考察。

4. In part D, (1)强调对“what gets measured,gets done”的理解 参考历年考

题为 12 June Q1 (iii); (2)同样地,删除了以下两个主要知识点 一是与 employee

相关的非财务因素(NFIs); 二是对 quality,quality assurance, quality control

and quality management 的区分 以及 quality management 的益处。

5. In part E, 首先应当注意的是,考官把历年 part F 的内容一同并入其中,因而,整

个结构也更新为五大部分; 同时,最需要强调的是,重要的业绩分析模型

Performance Prism has been deleted.

除此之外,考官对整个大纲的结构也进行了调整,重新编排了各章节内容的顺序,

新增加了一些跟企业社会最新发展相关的话题。

- 26 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

学习建议:

P5 是一门学习起来相对容易,但考试并不容易的课程,事实上,它需要很多的实际工

作经验来支持,因为考试中很多都是现实中的案列,需要你利用积累的经验对它做出判

断然后提出一些改进意见和评价。

很多考生考完 p5 都是特别自信地走出考场,但是结果往往都会有些不尽人意,考官分

析报告指出主要的失败在于”答非所问“,这样往往会造成即使你写了很大一段,但结

果得分很低。

举一个很常见的例子, 之前考官就evaluate performance 和evaluate performance

report 做过重点考察,这两个问题的侧重点是完全不一样的,一旦答偏问题,则会失

去很大的分值,具体的实例看一下:2012 JUNE Q1 , 2014 JUNE Q1 考察的是

performance report 以 及 2012 DEC Q1 重 点 考 察 的 是 performance

(divisional),需要考生能好好总结两种不同的答法。

总而言之,P5 最重要的是在看懂考官问题的同时,每一问都能回答到点上,因此要求

考生在临考前完成至少三遍的真题训练,强调一定要自己动手去做,那么顺利通过考试

将不再是难事。

相关资源下载:

P5 2016-2017 syllabus and study guide

P5 2012 Jun Exam Question

P5 2012 Jun Exam Answer

- 27 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

P5 2012 Dec Exam Question

P5 2012 Dec Exam Answer

P5 2014 Jun Exam Question

P5 2014 Jun Exam Answer

- 28 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

P7:Advanced Audit and Assurance ( INT)

科目介绍:

The aim of ACCA Paper P7 ( INT ) is to analyses, evaluate and conclude on the

assurance engagement and other audit and assurance issues in the context of

best practice and current developments.

The Core areas of the syllabus:

