Embed Size (px)

Citation preview

Presentation for conference of Nowy Przemysł, 21.11.2005

Mittal Steel Poland

Vijay Bhatnagar – Chief Executive Officer

Conference of Nowy Przemysł Katowice, 21 November 2005

Presentation at conference of Nowy Przemsł, November 21, 2005 2

WHY POLAND

Poland - R&D centre„Silicon Valley” of CEE

Poland - centre of automotive sector suppliers

Poland - white goods centre

Poland - best agricultural products

Poland - health tourism destination

Poland - financial centre of the CEE

Industrial output - construction sector

High Growth

Big and Young Population

Skilled employees

Well-educated people

Biggest Area in CEE

Big internal market

Presentation at conference of Nowy Przemsł, November 21, 2005 3

Foreign Investment in PolandPoland's entry into the European Union on 1 May 2004 was the culmination of wide-ranging political and economic transformation initiated in 1989. As a part of the Single European Market, Poland is still undergoing economic and social changes. With economic growth at 5.4% (2004), a young, well-educated and ambitious labour force, location at the very heart of the continent and low corporate income tax (19%), Poland has become an exciting place for investors from around the world Poles are one of Europe’s youngest societies (half of the nation is below the age of 35). The country also holds the second place in Europe in terms of the number of students.

Presentation at conference of Nowy Przemsł, November 21, 2005 4

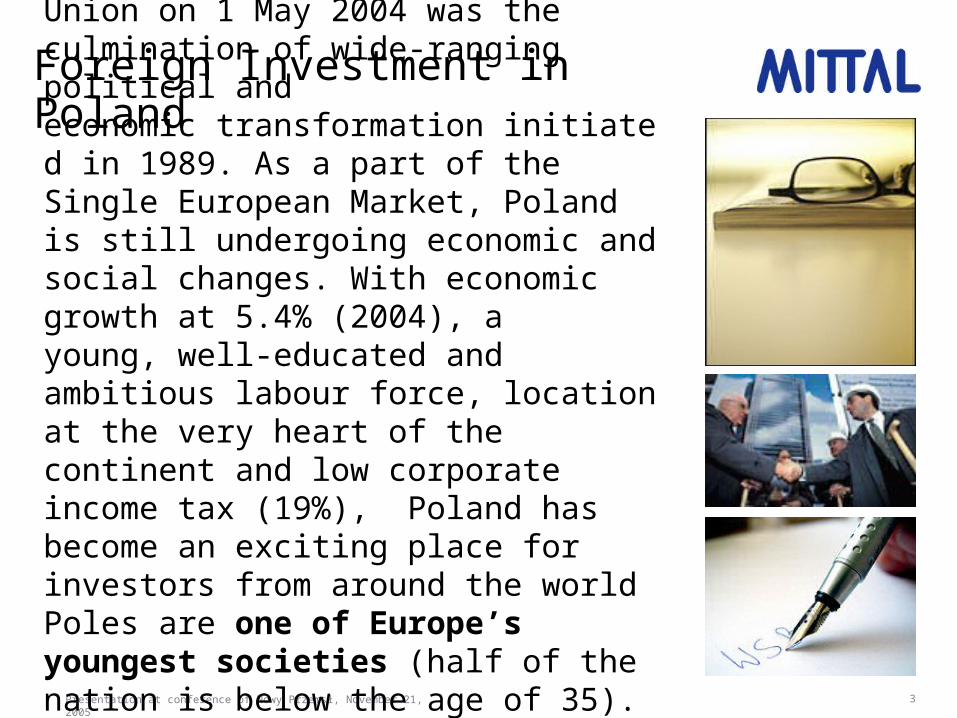

Foreign Investment in Poland

The inflow of foreign capital to Poland (mln USD)

