Embed Size (px)

Citation preview

FOREIGN TRADE UNIVERSITY

HO CHI MINH CITY CAMPUS

MID-COURSE INTERNSHIP REPORT

Major: International Business Economics

PAYMENT PROCEDURE BY LETTER

OF CREDIT FOR EXPORT CONTRACT

AT SEAFOOD JOINT-STOCK

COMPANY NO. 4

Internee: Nguyen Ngoc Dong Ha

Student ID: 1001017062

Class: K49CLC3

Supervisor: Mr. Tran Quoc Trung (MBA)

Ho Chi Minh City, July 2012

TABLE OF CONTENT

PREFACE .................................................................................................................. 1

CHAPTER 1: INTRODUCTION OF SEAFOOD JOINT-STOCK COMPANY

NO.4 ............................................................................................................................ 3

1.1. Brief history of the company............................................................................ 3

1.2. General information ......................................................................................... 4

1.3. Organizational structure ................................................................................... 6

1.3.1. Organizational hierarchy chart .................................................................. 6

1.3.2. Functions of main departments ................................................................. 7

1.4. Business outcomes from 2010 to 2012 ............................................................ 8

1.4.1. Revenues ................................................................................................... 8

1.4.2. Costs .......................................................................................................... 8

1.4.3. Pre-tax profits ............................................................................................ 9

1.4.4. Markets ...................................................................................................... 9

1.5. Roles of obtaining payment by letter of credit (L/C) in Seafood Joint-stock

Company No.4 ...................................................................................................... 10

1.6. Competitiveness of Seafood Joint-stock Company No.4 .............................. 11

CHAPTER 2: PAYMENT PROCEDURE BY LETTER OF CREDIT FOR

EXPORT CONTRACT AT SEAFOOD JOINT-STOCK COMPANY NO. 4 .. 12

2.1. Payment procedure by letter of credit for export contract

No.81DOTA/03/2013 at Seafood Joint-stock Company No. 4 ............................ 12

2.1.1. Description of export contract No.81DOTA/03/2013 ............................ 12

2.1.2. Steps performed before delivery of goods .............................................. 13

2.1.3. Description of the L/C opened for contract No.81DOTA/03/2013 ........ 16

2.1.4. Steps performed after delivery of goods ................................................. 17

2.2. Differences between the procedures in reality and in theory ......................... 19

2.3. Advantages and disadvantages of Seafood Joint-stock Company No.4 in

performing payment procedure by L/C for export contract .................................. 20

2.3.1. Advantages .............................................................................................. 20

2.3.2. Disadvantages ......................................................................................... 21

CHAPTER 3: THE OUTLOOK, ORIENTED DEVELOPMENT AND

RECOMMENDATIONS FOR PROMOTION OF PERFORMING

PAYMENT PROCEDURE BY LETTER OF CREDIT IN SEAFOOD JOINT-

STOCK COMPANY NO.4 ..................................................................................... 22

3.1. The outlook of payment by L/C for export contracts at Seafood Joint-stock

Company No.4 ...................................................................................................... 22

3.2. Oriented development of payment by L/C for export contract ...................... 23

3.3. Recommendations for promotion payment by L/C for export contract ......... 24

CONCLUSION ........................................................................................................ 25

NHẬN XÉT CỦA CƠ QUAN THỰC TẬP

Tên Doanh nghiệp/ Công ty: .....................................................................................................

Địa chỉ: .......................................................................................................................................

Mã số thuế: ................................................................................................................................

Mã số đăng ký kinh doanh/Mã số doanh nghiệp: .....................................................................

Ngành nghề kinh doanh chính: .................................................................................................

Chúng tôi xác nhận Sinh viên: ..................................................................................................

thực tập tại Doanh nghiệp/ Công ty từ ngày…… tháng….. năm……. đến ngày….

tháng…… năm…….. như sau:

- Về tinh thần thái độ:

....................................................................................................................................................

....................................................................................................................................................

- Về tiếp cận thực tế nghiệp vụ, hoạt động của doanh nghiệp/ Công ty:

....................................................................................................................................................

....................................................................................................................................................

....................................................................................................................................................

- Về số liệu sử dụng trong Thu hoạch (ghi rõ số liệu được sử dụng trong Thu hoạch có

phải do Doanh nghiệp/ Công ty cung cấp cho Sinh viên hay không):

....................................................................................................................................................

....................................................................................................................................................

....................................................................................................................................................

- Nhận xét khác:

....................................................................................................................................................

....................................................................................................................................................

....................................................................................................................................................

....................................................................................................................................................

………, ngày …… tháng …… năm ……

Ký tên

(Ghi rõ chức vụ, ký tên, đóng dấu)

SUPERVISOR’S REMARK

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

...........................................................................................................................................

LIST OF ABBREVIATIONS

B/E Bill of Exchange

B/L Bill of Lading

BIDV Bank for Development and Investment of Vietnam

C/O Certificate of Origin

E.C European Commission

EU European Union

L/C Letter of Credit

UCP 600 Uniform Customs and Practice for Documentary Credits, 2007

Revision, International Chamber of Commerce Publication No.600

LIST OF TABLES

Table 1.1. Business outcomes of Seafood Joint-stock Company No.4 from 2010 to

2012 ............................................................................................................................. 8

Table 1.2. Market Structure of Export Revenue from 2010 to 2012 ........................ 10

Table 1.3. Quantity and Value of Export Contracts paid by L/C in 2010 - 2012 ..... 10

Table 1.4. Proportion of Export Value of Seafood Joint-Stock Company No.4 to the

industry ...................................................................................................................... 11

LIST OF FIGURES

Figure 1.1. Organizational structure of Seafood Joint-stock Company No.4 ............. 6

Figure 1.2. Proportions of Costs and Pre-tax Profits to Revenues from 2010 to 2012

..................................................................................................................................... 9

Figure 2.1. Payment procedures for export contract in Seafood Joint-stock Company

No.4 ........................................................................................................................... 13

Figure 3.1. Proportions in number and value of export contracts paid by L/C in

Seafood Joint-stock Company No.4 in 2010 to 2012 ............................................... 22

1

PREFACE

In recent years, especially after the accession to World Trade Organization of

Vietnam in 2007, export of seafood has been increasing in scale and value. In 2012,

seafood export had reached 6,09 billion USD, which accounted for 5,3% of the total

export turnover of our country. With its high and stable increasing export turnover

lately, seafood has become a promising export commodity which would contribute

considerable turnover to the national export in the future.

Seafood Joint Stock Company No.4 was established in 1980 and operated as a

joint-stock company from 2001. Exporting is the main business activity and the

company has got a certain position in the industry. In the export procedure,

obtaining payment is a very important step as it relates to the turnover of export,

financial status of the company. On the other hand, international payment is a

difficult and complicated procedure, especially payment by Letter of Credit. To all

exporters in general and to Seafood Company No.4 in particular, it is essential to

perform precisely and timely all activities, from preparing goods to applying for

necessary documents and shipping goods.

