Embed Size (px)

Citation preview

UltaBeauty’sUnconven0onalGrowthStory:OmnichannelExpansionisaBeau0fulThing

JeffHammSrDirector,E-Commerce

UltaBeauty

Presented:September27,2016atRetail’sDigitalSummit

PatOgawaManagingDirector

DeloiQe

CONFIDENTIAL&PROPRIETARY2015 2

CONFIDENTIAL&PROPRIETARY2015 3

PlayUltaIntroVideo

CONFIDENTIAL&PROPRIETARY2015 4

• Founded in 1990

• The largest beauty retailer in the U.S.

• The premier beauty des<na<on that provides All Things Beauty, All in One Place

CONFIDENTIAL&PROPRIETARY2015 5

More than 900 retail stores with more than 28,000 employees na<onwide

CONFIDENTIAL&PROPRIETARY2015 6

Over 20,000 beauty products, from over 500 brands!

CONFIDENTIAL&PROPRIETARY2015 7

And a Salon in every store…..

CONFIDENTIAL&PROPRIETARY2015 8

More than 20 million ac<ve members!!

9

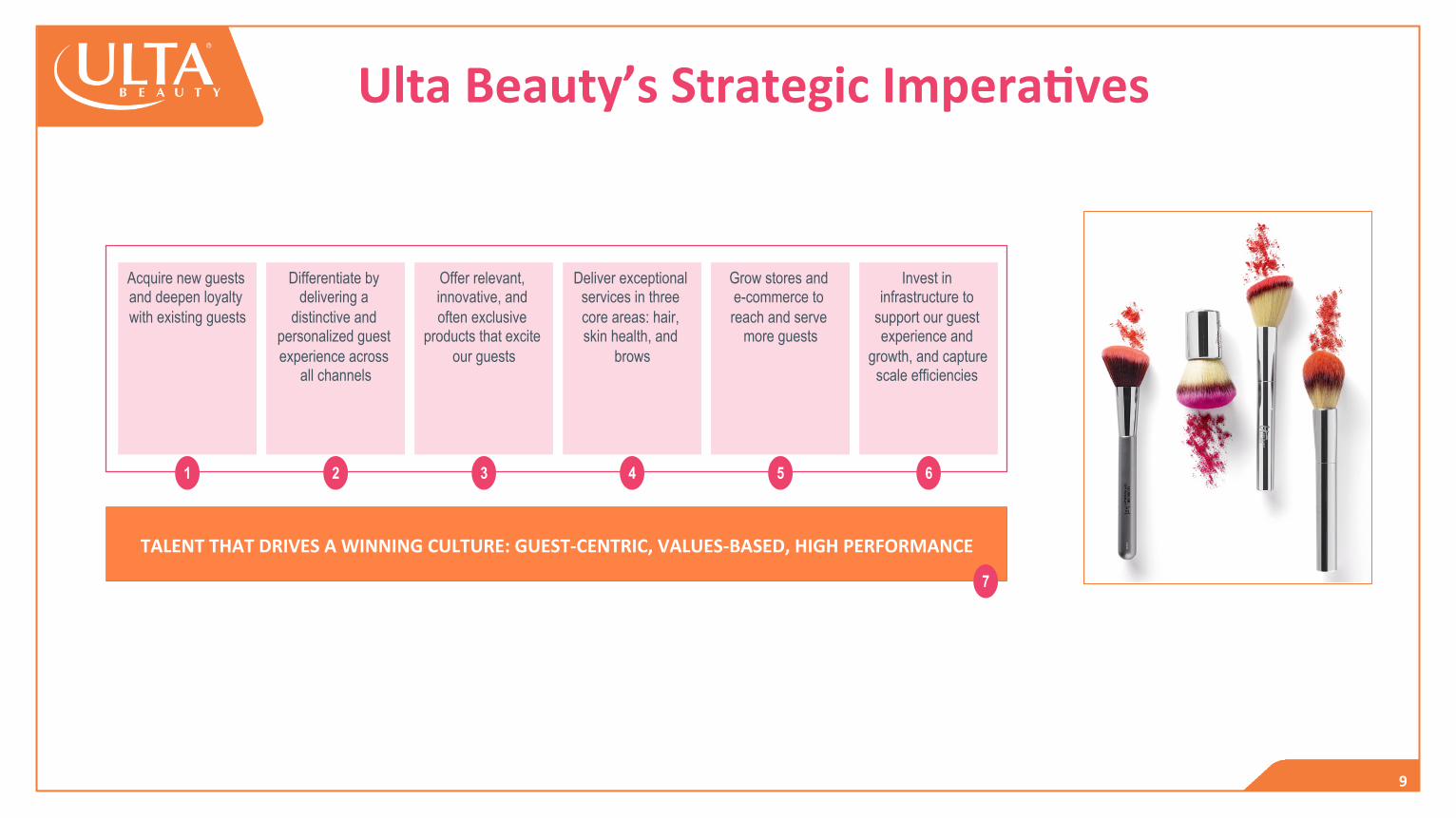

UltaBeauty’sStrategicImperaOves

Acquire new guests and deepen loyalty with existing guests

Differentiate by delivering a

distinctive and personalized guest experience across

all channels

Offer relevant, innovative, and often exclusive

products that excite our guests

Deliver exceptional services in three core areas: hair, skin health, and

brows

Grow stores and e-commerce to reach and serve

more guests

Invest in infrastructure to

support our guest experience and

growth, and capture scale efficiencies