Presentation at conference of Nowy Przemsł, November 21, 2005 5

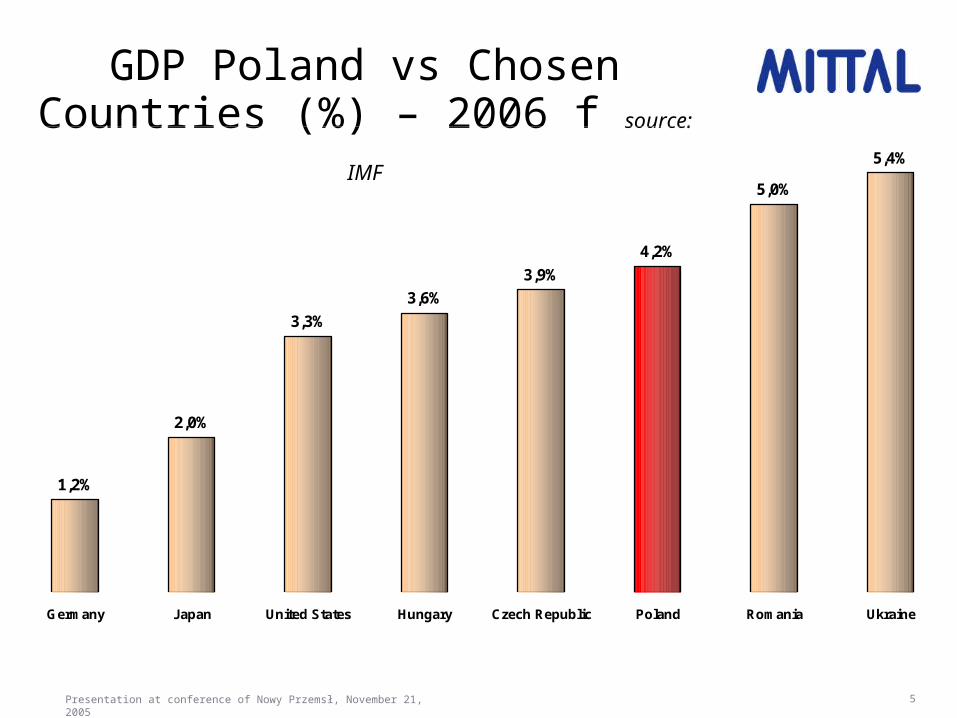

GDP Poland vs Chosen Countries (%) – 2006 f source: IMF

1,2%

2,0%

3,3%

3,6%

3,9%

4,2%

5,0%

5,4%

Germany Japan United States Hungary Czech Republic Poland Romania Ukraine

Presentation at conference of Nowy Przemsł, November 21, 2005 6

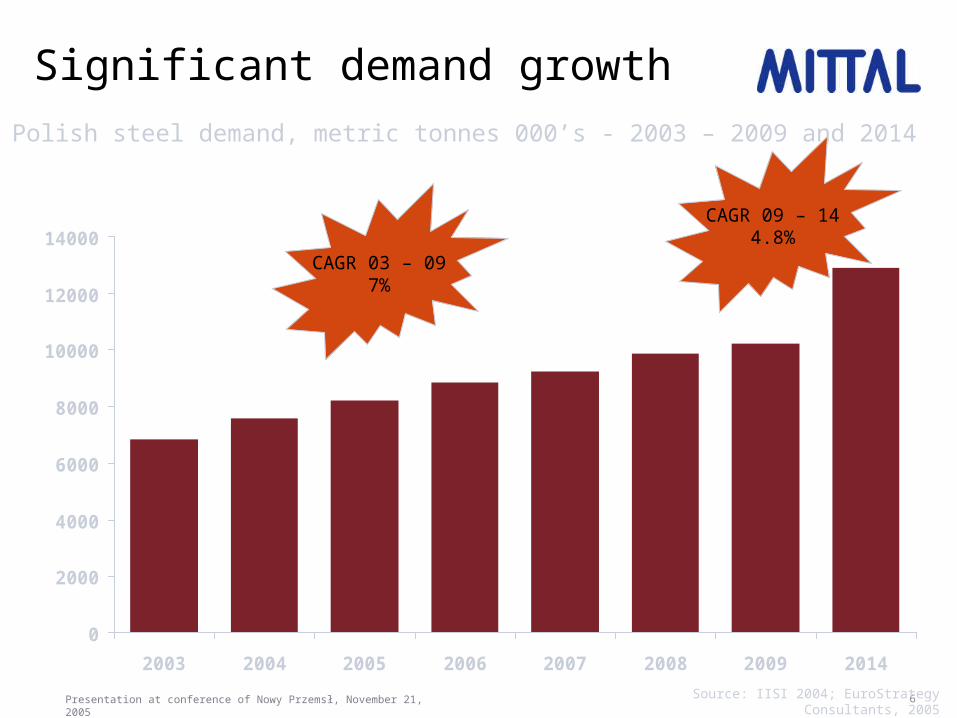

Significant demand growth

0

2000

4000

6000

8000

10000

12000

14000

2003 2004 2005 2006 2007 2008 2009 2014

Polish steel demand, metric tonnes 000’s - 2003 – 2009 and 2014

CAGR 03 – 097%

Source: IISI 2004; EuroStrategy Consultants, 2005

CAGR 09 – 144.8%

Presentation at conference of Nowy Przemsł, November 21, 2005 7

