Analys och bedömning av företag och förvaltning

7,5 högskolepoäng

Provmoment: Ordinarie tentamen

Ladokkod: SAN023

Tentamen ges för: ACEKO12h REDO

TentamensKod:

Tentamensdatum: 2017 – 01 - 13 Tid: Kl 09:00 – 13:00

Hjälpmedel:

Räknedosa

Ordbok/Lexikon

Totalt antal poäng på tentamen: 60 poäng

För att få respektive betyg krävs: För betyg G Minst 30 p. och för betyg VG minst 45 p.

Allmänna anvisningar:

Tentamen består av tre huvuddelar, dvs. Flervalsfrågor, Sanna/Falska frågor och essäfrågor.

Vid tentamen har ett formelblad och de specifika räntetabellerna bifogats. Ni kan använda dessa underlag om det behövs.

OBS! Skriv väldigt tydligt! Texter som inte kan läsas får inga poäng! Nästkommande tentamenstillfälle: Äger rum torsdagen den 2 maj 2017

Rättningstiden är i normalfall 15 arbetsdagar, till detta tillkommer upp till 5 arbetsdagar för administration, annars är det detta datum som gäller: Viktigt! Glöm inte att skriva Tentamenskod på alla blad du lämnar in. Lycka till! Ansvarig lärare: Ziaeddin Mansouri Telefonnummer: 0708 - 247 555

2

PART ONE Multiple-Choice Questions (25 Points)

Please read the following 25 questions and ring in one of the four alternative

answers of A, B, C, and D, which is the right one? (Note: each question gives max

1 point, and there is not any minus point in the case of wrong answer!)

1- Please choose which of the following options is not a common tool used in

financial statement analysis? (1 p.)

A. Random walk analysis

B. Ratio analysis

C. Common-size statement analysis

D. Credit analysis

2- As an analyst, you are analyzing a large stable Swedish company. For the

year ending 31-12-2015 the company reported earnings of $58,900. You

expect earnings to grow at 5% a year in perpetuity, and the dividend payout

ratio of 70% to continue. The company borrows at 8%, and has a cost of

equity of 12%. The company has 25,000 shares outstanding.

Please decide what your estimate of price per share is at the end of Year 2015

(31–12–2015), by using the dividend discount model? (1 p.)

A. $24.74

B. $23.56

C. $21.65

D. $20.62

3- A company issues 10%, 10-year $1,000 bonds paying interest semiannually.

Required return for bonds of this risk is 16%. Please decide at what price the

bond will be sold (pick closest answer)?

A. $659

B. $705

C. $710

D. $783

3

4- Please read the following statements and choose which one of them is an

example of judgments made in the accounting reporting process?

I. Useful life of machinery

II. Allowance for doubtful accounts

III. Obsolescence of assets

IV. Interest payment on bonds

A. I, II, III, and IV

B. I, II, and III

C. II and III

D. I and III

5- Please choose which of the following is a change in an accounting estimate?

I. A change from straight-line depreciation to declining balance method

II. A change in estimated salvage value of depreciable asset

III. A change in estimated useful life of an asset

IV. Recording depreciation for the first time on machinery purchased five

years ago

A. I, II, III, and IV

B. II, III, and IV

C. I, III, and IV

D. II and III

6- Please choose what economic income includes:

A. Recurring components only

B. Nonrecurring components only

C. Both recurring and nonrecurring components

D. Neither recurring nor nonrecurring components

7- Please choose which of the following is not a criterion for defining a lease as a

capital lease?

A. Ownership is transferred at the end of the lease agreement.

B. The lease contains an option to purchase the asset at a bargain price.

C. The present value of the lease payments at the beginning of the lease

is 75% or more than the value of the asset.

D. The lease term is at least 75% of the economic life of the asset.

4

8- Please choose the right definition of treasury stock among the following ones:

A. Investments in government securities.

B. Retained earnings that have been appropriated to make equity

investments.

