Embed Size (px)

Citation preview

Audit of Externally-assisted Projects (EAPs) by the Comptroller

& Auditor General of India – A Broad Framework and Case

Studies

- Dr. Abhishek Gupta, Principal Director,

Office of CAG of India, New Delhi

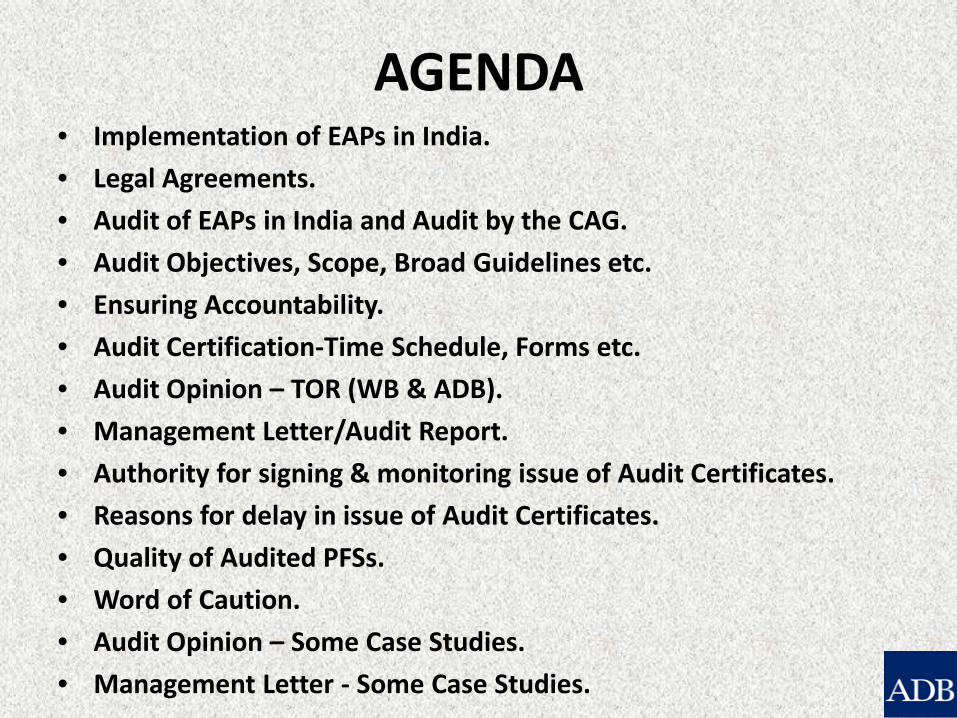

AGENDA • Implementation of EAPs in India.

• Legal Agreements.

• Audit of EAPs in India and Audit by the CAG.

• Audit Objectives, Scope, Broad Guidelines etc.

• Ensuring Accountability.

• Audit Certification-Time Schedule, Forms etc.

• Audit Opinion – TOR (WB & ADB).

• Management Letter/Audit Report.

• Authority for signing & monitoring issue of Audit Certificates.

• Reasons for delay in issue of Audit Certificates.

• Quality of Audited PFSs.

• Word of Caution.

• Audit Opinion – Some Case Studies.

• Management Letter - Some Case Studies.

Implementation of EAPs in India

• Implementation of Externally Assisted Projects (EAPs) including World Bank assisted projects has undergone a considerable change during the last decade.

• Earlier the project implementation was more centralized and department-centric.

• In recent times, implementation is carried out in a more decentralized manner through Special Purpose Vehicles (SPVs) like registered Societies, NGOs etc.

• There is also increasing trend of donors especially World Bank in devolving funds to the Local Bodies.

• Implementation: State-specific or Multi-State projects.