1 2 3 4 5 6

TALENTTHATDRIVESAWINNINGCULTURE:GUEST-CENTRIC,VALUES-BASED,HIGHPERFORMANCE

7

10

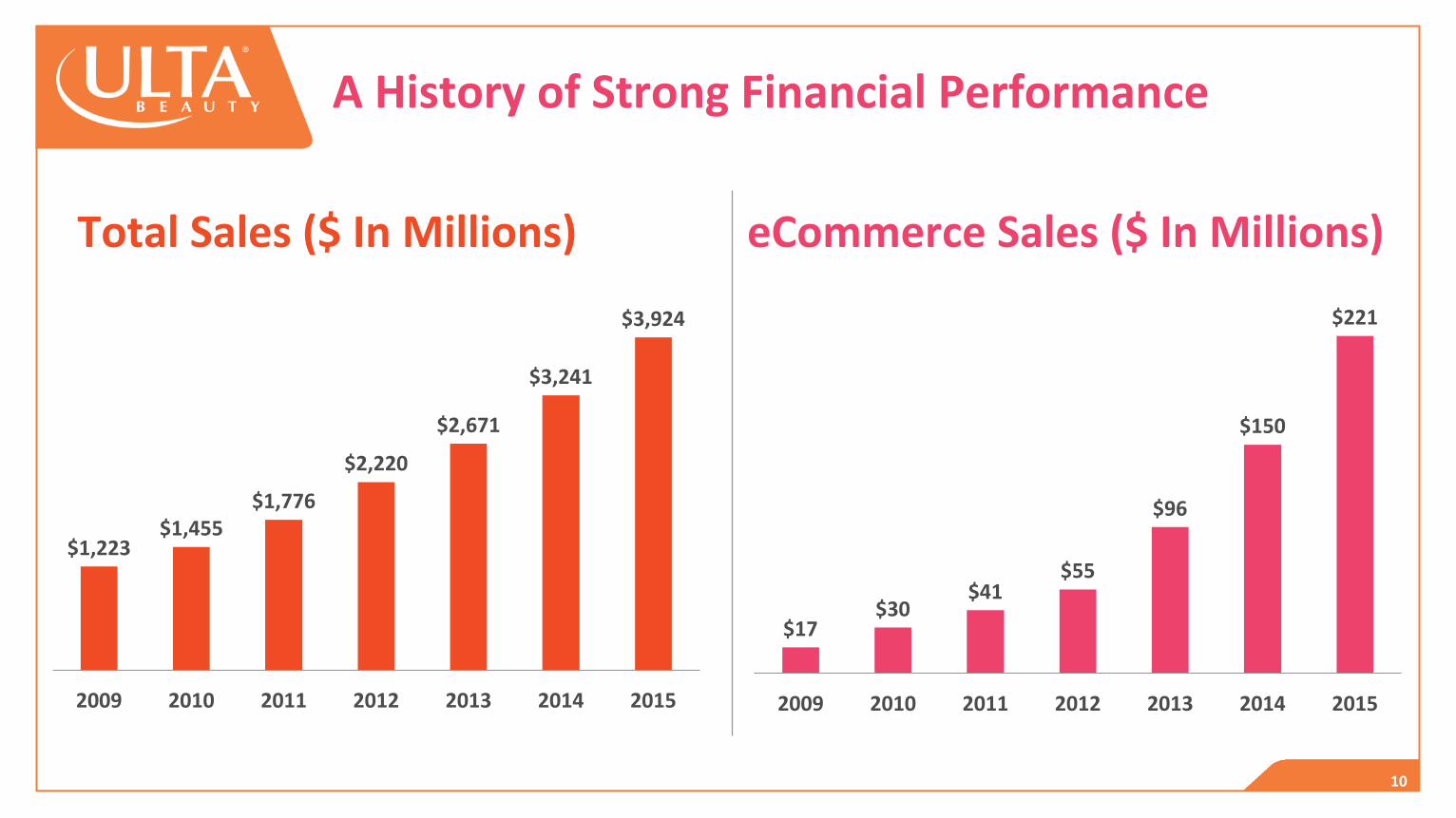

AHistoryofStrongFinancialPerformance

$1,223$1,455

$1,776

$2,220

$2,671

$3,241

$3,924

2009 2010 2011 2012 2013 2014 2015

TotalSales($InMillions)

$17$30

$41$55

$96

$150

$221

2009 2010 2011 2012 2013 2014 2015

eCommerceSales($InMillions)

CONFIDENTIAL&PROPRIETARY2015 11

Omni-ChannelatUltaBeauty–PuSngtheGuestattheCenter

12

ConnectedGuest

Home In-Store Mobile

13

What’sConnected….Online Salons

Stores Online Booking

Guest

14

What’sConnected….DC Inventory

Digital Marke<ng

CRM Data

Guest

15

….Bringingittogether,MobileFirst!