Fortunately, during my internship period at Seafood Joint-stock Company

No.4, I had had the opportunity to observe and learn about the payment procedure

in reality. Therefore, I had chosen the topic of “Payment Procedure by Letter of

Credit for Export Contract at Seafood Joint-Stock Company No. 4” for my

mid-course internship report. The purpose of this report is to provide a brief

analysis of the business situation and the position of Seafood Joint-stock Company

No.4, a clear description of the procedure of obtaining payment for export contracts

at the company and some recommendations to improve the activity in the future.

My report includes 3 chapters:

Chapter 1: Introduction of Seafood Joint-stock Company No.4

Chapter 2: Payment procedure by Letter of Credit for export contract at

Seafood Joint-stock Company No.4

Chapter 3: The outlook, oriented development and recommendations for

promotion of performing payment procedure by Letter of Credit in Seafood Joint-

stock Company No.4

2

I would like to give my deepest gratitude to Foreign Trade University for

giving me an opportunity to learn more about international payment activities in

reality. In addition, I would like to give my sincere thanks to Seafood Joint-stock

Company No.4 for creating favorable conditions for my internship period at the

company and especially Planning Department for their dedicated guidance during

my internship period. Finally, I would like to express my heartfelt appreciation to

Mr. Tran Quoc Trung for his careful instructions and valuable comments to help me

complete my report.

I have tried my best to study the subject and complete the report in the given

time. However, due to limited time, knowledge and experience, there are still a lot

of shortcomings and limitations in this report. Thus, I would be grateful to receive

feedbacks and comments for improvement in the future.

Ho Chi Minh City, July 2013

Nguyen Ngoc Dong Ha

3

CHAPTER 1: INTRODUCTION OF SEAFOOD JOINT-STOCK COMPANY

NO.4

1.1. Brief history of the company

Seafood Joint-stock Company No.4 was established from two private seafood

factories, Thai Binh Seafood Factory and Tan Nam Hai Seafood Factory. After the

country’s reunification in 1975, Ho Chi Minh City People’s Committee issued a

decision nationalizing two factories mentioned above. They became Seafood

Processing State-owned Factory No.8 and No.9.

On December 08, 1979, the Ministry of Seafood issued decision No. 1275/QD

merging two factories into Frozen Seafood Factory 4. On March 31, 1993, the

Ministry of Seafood issued decision No. 249 TS/QD-TC in which the factory was

given the right to use and the responsibility to reserve and develop its capital.

In 1995, the factory was renamed Seafood Processing Import – Export

Company No.4 according to decision No.60-TS/QD issued by Ministry of Seafood.

Following the economic innovation policy of the government, the company had

been promoting creativity and dynamism in business, raising its position in the

market and accumulating internal strength.

In 2001, the Prime Minister signed Decision No.09/2001/QDT.Tg of

transforming Seafood Processing Import – Export Company No.4 into Seafood

Joint-stock Company No.4 with the charter capital of 15.000.000.000 VND. The

company officially came into operation as a joint-stock company on June 1, 2001

with the Certificate of Business Registration No. 4103000436 issued by Ho Chi

Minh City Department of Planning and Investment on May 31, 2001.

In the attempt to diversify products, increase product value and export

revenue, in 2005, the company invested in building a high quality processing

factory at Tac Cau fishing port, Chau Thanh, Kien Giang. With the total investment

of 30 billion VND, the factory had the capacity of 4.000 tons of finished product per

year and came into operation in April, 2006. In 2007, the company proceeded to

construct a factory processing tra and basa fish and crayfish at Thanh Binh

Industrial Zone, Dong Thap with the total investment of 190 billion VND. The

4

factory started operations in 2009 with the designed capacity of 20.000 tons of

finished product per year.

The company also invested in constructing a building named ORIENT

APARTMENT for office combined with apartments at 331 Ben Van Don, Ward 1,

District 4, Ho Chi Minh City. The building has 17 floors with the total floor area of

22.000 m2 and the total investment of 240 billion VND.

With more than 30-year experience in business and processing frozen seafood,

Seafood Joint-stock Company No.4 has been able to produce high quality products

while building long-term relationships with strategic partners worldwide. By

promoting cultivation activities at Dong Tam branch in recent years, the company

has ensured part of its fresh water fish supplies while reducing costs. In the near

future, when the economy has positive changes, the company will be able to invest

more in aquaculture to create its own supplies and expand its foreign market. With

well-prepared development plans, Seafood Joint-stock Company No.4 will enhance

its prestige and strengthen its competitiveness in the industry.

1.2. General information

- Vietnamese name: Công ty Cổ phần Thủy sản Số 4

- International name: Seafood Joint-Stock Company No.4

- Headquarter: 320 Hung Phu Street, Ward 9, District 8, Ho Chi Minh City

- Tel: 08.39543361 – 39543363

- Fax: 08.39543362 - 39543367

- Website: http://www.seafoodno4.com/

- Email: [email protected]

- Logo:

- Factories:

+ At Ho Chi Minh City:

Address: 320 Hung Phu Street, Ward 9, District 8, Ho Chi Minh City

Area: 3.000 m2

5

+ At Kien Giang:

Address: Tac Cau fishing port, Chau Thanh, Kien Giang

Area: 8.000 m2

+ At Dong Thap:

Address: Binh Thanh Industrial Zone, Thanh Binh, Dong Thap

Area: 30.000 m2 and 60 hectares of Pangasius Hypophthalmus

(tra fish) aquaculture

Seafood Joint-stock Company No.4 also hold dominant share (98% of the 60

billion VND total investment of the project) of Toan Thang Joint-stock Company

in Long Hau Industrial Zone, Can Giuoc, Long An.

- Main business activities:

According to Certificate of business registration No.4103000436 issued by Ho

Chi Minh City Department of Planning and Investment on May 31, 2001 and

amended the eighth time on June 22, 2011, Seafood Joint-stock Company No.4 is

allowed to perform following businesses:

+ Processing aquaculture, agriculture and animal husbandry products

+ Maintaining, repairing refrigeration electrical equipment

+ Leasing office; real estate

+ Producing garments (except bleaching, dyeing, starching, printing)

+ Exporting, importing aquaculture products, agriculture products (except rice,

cane sugar, beet sugar), animal husbandry products and types of merchandises,

materials, equipment, technology for production and trading, garments; import

and export rights of above-mentioned merchandises

+ Growing freshwater aquaculture species (not at the headquarter)

+ Producing cattle feed, poultry feed and aquaculture feed (except processing

fresh feed)