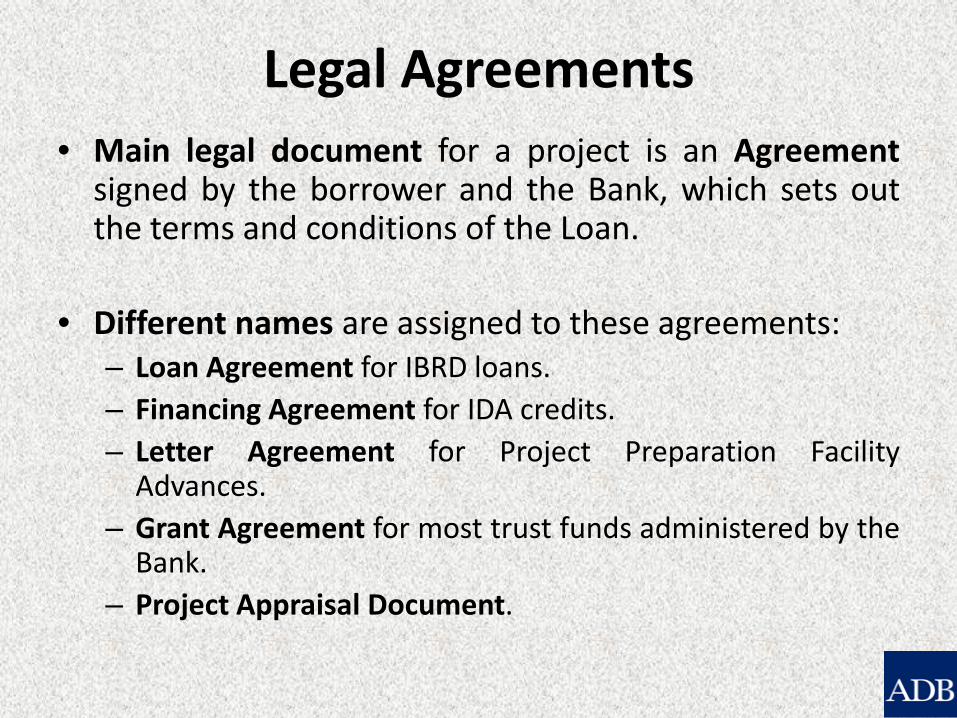

Legal Agreements • Main legal document for a project is an Agreement

signed by the borrower and the Bank, which sets out the terms and conditions of the Loan.

• Different names are assigned to these agreements:

– Loan Agreement for IBRD loans. – Financing Agreement for IDA credits. – Letter Agreement for Project Preparation Facility

Advances. – Grant Agreement for most trust funds administered by the

Bank. – Project Appraisal Document.

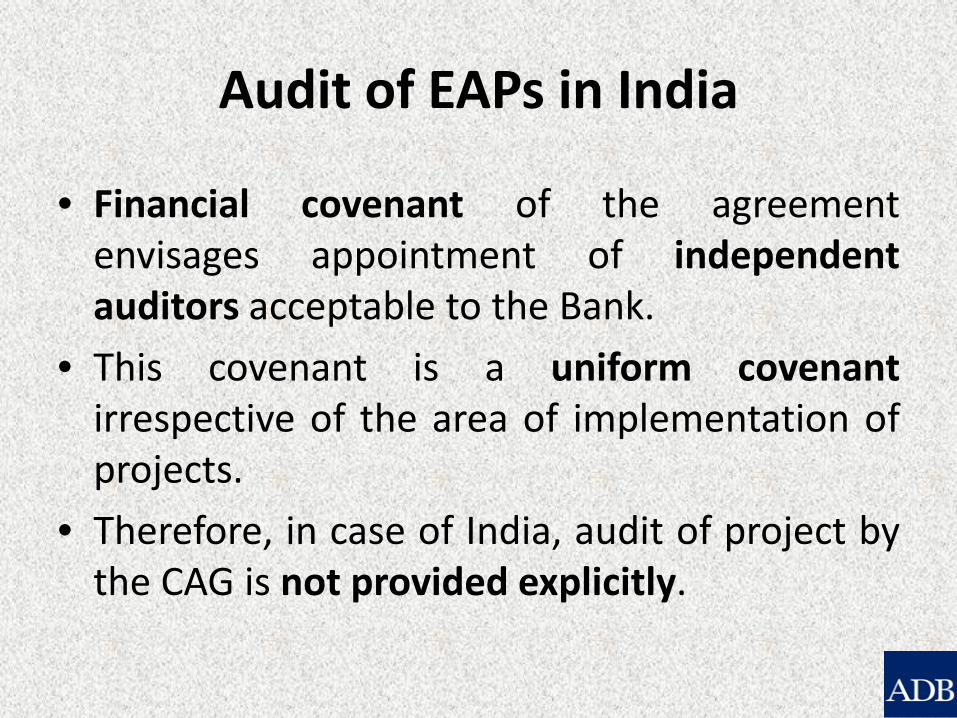

Audit of EAPs in India

• Financial covenant of the agreement envisages appointment of independent auditors acceptable to the Bank.

• This covenant is a uniform covenant irrespective of the area of implementation of projects.

• Therefore, in case of India, audit of project by the CAG is not provided explicitly.