16

LeadershipModel

SUBHEADOmniChannelisnotjustaboutfeaturesandfuncOonality

17

Procurement

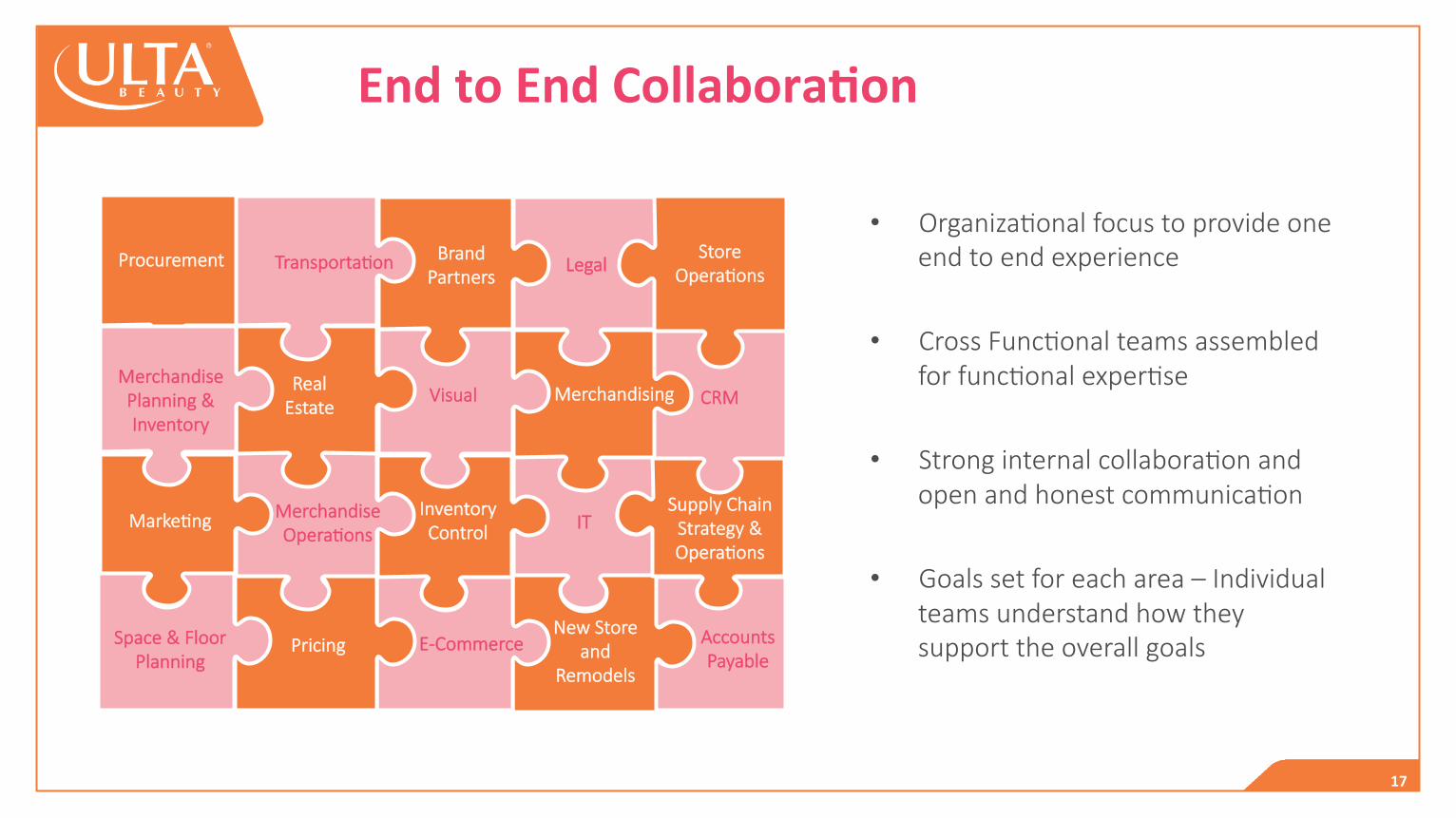

EndtoEndCollaboraOon

• Organiza<onal focus to provide one end to end experience

• Cross Func<onal teams assembled for func<onal exper<se

• Strong internal collabora<on and open and honest communica<on

• Goals set for each area – Individual teams understand how they support the overall goals