C. A company's own stock that it has repurchased.

D. Assets held for safekeeping in company's vaults.

9- A company's current ratio is 1.5. If the company uses cash to retire notes

payable due within one year, would this transaction increase or decrease the

current ratio and return on assets ratio?

A. Current ratio: Increase; Return on assets: Increase

B. Current ratio: Increase; Return on assets: Decrease

C. Current ratio: Decrease; Return on assets: Increase

D. Current ratio: Decrease; Return on assets: Decrease

10- We have obtained following information about the inventories of the

manufacturing company Alfa Inc. at the end of Years 2005 and 2006.

In order to restate Year 2006 LIFO inventories to a FIFO basis, please choose

the right option that we have used in the following analytical entries:

5

11- You have access to the financial statements of Beta Company, which

indicates that ending inventory levels in 2014 and 2015 were $400,000 and

$700,000 respectively. Cost of goods sold for 2014 and 2015 were $3,800,000

and $4,400,000 respectively. Please calculate the Beta’s purchases in 2015:

A. 3,900,000

B. 4,700,000

C. 4,300,000

D. 3,700,000

12- Which of the following statements is not an effect of capitalization approach?

A. Capitalization usually increases net income.

B. Capitalization usually yields a smoother net income.

C. Capitalization usually decreases the volatility of the return on

investment.

D. Capitalization usually reduces net income.

13- Please choose one of the following statements, which is incorrect with respect

to recognized goodwill on the balance sheet?

A. It should not be amortized.

B. It arises when another company is purchased or when internally

generated.

C. It should be written-down if the future benefits no longer exist.

D. It may be negative.

14- Assume that company Alfa acquires 45% of Company Beta in a stock-for-

stock exchange. With respect to preparing financial statements, which of the

following statements is correct?

A. Company Alfa will most likely use pooling-of-interest accounting for

consolidation purposes.