+ Selling feed or ingredients to produce cattle feed, poultry feed or aquaculture

feed

6

1.3. Organizational structure

1.3.1. Organizational hierarchy chart

Figure 1.1. Organizational structure of Seafood Joint-stock Company No.4

General Assembly of

Shareholders

Board of Directors

Board of

Supervisors

Director General

Director of

Dong Tam

BranchDeputy

Director

General of

Interior

Technical

Deputy

Director

General

Deputy

Director

General of

Import &

Export

Director of

Kien Giang

Branch

Refrigeration

Electrical

Engineering

Department

Administration

& Human

Resource

Department

Planning

Department

Financial &

Accounting

Department

Quality

Control

Department

Factory

Deputy Director

of Production

Deputy Director

of Sales

Cultivation

Department

Factory

Quality Control

DepartmentSales Department

Accounting

Department

Market Research

Department

Deputy Director

of Production

Deputy Director

of Sales

Cultivation

Department

Factory

Quality Control

DepartmentSales Department

Accounting

Department

Market Research

Department

(Source: Administration & Human Resource Department

of Seafood Joint-Stock Company No.4)

7

1.3.2. Functions of main departments

- General Assembly of Shareholders: According to the Enterprise Law and the

Articles, this is the highest body of the company. General Assembly of

Shareholders has the responsibilities of discussing and approving long-term and

short-term development policies of the company; deciding capital structure;

electing other bodies to manage and control production and business activities of

the company.

- Board of Management: As the managing body, the Board of Management can

act on behalf of the company to decide all issues related to the purpose, rights

and activity of the company, except for those within the authority of General

Assembly of Shareholders that are not delegated. Board of Management is

responsible for setting up business plan, giving measures and decisions to

achieve targets set by the General Assembly of Shareholders. Currently, the

Board of Management includes 5 members working on a 5-year term.

- Board of Supervisors: This is the body directly under General Assembly of

Shareholders, elected by General Assembly of Shareholders. Currently the Board

of Supervisors consists of 3 members working on a 5-year term. The Board of

Supervisors has the authority and responsibilities to oversee the reasonableness

and legality of the business management and financial statements of the

company.

- Board of Directors: This is the body governing all business activities of the

company. Director General is most responsible to General Assembly of

Shareholders, Board of Management and before the law for all business

activities. Assisting the Director General are 3 Deputy Director Generals.

- Planning department: This is one of the most important departments in the

company. Planning department is in charge of organizing domestic business and

import - export activities; setting up and implementing business plans;

developing sales policy.

- Other departments: Other departments perform their functional activities to

ensure effective and efficient control, management and administration of

business activities.

8

1.4. Business outcomes from 2010 to 2012

Table 1.1. Business outcomes of Seafood Joint-stock Company No.4

from 2010 to 2012

(Unit: million VND)

2010 2011 2012

Revenue 380.446 649.071 598.218

Costs 339.974 613.532 578.383

Pre-tax profit 40.472 35.539 19.835

(Source: Financial statements in 2010, 2011 and 2012

of Seafood Joint-stock Company No.4)

1.4.1. Revenues

From Table 1.1 above, it can be seen that in 2011, revenue had increased

dramatically from 380.446 million VND to 749.071 million VND, which means it

had rose by more than 70%. The growth in revenue resulted from the increased

demand of seafood of the world in recent years and the rise in export price due to

inflation of the world economy. However, in 2012, revenue had decreased by

50.853 million VND, equaling a 7,83% drop compared to that of 2011 due to the

economic slump. Nevertheless, in the context of economic downturn which led to

the bankruptcy of many companies in the industry, the decline was not highly

significant.

1.4.2. Costs

Costs increased with revenues. In 2011, cost had risen to 613.532 million

VND, which is a dramatic increase of 80,46% compared to 339.974 million VND in

2010. In 2012, as revenue decreased, cost also decreased by 35.149 million VND,

reaching 578.383 million VND at the end of the year. Figure 1.2 shows that the

proportions of costs to revenues had increased from 89,36% in 2010 to 96,68% in

2012. The huge relative volume of costs compared to revenues in respective years

resulted from several reasons: scarce supplies, soaring input prices, unfavorable

weather which led to diseases on fish, shrimp,... and trade and technical barriers in

importers’ countries...

9

Figure 1.2. Proportions of Costs and Pre-tax Profits to Revenues

from 2010 to 2012

(Source: Financial statements in 2010, 2011 and 2012

of Seafood Joint-stock Company No.4)

1.4.3. Pre-tax profits

From 2010 to 2012, pre-tax profits had declined dramatically. In 2010, the

company got 40.472 million VND of pre-tax profit, accounting for 10,64% of

revenue. However, in 2011, profit had decreased by 4.933 million VND, to 35.539

million VND. More significantly, in 2012, profit had declined by 15.704 million

VND, equaled only 55,81% of profit in 2011. In 2012, profit only equaled 3,32% of

revenue, representing ineffective business activities. The remarkable decrease in

profits from 2010 to 2012 resulted from many sources. Apart from some reasons

mentioned in section 1.4.2 above, fierce competition with other exporters in the

industry also prevented the company from raising its output prices, which finally

resulted in low revenues, small profits and decreased proportions of pre-tax profits

to revenues in 2011 and 2012.

1.4.4. Markets

In recent years, Seafood Joint-stock Company No.4 has been exporting to

more than 25 countries around the world. Strategic markets are: EU, USA, Japan,

Thailand, Australia, South Korea, Malaysia,... Table 1.2 shows that 3 main markets

of the company in recent years are EU, Japan and Thailand. It is noteworthy that

exports to EU in 2011 and 2012 had accounted for about half of export revenues of

the company. This is proof that products of the company have high quality,

89,36% 94,52% 96,68%

10,64% 5,48% 3,32%

0%

20%

40%

60%

80%

100%

2010 2011 2012

Pre-tax profit

Costs

10

satisfying strict requirements of EU, Japan... Although USA is a potential market,

exports to this market only accounted for a small percentage of total export revenue

due to problems related to antidumping laws applied on seafood. In the future, the

company is going to strengthen the relationships with current partners while trying

to reach new customers all over the world.

Table 1.2. Market Structure of Export Revenue from 2010 to 2012

2010 2011 2012

USA 7,1% 5,9% 3,4%

Japan 36,6% 10,6% 11,9%

Thailand 13,9% 9,1% 17,8%

Australia 6,0% 3,7% 5,5%

EU 18,7% 53,2% 41,7%

Middle East 14,5% 9,8% 3,9%

Other 3,2% 7,7% 15,8%

(Source: Reports of Board of Supervisors in 2010, 2011 and 2012

of Seafood Joint-stock Company No.4)

1.5. Roles of obtaining payment by letter of credit (L/C) in Seafood Joint-

stock Company No.4

Table 1.3. Quantity and Value of Export Contracts paid by L/C in 2010 - 2012

2010 2011 2012

Number of contracts paid by L/C 19 50 62

Total number of contracts 124 317 306

Proportion 15,32% 15,77% 20,26%

Value of contracts paid by L/C (USD) 789860 2774257 2507781

Total value contract (USD) 13100000 25400000 22238000

Proportion 6,03% 10,92% 11,28%

(Source: Reports of Board of Supervisor in 2010, 2011 and 2012

of Seafood Joint-stock Company No.4)

Normally, documentary credit is considered the most preferred payment

method for exporters because it provides a safe way of getting paid for delivered

goods. In Seafood Joint-stock Company No.4, in the 2010 – 2012 period, 15% to

11

20% of the total number of export contracts were paid by L/C (Table 1.3). These

contracts constituted from 6% to more than 11% of the total export value. It can be

seen that both quantity and value of export contracts paid by L/C increased from

2010 to 2012. These contracts not only guarantee payment for delivered goods but

also provide cash shortly after delivery because these L/C are usually negotiated

before maturity. In the current economic situation, when most enterprises are short

of working capital, getting cash is very important to ensure continuous business

activities of the company. Although contracts paid by L/C accounted for only more

than 11% of the total value in 2012, they offered assured source of money to

maintain business and purchase supplies to execute other contracts.