IT

Accounts Payable

New Store and

Remodels

E-Commerce Pricing Space & Floor Planning

Inventory Control

Merchandise Opera<ons

Marke<ng Supply Chain

Strategy & Opera<ons

CRM Merchandising

Legal

Visual Real Estate

Merchandise Planning & Inventory

Brand Partners

Transporta<on Store Opera<ons

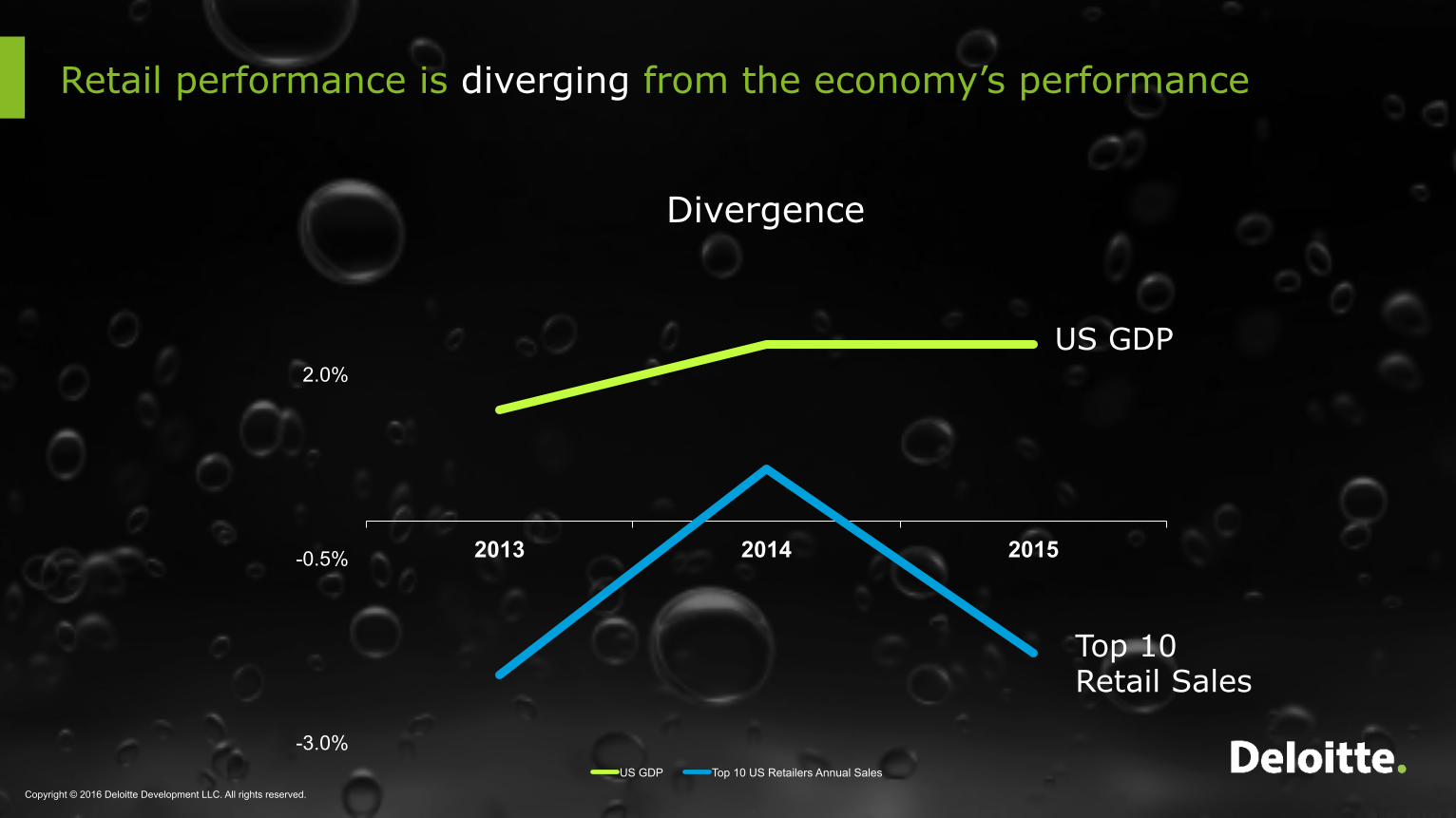

-3.0%

-0.5%

2.0%

2013 2014 2015

US GDP Top 10 US Retailers Annual Sales

Divergence

US GDP

Top 10 Retail Sales

Retail performance is diverging from the economy’s performance

Copyright © 2016 Deloitte Development LLC. All rights reserved.

And traffic to physical stores continues to plummet

Physical Store Traffic

-15%

-10%

-5%

0%

Apr '14 Jul '14 Oct '14 Jan '15 Apr '15*

Traffic Trend (Traffic)

Source: RetailNext, Retail Performance Pulse, Year-Over-Year reports (2015). Note: March/April spike due to movement of Spring Break and Easter holidays Copyright © 2016 Deloitte Development LLC. All rights reserved.