1.Regulatory environment

2.Professional and ethical considerations

3.Practice management

4.Audit of historical financial information

5.Other assignments

6.Reporting

7.Current issues and developments

- 29 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

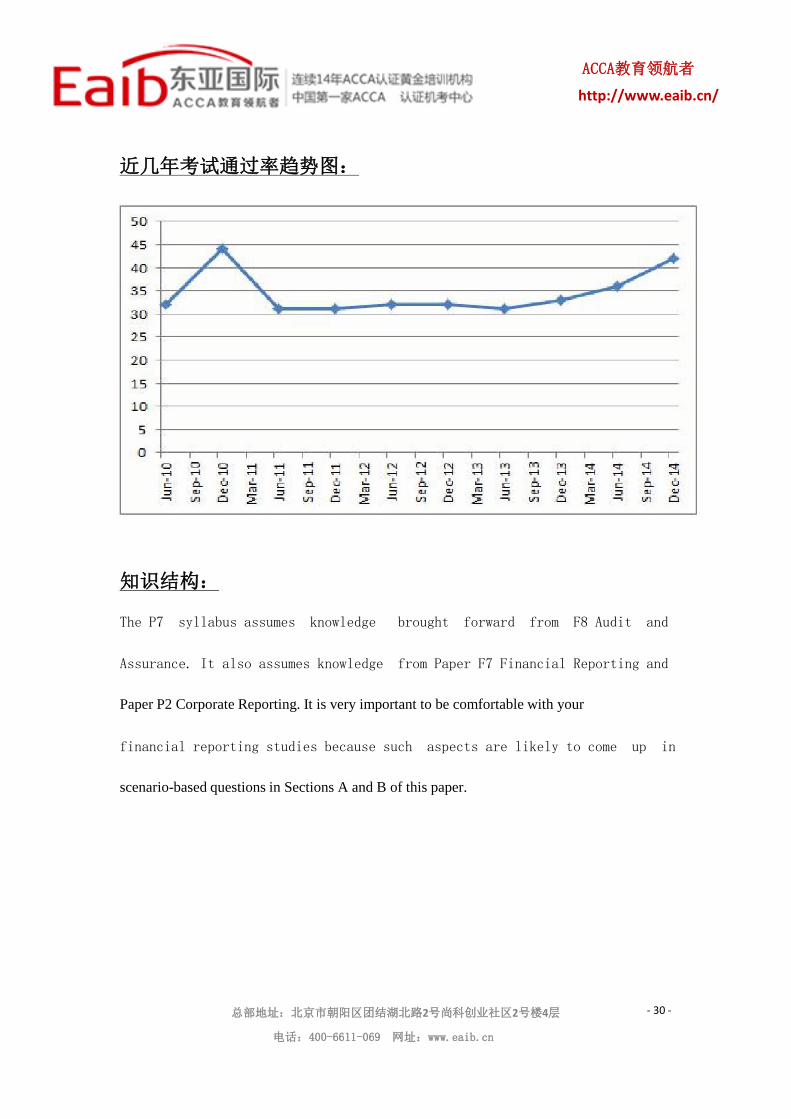

近几年考试通过率趋势图:

知识结构:

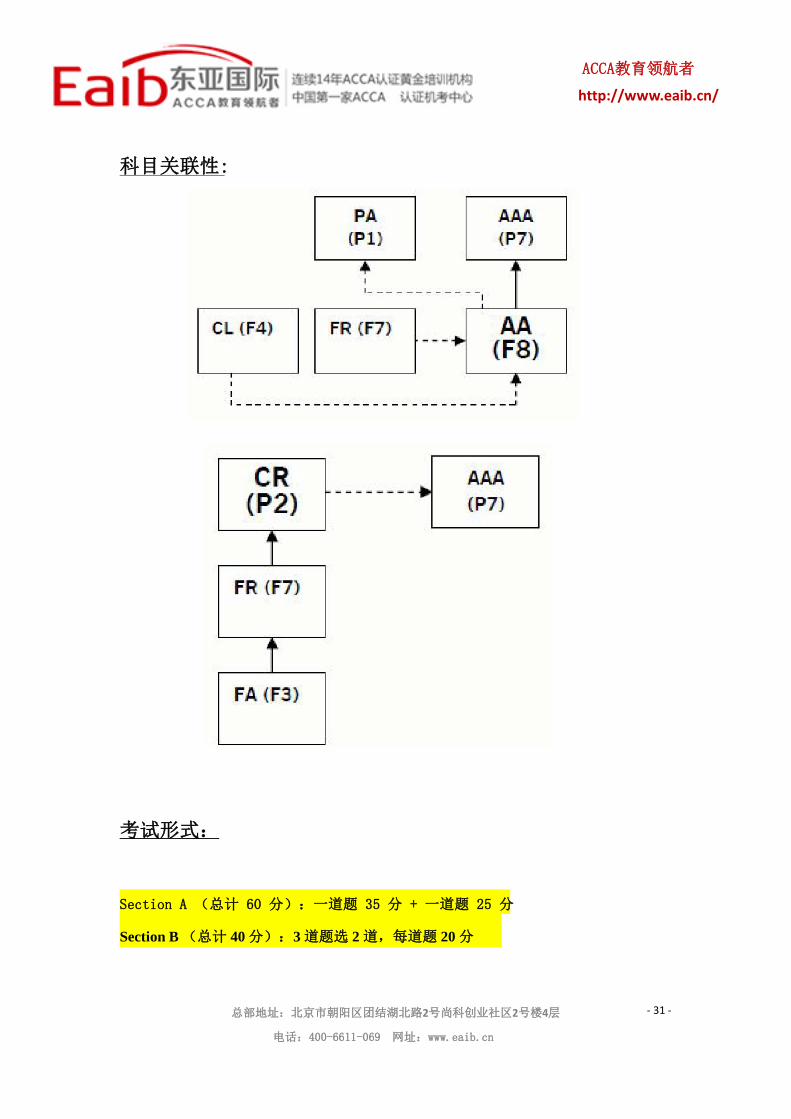

The P7 syllabus assumes knowledge brought forward from F8 Audit and

Assurance. It also assumes knowledge from Paper F7 Financial Reporting and

Paper P2 Corporate Reporting. It is very important to be comfortable with your

financial reporting studies because such aspects are likely to come up in

scenario-based questions in Sections A and B of this paper.

- 30 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

科目关联性:

考试形式:

Section A (总计 60 分):一道题 35 分 + 一道题 25 分

Section B (总计 40 分):3 道题选 2 道,每道题 20 分

- 31 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

新旧考纲的主要变化和题型列举:

2016 年 P7 考纲没有大的变化, 我们现在举两个例子来说明他的常考题型:

Q1,在 Section A 里,BOTH questions are compulsory and MUST be attempted

You are an audit manager in Davies & Co, responsible for the audit of Connolly Co,

a listed company operating in the pharmaceutical industry. You are planning the

audit of the financial statements for the year ending 31 December 2014, and the

audit partner, Ali Stone, has sent you this email:,

To: Audit manager

From: Ali Stone, Audit partner

Subject: Audit planning – Connolly Co

Hello, I would like you to start planning the audit of Connolly Co. The company’s

finance director, Maggie Ram, has sent to me this morning some key financial

information discussed at the latest board meeting. I have also provided you with

minutes of a meeting I had with Maggie last week and some background

information about the company. Using this information I would like you to prepare

briefing notes for my use in which you:

(a) Evaluate the business risks faced by Connolly Co; (11 marks)

(b) Identify and explain FOUR risks of material misstatement to be considered in

planning the audit; (8 marks)

- 32 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

(c) Recommend the principal audit procedures to be performed in respect of the

acquired‘Cold Comforts’brand name; and (5 marks) (d) Discuss the ethical issues

relevant to the audit firm, and recommend appropriate actions to be taken.

marks)

Thank you!

Background information: Connolly Co is a pharmaceutical company, developing

(7

drugs to be licensed for use around the world. Products include medicines such as

tablets and medical gels and creams. Some drugs are sold over the counter at

pharmacy stores, while others can only be prescribed for use by a doctor. Products

are heavily advertised to support the company’s brand names. In some countries

television advertising is not allowed for prescription drugs. The market is very

competitive, encouraging rapid product innovation. New products are continually

in development and improvements are made to existing formulations. Four new

drugs are in the research and development phase. Drugs have to meet very

stringent regulatory requirements prior to being licensed for production and sale.

Research and development involves human clinical trials, the results of which are

scrutinized by the licensing authorities. It is common in the industry for patents to

be acquired for new drugs and patent rights are rigorously defended, sometimes

resulting in legal action against potential infringement.

- 33 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

Minutes from Ali Stone’s meeting with Maggie Ram Connolly Co has approached

its bank to extend its borrowing facilities. An extension of $10 million is being

sought to its existing loan to support the on-going development of new drugs. Our

firm has been asked by the bank to provide a guarantee in respect of this loan

extension. In addition, the company has asked the bank to make cash of $3

million available in the event that an existing court case against the company is

successful. The court case is being brought by an individual who suffered severe

and debilitating side effects when participating in a clinical trial in 2013. In

January 2014, Connolly Co began to sell into a new market – that of animal health.