1.6. Competitiveness of Seafood Joint-stock Company No.4

Table 1.4. Proportion of Export Value of Seafood Joint-Stock Company No.4

to the industry

2010 2011 2012

Company’s export value (million USD) 13,1 25,4 22,238

Total export value of the industry (million USD) 5034 6110 6090

Proportion 0,26% 0,42% 0,37%

(Source: Reports of Board of Supervisor of Seafood Joint-stock Company No.4 and

reports of Vietnam Customs in 2010, 2011 and 2012 )

Seafood Joint-stock Company No.4 has not been one of the top seafood

exporters, its export value only constituted less than 1% of the industry total value.

However, the proportion has been increasing, showing the prospect that the

company will elevate its position in the industry in the future. More importantly,

due to unfavorable economic situation, 30% of businesses in the industry couldn’t

export in the first quarter of 2012 and some enterprises even went bankruptcy in the

same year. Despite that, exporting activities at Seafood Joint-stock Company No.4

were still stable. At the end of the year, the company still generated profit. It is a

good sign that the company has built a strong and sufficient network of customers,

gained considerable prestige and got a certain position within the industry.

12

CHAPTER 2: PAYMENT PROCEDURE BY LETTER OF CREDIT FOR

EXPORT CONTRACT AT SEAFOOD JOINT-STOCK COMPANY NO. 4

2.1. Payment procedure by letter of credit for export contract

No.81DOTA/03/2013 at Seafood Joint-stock Company No. 4

2.1.1. Description of export contract No.81DOTA/03/2013

Contract No.81DOTA/03/2013 was in form of a purchase confirmation issued

by the importer, Solea International on March 12, 2013 and confirmed by Seafood

Joint-stock Company No.4.

- Exporter: Seafood Joint-stock Company No.4, Vietnam

- Importer: Solea International, Belgium

- Commodity: Raw Farmed skinless, boneless Pangasius

- Contract value: 47.520,00 USD

- Shipment: Shipment not later than March 29, 2013

- Payment terms: L/C 45 days after B/L date

- Delivery terms: CFR Antwerp (Kallo), Belgium

It can be seen that not only the purchase confirmation but also the payment

term are brief. Solea International is a regular partner of Seafood Joint-stock

Company No.4 in recent years. Thus, two companies are familiar with each other as

well as the terms and conditions and a detailed contract was not necessary but a

brief purchase confirmation. Payment by L/C has been the method chosen by Solea

International for all contracts and the two parties have been accustomed to the

transaction. Therefore, it was not compulsory to have detailed payment terms as

both parties have agreed on all terms and conditions to be included in the L/C.

As usual, Solea International would apply for an irrevocable, 45 day at sight

L/C at BNP Paribas Fortis (Fortis Bank) in the favor of Seafood Joint-stock

Company No.4, and advise through Bank of Investment and Development of

Vietnam (BIDV). Details of the L/C shall be described in section 2.1.3.

Operations to obtain payment for this contract as well as other export contracts

are performed by staff in Planning Department. The procedure for this contract is

shown in Figure 2.1.

13

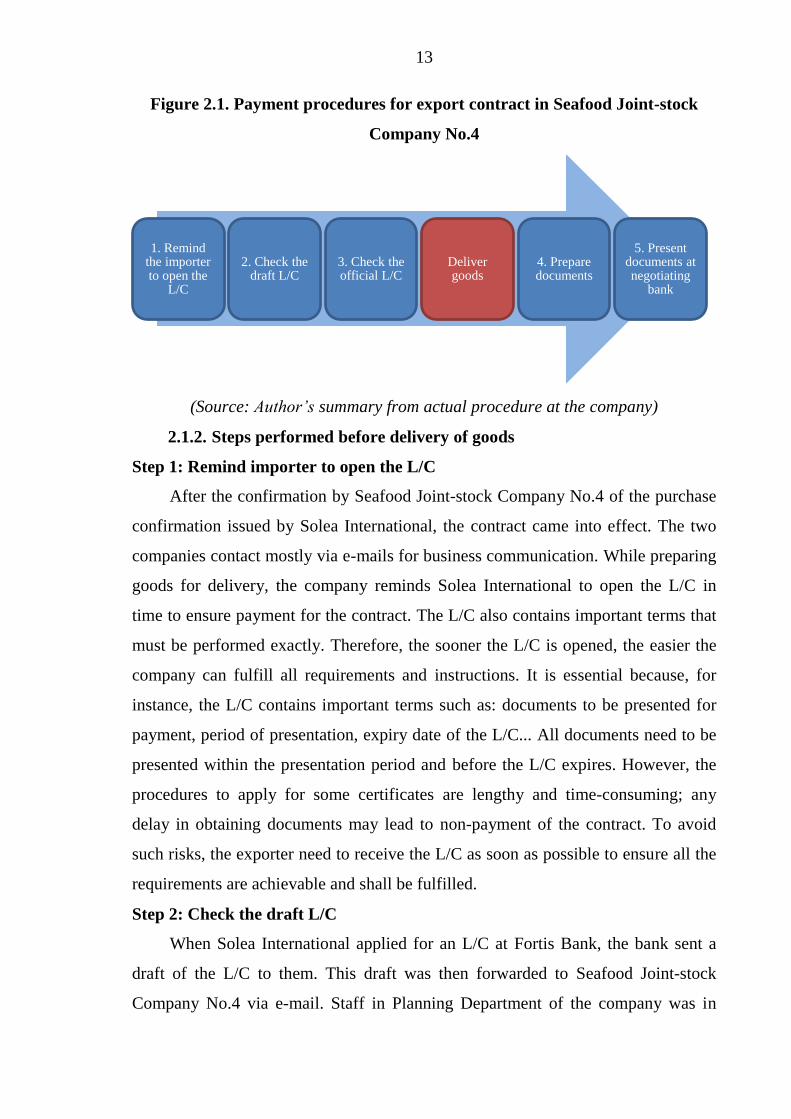

Figure 2.1. Payment procedures for export contract in Seafood Joint-stock

Company No.4

(Source: Author’s summary from actual procedure at the company)