B. Company Alfa will most likely use purchase accounting.

C. Company Alfa will most likely use the cost method.

D. Company Alfa will most likely use the equity method.

6

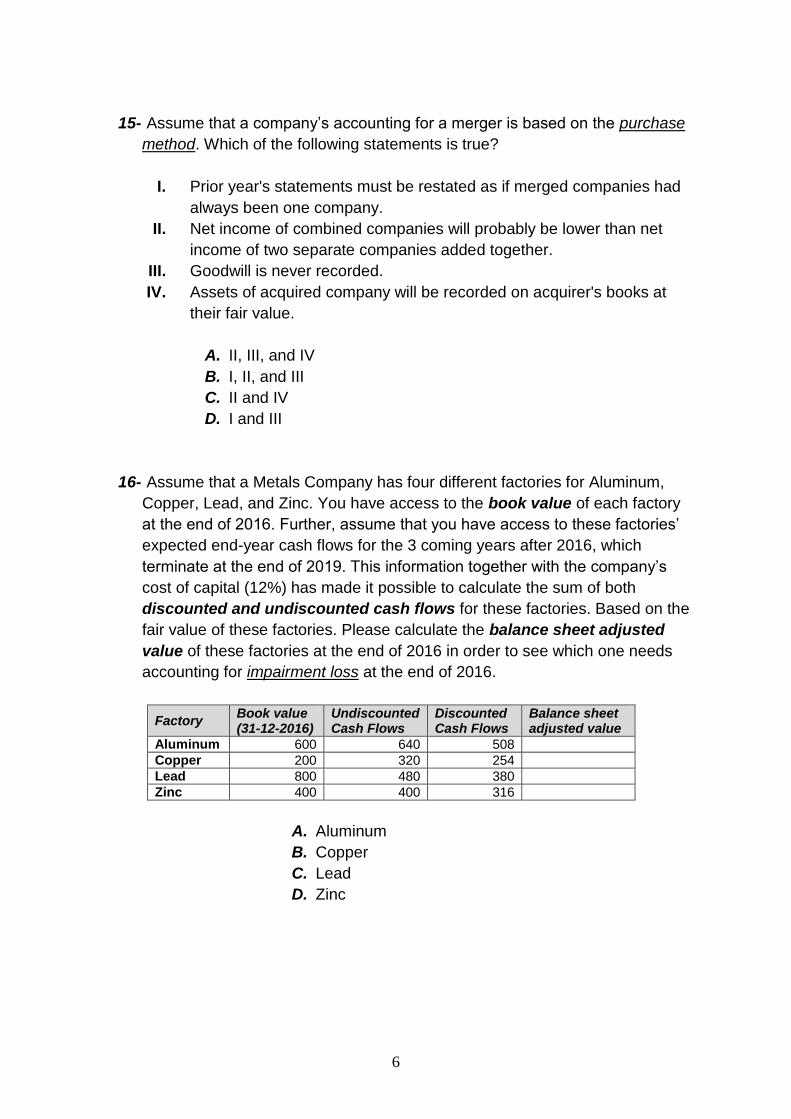

15- Assume that a company’s accounting for a merger is based on the purchase

method. Which of the following statements is true?

I. Prior year's statements must be restated as if merged companies had

always been one company.

II. Net income of combined companies will probably be lower than net

income of two separate companies added together.

III. Goodwill is never recorded.

IV. Assets of acquired company will be recorded on acquirer's books at

their fair value.

A. II, III, and IV

B. I, II, and III

C. II and IV

D. I and III

16- Assume that a Metals Company has four different factories for Aluminum,

Copper, Lead, and Zinc. You have access to the book value of each factory

at the end of 2016. Further, assume that you have access to these factories’

expected end-year cash flows for the 3 coming years after 2016, which

terminate at the end of 2019. This information together with the company’s

cost of capital (12%) has made it possible to calculate the sum of both

discounted and undiscounted cash flows for these factories. Based on the

fair value of these factories. Please calculate the balance sheet adjusted

value of these factories at the end of 2016 in order to see which one needs

accounting for impairment loss at the end of 2016.

Factory Book value (31-12-2016)

Undiscounted Cash Flows

Discounted Cash Flows

Balance sheet adjusted value

Aluminum 600 640 508

Copper 200 320 254

Lead 800 480 380

Zinc 400 400 316

A. Aluminum

B. Copper

C. Lead

D. Zinc

7

Please use the following case to answer questions 17-20.

Prospective Inc. is a manufacturing company within hardware computer industry.

The company's sales in December were $5,500. Its sales expect to increase 10% in

January and February and 15% in March. All of its sales are made on credit. The

typical collection pattern is:

Percentages for collections of total receivables

In month of sale 10%

In second month 70%

In third month 15%

Not collectable 5%

Moreover you can assume that the Prospective Company’s Gross margin is 30%.

Inventory levels at the end of December are $900 and are expected to grow at the

same rate as sales. Purchases are paid for the month after they are made. Net

accounts receivable at the end of December are $400.

17- How much Prospective should collect in March?

A. $7,653.25 cash from sales made in March and previous months.

B. $7,342.50 cash from sales made in March and previous months.

C. $7,030.10 cash from sales made in March and previous months.

D. $6,331.30 cash from sales made in March and previous months.

18- How much is the Prospective’s anticipated inventory level at the end of

March?

A. $1,252.35

B. $1,197.90

C. $1,089

D. $900

19- How much cash has Prospective paid for purchases in the month of March?

A. $5,520.62

B. $4,757.50

C. $4,559.50

D. $2,095.50

8

20- Prospective’s net account receivable at the end of March is closest to:

A. $7,503.51

B. $7,886.17

C. $8,218.93

D. None of the above

9

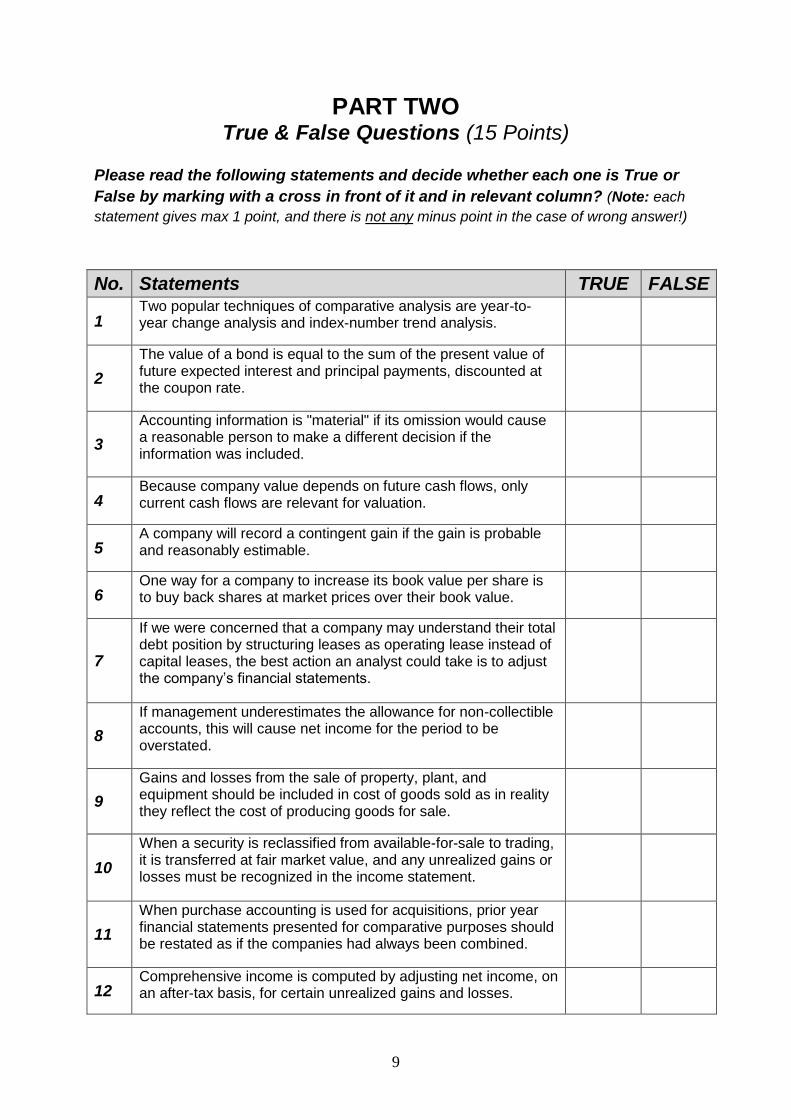

PART TWO True & False Questions (15 Points)

Please read the following statements and decide whether each one is True or

False by marking with a cross in front of it and in relevant column? (Note: each

statement gives max 1 point, and there is not any minus point in the case of wrong answer!)

No. Statements TRUE FALSE

1 Two popular techniques of comparative analysis are year-to-year change analysis and index-number trend analysis.

2

The value of a bond is equal to the sum of the present value of future expected interest and principal payments, discounted at the coupon rate.

3

Accounting information is "material" if its omission would cause a reasonable person to make a different decision if the information was included.

4 Because company value depends on future cash flows, only current cash flows are relevant for valuation.

5 A company will record a contingent gain if the gain is probable and reasonably estimable.

6 One way for a company to increase its book value per share is to buy back shares at market prices over their book value.

7

If we were concerned that a company may understand their total debt position by structuring leases as operating lease instead of capital leases, the best action an analyst could take is to adjust the company’s financial statements.

8

If management underestimates the allowance for non-collectible accounts, this will cause net income for the period to be overstated.

9

Gains and losses from the sale of property, plant, and equipment should be included in cost of goods sold as in reality they reflect the cost of producing goods for sale.

10

When a security is reclassified from available-for-sale to trading, it is transferred at fair market value, and any unrealized gains or losses must be recognized in the income statement.

11

When purchase accounting is used for acquisitions, prior year financial statements presented for comparative purposes should be restated as if the companies had always been combined.

