Embed Size (px)

Citation preview

8/7/2019 business risk report

http://slidepdf.com/reader/full/-business-risk-report 1/8

01

01

Business Risk ReportA survey on nancial market risks for UK businesses

September 2010 | 3rd Edition

PRINT EXIT NEXT PAGE

8/7/2019 business risk report

http://slidepdf.com/reader/full/-business-risk-report 2/8

02

Business Risk Report | Sept 2010

Business condence appears to be improving which implies that

the economy is recovering at a moderate pace. Nevertheless,we feel that it is important to keep clients abreast with the latest

insight into UK companies’ approach to risk management.

This 3rd edition continues to focus on the impact of key asset

classes – interest rates, commodities, ination and FX – on UK

businesses. We have also broken our results down by industry to

provide an additional level of analysis.

Although the economic recovery is expected to continue,

companies remained cautious about hiring and capital

expenditure. Business owners were more concerned about the

impact on their business from interest rate volatility, ination and

commodity prices than six months ago. Yet, despite this anxiety,more than 80% of companies had no hedging strategies in place

to mitigate against nancial market risks.

This report also highlights that companies with larger turnover

(above £25m) tended to have more hedging strategies in place

for nancial market risks. This may reect the fact that larger

companies are more likely to be exposed to such risks or that the

potential benets from hedging outweigh the costs.

The main reasons cited by those companies that did not hedge

against nancial market risks was that it was considered that

the risks were either not applicable to their business or were not

considered by companies to be signicant enough. It is here that

our expertise can really add value in our role in exploring ideas

with you in risk mitigation. Building a trusted risk advisory capacity

for our customers is key for us so we can provide alternative

ideas for you in expert advice and tailored risk managementsolutions. Our aim is to help companies to better weigh the costs

versus the benets of hedging. In this way, companies can ensure

they are adequately covered against the risks that may threaten

the nancial performance of their businesses.

With this in mind, I hope the Business Risk Report serves as

a useful reminder about the importance of pro-active risk

management strategies and helps to ll any potential knowledge

gap that companies have.

Clare Francis

Managing Director andHead of Sales and Derivatives Structuring,

Lloyds Banking Group

Welcome to the third editionof our Business Risk Report,which gauges both theattitudes and hedgingapproaches of UK businessesto nancial market risks.

Contents

03 The overall picture

04 Businesses’ perception of risk

05 Analysis by industry sector

08 Contact us

Introduction

PRINT EXIT PREVIOUS PAGE NEXT PAGE

8/7/2019 business risk report

http://slidepdf.com/reader/full/-business-risk-report 3/8

03

Business Risk Report | Sept 2010

Business condence increased for the third consecutive survey, up 2 points to 18 and well

above the low of -32 at the end of 2008. However, it remains slightly below the long-term

average of 22, implying a relatively moderate pace of recovery.

Our business condence index is a forward-looking indicator, reecting expectations of sales

(turnover), order book levels and prots, which are anticipated to improve in the next six

months. The condence index correctly anticipated both the onset of the recession in mid-2008

and its exit at the end of 2009, and indicates that the recovery will continue in the second half

of this year, albeit at a relatively restrained pace.

The overall pictureOur business condence index suggests the economic recovery remains on track

Business condence index

0

-10

-20

-30

-40

40

30

20

10

50

2006 H1 2006 H2 2007 H1 2007 H2 2008 H1 2008 H2 2009 H1 2009 H2 2010 H1 2010 H2

Index Recession

Forward-looking business confidence index

Companies are beneting from strong external demand. In the rst half of the year,

the export sales balance rose to 20%, exceeding the total sales balance of 3%. Further

improvements are expected in the second half of the year.

A key takeaway from the latest survey is that companies

with greater exposure to external demand tended to be more positive about prospects than

those more reliant on domestic demand. Indeed, companies cited weak domestic demand

as the biggest threat to their business in the next six

months. Although the economic recovery is expected to continue, companies remained

cautious about hiring and capital expenditure.