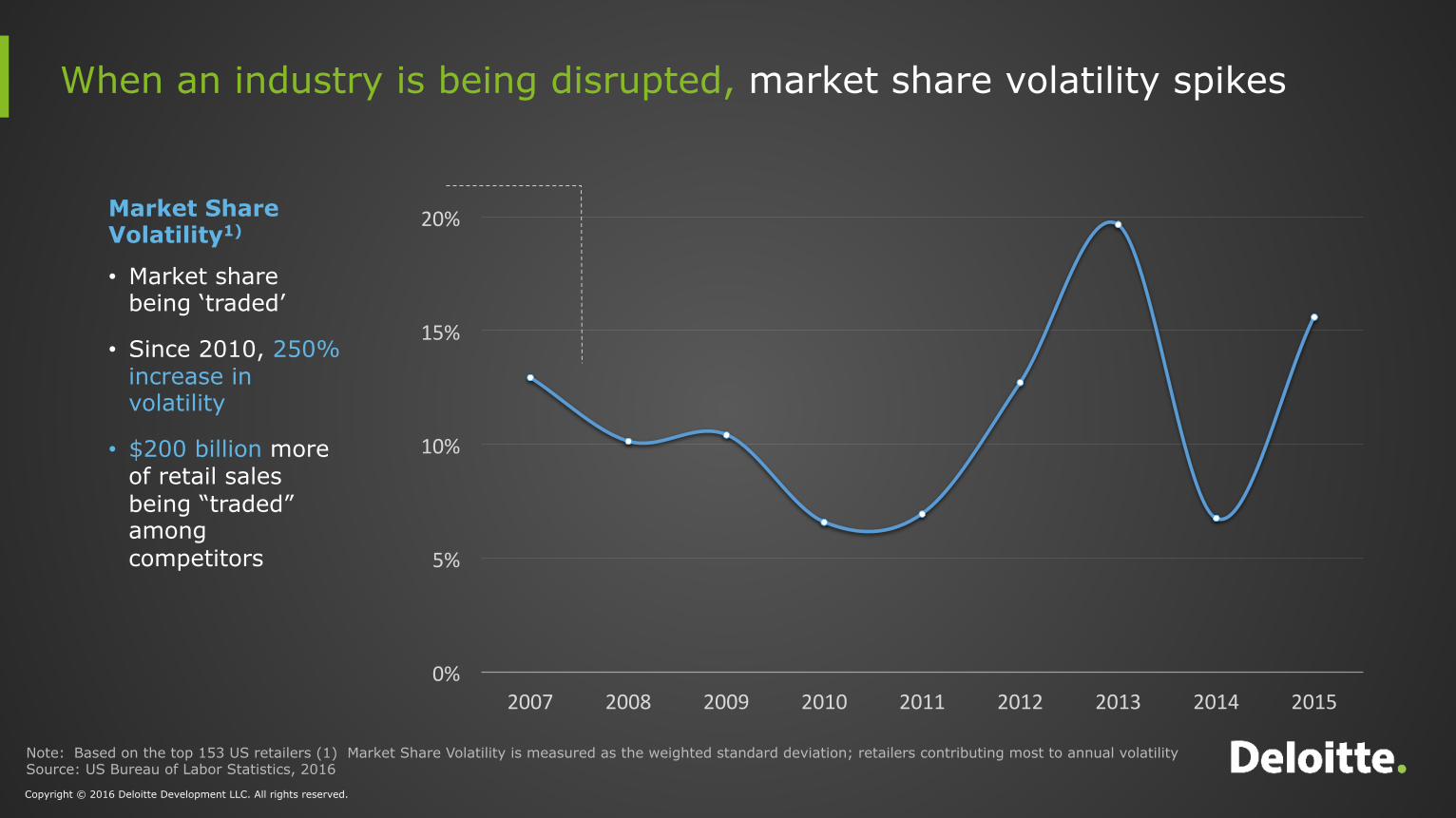

0%

5%

10%

15%

20%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Note: Based on the top 153 US retailers (1) Market Share Volatility is measured as the weighted standard deviation; retailers contributing most to annual volatility Source: US Bureau of Labor Statistics, 2016

Market Share Volatility1)

• Market share being ‘traded’

• Since 2010, 250% increase in volatility

• $200 billion more of retail sales being “traded” among competitors

When an industry is being disrupted, market share volatility spikes

Copyright © 2016 Deloitte Development LLC. All rights reserved.