12 Comprehensive income is computed by adjusting net income, on an after-tax basis, for certain unrealized gains and losses.

10

13

Under long-term performance contracts—such as product warranty contracts and software maintenance contracts, revenues are often collected in advance and are recognized proportionally over the entire period of the contract.

14

Once the projected financial statements are prepared, there is no need for sensitivity analysis to examine the assumptions used in the preparation.

15

If a company chooses the fair value option for an asset or liability, all changes in the fair value of the asset (or liability), including unrealized gain and losses, will be included in net income.

11

PART THREE Essay Questions (25 Points)

Please read each of the following 5 questions and answer them by calculating

and explaining your answer whatever it needs. (When necessary you can use tear

sheets available at the exam. If you are to explain your answers please write very clearly in

Swedish or English. The texts that are not readable don’t obtain any marks. Each question

gives max 5 points!)

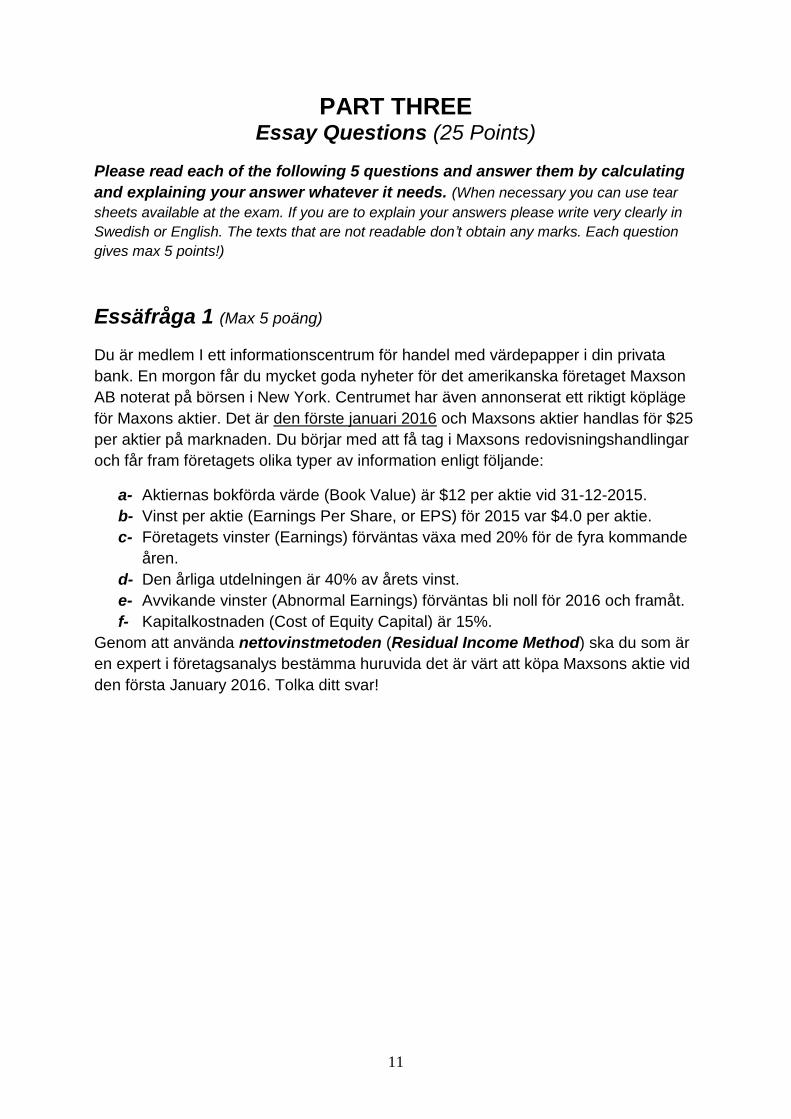

Essäfråga 1 (Max 5 poäng)