2.1.2. Steps performed before delivery of goods

Step 1: Remind importer to open the L/C

After the confirmation by Seafood Joint-stock Company No.4 of the purchase

confirmation issued by Solea International, the contract came into effect. The two

companies contact mostly via e-mails for business communication. While preparing

goods for delivery, the company reminds Solea International to open the L/C in

time to ensure payment for the contract. The L/C also contains important terms that

must be performed exactly. Therefore, the sooner the L/C is opened, the easier the

company can fulfill all requirements and instructions. It is essential because, for

instance, the L/C contains important terms such as: documents to be presented for

payment, period of presentation, expiry date of the L/C... All documents need to be

presented within the presentation period and before the L/C expires. However, the

procedures to apply for some certificates are lengthy and time-consuming; any

delay in obtaining documents may lead to non-payment of the contract. To avoid

such risks, the exporter need to receive the L/C as soon as possible to ensure all the

requirements are achievable and shall be fulfilled.

Step 2: Check the draft L/C

When Solea International applied for an L/C at Fortis Bank, the bank sent a

draft of the L/C to them. This draft was then forwarded to Seafood Joint-stock

Company No.4 via e-mail. Staff in Planning Department of the company was in

1. Remind the importer to open the

L/C

2. Check the draft L/C

3. Check the official L/C

Deliver goods

4. Prepare documents

5. Present documents at negotiating

bank

14

charge of checking the draft L/C. This step is very important as the company can

check and amend all the details without banking charges. (Normally, all amendment

fees are for the Beneficiary’s account). For contract No.81DOTA/03/2013, the

company asked Solea International to extend the period of delivery one more week,

until April 05, 2013. The request was sent back to Solea International and was

accepted. All other terms and conditions of the L/C were agreed. Solea International

then opened the official L/C at Fortis Bank.

Step 3: Check the official L/C

The L/C was issued by Fortis Bank through SWIFT MT700 with terms and

conditions recorded in fields and sent to advising bank, BIDV Saigon Branch on

April 03, 2013. BIDV Saigon Branch then notified Seafood Joint-stock Company

No.4 that the L/C had been opened. On April 04, 2013, the company checked the

L/C. Although the draft L/C had been checked, the official one must not be

overlooked. Checking various sections carefully would reduce discrepancies,

related unplanned costs; and the risk of losing the secured payment. Important

details that need to be checked carefully include:

- L/C header under “Received from”: Issuing bank should be a prestige bank. If

not, check whether the L/C is confirmed by another bank (Field 49)

- Field 40A: Form of Documentary Credit: The L/C should be irrevocable to

secure payment for the company as it is cannot be cancelled or amended unless

all parties agree. If it isn’t stated, the L/C is irrevocable as regulated in UCP 600.

- Field 31D: Date and Place of Expiry: All documents must be presented by the

expiry date; if not, the L/C shall be null and void. The company must consider all

the time needed to perform various activities: production and packing, shipment,

time to obtain certificates, etc. Place of expiry in Beneficiary’s country shall be

an advantage.

- Field 50: Applicant and Field 59: Beneficiary: The name and address of the

Applicant and the Beneficiary (the company) must be spelled correctly to avoid

the risk of losing payment. If the name or address of the company is not correct

then even if all terms and conditions are fulfilled, the Issuing bank may not agree

to settle payment.

15

- Field 32B: Currency Code, Amount and 39A: Percentage Credit Amount

Tolerance: Check the amount and currency of L/C. Also, a tolerance amount

would give flexibility to the company during the preparation of goods.

- Field 41D: Available With...by: A freely negotiable L/C shall give advantage to

the exporter (to be explained later in section 2.1.3).

- Field 42C: Draft at...: The payment terms should be in accordance with the

contract.

- Field 44C: Latest date of shipment: The goods must be shipped on time. For

this L/C, the delivery period had been extended one more week from the date

stipulated in the contract based on the company’s request.

- Field 45A: Description of Goods: The unit price, weight, quantities, and other

requirements on goods must be met. Since the customer is in EU, where rules

and regulations on seafood products are very strict, this matter should be handled

carefully. The delivery terms should be in accordance with the contract.

- Field 46A: Documents required: All the documents listed in this field must be

obtained with the correct number of copies, information, title and the party issued

the documents. Furthermore, all the documents should be consistent. The

company must also check for any restrictions. For example, in this contract,

forwarder bill of lading is not acceptable.

- Field 71B: Charges: Only bank charges the company agreed to pay should be

stated to be for the company’s account.

- Field 48: Period of Presentation: The documents not only need preparing

exactly but also have to be presented within the stipulated period.

- Other terms and conditions are checked carefully as well.

If the company finds any the terms and conditions of the L/C unsatisfactory,

they must ask the Importer to instruct Issuing bank to make amendments (Normally,

amendment charges will be for the Beneficiary’s account, which means Seafood

Joint-stock Company No.4 have to pay). Because two parties have conducted

businesses many times in the past and the company had checked the draft, rarely did

they have to amend the official L/C. Thus, the company could save money on this.