Total sales

Export sales

% balance Recession

Total and export sales

0

-10

-20

-30

-40

40

30

20

10

50

2006 H1 2006 H2 2007 H1 2007 H2 2008 H1 2008 H2 2009 H1 2009 H2 2010 H1 2010 H2(e)

Companies benet from strong external sales

PRINT EXIT PREVIOUS PAGE NEXT PAGE

8/7/2019 business risk report

http://slidepdf.com/reader/full/-business-risk-report 4/8

04

Business Risk Report | Sept 2010

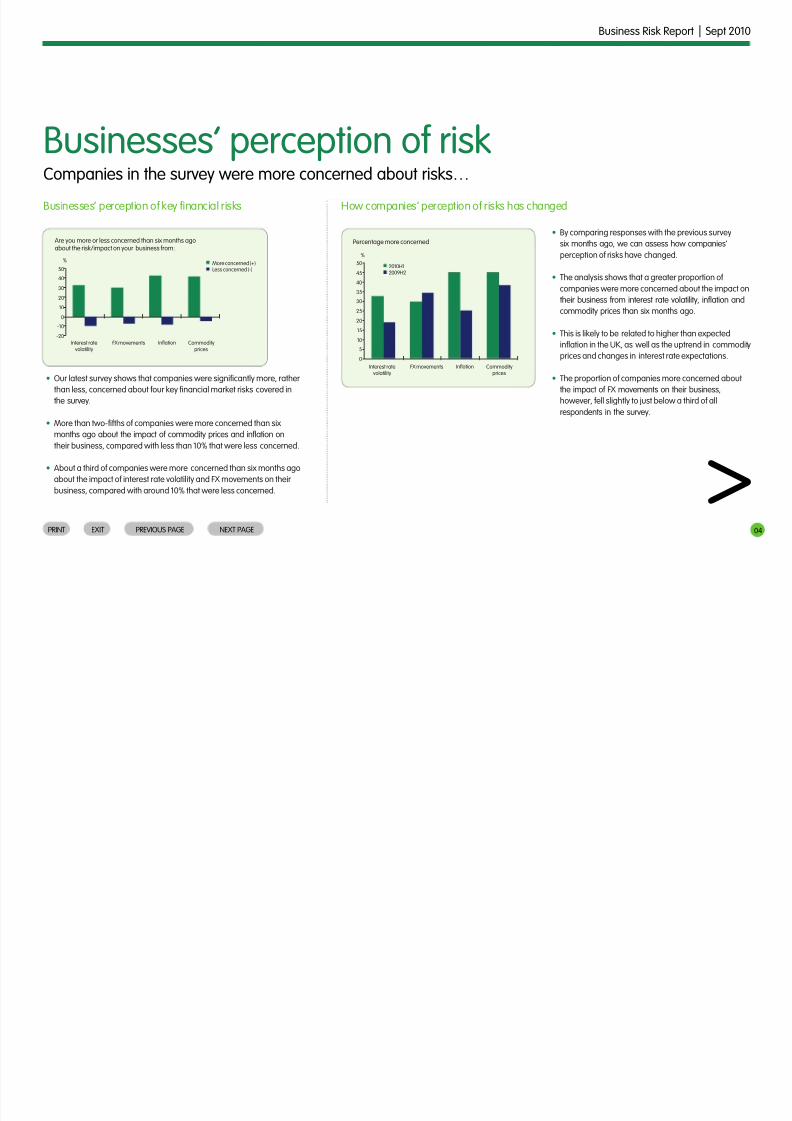

Companies in the survey were more concerned about risks…

Businesses’ perception of key nancial risks How companies’ perception of risks has changed

• Our latest survey shows that companies were signicantly more, rather

than less, concerned about four key nancial market risks covered in

the survey.

• More than two-fths of companies were more concerned than six

months ago about the impact of commodity prices and ination on

their business, compared with less than 10% that were less concerned.

• About a third of companies were more concerned than six months ago

about the impact of interest rate volatility and FX movements on their

business, compared with around 10% that were less concerned.

• By comparing responses with the previous survey

six months ago, we can assess how companies’

perception of risks have changed.

• The analysis shows that a greater proportion of companies were more concerned about the impact on

their business from interest rate volatility, ination and

commodity prices than six months ago.

• This is likely to be related to higher than expected

ination in the UK, as well as the uptrend in commodity

prices and changes in interest rate expectations.

• The proportion of companies more concerned about

the impact of FX movements on their business,

however, fell slightly to just below a third of all

respondents in the survey.

Businesses’ perception of risk

More concerned (+)Less concerned (-)

%

Are you more or less concerned than six months agoabout the risk/impact on your business from:

Interest ratevolatility

FX movements Inflation Commodityprices

0

-10

-20

40

30

20

10

502010H12009H2

%

Percentage more concerned

Interest ratevolatility

FX movements Inflation Commodityprices

10

5

0

30

25

20

15

35

40

45

50

>PRINT EXIT PREVIOUS PAGE NEXT PAGE

8/7/2019 business risk report

http://slidepdf.com/reader/full/-business-risk-report 5/8

05

Business Risk Report | Sept 2010

• Our survey shows that the proportion of companies with hedging strategies in place to

protect against nancial market risks is relatively low at around 10%. In contrast, more than

80% of companies had no hedging strategies in place.

• Companies with larger turnover tended to have more hedging strategies in place for nancial

market risks. This may reect the fact that larger companies are more likely to be exposed tosuch risks or that the potential benets from hedging outweigh the costs.