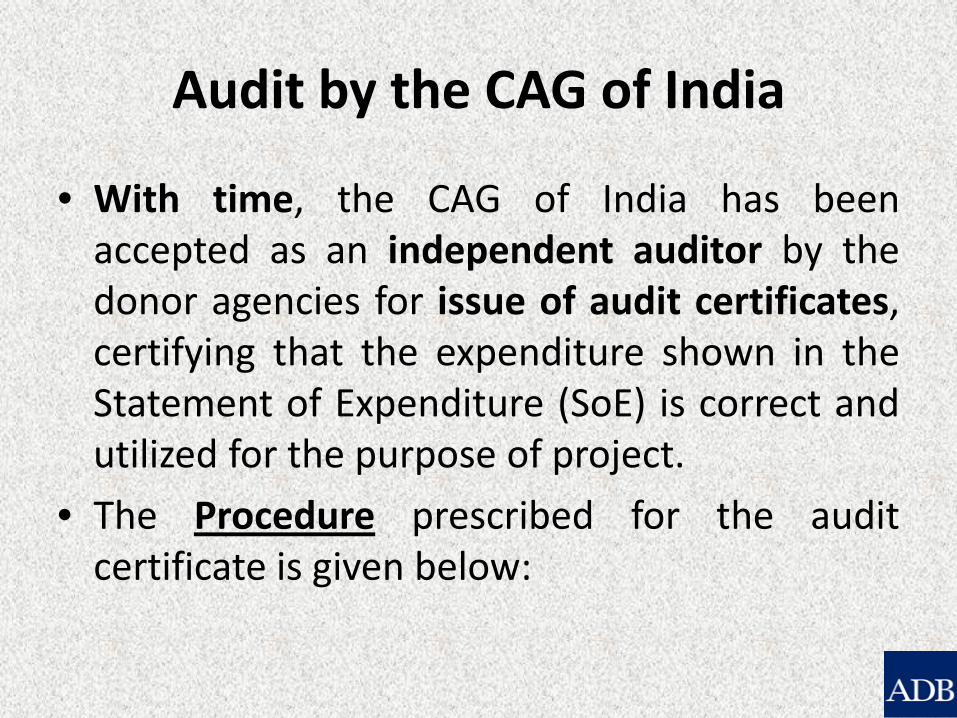

Audit by the CAG of India

• With time, the CAG of India has been accepted as an independent auditor by the donor agencies for issue of audit certificates, certifying that the expenditure shown in the Statement of Expenditure (SoE) is correct and utilized for the purpose of project.

• The Procedure prescribed for the audit certificate is given below:

Audit by the CAG of India (Contd.)

• Audit of the World Bank projects is being carried out by the CAG as envisaged in Chapter 17 of Manual of Standing Orders- Audit (2002).

• Audit Certificate on annual Project Financial Statements is issued on the basis of Local Audit and Central Audit.

• Independence of the CAG is ensured through provisions of the Constitution of India and CAG’s (DPC), Act, 1971.

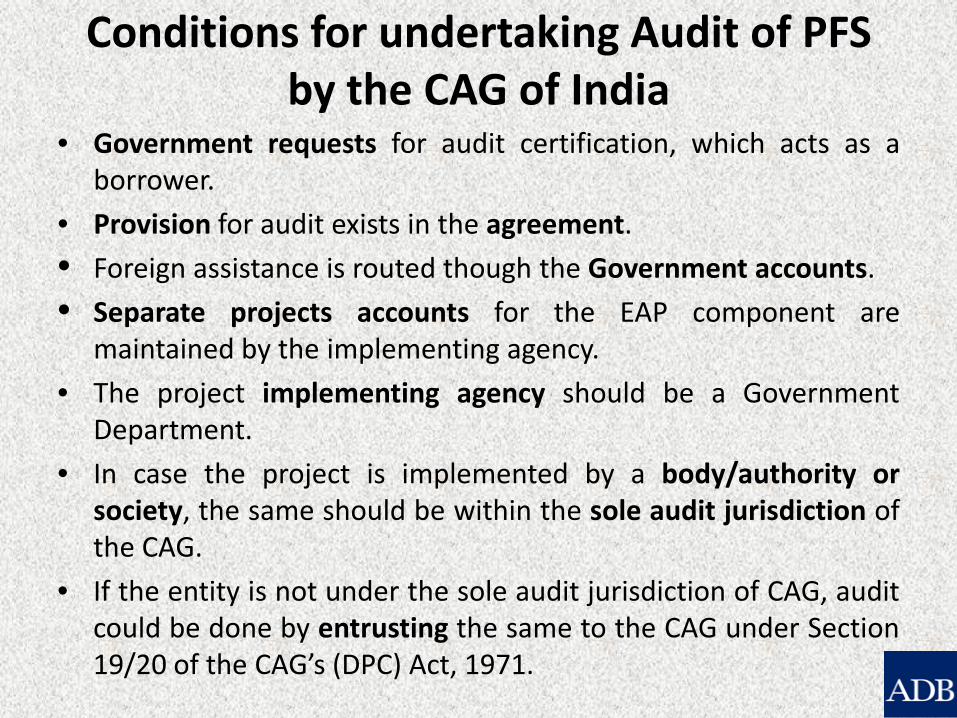

Conditions for undertaking Audit of PFS by the CAG of India

• Government requests for audit certification, which acts as a borrower.

• Provision for audit exists in the agreement.

• Foreign assistance is routed though the Government accounts.

• Separate projects accounts for the EAP component are maintained by the implementing agency.

• The project implementing agency should be a Government Department.

• In case the project is implemented by a body/authority or society, the same should be within the sole audit jurisdiction of the CAG.

• If the entity is not under the sole audit jurisdiction of CAG, audit could be done by entrusting the same to the CAG under Section 19/20 of the CAG’s (DPC) Act, 1971.