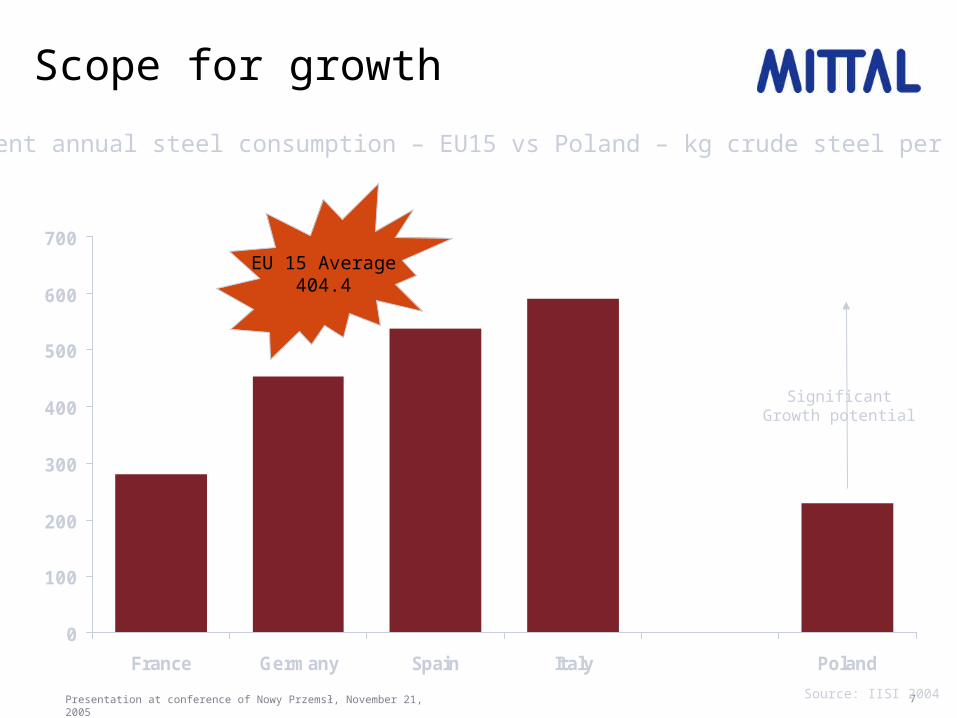

Scope for growth

0

100

200

300

400

500

600

700

France Germany Spain Italy Poland

Apparent annual steel consumption – EU15 vs Poland – kg crude steel per capita

Source: IISI 2004

EU 15 Average404.4

SignificantGrowth potential

Presentation at conference of Nowy Przemsł, November 21, 2005 8

Mittal Steel Poland –At a glance

• Represents about 70% of steel production capacity in Poland• Groups four of the largest Polish steel plants• Production capacity:

– 7.6m tonnes of crude steel– 6.6m tonnes of rolled products

• One of the largest steel products exporters in Poland, reaching over 60 foreign markets