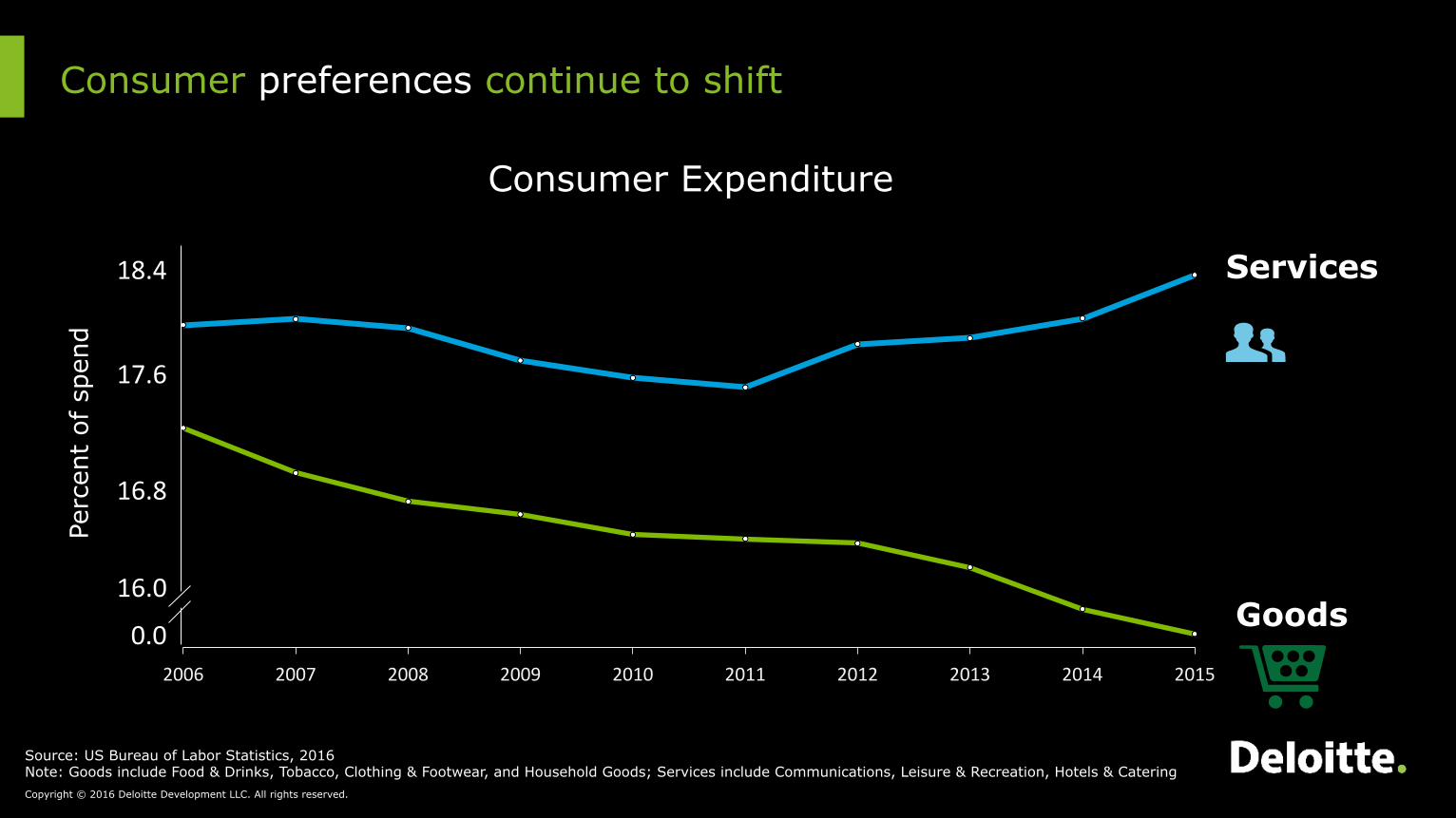

Consumer preferences continue to shift

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0.0

17.6

16.0

16.8

18.4

Consumer Expenditure

Services

Goods

Source: US Bureau of Labor Statistics, 2016 Note: Goods include Food & Drinks, Tobacco, Clothing & Footwear, and Household Goods; Services include Communications, Leisure & Recreation, Hotels & Catering

Perc

ent

of s

pend

Copyright © 2016 Deloitte Development LLC. All rights reserved.