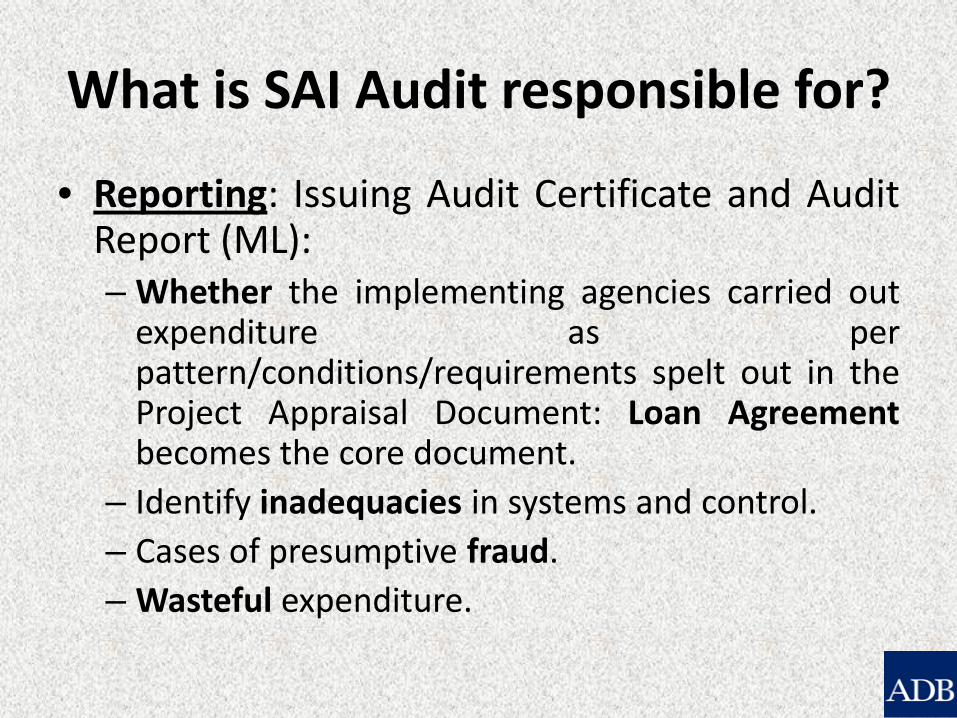

What is SAI Audit responsible for?

• Reporting: Issuing Audit Certificate and Audit Report (ML): – Whether the implementing agencies carried out

expenditure as per pattern/conditions/requirements spelt out in the Project Appraisal Document: Loan Agreement becomes the core document.

– Identify inadequacies in systems and control. – Cases of presumptive fraud. – Wasteful expenditure.

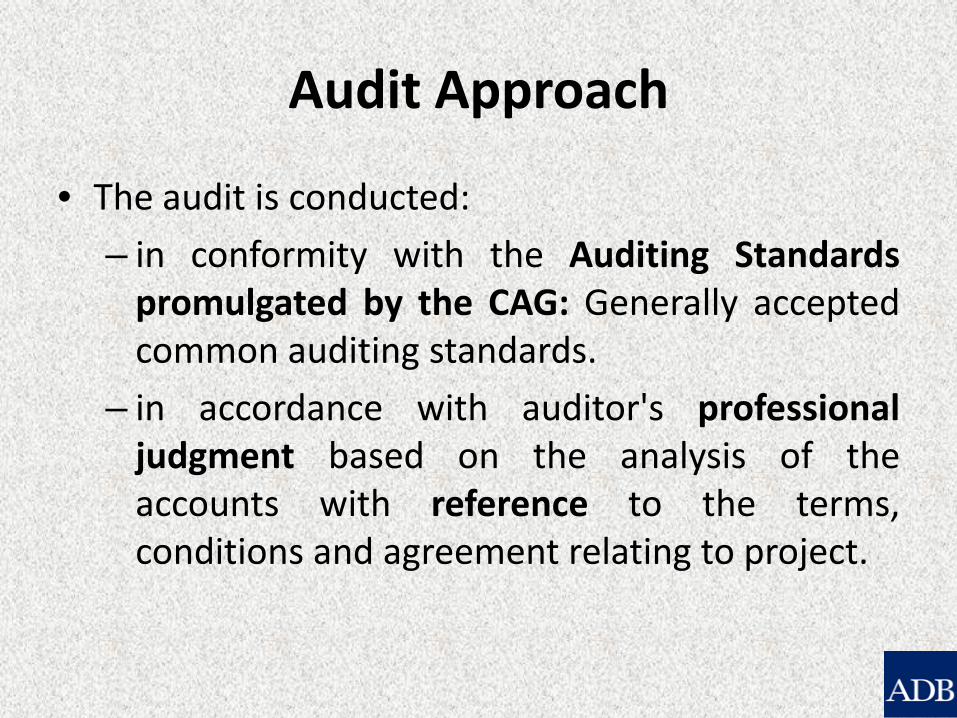

Audit Approach

• The audit is conducted:

– in conformity with the Auditing Standards promulgated by the CAG: Generally accepted common auditing standards.

– in accordance with auditor's professional judgment based on the analysis of the accounts with reference to the terms, conditions and agreement relating to project.