This has been very successful, and the sales of veterinary pharmaceuticals and

grooming products for livestock and pets amount to approximately 15% of total

revenue for 2014. Another success in 2014 was the acquisition of the ‘Cold

Comforts’ brand from a rival company. Products to alleviate the symptoms of

coughs and colds are sold under this brand. The brand cost $5 million and is being

amortize over an estimated useful life of 15 years. with minutes of a meeting I had

with Maggie last week and some background information about the company.

Connolly Co’s accounting and management information systems are out of date.

This is not considered to create any significant control deficiencies, but the

company would like to develop and implement new systems next year.

- 34 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

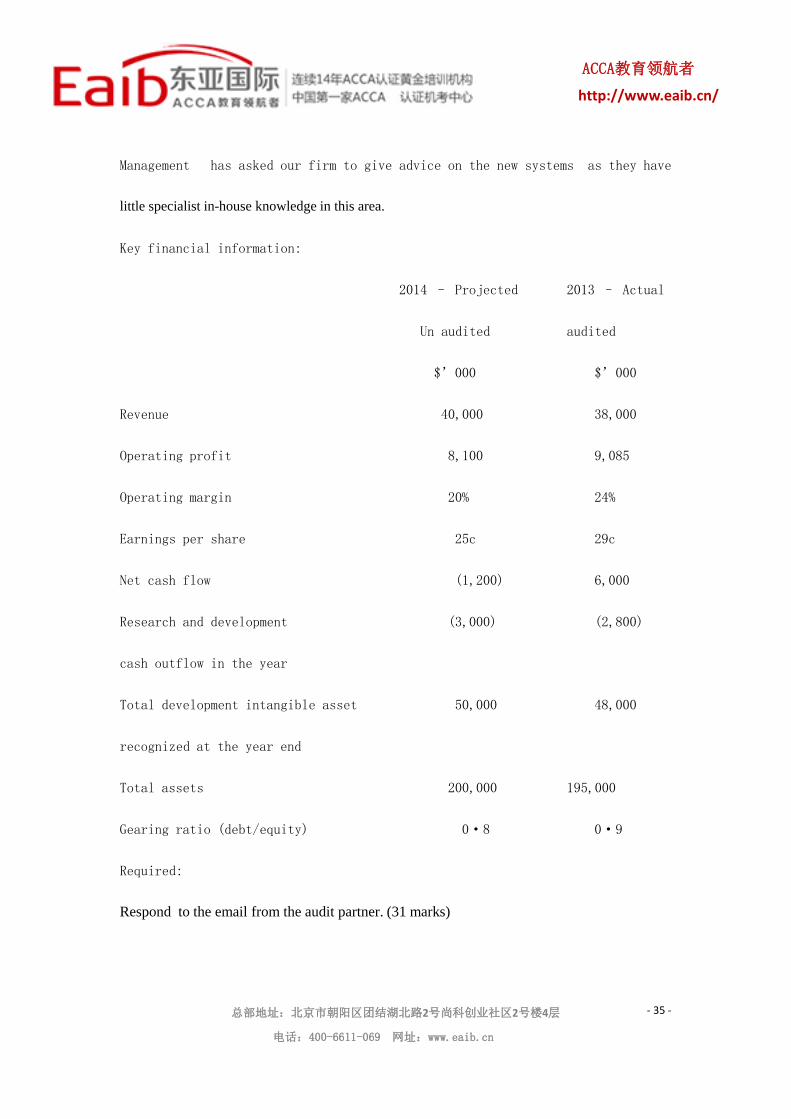

Management has asked our firm to give advice on the new systems as they have

little specialist in-house knowledge in this area.