• The largest coke producer within Mittal Steel operations and throughout CEE

Presentation at conference of Nowy Przemsł, November 21, 2005 9

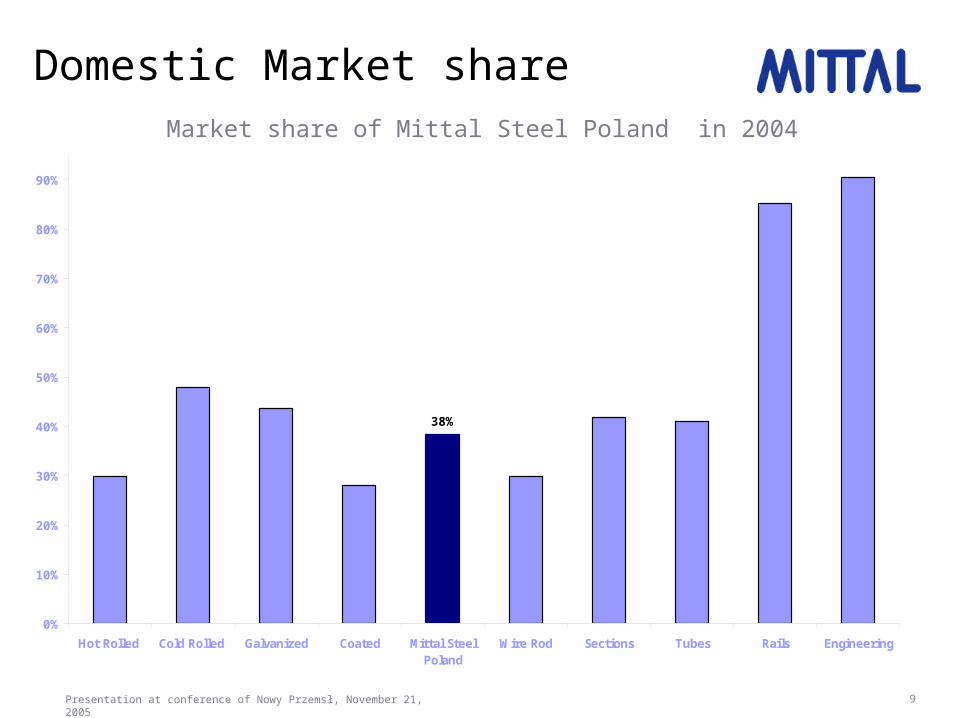

Domestic Market share Market share of Mittal Steel Poland in 2004

38%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Hot Rolled Cold Rolled Galvanized Coated Mittal SteelPoland

Wire Rod Sections Tubes Rails Engineering

Presentation at conference of Nowy Przemsł, November 21, 2005 10

Mittal Steel Poland: The future

• Utilization of global sales and marketing network of Mittal

Steel

• Move product mix towards higher value products (for

automotive and white goods industry)

• Increasing domestic presence in Poland

• Coming close to end customers

• New investments to reduce cost, improve quality and

reliability, and to increase range of products

Presentation at conference of Nowy Przemsł, November 21, 2005 11

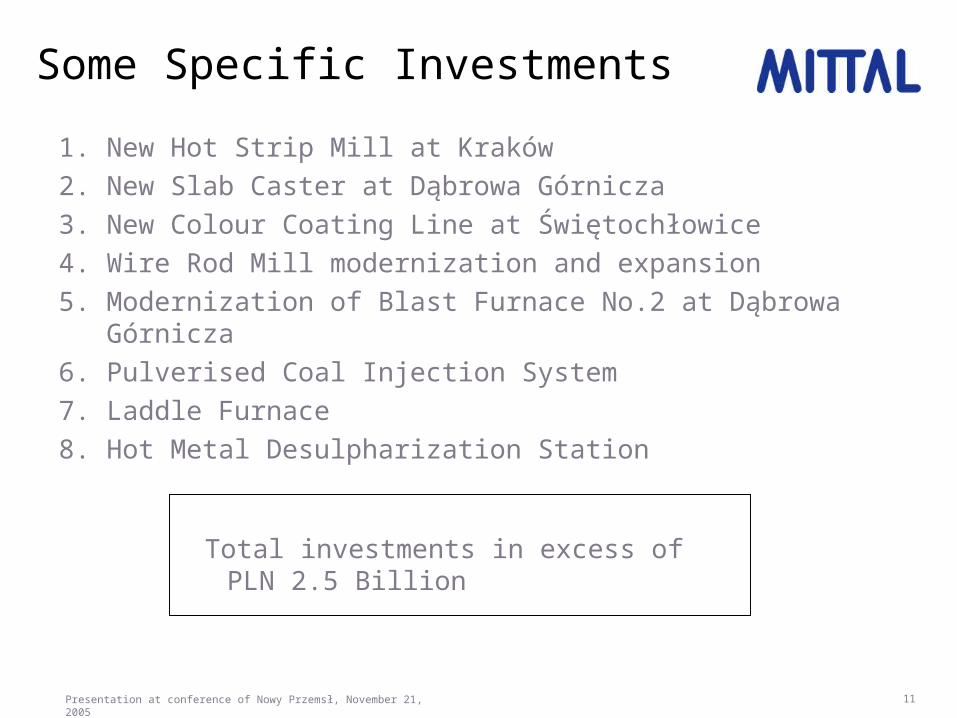

Some Specific Investments

1. New Hot Strip Mill at Kraków2. New Slab Caster at Dąbrowa Górnicza3. New Colour Coating Line at Świętochłowice4. Wire Rod Mill modernization and expansion5. Modernization of Blast Furnace No.2 at Dąbrowa

Górnicza6. Pulverised Coal Injection System7. Laddle Furnace8. Hot Metal Desulpharization Station

Total investments in excess of PLN 2.5 Billion

Presentation at conference of Nowy Przemsł, November 21, 2005 12

Conclusions

• Support of world-class R&D Centres in USA & France will play a key role

• Quick knowledge transfer (technical, operational and commercial) through Mittal Steel worldwide KMP will be its Cornerstone

• Proactively address issues of its Stakeholders

It is our plan to make the Polish operations to be

one of the most competitive and admired in

Europe