• Nearly half of companies with turnover above £25m have a hedging strategy in place for FX

risks and nearly a third have insured against commodity price risks.

• A quarter of companies with turnover above £25m have a hedging strategy in place for

interest rate risks, while about one in ten have insured against ination risks.

• Of companies that did not hedge against nancial risks, nearly three-quarters indicated that the

risks were either not applicable to their business or were not considered by companies to be

signicant enough.

• Most of the remaining companies that did not hedge indicated that it was due to costs or a lackof knowledge of hedging products.

All companiesTurnover above £25m

% yes

Hedging strategies in place

Interest rates FX Inflation Commodityprices

10

0

40

30

20

50

60

%

Why do companies not hedge?

Notapplicable to

buiness

Notconsideredsignificantenought

Cos ts L ack of knowledge

Other

10

5

0

30

25

20

15

35

40

45

...But hedging ratios remain lowAnalysis by industry sector

PRINT EXIT PREVIOUS PAGE NEXT PAGE

8/7/2019 business risk report

http://slidepdf.com/reader/full/-business-risk-report 6/8

06

Business Risk Report | Sept 2010

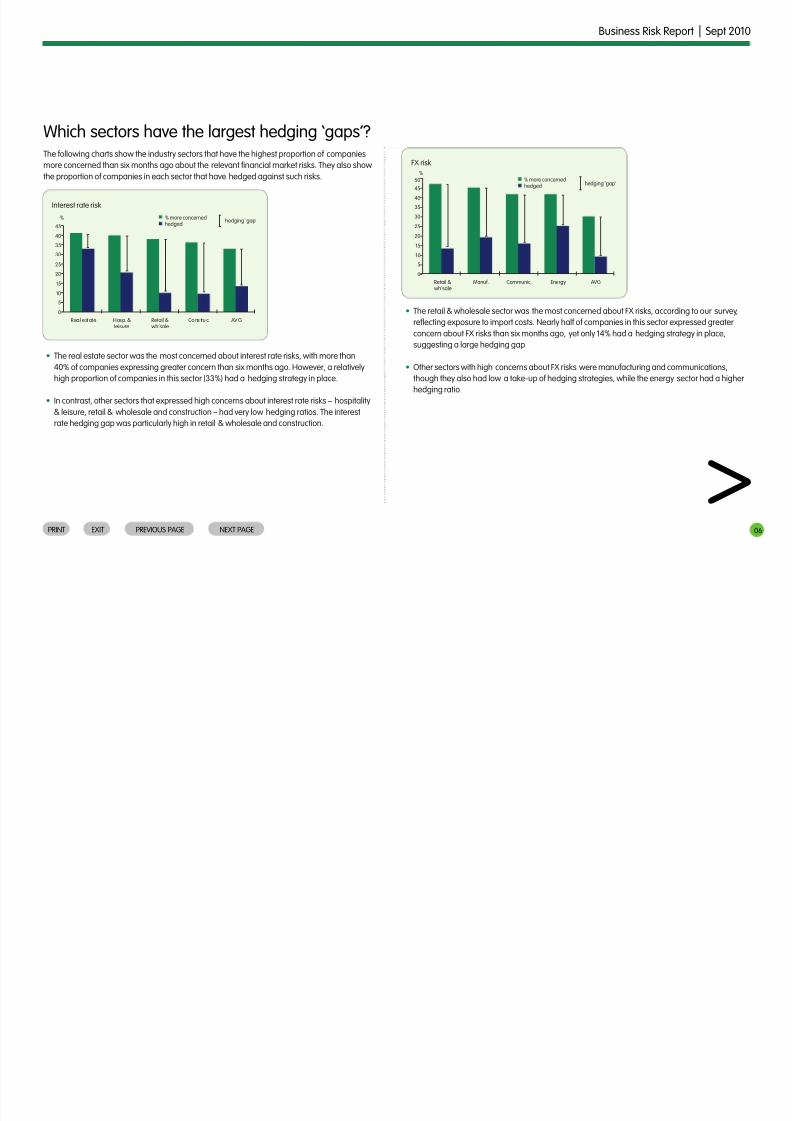

• The real estate sector was the most concerned about interest rate risks, with more than

40% of companies expressing greater concern than six months ago. However, a relatively

high proportion of companies in this sector (33%) had a hedging strategy in place.

• In contrast, other sectors that expressed high concerns about interest rate risks – hospitality

& leisure, retail & wholesale and construction – had very low hedging ratios. The interestrate hedging gap was particularly high in retail & wholesale and construction.

The following charts show the industry sectors that have the highest proportion of companies

more concerned than six months ago about the relevant nancial market risks. They also show

the proportion of companies in each sector that have hedged against such risks.