Key financial information:

2014 – Projected

Un audited

$’000

Revenue

Operating profit

Operating margin

Earnings per share

Net cash flow

Research and development

cash outflow in the year

Total development intangible asset

recognized at the year end

Total assets

Gearing ratio (debt/equity)

Required:

200,000

0·8

195,000

0·9

50,000 48,000

40,000

8,100

20%

25c

(1,200)

(3,000)

2013 – Actual

audited

$’000

38,000

9,085

24%

29c

6,000

(2,800)

Respond to the email from the audit partner. (31 marks)

- 35 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

Professional marks will be awarded in question 1 for the presentation, clarity of

explanations and logical flow of the answer. (4 marks)

Q2 在 Section B 里, TWO questions ONLY to be attempted

(a) You are an audit manager in Weston & Co which is an international firm of

Chartered Certified Accountants with branches in many countries and which

offers a range of audit and assurance services to its clients. Your responsibilities

include reviewing ethical matters which arise with audit clients, and dealing

with approaches from prospective audit clients. The management of Jones Co

has invited Weston & Co to submit an audit proposal (tender document) for

their consideration. Jones Co was established only two years ago, but has

grown rapidly, and this will be the first year that an audit is required. In previous

years a limited assurance review was performed on its financial statements by

an unrelated audit firm. The company specialises in the recruitment of medical

personnel and some of its start up funding was raised from a venture capital

company. There are plans for the company to open branches overseas to help

recruit personnel from foreign countries. Jones Co has one full-time accountant

who uses an off-the-shelf accounting package to record transactions and to

prepare financial information. The company has a financial year ending 31

March 2015. The following comment was made by Bentley Jones, the company’

- 36 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

s founder and owner-manager, in relation to the audit proposal and potential

audit fee:‘I am looking for a firm of auditors who will give me a competitive

audit fee. I am hoping that the fee will be quite low, as I am willing to pay more

for services that I consider more beneficial to the business, such as strategic

advice. I would like the audit fee to be linked to Jones Co ’ s success in

expanding overseas as a result of the audit firm’s advice. Hopefully the audit

will not be too disruptive and I would like it completed within four months of

the year end.’

Required: (i) Explain the specific matters to be included in the audit proposal

(tender document), other than those relating to the audit fee; and (8 marks)

(ii) Assuming that Weston & Co is appointed to provide the audit service to

Jones Co, discuss the issues to be considered by the audit firm in determining a

fee for the audit including any ethical matters raised. (6 marks)

(b) Ordway Co is a long-standing audit client of your firm and is a listed

company. Bobby Wellington has acted as audit engagement partner for seven

years and understands that a new audit partner needs to be appointed to take

his place. Bobby is hoping to stay in contact with the client and act as the

engagement quality control reviewer in forthcoming audits of Ordway Co.

Required: Explain the ethical threats raised by the long association of senior

audit personnel with an audit client and the relevant safeguards to be applied,

- 37 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

and discuss whether Bobby Wellington can act as engagement quality control

reviewer in the future audits of Ordway Co. (6 marks)

(20 marks)

