Embed Size (px)

Citation preview

c o n s o r t i u m

ALFA-GROUP

w w w . a l f a g r o u p . r u

w w w . a l f a g r o u p . o r g

A n n u a l R e p o r t

2 0 0 1

CONTENTS

S C S B D ......................

A G F H ..................................................................................

F R S D G......................................

A G’ I P .........................................................................

S B D ..................................................................................

A G’ C C ..................................................................................

A G’ P H ................................................................................

F S – Alfa Bank Group, AlfaInsurance............................................

O P – Tyumen Oil Company, SIDANCO Oil Company ......................

C T – Crown Resources AG, Alfa-Eco Group ............................

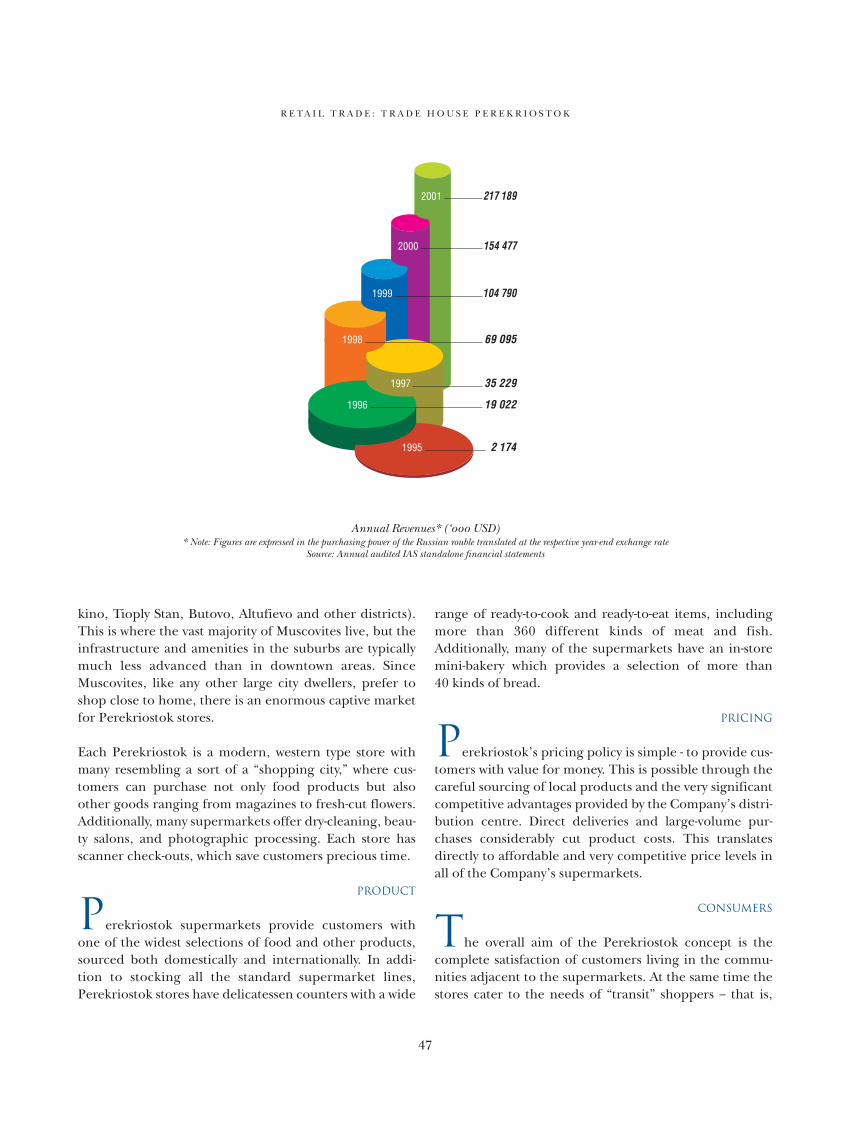

R T – Trade House Perekriostok ..............................................................

F P – United Food Company ..............................................................

T – Golden Telecom Inc, VimpelCom ....................................

S O C..............................................................................................

C I......................................................................................................

C F S G

R A ..........................................................................................

Alfa Group Consortium

Founded in , Alfa Group Consortium is one of Russia’s largest privatelyowned financial-industrial conglomerates with interests in oil, commodities trad-ing, commercial and investment banking, insurance, retail trade, food processing,and telecommunications. The Group typically focuses on value-oriented, longer-term opportunities, primarily in Russia and the CIS, but also invests in other mar-kets which form part of the Group's strategic business objectives.

We ArE leading...by example

As one of the leading financial-industrial groups in Russia, and as one of the largest

investors into emerging markets in the world, Alfa Group, its companies, and its people are

recognised by prestigious independent organisations and the media as leaders in their

industries. Following is a selection of some of this recognition:

A S C TNK: Philip B. Crosby Medallion for Entrepreneurial Leadership

A M K P H “ Most Professional Managers in Russia” () (No. ) Mikhail Fridman, Chairman of

the Supervisory Board of Directors of Alfa Group; (No. ) Pyotr Aven, President of Alfa Bank

Group; (No. ) German Khan, Deputy Chairman of Management Board and Executive

Director of TNK; (No. ) Leonard Vid, Chairman of the Executive Board of Alfa Bank Group

C LAlfaInsurance: st Place, “Best Creative Idea for a Television Commercial” ()

C Joseph Bakaleinik, CFO of TNK: “Best CFO in Russia” ()

E A VimpelCom’s “BeeLine GSM”: “Brand of the Year – Russia” ()

E M I Alfa Bank: “Best Domestic Bank” ()

E Alfa Bank: “Highly Commended Bank – Russia” (), “Best Bank in Russia” ()

E’ C E Alfa Bank: “Best Bank in Russia” (, , , )

E (A B A R) Alfa Group: nd Place, “Internet Presentation” ()

Alfa Bank: st Place, “Classic Genre” (), st Place, “Richness of Information” (),

st Place, “Internet Presentation” (), st Place, “Richness of Information” (),

nd Place, “Design and Printing” ()

F T - E TNK: “Worlds Best Oil and Gas Company” ()

G F Alfa Bank: “Best Russian Domestic Bank” (, , , )

Alfa Bank: “Best Russian Trade Finance Bank” (, )

I C G VimpelCom: Highest Overall Corporate Governance Rating for a Russian Company

(, , )

I E S E S Alfa Bank: st Place, “Leading Russian Companies” ()

AlfaInsurance: rd Place, “Leading Russian Insurance Companies” ()

I A B CPerekriostok: st Place, “Golden Net – Foodstuffs” ()

TNK: st Place, “Golden Net – Petrol Stations” ()

I B I F Alfa-Eco: Gold Medal for Cognac; Bronze Medals for Smirnov vodka and Armina

Star Brandy ()

I Alfa Bank: st Place, “Best Bank Web-sites” ()

K TNK: “Best Fuel and Energy Company” ()

VimpelCom: “Best Telecommunications Company” ()

Josef Bakaleinik, CEO of TNK: “Best Financial Manager” ()

Evgeny Bernshtam, First Deputy Chairman of the Management Board of Alfa

Bank: “Best Manager – Finance Sector” ()

Alex Knaster, CEO of Alfa Bank: “Best Manager – Finance Sector” ()

Simon Kukes, President of TNK: “Best Manager – Oil & Gas Sector” (, )

Jo Lunder, President and COO of VimpelCom: “Best Manager – Retail and

Distribution” ()

Stewart Reich, CEO of Golden Telecom Inc :“Best Manager – Telecommunications” ()

M “Top Managers in Russia” () (No. ) Mikhail Fridman, Chairman of the

Supervisory Board of Directors of Alfa Group; (No. ) Alexander Fain, General

Director of Alfa-Eco Group; (No. ) German Khan, Deputy Chairman of

Management Board and Executive Director of TNK;

(No. ) Simon Kukes, President of TNK;

(No. ) Jo Lunder, President and COO of VimpelCom

N A S M P (NAUFOR) S M E A Alfa Bank: “Best Credit Institution” ()

N T A Perekriostok:“Best Trading Chain” ()

P D P RF, V P Leonard Vid, Chairman of the Executive Board of AlfaBank Group: “Order of

Honour of Achievements, Contributions and Long-term Conscientious Work in the Area of

Promoting Friendship and Co-operation Between Nations” ()

RBC VimpelCom: “Best Service Company” ()

S & P’ Alfa Bank: “Best Outlook of All Rated Banks in Russia” ()

S C S R F TNK’s ecologically friendly high-octane gasoline :

“ Best Russian Products” ()

T B Alfa Bank: “Bank of the Year – Russia” ()

U E Alexander Fain, General Director of Alfa-Eco Group:

“Best Entrepreneur of the Decade – Trading Activities” ()

STATEMENT BY THE CHAIRMAN OF THE SUPERVISORY BOARD OF DIRECTORSO ver the past year, the inevitable trend of Russia’s integration into the world

economy continued with increasing momentum. Russia and the west moved closer

together, finding common ground on various important issues. International sov-

ereign and corporate credit ratings continued to rise for well-run Russian compa-

nies providing them with increasing access to international capital markets and pri-

vate investment. In an uneven year for the world’s economies and stock markets,

Russia’s economy expanded and its stock markets thrived - with the exception of

the Chinese Shanghai B Index, Russia equities recorded the best US dollar return

of all emerging markets during 2001.

Alfa Group Consortium participated fully in these positive developments, with 2001

marking our second most profitable year ever with consolidated Group net profits of

US $797 million and correspondingly, our highest-ever consolidated Group sharehold-

ers’ equity of US $1.74 billion at 31 December 2001.

In the second half of 2001 we made our first significant investments into the “new

economy,” through the purchase of large stakes in US-listed Golden Telecom and

VimpelCom, on our belief that certain telecommunications shares in Russia, having

fallen in sympathy with battered world shares of technology and telecommunications

companies, offered compelling value. Although it’s early, and we expect a great deal of

value generation for the Group in the years to come, since making our initial invest-

ment a little more than one year ago, Golden Telecom’s ADR share price has risen by

18% and VimpelCom’s ADR share price has risen by 58% from our entry prices,

through the end of September 2002. In July 2002, we made further investment into

telecommunications by purchasing 16.2% of Kyivstar, Ukraine’s largest cellular com-

munication company, for US $66.5 million.

Despite tough world-wide credit conditions during the latter half of 2001 and through-

out 2002, improving fundamentals in our companies have helped us to attract longer

and more stable financing and investment. Notably, VimpelCom floated US $250 mil-

STATEMENT BY THE CHAIRMANOF THE SUPERVISORY BOARD

OF DIRECTORS

S T A T E M E N T B Y T H E C H A I R M A N O F T H E S U P E R V I S O R Y B O A R D O F D I R E C T O R S

lion in three year Eurobonds. Additionally, TNK and Alfa Bank are actively considering

possible medium-term Eurobond offerings.

Also, during 2002, we made two key sales of our investments – in September 2002 we

entered into agreements to sell the full interest in our food processing business, United

Food Company to a strategic investor for US $80 million and in April 2002 we further

strengthened our co-operation with British Petroleum through the sale of a 15% stake

in oil and gas company, SIDANCO for US $375 million.

On the belief that re-investment of our profits is the best and highest use of our capital,

we continued to re-invest large portions of profit back into all of our companies, pay-

ing out 12% of year 2000 net profits as dividends and a minimal amount of 2001 net

profits as dividends. In addition, we injected fresh capital into three of our businesses

during 2001 and 2002 – US $56.4 million into Alfa Bank, US $12.2 million into Alfa-Eco,

and committed to funding of US $30 million for Perekriostok.