16

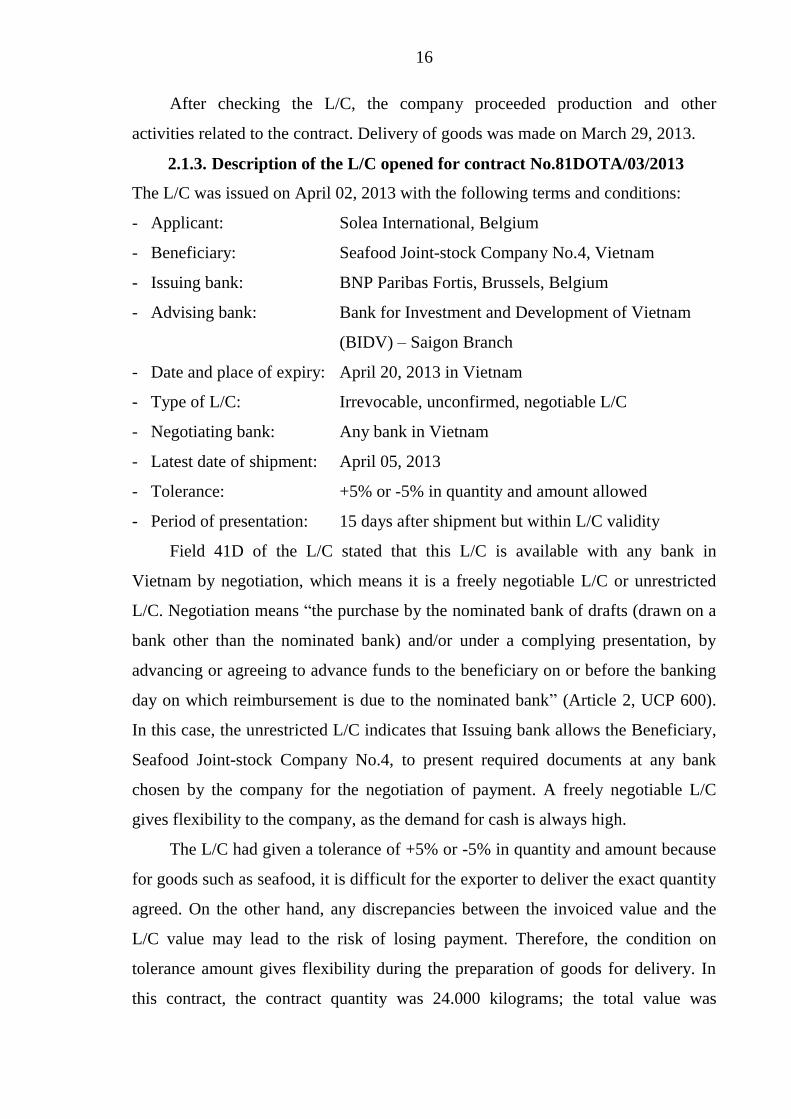

After checking the L/C, the company proceeded production and other

activities related to the contract. Delivery of goods was made on March 29, 2013.

2.1.3. Description of the L/C opened for contract No.81DOTA/03/2013

The L/C was issued on April 02, 2013 with the following terms and conditions:

- Applicant: Solea International, Belgium

- Beneficiary: Seafood Joint-stock Company No.4, Vietnam

- Issuing bank: BNP Paribas Fortis, Brussels, Belgium

- Advising bank: Bank for Investment and Development of Vietnam

(BIDV) – Saigon Branch

- Date and place of expiry: April 20, 2013 in Vietnam

- Type of L/C: Irrevocable, unconfirmed, negotiable L/C

- Negotiating bank: Any bank in Vietnam

- Latest date of shipment: April 05, 2013

- Tolerance: +5% or -5% in quantity and amount allowed

- Period of presentation: 15 days after shipment but within L/C validity

Field 41D of the L/C stated that this L/C is available with any bank in

Vietnam by negotiation, which means it is a freely negotiable L/C or unrestricted

L/C. Negotiation means “the purchase by the nominated bank of drafts (drawn on a

bank other than the nominated bank) and/or under a complying presentation, by

advancing or agreeing to advance funds to the beneficiary on or before the banking

day on which reimbursement is due to the nominated bank” (Article 2, UCP 600).

In this case, the unrestricted L/C indicates that Issuing bank allows the Beneficiary,

Seafood Joint-stock Company No.4, to present required documents at any bank

chosen by the company for the negotiation of payment. A freely negotiable L/C

gives flexibility to the company, as the demand for cash is always high.

The L/C had given a tolerance of +5% or -5% in quantity and amount because

for goods such as seafood, it is difficult for the exporter to deliver the exact quantity

agreed. On the other hand, any discrepancies between the invoiced value and the

L/C value may lead to the risk of losing payment. Therefore, the condition on

tolerance amount gives flexibility during the preparation of goods for delivery. In

this contract, the contract quantity was 24.000 kilograms; the total value was

17

47.520,00 USD. With a tolerance of +5% or -5%, the company could deliver from

22.800 to 25.200 kilograms with the real value ranged from 45.144 USD to 49.896

USD. For this contract, the company decided to deliver 23.300 kilograms of

Pangasius for the amount of 46.134 USD.

Solea International is a company in Belgium, EU, where rules and regulations

are very strict, from quality of goods to documents. The L/C not only required the

company to issue a Beneficiary’s Declaration stating: “If the goods are rejected for

any reason by the E.C. customs health authorities [...] or an independent

laboratory”, Beneficiary (the company) “will pay back the full invoice value and

other related costs cause by the rejection and allow the return of the container...”

(Field 46A) but also stated that in such case, the L/C “will be cancelled

automatically”. Therefore, not only Planning Department but all departments

needed to cooperate closely to ensure that the goods’ quality and documents would

meet the requirements from the importer and their bank.

2.1.4. Steps performed after delivery of goods

Step 4: Prepare documents necessary for payment

The process of preparing documents to obtain payment actually started before

delivery of goods. Field 46A of the L/C has stated all documents required. These

documents can be divided into 4 groups:

- Goods-related documents:

+ Commercial Invoice, Packing List/Weight Note, Traceability Code List: these

documents are issued by the company in the name of the Applicant- Solea

International. The commercial invoice is used to ask for payment of the goods, its

content must include descriptions of the goods, unit price, total value, delivery

terms, marking, container number and seal number and other details as stipulated in

the L/C. Normally the commercial invoice needn’t be signed. However, for this

contract, the L/C required the original and 3 copies of signed commercial invoice.

+ The Packing list must show information about packing of the goods, including:

quantity per bag, packing materials, marks, number of packages, weight of empty

bag, rider and master carton, etc. One original and 2 copies of packing list must be

submitted to the bank.

18

+ The Traceability Code List is a document on details about the code stamped on

the bottom of the cartons. Its main purpose is to facilitate the process of checking

products of the importer. The Traceability Code List must contain code number,

number of cartons carrying the same traceability code and other information about

the product and shipment.

Besides, the company needed to provide copy of printing of the master cartons and

riders.

+ Certificate of Origin (C/O): This is a document stated the origin of the goods,

signed and confirmed by Chamber of Commerce and Industry of Vietnam. Because

the consignment was exported to EU, Form A of C/O was used to confirm origin of

goods from developing country (Vietnam) to developed country (Belgium, EU) to

enjoy preferential taxes under Generalized System of Preference (GSP). Documents

needed to apply for C/O include: registration form, Form A of C/O, commercial

invoice, Customs Declaration, Packing List, B/L and other documents to prove the

origin of goods. Because the C/O was issued on April 03, 2013, later than B/L date

(March 29, 2013), it mentioned “Issue Retrospectively” in Box 4.

+ Health Certificate, Chemical Analysis Certificate and Microbiology Analysis

Certificate: These certificates must be issued by National Agro-Forestry-Fisheries

Quality Assurance Department (NAFIQAD) of Ministry of Agriculture and Rural

Development in Vietnam. The export seafood must be inspected before delivery to

ensure that they are in conformity with export standards, free from types of

antibiotics, bacteria stated in the L/C and fit for human consumption.

- Shipping document:

+ Bill of Lading (B/L): this is an essential document as it is the proof of delivery of

goods on board the vessel and it is an evidence of the contract of carriage.

Furthermore, it is the document of title of the goods delivered. B/L must contain all

information required in the L/C.

- Financial document:

+ Bill of exchange (B/E): This is an unconditional order to ask for payment drawn

by Seafood Joint-stock Company No.4 on Fortis Bank. This document is not

19

required in the L/C. However, Seafood Joint-stock Company must issue B/E asking

Fortis Bank to pay to the order of negotiating bank (BIDV Saigon branch).