Du är medlem I ett informationscentrum för handel med värdepapper i din privata

bank. En morgon får du mycket goda nyheter för det amerikanska företaget Maxson

AB noterat på börsen i New York. Centrumet har även annonserat ett riktigt köpläge

för Maxons aktier. Det är den förste januari 2016 och Maxsons aktier handlas för $25

per aktier på marknaden. Du börjar med att få tag i Maxsons redovisningshandlingar

och får fram företagets olika typer av information enligt följande:

a- Aktiernas bokförda värde (Book Value) är $12 per aktie vid 31-12-2015.

b- Vinst per aktie (Earnings Per Share, or EPS) för 2015 var $4.0 per aktie.

c- Företagets vinster (Earnings) förväntas växa med 20% för de fyra kommande

åren.

d- Den årliga utdelningen är 40% av årets vinst.

e- Avvikande vinster (Abnormal Earnings) förväntas bli noll för 2016 och framåt.

f- Kapitalkostnaden (Cost of Equity Capital) är 15%.

Genom att använda nettovinstmetoden (Residual Income Method) ska du som är

en expert i företagsanalys bestämma huruvida det är värt att köpa Maxsons aktie vid

den första January 2016. Tolka ditt svar!

12

Essäfråga 2 (Max 5 poäng)

Swedish Entertainment AB (SEAB) är ett noterat företag på Stockholmbörsen och

aktiv inom musikbranschen. SEAB startade sin affärsverksamhet med 2,200 tkr i

kontanter, dels genom att sälja 1 200 tkr aktier och dels genom att sälja 1,000 tkr

företagsobligationer till nominellt värde med en kupongränta på 6%.

SEAB använde hela dessa kontanter för att köpa en fastighet (en byggnad). Därefter

hyrde företaget ut sin fastighet för 200 tkr per år. Härmed har SEAB:s begynnelse-

balansräkning ställts upp enligt följande:

Begynnelsebalansräkningen (År 1)

Tillgångar Eget kapital och Skulder

Byggnad 2,200 Aktiekapital 1,200

Kassa 0 Långfristigt lån 1,000

Summa Tillgångar 2,200 Summa Eget kapital och Skulder 2,200

Vid slutet av första året har dock byggnaden värderats upp till 3000 tkr och företags-

obligationens marknadsvärde fallit ner till 980 tkr. Anta att byggnadens nyttjande-

period är på 30 år och dess restvärde kommer att ligga på 1,000 tkr vid slutet av den

här perioden. Anta vidare att SEAB:s hyresgäst betalar sin hyra i slutet av året och

att ränteutgifterna (Kuponräntorna) för företagsobligationen också betalas ut i slutet

av året.

Som en företagsanalytiker ska du ställa upp SEAB:s resultat- och balansräkning

genom att ta hänsyn till både redovisning till verkligt värde (Fair Value Accounting)

och redovisning baserad på historisk kostnad (Historical Cost Accounting). Ni ska

alltså utforma SEAB:s resultat- och balansräkning i två skilda kolumner bredvid

varandra för att kunna jämföra och tolka effekterna av tillämpningen av dessa två

redovisningsmetoder.