As we move beyond 2002 it is clear to us that the consolidation of assets in the Russian

marketplace will continue with the increasing participation of foreign investors. It fol-

lows, that the ability to co-operate successfully with foreign partners will become an

increasingly critical factor in determining the future success of Russian financial-indus-

trial conglomerates. We believe that the strength and depth of the management at our

companies, our strong leadership position and reputation on the marketplace, our

demonstrated commitment to the highest levels of transparency and governance prin-

ciples, and our already extensive and successful co-operation with foreign partners

place us in an advantageous position to fully avail ourselves of the most interesting

opportunities which will present themselves.

I wish to express my personal appreciation to all of our clients and business partners

whose continued confidence and support are key to our growth and profitability.

I would also like to thank our employees whose professionalism, dedication and ability

to meet the tough challenges we set for them, have made us all proud.

Mikhail Fridman

8 October 2002

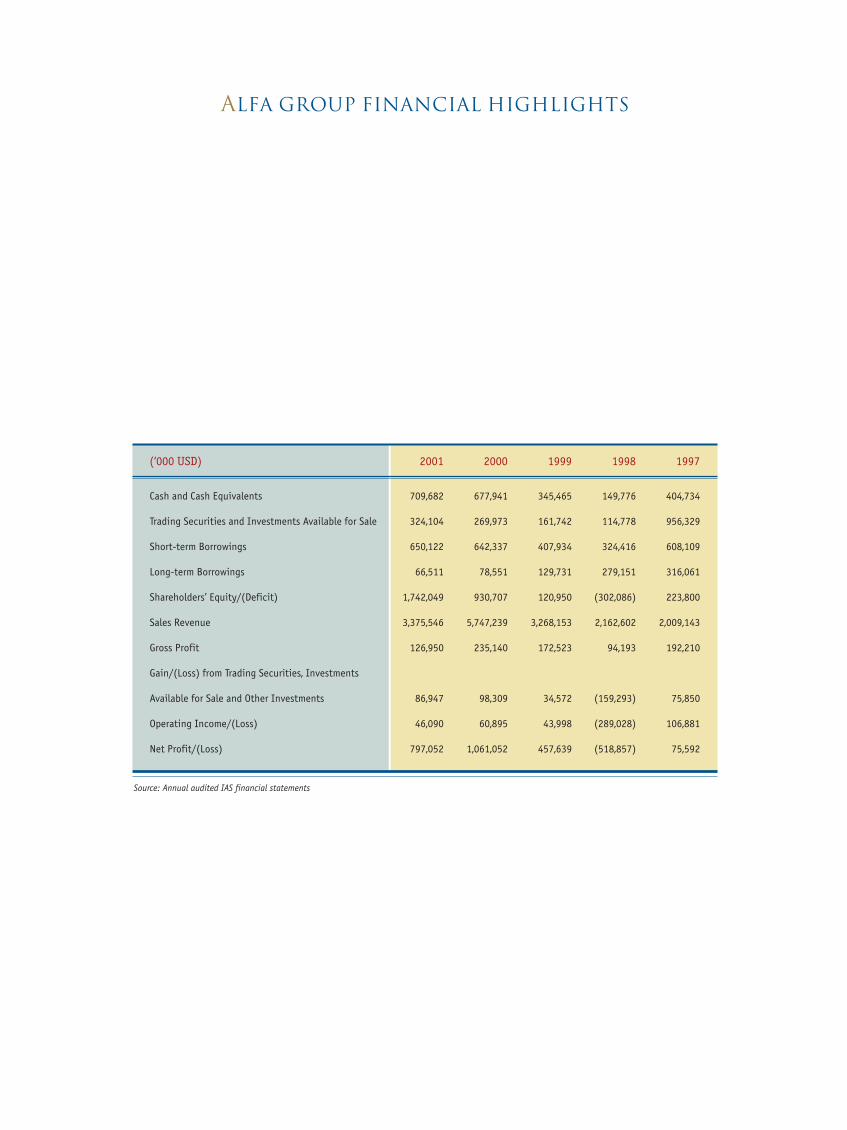

Cash and Cash Equivalents 709,682 677,941 345,465 149,776 404,734

Trading Securities and Investments Available for Sale 324,104 269,973 161,742 114,778 956,329

Short-term Borrowings 650,122 642,337 407,934 324,416 608,109

Long-term Borrowings 66,511 78,551 129,731 279,151 316,061

Shareholders’ Equity/(Deficit) 1,742,049 930,707 120,950 (302,086) 223,800

Sales Revenue 3,375,546 5,747,239 3,268,153 2,162,602 2,009,143

Gross Profit 126,950 235,140 172,523 94,193 192,210

Gain/(Loss) from Trading Securities, Investments

Available for Sale and Other Investments 86,947 98,309 34,572 (159,293) 75,850

Operating Income/(Loss) 46,090 60,895 43,998 (289,028) 106,881

Net Profit/(Loss) 797,052 1,061,052 457,639 (518,857) 75,592

(‘000 USD) 2001 2000 1999 1998 1997

ALFA GROUP FINANCIAL HIGHLIGHTS

Source: Annual audited IAS financial statements

Overall Analysis of the Group’s

Financial Results for 2001

2001 was another very strong year for AlfaGroup. In fact, 2001, marked the second most prof-itable year in our history. Net Profit for 2001 was US$797 million as compared with US $1.06 billion in 2000,with the largest part of this decline attributable to a fallin world oil and gas prices which directly impacted onthe profitability of our oil and gas production assets.At 31 December 2001, consolidated shareholders’ equi-ty for the Group rose to an unprecedented high ofUS $1.74 billion, a year-on-year increase of 87%. Returnon shareholders’ equity for 2001 was 60% while returnon assets was 18%.

We continued to fortify our balance sheet with a year-on-year reduction in debt levels. The ratio of debt to share-holders’ equity fell to 0.41 at the end of 2001 from 0.77 atthe end of 2000, and the ratio of debt to assets fell to 0.14at the end of 2001 from 0.19 at the end of 2000.

The strengthening of our balance sheet gives us an evenstronger financial flexibility to be opportunistic in pursu-ing strategic acquisitions and internal investment oppor-tunities.

