Embed Size (px)

DESCRIPTION

Desciption of Reduced Gradient Method for Optimization in Excel.

Citation preview

How does Microsoft Excel solver deal with nonlinear problems – A simple example

劉亮志

Recall our question

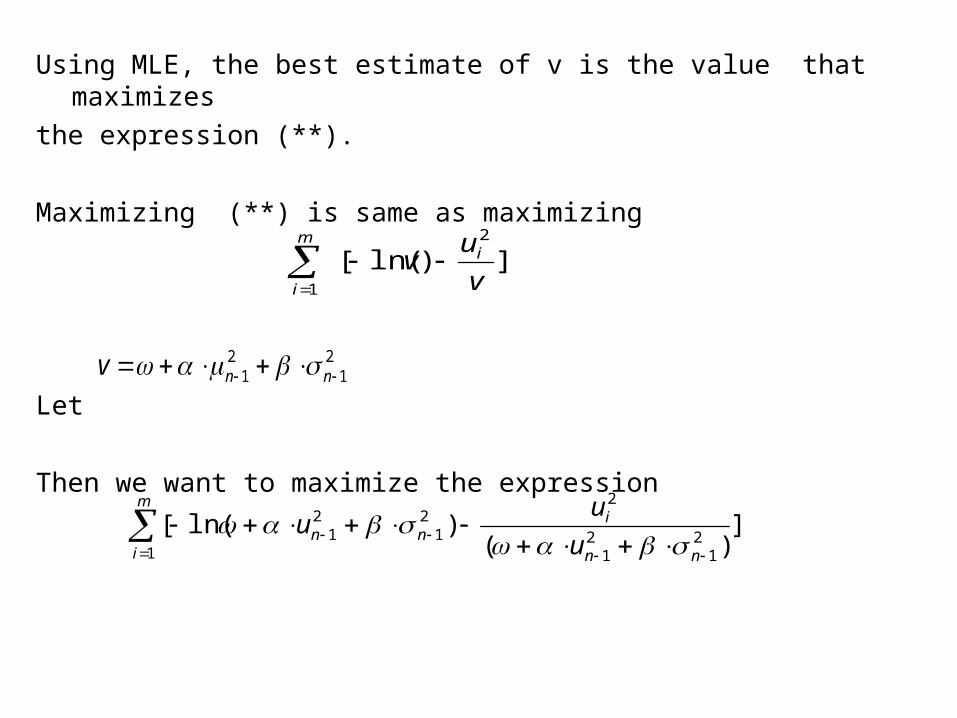

• The equation for GARCH(1,1) is

where

Set ,

Then we get

1

21

21

2 nnLn V

LV 0

21

21

2 nnn

• Later, we met an example about MLE method :

Consider the problem of estimating the variance

of variable X from m observations on X when

underlying distribution is normal with zero mean.

Assume that the observations are .

Denote the variance v . The likelihood of being

observed is defined as the probability density function

for X when . This is

Then the joint density function of this m observations is

(**)

muuu ,...,, 21

iu

iuX

)2

exp(2

1 2

v

u

vi

)]2

exp(2

1[

2

1 v

u

vi

m

i

Using MLE, the best estimate of v is the value that maximizes

the expression (**).

Maximizing (**) is same as maximizing

Let

Then we want to maximize the expression

])ln([2

1 v

uv i

m

i

21

21 nnv

m

i nn

inn u

uu

121

21

221

21 ]

)()ln([

• We wonder what’s the value of that maximizes

subject to the boundary conditions

,,

m

i nn

inn u

uu

121

21

221

21 ]