- Other document: Beneficiary’s Attestation and Beneficiary’s Declaration: these

documents are required to guarantee that all requirements of the importer have

been fulfilled and the exporter would be responsible if the consignment is

rejected by E.C customs.

Step 5: Present required documents at negotiating bank to obtain payment

After delivery of goods and preparation of documents, Seafood Joint-stock

Company No.4 present documents at BIDV Saigon Branch for negotiation of

payment. Besides documents as required in the L/C, the company needed to submit

a request for negotiation, the L/C and B/E. BIDV Saigon Branch would finance

through negotiation with recourse by buying back the B/E and the export documents

under L/C before maturity and paying the company a sum of money to receive right

of claim from the draft. For this contract, Issuing bank would settle payment after

45 days from B/L date, so the discount rate was 90% of the invoice value, which

equals 41.520 USD. (For at sight L/C, the discount rate would be 95%). After

checking the documents, BIDV Saigon Branch would credit the amount to the

company account. When it reached the maturity of the L/C, BIDV Saigon Branch

would ask Fortis Bank to honor drafts. In case Fortis Bank refused the documents

due to discrepancies, BIDV Saigon Branch can ask Seafood Joint-stock Company

No.4 to reimburse the amount credited before.

2.2. Differences between the procedures in reality and in theory

From the procedure explained above, it can be seen that in reality, the

procedure to obtain payment for export contract is basically similar to the procedure

in theory. However, there are some differences. Firstly, in reality, amendment of the

official L/C can be avoided. If exporter and importer have had a long-term

relationship and importer has become a regular customer of the issuing bank, the

importer can ask the bank to send them the draft L/C and then forward it to the

exporter. The draft L/C can facilitate the process of executing the contract as well as

save money for the exporter. In particular, by reviewing the draft L/C, the exporter

can avoid amendments of the official L/C. It is beneficial because normally, all

20

amendment fees are to the account of the exporter and by avoiding amendments on

the official L/C, the exporter can save such money. In addition, the process of

amendment are time-consuming: the exporter has to ask the applicant to instruct the

issuing bank to amend the L/C, then the exporter has to check the L/C again until all

the terms and conditions are satisfactory. Such process can prolong the time to

obtain the L/C while the exporter normally would not ship the goods before the L/C

correspond to the agreement, which would finally result in delay in the execution of

the contract and cause inconvenience for both the exporter and the importer.

Secondly, in reality, the exporter can deliver goods before the issuance of the

L/C. In this case, it can be seen that Seafood Joint-stock Company No.4 delivered

goods on March 29, 2013 while the L/C was opened on April 2, 2013. In theory, it

is recommended that the exporter do not ship the goods until the L/C has been

opened and all terms and conditions in it are satisfactory. However, in fact, if the

importer is a regular partner and the exporter has been able to check the draft L/C,

the exporter can ship the consignment before receiving the L/C.

Finally, documents to be presented for payment at the bank can be submitted

in parts. When presenting documents for negotiation at negotiating bank, the

exporter can submit some important documents to obtain payment first and present

remaining documents later. In this case, Seafood Joint-stock Company No.4 only

submitted Drafts, Invoices, B/Ls and Packing Lists. Other documents including

Health Certificate, C/O, Chemical Analysis Certificate, Microbiology Analysis

Certificate, Traceability Code List, Copy of printing of master cartons and riders,

Beneficiary’s Attestation and Beneficiary’s Declaration were presented later. It is a

huge advantage for the exporter as they can obtain payment as soon as possible after

the delivery of goods and prepare and submit the remaining documents later.

2.3. Advantages and disadvantages of Seafood Joint-stock Company No.4 in

performing payment procedure by L/C for export contract

2.3.1. Advantages

From the procedure to obtain payment by L/C for contract

No.81DOTA/03/2013 above, it can be seen that the company has some advantages

as follows: First, Seafood Joint-stock Company No.4 has skillful staffs who are

21

familiar with the procedure. Young yet dynamic and enthusiastic staff can manage

different situations and problems. They always try to fulfill their tasks in short time,

which facilitate and hasten the procedure. Therefore, the company can reduce the

risks of losing payment due to late or insufficient presentation of documents.

In addition, all departments cooperate closely, from the factory to the Planning

Department. For example, after signing the contract, the factory will be in charge of

producing and packing products as the instructions in the contract while Planning

Department prepares necessary documents. The cooperation among departments

ensures that all requirements from importers can be fulfilled.

Finally, Seafood Joint-stock Company No.4 has been able to build close

relationships with many partners. Hence, the company can negotiate for

advantageous terms and conditions while reducing costs such as amendment

charges. Furthermore, the company and staffs have been accustomed to

requirements from regular importers, which saves time and effort to fulfill such

instructions.

2.3.2. Disadvantages

Despite many advantages mentioned above, Seafood Joint-stock Company

No.4 still has some disadvantages. Firstly, the staffs of the Planning Department are

young but some are inexperienced and have limited knowledge in English. This

disadvantage can lead to difficulties not only in the negotiation of the contracts but

also in understanding documents, especially when checking the L/C.

Secondly, because of lack of working capital, the company usually get these

L/Cs negotiated to satisfy cash demand. However, the company would lose from

5% to 10% of the contract value, which equals from 125.000 USD to more than

250.000 USD in 2012 (calculated from Table 1.3). It is a tremendous loss compared

to pre-tax profits of the company.

Finally, when negotiating with new customers, the company is usually in a

weaker position. Such lack of bargaining power may result in unfavorable payment

terms for the company as an exporter such as deferred payment or documentary

collection terms.

22

CHAPTER 3: THE OUTLOOK, ORIENTED DEVELOPMENT AND

RECOMMENDATIONS FOR PROMOTION OF PERFORMING

PAYMENT PROCEDURE BY LETTER OF CREDIT IN SEAFOOD JOINT-

STOCK COMPANY NO.4

3.1. The outlook of payment by L/C for export contracts at Seafood Joint-

stock Company No.4

Figure 3.1. Proportions in number and value of export contracts paid by L/C

in Seafood Joint-stock Company No.4 in 2010 to 2012

(Source: Reports of Board of Supervisor in 2010, 2011 and 2012

of Seafood Joint-stock Company No.4)

It can be seen from Table 1.3 and Figure 3.1 that the number and proportion of

contracts paid by L/C have been increasing recently. There are some advantages

which would facilitate such increase in the future. First, some regular customers at

the present will maintain payment terms by L/C. As both parties strengthen their

relationship in the future, it is possible that the value of contracts paid by L/C would

also increase. Furthermore, when the company expands its production and business,

they will be able to sign more contracts with importers around the world. For new

customers, it would be rational to settle payment by L/C as both parties haven’t

known much about each other. Therefore, it is predictable that the number of

contracts paid by L/C shall be increasing in the next years. As the company has

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

2010 2011 2012

Number

Value

23

been building its image, prestige and brand name while fostering production

activities, they will be able to sign contracts with bigger value.