Analysis of the Group’s Financial Results

by Industry Segment for 2001

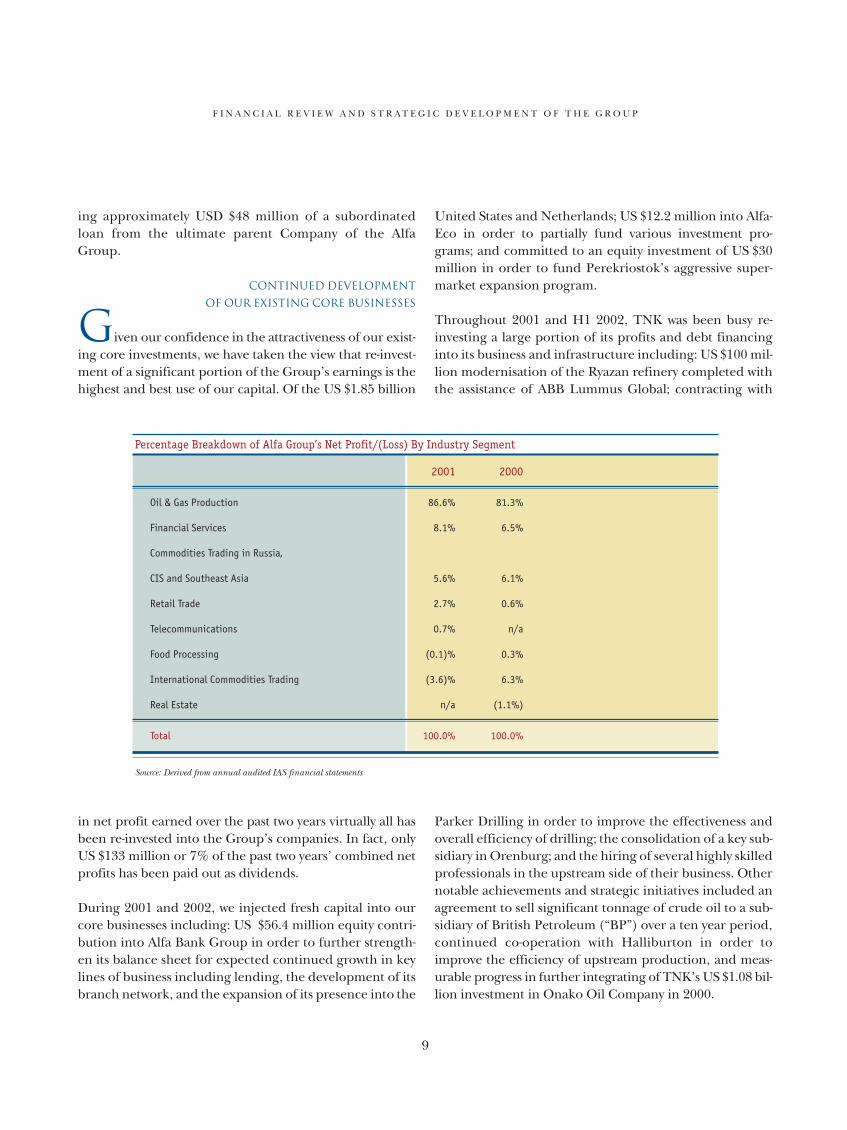

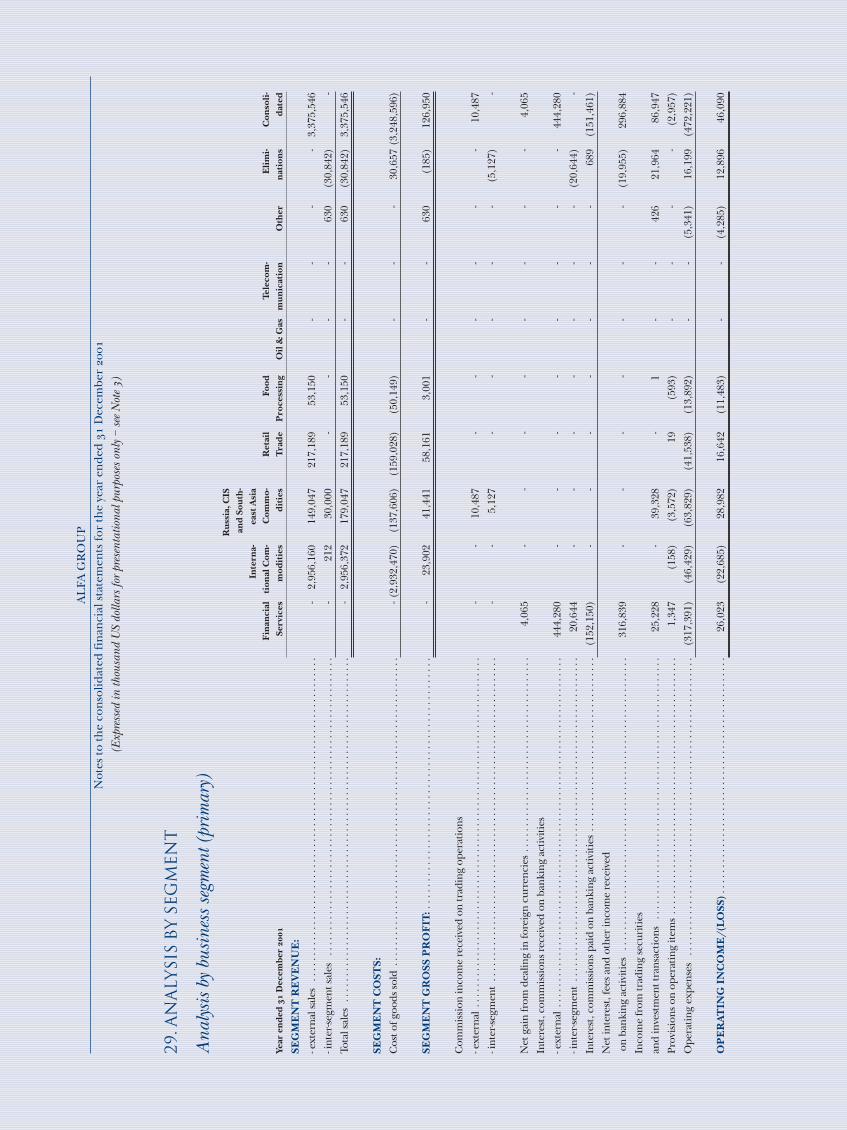

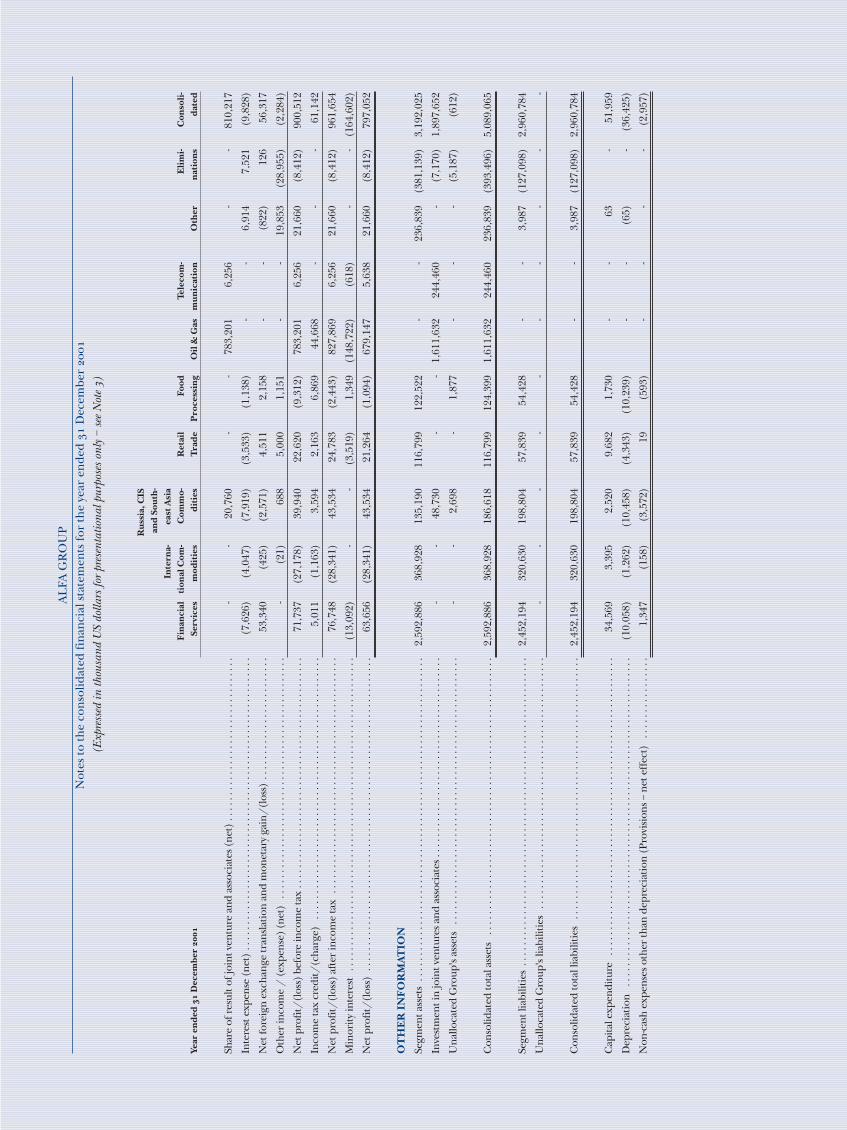

Five of the Group’s seven different business segmentscontributed positively to the 2001 Group net profit ofUS $797 million (see table on page 9). As was the case in2000, the major portion of the Group’s net profit wasderived from the Group’s investment in oil and gas assets,by virtue of our investment in TNK and SIDANCO. Lastyear in these pages, we acknowledged our large invest-ment exposure to oil and gas. We continue to carry thisexposure and it is an exposure with which we continue tofeel comfortable because of: 1) Our perception of thefavourable risk-to-reward ratio of Russian oil and gasassets; 2) The diversification efforts which have beenundertaken by the Group in the past two years, primarilyinto telecommunications; and 3) The continued andgrowing strategic importance of other industry segmentsof the Group.

Our financial services segment (comprising both AlfaBank Group which enjoyed record net profits during2001, and AlfaInsurance) contributed the next largestamount to Group net profit, followed by the segment ofcommodities trading in Russia, CIS and Southeast Asia(Alfa-Eco Group). Retail trade (Trade HousePerekriostok), one of the faster growing sectors in theGroup, while contributing a relatively small amount toGroup net profit in 2001, nevertheless more than tripledits net profits, as compared with 2000. The impact oftelecommunications assets (Golden Telecom Inc,VimpelCom and VimpelCom-R), the newest segment forthe Group, also contributed positively, albeit modestly,to net profits during 2001 as these assets were acquiredin the second half of 2001. Although Perekriostok,Golden Telecom and VimpelCom had relatively minorcontributions to net profits in 2001, we expect this con-tribution to increase on a relative basis as our relativelylarge, recent capital investment into these companiesbegins to pay off.

The two segments posting negative results for 2001 werefood processing (United Food Company), a growing busi-ness, which registered a small loss in 2001 and interna-tional commodities trading (Crown Resources AG).

The loss in our international commodities trading seg-ment was the result of a combination of several factorsincluding unfavourable market conditions, price volatil-ity resulting from the tragic events in the United Stateson 11 September, pre-merger costs from the failed merg-er with Marc Rich Investments, as well as significantinvestment costs relating to the expansion of theCompany’s trading activities. After posting excellentresults in 2000, Crown’s 2001 results were quite disap-pointing to us, and we have quickly taken a series ofexplicit measures to remedy the situation. Since early2002, the Company has undergone significant internalrestructuring which includes a new senior managementteam and the reorganisation of trading activities to focuson core activities and overhead infrastructure costs.Whilst the impact of these measures will be marginal in2002, we expect that they will create a strong base for theCompany moving into 2003. To demonstrate its commit-ment to Crown in the transition period, the Group tooka decision to increase the Company’s equity by capitalis-

FINANCIAL REVIEW AND STRATEGIC DEVELOPMENT OF THE GROUP

ing approximately USD $48 million of a subordinatedloan from the ultimate parent Company of the AlfaGroup.

Continued Development

of Our Existing Core Businesses

Given our confidence in the attractiveness of our exist-ing core investments, we have taken the view that re-invest-ment of a significant portion of the Group’s earnings is thehighest and best use of our capital. Of the US $1.85 billion

in net profit earned over the past two years virtually all hasbeen re-invested into the Group’s companies. In fact, onlyUS $133 million or 7% of the past two years’ combined netprofits has been paid out as dividends.

During 2001 and 2002, we injected fresh capital into ourcore businesses including: US $56.4 million equity contri-bution into Alfa Bank Group in order to further strength-en its balance sheet for expected continued growth in keylines of business including lending, the development of itsbranch network, and the expansion of its presence into the

United States and Netherlands; US $12.2 million into Alfa-Eco in order to partially fund various investment pro-grams; and committed to an equity investment of US $30million in order to fund Perekriostok’s aggressive super-market expansion program.

Throughout 2001 and H1 2002, TNK was been busy re-investing a large portion of its profits and debt financinginto its business and infrastructure including: US $100 mil-lion modernisation of the Ryazan refinery completed withthe assistance of ABB Lummus Global; contracting with

Parker Drilling in order to improve the effectiveness andoverall efficiency of drilling; the consolidation of a key sub-sidiary in Orenburg; and the hiring of several highly skilledprofessionals in the upstream side of their business. Othernotable achievements and strategic initiatives included anagreement to sell significant tonnage of crude oil to a sub-sidiary of British Petroleum (“BP”) over a ten year period,continued co-operation with Halliburton in order toimprove the efficiency of upstream production, and meas-urable progress in further integrating of TNK’s US $1.08 bil-lion investment in Onako Oil Company in 2000.

F I N A N C I A L R E V I E W A N D S T R A T E G I C D E V E L O P M E N T O F T H E G R O U P

Oil & Gas Production 86.6% 81.3%

Financial Services 8.1% 6.5%

Commodities Trading in Russia,

CIS and Southeast Asia 5.6% 6.1%

Retail Trade 2.7% 0.6%

Telecommunications 0.7% n/a

Food Processing (0.1)% 0.3%

International Commodities Trading (3.6)% 6.3%

Real Estate n/a (1.1%)

Total 100.0% 100.0%

Source: Derived from annual audited IAS financial statements

2001 2000

Percentage Breakdown of Alfa Group’s Net Profit/(Loss) By Industry Segment

In June 2001, AlfaInsurance expanded its presence in theinsurance market by purchasing 98.1% of VESTA, one ofthe leading insurance companies in Russia, for US $6 mil-lion. Additionally, over the past 1.5 years, AlfaInsurancehas undertaken an aggressive expansion program andadvertising campaign which successfully leverages the“Alfa” name. Importantly, we have recently created andfilled a number of key management positions in anticipa-tion of the rapid growth in this industry.

Despite tough world-wide credit conditions VimpelComwas able to successfully access international debt marketsin April 2002, raising US $250 million in a three yearEurobond issue (yield 10.45%). Also, TNK and Alfa Bankare actively considering possible medium-term Eurobondofferings in the second half of 2002.

Disciplined InvestMENT Into New Businesses

During 2000 and 2001 the share prices ofRussian/CIS telecommunications companies fell in sym-pathy with stock prices of world technology and telecom-munications shares. Our belief that this fall in share priceswas not representative of the intrinsic value in these com-panies, coupled with our conviction that Russia/CIStelecommunications assets would experience tremendousgrowth over the next several years, convinced us thatassets in this sector represented a compelling value.

Our first investment into telecommunications wascompleted in March 2001 when we invested US $110million for a 43.8% stake of US-listed Golden TelecomInc, an integrated telecommunications and Internetcompany operating throughout Russia and the CIS. Weinvested alongside Baring Vostok Capital Partners,Capital International Inc, both investment managersof international private equity funds, and theEuropean Bank for Reconstruction and Development.Since our investment, through the end of September2002, Golden’s ADR share price has risen by 18%.Over the past 1.5 years, Golden has been busy pursuinga shareholder value enhancing strategy of optimisingits ownership in key operating subsidiaries for the pur-pose of consolidating tactical and strategic control. Inthis regard, Golden concluded a key deal in March2002 for the purchase of 50% of shares of Sovintel, aleading Russian telecommunications company, fromRostelecom, thereby raising Golden’s ownership inter-est to 100%.

In May 2001, Alfa-Eco Group completed a US $246.8 milliontransaction for a blocking voting stake (25% + 1 share) ofUS-listed VimpelCom and VimpelCom-Region, leadingproviders of wireless telecommunications services inMoscow and Russia’s regions. We invest alongside Telenor, aNorwegian telecommunications Group. Our investment isspecifically for the network build-out and infrastructuredevelopment in Russia’s regions. Since May 2001,VimpelCom-R has made notable progress expanding active-ly into Russia’s regions, having secured licenses to operatein Siberia, Volga River area, Central Russia, and theNorthern Caucuses, the rights to which cover 16 majorcities. VimpelCom’s ADR share price has risen by 58% sinceour initial investment through the end of September 2002.