• The retail & wholesale sector was the most concerned about FX risks, according to our survey,

reecting exposure to import costs. Nearly half of companies in this sector expressed greater

concern about FX risks than six months ago, yet only 14% had a hedging strategy in place,

suggesting a large hedging gap.

• Other sectors with high concerns about FX risks were manufacturing and communications,

though they also had low a take-up of hedging strategies, while the energy sector had a higher

hedging ratio.

Which sectors have the largest hedging ‘gaps’?

>

%

Interest rate risk

Real estate Hosp. &leisure

Retail &wh’sale

Co ns tru c. AV G

10

5

0

30

25

2015

35

40

45

% more concernedhedged

hedging ‘gap’

%

FX risk

Retail &wh’sale

Manuf. Communic. Energy AVG

10

5

0

30

25

20

15

35

40

45

50 % more concernedhedged hedging ‘gap’

PRINT EXIT PREVIOUS PAGE NEXT PAGE

8/7/2019 business risk report

http://slidepdf.com/reader/full/-business-risk-report 7/8

07

Business Risk Report | Sept 2010

• On average, less than 10% of companies in our survey had a hedging strategy in place for

ination risks. The public sector had the highest hedging ratio at 12%.

• The sectors with the highest share of companies indicating more concern about ination

risks than six months ago were transport, healthcare, hospitality & leisure and construction

– about half of companies in those sectors were more concerned. Yet, hedging ratios were

very low, particularly in healthcare and construction at 5% and 6%, respectively.

• The manufacturing sector was the most concerned about commodity price risks, with nearly

two-thirds of companies more concerned than six months ago. Although the sector had the

highest hedging ratio (22%), the hedging gap was signicant.

• Construction, retail & wholesale and transport were sectors also particularly concerned about

commodity price risks, with about half of companies expressing concerns. However, hedging

ratios were only just above 10%.

Inflation risk

Transport Healthcare Hosp. &leisure

Construc. AVG

10

0

40

30

20

50

60% more concerned% hedged

hedging ‘gap’

Commodity price risk

Ma nuf . C ons tru c. R et ai l &wh’sale

Con st ruc . AV G

10

0

40

30

20

50

60

70% more concerned% hedged

hedging ‘gap’

PRINT EXIT PREVIOUS PAGE NEXT PAGE

8/7/2019 business risk report

http://slidepdf.com/reader/full/-business-risk-report 8/8

08

Business Risk Report | Sept 2010

About us Contact usLloyds TSB Corporate Markets’ Economic Research team

works in tandem with relationship and nancial markets

teams to provide analysis of issues impacting the economy

and business areas its customers operate in. The mission

of the team is to add value to customers, through superior

economic analysis and insightful research into nancial

markets and industrial sectors.

Our Financial Markets team provides solutions tobusinesses of varying size – from commercial through

to global corporations and nancial institutions. The

complexities of today’s volatile nancial markets mean

that businesses have an even greater need for a risk

management partner. Our Financial Markets experts take

a consultative approach and can provide you with a risk

strategy that includes FX, Ination, Interest Rates and

Commodity Solutions.

Sales and Derivatives Structuring

For information on how we can help you with yourrisk management strategies:

Kathryn Ball, Head of Large Corporate, Wholesale Markets

Email: [email protected]

Tel: 020 7158 1672

Matthew Lawrence, Head of Commercial, Wholesale Markets

Email: [email protected]

Tel: 020 7158 1661

Economic Research can be accessed online at:

lloydstsb.com/corporatemarkets

Business Risk Report is based on the responses of 2,386

companies surveyed via Lloyds TSB Commercial Business in Britain

June 2010 questionnaire.

Economic Research

More detailed analysis is availableon request from the author:

Hann-Ju Ho, Head of Sector Economics, Lloyds TSB Corporate

Markets Economic Research.

Email: [email protected]

Tel: 020 7158 1745

For additional copies of the Business Risk Report and queries:

Email: nancialmarketsdivision.economicresearch@

lloydsbanking.com

Lloyds TSB Corporate Markets is a trading name of Lloyds TSB Bank plc and Lloyds TSB Scotland plc. Lloyds TSB Bank plc. Registered Ofce: 25 Gresham Street,London EC2V 7HN. Registered in England and Wales no 2065. Lloyds TSB Scotland plc. Registered Ofce: Henry Duncan House, 120 George Street, Edinburgh EH2 4LHRegistered in Scotland no: 95237. Authorised and regulated by the Financial Services Authority.

Bank of the Year and Advisor of the year 2005, 2006, 2007, 2008, 2009 and 2010.

PRINT EXIT PREVIOUS PAGE