However, as mentioned above, due to the lack of bargaining power, the

company may not have favorable payment terms for new contracts. As the world

economy is now still facing many difficulties, every company would have stricter

financial policies and it is rational for companies to restrict at sight payment but to

delay payment as long as possible.

Therefore, although it is possible that not only the number but also the value

of contracts settled by L/C shall be increasing in the next years, the scale and

volume of such increase are not predictable.

3.2. Oriented development of payment by L/C for export contract

In the future, the company will expand its production activities, which requires

more capital. To ensure the operations, the company will need regular income to

facilitate its activities. As documentary credit method ensures the payment for

deliver goods, obtaining payment by L/C shall be an important solution. Therefore,

in the future, the company will try to limit the number of contracts settled by

documentary collection while increasing number of customers paid by L/C and

maintaining favorable payment terms with current customers.

From Figure 3.1 above, it can be seen that the proportion of number of

contracts settled by L/C is always smaller than the proportion of value of such

contracts. It means that although the company got quite a number of contracts paid

by L/C, their values were not very high. Hence, in the future, the company plans to

not only increase the number but also increase the value of such contracts.

In order to achieve such rise in both number and value, the company can

execute several methods. First, it is necessary to ensure the supply of seafood for

the company. It is important because if the company want to expand business, it

needs to have stable supply to ensure they can fulfill as many orders as possible,

especially large scale order. In addition, the company can the promote export to

current customers not only to have regular income but also to build its image and

position in international market. Therefore, the company will have good reputation

and brand name, which would elevate their position in negotiation.

24

3.3. Recommendations for promotion payment by L/C for export contract

In other to achieve the target mentioned in section 3.2 above, the company

would need to perform several activities to promote payment by L/C for export

contract in the future:

Firstly, it is necessary to create opportunities for staff to improve their English

and knowledge about international payment to minimize possible difficulties they

might be facing in the procedure. Staff should be able to communicate and share

their experience as well as their difficulties so that they can find possible resolves.

Having staff good at communication, negotiation as well as professional

competence would build up internal strength for the company. Communication with

current customers, partners and good negotiation with potential customers are

important activities to build a worldwide business network.

Secondly, the company needs to maintain a suitable level of working capital to

reduce negotiation of L/C in the future. It is essential to raise capital while having

reasonable financial policies. The company should consider investment plans

carefully to ensure the profitability of such projects and maintain a sufficient

amount of working capital. By this way, the company can avoid losing from 5% to

10% of the L/C value and claim the full amount of the L/C. Minimizing such loss

would increase the profit of the company and attract more investment for the future

development.

Finally, the company should promote marketing activities as well as building

its image in the international market in order to elevate its position in negotiation of

new contracts. Having negotiating power would give more advantages to the

company to get favorable payment terms, such as asking importers to settle payment

by at sight L/C. However, it would be very difficult and must be a long-term task of

the company. Besides having stable supply at stable prices to ensure the

performance of the company, it is compulsory to promote the company’s brand

name to importers worldwide at international fairs,... In addition, the company must

maintain and strengthen good relationships with regular customers to improve its

bargaining power and negotiate for more favorable terms in further contracts,

especially payment terms.

25

CONCLUSION

With more than 30-year experience in business and processing frozen seafood,

Seafood Joint-stock Company No.4 has been having a certain position in the

industry as well as in international market. By promoting cultivation activities in

recent years, the company has been able to ensure part of its supplies while reducing

costs. In the near future, when the economy has positive changes, the company will

be able to expand its business.

In the procedure of executing export contracts, obtaining payment for

contracts paid by L/C plays an important role in the operations of the Seafood Joint-

stock Company No.4. My report including 3 chapters have expressed my

understandings of the payment procedure by L/C for export contracts at Seafood

Joint-stock Company No.4. First, although payment by L/C for export contracts

hasn’t accounted for most of the turnover of the company, contracts settled by L/C

have important roles in the company’s operation. Second, the procedure to obtain

payment for such contracts at Seafood Joint-stock Company No.4 has been

reasonable and complete. Finally, from the analysis of the advantages and

disadvantages of the company in performing the procedure, I’ve recommended

some solutions to overcome the disadvantages of the company and promote the

procedure in the future by building internal strength and increasing its negotiation

power.

Although my knowledge is still limited and shortcomings are inevitable in this

report, I hope that the ideas can be helpful for the company, particularly for

payment procedure of the company in the future.

Finally, I would like to give my best wishes for the development of Seafood

Joint-stock Company No.4. Hopefully, with well-prepared development plans,

clear-sighted leadership of efforts of all the staff, Seafood Joint-stock Company

No.4 will enhance its prestige and strengthen its competitiveness in the industry,

elevate its position in the international market and achieve more success in the

future.

26

REFERENCES

1. Nguyen Xuan Minh, 2011, Import – Export and International Payment, Vietnam

National University – Ho Chi Minh Publishing House, Ho Chi Minh City.

2. Dinh Xuan Trinh, Dang Thi Nhan, 2011, Giáo trình Thanh toán Quốc tế, Science

and Technology Publishing House, Ha Noi.

3. International Chamber of Commerce (ICC), 2007, ICC Uniform Customs and

Practice for Documentary Credits, 2007 Revision, ICC Publication No.600.

4. Seafood Joint-stock Company No.4, 2010, 2011, 2012, Financial Reports, Ho

Chi Minh City.

5. Seafood Joint-stock Company No.4, 2010, 2011, 2012, Reports of the Board of

Supervisors, Ho Chi Minh City.

6. Mark Kinver, 2011, Global fish consumption hits record high. [online] Available

at: http://www.bbc.co.uk/news/science-environment-12334859 [Accessed June

12, 2013]

7. Seafood Joint-stock Company No.4, 2013, Introduce Our Company. [online]

Available at http://www.seafoodno4.com/aboutus.php?id=1 [Accessed June 12,

2013]

8. Vietnam Customs, 2013, Tong quan tinh hinh xuat khau thuy san cua Viet Nam

trong nam 2012. [online] Available at:

http://www.customs.gov.vn/lists/tinhoatdong/ViewDetails.aspx?ID=19655&Cate

gory=Th%E1%BB%91ng%20k%C3%AA%20H%E1%BA%A3i%20quan

[Accessed June 22, 2013]

9. VnExpress, 2012, 30% doanh nghiệp thủy sản không thể xuất khẩu [online]

Available at http://kinhdoanh.vnexpress.net/tin-tuc/vi-mo/30-doanh-nghiep-thuy-

san-khong-the-xuat-khau-2722943.html [Accessed on June 12, 2013]

27

ANNEXES

1. Purchase confirmation/Contract No.81DOTA/03/2013

2. L/C opened for Contract No.81DOTA/03/2013

3. Documents required for presentation

4. Electronic customs declaration

5. Request for negotiation of the L/C