In July 2002, we made further investment into telecommu-nications by purchasing 16.2% of Kyivstar for US $66.5 mil-lion. Kyivstar, having a subscriber base of more than 2.6 mil-lion users, is one of the largest cellular communicationsproviders in Ukraine. We believe that the Ukraine marketoffers strong growth opportunities as the rate of mobilepenetration is relatively low at 5.3% and expect the pene-tration rate to reach 16% by 2004.

Our three investments into Golden, VimpelCom andKyivstar make Alfa Group one of the most significant pri-vate investors into the telecommunications sector inRussia and CIS.

Apart from telecommunications, another major invest-ment in 2001 was made by Alfa-Eco Group, who togetherwith an equal joint-venture partner, acquired just under93% of Volga, the largest manufacturer of newsprint inRussia, for US $68.1 million.

Divestiture of Group Assets

and Other Transactions

From time to time, we take the decision to exit certainof our investments. As investors, divestiture allows us tofocus our resources and management attention on invest-ments of strategic relevance to the Group, and important-ly, realise profits from our efforts. We make these deci-sions, typically, for the following reasons:

• We no longer view the investment as strategic to theGroup;

• We have identified higher-return opportunities in otherindustry segments;

F I N A N C I A L R E V I E W A N D S T R A T E G I C D E V E L O P M E N T O F T H E G R O U P

F I N A N C I A L R E V I E W A N D S T R A T E G I C D E V E L O P M E N T O F T H E G R O U P

• We are able to exit our investment under terms which weconsider to be attractive

In mid-2001, after undertaking a critical review of the cur-rent competitive position of Alfa-Development, we took adecision that real estate investment and development wasnot strategic to the Group and should no longer form partof the Group’s core activities. Accordingly, it was decidedto liquidate Alfa-Development and transfer two of theuncompleted projects to Alfa Bank Group and sell theremaining project.

In August 2001 we reached a final, amicable settlementwith BP and other parties in the matters with respect toTNK-Nizhnevartovsk (formerly, Chernogorneft),SIDANCO’s main production subsidiary. TNK-Nizhnevartovsk was returned to SIDANCO and BP wasgiven day-to-day management control of SIDANCO for atleast a three year period. In April 2002, we furtherstrengthened our co-operation with BP through the saleof a 15% stake in SIDANCO for US $375 million, bringingBP’s total stake to 25% + 1 share. Together with our equaljoint venture partner, we control an approximate 57%stake in SIDANCO.

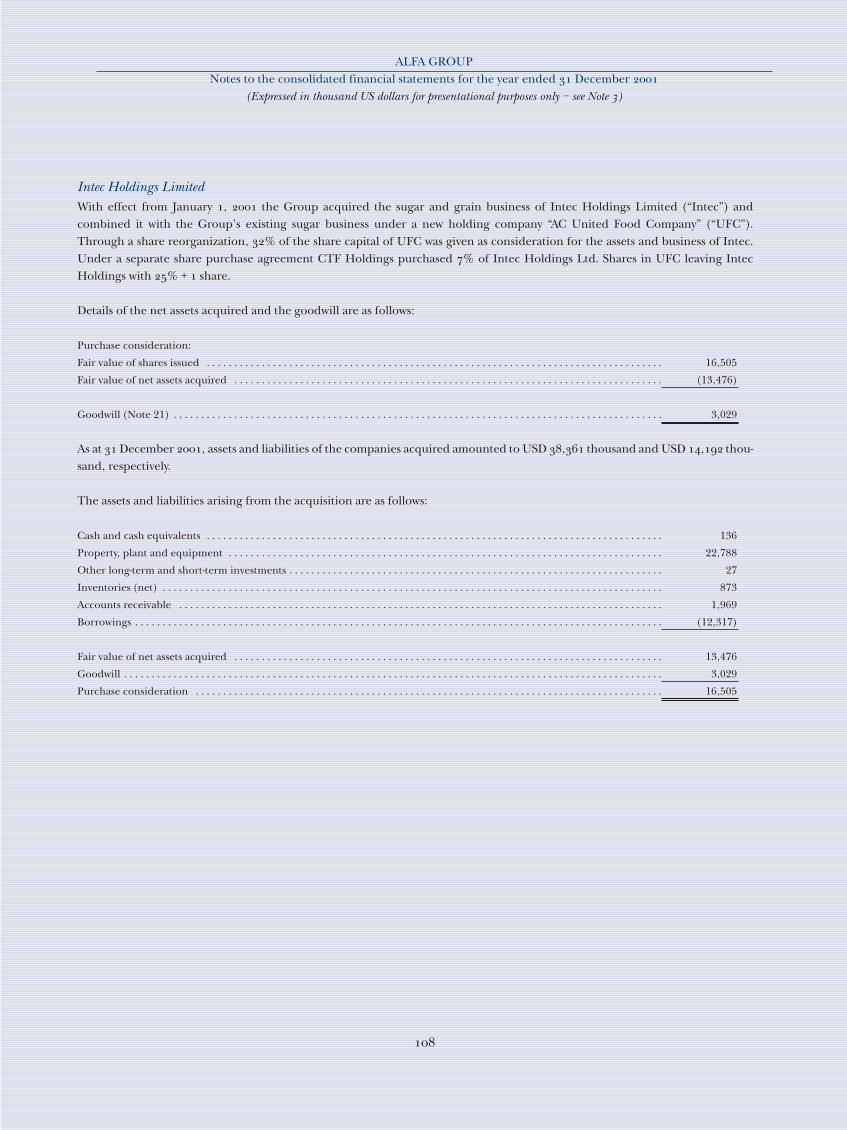

In April 2001, we merged our sugar business,Kubansakhar, with Intec Group’s sugar and grain busi-ness, creating United Food Company in order to takeadvantage of definite synergies between the companies.The merger gave us certain competitive advantages andunquestionably was a case where the whole was greaterthan the sum of the individual parts. In September 2002,after receiving multiple attractive offers for UFC fromstrategic investors and competitors, we took a decisionto sell our entire stake in UFC, by selling separately,

UFC’s sugar and the grain businesses to a private strate-gic investor for US $80 million.

Looking AHEAD

Moving beyond 2002, we see further consolidationof business in Russia and in the other emerging marketsin which we operate. To be sure, a good deal of this con-solidation will involve the participation of foreigninvestors. We have anticipated the current re-emergenceof foreign interest in Russia and the CIS and view co-operation with foreign investors as essential to thedevelopment of our companies and as a logical andattractive means of exiting our investments. It’s not acci-dental that our companies have a long history of co-operating extensively, and successfully with bothRussian and foreign partners.

There are three main factors which are responsible forour position on the marketplace today and we are certainthat these same three factors will continue to play an influ-ential role in our continued success:

• We are unyielding in our commitment to hiring the bestavailable professional talent;

• We steadfastly adhere to our investment philosophy(page 12-13);

• We have repeatedly demonstrated, through our actions,our strong commitment to the highest levels of trans-parency and governance principles.

Early indications suggest that 2002 promises to be anotherexcellent year. We remain confident in the long-term suc-cess of the Group and are making extensive preparationsto secure an even more successful future for the Group.

WE ARE OPPORTUNISTIC INVESTORS.

SIMPLY STATED, WE ARE VALUE-ORIENTED INVESTORS. IN EVALUATING ANY INVESTMENT

OPPORTUNITY, OUR INVESTMENT PHILOSOPHY IS DRIVEN BY THE OPPORTUNITY TO PUR-

CHASE ASSETS THAT, DUE TO PERCEIVED RISK, LOW LIQUIDITY, DISINTEREST OR A LACK OF

UNDERSTANDING ON THE PART OF MARKET PARTICIPANTS, ARE UNDERVALUED.

WE BELIEVE THE MOST ATTRACTIVE OPPORTUNITIES ARE IN WORLD EMERGING MARKETS.

MUCH OF OUR PAST SUCCESS HAS BEEN THE RESULT OF OUR INTIMATE KNOWLEDGE AND

UNDERSTANDING OF THE RUSSIAN AND CIS MARKETS. WE BELIEVE THERE ARE STILL SUBSTAN-

TIAL OPPORTUNITIES IN THESE EMERGING MARKETS AND THAT WE ARE WELL PLACED TO

TAKE FULL ADVANTAGE OF THEM.

WE ARE INTERESTED IN INVESTMENTS OVER WHICH WE CAN EXERCISE CONTROL.

WE MAKE INVESTMENTS ON THE BASIS THAT WE WILL HAVE EITHER MAJORITY OR JOINT CON-

TROL, THROUGH SHARE OWNERSHIP, BOARD REPRESENTATION, OR BOTH. NON-CONTROLLED

INVESTMENTS ARE NOT ATTRACTIVE TO US BECAUSE THE LACK OF CONTROL MAKES IT DIFFI-

CULT TO GUIDE THE DEVELOPMENT OF THESE COMPANIES AND MAXIMISE SHAREHOLDER

VALUE. JOINT CONTROL IS ACCEPTABLE IN CASES WHERE THE JOINT VENTURE PARTNER IS RELI-

ABLE AND BRINGS EXPERIENCE OR SKILLS THAT COMPLEMENT OUR OWN, OR SHARES FUNDING

OBLIGATIONS AND RISKS, WHICH DUE TO THEIR SIZE OR NATURE, WE WISH TO SHARE.

WE TYPICALLY TAKE A LONGER-TERM VIEW, IN ORDER TO REALISE THE FULL POTENTIAL

OF OUR INVESTMENTS.

THE LACK OF LIQUIDITY OF EMERGING MARKET ASSETS MAKES ANY EXIT STRATEGY TENU-

OUS. IN RUSSIA AND THE CIS IN PARTICULAR, THE LACK OF LIQUIDITY IS PERVASIVE, WHICH

WE HAVE REMAINED FAITHFUL TO A BASIC, YET SUCCESSFUL

INVESTMENT PHILOSOPHY WHICH HAS SERVED US WELL FOR MORE THAN

YEARS. WE CONTINUE TO BELIEVE THAT MUCH OF OUR FUTURE SUC-

CESS WILL BE ROOTED FIRMLY IN THIS INVESTMENT PHILOSOPHY:

ALFA GROUP’S INVESTMENT PHILOSOPHY

PLACES IT OUTSIDE OUR DIRECT CONTROL. UNLESS WE WISH TO SELL OUR ASSETS AT

EXTREMELY UNDERVALUED PRICES, WE MUST USE THIS TIME TO DEVELOP THESE ASSETS AND

GUIDE THE COMPANY TO CLOSE THE VALUE GAP. WHILE WE DO NOT PARTICULARLY WEL-

COME THE INFLEXIBILITY OF BEING WED TO AN INVESTMENT FOR THE LONGER TERM, WE

LOWER OUR RISKS BY SEEKING UNDERVALUED INVESTMENTS THAT PROVIDE AMPLE DOWN

SIDE PROTECTION AND, AS FAR AS POSSIBLE, INTERIM CASH FLOWS.

WE VIEW CO-OPERATION WITH FOREIGN INVESTORS AND THE ATTRACTION OF FOREIGN CAPITAL AS IMPORTANT

TO THE DEVELOPMENT OF OUR COMPANIES.

THE NEED TO ATTRACT FOREIGN INVESTMENT IS BECOMING INCREASINGLY CRITICAL.

FOREIGN INVESTORS PROVIDE NOT ONLY CAPITAL INVESTMENT, BUT ALSO THE EXPERTISE,

CREDIBILITY AND ADVANCEMENT OF REPUTATION WHICH IS NEEDED TO SUCCESSFULLY

DEVELOP AND REALISE THE FULL VALUE OF OUR INVESTMENTS. WE ARE FULLY AWARE THAT

THE FAILURE TO ATTRACT LONGER-TERM FOREIGN INVESTMENT WILL RESULT IN UNDER-

DEVELOPED ASSETS AND MISSED BUSINESS OPPORTUNITIES.