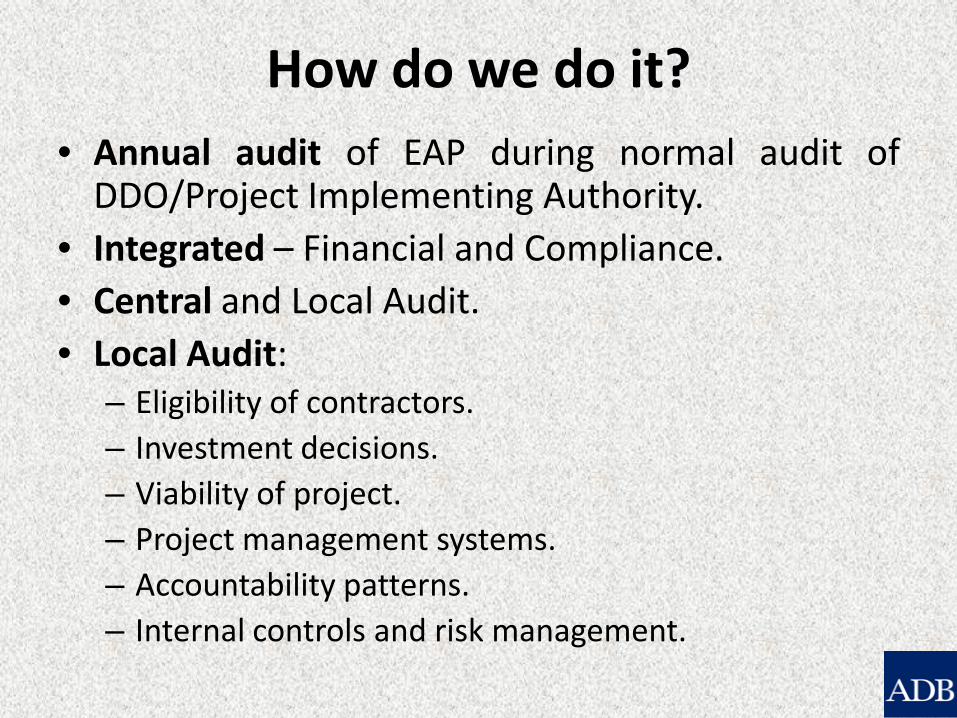

How do we do it? • Annual audit of EAP during normal audit of

DDO/Project Implementing Authority. • Integrated – Financial and Compliance. • Central and Local Audit. • Local Audit:

– Eligibility of contractors. – Investment decisions. – Viability of project. – Project management systems. – Accountability patterns. – Internal controls and risk management.

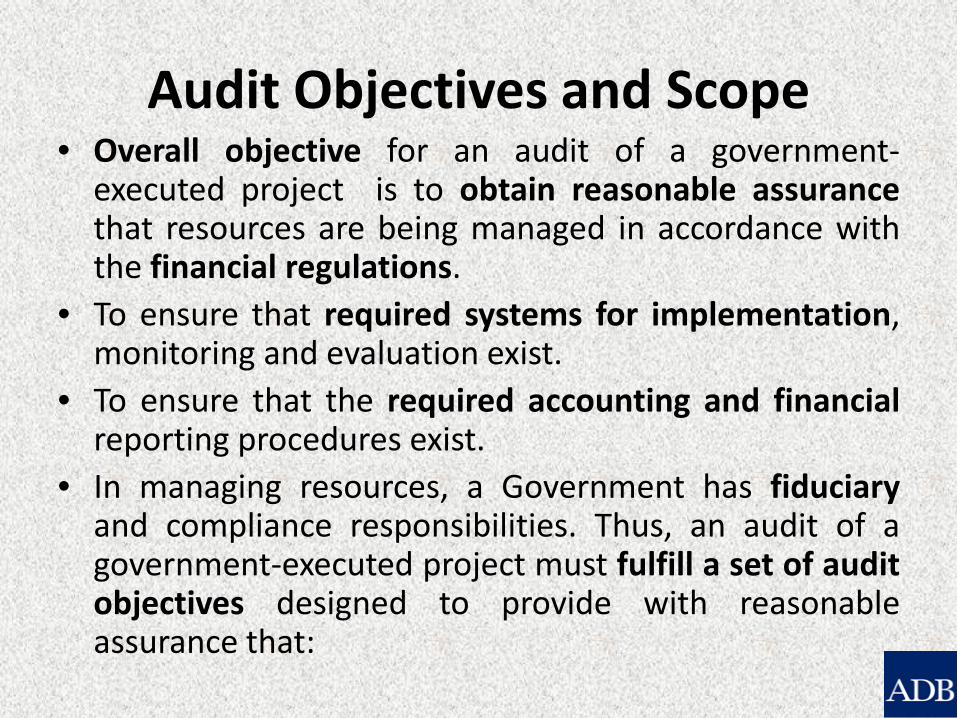

Audit Objectives and Scope • Overall objective for an audit of a government-

executed project is to obtain reasonable assurance that resources are being managed in accordance with the financial regulations.

• To ensure that required systems for implementation, monitoring and evaluation exist.

• To ensure that the required accounting and financial reporting procedures exist.

• In managing resources, a Government has fiduciary and compliance responsibilities. Thus, an audit of a government-executed project must fulfill a set of audit objectives designed to provide with reasonable assurance that:

Audit Objectives and Scope (Contd.)

• Project disbursement is made in accordance with the project document.

• Project disbursements are validly supported by adequate documentation.

• Project financial reports are fairly and accurately presented.

• An appropriate management structure, internal controls and record-keeping systems are maintained by the project management and can be relied upon.