- 38 -

ACCA教育领航者

http://www.eaib.cn/

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

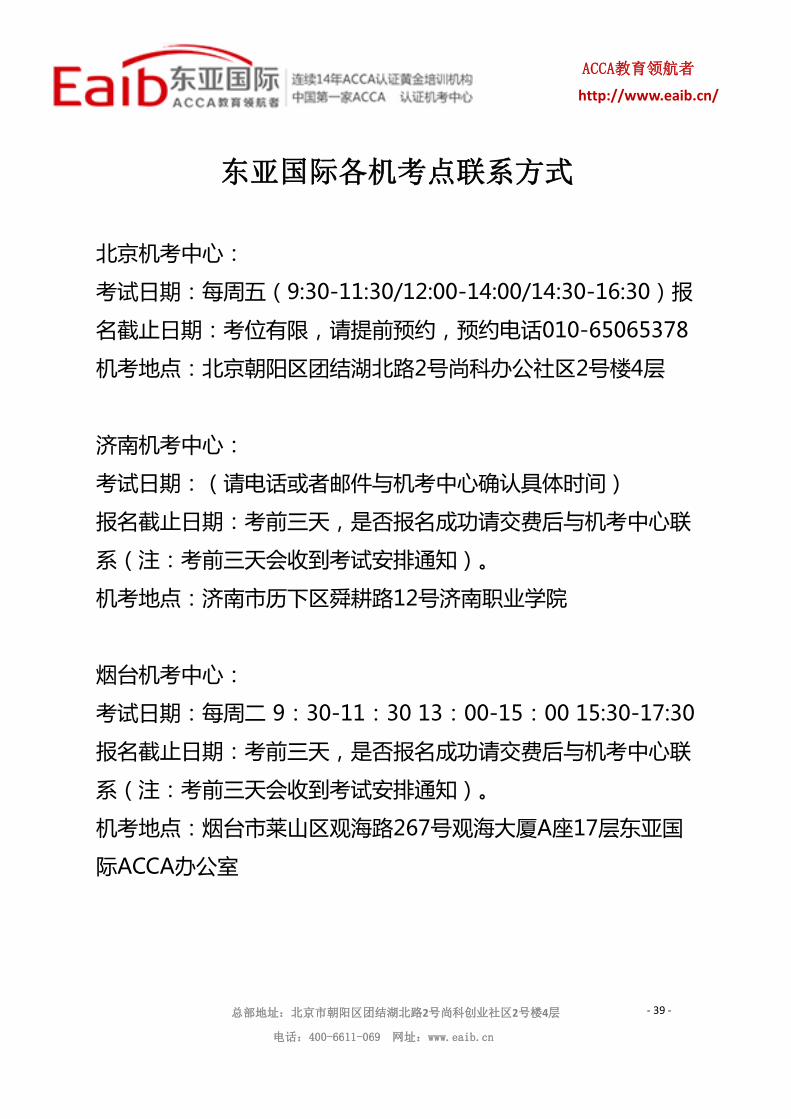

东亚国际各机考点联系方式

- 39 -

ACCA教育领航者

http://www.eaib.cn/

北京机考中心:

考试日期:每周五(9:30-11:30/12:00-14:00/14:30-16:30)报

名截止日期:考位有限,请提前预约,预约电话010-65065378

机考地点:北京朝阳区团结湖北路2号尚科办公社区2号楼4层

济南机考中心:

考试日期:(请电话或者邮件与机考中心确认具体时间)

报名截止日期:考前三天,是否报名成功请交费后与机考中心联

系(注:考前三天会收到考试安排通知)。

机考地点:济南市历下区舜耕路12号济南职业学院

烟台机考中心:

考试日期:每周二 9:30-11:30 13:00-15:00 15:30-17:30

报名截止日期:考前三天,是否报名成功请交费后与机考中心联

系(注:考前三天会收到考试安排通知)。

机考地点:烟台市莱山区观海路267号观海大厦A座17层东亚国

际ACCA办公室

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

我要机考报名

报名步骤:

1、登录东亚国际官网:http://www.eaib.cn/

- 40 -

ACCA教育领航者

http://www.eaib.cn/

点击机考报名

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

我要机考报名

报名步骤:

2、点击北京在线机考报名:

- 41 -

ACCA教育领航者

http://www.eaib.cn/

3、填写表单:

总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层

电话:400-6611-069 网址:www.eaib.cn

- 38 -

ACCA教育领航者

http://www.eaib.cn/

国际会计师培训基地 认证机考中心

连续14年认证黄金培训机构

东亚国际官网:http://www.eaib.cn/ 咨询电话:400-6611-069 总部地址:北京市朝阳区团结湖北路2号尚科创业社区2号楼4层