WE DO NOT CONSIDER OURSELVES EXPERTS IN MANAGING AND OPERATING

THE COMPANIES THAT WE OWN.

FIRST AND FOREMOST WE ARE INVESTORS, NOT BUSINESS MANAGERS –WE LEAVE THE DAY-TO-

DAY MANAGEMENT AND OPERATING DECISIONS OF OUR COMPANIES TO PROFESSIONAL, COM-

PETENT MANAGEMENT WITH INDUSTRY EXPERIENCE. OUR COMPANIES ARE INDEPENDENT

ENTITIES AND ARE GIVEN FAIRLY WIDE LATITUDE TO CONDUCT THEIR AFFAIRS. HOWEVER, WE

ACTIVELY ADVISE AND TAKE DECISIONS ON IMPORTANT STRATEGIC MATTERS THAT HAVE AN

IMPACT ON THE SHAREHOLDER VALUE OF OUR COMPANIES. WE ALSO CONTINUALLY EVALUATE

MANAGEMENT AND MEASURE THE FINANCIAL PERFORMANCE OF OUR INVESTMENTS.

WE ARE GUIDED BY THE PHILOSOPHY OF INVESTING IN ONLY THOSE COMPANIES THAT ARE LEADERS

IN THEIR RESPECTIVE FIELDS OF BUSINESS.

WE REQUIRE THOSE IN WHICH WE INVEST TO BE ONE OF THE TOP THREE IN THEIR BUSINESS

FIELD OR WITH A CLEAR POTENTIAL TO BECOME ONE OF THE TOP THREE WITHIN A REASON-

ABLE PERIOD. WHERE WE SEE THAT OUR INVESTMENTS ARE NOT MEETING THIS CRITERION,

WE TAKE ACTIVE MEASURES TO DIVEST AND FREE UP OUR FINANCIAL AND MANAGEMENT

RESOURCES FOR MORE EFFECTIVE INVESTMENTS.

A L F A G R O U P ’ S I N V E S T M E N T P H I L O S O P H Y

Seated (left to right): German Khan, Mikhail Fridman, Alexei Kuzmichov. Standing (left to right): Pyotr Aven, Leonard Vid, Alexander Fain, Nigel Robinson, Mikhail Gamzin, Alexander Kosyanenko, Vladimir Bernstein.

The Supervisory Board of Directors of Alfa Group guides and co-ordinates thestrategic development of Alfa Group and its companies. The Board, which meets twicea month, consists of a total of 10 senior executive and senior non-executive directorswho are primarily drawn from the main companies of the Group. These directors pro-vide different important insights into political, economic and industry developmentsin Russia and internationally.

The Supervisory Board considers the most important matters concerning the strategicdevelopment of the Group and the management of its businesses and serves as a con-duit for the senior management of the Group to share ideas and resolve issues in a co-ordinated manner. The most important issues include the clarification and develop-ment of the overall business strategy for the Group’s companies, the criticalevaluation of company performance, the formal review of significant transactionsbefore they are undertaken, and the establishment of strong mechanisms of corporategovernance and controls.

German KHAN . . . . . . . . . .Chairman of Management Board and Executive Director of TNK

Mikhail FRIDMAN . . . . . . . . .Chairman of the Supervisory Board of Alfa Group Consortium

Alexei KUZMICHOV . . . . . . . . . . . . . . . . . . .Chairman of the Board of Crown Resources AG

Pyotr AVEN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .President of Alfa Bank Group

Leonard VID . . . . . . . . . . . . . . . . . . . .Chairman of the Executive Board of Alfa Bank Group

Alexander FAIN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .General Director of Alfa-Eco Group

Nigel ROBINSON . . . .Director of Corporate Development, Finance and Control - Alfa Group

Mikhail GAMZIN . . .Member of the Board and Chief Executive Officer of United Food Company

Alexander KOSYANENKO . . . . . . . . . . .Chief Executive Officer of Trade House Perekriostok

Vladimir BERNSTEIN . . . . . . . .Director of Strategic and Investment Planning - Alfa Group

SUPERVISORY BOARD OF DIRECTORS

Since its establishment in May 1996, CTF Holdings Ltd(“CTF”), the ultimate holding company of the AlfaGroup, has effectively served as the Group’s corporatecentre. The corporate centre’s team of professional staffreports directly to the Supervisory Board of Directorsthrough the Director for Corporate Development,Finance & Control.

The Supervisory Board of Directors has vested theGroup’s corporate centre with wide-ranging responsibilityand authority to carry out numerous holding companyand corporate centre functions – some of which are tradi-tional and some of which have been specifically tailored totake into account the peculiarities of Russia and therequirements of the Group. Although the corporate cen-tre’s functions vary widely in scope, they can generally besummarised as:

• Decision-making and implementation support to theSupervisory Board of Directors;

• Direct assistance to the companies forming the Group; • Development and maintenance of strong formal mecha-

nisms of corporate and strategy development, invest-ment planning and control for the benefit of the com-panies forming the Group and for the Group as a whole.

More specifically, the primary functions of the Group’scorporate centre include setting Group wide accountingpolicy, the review and approval of quarterly companyaccounts prepared under International AccountingStandards, preparation of Group annual consolidated IASaccounts, and providing assistance to our companies inrecruiting qualified finance, accounting and other key per-sonnel. Responsibilities also extend to control over thedevelopment of an efficient Group-wide ownership struc-ture, the maintenance and enforcement of the Group’scorporate statute which defines and regulates decisionmaking within the Group, and improving all aspects ofoverall functioning of the effectiveness of our companies’Boards of Directors including the recruitment of qualifiedindependent, non-executive directors. Additionally, the

corporate centre is also responsible for other initiativesincluding the development of the Group’s corporate web-site, the production of the Group annual report as well asother public relations and marketing initiatives in co-oper-ation with the Group’s companies.

At the end of 2001, we created several new functions in thecorporate centre in the areas of business strategy, invest-ment planning, improvement of business processes, andthe critical review and development of IT strategy for theGroup and its companies. Some of the specific undertak-ings in these areas to date include the standardisation ofprocedures for analysis, modeling and presentation ofinvestment projects across all Group companies, theintroduction of protocols and procedures for investmentcommittees, and the critical evaluation of our companies’strategies. Also, IT related projects have included the crit-ical review and development of an effective, sustainableIT strategy at each company and for the Group as a whole,as well as the organisation and leading of the IT ExpertCommittee which effectively transfers IT expertise andknowledge between Group companies.

Well before it became fashionable, the Alfa Group recog-nised the importance of adopting western standards ofcorporate development and controls. In taking the longview, it became very clear to us that future shareholdervalue would be sacrificed if we did not act decisively andaggressively to develop strong governance mechanisms forthe Group.

We are proud of the progress that we have made since theformal establishment of our corporate centre, and aretoday reaping the benefits of our efforts. However we haveno illusions. We appreciate the realities and difficulties ofthe Russian marketplace and realise that the developmentof strong governance mechanisms for our Group is an evo-lutionary process. We are determined to meet this chal-lenge and realise our ambition of staying ahead of therequirements of the market and the expectations of ourstakeholders.

ALFA GROUP’S CORPORATE CENTRE

Alfa Group’s Principal Holdings

2001 was the eleventh year of Alfa Bank’s suc-cessful operation in the Russian and international finan-cial markets. Although years is not a long period whenjudged against the history of some international banks, itis nevertheless a noteworthy achievement in post-SovietRussia.

During and , Alfa Bank continued to receiveaccolades in the financial media both domestically andinternationally. Alfa Bank was nominated for a GoldenDiploma of the Financial Press Club for informationalopenness. Also, in , Global Finance, an influentialUS business journal, named Alfa Bank “Best Russian

Domestic Bank” for the fourth consecutive year and“Best Russian Trade Finance Bank” for the second con-secutive year.

During the leading international credit rating agen-cies (Moody’s, Standard & Poor’s, and Fitch IBCA)increased the Bank’s rating, some of them up to a levelclose to Russian sovereign ratings.

Financial Highlights

A lfa Bank’s net profits increased to US $. millionin , a .% increase on and total assets grew

FINANCIAL SERVICES

Alfa Bank

Founded in , Alfa Bank has developed rapidly to become Russia’s largest privately

owned bank. It provides a full range of banking services — comercial banking, investment

banking, asset management, securities trading, trade finance and leasing. The Bank has

the second largest branch network in Russia over nine time zones in Russia, Ukraine and

Kazakhstan, as well as subsidiaries in the United Kingdom, the United States and the

Netherlands.

www.alfabank.ru

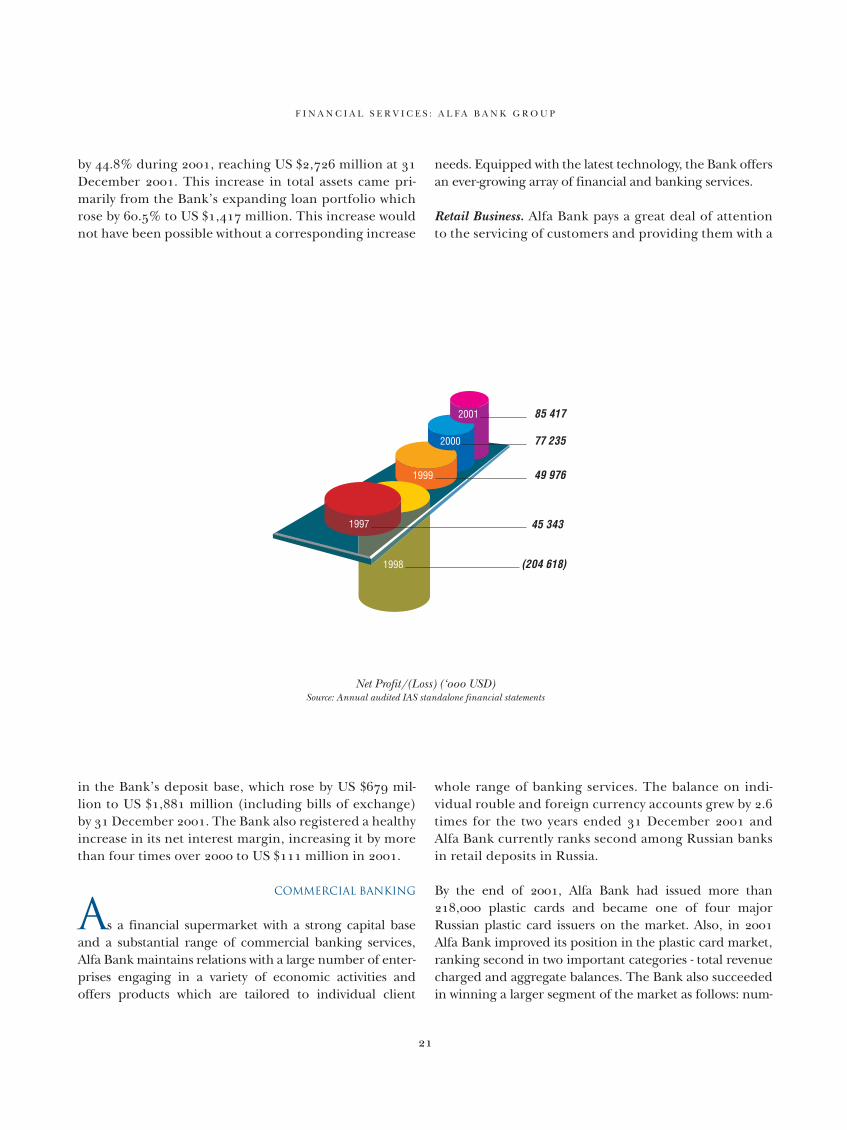

by .% during , reaching US $, million at December . This increase in total assets came pri-marily from the Bank’s expanding loan portfolio whichrose by .% to US $, million. This increase wouldnot have been possible without a corresponding increase

in the Bank’s deposit base, which rose by US $ mil-lion to US $, million (including bills of exchange)by December . The Bank also registered a healthyincrease in its net interest margin, increasing it by morethan four times over to US $ million in .