)()ln([

1

0

1

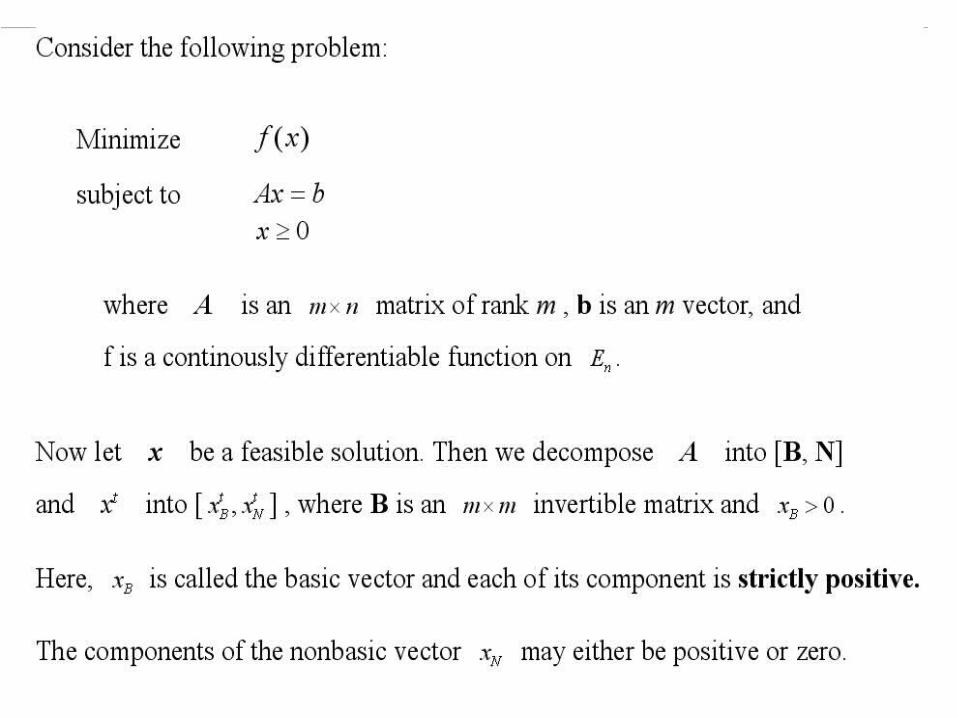

How does Microsoft Excel solver deal with nonlinear programs?

(1) the long …long way to find the method out

(2) basic idea and a simple example

(3) reference

Long way

Microsoft Office Online

http://office.microsoft.com/zh-tw/

• Excel adopts the generalized reduced gradient (GCG)

method to deal with nonlinear problems.

• GCG originates from the method of reduced gradient

of Wolf.

• More specifically, the question (MLE) we met is a nonlinear

programming problem with linear constraints.