13

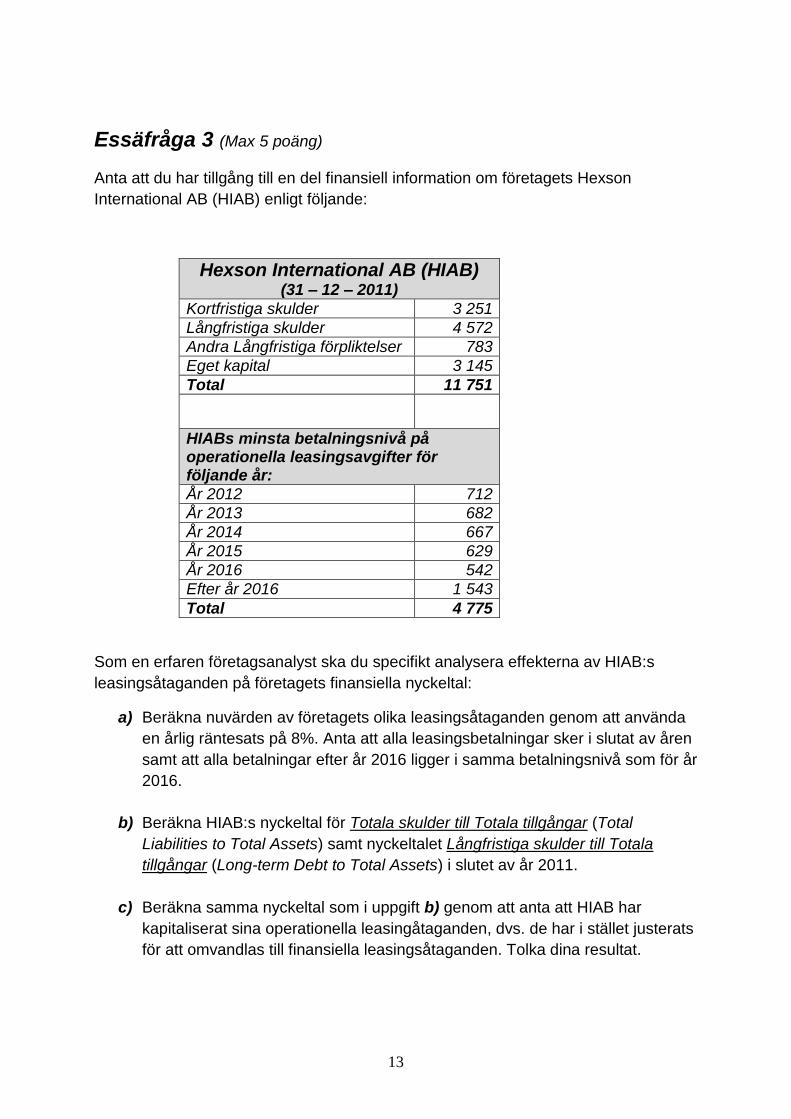

Essäfråga 3 (Max 5 poäng)

Anta att du har tillgång till en del finansiell information om företagets Hexson

International AB (HIAB) enligt följande:

Hexson International AB (HIAB) (31 – 12 – 2011)

Kortfristiga skulder 3 251

Långfristiga skulder 4 572

Andra Långfristiga förpliktelser 783

Eget kapital 3 145

Total 11 751

HIABs minsta betalningsnivå på operationella leasingsavgifter för följande år:

År 2012 712

År 2013 682

År 2014 667

År 2015 629

År 2016 542

Efter år 2016 1 543

Total 4 775

Som en erfaren företagsanalyst ska du specifikt analysera effekterna av HIAB:s

leasingsåtaganden på företagets finansiella nyckeltal:

a) Beräkna nuvärden av företagets olika leasingsåtaganden genom att använda

en årlig räntesats på 8%. Anta att alla leasingsbetalningar sker i slutat av åren

samt att alla betalningar efter år 2016 ligger i samma betalningsnivå som för år

2016.

b) Beräkna HIAB:s nyckeltal för Totala skulder till Totala tillgångar (Total

Liabilities to Total Assets) samt nyckeltalet Långfristiga skulder till Totala

tillgångar (Long-term Debt to Total Assets) i slutet av år 2011.

c) Beräkna samma nyckeltal som i uppgift b) genom att anta att HIAB har

kapitaliserat sina operationella leasingåtaganden, dvs. de har i stället justerats

för att omvandlas till finansiella leasingsåtaganden. Tolka dina resultat.