Commercial Banking

As a financial supermarket with a strong capital baseand a substantial range of commercial banking services,Alfa Bank maintains relations with a large number of enter-prises engaging in a variety of economic activities andoffers products which are tailored to individual client

needs. Equipped with the latest technology, the Bank offersan ever-growing array of financial and banking services.

Retail Business. Alfa Bank pays a great deal of attentionto the servicing of customers and providing them with a

whole range of banking services. The balance on indi-vidual rouble and foreign currency accounts grew by .times for the two years ended December andAlfa Bank currently ranks second among Russian banksin retail deposits in Russia.

By the end of , Alfa Bank had issued more than, plastic cards and became one of four majorRussian plastic card issuers on the market. Also, in Alfa Bank improved its position in the plastic card market,ranking second in two important categories - total revenuecharged and aggregate balances. The Bank also succeededin winning a larger segment of the market as follows: num-

F I N A N C I A L S E R V I C E S : A L F A B A N K G R O U P

Net Profit/(Loss) (‘ USD)Source: Annual audited IAS standalone financial statements

ber of international plastic cards (% market share); PayLater cards (%); revenue on issued cards (%); tradeoutlets (%); acquisition turnover (%). Importantly,this growth in market position was accompanied by a %increase in the profitability of Alfa Bank’s plastic card busi-ness during as compared to the year earlier period.

Significant attention to the retail segment of the bankingindustry is a main strategic focus of the Bank as it seeks towin back tremendous cash resources accumulated by indi-vidual savers.

Regional Network. In a number of Alfa Bank branch-es were set up across Russia including in Izhevsk,Voronezh, Yaroslavl and Sakhalin. Also, a representativeoffice was set up in Tatarstan, and eight new offices wereestablished in Moscow and other Russian regions.Currently, Alfa Bank’s branch network stretches fromSakhalin in the east to Kaliningrad in the west.

International Network. The Bank also has branches inKazakhstan and Ukraine as well as in the Netherlands,the latter being the only % privately owned Russian

commercial bank in Europe (Amsterdam Trade Bankor “ATB”), which holds a comprehensive bankinglicense. In , ATB intends to enlarge its productrange, through the implementation of the FontisElectronic Banking System, simultaneously with theinstallation of an additional Equation Clean PaymentsSystem. This will allow ATB to attract major corporateclients and correspondent banks for settlement andclearing services.

Alfa Bank branches also operate in London and NewYork. Alfa Securities (London), created in June cur-rently holds all of the required licenses of the UKFinancial Services Authority (“FSA”) and was the firstRussian financial company to obtain a FSA license, afterthe Russian financial crisis. saw the openingof an Alfa Bank representative office – Alfa CapitalMarkets (USA) Inc in New York. Alfa Capital Markets(USA) Inc has a NASD license for carrying out brokerageand dealer operations and specialises in operationsinvolving brokerage and trading in shares issued byRussian companies as well as providing corporatefinance services to its clients.

F I N A N C I A L S E R V I C E S : A L F A B A N K G R O U P

Alfa Bank’s Branch Network

Co-operation with Financial Institutions and Inter-BankOperations. During , the establishment of new andthe consolidation of existing correspondent relationswith major banks in Europe, the US, Japan, Asia, Africaand Latin America secured Alfa Bank the leading posi-tion among Russian non-government banks in clearingactivity.

In co-operation with its foreign partners Alfa Bank ren-ders a highly diversified range of top-notch services in theareas of project finance, syndicated lending related totrade financing, export credit operations, clearing, for-eign exchange and banknote services.

During , Alfa Bank obtained an unsecured syndicat-ed loan of US $ million from a consortium of leadingEuropean banks. This was the largest unsecured Russianfinancial institution risk syndicated in the internationalloan market since Russia’s financial crisis.

Loans. In , the extension of loans, bank guarantees andother credit related products was considerably intensifiedand enlarged due to a broader client base, and use of loan

facilities by newly opened branches and additional offices.As such, in income derived from lending activitymade the largest overall contribution to the Bank’s aggre-gate income. By December the Bank’s loan portfo-lio reached US $, million, a .% increase over .

An expanding and diversified client base has enabled theBank to spread the risk of its loan portfolio across differ-ent sectors of the economy. Specifically, the Bankincreased significantly, lending to manufacturing, con-struction, trade and commerce enterprises during .Despite the large increase in the Bank’s lending base, thecredit process at Alfa Bank continues to be based on astrict lending and risk management culture.

Currency Markets. For several years, Alfa Bank has enjoyeda leading position on the domestic and international for-eign exchange and money markets, including the marketsof the CIS. saw a further steady growth of the Bank’srevenues from currency operations in the Russian marketcaused by a sustainable increase in the volume of clientoperations, and by an increase in volume of Alfa Bank’soperations in the inter-bank market and MICEX. Today,

F I N A N C I A L S E R V I C E S : A L F A B A N K G R O U P

% Contribution to Bank’s Net Profit by Business SegmentSource: Company data

Alfa Bank’s controls between % and % of the marketfor RR/USD transactions.

Investment Banking

Equity Markets and Trading. In , Alfa Bank carried outits largest volume of equity operations on the RTS,MICEX and the international ADR markets. During ,the total equity trading volume for the Bank increased by% as compared with and the Bank’s market sharewas .% of the total market at the end of .

Fixed Income Markets and Trading. In this segment of themarket Alfa Bank enjoys many competitive advantages.Importantly, Alfa Bank is a market maker in GKO andOFZ bonds as well as in corporate Russian and otherEurobonds. Also, the wide Alfa Bank branch networkensures access to regional issuers and creates possibili-ties for an objective assessment of their creditworthiness.

One of the highlights of in the area of fixed incometrading was that profits from REPO operations increasedby three-fold as compared to the previous year.

Asset Management. Alfa Bank, through its subsidiary AlfaCapital is a trusted leader in the Russian financial mar-

ket in asset management services to a wide range ofinvestors, including private individuals, pension funds,insurance companies and corporate treasury depart-ments. With over million unit holders, Alfa Bank man-ages the most widely-held open-end mutual fund inRussia. In the Fund’s per unit rouble priceincreased by approximately %. In , the mostimportant strategic goals will be the attraction of pen-sion fund assets for management and the effective use ofexisting distribution channels in the Bank’s branch net-work to market and sell a range of newly created familyof investment funds.

Corporate Finance. In , the strategic co-operation andsynergies between commercial and investment bankingsides of Alfa Bank ensured Alfa Bank’s success in the areaof corporate finance. A summary of some of the more sig-nificant transactions which the Bank’s CorporateFinance team were involved in and early :

• Purchase by Tyumen Oil Company of a controlling stakeof shares in SIDANCO Oil Company;

• Purchase of Golden Telecom, a US public companywhose shares are listed on NASDAQ, for Alfa Group anda consortium of western investors;

F I N A N C I A L S E R V I C E S : A L F A B A N K G R O U P

• Financial consultant to Svyazinvest subsidiaries withregard to the consolidation of the regional electroniccommunication operators in Siberia and Far East;

• Purchase by Alfa-Eco Group of a controlling block ofshares in Volga Pulp and Paper Mill, a major Russianproducer of newsprint paper;

• Acquisition of AO Milk Plant and AO Kiev City MilkPlant for Wimm-Bill-Dann, a large Russian dairy;

• Manager (with ING Barings acting as lead manager andglobal co-ordinator) on the New York Stock ExchangeUS ADS issue of Wimm-Bill-Dann

Strategy

L ooking beyond , there are a number of strate-gic initiatives which are being undertaken at the Bank.Some of the key elements on the commercial bankingside of our business include the aggressive expansion ofthe Bank’s branch network into Russia’s regions, arelentless focus on the reduction of operating costs –especially within the branch network, and the provisionof improved services, including the introduction ofnew products to our clients. Underpinning these strate-

gic objectives will be the further successful implemen-tation of information systems and technologies whichwe have invested in heavily, over the past few years.During Alfa Bank launched a comprehensiveretail business program named Mercury Project, whichenvisages an aggressive expansion of retail bankingservices in Russia and the CIS. The Project includes therapid opening of branches, state-of-the-art technologiesfor the customer, the provision of timely and accuratefinancial and operating information for decision-mak-ing, and a strict control over expenses. Continuedgrowth in our commercial banking business will also beenhanced by our commitment to maintain a capitaladequacy ratio above %.

On the investment banking side, we will continue tocentre our attention on divesting ourselves of assetswhich were acquired during privatisation, which are notstrategic to the Bank and whose potential has beenrealised. After hiring several key managers in and, we are focused keenly on expanding our presencein the area of asset management. We are also focused onincreasing equity trading, brokerage and other serviceswhich we provide to foreign corporates and individualswho wish to access the Russian public and private equi-ty markets.

F I N A N C I A L S E R V I C E S : A L F A B A N K G R O U P

AlfaInsurance

AlfaInsurance Group is one of Russia’s largest insurers and offers a diversified portfolio

of insurance services including comprehensive business insurance protection as well as a

wide range of products for individuals. AlfaInsurance is consistently ranked as one of the

top five insurance companies and actively works across the whole of Russia and Ukraine.

www.alfastrah.ru

In September 2000, a new insurance unit was launchedwithin Alfa Group with the establishment of the market-oriented insurance company – Alfa Guaranty – whose aimwas to provide a range of comprehensive financial serv-ices to its customers. Since then, development of theinsurance business has been considered a strategic pri-ority of the Alfa Group. The business of the Groupdeveloped rapidly during 2001 when the holdingacquired the controlling interest of shares in EastEuropean Insurance Agency (“VESTA”) and the Ukraine-based Ostra Kiev. Beginning in September 2001, theentire insurance business of the Group was united undera single trademark – AlfaInsurance Group.

At the end of 2001, over 25,000 companies and more than80,000 individual customers entrusted the Company withprotection of their financial interests, which helped theCompany secure its place as the second largest companyin the Russian voluntary insurance market (by insurancepremiums collected).

Review of 2001

During 2001, AlfaInsurance expanded its presencein Russia’s regions considerably: the number of affiliatesrose from 38 to 43 and by the end of the year twelve affili-ates gained leading positions on local regional markets,

including St. Petersburg, Tyumen, Yekaterinburg,Novorossiysk, and Western Siberia.

In 2001, the Company’s total turnover was US $683.5 mil-lion, which was 3.2 times more than in 2000. The share ofproceeds from insurance premiums soared by 2.2 timesover the same period last year and accounted for approxi-mately 25% of the total increase of AlfaInsurance Group’sproceeds. At the end of 2001, the Company controlled7.4% of the Russian insurance market (as measured byinsurance premiums collected), an increase in marketshare of 4% as compared with end of 2000.

AlfaInsurance Group was the first Russian insurance com-pany to increase its share capital above the threshold of1 billion roubles and the Company’s share capital reachedUS $64 million in 2001. A substantial amount of share-holders’ equity as well as a reliable re-insurance programaimed at protecting the Company’s portfolio throughleading trans-national companies, such as Munich Re,General Cologne Re, Swiss Re, SCOR, and Lloyd’s ofLondon, enable the Company to undertake large finan-cial risks of its customers, almost without limitation.