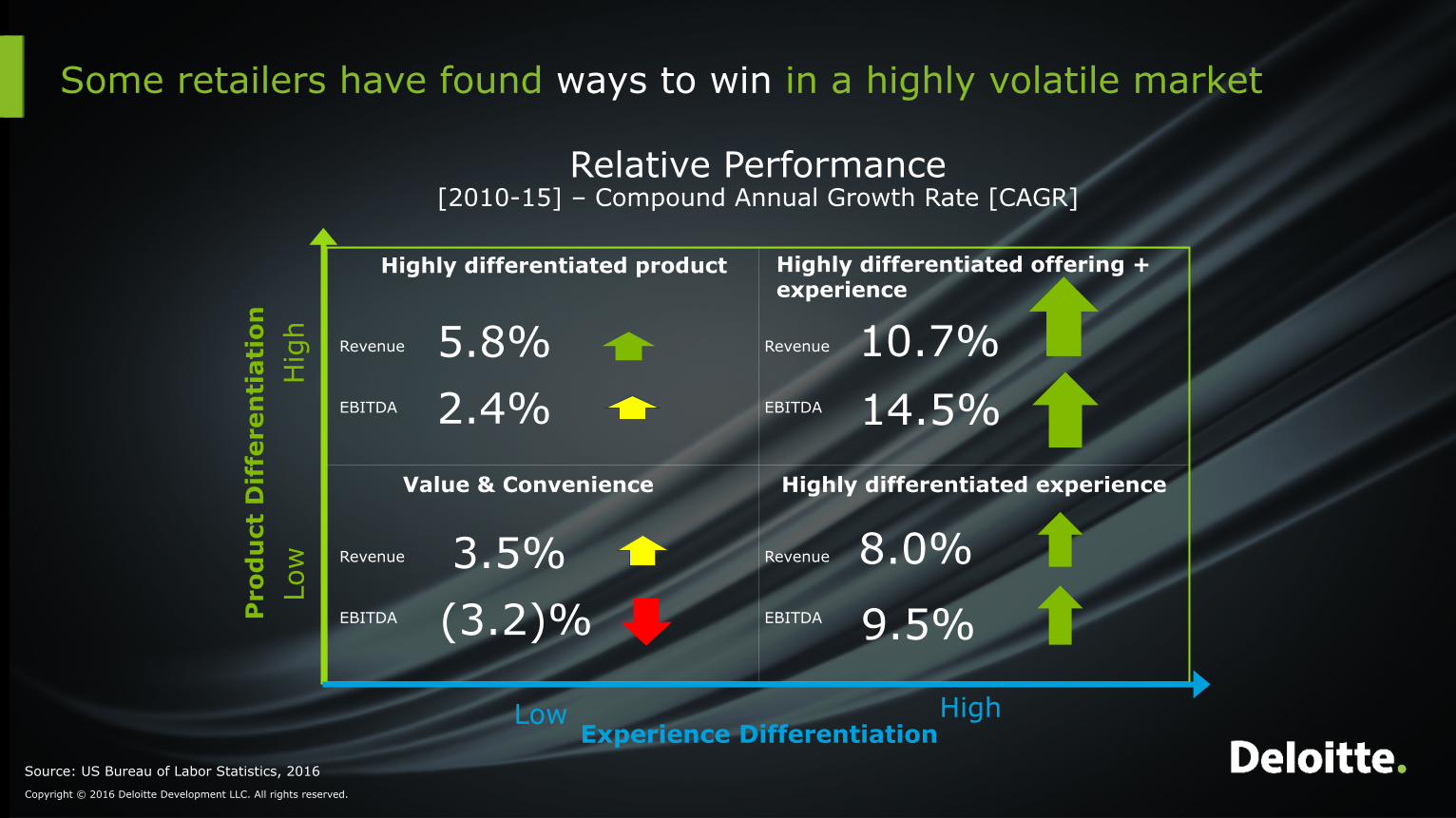

Some retailers have found ways to win in a highly volatile market

10.7%

Relative Performance [2010-15] – Compound Annual Growth Rate [CAGR]

Experience Differentiation

Pro

du

ct D

iffe

ren

tiat

ion

Low High

Low

H

igh

Value & Convenience

Highly differentiated product

Highly differentiated experience

Highly differentiated offering + experience

5.8%

3.5% 8.0%

Source: US Bureau of Labor Statistics, 2016

2.4% 14.5%

(3.2)% 9.5%

Revenue

EBITDA

Revenue

EBITDA

Revenue

EBITDA

Revenue

EBITDA

Copyright © 2016 Deloitte Development LLC. All rights reserved.

QuesOonsfortheSpeaker?

Goto:www.pollev.com/ultaretailortextultaretailto22333