14

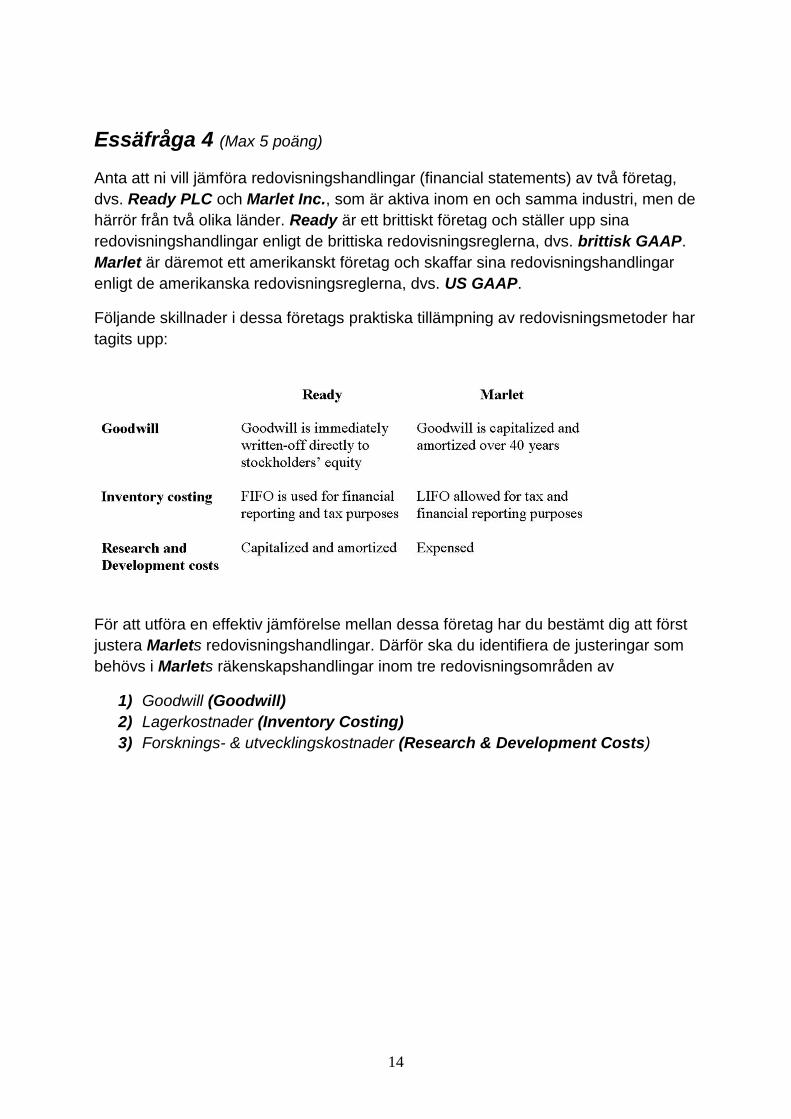

Essäfråga 4 (Max 5 poäng)

Anta att ni vill jämföra redovisningshandlingar (financial statements) av två företag,

dvs. Ready PLC och Marlet Inc., som är aktiva inom en och samma industri, men de

härrör från två olika länder. Ready är ett brittiskt företag och ställer upp sina

redovisningshandlingar enligt de brittiska redovisningsreglerna, dvs. brittisk GAAP.

Marlet är däremot ett amerikanskt företag och skaffar sina redovisningshandlingar

enligt de amerikanska redovisningsreglerna, dvs. US GAAP.

Följande skillnader i dessa företags praktiska tillämpning av redovisningsmetoder har

tagits upp:

För att utföra en effektiv jämförelse mellan dessa företag har du bestämt dig att först

justera Marlets redovisningshandlingar. Därför ska du identifiera de justeringar som

behövs i Marlets räkenskapshandlingar inom tre redovisningsområden av

1) Goodwill (Goodwill)

2) Lagerkostnader (Inventory Costing)

3) Forsknings- & utvecklingskostnader (Research & Development Costs)

15

Essäfråga 5 (Max 5 poäng)

(Denna uppgift är baserade på Glenn Fihns del av kursen!)

DELUPPGIFT A: Redogör för vad som karaktäriserar Realizable profit och Business

profit: deras delar; värderingsbegrepp; förhållande till realisationsprincipen.

DELUPPGIFT B: Redogör kortfattat för vad Income Smoothing och Earnings

Management är för något.

Recommended