Upon unification of three companies under one trade mark,AlfaInsurance Group was faced with a challenge to re-launchitself in the market as quickly as possible. Since September

F I N A N C I A L S E R V I C E S : A L F A I N S U R A N C E G R O U P

% of Market Share Controlled by AlfaInsurance (by insurance premiums)Source: Company data, Company analysis of market data

Mix of Risk Based Insurance Policies Written by AlfaInsurance – End of Source: Company data

2001, a full-scale promotion campaign that involved all avail-able media sources was launched. The opinion poll that fol-lowed confirmed the high efficiency of the campaign withbrand recognition among the target audience reaching 85%.The AlfaInsurance trademark has solidly positioned itselfwithin the top five insurance companies of the market.

Looking Ahead

We believe that in the next few years an “insuranceculture” in Russia will continue to steadily grow and will

support the development of the Russian insurance mar-ket. One of the main strategic tasks of AlfaInsurance willbe to capture a substantial amount of new business and inkey segments of the corporate and individual markets aswell as further strengthen the Company’s positions as amajor national player of the insurance community. Thisdevelopment strategy will be based on the ability to effec-tively utilise existing opportunities of the Company,regional expansion, optimization of business processes,reinforcement of the sales organisation and building onsynergies with Alfa Bank.

PROGRESSIVE

THINKING

OR

SEEKING PIONEERING

SOLUTIONS.

SOMETIMES STRIKING

AND UNCONVENTIONAL,

BUT ALWAYS EFFECTIVE

AND TIMELY

Tyumenskaya Neftianaya Kompaniya (“Tyumen OilCompany” or “TNK”) was formed as an open-type jointstock company by a government decree in August 1995. Atthat time, the Russian government was the largest ofTNK's shareholders.

In July 1997, 40% of the Company's shares were put up forprivatisation in an investment tender that was won byNovy Holdings (a company jointly owned and controlledby Alfa Group and Access Industries/Renova Group).Early in 1998, the new shareholders together bought a fur-ther 9% of TNK shares from private shareholders and anadditional 1.1% at a specialised auction, thus consolidat-ing a controlling block (50.1%) in TNK.

In December 1999, when the Russian government (rep-resented by the Federal Property Fund) put up theremaining 49.8% of TNK for privatisation, Alfa Groupand Access Industries/Renova Group again, jointly wonthe tender, bringing their total ownership in TNK to99.9%. In February 2001, after the completion of aninvestment program as per the terms of the tender, AlfaGroup and Access Industries/Renova Group gained

full control of the purchased shareholding, fully pri-vatising the company.

During December 2001, TNK, completed a single shareswap whereby minority shareholders voluntarilyswapped their ownership in TNK’s production sub-sidiaries for ownership in TNK and continuing through2002, TNK purchased shares in its production sub-sidiaries directly from existing shareholders. Currently,Alfa Group, together with Access Industries/RenovaGroup own approximately 97% of the outstandingshares of TNK.

Company Structure

TNK, together with its subsidiaries (includingONAKO Oil Company, 85% of which was purchased atend of 2000 for US $1.08 billion), is one of the largest ver-tically integrated oil companies in Russia, ranking secondin oil reserves and fourth in oil production. Its primaryoperations include the production and refining of crudeoil and gas, as well as distribution of oil and gas, premiumoil products and motor oils.

OIL production

Tyumen Oil Company

Established in , Tyumen Oil Company (“TNK”) together with its subsidiaries, is

today one of the largest vertically integrated oil and gas companies in Russia, ranking

fourth in oil production and second in oil reserves. TNK’s primary operations include

the production of crude oil and gas, refining, as well as the distribution and retail sale of

refined oil products.

www.tnk.ru

The Company includes four oil producers (Samotlor-neftegas, Nizhnevartovsk Oil and Gas ProductionCompany, Tyumenneftegas, and TNK-Nyagan), fiverefineries (Ryazan NPZ, Nizhnevartovsk NPO, Krasno-leninsky NPZ, Lisichansknefteorgsintez and Orsk-orgsintez); and five distribution and marketing enter-prises (Kaluganefteproduct, Karelnefteproduct, Tula-nefteproduct, Ryazannefteproduct and Kursknefte-product).

Exploration and Production

TNK's primary oil fields are located in the Tyumenregion of western Siberia, the largest region of hydrocar-bon reserves in Russia. The wells are highly productive,with high quality sweet crude oil with good physicochem-ical properties. Sweet crude commands a higher price,and is easier to manufacture into environmentally-friend-ly oil products without requiring investment in expensivede-sulfurisation equipment.

According to 2001 production results, TNK, togetherwith all its subsidiaries, currently produces 114.9 thou-

sand tonnes of oil per day, 42% of which is exported,while the remaining oil is delivered to its own refineriesand goes for free sale on the domestic market. TNK isone of the few national oil companies operating its pro-cessing facilities at full capacity. As of 1 January 2002,TNK's proven oil reserves based on international stan-dards were at 1.03 billion tonnes, and total reservesincluding proven, probable and possible, were estimatedat 2.17 billion tonnes.

Refining and Distribution

In 2001, the Company refined 20.9 million tonnes ofcrude and produced 10.7 million tonnes of light oil. TheRyazan Refinery is the primary refining unit for TNK’supstream operations. The location of Ryazan, in close prox-imity to the largest sales markets in Central Russia (includesMoscow), provides TNK with a strategic competitive advan-tage. TNK's management has been actively working toincrease Ryazan Refinery's outputs and to improve the qual-ity of its refined products. In 2001, the Ryazan Refineryrefined approximately 11.1 million tonnes, with 10.5 milliontonnes of oils and 572 thousand tonnes of petrol.

O I L P R O D U C T I O N : T Y U M E N O I L C O M P A N Y

TNK Volume of Crude Oil Production (' of barrels per day)Source: Company data

TNK owns and operates a network of retail petroleum sta-tions throughout Central Russia, in the Tyumen region,Karelia, Orenburg region and Ukraine. In addition toTNK-owned petroleum stations, from 1998, the Companyhas been successfully developing Russia's first unique job-ber network where jobbers, while being independent gasstation owners, have exclusive rights to sell TNK productsunder franchises. At the end of 2001, the total number ofTNK-owned and jobber gas stations was 969.

Strategy

The cornerstone of TNK's long-term corporate strategyis to increase its market value by maximising the economicbenefits of vertical integration, improving production effi-ciency, lowering costs, and reorienting production andsales towards competitive high value-added products.

The strategy developed to achieve this includes:

• Focusing corporate efforts on using vertical integrationbenefits and adding value by:

– Optimisation of oil and gas production and quality;– Higher technical and economic efficiency of refineries

including increasing the share of production of light oils;– Expansion and higher efficiency of retail sales in the

most attractive fuel market segments;– Greater capital efficiency in every part of the chain;

• Continued international development through joint ven-tures, mergers, affiliations and other strategic partnershipsincluding co-partnership in projects for the developmentof oil, oil products, and gas transportation infrastructure;

• Improvement of efficient organisational and manage-ment system based on encouraging “bottom-to-top” ini-tiatives and improvement of “top-to-bottom” control tothe international standards of corporate governance andoperating and financial transparency;

O I L P R O D U C T I O N : T Y U M E N O I L C O M P A N Y

TNK Presence in Russia and Ukraine

O I L P R O D U C T I O N : T Y U M E N O I L C O M P A N Y

• Improvement of management, information and safeoperation technologies

Key results for 2001 and H1 2002

In 2001, TNK highlights included:

• Strategic partnership with British Petroleum (“BP”), andamicable settlement of relations regarding SIDANCO OilCompany which regained its ownership of TNK-Nizhnevartovsk (Chernogorneft) acquired by TNK in 1999following bankruptcy proceedings. The Company increasedto approximately 29% its interest in Rusia Petroleum, whichhas a license to develop a major Kovyktinskoye gas field.Additionally, in April 2002, we sold to BP, a 15% stake in oiland gas company, SIDANCO for US $375 million.

• Launching a new catalytic cracking unit at theCompany’s Ryazan Refinery six months ahead of sched-ule. The unit improves the quality of refined productsand increases throughput and efficiency, increasing oilconversion from 59% to 68%. Additional planned con-struction will further increase conversion rates to 75% byend of 2002 and 82% by end of 2003;

• The development of new and considerable expansionof existing oil products and distribution networks,including positions on the highly profitable Moscowmarket;

• TNK was the first Russian oil company to join theEcology and Energy Committee of the AmericanChamber of Commerce

With 380,000 barrels per day production, SIDAN-CO Oil Company ranks amongst the ten largest oil and gasproducers in Russia, employing 29,000 people.SIDANCO’s upstream subsidiaries are currently develop-ing over 120 fields located in Udmurtia, Saratov Oblast(Volga Region), the Khanty-Mansiysk Autonomous Area(Tyumen Oblast), and Novosibirsk Oblast in westernSiberia.

The Alfa Group, together with its joint venture partnersAccess Industries / Renova Group, owns approximately57% of SIDANCO and invests alongside BritishPetroleum (“BP”), a 25% + 1 share shareholder, as well asother minority shareholders. Under the terms of theshareholders agreement, as a controlling shareholder,Alfa Group, Access Industries and Renova Group hasmajority Board representation, and BP has been grantedmanagement control of the Company for at least the nextthree years.

Company Structure

SIDANCO has five main production companies whichcomprise: TNK-Nizhnevartovsk (2001 production – 6.5 mil-lion tonnes) which also has a share in two joint venturesadding over 1.5 million tonnes in 2001, UdmurtNeft(2001 production – 4.98 million tonnes) VaryoganNefteGaz(2001 production – 2.99 million tonnes), SaratovNefteGaz(2001 production – 1.43 million tonnes), andNovosibirskNefteGaz (2001 production – 0.08 milliontonnes). In addition the Company owns Saratov Refinery,which in 2001 improved its depth of refining by 6.5%, pro-duced 3 million tonnes of oil products and increased gaso-line production by more than 50% as compared to2000 levels. The Refinery is working on an investmentproject to install a cracking unit to further boost the yieldof light products.

SIDANCO’S retail network comprises 149 service stations,located in the Saratov and Rostov regions, where theydominate their respective markets.

SIDANCO Oil Company

Established in , SIDANCO Oil Company together with its subsidiaries, is one of

Russia’s largest vertically integrated oil and gas companies, ranking among the top-ten in

oil production and th in oil reserves. SIDANCO’s primary operations include oil and gas

exploration, production and refining as well as oil and chemical products distribution.

www.sidanco.ru

Management

In late 1999, BP seconded a team of six senior managerswith vast experience in the petroleum industry to join theSIDANCO management team. Since that time, SIDANCO’smanagement team has grown stronger and is now supple-

mented by additional BP and Russian resource, particularlyin key operational positions. The management team hasbeen very successful in driving the strategic objectives of theCompany, including the integration of advanced Westernpractices in the context of best Russian experience.

Strategy

The central aim of SIDANCO is to maximise share-holder value. The Company has identified its corestrengths as hydrocarbon development and extractionand seeks to maximise its performance in every aspect ofthis activity. Necessarily, a cornerstone of this strategy is tofocus on operational excellence. This obviously requireschanging the way that SIDANCO does things and is cur-rently embarking on a major change initiative in order toachieve its goals. Operationally, the Company is in theprocess of changing its structure and processes with a

focus on performance units of core production assets.These units will be supported by other services, but wher-ever possible, the Company seeks to concentrate on itscore competencies. Non-core activity, including oil-fieldservices will be separated to eventually form a part of theoil service industry in Russia.