• Project monitoring and evaluation are undertaken and reports are prepared as required.

Broad Guidelines for Audit of these Projects

• Project Authorities are expected to send the statements of expenditure within one month of the close of the financial year.

• No separate or detailed audit needs to be conducted for the projects.

• Certificate is to be given on the basis of the observation made in the central as well as local audit.

• Audit Certificate is to be issued to the project authorities with a copy to the Ministry of Finance.

• Audit Certificate should not contain material which would be reflected in the Audit Reports to be placed before the Legislature.

Broad Guidelines for Audit of these Projects (Contd.)

• However, in case of Autonomous Bodies/Corporations where Separate Audit Reports (SARs) are issued, material which go into such Reports can be incorporated in the Audit Certificate.

• The Donors suspend assistance to the projects if the audit certificate is not received by them in time.

• Therefore, there is a great responsibility on SAI, India to be timely.

• Timely PFSs are critical for sound public financial management and fiduciary oversight.

• Fair & accurate PFSs are also a pre-requisite for Transparency.

• Shift from SOEs to PFSs. • In Fiscal Year 2008-09, total of 202 sets of

audited Financial Statements were issued, 79 by the CAG and balance by the private sector auditing firms.

Ensuring Accountability

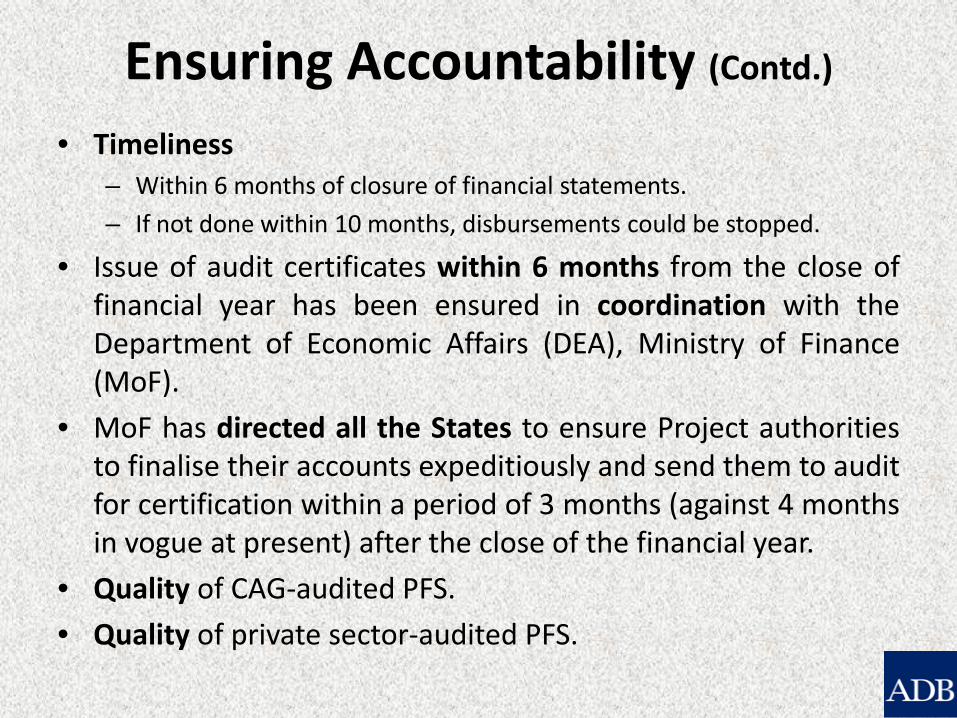

• Timeliness – Within 6 months of closure of financial statements.

– If not done within 10 months, disbursements could be stopped.

• Issue of audit certificates within 6 months from the close of financial year has been ensured in coordination with the Department of Economic Affairs (DEA), Ministry of Finance (MoF).

• MoF has directed all the States to ensure Project authorities to finalise their accounts expeditiously and send them to audit for certification within a period of 3 months (against 4 months in vogue at present) after the close of the financial year.

• Quality of CAG-audited PFS.

• Quality of private sector-audited PFS.

Ensuring Accountability (Contd.)

• 225 Projects across the country are audited by the CAG.

• Special audits also undertaken on the request of MoF.

• Only projects either being implemented by Government Departments or by the authorities under sole audit of CAG are audited.

• Extent and Scope of Audit is to be decided by the CAG.

Status of Audit of EAPs

Audit Certificate (AC) • AC is to be issued on Project Financial Statements

accompanied by management's assertion for fair presentation of the PFS – Allowing expenditure.

• A separate certificate should be issued for each project indicating the amount held under objection in relation to wanting voucher, D.C. bills, sanctions etc. and mis-classifications, defalcation, overpayments etc. that come to notice.

• Irregularities noticed during central audit as well as local audit should be distinctly recorded and separate file for certification in respect of each project maintained.

• Management Letter pointing out issues other than financial statements like weaknesses in internal control or value for money issues.

Time Schedule of Certification • As prescribed in the agreement. • Normally 6 months. • The audit certificates are required to be issued within 6

months from the closure of Accounts, i.e. accounts are required to be certified latest by 30th September every year.