Basic idea of method of reduced gradient

Summary of Reduced Gradient Algorithm

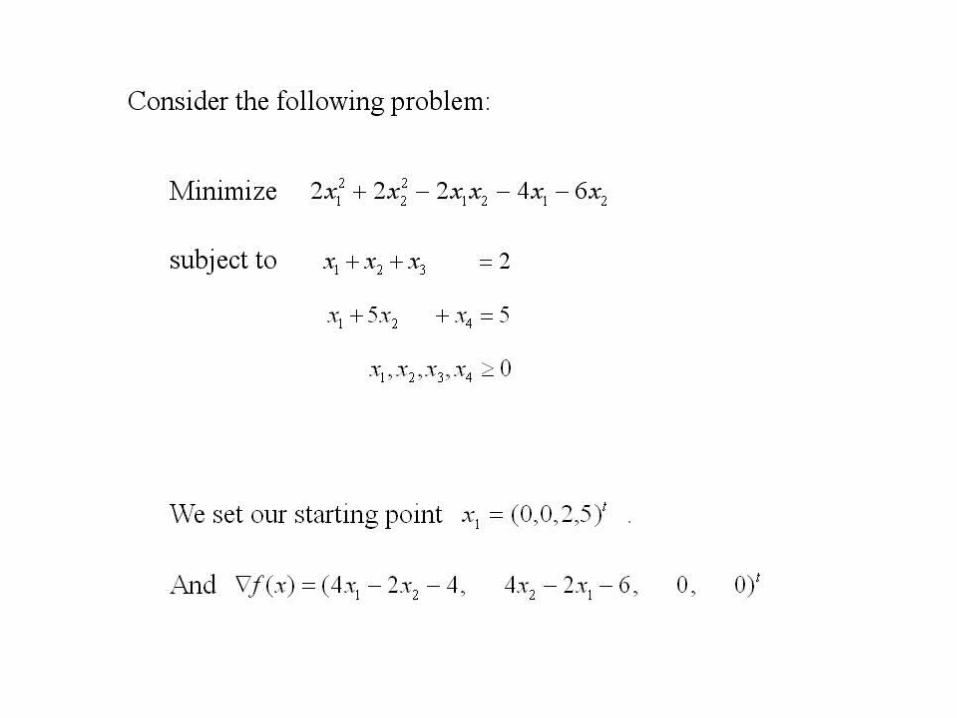

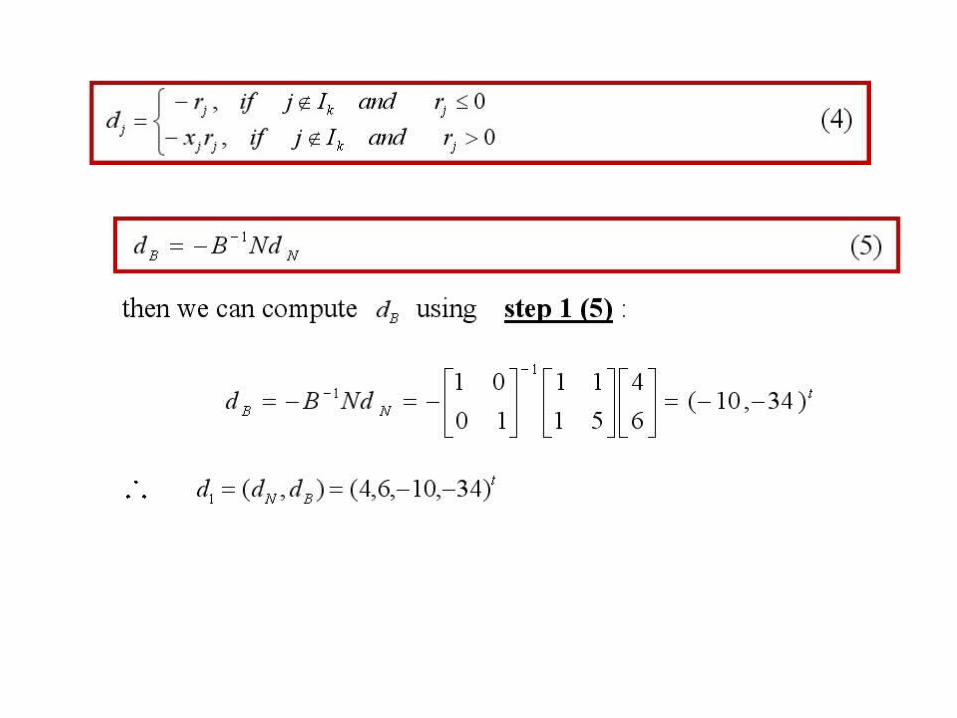

A simple example

Iterative 1

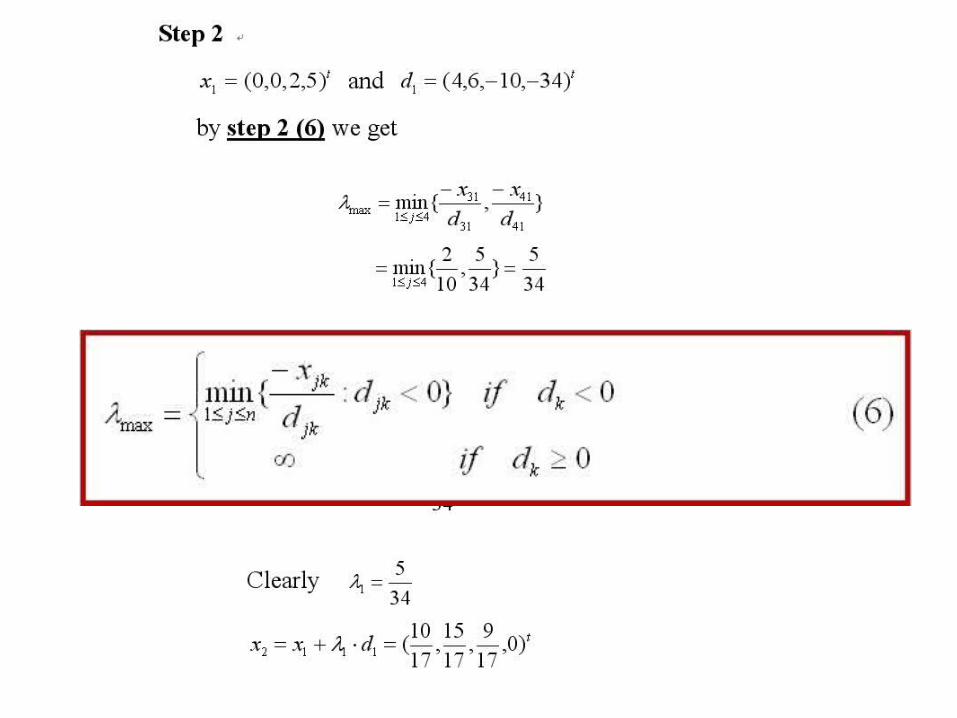

Iterative 2

Iterative 3

Reference

• Mokhtar s. Bazraa, Hanif D. Sherali ,and C. M. Shetty. Nonlinear Programming: Theory and Algorithm second edition Section 10.6

• Wenyu Sun, and Ya-Xiang Yuan. Optimization Theory and Methods: Nonlinear Programming Section 11.3

• Hong-Tau Lee, Sheu-Hua Chen, He-Yau Kang.

A Study of Generalized Reduced Gradient Method

with Different Search Directions • Daniel Fylstra, Leon Lasdon, John Waston, Allen

Waren. Design and Use of the Microsoft Excel Solver.