Other initiatives supporting operational excellenceinclude changing the management information systemsand processes to support greater transparency in the busi-ness. In view of its strategy, the Company focuses on suchimportant issues as health, safety and environment (HSE).A major initiative has commenced to assess and improveSIDANCO’s safety perfomance to world-class standadsusing the assistance of DuPont, a recognized world leaderin safety. In cooperation with IT Russia, a leader in envi-ronmental management, SIDANCO is implementing amonitoring and improvement system which is designed tocomply with ISO 14001.

This change process obviously impacts people. In SIDAN-CO, the combination of key BP resources and Russianexpertise is blended to make the change process workfrom inside. This blend of expertise is working to improveprocesses and achieve operational excellence.

O I L P R O D U C T I O N : S I D A N C O O I L C O M P A N Y

SIDANCO Volume of Crude Oil Production (in millions of tonnes)Note: TNK-Nizhnevartovsk and its two subsidiaries are included from December

Source: Company data

FORESIGHT

OR

THINKING

WHICH IS AHEAD OF ITS TIME.

THE OPENING OF NEW HORIZONS,

BY THOSE WHO TODAY THINK

ABOUT TOMORROW

CROWN RESOURCES AG

Founded in 1992 and based in Zug, Switzerland, withbranches in London and Gibraltar and representativeoffices in Moscow, Baghdad, Havana, Caracas andSingapore, Crown has more than 100 employees in itsworld-wide operations. Crown is actively involved in thetrading of physical goods with the territories of theCaribbean basin and Latin America, the Middle and FarEast, Africa, and Russia as well as other CIS countries.

Crude Oil and Oil Products

Through long-standing relationships with oil produc-ers, Crown’s crude oil and oil products department main-tained their significant presence as a major participant ininternational oil markets in 2001. The main providers ofoil are companies such as TNK and Bashneft (Russia),Somo (Iraq), and TotalFinaElf (France).

Crown trades a wide range of Russian and international-ly sourced oil products, including gasoline, kerosene,fuel oils, blend stocks and cycle oils, and for the last sev-eral years has placed particular emphasis on expandingits non-Russian oil products business.

Crown has established trading and credit lines with a num-ber of companies in order to participate in the derivative

markets and be able to conclude OTC deals as required forhedging. As a result, Crown’s access to international mar-kets and its ability to use various hedging techniques allowssignificant flexibility in negotiating terms and conditionswith its suppliers. These include various pricing mecha-nisms that add to Crown’s competitiveness in trading crudeoil and oil products. This also allows Crown to realise, infull, the trading potential offered by a stable supply baseand strong relationships with many customers world-wide.Among Crown’s customers are numerous state-owned andprivate companies, including: Somo, NIOC, PDVSA, BP,TotalFinaElf, Shell, ExxonMobil, Agip, and Cargill.

Metals

Having recently established offices in New York andNew Orleans, Crown initiated its metals trading businessduring the second half of 2001. Since that time theCompany has been actively trading in Europe, CIS, Asia,Australia, South America and the Middle East.

Crown is determined to cultivate the natural progressionof the Company into metals trading and believes that theCompany’s robust expertise and ability in the financialmarkets will allow for an acceleration of exponentialgrowth in the years to come. Already, Crown’s trading

COMMODITIES TRADING

Crown Resources AG

Founded in , Crown Resources AG is a major international commodities business

trading Russian and internationally sourced commodities – primarily oil and oil prod-

ucts and metals. Based in Zug, Switzerland, Crown has branches in London and Gibraltar

and representative offices in Moscow, Baghdad, Havana, Caracas and Singapore.

www.crownresourcesag.com

team has extensive experience in international finance,arbitrage, risk management, terminal markets, physicalproduction and consumption. Also, the Company is inte-grally involved in the supply chain by means of trade,investment and financial arrangements.

Crown’s current activities are focused on primary, second-ary, alloy, semi-fabricated products and scrap aluminum,and are currently in the process of introducing a copperdepartment. It is anticipated that other non-ferrous basemetals will follow.

Financing

Credit lines opened at major international banks,which exceeded US $1 billion at the end of 2001, allow theCompany to engage in a variety of trading activities basedon trade financing, including the pre-financing of rawmaterial suppliers, the financing of the production andprocessing of goods, the financing of the storage of com-modity stocks, and hedging. Banks with which theCompany co-operates include Raiffeisen Zentralbank,

Banque BNP Paribas, Natexis Banque, Societe GeneraleBanque and others.

A Year of Changes

The nature of the Company’s business changed during2001 in that much less reliance is being placed on sourcingdeals through Alfa Group companies as Crown continuesto develop its own independent base. These changes, com-bined with extremely difficult trading conditions following11 September 2001, have resulted in the Company review-ing all of its operations, with a view to restructuring.In early 2002, a comprehensive reorganisation was initiat-ed in order to adjust the overhead levels to fit this new pro-file. In addition, the Company wrote off one-time expens-es associated with the hiring of high level energy traderswho will be leading new initiatives through 2002 and sub-sequent years. Also a new management team was broughtinto the Company. To demonstrate its commitment toCrown in this transition period, the Alfa Group decided toincrease Crown’s equity by capitalising approximatelyUS $48 million of an Alfa Group subordinated loan.

C O M M O D I T I E S T R A D I N G : C R O W N R E S O U R C E S A G

Contribution by Different Commodity Types to Company TurnoverSource: Company data

ALFA-ECO GROUP

In addition to being one of Russia’s leading tradingcompanies, in recent years, Alfa-Eco Group’s (“Alfa-Eco”or the “Group”) key focus has been on large-scale invest-ments in Russian industrial assets. Accordingly, one ofthe Group’s top priorities has been the acquisition ofpromising companies. Alfa-Eco places key managementpersonnel into these companies who introduce advancedmanagement, operating, and marketing practices andalso makes necessary capital investment in order to mod-ernise the companies. The desired result is to raise thevalue of the company by realising a significant increase inproduction output and strengthening of market position.

Energy

In 2001, the Group delivered approximately 11.5 mil-lion tonnes of crude oil and oil products to internationalmarkets, including exports made under the UN SecurityCouncil’s Oil-For-Food Programme for Iraq. Export deliv-eries of oil products from Russia in 2001 were more than473 thousand tonnes, while Russian domestic-marketsales were 485 thousand tonnes. In 2002, the Group’splans call for exporting approximately 9 million tonnes ofoil and oil products.

In 2001, Alfa-Eco continued the management of its95% owned stake of Sakhalin-based ZAO Petrosakh, avertically-integrated complete cycle oil companyinvolved in the exploration, production and export ofcrude oil, as well as the refining and sale of oil prod-ucts. Petrosakh is currently carrying out an explorationand drilling programme which will allow for produc-tion of more than 1 million tonnes of oil annually. TheCompany’s plans call for meeting fully Sakhalin’sdemand for oil products, as well as supplying oil prod-ucts to other regions of Russia’s Far East. Additionally,Petrosakh has obtained a license from the RussianFederation’s Ministry of Natural Resources for the geo-logical exploration of oil blocks in the Sakhalin-6coastal shelf zone, whose potential deposits are esti-mated at 200 million tonnes of oil (total potentialSakhalin-6 coastal shelf zone reserves are approximate-ly 1 billion tonnes).

Other Alfa-Eco activities in the energy sector include:

• Active participation in federally sponsored programmesfor the delivery of oil products, including fuel to theRussian armed forces and to Russia’s Far North;

• In 2001, Alfa-Eco continued its activities in the coal mar-ket delivering 497 thousand tonnes of coal to energy and

Alfa-Eco Group

Founded in as a trading company of the Alfa Group Consortium in Russia, Alfa-Eco

has built a large and diversified business in producing and trading a wide range of com-

modities and products both domestically and internationally including oil and oil prod-

ucts, coal, grain, meat, alcoholic beverages, pulp and paper products and others. Also,

Alfa-Eco has made a significant strategic investment into telecommunications assets.

www.alfaeco.ru

metallurgical enterprises. Significant growth in coalsales is expected in 2002.

Metals

Alfa-Eco has established a significant presence in theRussian metals industry and has developed an effectivemanagement structure for the metallurgical enterprisesthat it owns and manages. Enterprises in which Alfa-Ecohas management participation produced 9.7 milliontonnes of iron ore, 3.5 million tonnes of iron-ore con-centrate, 448.4 thousand tonnes of steel and 503.8 thou-sand tonnes of steel pipe in 2001.

In 2001, Alfa-Eco’s portfolio of investments in the industrychanged significantly as the Group finalised the sale of itsequity stake in Korshunovsky Mining and EnrichmentPlant. In addition, the disposal of a 50% stake in Volgograd’sKrasny Oktyabr Metallurgical Plant was carried out, and theNOSTA (Orsko-Khalilovsky Integrated Metals Plant,Orenburg Region) and Vtormet (Krasnoyarsk) investmentprogrammes were brought to successful completion.

The year 2001 also saw continued progress in the imple-mentation of a series of other investment programmes bythe Alfa-Eco Metallurgical Department. In particular,these included:

• The Sibelectrostal investment programme, aKrasnoyarsk-based metallurgical plant, which is aunique manufacturer of special and high-alloy steels.The bankruptcy proceedings were halted, the plant’sorder book was replenished and additional jobs werecreated, thus facilitating the hiring of highly qualifiedmanagement and staff specialists. Production volumetripled in the period November 2000 throughDecember 2001;

• The Taganrog Metallurgical Works (“Tagmet”), one ofRussia’s largest manufacturers of high-quality pipewith an annual production volume of 460 thousandtonnes and over 5,000 customers. By January 2002,Alfa-Eco’s equity interest in Tagmet increased from25.2% to 41.9%;

• The Amurmetal investment programme (Komsomolsk-on-Amur based metallurgical works), with an annual out-put 360 thousand tonnes of metal products, 85% ofwhich are exported, and annual revenues of US $60 mil-

lion. Alfa-Eco Group holds a 74.5% share of the votingstock in Amurmetal.

Telecommunications

In May 2001, Alfa-Eco acquired a blocking voting stake(25% + 1 share) in cellular communications providerVimpel-Communications (“VimpelCom”), and in itsregional subsidiary VimpelCom-R, which providemobile telephony services under the BeeLine trade-mark. The total amount of investment in this project byAlfa-Eco is US $246.8 million, making it the largest dealin the Russian telecom market in recent years. In theperiod from May through December 2001, VimpelCom’scapitalisation increased from US $806.6 million toUS $1.4 billion.

Alfa-Eco, together with other Alfa Group companies, alsoactively co-operates with international organisations suchas Intersputnik, which is one of the largest internationalspace organisations which carries out launches and run-ning of the largest group of civil sattelites and relatedequipment.

Pulp and Paper and Forest Products Industry

In early 2001, the Group gained significant influenceover Balakhninsky Pulp and Paper Mill (“Volga”), whichproduces one-third of all newsprint in Russia (2001 pro-duction was 542 thousand tonnes of paper). In 2001,Volga achieved year-on-year sales growth of 12%.

In the fourth quarter of 2001, Alfa-Eco increased its par-ticipation in the management of Kama Pulp and PaperMill (Perm Region). In early 2002, the plant’s operationswere stabilised, resulting in an increase in average month-ly paper output from below 5 thousand tonnes to 7.5 thou-sand tonnes. In the near future, the plant should reach amonthly production level not less than 9 thousand tonnesof paper.

The combined output of Volga and Kama Pulp and PaperMill accounts for approximately 40% of Russia’snewsprint production.

Since 2001, Alfa-Eco has been implementing a lumbertrading programme and, in the reporting year, theGroup’s share of round timber exports to Finlandreached 2% of the Finnish export market.

C O M M O D I T I E S T R A D I N G : A L F A - E C O G R O U P