• Implementing agencies are required to furnish PFS to Audit by 1st May and remaining five months are available for Central and Local Audit.

• We certify the project accounts throughout the year (for arrear period as also for the current year) depending upon the production of PFS and other documents.

21

To whom Audit Certificates are issued?

• Issued to the Implementing Agencies/Entities audited.

• Not directly issued to the Donor.

22

Follow-up on and Impact of Audit Certificate

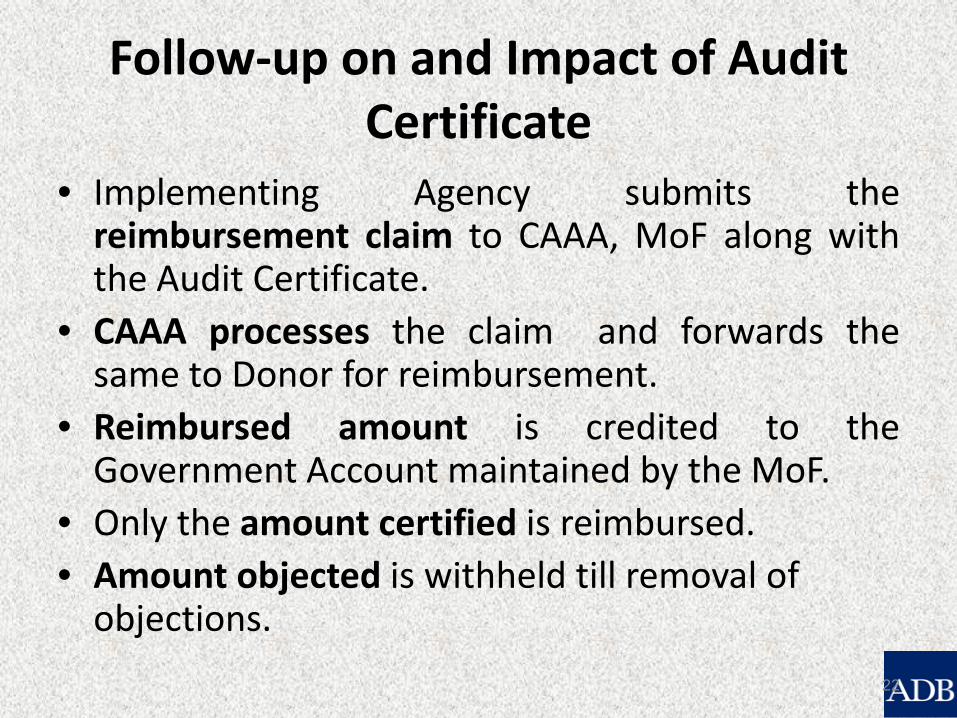

• Implementing Agency submits the reimbursement claim to CAAA, MoF along with the Audit Certificate.

• CAAA processes the claim and forwards the same to Donor for reimbursement.

• Reimbursed amount is credited to the Government Account maintained by the MoF.

• Only the amount certified is reimbursed. • Amount objected is withheld till removal of

objections.

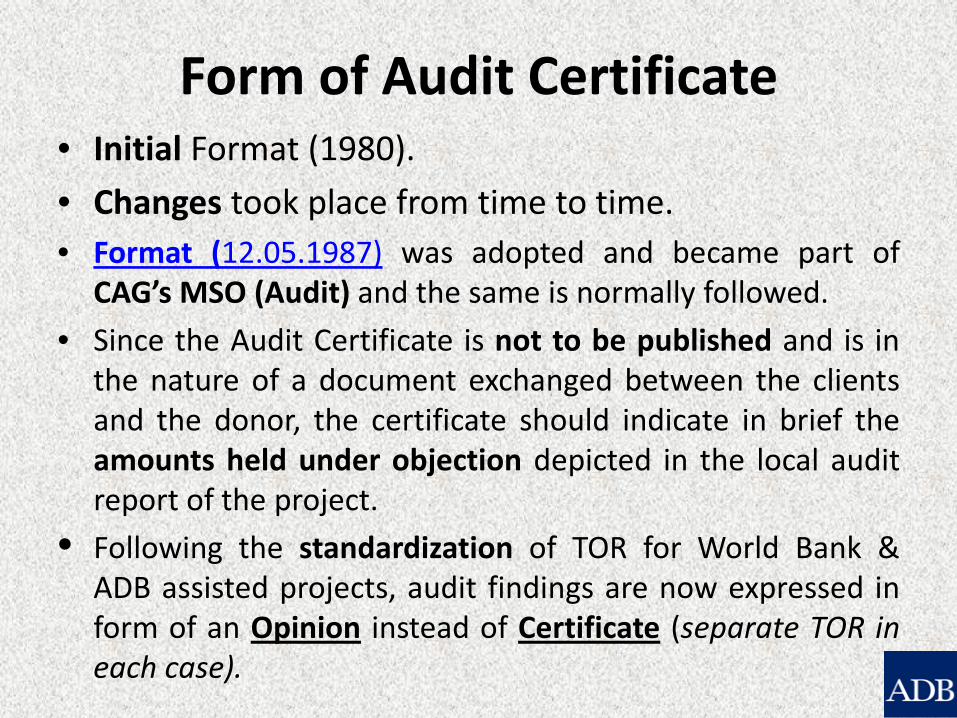

Form of Audit Certificate • Initial Format (1980).

• Changes took place from time to time. • Format (12.05.1987) was adopted and became part of

CAG’s MSO (Audit) and the same is normally followed.

• Since the Audit Certificate is not to be published and is in the nature of a document exchanged between the clients and the donor, the certificate should indicate in brief the amounts held under objection depicted in the local audit report of the project.

• Following the standardization of TOR for World Bank & ADB assisted projects, audit findings are now expressed in form of an Opinion instead of Certificate (separate TOR in each case).

Audit Opinion: TOR – World Bank • Consequent upon approval of draft TOR for audit of

World Bank assisted Kerala State Transport Project, more project specific draft TORs were received at regular intervals.

• TORs took in all the standard aspects of the auditing standards and differed only in regard to the objective, background and components of the projects.

• Hence, to avoid piece meal examination, vetting of individual TOR each time and also to have a uniform approach, it was decided to have standardized Terms of Reference for audit of World Bank Projects, which would be negotiated in future.

Audit Opinion: TOR – World Bank (Contd.)

• World Bank came up with draft standardized TOR through DEA, MoF.

• Examined and sent to the Ministry with the approval of CAG.

• Ministry accepted this TOR and circulated to all States in March 2009.

• As such, the World Bank projects effective from 20th March 2009 would be subject to the Standardized TOR.

Audit Opinion: TOR – ADB • Issue of standardization of TOR for audit of the

ADB-assisted projects was under consideration for quite some time.

• These were approved by the SAI and DAE, MoF was apprised of this decision under intimation to the ADB.

• Ministry circulated the standardized TOR to all concerned including all project directors of ADB projects in September 2013.

• Audit Certification of all new ADB-assisted projects would be undertaken as per provisions contained in the standardized TOR.

27

Management Letter/Audit Report • Significant weaknesses which are not reflected in

the Audit Opinion are reported in a Management Letter addressed to the Borrower.

• Indicates:

– weaknesses in internal controls.

– inappropriate accounting policies and practices.

– general issues of 3Es.

– any other matter which the auditor considers material and significant.

28

Authority for signing the Certificate

• Audit Certificate should be issued in the proper printed letter head and signed by an officer not below the rank of Deputy Accountant General/Deputy Director.

29

Monitoring the Progress of Audit Certification

• A monthly return is prescribed by the SAI Headquarters.

• SAI Field offices are required to send it to the Headquarters by 10th of next month.

• Required to be sent to Headquarters till all the project accounts are certified during the year.

• The return contains information on project name, date of receipt of SOE/PFS, date of issue of Audit certificate etc.

30

Reasons for Delay in issue of Audit Certificates

• Non-receipt/delayed receipt of SOE/PFS. • Non-receipt of project documents like loan

agreement, project agreement etc. • Non-production of original documents by the

IA. • Non-submission of satisfactory replies to

audit queries. • Delayed request by the MoF, GoI to the CAG. • Delayed entrustment of audit of

Implementing Agency.

31

Quality of Audited PFSs

• Study undertaken by World Bank on the quality of PFS audits by CAG and private firms.

• Overall quality of CAG audits of PFSs showed more significant improvement in recent years than private audits of PFSs.

• CAG improved on all categories of quality assessed in this study, while for private audits, there was no clear trend of improvement except in respect of the criteria for management letters.

32

Quality of Audited PFSs (Contd.)

• A major difference: CAG consistently includes a separate paragraph in its audit reports to express an independent opinion as to the adequacy of the documentation maintained by the project to support claims to the Bank for reimbursements of expenditures incurred.

• This paragraph explicitly states the auditor’s opinion with respect to the eligibility of expenditures under the relevant Loan or Credit Agreement.

• This additional opinion paragraph is present in under two-thirds of the sample of private audit reports.

33

Word of Caution • Considering the overall volume of expenditure

under EAPs vis-à-vis the overall Government expenditure, audit could not rightfully divert substantive effort towards auditing these projects.

• As per existing procedure for audit of EAPs, we do not undertake audit of all the projects financed by external donors.

• Audit of such projects is undertaken only when the implementing agency is within the sole audit jurisdiction of the CAG.

• As a result, our opinion may not give a broad view on all the projects.

34

Audit Opinion – Some Illustrations

• Emergency Tsunami Reconstruction Project (ETRP).

• National Ganga River Basin Project (NGRBP).

• Vocational Training Improvement Project (VTIP).

• Tamil Nadu Irrigated Agriculture Modernization & Water Bodies Restoration and Modernization Project (TNIAMWARM).

Management Letter - Some Illustrations

• Biodiversity Conservation and Rural Livelihood Improvement Project (BCRLIP).

• Capacity Building for Industrial Pollution Management Project (CBIPMP).

• Capacity Development for Forest Management and Training of Personnel (CDFMTP).

• National Mission for Clean Ganga (NMCG).

THANKS…..